Detailed Report on Management Accounting and Costing for Austin Fraser

VerifiedAdded on 2020/01/23

|20

|5050

|187

Report

AI Summary

This report offers a comprehensive analysis of management accounting, using Austin Fraser, a recruitment consultant, as a case study. It delves into key aspects like financial planning, financial statement analysis, and the importance of various management accounting systems. The report explores different costing methods, including absorption and marginal costing, and their impact on net profit calculation. It also covers various reporting modes, such as performance reports, sales reports, and inventory costing reports. Furthermore, the document highlights the differences between absorption and marginal costing techniques, providing insights into their applications and implications. The report emphasizes the role of management accounting in making informed decisions, monitoring risks, and achieving sustainable development within a business context. This assignment is a valuable resource for students seeking to understand the practical application of management accounting principles.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 ..........................................................................................................................................1

1.2 ..........................................................................................................................................2

TASK 2............................................................................................................................................3

2.1 Calculation of net profit using absorption costing and marginal costing techniques.......3

TASK 3 ...........................................................................................................................................8

3.1 ..........................................................................................................................................8

3.2 ........................................................................................................................................11

CONCLUSION..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 ..........................................................................................................................................1

1.2 ..........................................................................................................................................2

TASK 2............................................................................................................................................3

2.1 Calculation of net profit using absorption costing and marginal costing techniques.......3

TASK 3 ...........................................................................................................................................8

3.1 ..........................................................................................................................................8

3.2 ........................................................................................................................................11

CONCLUSION..............................................................................................................................13

INTRODUCTION

Management system is a process through which cited entity can reports of management

and financial statements which provides a detailed description of the financial position of cited

entity which is required by the stakeholders of cited entity. All the material information that is

necessary for stakeholders which can affect their decisions regarding a business organisation are

included in those financial statements. Reports which are prepared as per management

accounting shows amount which is available with the cited entity as well as revenue generated

out of sales. Further, these reports also give a detailed information regarding account payables

and account receivables(Christ and Burritt, 2013). In this report, a detailed description on the

working of accounting will be done along with the need of various systems is done. This

document is based on the case study of Austin Fraser which is a recruitment consultant that deals

in engineering, information technology and sectors related to life sciences sectors. Through this

report, management accounting methods and income statements using techniques of cost

accounting such as marginal and absorption costing will be discussed.

TASK 1

1.1

Management accounting: It is refers to be the process of identifying, measuring,

summarising and analysing the various financial transaction which are done by the company

during the year. It is based on display of professional skills and ability which is required to

manage accounting information.

Importance of MA:

It is use to avoid seasonal fluctuations.

It also help in ascertainment of cost.

Management accounting helps to determine unprofitable activities.

Administration system is a process through which several reports have been prepared so

that management of cited entity can make suitable decisions regarding various financial and non-

financial factors. Absorption and marginal costing are some tools or techniques of cost

accounting through which cited entity can prepare better strategies for maintaining its

productivity. Management accounting combines various aspects of a business enterprise like

finance, accounting and management so that better strategies can be planned or framed and value

of cited entity could be increased (Cinquini and Tenucci, 2010). Management accounting does

1

Management system is a process through which cited entity can reports of management

and financial statements which provides a detailed description of the financial position of cited

entity which is required by the stakeholders of cited entity. All the material information that is

necessary for stakeholders which can affect their decisions regarding a business organisation are

included in those financial statements. Reports which are prepared as per management

accounting shows amount which is available with the cited entity as well as revenue generated

out of sales. Further, these reports also give a detailed information regarding account payables

and account receivables(Christ and Burritt, 2013). In this report, a detailed description on the

working of accounting will be done along with the need of various systems is done. This

document is based on the case study of Austin Fraser which is a recruitment consultant that deals

in engineering, information technology and sectors related to life sciences sectors. Through this

report, management accounting methods and income statements using techniques of cost

accounting such as marginal and absorption costing will be discussed.

TASK 1

1.1

Management accounting: It is refers to be the process of identifying, measuring,

summarising and analysing the various financial transaction which are done by the company

during the year. It is based on display of professional skills and ability which is required to

manage accounting information.

Importance of MA:

It is use to avoid seasonal fluctuations.

It also help in ascertainment of cost.

Management accounting helps to determine unprofitable activities.

Administration system is a process through which several reports have been prepared so

that management of cited entity can make suitable decisions regarding various financial and non-

financial factors. Absorption and marginal costing are some tools or techniques of cost

accounting through which cited entity can prepare better strategies for maintaining its

productivity. Management accounting combines various aspects of a business enterprise like

finance, accounting and management so that better strategies can be planned or framed and value

of cited entity could be increased (Cinquini and Tenucci, 2010). Management accounting does

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

research over financial and non-financial data so that cited entity can achieve sustainable

development. Unlike a normal accountant who deals in figures to report his financial statements,

a management accountant frames business strategies for the development of cited entity and

monitors risk which is involved in operational management.

Primary need of various variety of management accounting: There are certain

necessary needs for which various kind of management accounting are to be managed. These

essential needs of requirements are mentioned as below: Traditional Management Accounting: It focuses on cost by the means of job order or

methods of process costing. Through these methods, Austin Fraser can allocate different

types of costs related with direct material, direct labour and manufacturing overheads. Requirements for Traditional Management Accounting: Generally, job order costing

technique is used in manufacturing industry which has large projects as in such case,

various types of costs are easily traceable and further, cited entity can easily allocate

them to respective project. On the other hand, process costing techniques allocate cost to

various processes which produces homogeneous goods. Lean Accounting: It is a newly emerged technique of management accounting. Lean

accounting is really revolutionary because it does not only concentrated over cost, but

also it supports strategy making to reduce or control the cost by management of waste.

Requirements for Lean Accounting: Through lean accounting, management accountant

can make strategies regarding cost reduction and he can implement such strategies for the

benefit of Austin Fraser. Through the same, managerial personnel can take required

decisions.

Different types of costing system:

1. Inventory management system – Keeping in mind the end goal to complete the

production procedure stock is required in an association. For this it is extremely pivotal

that administration of same is done in such a way, to the point that viable utilization of

stock is done as such that yield can be expanded which is done trough this system.

2. Job costing framework – To give the final products different employments are performed

in an association. Keeping in mind the end goal to quantify the execution of each

occupation it is essential that assessment of each is done independently with the goal that

likewise results can be learn.

2

development. Unlike a normal accountant who deals in figures to report his financial statements,

a management accountant frames business strategies for the development of cited entity and

monitors risk which is involved in operational management.

Primary need of various variety of management accounting: There are certain

necessary needs for which various kind of management accounting are to be managed. These

essential needs of requirements are mentioned as below: Traditional Management Accounting: It focuses on cost by the means of job order or

methods of process costing. Through these methods, Austin Fraser can allocate different

types of costs related with direct material, direct labour and manufacturing overheads. Requirements for Traditional Management Accounting: Generally, job order costing

technique is used in manufacturing industry which has large projects as in such case,

various types of costs are easily traceable and further, cited entity can easily allocate

them to respective project. On the other hand, process costing techniques allocate cost to

various processes which produces homogeneous goods. Lean Accounting: It is a newly emerged technique of management accounting. Lean

accounting is really revolutionary because it does not only concentrated over cost, but

also it supports strategy making to reduce or control the cost by management of waste.

Requirements for Lean Accounting: Through lean accounting, management accountant

can make strategies regarding cost reduction and he can implement such strategies for the

benefit of Austin Fraser. Through the same, managerial personnel can take required

decisions.

Different types of costing system:

1. Inventory management system – Keeping in mind the end goal to complete the

production procedure stock is required in an association. For this it is extremely pivotal

that administration of same is done in such a way, to the point that viable utilization of

stock is done as such that yield can be expanded which is done trough this system.

2. Job costing framework – To give the final products different employments are performed

in an association. Keeping in mind the end goal to quantify the execution of each

occupation it is essential that assessment of each is done independently with the goal that

likewise results can be learn.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Price optimisation plan – Cost of any item assumes an extremely centrality part in the

decision determination of the clients. In this manner, it is exceptionally fundamental for

an association to set the most appropriate cost of the item which can full fill the

prerequisite of both customer and maker. Through this arrangement of bookkeeping it

can be ascertained what cost can give greatest advantage to maker without having loss of

potential clients.

4. Cost accounting system: The management accounting is used to maintain extra cost

which are used by the company during the process of product development. It consist of

various costing methods such as standard costing, normal costing and actual costing.

1.2

A variety of modes are used for reporting under management system (Dillard and

Roslender, 2011). They are based on various aspects of business enterprise such as financial and

cost accounting information based on mathematical aspects and information available regarding

future projects. These methods or techniques are mentioned as below: Financial Planning: Financial planning is really important for Austin Fraser as planning

for financial factors. Main objective for any entity is profitability(Schaltegger and

Zvezdov, 2013). They want to increase their profit by reducing cost and maintaining

quality in their products and services. Financial planning can be considered as a vital tool

for the achievement of various business objectives. Planning of various factors related to

finance through financials can help stakeholder of Austin Fraser to make better decisions

related with cited entity. On the other hand management accounting officer can make

better financial structure which fulfil requirements of firm through its available resources.

Other than this financial planning helps to employ available resources in better projects

are potential enough to give more returns so that the financial resources can be utilized in

a better way. Analysis of Financial Statements: There are several financial statements which are

required to be prepared by the cited entity(Schaltegger and Zvezdov, 2013). Austin Fraser

needs to prepare final accounts, statement of alteration in business position and notes to

accounts. These financial statements reflect the financial position of cited entity.

3

decision determination of the clients. In this manner, it is exceptionally fundamental for

an association to set the most appropriate cost of the item which can full fill the

prerequisite of both customer and maker. Through this arrangement of bookkeeping it

can be ascertained what cost can give greatest advantage to maker without having loss of

potential clients.

4. Cost accounting system: The management accounting is used to maintain extra cost

which are used by the company during the process of product development. It consist of

various costing methods such as standard costing, normal costing and actual costing.

1.2

A variety of modes are used for reporting under management system (Dillard and

Roslender, 2011). They are based on various aspects of business enterprise such as financial and

cost accounting information based on mathematical aspects and information available regarding

future projects. These methods or techniques are mentioned as below: Financial Planning: Financial planning is really important for Austin Fraser as planning

for financial factors. Main objective for any entity is profitability(Schaltegger and

Zvezdov, 2013). They want to increase their profit by reducing cost and maintaining

quality in their products and services. Financial planning can be considered as a vital tool

for the achievement of various business objectives. Planning of various factors related to

finance through financials can help stakeholder of Austin Fraser to make better decisions

related with cited entity. On the other hand management accounting officer can make

better financial structure which fulfil requirements of firm through its available resources.

Other than this financial planning helps to employ available resources in better projects

are potential enough to give more returns so that the financial resources can be utilized in

a better way. Analysis of Financial Statements: There are several financial statements which are

required to be prepared by the cited entity(Schaltegger and Zvezdov, 2013). Austin Fraser

needs to prepare final accounts, statement of alteration in business position and notes to

accounts. These financial statements reflect the financial position of cited entity.

3

Management of Austin Fraser can analyse these statements for different period of time so

that they can get information about their current financial position. Through such analysis Cost Accounting: Cost accounting is a method through which organisation can allocate

its cost and it can present its cost figures as per the unit of product, process involved in

production and also, according to various departments and branches of cited entity.

Through a better cost allocation system, Austin Fraser and its management can

implement better strategies which can assist them in the cost reduction. Fund Flow Analysis: Through fund flow analysis, cited entity can analyse the movement

of funds for a particular period. They can also compare such movement of funds for

current period with the movement of funds of some other or previous period. Through

such analysis, they can get information regarding the utilization of funds, its sources and

application.

Cash Flow Analysis: Management accountant of Austin Fraser can use cash flow

analysis to analyse the flow of cash during financial year. Thus, he can get a clear cut

information about various sources through which cash has been generated in the cited

entity in which projects or activities cash has been employed (Lee, 2011). movement of

cash and its tracking can assist an entity to employ available funds in required areas. As a

cash flow statements is divided into three sections i.e. Cash flow from operating,

investing and financing activities. Hence through analysis of cash flow cited entity can

get a detailed information with figures that in which activities how much of cash is

employed and weather they returning adequate cash flow or not.

There are different reports which are utilised in order to keep check over the operations of the

organisation:

Execution report – In an association assessment of results is especially required so

deviations in the required and real outcomes can be recorded. Through this report the

consequences of a specific undertaking are exhibited in a compact shape which unveil all

the related information with respect to the work done.

Target costing report: Under it data about target use will be given. The cost will be stayed

aware of the objective that the appealing advantages can be accomplished.

Sales report – It is an archive which incorporates data with respect to the offers of a

specific period. It is keep up by the either the business division or their management.

4

that they can get information about their current financial position. Through such analysis Cost Accounting: Cost accounting is a method through which organisation can allocate

its cost and it can present its cost figures as per the unit of product, process involved in

production and also, according to various departments and branches of cited entity.

Through a better cost allocation system, Austin Fraser and its management can

implement better strategies which can assist them in the cost reduction. Fund Flow Analysis: Through fund flow analysis, cited entity can analyse the movement

of funds for a particular period. They can also compare such movement of funds for

current period with the movement of funds of some other or previous period. Through

such analysis, they can get information regarding the utilization of funds, its sources and

application.

Cash Flow Analysis: Management accountant of Austin Fraser can use cash flow

analysis to analyse the flow of cash during financial year. Thus, he can get a clear cut

information about various sources through which cash has been generated in the cited

entity in which projects or activities cash has been employed (Lee, 2011). movement of

cash and its tracking can assist an entity to employ available funds in required areas. As a

cash flow statements is divided into three sections i.e. Cash flow from operating,

investing and financing activities. Hence through analysis of cash flow cited entity can

get a detailed information with figures that in which activities how much of cash is

employed and weather they returning adequate cash flow or not.

There are different reports which are utilised in order to keep check over the operations of the

organisation:

Execution report – In an association assessment of results is especially required so

deviations in the required and real outcomes can be recorded. Through this report the

consequences of a specific undertaking are exhibited in a compact shape which unveil all

the related information with respect to the work done.

Target costing report: Under it data about target use will be given. The cost will be stayed

aware of the objective that the appealing advantages can be accomplished.

Sales report – It is an archive which incorporates data with respect to the offers of a

specific period. It is keep up by the either the business division or their management.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory costing report: In this technique the whole cost will be recognized on the

introduce of the activities led in a money related year. Cost instrument will be settled in

association with the unmistakable costs that are procured and after that they will be

dispersed by them

Job costing reporting: Under this, those costs which are recognized by the organization

from the individual items are recorded in it. The aggregate incomes are decide by primary

with a specific end goal. The fundamental analysis which should be considered under this

revealing is to record each part points of interest those are delivered at the time. Those

stages are maintained as strategic distance from which are creating less benefit.

Performance reporting: In the 4COM organization, the performance report of every

individuals are set up keeping in mind the end goal to break down position of items and

administrations. In connection to create points of interest from the referred to

organization's they generally performed.

TASK 2

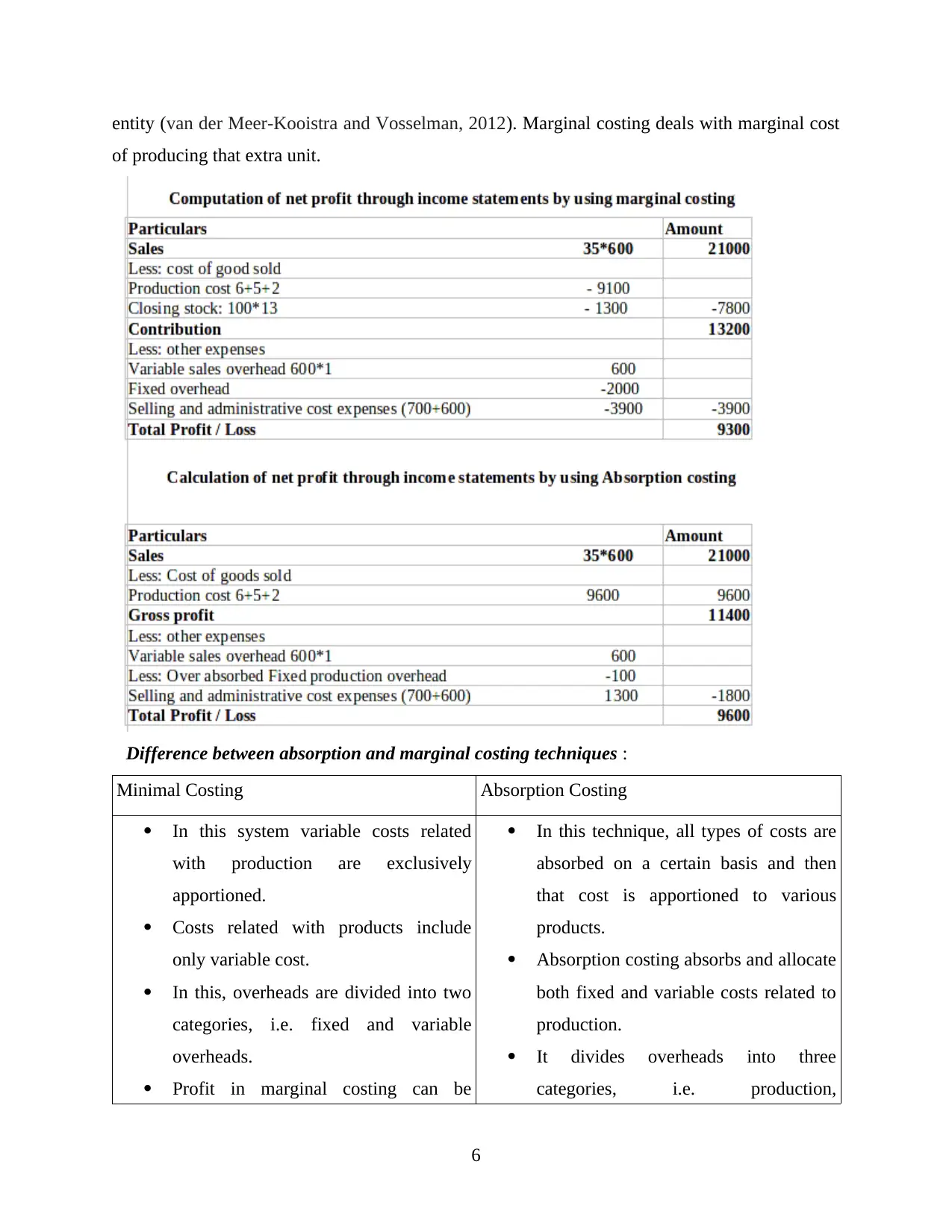

2.1 Calculation of net profit using absorption costing and marginal costing techniques

Net profit can be calculated through various techniques in the management accounting.

Net profit of Austin Fraser as per the absorption costing and marginal costing is shown as below:

Absorption Cost accounting: Absorption costing is a method of management accounting

through which various costs which are related with different types of production processes are

absorbed on a product. Further, this method is required to evaluate the inventory of an

entity(Busco and Scapens, 2011). Forecasting is the main element of management accounting.

All expenses are ascertained on a certain basis hence when those expenses actually occur, at that

time, it may be possible that budget expenses may vary from the actual one. Through absorption

costing, such over or under absorption can be treated accordingly.

Marginal Costing: Marginal costing principles are used for the internal decision making

purpose for short term. At different levels of activities, purpose of marginal costing can be

determined about the level to which contribution can be generated(Lukka and Modell, 2010). In

other words, marginal cost can be defined as change in cost of opportunity which changes due to

change in production. Change in opportunity cost due to increased production by one unit hence

cost of producing that one unit above a certain level can be determined as marginal cost for cited

5

introduce of the activities led in a money related year. Cost instrument will be settled in

association with the unmistakable costs that are procured and after that they will be

dispersed by them

Job costing reporting: Under this, those costs which are recognized by the organization

from the individual items are recorded in it. The aggregate incomes are decide by primary

with a specific end goal. The fundamental analysis which should be considered under this

revealing is to record each part points of interest those are delivered at the time. Those

stages are maintained as strategic distance from which are creating less benefit.

Performance reporting: In the 4COM organization, the performance report of every

individuals are set up keeping in mind the end goal to break down position of items and

administrations. In connection to create points of interest from the referred to

organization's they generally performed.

TASK 2

2.1 Calculation of net profit using absorption costing and marginal costing techniques

Net profit can be calculated through various techniques in the management accounting.

Net profit of Austin Fraser as per the absorption costing and marginal costing is shown as below:

Absorption Cost accounting: Absorption costing is a method of management accounting

through which various costs which are related with different types of production processes are

absorbed on a product. Further, this method is required to evaluate the inventory of an

entity(Busco and Scapens, 2011). Forecasting is the main element of management accounting.

All expenses are ascertained on a certain basis hence when those expenses actually occur, at that

time, it may be possible that budget expenses may vary from the actual one. Through absorption

costing, such over or under absorption can be treated accordingly.

Marginal Costing: Marginal costing principles are used for the internal decision making

purpose for short term. At different levels of activities, purpose of marginal costing can be

determined about the level to which contribution can be generated(Lukka and Modell, 2010). In

other words, marginal cost can be defined as change in cost of opportunity which changes due to

change in production. Change in opportunity cost due to increased production by one unit hence

cost of producing that one unit above a certain level can be determined as marginal cost for cited

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity (van der Meer-Kooistra and Vosselman, 2012). Marginal costing deals with marginal cost

of producing that extra unit.

Difference between absorption and marginal costing techniques :

Minimal Costing Absorption Costing

In this system variable costs related

with production are exclusively

apportioned.

Costs related with products include

only variable cost.

In this, overheads are divided into two

categories, i.e. fixed and variable

overheads.

Profit in marginal costing can be

In this technique, all types of costs are

absorbed on a certain basis and then

that cost is apportioned to various

products.

Absorption costing absorbs and allocate

both fixed and variable costs related to

production.

It divides overheads into three

categories, i.e. production,

6

of producing that extra unit.

Difference between absorption and marginal costing techniques :

Minimal Costing Absorption Costing

In this system variable costs related

with production are exclusively

apportioned.

Costs related with products include

only variable cost.

In this, overheads are divided into two

categories, i.e. fixed and variable

overheads.

Profit in marginal costing can be

In this technique, all types of costs are

absorbed on a certain basis and then

that cost is apportioned to various

products.

Absorption costing absorbs and allocate

both fixed and variable costs related to

production.

It divides overheads into three

categories, i.e. production,

6

ascertained through profit-volume

ration (PV Ratio)

administration and overheads related

with selling and distribution.

In absorption costing technique, net

profit as per income statement is

considered as a profit under absorption

costing.

Application of management accounting techniques in case of Austin Fraser :

Austin Fraser is an entity which has less than 50 employees in its organisational structure.

The net turnover of Austin Fraser is £500,000 hence it can be seen that the revenue of cited

entity is very low as compared to other companies working in the same sector and performing

same operations(Quinn, 2011). Management accounting and its techniques are very essential for

better operational and functional management. They coordinate with each other in assisting

management of cited entity in achievement of its objectives and goals(Nandan, 2010). Now a

days business environment managerial personnels needs to track performance of cited entity so

that they can trace that business organisation and its development is going in the right direction

and does it achieving desired targets(Macintosh and Quattrone, 2010). There are several

techniques of accounting and its management which can be used by management of Austin

Fraser , these techniques are mentioned below :

Cost Volume Profit Analysis(CVP Analysis) : Cost volume profit analysis is a technique

which is used by management of organisation for determining the impact of change in

cost of product and its volume on Austin Fraser's operating income and net income. Cited

entity needs to make an assumption that selling price will remain constant during course

of business. Reliability of CVP analysis depends on the fact that cost of production is

fixed during a given period of time(Sánchez-Rodríguez and Spraakman, 2012). In given

period actual production overhead, administration cost and selling cost is more than

budgeted cost, as collectively budgeted total cost of these three element was £ 2600 but

actual cost is £ 3300.On the other hand Budgeted selection of candidates through Austin

Fraser was 600 candidates during a particular time period but the actual population of

recruitment was 700 candidates during a particular period. Hence management

accounting officer of can analyse through cost volume profit analysis that how volume of

recruited candidates impacts the total cost.

7

ration (PV Ratio)

administration and overheads related

with selling and distribution.

In absorption costing technique, net

profit as per income statement is

considered as a profit under absorption

costing.

Application of management accounting techniques in case of Austin Fraser :

Austin Fraser is an entity which has less than 50 employees in its organisational structure.

The net turnover of Austin Fraser is £500,000 hence it can be seen that the revenue of cited

entity is very low as compared to other companies working in the same sector and performing

same operations(Quinn, 2011). Management accounting and its techniques are very essential for

better operational and functional management. They coordinate with each other in assisting

management of cited entity in achievement of its objectives and goals(Nandan, 2010). Now a

days business environment managerial personnels needs to track performance of cited entity so

that they can trace that business organisation and its development is going in the right direction

and does it achieving desired targets(Macintosh and Quattrone, 2010). There are several

techniques of accounting and its management which can be used by management of Austin

Fraser , these techniques are mentioned below :

Cost Volume Profit Analysis(CVP Analysis) : Cost volume profit analysis is a technique

which is used by management of organisation for determining the impact of change in

cost of product and its volume on Austin Fraser's operating income and net income. Cited

entity needs to make an assumption that selling price will remain constant during course

of business. Reliability of CVP analysis depends on the fact that cost of production is

fixed during a given period of time(Sánchez-Rodríguez and Spraakman, 2012). In given

period actual production overhead, administration cost and selling cost is more than

budgeted cost, as collectively budgeted total cost of these three element was £ 2600 but

actual cost is £ 3300.On the other hand Budgeted selection of candidates through Austin

Fraser was 600 candidates during a particular time period but the actual population of

recruitment was 700 candidates during a particular period. Hence management

accounting officer of can analyse through cost volume profit analysis that how volume of

recruited candidates impacts the total cost.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

3.1

There can be two type of control, i.e. budgetary control and financial control in

management accounting. Budget can be defined as a statement for forecasting of expenses over a

project. Through it Austin Fraser and its managerial team can decide that how much of fund is to

be employed on a particular project. Budgetary control assist an entity and its department to

coordinate with each other(Setthasakko, 2010). It is actually a technique through which the

budgeted or forecasted facts and figures are compared with the actual figures. Through such

analysis variances if any can be controlled easily and effectively(Pipan and Czarniawska, 2010).

The different type of budgetary tools are mentioned below : Master Budget : This is a comprehensive projection through which it can be explained

that in which manner cited entity wants to conducts its business operations for budgeted

period. Master budget is supported through cash budget, budgeted outgo statement, and a

budgeted statement for changes in business position. Cited entity requires to relate

various budgets of different departments of cited entity for preparation of a master

budget.

Operational Budget : it deals with revenue and expenses which are related with operating

activities(Renz, 2016). Proceeds from selling activity is considered as revenue and the

expenses which occurred in this process are considered as operating expenses. These

budgets are usually divided into various small reporting periods.

Advantages:

Regular maintain of expenses records are controlled and managed under this reports. It is

easy to maintain daily or monthly reports.

Disadvantage:

It is difficult to manage their daily transactions. Because they are in large amount. Cash Flow Budget : A cash flow budget is actually prepared so that cash flows which

arises during the course of business operations can be managed in a proper way.

Management Accounting Officer prepares cash flow budget to get information regarding

shortfall if any in sales and expenses(Shah, Malik and Malik, 2011). Through this an

entity can monitor the movement of cash and management can utilize such available cash

in better projects which can cultivate better results.

8

3.1

There can be two type of control, i.e. budgetary control and financial control in

management accounting. Budget can be defined as a statement for forecasting of expenses over a

project. Through it Austin Fraser and its managerial team can decide that how much of fund is to

be employed on a particular project. Budgetary control assist an entity and its department to

coordinate with each other(Setthasakko, 2010). It is actually a technique through which the

budgeted or forecasted facts and figures are compared with the actual figures. Through such

analysis variances if any can be controlled easily and effectively(Pipan and Czarniawska, 2010).

The different type of budgetary tools are mentioned below : Master Budget : This is a comprehensive projection through which it can be explained

that in which manner cited entity wants to conducts its business operations for budgeted

period. Master budget is supported through cash budget, budgeted outgo statement, and a

budgeted statement for changes in business position. Cited entity requires to relate

various budgets of different departments of cited entity for preparation of a master

budget.

Operational Budget : it deals with revenue and expenses which are related with operating

activities(Renz, 2016). Proceeds from selling activity is considered as revenue and the

expenses which occurred in this process are considered as operating expenses. These

budgets are usually divided into various small reporting periods.

Advantages:

Regular maintain of expenses records are controlled and managed under this reports. It is

easy to maintain daily or monthly reports.

Disadvantage:

It is difficult to manage their daily transactions. Because they are in large amount. Cash Flow Budget : A cash flow budget is actually prepared so that cash flows which

arises during the course of business operations can be managed in a proper way.

Management Accounting Officer prepares cash flow budget to get information regarding

shortfall if any in sales and expenses(Shah, Malik and Malik, 2011). Through this an

entity can monitor the movement of cash and management can utilize such available cash

in better projects which can cultivate better results.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages

Cash budgets are used to estimated the total cash expenditure which are done by the

company during the year.

Disadvantage:

It is difficult to control the extra cost which are incurred on production of a product

but one they can be control up to a extent. Financial Budget : A financial budget provides a detailed view over how Austin Fraser

procures funds and how and where it employs such available funds. It also provides

information about revenue form main business activity and return from other capital

expenditure. Management of organisational assets like building and other property where

cited entity has invested its fund needs to be managed so that they can provide better

return on investment(Jansen, 2011). Management accounting officer of Austin Fraser can

manage assets and other investment of Austin Fraser through preparation of financial

budget. Further financial budget can assist him in valuation of company in case of

mergers.

Static Budget : A static budget contains such elements which are not changed as per the

level of sales. Cost related with overheads shows a type of static budget(Vaivioand Sirén,

2010). Austin Fraser has certain department which has fixed budget hence head of such

departments needs to frame such strategies so that the expenses of departments will not

go over budget. Static budgets are mostly used by non profit sectors and small business

enterprises as they usually have less finance available as a result they allocate a limited

budget having a limited expenditure limit.

Benefit and limitations of various budgets:

Benefit Limitations

Planning tools of budgetary controls

can assist management accounting

officer in preparation of strategies

related to future operations. It can be

considered as most prominent feature

of budgetary control. Because through

they can make plan and after

Planning tools which are used in

budgetary control may put a certain

pressure over the employees of Austin

Fraser. As it creates a target to be

achieved but problem arises when such

targets are not easy to achieve hence in

this case a work load has been created

9

Cash budgets are used to estimated the total cash expenditure which are done by the

company during the year.

Disadvantage:

It is difficult to control the extra cost which are incurred on production of a product

but one they can be control up to a extent. Financial Budget : A financial budget provides a detailed view over how Austin Fraser

procures funds and how and where it employs such available funds. It also provides

information about revenue form main business activity and return from other capital

expenditure. Management of organisational assets like building and other property where

cited entity has invested its fund needs to be managed so that they can provide better

return on investment(Jansen, 2011). Management accounting officer of Austin Fraser can

manage assets and other investment of Austin Fraser through preparation of financial

budget. Further financial budget can assist him in valuation of company in case of

mergers.

Static Budget : A static budget contains such elements which are not changed as per the

level of sales. Cost related with overheads shows a type of static budget(Vaivioand Sirén,

2010). Austin Fraser has certain department which has fixed budget hence head of such

departments needs to frame such strategies so that the expenses of departments will not

go over budget. Static budgets are mostly used by non profit sectors and small business

enterprises as they usually have less finance available as a result they allocate a limited

budget having a limited expenditure limit.

Benefit and limitations of various budgets:

Benefit Limitations

Planning tools of budgetary controls

can assist management accounting

officer in preparation of strategies

related to future operations. It can be

considered as most prominent feature

of budgetary control. Because through

they can make plan and after

Planning tools which are used in

budgetary control may put a certain

pressure over the employees of Austin

Fraser. As it creates a target to be

achieved but problem arises when such

targets are not easy to achieve hence in

this case a work load has been created

9

implementation of such plans they can

control over future activities.

It can assist in coordination of different

department of Austin Fraser(Van

Helden and et. al., 2010). Hence they

can work in accordance with each other

and at last they can get satisfactory

results. Planning tools of budgetary

control can also help departments of

Austin Fraser to communicate various

important facts and figures with each

other that can affect cited entities

operations(Weißenberger and

Angelkort, 2011). Coordination and

communication between various

departments of cited entity helps them

to collectively achieve goals and

objectives of Austin Fraser.

Through planning tools of budgetary

control Austin Fraser has made a

system through which its limited

number of employees can acknowledge

of their responsibilities(Håkansson,

Kraus and Lind, 2010). So that it

becomes easy for them to achieve such

responsibilities. Budget managers can

be held responsible for managing

budgets of different departments and to

achieve forecasted output.

It also works as a base for performance

appraisal of employees who are

on employees through budgeting.

Which results in bad human relation in

business enterprise and inaccurate and

ineffective record keeping.

Resources are allocated through

planning tools of budgetary control.

Hence it may be possible less effective

allocation or improper allocation of

organisational gives rise to dispute

between various departments of Austin

Fraser.

If targets are not achieved then it may

be possible that all the department start

blaming each other(Ward, 2012). This

will increase disputes between various

departments and various employees.

It may be possible that managers of

Austin Fraser may estimate a high cost

at the time of preparation of budget so

that they will not get blamed in case of

over spending on a certain project.

10

control over future activities.

It can assist in coordination of different

department of Austin Fraser(Van

Helden and et. al., 2010). Hence they

can work in accordance with each other

and at last they can get satisfactory

results. Planning tools of budgetary

control can also help departments of

Austin Fraser to communicate various

important facts and figures with each

other that can affect cited entities

operations(Weißenberger and

Angelkort, 2011). Coordination and

communication between various

departments of cited entity helps them

to collectively achieve goals and

objectives of Austin Fraser.

Through planning tools of budgetary

control Austin Fraser has made a

system through which its limited

number of employees can acknowledge

of their responsibilities(Håkansson,

Kraus and Lind, 2010). So that it

becomes easy for them to achieve such

responsibilities. Budget managers can

be held responsible for managing

budgets of different departments and to

achieve forecasted output.

It also works as a base for performance

appraisal of employees who are

on employees through budgeting.

Which results in bad human relation in

business enterprise and inaccurate and

ineffective record keeping.

Resources are allocated through

planning tools of budgetary control.

Hence it may be possible less effective

allocation or improper allocation of

organisational gives rise to dispute

between various departments of Austin

Fraser.

If targets are not achieved then it may

be possible that all the department start

blaming each other(Ward, 2012). This

will increase disputes between various

departments and various employees.

It may be possible that managers of

Austin Fraser may estimate a high cost

at the time of preparation of budget so

that they will not get blamed in case of

over spending on a certain project.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.