Management Accounting Report: Costing and Profitability Analysis

VerifiedAdded on 2021/02/19

|25

|4606

|45

Report

AI Summary

This report delves into the core concepts of management accounting, emphasizing its role in decision-making within organizations. It examines various management accounting systems, including stock management, cost accounting, job costing, and price optimization systems, highlighting their benefits and applications. The report focuses on TPG Processing, a manufacturing company, and applies absorption and marginal costing techniques to prepare income statements. It also explores the advantages and disadvantages of different planning tools and compares how various organizations utilize management accounting to address financial challenges, ultimately demonstrating how management accounting contributes to sustainable success. The report further analyzes the importance of management accounting reporting, detailing account receivables, cost, performance, stock and production, and budget reports. It also critically evaluates the management accounting system and its reporting methods, while comparing and contrasting absorption and marginal costing methods.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

P1. Requirement of management accounting systems................................................................1

P2. Methods of management accounting reporting.....................................................................3

Benefits of management accounting system................................................................................4

Critically evaluate management accounting system and reporting.............................................4

P3 Preparing cost and profitability statement using absorption & marginal costing system......5

Interpretation:................................................................................................................................11

Part B.............................................................................................................................................12

P4. Advantage and disadvantage of different planning tool......................................................12

P5. Compare organizations that adapting to system of this accounting to respond to financial

problems....................................................................................................................................14

Conclusion.....................................................................................................................................16

REFERENCES..............................................................................................................................17

Books and journals....................................................................................................................17

2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

P1. Requirement of management accounting systems................................................................1

P2. Methods of management accounting reporting.....................................................................3

Benefits of management accounting system................................................................................4

Critically evaluate management accounting system and reporting.............................................4

P3 Preparing cost and profitability statement using absorption & marginal costing system......5

Interpretation:................................................................................................................................11

Part B.............................................................................................................................................12

P4. Advantage and disadvantage of different planning tool......................................................12

P5. Compare organizations that adapting to system of this accounting to respond to financial

problems....................................................................................................................................14

Conclusion.....................................................................................................................................16

REFERENCES..............................................................................................................................17

Books and journals....................................................................................................................17

2

INTRODUCTION

Managerial accounting (MA) is that branch of accounting which is concerned with

recording and analysing the cost related, financial information along with qualitative information

of the business. The main purpose of management accounting is to assist the managers of a

company in their decision-making process. Techniques of managerial accounting system are

applied by the companies for deriving the meaningful information from cost data that eventually

helps them in taking quality-decision for the entire organization. In the present report, concept of

MA will be discussed, various kinds of management accounting systems along with their

benefits will be highlighted. Further, why integration of management accounting is required is

going to be covered in the report.

The report is about TPG Processing, a company belonging to manufacturing sector. The

company deals manufacturing, transportation, distribution and services relating to business.

Different techniques of management such as absorption and marginal costing will be applied for

preparing the income statements. Moreover, a comparison will be seen in the project report

regarding how different organizations apply management accounting in dealing with their

financial issue and how management accounting leads an organization to sustainable success.

PART A

Requirement of MA System

Definitions of management accounting

Managerial accounting is defined as a procedure of evaluating and analysing the

expenses and costs of a business organization for preparing financial report meant for internal

use by the management of the company (Krishnan, 2015).

Management accounting implies for the process which in turn lays emphasis on providing

managers with financial information and resources for decision making purpose (Langfield-

Smith and et.al., 2017).

The aim of managerial accounting is to facilitate the manager of a business enterprise

with the much-needed information relating to costs through which manager becomes enable in

setting the prices of company's products and services. Management accountants focuses on

predicting the future expenses and income of then company by preparing budgets. They very

thoroughly analyse each and every activity of the business for the purpose of appropriately

1

Managerial accounting (MA) is that branch of accounting which is concerned with

recording and analysing the cost related, financial information along with qualitative information

of the business. The main purpose of management accounting is to assist the managers of a

company in their decision-making process. Techniques of managerial accounting system are

applied by the companies for deriving the meaningful information from cost data that eventually

helps them in taking quality-decision for the entire organization. In the present report, concept of

MA will be discussed, various kinds of management accounting systems along with their

benefits will be highlighted. Further, why integration of management accounting is required is

going to be covered in the report.

The report is about TPG Processing, a company belonging to manufacturing sector. The

company deals manufacturing, transportation, distribution and services relating to business.

Different techniques of management such as absorption and marginal costing will be applied for

preparing the income statements. Moreover, a comparison will be seen in the project report

regarding how different organizations apply management accounting in dealing with their

financial issue and how management accounting leads an organization to sustainable success.

PART A

Requirement of MA System

Definitions of management accounting

Managerial accounting is defined as a procedure of evaluating and analysing the

expenses and costs of a business organization for preparing financial report meant for internal

use by the management of the company (Krishnan, 2015).

Management accounting implies for the process which in turn lays emphasis on providing

managers with financial information and resources for decision making purpose (Langfield-

Smith and et.al., 2017).

The aim of managerial accounting is to facilitate the manager of a business enterprise

with the much-needed information relating to costs through which manager becomes enable in

setting the prices of company's products and services. Management accountants focuses on

predicting the future expenses and income of then company by preparing budgets. They very

thoroughly analyse each and every activity of the business for the purpose of appropriately

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

allocating and assigning the costs and other resources to each of the responsibility centre in the

business.

The primary difference between the managerial accounting and financial accounting is

that latter is concerned with the presenting and reporting the financial information for the

external use by different stakeholders such as customer, investors, government etc. While former

is concerned with the presentation and reporting of financial data for internal use by the

management for decision-making.

Role of management accounting :-

Managerial accounting plays an integral role within the business as :

It facilitates managers with necessary planning tools through which they undertake their

short and long term planning.

It aids in developing a management information system as reports from all other

departments are forwarded to management accountant for taking corrective actions (7

Roles of Management Accountant, 2019).

Managerial accounting helps the managers in exercising the controlling functions by

performing various techniques of measuring performance such as variance analysis,

budget etc. and evaluating it in order to find the reasons for deviations so that needed

actions could be taken.

It facilitates the managers in accurately forecasting the costs and income of the business

for a future accounting period.

It also allows the managers in keeping a check on the cash inflow and cash outflow which

takes place in the business, which in turn aid the managers in making more effective

strategies for increasing the cash inflows and reduce unnecessary cash outflow.

Different types of MA systems exists which different organizations employs in

accordance with their business requirements. They are as follows:

Stock management system:- This system of management accounting is a process of

tracking inventory, order, sales and deliveries of products. Through this system, managers of

organization evaluate and analyse to movement of stock from production to storage and from

storage to delivery (Hald and Thrane, 2016). It includes FIFO and LIFO method and managers

making decision about to order and maintaining to manufacture process.

2

business.

The primary difference between the managerial accounting and financial accounting is

that latter is concerned with the presenting and reporting the financial information for the

external use by different stakeholders such as customer, investors, government etc. While former

is concerned with the presentation and reporting of financial data for internal use by the

management for decision-making.

Role of management accounting :-

Managerial accounting plays an integral role within the business as :

It facilitates managers with necessary planning tools through which they undertake their

short and long term planning.

It aids in developing a management information system as reports from all other

departments are forwarded to management accountant for taking corrective actions (7

Roles of Management Accountant, 2019).

Managerial accounting helps the managers in exercising the controlling functions by

performing various techniques of measuring performance such as variance analysis,

budget etc. and evaluating it in order to find the reasons for deviations so that needed

actions could be taken.

It facilitates the managers in accurately forecasting the costs and income of the business

for a future accounting period.

It also allows the managers in keeping a check on the cash inflow and cash outflow which

takes place in the business, which in turn aid the managers in making more effective

strategies for increasing the cash inflows and reduce unnecessary cash outflow.

Different types of MA systems exists which different organizations employs in

accordance with their business requirements. They are as follows:

Stock management system:- This system of management accounting is a process of

tracking inventory, order, sales and deliveries of products. Through this system, managers of

organization evaluate and analyse to movement of stock from production to storage and from

storage to delivery (Hald and Thrane, 2016). It includes FIFO and LIFO method and managers

making decision about to order and maintaining to manufacture process.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIFO :- it is the method of stock management that means product that recent purchased on

particular cost so it first to be sale.

FIFO :- it stands for first In first out and it refers that the oldest inventory recorded swill be sold

first.

In addition to this, there are several tools available which can be used for inventory

management include EOQ, JIT etc. Stock management tools provide deeper insight about stock

which need to maintain within an organization for ensuring smooth functioning of operations.

This in turn helps in maximizing profitability by reducing the cost associated with holding and

ordering aspects.

Cost accounting system :- It is an essential type of management accounting that is used

by management of TPG to estimate the cost of their product to analysis profit. Production

process includes fixed and variable cost. Cost that never changing with quantity and quality of

product is called fixed cost. Those cost that changing with unit of production, is called as

variable cost (Schaltegger and Burritt, 2017). It also reduces difficulties because many

departments includes in organization and all have different income and expenditure. Managers

use to this system and calculate to cost very effectively and efficiently. For example – labour

cost and overhead. Cost management system is highly significant which in turn helps in turn

helps in setting appropriate prices of products or services. It clearly presents expenses incurred

for offering products or services. Hence, by dividing total costs from number of items per unit

cost can be assessed. Further, by adding gross margin % in per unit cost price can be determined

effectually.

Job costing system :- It can be defined as the framework for allocating and accumulating

the costs of manufacturing of a particular product or job. It uses by manufacturing organization

who produce products according to demand and order of customers. This system makes to easy

process of organization because in TPG, many types of job considered and every job consume

cost like labour, overhead and material. Mangers also keep records in proper manner through it

(Armitage, Webb and Glynn, 2016).

Price optimization system :- Management of TPG use to this system of accounting that

helps to evaluate and understand behaviour of customer with changing price of products. It also

helpful for organization because they understand through fluctuation in demand and supply and

3

particular cost so it first to be sale.

FIFO :- it stands for first In first out and it refers that the oldest inventory recorded swill be sold

first.

In addition to this, there are several tools available which can be used for inventory

management include EOQ, JIT etc. Stock management tools provide deeper insight about stock

which need to maintain within an organization for ensuring smooth functioning of operations.

This in turn helps in maximizing profitability by reducing the cost associated with holding and

ordering aspects.

Cost accounting system :- It is an essential type of management accounting that is used

by management of TPG to estimate the cost of their product to analysis profit. Production

process includes fixed and variable cost. Cost that never changing with quantity and quality of

product is called fixed cost. Those cost that changing with unit of production, is called as

variable cost (Schaltegger and Burritt, 2017). It also reduces difficulties because many

departments includes in organization and all have different income and expenditure. Managers

use to this system and calculate to cost very effectively and efficiently. For example – labour

cost and overhead. Cost management system is highly significant which in turn helps in turn

helps in setting appropriate prices of products or services. It clearly presents expenses incurred

for offering products or services. Hence, by dividing total costs from number of items per unit

cost can be assessed. Further, by adding gross margin % in per unit cost price can be determined

effectually.

Job costing system :- It can be defined as the framework for allocating and accumulating

the costs of manufacturing of a particular product or job. It uses by manufacturing organization

who produce products according to demand and order of customers. This system makes to easy

process of organization because in TPG, many types of job considered and every job consume

cost like labour, overhead and material. Mangers also keep records in proper manner through it

(Armitage, Webb and Glynn, 2016).

Price optimization system :- Management of TPG use to this system of accounting that

helps to evaluate and understand behaviour of customer with changing price of products. It also

helpful for organization because they understand through fluctuation in demand and supply and

3

then change prices of product (Lapsley and Rekers, 2017). That consumer can easily afford and

organization achieve goal and meet objective.

Methods of management accounting reporting.

Reporting of management accounting helps to evaluate and analyse accuracy of data and

informations of all reports of TPG. All report of organization provide helps to managers in

making effective decision, and they easily achieve goal and objective. Reports of management

accounting is essential and useful for stakeholders because they can measure performance and

situation of organizational profit. Stakeholders like CEO, owners and investors.

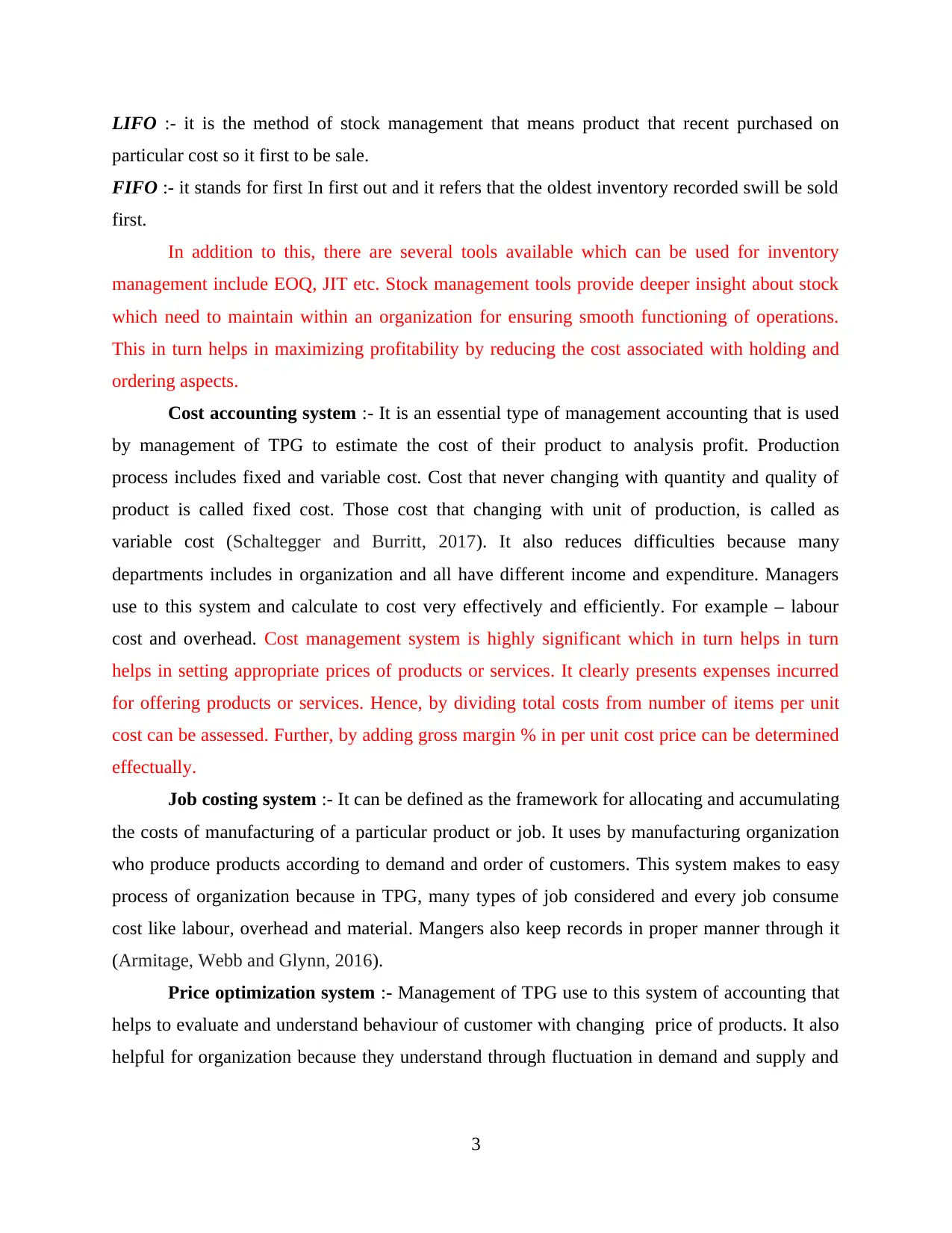

Account receivables report :- This report includes those types of customers that they

used to products and services of TPG but not yet paid by customers. That means customers owe

organization's payment. On the bases of those customers, management make to this report. TPG

also evaluate to health of customers related to finance. Account receivables is the assets of

organization.

4

organization achieve goal and meet objective.

Methods of management accounting reporting.

Reporting of management accounting helps to evaluate and analyse accuracy of data and

informations of all reports of TPG. All report of organization provide helps to managers in

making effective decision, and they easily achieve goal and objective. Reports of management

accounting is essential and useful for stakeholders because they can measure performance and

situation of organizational profit. Stakeholders like CEO, owners and investors.

Account receivables report :- This report includes those types of customers that they

used to products and services of TPG but not yet paid by customers. That means customers owe

organization's payment. On the bases of those customers, management make to this report. TPG

also evaluate to health of customers related to finance. Account receivables is the assets of

organization.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost report :- TPG prepare report related to cost and it helpful to analyse cost and

charges related to job, products and activity and process. Through this report managers can

control to cost in effective manner. All expenses and revenue also considered in this report and

management use for making decision (Armitage, Webb and Glynn, 2016). It also makes to

calculation process effective so members of organization can calculate to all types of cost that

occurred and use in organization.

Performance report :- Individual performance in organization is recorded by

management in this report. Data and informations related to operation also includes in it. TPG's

performance present by this report in front of stakeholders, so stakeholders evaluate and

5

charges related to job, products and activity and process. Through this report managers can

control to cost in effective manner. All expenses and revenue also considered in this report and

management use for making decision (Armitage, Webb and Glynn, 2016). It also makes to

calculation process effective so members of organization can calculate to all types of cost that

occurred and use in organization.

Performance report :- Individual performance in organization is recorded by

management in this report. Data and informations related to operation also includes in it. TPG's

performance present by this report in front of stakeholders, so stakeholders evaluate and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understand performance of organization before invest their capital. Mangers of TPG analyse the

performance report and if they get any types of weakness and loophole, so they make strategies

to overcome and developing their action to increase profit.

Stock and production report :- It contains all types of data and information related to

stock and manufacturing so management of TPG evaluate this report and find wastage of time

by labour and wastage of products. The process of Elimination of wastage of products and hours

influence to profitability and productivity. This report is very effective because wastage put more

effect on organizational profit.

Budget report :- Budget report is an internal report that js used by management of TPG

and make estimate. Different department and function includes in organization so management

prepare budget for all of them. It makes for future on the basis of current budget. They also

6

performance report and if they get any types of weakness and loophole, so they make strategies

to overcome and developing their action to increase profit.

Stock and production report :- It contains all types of data and information related to

stock and manufacturing so management of TPG evaluate this report and find wastage of time

by labour and wastage of products. The process of Elimination of wastage of products and hours

influence to profitability and productivity. This report is very effective because wastage put more

effect on organizational profit.

Budget report :- Budget report is an internal report that js used by management of TPG

and make estimate. Different department and function includes in organization so management

prepare budget for all of them. It makes for future on the basis of current budget. They also

6

measure past and present performance in given budget. Organization get helps in making

effective decision for future. It is an estimation of revenue and cost for particular period.

Sales report :- TPG earn profit and revenue through sale of product so it includes and

considered in this report. It sales their products through wholesaler and retailer and management

observe through this report that who make more profit in organization. They also make strategies

and provide motivation through provide bonus, incentives and reward against to their work.

Through all these employees and members get motivation and do work with their full efforts.

Benefits of management accounting system.

Management accounting system is very beneficial for organization because management

of TPG measures past results and make action plan for future (Christ and Burritt, 2015). It also

beneficial in making decision about future and measures actual performance with given budgets.

All these things useful in raising profitability and productivity of organization.

Critically evaluate management accounting system and reporting.

Accounting system of management in TPG play vital role because they make future

decision with the helps of past financial data. Managers understand all condition and situation of

future related to budget so this system provide major helps to them in making decision.

Efficiency of business increasing through this and customer get quality services and products so

all these things increasing profitably and productivity. Its negative aspect that it has a futuristic

nature and future is uncertain so it provides data and informations for planing and decision-

making and it not necessary that plan of management provide positive and expected results. This

process consume more cost and time.

Management accounting report is also effective tool and it helpful for business. All

stakeholders get many types of data and informations, and they can easily understand to

performance of TPG. It has negative aspect that it takes higher cost and time because managers

of organization has to make many rules and regulations.

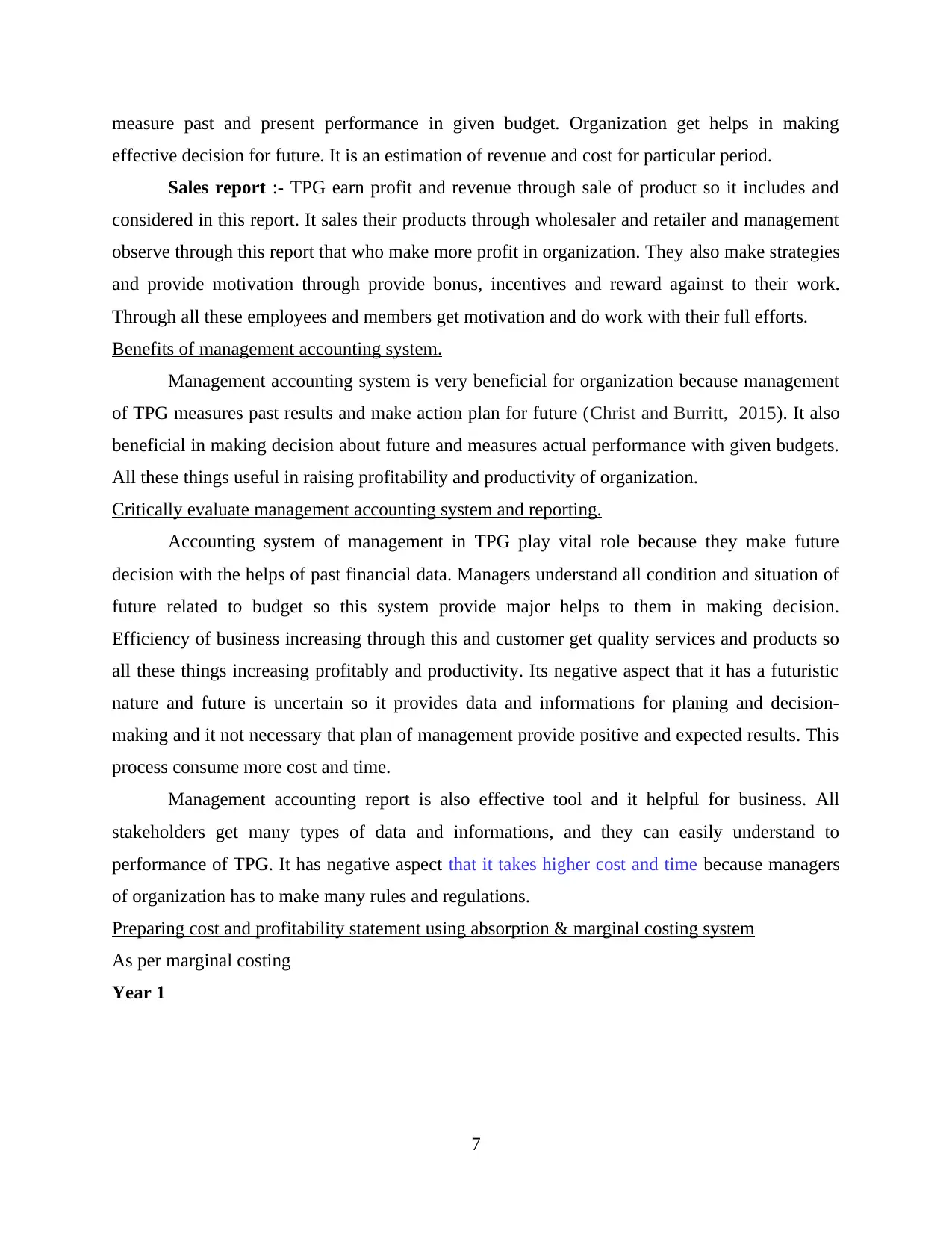

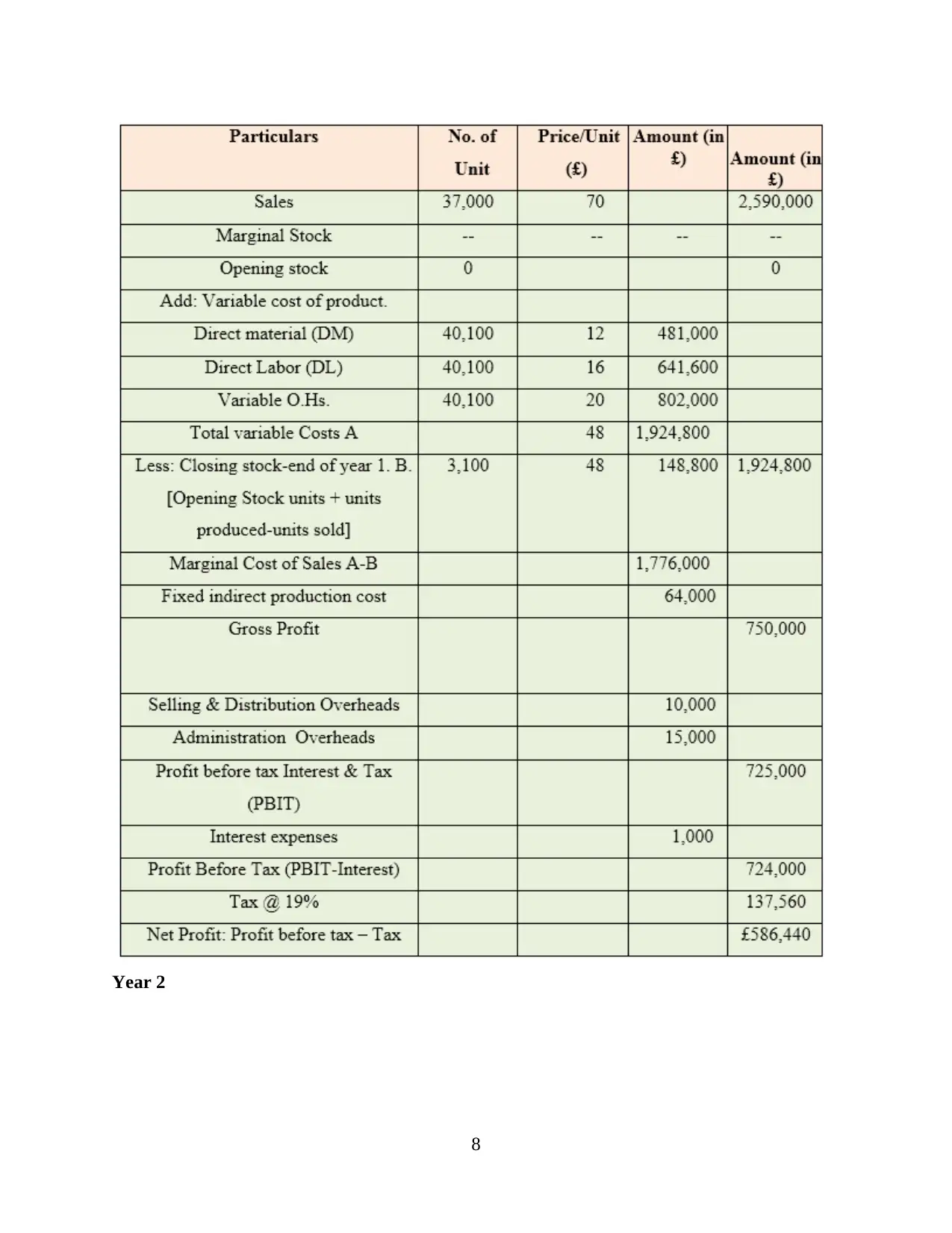

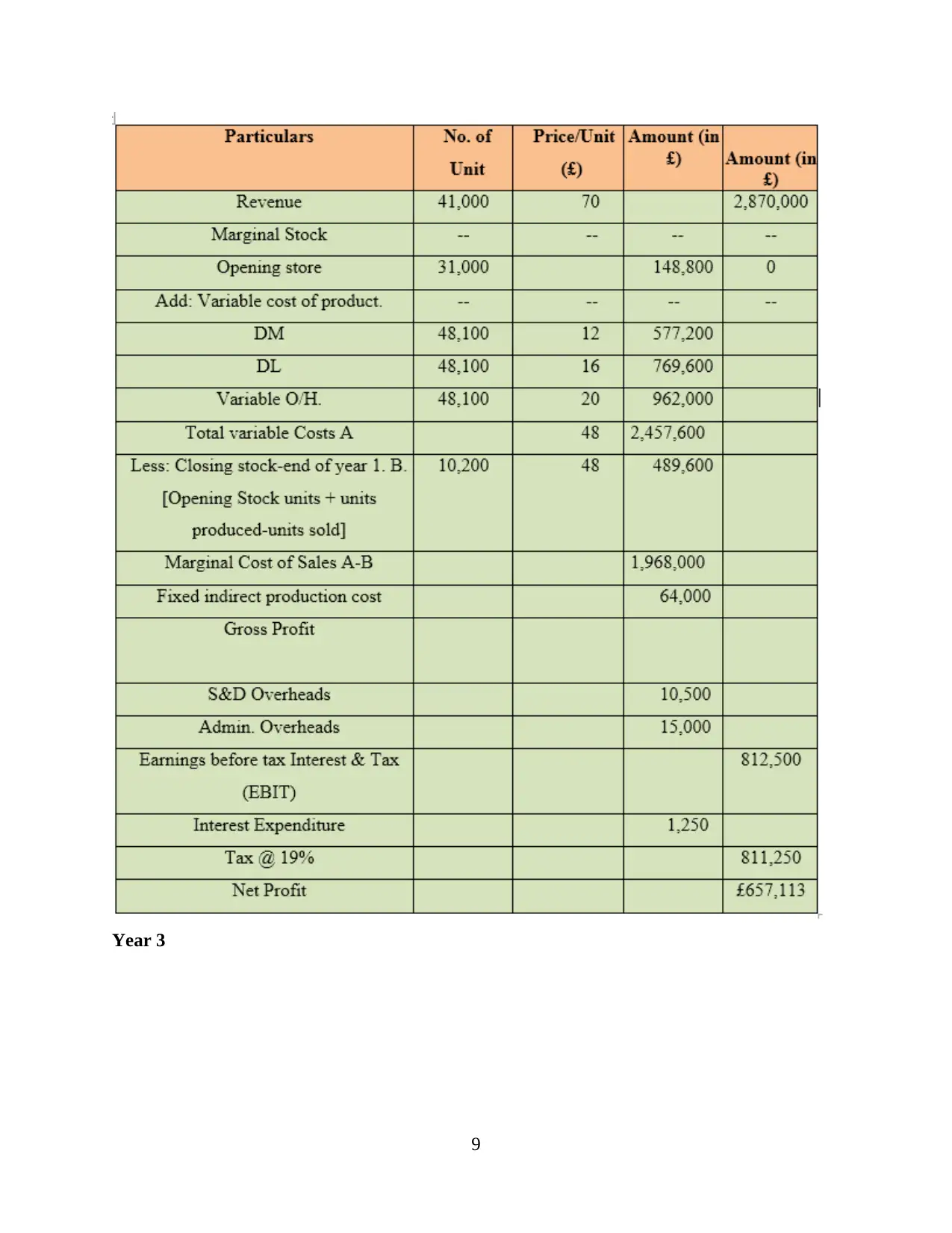

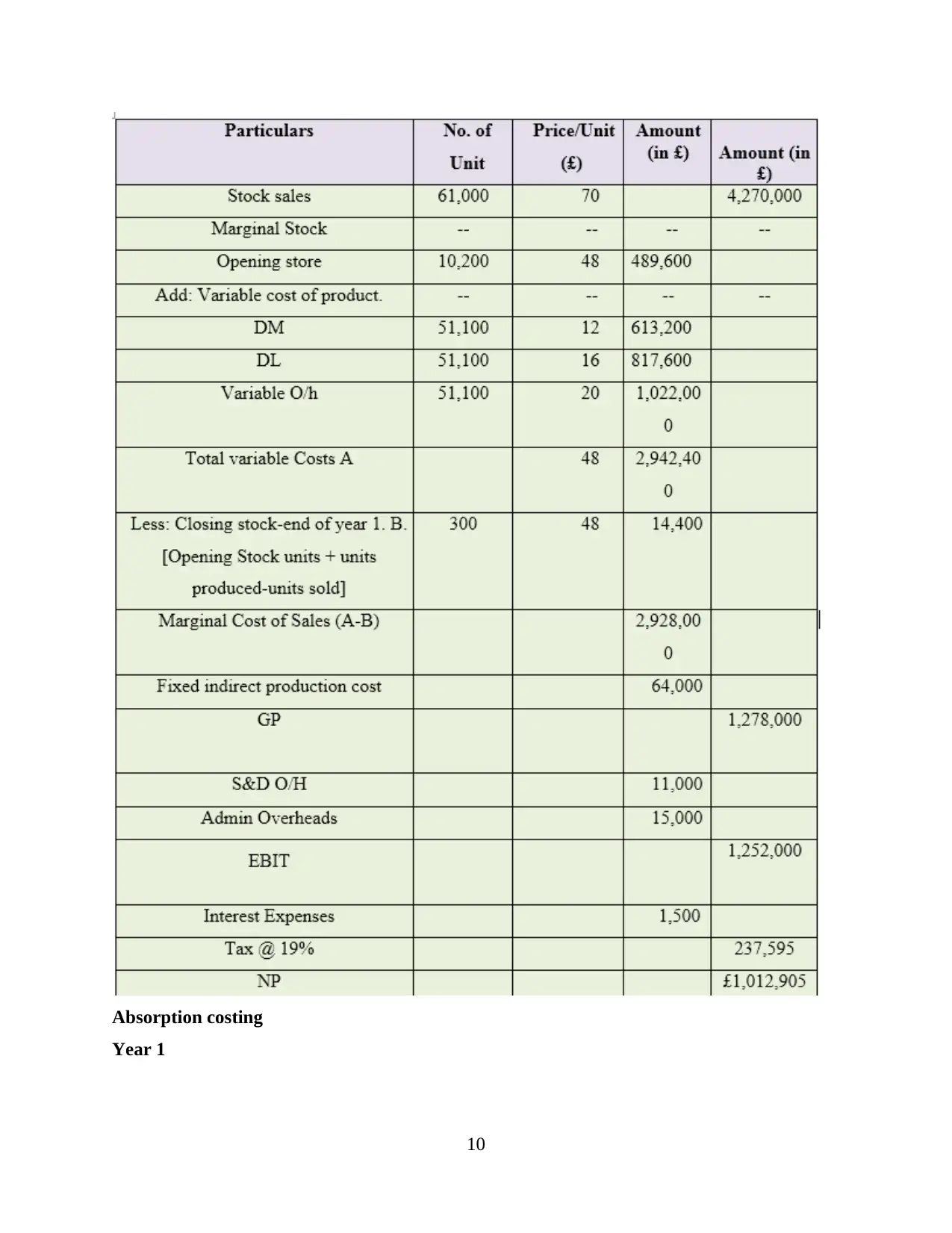

Preparing cost and profitability statement using absorption & marginal costing system

As per marginal costing

Year 1

7

effective decision for future. It is an estimation of revenue and cost for particular period.

Sales report :- TPG earn profit and revenue through sale of product so it includes and

considered in this report. It sales their products through wholesaler and retailer and management

observe through this report that who make more profit in organization. They also make strategies

and provide motivation through provide bonus, incentives and reward against to their work.

Through all these employees and members get motivation and do work with their full efforts.

Benefits of management accounting system.

Management accounting system is very beneficial for organization because management

of TPG measures past results and make action plan for future (Christ and Burritt, 2015). It also

beneficial in making decision about future and measures actual performance with given budgets.

All these things useful in raising profitability and productivity of organization.

Critically evaluate management accounting system and reporting.

Accounting system of management in TPG play vital role because they make future

decision with the helps of past financial data. Managers understand all condition and situation of

future related to budget so this system provide major helps to them in making decision.

Efficiency of business increasing through this and customer get quality services and products so

all these things increasing profitably and productivity. Its negative aspect that it has a futuristic

nature and future is uncertain so it provides data and informations for planing and decision-

making and it not necessary that plan of management provide positive and expected results. This

process consume more cost and time.

Management accounting report is also effective tool and it helpful for business. All

stakeholders get many types of data and informations, and they can easily understand to

performance of TPG. It has negative aspect that it takes higher cost and time because managers

of organization has to make many rules and regulations.

Preparing cost and profitability statement using absorption & marginal costing system

As per marginal costing

Year 1

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year 2

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 3

9

9

Absorption costing

Year 1

10

Year 1

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.