Management Accounting Report: Strategies, Analysis, and Comparison

VerifiedAdded on 2020/06/05

|14

|3958

|58

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within R. L. Maynard Ltd, a construction business. It begins with definitions of management accounting and its essential systems, including cost accounting, inventory management, job costing, and price optimization. The report then delves into various management accounting reporting methods such as budget reports, accounts receivable aging, job cost reports, and inventory and manufacturing reports, highlighting their importance in decision-making and financial control. A significant portion of the report focuses on cost analysis, comparing and contrasting marginal and absorption costing methods to prepare profit and loss statements. The report also explores strategies and techniques used for budgetary control, discussing their advantages and disadvantages. Finally, it examines methods for addressing financial problems through management accounting systems. The report concludes by summarizing the key findings and insights, offering a practical understanding of management accounting's role in business operations and financial management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P1. Definition of management accounting and necessary needs of management accounting

systems...................................................................................................................................1

P2. Methods for management accounting reporting...............................................................3

P3 Cost analysis to prepare an P&L by marginal and absorption costs for R. L. Maynard Ltd 6

Difference among two techniques of MA used t prepare income statements........................7

Task 3...............................................................................................................................................8

P4 Various Strategies techniques used for budgetary control and Advantages and

disadvantages within R. L. Maynard Ltd..............................................................................8

Task 4...............................................................................................................................................9

P5 Comparing method through which systems of management accounting used by combating

financial problems..................................................................................................................9

Conclusion.....................................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................12

INTRODUCTION...........................................................................................................................1

P1. Definition of management accounting and necessary needs of management accounting

systems...................................................................................................................................1

P2. Methods for management accounting reporting...............................................................3

P3 Cost analysis to prepare an P&L by marginal and absorption costs for R. L. Maynard Ltd 6

Difference among two techniques of MA used t prepare income statements........................7

Task 3...............................................................................................................................................8

P4 Various Strategies techniques used for budgetary control and Advantages and

disadvantages within R. L. Maynard Ltd..............................................................................8

Task 4...............................................................................................................................................9

P5 Comparing method through which systems of management accounting used by combating

financial problems..................................................................................................................9

Conclusion.....................................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................12

INTRODUCTION

Management accounting provides information of accounting to managers within

companies. It is to give company with the base for make informed enterprise conclusion that will

permit organisation to be healthier equip in their direction and power functions. This is the

activity of ready accounts and management reports and gives straight report by managers to

make daily and little period decisions. This present report based on R. L. Maynard Ltd. which

was registered on 22nd March 1973 with construction business. There are 20-49 employees

currently working and they have one subsidiary for prepare management accounting report,

there are different methods used and that have some advantage and disadvantage. Through

management accounting system entire financial problems can be solve in the organisations

P1. Definition of management accounting and necessary needs of management accounting

systems

From: - Management accounting officer

To: - General Manager of R. L. Maynard Ltd.

Subject: - Management accounting system

Introduction:-

The present task cover meaning of management accounting, essential requirement and

different types of management accounting system for R. L. Maynard Ltd.

Meaning of Management accounting system:-

Management accounting is an occupation that concern in management decision making

by partnering, performance management and making planning methods with control to assist

management in the preparation, providing expertise in financial reporting and execution of

organisation's plan of action. Financial accounting produces yearly report in order to

stakeholders and generate monthly reports for organization's department employees and the chief

executive msnsgers (Renz, 2016.). This report shows the amount of money of acquirable cash

and orders in hand, sales income generated, accounts payable and receivable, outstanding debts,

raw material and inventory.

Methods of management accounting systems:

1. Cost accounting systems

Management accounting provides information of accounting to managers within

companies. It is to give company with the base for make informed enterprise conclusion that will

permit organisation to be healthier equip in their direction and power functions. This is the

activity of ready accounts and management reports and gives straight report by managers to

make daily and little period decisions. This present report based on R. L. Maynard Ltd. which

was registered on 22nd March 1973 with construction business. There are 20-49 employees

currently working and they have one subsidiary for prepare management accounting report,

there are different methods used and that have some advantage and disadvantage. Through

management accounting system entire financial problems can be solve in the organisations

P1. Definition of management accounting and necessary needs of management accounting

systems

From: - Management accounting officer

To: - General Manager of R. L. Maynard Ltd.

Subject: - Management accounting system

Introduction:-

The present task cover meaning of management accounting, essential requirement and

different types of management accounting system for R. L. Maynard Ltd.

Meaning of Management accounting system:-

Management accounting is an occupation that concern in management decision making

by partnering, performance management and making planning methods with control to assist

management in the preparation, providing expertise in financial reporting and execution of

organisation's plan of action. Financial accounting produces yearly report in order to

stakeholders and generate monthly reports for organization's department employees and the chief

executive msnsgers (Renz, 2016.). This report shows the amount of money of acquirable cash

and orders in hand, sales income generated, accounts payable and receivable, outstanding debts,

raw material and inventory.

Methods of management accounting systems:

1. Cost accounting systems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This accounting system is a model used by organisations to figure the expenditure of their

goods for gainfulness investigation, inventory valuation and cost control. This system is based on

company's entire cost of the products. Company must know that which product are profitable

and which products are not profitable in the organisation (Chenhall, and Moers, 2015). There are

two types of cost accounting systems i.e. the job order and process costing. Job order costing is a

cost accounting system that roll up manufacturing costs separately for each job and procedure

costing for all process. R. L. Maynard Ltd. also uses this system for their operational work. As

company can know that how much their cost of product and how much price for the selling. All

construction goods can be used in the cost accounting system for controlling their cost.

2. Inventory management system

An inventory management is a model used by company for maintaining the inventory of

good selling and purchasing . This system is for following inventory levels, sales and deliveries.

It can also be used in the construction industry to create a work order, bill of materials and

another industry related papers. All data of sales, purchase, raw material, sales return, purchase

return, packaging, deliveries, unfinished of goods are maintaining in the inventory management

system (Quinn, 2014. ). R. L. Maynard Ltd can use this system for making their inventory and

manage the entire data. They also can used into sales and purchase report, so they will easily find

the details in future,when they require it. its also can be used in company's product's succefull

and pending deliveries. So it is the best system to keep the in safe for the further query.

3. Job costing system

Through this system company can easily track the record of cost revenue by job and

reporting of profitability. It is the procedure of determining the labour and material cost for each

job in a systematic way. It can be used in the industry to secure their goods and prices cover

actual cost and provides a profit to the company. The reason of any business is to make more

profit from their business, and job costing is the most effective system to ensure that happen

(Wagenhofer, 2016.). R. L. Maynard Ltd use this system for their labour, that how much

revenues are getting from them. and how much pay, they are receiving. Company can use this

system for their productivity and profitability of the organisation. This system is based on

emplyee's productivity, so if employees can not be able to provide their productivity according to

target, then company can take action, which can decrease the further budget.

4. Price optimising system

goods for gainfulness investigation, inventory valuation and cost control. This system is based on

company's entire cost of the products. Company must know that which product are profitable

and which products are not profitable in the organisation (Chenhall, and Moers, 2015). There are

two types of cost accounting systems i.e. the job order and process costing. Job order costing is a

cost accounting system that roll up manufacturing costs separately for each job and procedure

costing for all process. R. L. Maynard Ltd. also uses this system for their operational work. As

company can know that how much their cost of product and how much price for the selling. All

construction goods can be used in the cost accounting system for controlling their cost.

2. Inventory management system

An inventory management is a model used by company for maintaining the inventory of

good selling and purchasing . This system is for following inventory levels, sales and deliveries.

It can also be used in the construction industry to create a work order, bill of materials and

another industry related papers. All data of sales, purchase, raw material, sales return, purchase

return, packaging, deliveries, unfinished of goods are maintaining in the inventory management

system (Quinn, 2014. ). R. L. Maynard Ltd can use this system for making their inventory and

manage the entire data. They also can used into sales and purchase report, so they will easily find

the details in future,when they require it. its also can be used in company's product's succefull

and pending deliveries. So it is the best system to keep the in safe for the further query.

3. Job costing system

Through this system company can easily track the record of cost revenue by job and

reporting of profitability. It is the procedure of determining the labour and material cost for each

job in a systematic way. It can be used in the industry to secure their goods and prices cover

actual cost and provides a profit to the company. The reason of any business is to make more

profit from their business, and job costing is the most effective system to ensure that happen

(Wagenhofer, 2016.). R. L. Maynard Ltd use this system for their labour, that how much

revenues are getting from them. and how much pay, they are receiving. Company can use this

system for their productivity and profitability of the organisation. This system is based on

emplyee's productivity, so if employees can not be able to provide their productivity according to

target, then company can take action, which can decrease the further budget.

4. Price optimising system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price management system is based on accounting analysis of how customers will gives

response to different prices for its services and goods through different souces. Through this

system, company fixes their product's prices for selling in the different market (Morales, and

Lambert, 2013.). This system is also used by R. L. Maynard Ltd. for their selling price in the

market.

So its valuable for the company, because an organisation want to make money from their

products and services, but they can not able to do make more profit from only selling and

purchasing. They required of all these system, which will be profitable for their organisation and

it is also a record or report, which help in future.

P2. Methods for management accounting reporting

From: - Management accounting officer

To: - General Manager of R. L. Maynard Ltd

Subject: - Management accounting reports

Introduction:-

The present task will cover definition of management accounting report, essential

requirements of different methods of management accounting reporting and their use in the same

for R. L. Maynard Ltd.

Definition of Management accounting reporting:-

Management accounting report is portion of making sure that Company has

accomplished presentation of how business performance and what finance condition of the

company. This report help R. L. Maynard Ltd business owner and managers monitor the

company's performance and prepared rarely throughout accounting period as required (Nielsen,

and Nørreklit, 2015,).

Methods of management accounting reporting:

1. Budget report

Budget report is based on performance of company, if organisation's enterprise is large

enough, then managers require to analysis their department's performance and how can control

their costing. Company's estimated budget based on the expenses, which done in past years. If

department's employee productivity not accomplish according to cost then it budget will decrease

in future. This budget report can be used in employee's incentive report by the manager. In this

response to different prices for its services and goods through different souces. Through this

system, company fixes their product's prices for selling in the different market (Morales, and

Lambert, 2013.). This system is also used by R. L. Maynard Ltd. for their selling price in the

market.

So its valuable for the company, because an organisation want to make money from their

products and services, but they can not able to do make more profit from only selling and

purchasing. They required of all these system, which will be profitable for their organisation and

it is also a record or report, which help in future.

P2. Methods for management accounting reporting

From: - Management accounting officer

To: - General Manager of R. L. Maynard Ltd

Subject: - Management accounting reports

Introduction:-

The present task will cover definition of management accounting report, essential

requirements of different methods of management accounting reporting and their use in the same

for R. L. Maynard Ltd.

Definition of Management accounting reporting:-

Management accounting report is portion of making sure that Company has

accomplished presentation of how business performance and what finance condition of the

company. This report help R. L. Maynard Ltd business owner and managers monitor the

company's performance and prepared rarely throughout accounting period as required (Nielsen,

and Nørreklit, 2015,).

Methods of management accounting reporting:

1. Budget report

Budget report is based on performance of company, if organisation's enterprise is large

enough, then managers require to analysis their department's performance and how can control

their costing. Company's estimated budget based on the expenses, which done in past years. If

department's employee productivity not accomplish according to cost then it budget will decrease

in future. This budget report can be used in employee's incentive report by the manager. In this

case, some of the money budgeted may be given out up as incentive to their workers for

accomplish their financial target.

2. Accounts receivable aging

This report is a critical way for managing cash flow for organisations that increase credit

to their customers. Many of the aging reports include separate columns for bills that are 30 , or

60 days late or more than that. Manager can use this report to find some problems which is with

organisation's collection process. If any customer can not be able to pay their outstanding

amount, then company will take serious action according to their credit policies (Alawattage,

and Uddin 2017). R. L. Maynard Ltd can make a report for the customers, who pay their

outstanding on time and who can not able to pay their remaining amount in time. So company

can take an action according to credit policies and get the outstanding amount from their

customers. This report is valuable for the organisation, because account receivable report keep

all data of organisation for further issues.

accomplish their financial target.

2. Accounts receivable aging

This report is a critical way for managing cash flow for organisations that increase credit

to their customers. Many of the aging reports include separate columns for bills that are 30 , or

60 days late or more than that. Manager can use this report to find some problems which is with

organisation's collection process. If any customer can not be able to pay their outstanding

amount, then company will take serious action according to their credit policies (Alawattage,

and Uddin 2017). R. L. Maynard Ltd can make a report for the customers, who pay their

outstanding on time and who can not able to pay their remaining amount in time. So company

can take an action according to credit policies and get the outstanding amount from their

customers. This report is valuable for the organisation, because account receivable report keep

all data of organisation for further issues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Job cost report -

Job cost report provide view an entire sides of the entire cost accumulated in a single

project compared to the required revenue output by the project. Its provides expenses for a

specific projection. Managers are usually matched with estimated of revenue, so they can easily

evaluate the job's productivity or profitability. It report shows high profitable departments of the

company (Otley, 2015.). So the organisation can focus on that departments instead of wasting

money and time on jobs with less profit margins. In the R. L. Maynard Ltd, job cost report can

be made with some effective points. They can make a report of employees productivity and their

revenue, which required by company. Further, they will be able to evaluate job's profitability.

4. Inventory and manufacturing report-

This report is the based on company's inventory and manufacturing product, which

produce and sale in the market. Organisations that produce with physical inventory can use

managerial accounting reports to make their manufacturing processes more cost effective. They

help centralize data on inventory costs, labour, and other forms of operating expense

participating in the production process, providing raw data to optimize assembly or machining.

This report can gives most effective use to R. L. Maynard Ltd. In order to get the number of

sale, purchase, sales return, purchase return, raw material, deliveries, pending deliveries and

outstanding amount. Then company can know the cost of entire task and will be able to evaluate

company's effective cost and expenses. So these reports are valuable for R. L. Maynard Ltd and

through these, they can control their cost, increase budget for most profitable departments,

decrease budget for low productivity department and provide bonus or incentive to their valuable

employees. This bonus and incentives are make them happy and motivated for their best work

(Ashraf, and Uddin,2015).

Importance of management accounting reporting :-

Helping in make or buy decisions and forecasting cash flow.

Helping understand performance variances and analysing the rate of return.

Helping forecast the future.

Job cost report provide view an entire sides of the entire cost accumulated in a single

project compared to the required revenue output by the project. Its provides expenses for a

specific projection. Managers are usually matched with estimated of revenue, so they can easily

evaluate the job's productivity or profitability. It report shows high profitable departments of the

company (Otley, 2015.). So the organisation can focus on that departments instead of wasting

money and time on jobs with less profit margins. In the R. L. Maynard Ltd, job cost report can

be made with some effective points. They can make a report of employees productivity and their

revenue, which required by company. Further, they will be able to evaluate job's profitability.

4. Inventory and manufacturing report-

This report is the based on company's inventory and manufacturing product, which

produce and sale in the market. Organisations that produce with physical inventory can use

managerial accounting reports to make their manufacturing processes more cost effective. They

help centralize data on inventory costs, labour, and other forms of operating expense

participating in the production process, providing raw data to optimize assembly or machining.

This report can gives most effective use to R. L. Maynard Ltd. In order to get the number of

sale, purchase, sales return, purchase return, raw material, deliveries, pending deliveries and

outstanding amount. Then company can know the cost of entire task and will be able to evaluate

company's effective cost and expenses. So these reports are valuable for R. L. Maynard Ltd and

through these, they can control their cost, increase budget for most profitable departments,

decrease budget for low productivity department and provide bonus or incentive to their valuable

employees. This bonus and incentives are make them happy and motivated for their best work

(Ashraf, and Uddin,2015).

Importance of management accounting reporting :-

Helping in make or buy decisions and forecasting cash flow.

Helping understand performance variances and analysing the rate of return.

Helping forecast the future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

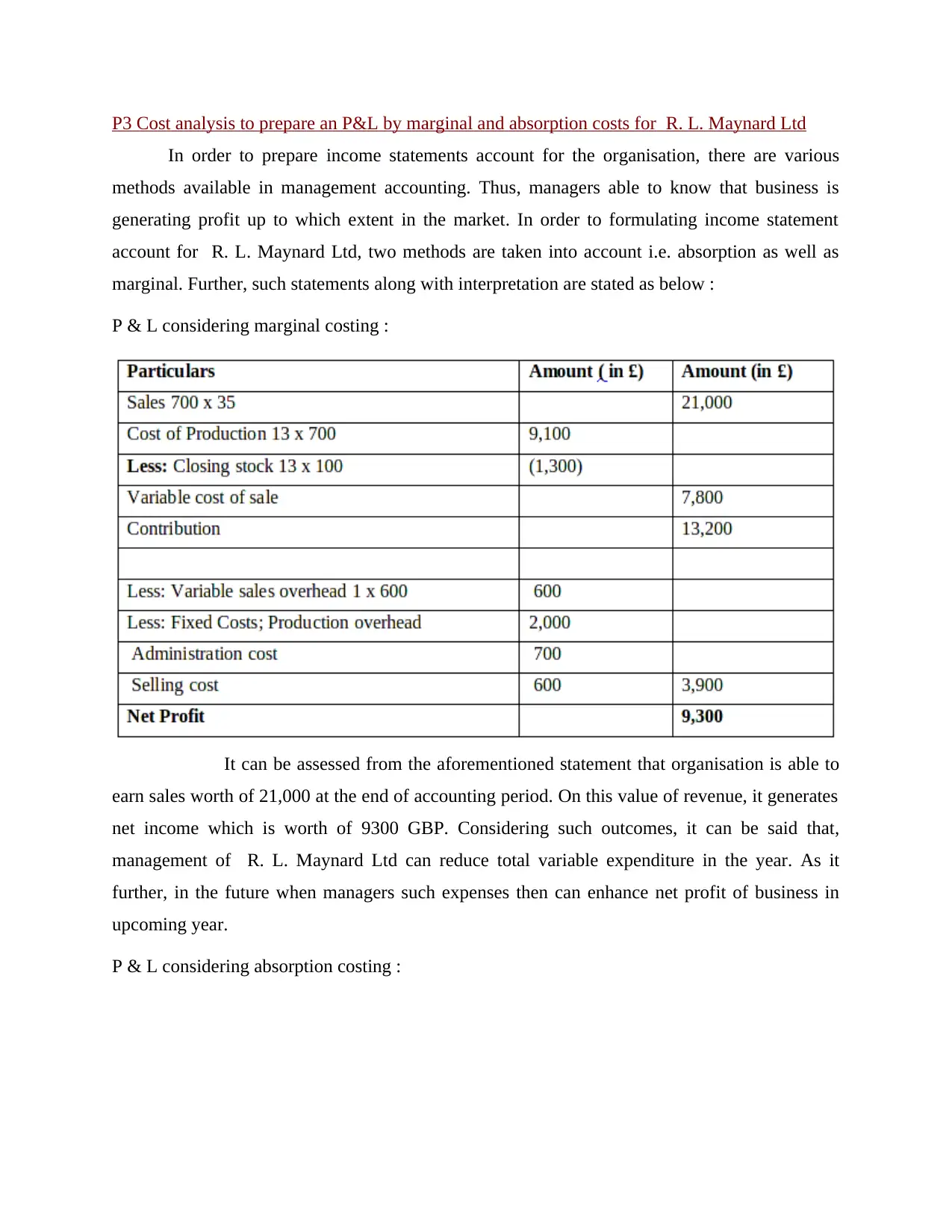

P3 Cost analysis to prepare an P&L by marginal and absorption costs for R. L. Maynard Ltd

In order to prepare income statements account for the organisation, there are various

methods available in management accounting. Thus, managers able to know that business is

generating profit up to which extent in the market. In order to formulating income statement

account for R. L. Maynard Ltd, two methods are taken into account i.e. absorption as well as

marginal. Further, such statements along with interpretation are stated as below :

P & L considering marginal costing :

It can be assessed from the aforementioned statement that organisation is able to

earn sales worth of 21,000 at the end of accounting period. On this value of revenue, it generates

net income which is worth of 9300 GBP. Considering such outcomes, it can be said that,

management of R. L. Maynard Ltd can reduce total variable expenditure in the year. As it

further, in the future when managers such expenses then can enhance net profit of business in

upcoming year.

P & L considering absorption costing :

In order to prepare income statements account for the organisation, there are various

methods available in management accounting. Thus, managers able to know that business is

generating profit up to which extent in the market. In order to formulating income statement

account for R. L. Maynard Ltd, two methods are taken into account i.e. absorption as well as

marginal. Further, such statements along with interpretation are stated as below :

P & L considering marginal costing :

It can be assessed from the aforementioned statement that organisation is able to

earn sales worth of 21,000 at the end of accounting period. On this value of revenue, it generates

net income which is worth of 9300 GBP. Considering such outcomes, it can be said that,

management of R. L. Maynard Ltd can reduce total variable expenditure in the year. As it

further, in the future when managers such expenses then can enhance net profit of business in

upcoming year.

P & L considering absorption costing :

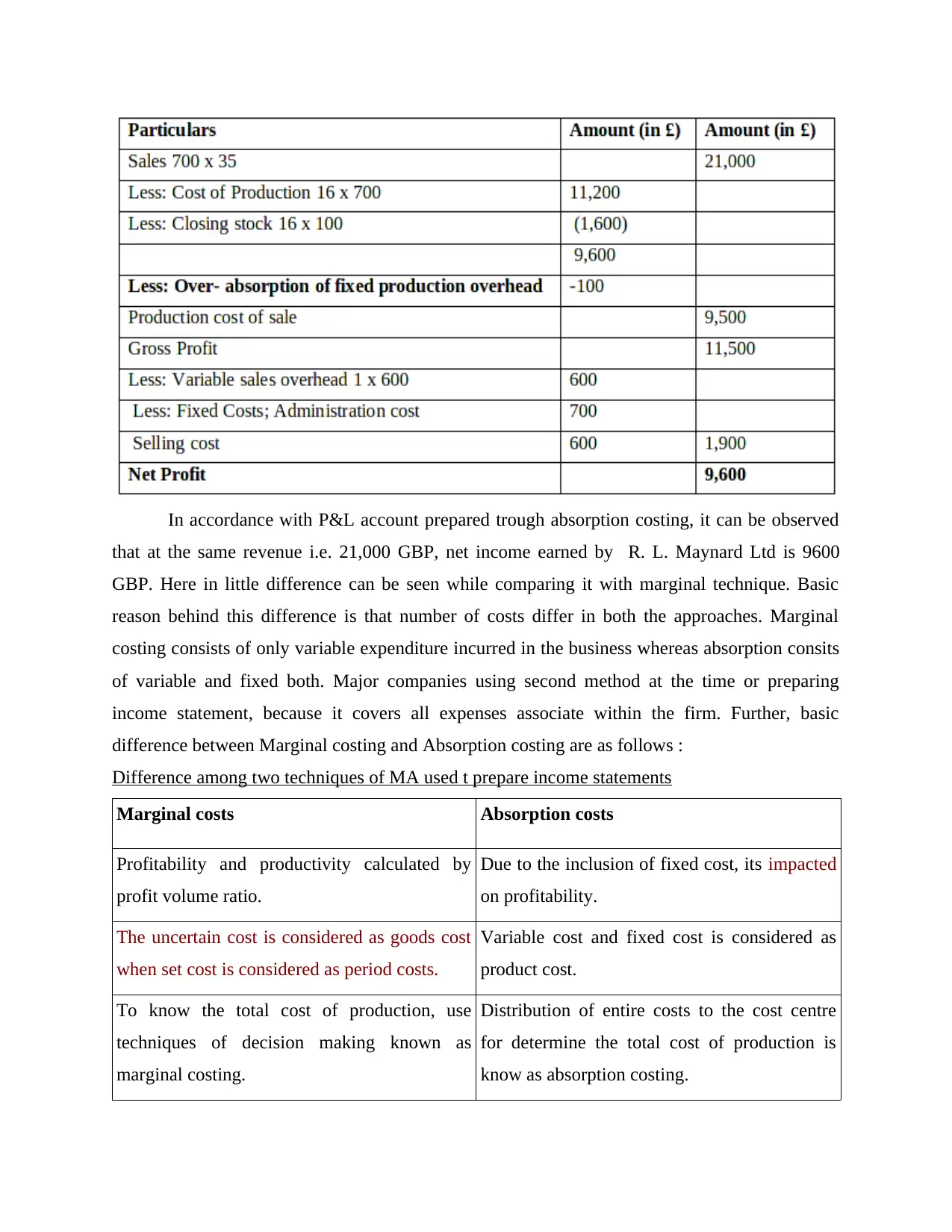

In accordance with P&L account prepared trough absorption costing, it can be observed

that at the same revenue i.e. 21,000 GBP, net income earned by R. L. Maynard Ltd is 9600

GBP. Here in little difference can be seen while comparing it with marginal technique. Basic

reason behind this difference is that number of costs differ in both the approaches. Marginal

costing consists of only variable expenditure incurred in the business whereas absorption consits

of variable and fixed both. Major companies using second method at the time or preparing

income statement, because it covers all expenses associate within the firm. Further, basic

difference between Marginal costing and Absorption costing are as follows :

Difference among two techniques of MA used t prepare income statements

Marginal costs Absorption costs

Profitability and productivity calculated by

profit volume ratio.

Due to the inclusion of fixed cost, its impacted

on profitability.

The uncertain cost is considered as goods cost

when set cost is considered as period costs.

Variable cost and fixed cost is considered as

product cost.

To know the total cost of production, use

techniques of decision making known as

marginal costing.

Distribution of entire costs to the cost centre

for determine the total cost of production is

know as absorption costing.

that at the same revenue i.e. 21,000 GBP, net income earned by R. L. Maynard Ltd is 9600

GBP. Here in little difference can be seen while comparing it with marginal technique. Basic

reason behind this difference is that number of costs differ in both the approaches. Marginal

costing consists of only variable expenditure incurred in the business whereas absorption consits

of variable and fixed both. Major companies using second method at the time or preparing

income statement, because it covers all expenses associate within the firm. Further, basic

difference between Marginal costing and Absorption costing are as follows :

Difference among two techniques of MA used t prepare income statements

Marginal costs Absorption costs

Profitability and productivity calculated by

profit volume ratio.

Due to the inclusion of fixed cost, its impacted

on profitability.

The uncertain cost is considered as goods cost

when set cost is considered as period costs.

Variable cost and fixed cost is considered as

product cost.

To know the total cost of production, use

techniques of decision making known as

marginal costing.

Distribution of entire costs to the cost centre

for determine the total cost of production is

know as absorption costing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

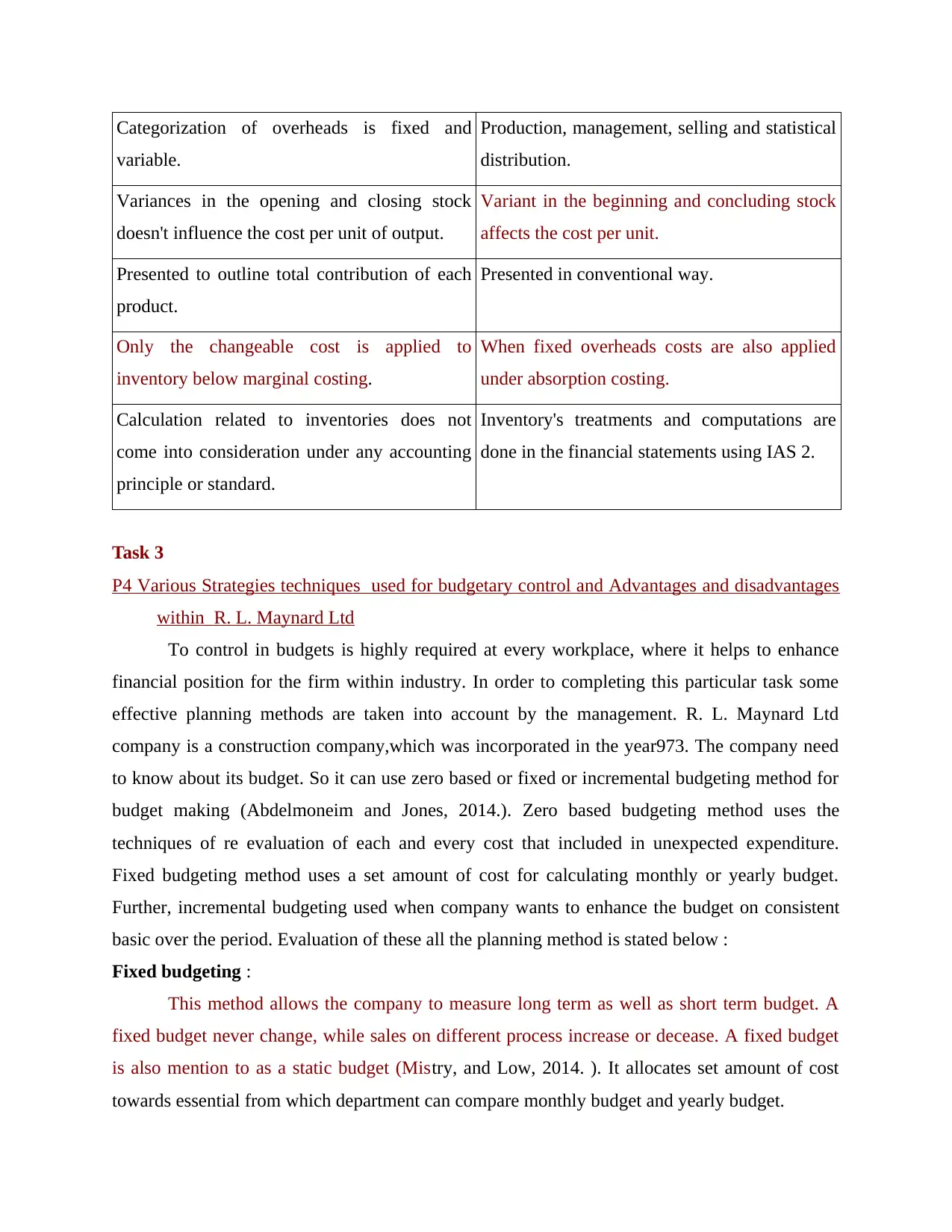

Categorization of overheads is fixed and

variable.

Production, management, selling and statistical

distribution.

Variances in the opening and closing stock

doesn't influence the cost per unit of output.

Variant in the beginning and concluding stock

affects the cost per unit.

Presented to outline total contribution of each

product.

Presented in conventional way.

Only the changeable cost is applied to

inventory below marginal costing.

When fixed overheads costs are also applied

under absorption costing.

Calculation related to inventories does not

come into consideration under any accounting

principle or standard.

Inventory's treatments and computations are

done in the financial statements using IAS 2.

Task 3

P4 Various Strategies techniques used for budgetary control and Advantages and disadvantages

within R. L. Maynard Ltd

To control in budgets is highly required at every workplace, where it helps to enhance

financial position for the firm within industry. In order to completing this particular task some

effective planning methods are taken into account by the management. R. L. Maynard Ltd

company is a construction company,which was incorporated in the year973. The company need

to know about its budget. So it can use zero based or fixed or incremental budgeting method for

budget making (Abdelmoneim and Jones, 2014.). Zero based budgeting method uses the

techniques of re evaluation of each and every cost that included in unexpected expenditure.

Fixed budgeting method uses a set amount of cost for calculating monthly or yearly budget.

Further, incremental budgeting used when company wants to enhance the budget on consistent

basic over the period. Evaluation of these all the planning method is stated below :

Fixed budgeting :

This method allows the company to measure long term as well as short term budget. A

fixed budget never change, while sales on different process increase or decease. A fixed budget

is also mention to as a static budget (Mistry, and Low, 2014. ). It allocates set amount of cost

towards essential from which department can compare monthly budget and yearly budget.

variable.

Production, management, selling and statistical

distribution.

Variances in the opening and closing stock

doesn't influence the cost per unit of output.

Variant in the beginning and concluding stock

affects the cost per unit.

Presented to outline total contribution of each

product.

Presented in conventional way.

Only the changeable cost is applied to

inventory below marginal costing.

When fixed overheads costs are also applied

under absorption costing.

Calculation related to inventories does not

come into consideration under any accounting

principle or standard.

Inventory's treatments and computations are

done in the financial statements using IAS 2.

Task 3

P4 Various Strategies techniques used for budgetary control and Advantages and disadvantages

within R. L. Maynard Ltd

To control in budgets is highly required at every workplace, where it helps to enhance

financial position for the firm within industry. In order to completing this particular task some

effective planning methods are taken into account by the management. R. L. Maynard Ltd

company is a construction company,which was incorporated in the year973. The company need

to know about its budget. So it can use zero based or fixed or incremental budgeting method for

budget making (Abdelmoneim and Jones, 2014.). Zero based budgeting method uses the

techniques of re evaluation of each and every cost that included in unexpected expenditure.

Fixed budgeting method uses a set amount of cost for calculating monthly or yearly budget.

Further, incremental budgeting used when company wants to enhance the budget on consistent

basic over the period. Evaluation of these all the planning method is stated below :

Fixed budgeting :

This method allows the company to measure long term as well as short term budget. A

fixed budget never change, while sales on different process increase or decease. A fixed budget

is also mention to as a static budget (Mistry, and Low, 2014. ). It allocates set amount of cost

towards essential from which department can compare monthly budget and yearly budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages and disadvantage :

One of the most important advantage of the fixed budget is that it's a very easiest to

follow and implement, because it don't require to be updated on regular basis. One of the

major disadvantage of fix budget is its lot of flexibility. If company expand a budget

based on sales level and that level increases. It can not allocate addition resources to keep

up (Mack, and Goretzki, 2017).

This method helps to survive the business to make same position at all financial levels.

AS costs go down in the firm then R. L. Maynard Ltd will become to generate more

profit at the end of year. Disadvantage of this method is not accurate as compared to zero

budgeting method. It is based on a set amount of cost which is not calculated by the R. L.

Maynard Ltd.

Incremental budgeting :

In order to prepare budget using this method, base of previous is taken into consideration.

Further, increment in values like sales, profit, costs is done while formulating the budget

statement. After that sales and profit enhance with high rate whereas cost improve with low rate.

Advantages and disadvantage :

This type of method of budgeting is very easy and simple as well as to understand by

financial and non financial both kinds of employees. After that it is helpful to make

comparison with previous year's budget and assess performance properly. As its

simplicity in understand, but it has major limitation which is related to generating

incentives. Through this employee can not be motivate for their work and can not be able

to give their best at workplace.

Incremental budgeting is valuable for the organisations where funding requirement are

usually fixed. Disadvantage is when company need the more funding, then they can not

get the funding from the sources.

Task 4

P5 Comparing method through which systems of management accounting used by combating

financial problems

At the time of operating various kinds of problems and challenges faced by the company.

Due to this, they can not complete all the activities in proper way and unable to fulfil desired

aims as well as objectives (Otley, 2015.).

One of the most important advantage of the fixed budget is that it's a very easiest to

follow and implement, because it don't require to be updated on regular basis. One of the

major disadvantage of fix budget is its lot of flexibility. If company expand a budget

based on sales level and that level increases. It can not allocate addition resources to keep

up (Mack, and Goretzki, 2017).

This method helps to survive the business to make same position at all financial levels.

AS costs go down in the firm then R. L. Maynard Ltd will become to generate more

profit at the end of year. Disadvantage of this method is not accurate as compared to zero

budgeting method. It is based on a set amount of cost which is not calculated by the R. L.

Maynard Ltd.

Incremental budgeting :

In order to prepare budget using this method, base of previous is taken into consideration.

Further, increment in values like sales, profit, costs is done while formulating the budget

statement. After that sales and profit enhance with high rate whereas cost improve with low rate.

Advantages and disadvantage :

This type of method of budgeting is very easy and simple as well as to understand by

financial and non financial both kinds of employees. After that it is helpful to make

comparison with previous year's budget and assess performance properly. As its

simplicity in understand, but it has major limitation which is related to generating

incentives. Through this employee can not be motivate for their work and can not be able

to give their best at workplace.

Incremental budgeting is valuable for the organisations where funding requirement are

usually fixed. Disadvantage is when company need the more funding, then they can not

get the funding from the sources.

Task 4

P5 Comparing method through which systems of management accounting used by combating

financial problems

At the time of operating various kinds of problems and challenges faced by the company.

Due to this, they can not complete all the activities in proper way and unable to fulfil desired

aims as well as objectives (Otley, 2015.).

Balanced scorecard : As approach which is used to analyse business performance only is referred

as balanced scorecard (Datta, 2016). It consists of basic four kinds of perspectives which include

customer, financial. learning and growth as well as internal business process (Fullerton, and

Widener, 2013). When company required more fund for expand the business, them one of the

major problem is fund, because arrangement of fund, it is not easy processing the market. At this

specific kind of report, financial perspective is taken into account where R. L. Maynard Ltd can

analyse efficiency and productivity against to financial resources allocated.

Financial governance : It is very small proportion of corporate governance which takes care of

the financial resources (Segun, and Olamide, 2015) . Apart from this, utilisation of such

resources at the workplace is also evaluated by this particular method. It is highly supportive

tactic to assess issues come into consideration in the company. Once resources of financial

allocated to the departments then financial governance evaluate efficiency against to this. So

that, R. L. Maynard Ltd can prepare as well as apply strategies accordingly in the working

environment (Bebbington, and O'Dwyer, 2014).

Conclusion

From the above report, can be articulated that management accounting has one of the

important roles at workplace of any organisation. Reason is that it helps to prepare financial

plans where company is able to become more financially sound in respective industry. Basic

systems of management accounting uses to make internal decisions are like job costing, stock

management, process optimisation as well as the cost accounting. Apart from this, for

completing process of management accounting reporting, some methods are used by R. L.

Maynard Ltd like performance, segmental or departmental, operation budget, inventory and

accounts receivables ageing report.

as balanced scorecard (Datta, 2016). It consists of basic four kinds of perspectives which include

customer, financial. learning and growth as well as internal business process (Fullerton, and

Widener, 2013). When company required more fund for expand the business, them one of the

major problem is fund, because arrangement of fund, it is not easy processing the market. At this

specific kind of report, financial perspective is taken into account where R. L. Maynard Ltd can

analyse efficiency and productivity against to financial resources allocated.

Financial governance : It is very small proportion of corporate governance which takes care of

the financial resources (Segun, and Olamide, 2015) . Apart from this, utilisation of such

resources at the workplace is also evaluated by this particular method. It is highly supportive

tactic to assess issues come into consideration in the company. Once resources of financial

allocated to the departments then financial governance evaluate efficiency against to this. So

that, R. L. Maynard Ltd can prepare as well as apply strategies accordingly in the working

environment (Bebbington, and O'Dwyer, 2014).

Conclusion

From the above report, can be articulated that management accounting has one of the

important roles at workplace of any organisation. Reason is that it helps to prepare financial

plans where company is able to become more financially sound in respective industry. Basic

systems of management accounting uses to make internal decisions are like job costing, stock

management, process optimisation as well as the cost accounting. Apart from this, for

completing process of management accounting reporting, some methods are used by R. L.

Maynard Ltd like performance, segmental or departmental, operation budget, inventory and

accounts receivables ageing report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.