Comprehensive Management Accounting Report: Jacksons Fencing

VerifiedAdded on 2021/02/20

|18

|3900

|97

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Jacksons Fencing, a medium-scale manufacturing company. It begins by defining management accounting and its importance in decision-making, cost management, and financial planning. The report covers various reporting methods, including balance sheets, income statements, and cash flow statements, and demonstrates the use of marginal and absorption costing for income statement preparation. It also explores different planning tools, such as budgeting, and their advantages and disadvantages. Furthermore, the report addresses how management accounting can be used to resolve financial problems, such as budget variances and controlling business activities. The analysis includes cost card examples, profit statements using marginal and absorption costing, and a discussion of cost volume analysis. The report concludes with a summary of the key findings and their implications for the company's financial performance and strategic planning.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management accounting and their requirement.....................................................................3

P2 Various methods for report the management accounting......................................................4

LO 2.................................................................................................................................................5

P3 Using marginal and absorption cost for income statements..................................................5

LO 3...............................................................................................................................................10

P4 Different planning tools and their advantages and disadvantages.......................................10

LO 4 ..............................................................................................................................................13

P5 Adopting management accounting to resolve the financial problems.................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management accounting and their requirement.....................................................................3

P2 Various methods for report the management accounting......................................................4

LO 2.................................................................................................................................................5

P3 Using marginal and absorption cost for income statements..................................................5

LO 3...............................................................................................................................................10

P4 Different planning tools and their advantages and disadvantages.......................................10

LO 4 ..............................................................................................................................................13

P5 Adopting management accounting to resolve the financial problems.................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is used to present data in proper format through the various

methods and tools to provide the information to the management for taking efficient decisions in

business unit. Jacksons Fencing is a medium scale manufacturing company. They started their

business by selling chestnut stakes and sale agriculture fencing to the local farmers. They also

sale timber security fence to their customer. The report highlights the requirement of

management accounting in the organization and their importance in calculating the profit of the

organization and managing the cost. It also explains the different methods of reporting like

balance sheet, income statements, cash flow etc. It demonstrates the purpose of various cost to

prepare the income statement of the company like absorption and marginal cost. It also explains

the pros and cons of different planning tools. The report also help to resolve the financial

problems like variances in the budget, control the business activity etc.

LO 1

P1 Management accounting and their requirement

Management accounting :

It is the process of presenting data in useful manner which provide the information to top

management for taking decisions and formulate the policy and procedure for the company. The

component are managing the risk, performance and strategy in the business organization.

Key function of management accounting system

Providing data and information : Planning is the process of formulating long term and

short term plan for achieving the organization objective. Management accounting system

function is to provide the useful data and information for decision-making process (Kaplan, and

Atkinson, 2015). Jacksons Fencing manufacture company use the data and information to

improve their productivity and profitability and make proper plan to accomplish the process.

They provide the information regarding their agriculture fencing product to their customer.

Organizing : Organizing is the process of assigning roles and responsibility to the

managers and employees for accomplish the business goal and target. Management accounting

help the Jacksons Fencing company by providing the report and useful information to control the

activity of the managers and assigning responsibility according to their efficiency. For example

Jacksons Fencing company use the information and organize them in proper format like balance

sheet, income statement to get the true profit of the company.

3

Management accounting is used to present data in proper format through the various

methods and tools to provide the information to the management for taking efficient decisions in

business unit. Jacksons Fencing is a medium scale manufacturing company. They started their

business by selling chestnut stakes and sale agriculture fencing to the local farmers. They also

sale timber security fence to their customer. The report highlights the requirement of

management accounting in the organization and their importance in calculating the profit of the

organization and managing the cost. It also explains the different methods of reporting like

balance sheet, income statements, cash flow etc. It demonstrates the purpose of various cost to

prepare the income statement of the company like absorption and marginal cost. It also explains

the pros and cons of different planning tools. The report also help to resolve the financial

problems like variances in the budget, control the business activity etc.

LO 1

P1 Management accounting and their requirement

Management accounting :

It is the process of presenting data in useful manner which provide the information to top

management for taking decisions and formulate the policy and procedure for the company. The

component are managing the risk, performance and strategy in the business organization.

Key function of management accounting system

Providing data and information : Planning is the process of formulating long term and

short term plan for achieving the organization objective. Management accounting system

function is to provide the useful data and information for decision-making process (Kaplan, and

Atkinson, 2015). Jacksons Fencing manufacture company use the data and information to

improve their productivity and profitability and make proper plan to accomplish the process.

They provide the information regarding their agriculture fencing product to their customer.

Organizing : Organizing is the process of assigning roles and responsibility to the

managers and employees for accomplish the business goal and target. Management accounting

help the Jacksons Fencing company by providing the report and useful information to control the

activity of the managers and assigning responsibility according to their efficiency. For example

Jacksons Fencing company use the information and organize them in proper format like balance

sheet, income statement to get the true profit of the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysing : Controlling refers to monitor, evaluate and analyse productivity of business

unit and take effective measures for improving the performance (Renz, 2016). It provides the

useful data to calculate the differences between the standard and actual output and analyse the

different activities to find the reason behind the variances and manage them to get the higher

profitability and productivity in the market.

Communication : It works as a link between the management and employees by

providing information to different department and evaluate the department to control their

activities and improve their performance. For example Jacksons Fencing company use the

management accounting to communicate their decisions with the managers and employees to

integrate their work in same direction.

Different accounting system

Cost accounting : Cost accounting is help to evaluate the price of the products and

services of manufacturing business. The correct cost of the product support the firm to produce

the goods which gives the maximum return with minimum cost (Maas, Schaltegger, and Crutzen,

2016). Activity based costing in the Jacksons Fencing help to assign more logically the

manufacturing overhead cost of the product (Cost Accounting Systems, 2013).

Financial accounting : It is used to keep records of financial information and present

them in different statements like balance sheet, income statement and cash flow statement to

aware investor and customer about the financial position of the business organization. Jackson

fencing company use the financial accounting system to control the information and data. It

helps the company to audit the financial statements like cash flow, Income statement to get the

true data and present the fair position to the customer and stakeholders and control the internal

activity like management functions, manufacturing process etc.

Management accounting : It is used to produce information for taking decisions and

control the company activity by evaluating the variances in comparison of actual and expected

cost (Management Accounting – Meaning, Advantages & Functions, 2018).

P2 Various methods for report the management accounting

Management accounting works as a tool for understanding the data and interpret them

through different reports like financial reports, cash flow, revenue report, product cost report etc.

in organization.

Purpose and uses of reporting tools

4

unit and take effective measures for improving the performance (Renz, 2016). It provides the

useful data to calculate the differences between the standard and actual output and analyse the

different activities to find the reason behind the variances and manage them to get the higher

profitability and productivity in the market.

Communication : It works as a link between the management and employees by

providing information to different department and evaluate the department to control their

activities and improve their performance. For example Jacksons Fencing company use the

management accounting to communicate their decisions with the managers and employees to

integrate their work in same direction.

Different accounting system

Cost accounting : Cost accounting is help to evaluate the price of the products and

services of manufacturing business. The correct cost of the product support the firm to produce

the goods which gives the maximum return with minimum cost (Maas, Schaltegger, and Crutzen,

2016). Activity based costing in the Jacksons Fencing help to assign more logically the

manufacturing overhead cost of the product (Cost Accounting Systems, 2013).

Financial accounting : It is used to keep records of financial information and present

them in different statements like balance sheet, income statement and cash flow statement to

aware investor and customer about the financial position of the business organization. Jackson

fencing company use the financial accounting system to control the information and data. It

helps the company to audit the financial statements like cash flow, Income statement to get the

true data and present the fair position to the customer and stakeholders and control the internal

activity like management functions, manufacturing process etc.

Management accounting : It is used to produce information for taking decisions and

control the company activity by evaluating the variances in comparison of actual and expected

cost (Management Accounting – Meaning, Advantages & Functions, 2018).

P2 Various methods for report the management accounting

Management accounting works as a tool for understanding the data and interpret them

through different reports like financial reports, cash flow, revenue report, product cost report etc.

in organization.

Purpose and uses of reporting tools

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trading and profit and loss account : The purpose of using these account is the present

all operating and non operating income and expenses of the organization and calculate the profit

of the business for different organizational function. It is used by the Jacksons Fencing company

to present their financial data and activity in systematic manner to get the useful information

from the data and used in decision, policy and procedure making process. It also used to

communicate the financial position to the stakeholders, suppliers and owner, so they can improve

their performance and manage the activities in better way.

Balance sheet : Balance sheets of the organization represent the assets and liability to its

stakeholder (Pavlatos, and Kostakis, 2015). The motive of preparing balance sheet statement in

the organization is for attracting the customer and investor toward the organization by presenting

the true position of company in market. Jacksons Fencing company use the balance sheet to

present the cash and assets of the business in market.

Cash flow statement : This statement is used to analysis real inflow and outflow of the

cash. The motive of the statement is to measure the cash and non cash activity and find the total

cash transaction in the company. It was used by the Jacksons Fencing company to control the

day to day activity and manage the cash flow in the organization.

Stock management system : Inventory management system is support to manage the

inventory level within the company by regulating the stock level in warehouses, order level, sales

receipts etc. For example inventory management system help the Jacksons Fencing company to

manage the timber level in the warehouses and fulfilling the demand of the customer in the

market (Lopez-Valeiras, Gomez-Conde, and Naranjo-Gil, 2015).

Price optimizing system : This system is used to evaluate the customer behaviour

towards the cost of the goods and services and determine the price of product to enhance and

regulate profit of the organization. For example : Jacksons fencing company use the system to set

the price of the product to get maximum profit.

LO 2

P3 Using marginal and absorption cost for income statements

Marginal cost : marginal cost refers to the change in unit of production to increase a

decrease in additional unit.

Absorption cost : It indicates that cost of the product include the various cost like direct

material, labour, overhead, fixed cost etc.

5

all operating and non operating income and expenses of the organization and calculate the profit

of the business for different organizational function. It is used by the Jacksons Fencing company

to present their financial data and activity in systematic manner to get the useful information

from the data and used in decision, policy and procedure making process. It also used to

communicate the financial position to the stakeholders, suppliers and owner, so they can improve

their performance and manage the activities in better way.

Balance sheet : Balance sheets of the organization represent the assets and liability to its

stakeholder (Pavlatos, and Kostakis, 2015). The motive of preparing balance sheet statement in

the organization is for attracting the customer and investor toward the organization by presenting

the true position of company in market. Jacksons Fencing company use the balance sheet to

present the cash and assets of the business in market.

Cash flow statement : This statement is used to analysis real inflow and outflow of the

cash. The motive of the statement is to measure the cash and non cash activity and find the total

cash transaction in the company. It was used by the Jacksons Fencing company to control the

day to day activity and manage the cash flow in the organization.

Stock management system : Inventory management system is support to manage the

inventory level within the company by regulating the stock level in warehouses, order level, sales

receipts etc. For example inventory management system help the Jacksons Fencing company to

manage the timber level in the warehouses and fulfilling the demand of the customer in the

market (Lopez-Valeiras, Gomez-Conde, and Naranjo-Gil, 2015).

Price optimizing system : This system is used to evaluate the customer behaviour

towards the cost of the goods and services and determine the price of product to enhance and

regulate profit of the organization. For example : Jacksons fencing company use the system to set

the price of the product to get maximum profit.

LO 2

P3 Using marginal and absorption cost for income statements

Marginal cost : marginal cost refers to the change in unit of production to increase a

decrease in additional unit.

Absorption cost : It indicates that cost of the product include the various cost like direct

material, labour, overhead, fixed cost etc.

5

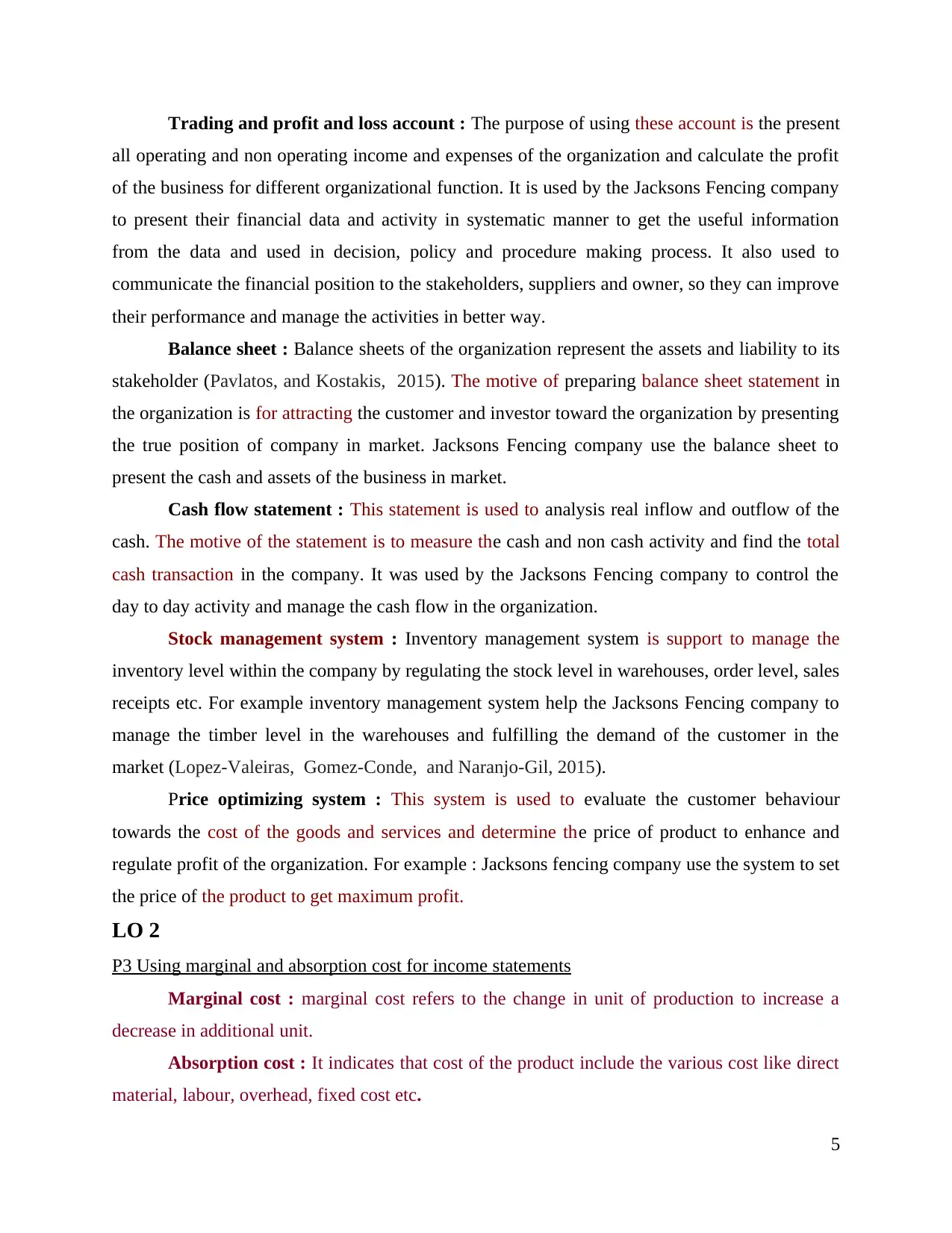

Case 1

Cost card using marginal costing

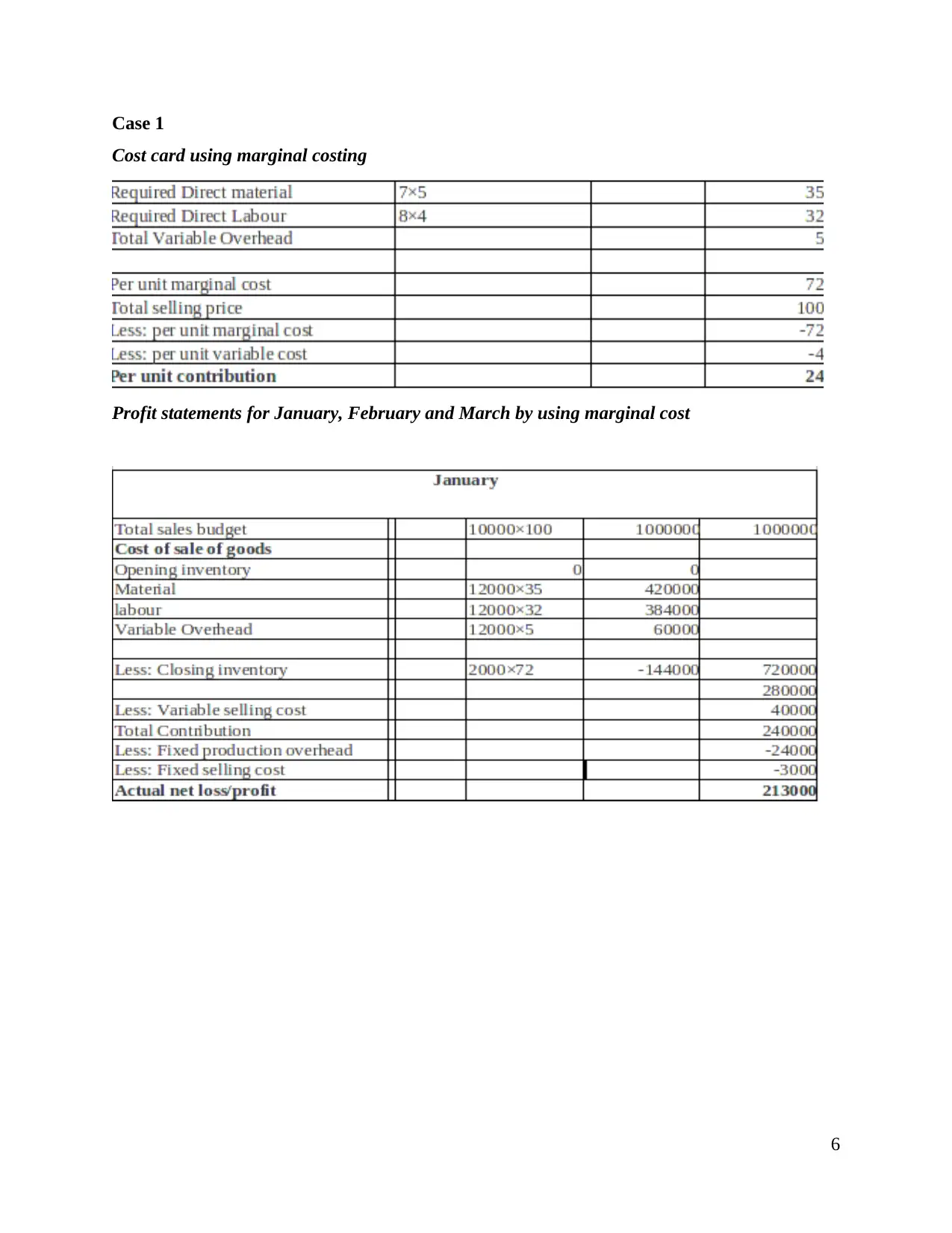

Profit statements for January, February and March by using marginal cost

6

Cost card using marginal costing

Profit statements for January, February and March by using marginal cost

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

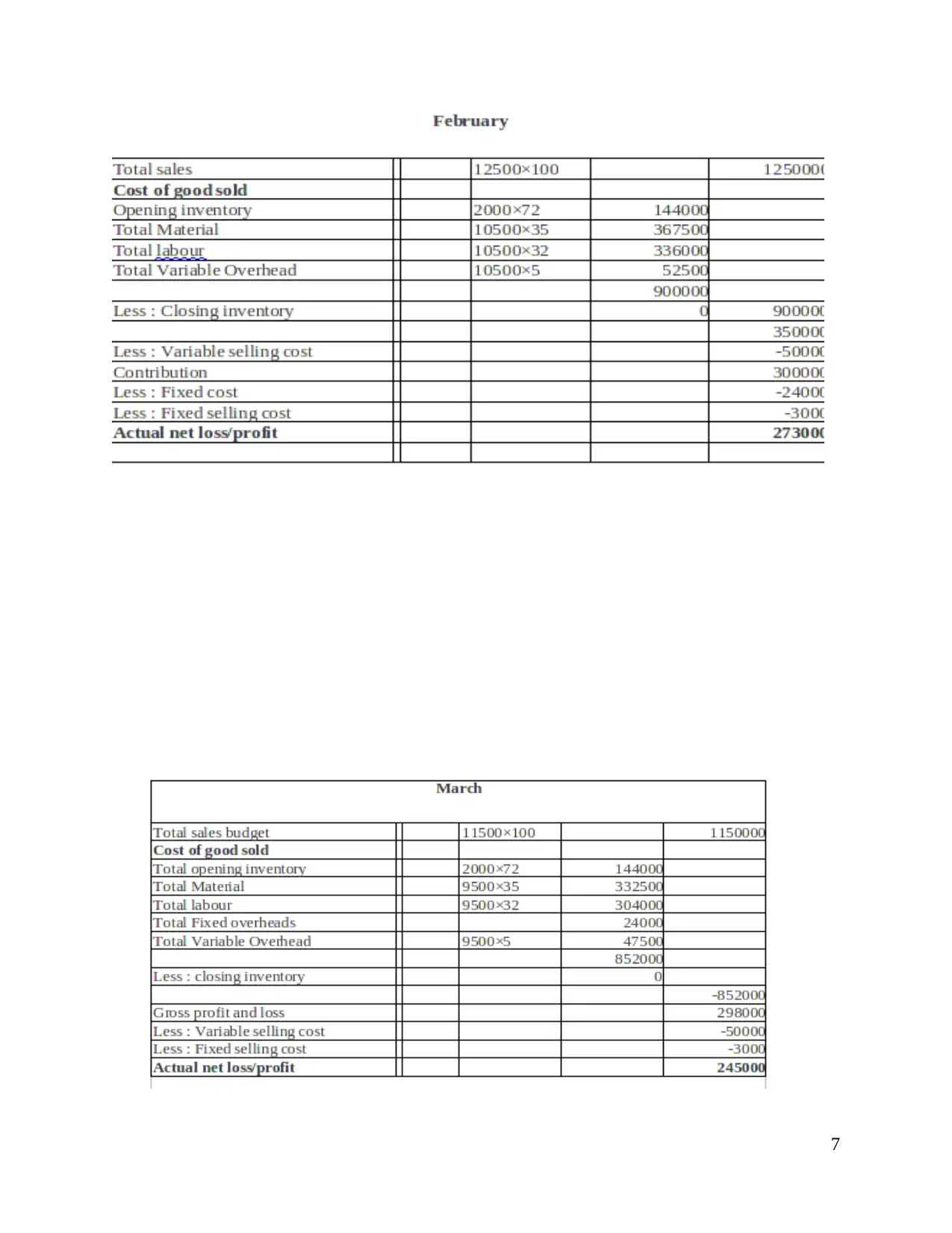

Case 2

Cost card using absorption costing

Required material 7×5 35

Required Labour 8×4 32

Variable Overhead 5

Fixed cost 2

Per unit marginal price 74

Selling price 100

Less : per unit marginal cost -74

Less : per unit variable cost -4

Contribution per unit 22

Profit statements for January, February and March by using absorption cost

January

Budgeted sales 10000×100 1000000

COGS

Opening stock

Labour 12000*32 384000

Material 12000*35 420000

Fixed overheads 24000

Variable Overhead 12000*5 60000

888000

Less : Closing stock 2000*72 144000

744000

Total gross profit and loss 256000

Less : Variable selling cost -40000

Less : Fixed selling cost -3000

Actual net loss/profit 213000

8

Cost card using absorption costing

Required material 7×5 35

Required Labour 8×4 32

Variable Overhead 5

Fixed cost 2

Per unit marginal price 74

Selling price 100

Less : per unit marginal cost -74

Less : per unit variable cost -4

Contribution per unit 22

Profit statements for January, February and March by using absorption cost

January

Budgeted sales 10000×100 1000000

COGS

Opening stock

Labour 12000*32 384000

Material 12000*35 420000

Fixed overheads 24000

Variable Overhead 12000*5 60000

888000

Less : Closing stock 2000*72 144000

744000

Total gross profit and loss 256000

Less : Variable selling cost -40000

Less : Fixed selling cost -3000

Actual net loss/profit 213000

8

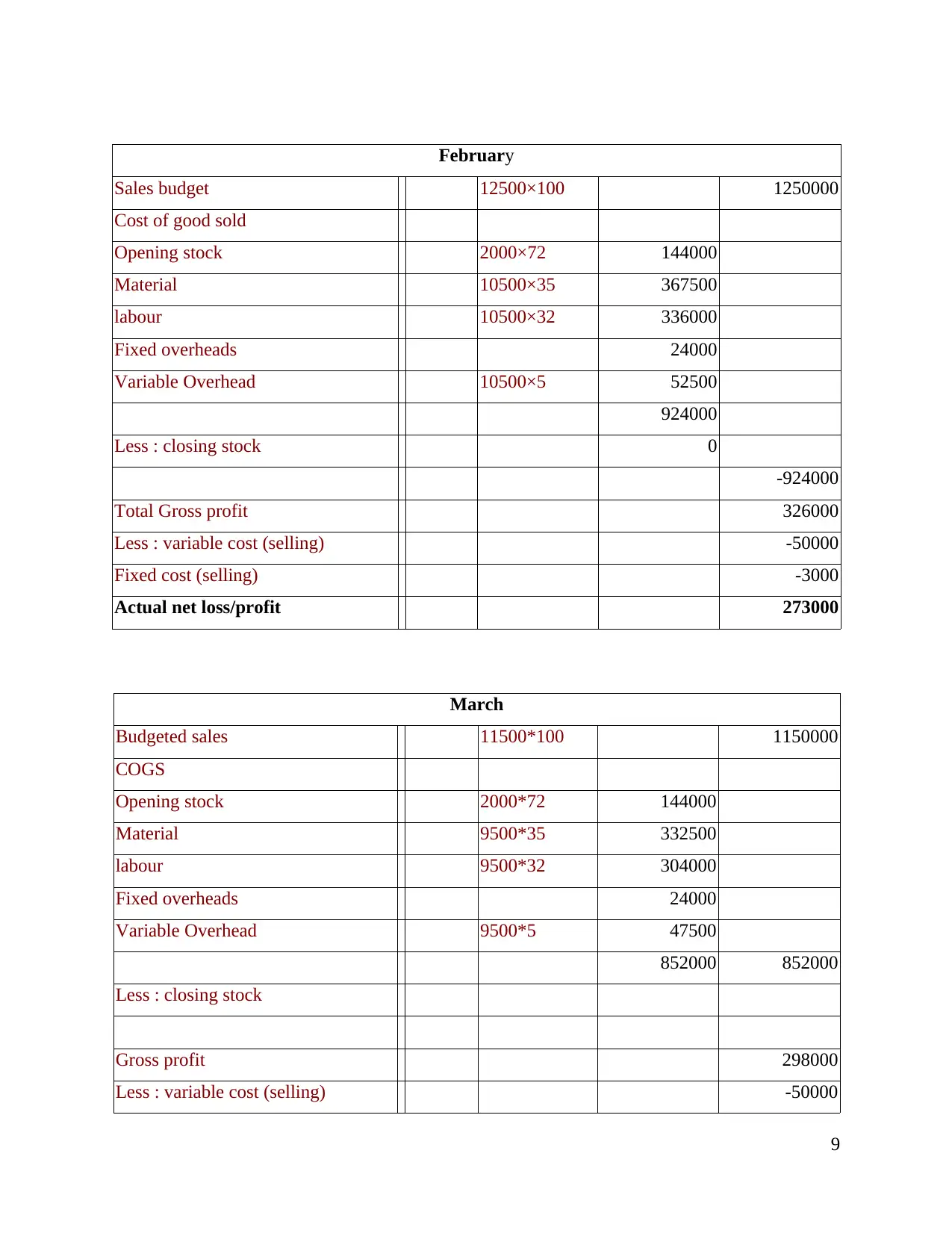

February

Sales budget 12500×100 1250000

Cost of good sold

Opening stock 2000×72 144000

Material 10500×35 367500

labour 10500×32 336000

Fixed overheads 24000

Variable Overhead 10500×5 52500

924000

Less : closing stock 0

-924000

Total Gross profit 326000

Less : variable cost (selling) -50000

Fixed cost (selling) -3000

Actual net loss/profit 273000

March

Budgeted sales 11500*100 1150000

COGS

Opening stock 2000*72 144000

Material 9500*35 332500

labour 9500*32 304000

Fixed overheads 24000

Variable Overhead 9500*5 47500

852000 852000

Less : closing stock

Gross profit 298000

Less : variable cost (selling) -50000

9

Sales budget 12500×100 1250000

Cost of good sold

Opening stock 2000×72 144000

Material 10500×35 367500

labour 10500×32 336000

Fixed overheads 24000

Variable Overhead 10500×5 52500

924000

Less : closing stock 0

-924000

Total Gross profit 326000

Less : variable cost (selling) -50000

Fixed cost (selling) -3000

Actual net loss/profit 273000

March

Budgeted sales 11500*100 1150000

COGS

Opening stock 2000*72 144000

Material 9500*35 332500

labour 9500*32 304000

Fixed overheads 24000

Variable Overhead 9500*5 47500

852000 852000

Less : closing stock

Gross profit 298000

Less : variable cost (selling) -50000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less : Fixed cost (selling) -3000

Actual net loss/profit 245000

Cost : Cost refers to the monetary value which is used by the company to produce or

manufacturing some product or services in their firm. It is used to estimate total benefit on the

charged cost on the product and services. It helps to select the best alternative from the various

choices (Arnaboldi, Lapsley, and Steccolini, 201).

Cost volume analysis is a kind of process used by the business firm to determine the

effect of changing cost and volume on the cost of product and services.

Cost variance refers to the difference in the actual cost and estimated cost of the project

and services. It supports the organization to find the reason behind the variances and improve the

activities to minimize the cost. It includes various factor such as direct material variance,

purchase price variance, labour variance etc.

Fixed cost refers to cost of the product and services which remains constant with the

variation in quantity or result of the product. On the other hand variable cost change with change

in output.

LO 3

P4 Different planning tools and their advantages and disadvantages

Budgeting refers to prepare the plan for the company to spend the amount in efficient

manner, so they can achieve the target within the proper time. There are different types of budget

like operation budget, financial budget, increment budget, cash budget etc.

Operational budget : operational budget is prepared to present the company expected

revenue and associated expenses of the business (Anand, and Grover, 2015). Operating budget

include the various factor such as sales budget, production budget, material purchase, variable

cost etc.

Advantages : it helps the business organization to plan the day to day activity expenses

and evaluate the cost related to the different activities. It keeps the information real, accurate and

present the true position of the firm.

From case 3 & 4 it can be concluded that sales budget help the company to estimate the

various expenses and control the selling expenses to get the favourable variances.

10

Actual net loss/profit 245000

Cost : Cost refers to the monetary value which is used by the company to produce or

manufacturing some product or services in their firm. It is used to estimate total benefit on the

charged cost on the product and services. It helps to select the best alternative from the various

choices (Arnaboldi, Lapsley, and Steccolini, 201).

Cost volume analysis is a kind of process used by the business firm to determine the

effect of changing cost and volume on the cost of product and services.

Cost variance refers to the difference in the actual cost and estimated cost of the project

and services. It supports the organization to find the reason behind the variances and improve the

activities to minimize the cost. It includes various factor such as direct material variance,

purchase price variance, labour variance etc.

Fixed cost refers to cost of the product and services which remains constant with the

variation in quantity or result of the product. On the other hand variable cost change with change

in output.

LO 3

P4 Different planning tools and their advantages and disadvantages

Budgeting refers to prepare the plan for the company to spend the amount in efficient

manner, so they can achieve the target within the proper time. There are different types of budget

like operation budget, financial budget, increment budget, cash budget etc.

Operational budget : operational budget is prepared to present the company expected

revenue and associated expenses of the business (Anand, and Grover, 2015). Operating budget

include the various factor such as sales budget, production budget, material purchase, variable

cost etc.

Advantages : it helps the business organization to plan the day to day activity expenses

and evaluate the cost related to the different activities. It keeps the information real, accurate and

present the true position of the firm.

From case 3 & 4 it can be concluded that sales budget help the company to estimate the

various expenses and control the selling expenses to get the favourable variances.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages : Operating budget record the accurate data but there is high chances of

manipulation of data by the company for their personal benefits.

Zero base budgeting : Process of zero base budgeting start from zero base in which all

expenditure are resulted or calculated for new period.

Advantages : It helps organization to control the operation and events of the different

activities and allocate the resources to the company according to the requirement. It helps to

minimize the wastage of resources in the organization.

Disadvantages : It requires to evaluate the activity from the zero base which creates

problems in implementing the budget in the organization. It also times and cost consuming

activity. In formulating and evaluating the budget large number of problem arise because

manager are not agreed to fix the current level above the minimum level.

Increment budget : In increment budget previous year budget is used as base and in

these base increment amount is added to estimate the new budget for company.

Advantages : It supports the organization to prepare budget effectively and efficiently on

time. Increment budget is easy to make and evaluate the performance of the organization.

Disadvantages : It does not encourage the creativity and innovation in the organization

because it is based on the previous year budget. Increment budget does not show the true

position of the business activity and there are high chances of variances.

Case 3

a) Sales budget

b) Production budget.

Particulars Product EC1 Product EC2 Product EC3

Forecast unit of sales 2000 4000 3000

+ Closing stock 600 1000 800

Production required 2600 5000 3800

- Opening stock 500 800 700

Units to be manufactured 2100 4200 3100

11

manipulation of data by the company for their personal benefits.

Zero base budgeting : Process of zero base budgeting start from zero base in which all

expenditure are resulted or calculated for new period.

Advantages : It helps organization to control the operation and events of the different

activities and allocate the resources to the company according to the requirement. It helps to

minimize the wastage of resources in the organization.

Disadvantages : It requires to evaluate the activity from the zero base which creates

problems in implementing the budget in the organization. It also times and cost consuming

activity. In formulating and evaluating the budget large number of problem arise because

manager are not agreed to fix the current level above the minimum level.

Increment budget : In increment budget previous year budget is used as base and in

these base increment amount is added to estimate the new budget for company.

Advantages : It supports the organization to prepare budget effectively and efficiently on

time. Increment budget is easy to make and evaluate the performance of the organization.

Disadvantages : It does not encourage the creativity and innovation in the organization

because it is based on the previous year budget. Increment budget does not show the true

position of the business activity and there are high chances of variances.

Case 3

a) Sales budget

b) Production budget.

Particulars Product EC1 Product EC2 Product EC3

Forecast unit of sales 2000 4000 3000

+ Closing stock 600 1000 800

Production required 2600 5000 3800

- Opening stock 500 800 700

Units to be manufactured 2100 4200 3100

11

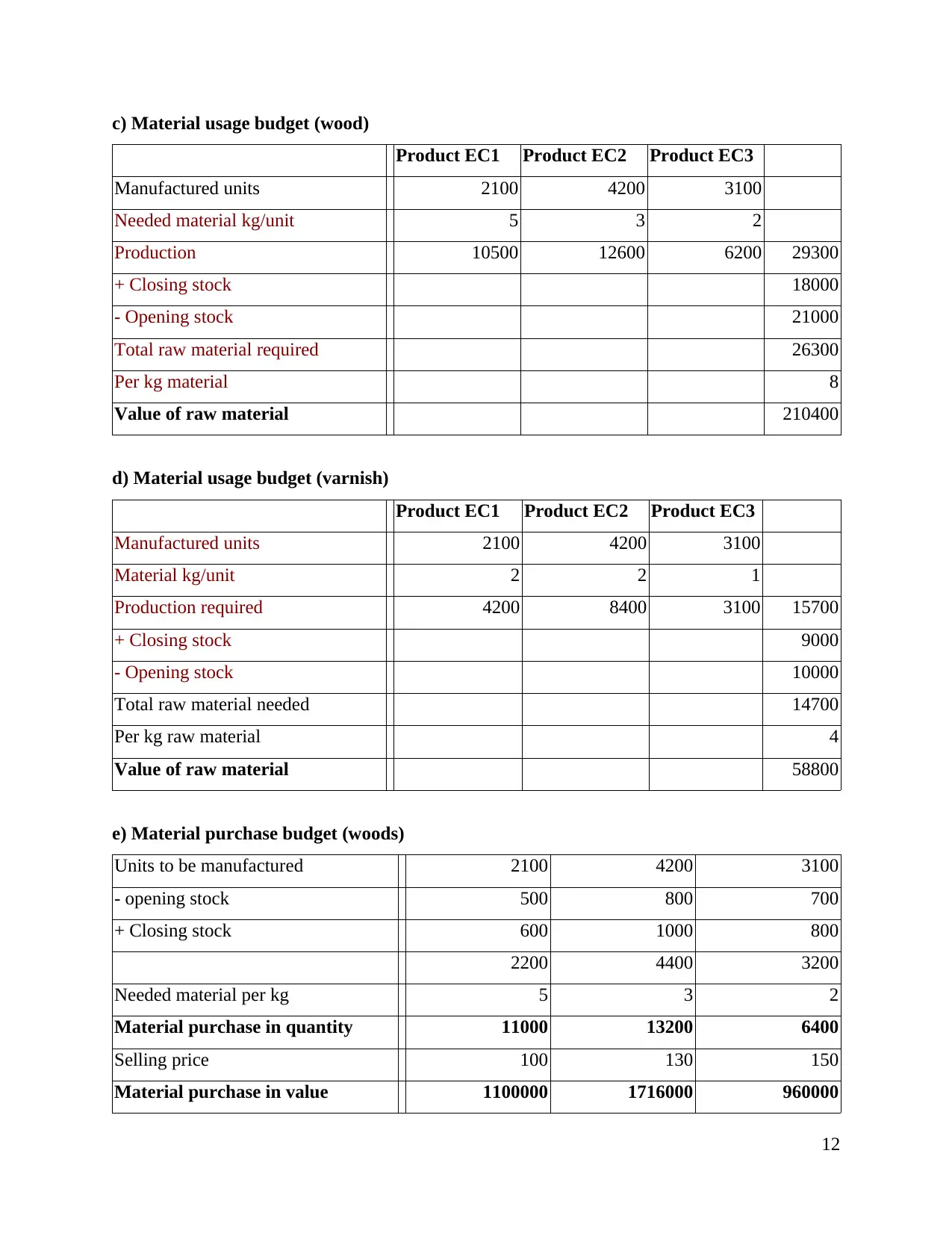

c) Material usage budget (wood)

Product EC1 Product EC2 Product EC3

Manufactured units 2100 4200 3100

Needed material kg/unit 5 3 2

Production 10500 12600 6200 29300

+ Closing stock 18000

- Opening stock 21000

Total raw material required 26300

Per kg material 8

Value of raw material 210400

d) Material usage budget (varnish)

Product EC1 Product EC2 Product EC3

Manufactured units 2100 4200 3100

Material kg/unit 2 2 1

Production required 4200 8400 3100 15700

+ Closing stock 9000

- Opening stock 10000

Total raw material needed 14700

Per kg raw material 4

Value of raw material 58800

e) Material purchase budget (woods)

Units to be manufactured 2100 4200 3100

- opening stock 500 800 700

+ Closing stock 600 1000 800

2200 4400 3200

Needed material per kg 5 3 2

Material purchase in quantity 11000 13200 6400

Selling price 100 130 150

Material purchase in value 1100000 1716000 960000

12

Product EC1 Product EC2 Product EC3

Manufactured units 2100 4200 3100

Needed material kg/unit 5 3 2

Production 10500 12600 6200 29300

+ Closing stock 18000

- Opening stock 21000

Total raw material required 26300

Per kg material 8

Value of raw material 210400

d) Material usage budget (varnish)

Product EC1 Product EC2 Product EC3

Manufactured units 2100 4200 3100

Material kg/unit 2 2 1

Production required 4200 8400 3100 15700

+ Closing stock 9000

- Opening stock 10000

Total raw material needed 14700

Per kg raw material 4

Value of raw material 58800

e) Material purchase budget (woods)

Units to be manufactured 2100 4200 3100

- opening stock 500 800 700

+ Closing stock 600 1000 800

2200 4400 3200

Needed material per kg 5 3 2

Material purchase in quantity 11000 13200 6400

Selling price 100 130 150

Material purchase in value 1100000 1716000 960000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.