Management Accounting Systems and Techniques: Oshodi PLC Report

VerifiedAdded on 2021/02/21

|15

|5059

|468

Report

AI Summary

This report examines management accounting systems and techniques employed by Oshodi PLC, a manufacturing company specializing in JOJO fruit juice. It covers various management accounting systems such as price optimization, job-order costing, inventory management, and cost managerial accounting. The report analyzes different types of management accounting reports including budget reports, performance reports, accounts receivable aging reports, and cost accounting reports. It details the benefits of these systems and reports, and how they are integrated to aid decision-making. The report further includes calculations of net profit using marginal costing, application of various management accounting techniques, and interpretation of financial reports. It also discusses planning tools used for budgetary control, advantages and disadvantages of these tools, and their use in forecasting budgets. Finally, the report explores how management accounting systems are used to resolve financial problems, analyzing how they lead to success. The report concludes with a summary of the key findings and recommendations for Oshodi PLC.

Management accounting

systems and techniques

systems and techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Different types of management accounting systems:.............................................................3

P2 Types of management accounting reports:.............................................................................5

M1 Benefits of management accounting systems:.......................................................................6

D1 Integration of management accounting systems with reporting:...........................................7

TASK 2............................................................................................................................................7

P3 Calculation of net profit with the help of management accounting techniques:....................7

M2 Application of various management accounting techniques:................................................9

D2 Interpretation of financial reports:.........................................................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of planning tools used for budgetary control:.....................10

M3 Use of planning tools for forecasting budgets:....................................................................12

TASK 4..........................................................................................................................................12

P5 Ways in which management accounting systems are used to resolve financial problems:..12

M4 Analysis of how management accounting can lead to attaining success by responding....14

to financial problems:................................................................................................................14

D3 Planning tools used to respond financial problems:.............................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Different types of management accounting systems:.............................................................3

P2 Types of management accounting reports:.............................................................................5

M1 Benefits of management accounting systems:.......................................................................6

D1 Integration of management accounting systems with reporting:...........................................7

TASK 2............................................................................................................................................7

P3 Calculation of net profit with the help of management accounting techniques:....................7

M2 Application of various management accounting techniques:................................................9

D2 Interpretation of financial reports:.........................................................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of planning tools used for budgetary control:.....................10

M3 Use of planning tools for forecasting budgets:....................................................................12

TASK 4..........................................................................................................................................12

P5 Ways in which management accounting systems are used to resolve financial problems:..12

M4 Analysis of how management accounting can lead to attaining success by responding....14

to financial problems:................................................................................................................14

D3 Planning tools used to respond financial problems:.............................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

In today's business environment, every organisation is required to manage its business

activities by preparing financial statements as it helps them to easily analyse the performance of

their company. For this purpose, management accounting is used which is defined as a provision

of both financial and non-financial information for the overall development of an enterprise.

Decision-making is a crucial aspect for every firm and an effective judgement can lead an

organisation to achieve greater heights. In the following report, a management accountant trainee

is selected who works at Oshodi PLC (Management accounting, 2019).

The manufacturing company specialises in the production of JOJO fruit juice across all

age gaps and offers them critical facts about the need of managerial decision-making. This report

highlights on various management accounting systems and reports opted by Oshodi PLC in order

to get clarification of information. It also includes various planning tools to identify and resolve

financial problems that may occur on a day-to-day basis. A calculation of net profit figures is

also done under this statement with the help of management accounting techniques.

TASK 1

P1 Different types of management accounting systems:

Management accounting: This refers to a practice where both financial and non-

financial information is identified, measured, analysed, interpreted & communicated among the

higher authorities for the pursuit of organisational goals & objectives. Its scope is quite wide and

varies among the three areas i.e. strategic, performance and risk management. It is required by

Oshodi PLC to analyse business cost & operations for preparation of reports or records which

aids the directors in taking valuable decisions for the welfare of company (Abdelhak, Grostick

and Hanken, 2014).

Management accounting systems: These generally consists of internal systems which

are used by an organisation to measure and evaluate its processes for the overall development of

a firm. Usually, this is required among the members of Oshodi PLC to produce goods as per the

need & requirement of the customer in order to get maximise consumer satisfaction. The

company also uses management accounting systems by providing accurate, timely, complete

data to the customers.

In today's business environment, every organisation is required to manage its business

activities by preparing financial statements as it helps them to easily analyse the performance of

their company. For this purpose, management accounting is used which is defined as a provision

of both financial and non-financial information for the overall development of an enterprise.

Decision-making is a crucial aspect for every firm and an effective judgement can lead an

organisation to achieve greater heights. In the following report, a management accountant trainee

is selected who works at Oshodi PLC (Management accounting, 2019).

The manufacturing company specialises in the production of JOJO fruit juice across all

age gaps and offers them critical facts about the need of managerial decision-making. This report

highlights on various management accounting systems and reports opted by Oshodi PLC in order

to get clarification of information. It also includes various planning tools to identify and resolve

financial problems that may occur on a day-to-day basis. A calculation of net profit figures is

also done under this statement with the help of management accounting techniques.

TASK 1

P1 Different types of management accounting systems:

Management accounting: This refers to a practice where both financial and non-

financial information is identified, measured, analysed, interpreted & communicated among the

higher authorities for the pursuit of organisational goals & objectives. Its scope is quite wide and

varies among the three areas i.e. strategic, performance and risk management. It is required by

Oshodi PLC to analyse business cost & operations for preparation of reports or records which

aids the directors in taking valuable decisions for the welfare of company (Abdelhak, Grostick

and Hanken, 2014).

Management accounting systems: These generally consists of internal systems which

are used by an organisation to measure and evaluate its processes for the overall development of

a firm. Usually, this is required among the members of Oshodi PLC to produce goods as per the

need & requirement of the customer in order to get maximise consumer satisfaction. The

company also uses management accounting systems by providing accurate, timely, complete

data to the customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimisation system: This refers to a system which is required by companies to set

value of their products & services after assessing need & want of the consumer. It is used as a

tool which does a deep study regarding customer perspective on using the goods. Also, this can

be affected by demand and supply factors as they usually fluctuate with rising or falling

conditions (Berry, Broadbent and Otley, 2016). This is required by management to estimate price

of products offered by rivals and set the cost of goods accordingly. Oshodi PLC uses price

optimisation system to evaluate price of various factors used while manufacturing JOJO fruit

juices like packaging, labelling, branding etc.

Job-order costing system: It is a system which aims at producing goods or services

according to the need & requirement of the user. Usually, all the activities performed under job-

order costing system are related to achievement of goals & objectives of the firm. The orders

placed by customers vary according to their desire, for example, some people can minimise on

the quality of products to get it for cheap however, other would want to get the best quality

products for which they can pay any amount. This technique is followed by directors of Oshodi

PLC to manufacture the production of JOJO fruit juices which can range from adding extra

quantity of product, offering multi packs etc.

Inventory management system: This is a system which ensures that stock is available

at the warehouse whenever in need. It confirms that adequate raw material for producing goods

are present at the right time and accurate place. To value inventory, various methods are opted by

a firm i.e. LIFO, FIFO, weighted average which are mentioned below:

LIFO: Last in, first out method states that the inventory which as arrived at the end is

consumed first.

FIFO: First in, first out method states that the stock which is arrived at the beginning is

consumed first.

Weighted average: This method divides COGS available for sale with the number of

units present during the time of sale.

Oshodi PLC values its inventory by using FIFO to avoid any products from getting

expired so sell those juices which are manufactured first (Braun and et.al., 2014). Usually, every

organisation follows and complies by this system and in this report, Oshodi PLC does the same

in order to maximise the production of JOJO fruit juice. The company ensures that appropriate

material, equipment is used in manufacturing the juice so that the quality is not compromised.

value of their products & services after assessing need & want of the consumer. It is used as a

tool which does a deep study regarding customer perspective on using the goods. Also, this can

be affected by demand and supply factors as they usually fluctuate with rising or falling

conditions (Berry, Broadbent and Otley, 2016). This is required by management to estimate price

of products offered by rivals and set the cost of goods accordingly. Oshodi PLC uses price

optimisation system to evaluate price of various factors used while manufacturing JOJO fruit

juices like packaging, labelling, branding etc.

Job-order costing system: It is a system which aims at producing goods or services

according to the need & requirement of the user. Usually, all the activities performed under job-

order costing system are related to achievement of goals & objectives of the firm. The orders

placed by customers vary according to their desire, for example, some people can minimise on

the quality of products to get it for cheap however, other would want to get the best quality

products for which they can pay any amount. This technique is followed by directors of Oshodi

PLC to manufacture the production of JOJO fruit juices which can range from adding extra

quantity of product, offering multi packs etc.

Inventory management system: This is a system which ensures that stock is available

at the warehouse whenever in need. It confirms that adequate raw material for producing goods

are present at the right time and accurate place. To value inventory, various methods are opted by

a firm i.e. LIFO, FIFO, weighted average which are mentioned below:

LIFO: Last in, first out method states that the inventory which as arrived at the end is

consumed first.

FIFO: First in, first out method states that the stock which is arrived at the beginning is

consumed first.

Weighted average: This method divides COGS available for sale with the number of

units present during the time of sale.

Oshodi PLC values its inventory by using FIFO to avoid any products from getting

expired so sell those juices which are manufactured first (Braun and et.al., 2014). Usually, every

organisation follows and complies by this system and in this report, Oshodi PLC does the same

in order to maximise the production of JOJO fruit juice. The company ensures that appropriate

material, equipment is used in manufacturing the juice so that the quality is not compromised.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost managerial accounting system: It is a system which manages as well as set value

of various products and services & also considers fixed, variable cost etc. This is used by Oshodi

PLC to estimate price for their variant JOJO fruit juice after analysing the need & desire of the

user. The allocation of cost done by the company is based on either traditional or ABC approach

which calculates single overhead rate and applies that within each department. On the other

hand, the second technique involves calculation of activity rate as well as application of

overheads based on the usage.

P2 Types of management accounting reports:

Management accounting reporting: This is a process of reporting where different

forecasts are prepared by managers in order to analyse the performance of activities performed

by an organisation. It involves a variety of reports which are produced by higher authorities of

Oshodi PLC to measure the performance of their product i.e. JOJO fruit juice among the market

participants (Charifzadeh and Taschner, 2017). Every organisation like Oshodi PLC produces a

forecast for all the expenses or incomes that may arise in the future. This can be done with the

help of a budget report which aims at allocating funds to each functional unit after assessing the

need of that department.

Budget report: These reports determine how much funds should be allocated to various

functional units of an organisation. It also involves preparing a forecast for the future expenses &

earnings after a detailed analysis of prior year's expenditure. The selected company i.e. Oshodi

PLC produces a budget report for estimating the gains & losses which may occur during an

accounting year. The organisation also considers how much finances should be assigned to each

department like production, sales, human resource, marketing, research & development etc.

Performance report: These are the reports prepared by management accountants to

analyse substantive expenditure and revenue with the amounts allotted to each department within

an organisation. Oshodi PLC prepares a performance report to assess the execution of work done

by each and every employee (Eterno and Silverman, 2017). The company uses this report to get

an idea about how well their variant JOJO fruit juice is performing in the market which can be

attained by interpreting customer response or rating given by them on a particular product.

Accounts receivable aging report: These are the reports that keep a continuous check

on defaulters of a company by checking the duration of time in which they have paid their dues.

Aging report also aids the management of Oshodi PLC by determining the problems which could

of various products and services & also considers fixed, variable cost etc. This is used by Oshodi

PLC to estimate price for their variant JOJO fruit juice after analysing the need & desire of the

user. The allocation of cost done by the company is based on either traditional or ABC approach

which calculates single overhead rate and applies that within each department. On the other

hand, the second technique involves calculation of activity rate as well as application of

overheads based on the usage.

P2 Types of management accounting reports:

Management accounting reporting: This is a process of reporting where different

forecasts are prepared by managers in order to analyse the performance of activities performed

by an organisation. It involves a variety of reports which are produced by higher authorities of

Oshodi PLC to measure the performance of their product i.e. JOJO fruit juice among the market

participants (Charifzadeh and Taschner, 2017). Every organisation like Oshodi PLC produces a

forecast for all the expenses or incomes that may arise in the future. This can be done with the

help of a budget report which aims at allocating funds to each functional unit after assessing the

need of that department.

Budget report: These reports determine how much funds should be allocated to various

functional units of an organisation. It also involves preparing a forecast for the future expenses &

earnings after a detailed analysis of prior year's expenditure. The selected company i.e. Oshodi

PLC produces a budget report for estimating the gains & losses which may occur during an

accounting year. The organisation also considers how much finances should be assigned to each

department like production, sales, human resource, marketing, research & development etc.

Performance report: These are the reports prepared by management accountants to

analyse substantive expenditure and revenue with the amounts allotted to each department within

an organisation. Oshodi PLC prepares a performance report to assess the execution of work done

by each and every employee (Eterno and Silverman, 2017). The company uses this report to get

an idea about how well their variant JOJO fruit juice is performing in the market which can be

attained by interpreting customer response or rating given by them on a particular product.

Accounts receivable aging report: These are the reports that keep a continuous check

on defaulters of a company by checking the duration of time in which they have paid their dues.

Aging report also aids the management of Oshodi PLC by determining the problems which could

arise in the company's collection cycle. It is essential to prepare for the benefit of the selected

organisation as the directors analyse any potential defaulters and offer them extended credit

terms which can help them in recovering their due amounts.

Cost accounting report: These reports are designed for providing internal information to

the user about the cost associated with different products or services. The major purpose of this

report is to help the management of Oshodi PLC by determining the value of goods to be kept

with effective planning, controlling and decision-making. The company prepares cost accounting

report to compute value of JOJO fruit juice produced on a day-to day basis which includes cost

incurred on packaging & labelling, overheads, labour, raw material etc.

M1 Benefits of management accounting systems:

Following mentioned are the benefits of using different management accounting systems:

Management accounting systems Benefits

Price optimisation The managers of Oshodi PLC use price optimisation

system as it helps them in saving time which reduces

the effort of internal manual resources. For this purpose,

the company selects appropriate pricing strategy to set

value of JOJO fruit juice lower than its competitors.

Job-order costing This is beneficial for the company as it helps in

reducing price of products by making proper

customisations in the product according to the need &

requirement of the user. It can be done with the help of

job-order costing system which is implemented by

Oshodi PLC.

Inventory management With the help of inventory management system

implemented by Oshodi PLC, risk of overselling or

overbuying the raw materials could be reduced as it

involves maintaining stock sheets which records how

much goods have been ordered or are present at the

warehouse.

Cost managerial accounting The managers of Oshodi PLC use cost accounting

organisation as the directors analyse any potential defaulters and offer them extended credit

terms which can help them in recovering their due amounts.

Cost accounting report: These reports are designed for providing internal information to

the user about the cost associated with different products or services. The major purpose of this

report is to help the management of Oshodi PLC by determining the value of goods to be kept

with effective planning, controlling and decision-making. The company prepares cost accounting

report to compute value of JOJO fruit juice produced on a day-to day basis which includes cost

incurred on packaging & labelling, overheads, labour, raw material etc.

M1 Benefits of management accounting systems:

Following mentioned are the benefits of using different management accounting systems:

Management accounting systems Benefits

Price optimisation The managers of Oshodi PLC use price optimisation

system as it helps them in saving time which reduces

the effort of internal manual resources. For this purpose,

the company selects appropriate pricing strategy to set

value of JOJO fruit juice lower than its competitors.

Job-order costing This is beneficial for the company as it helps in

reducing price of products by making proper

customisations in the product according to the need &

requirement of the user. It can be done with the help of

job-order costing system which is implemented by

Oshodi PLC.

Inventory management With the help of inventory management system

implemented by Oshodi PLC, risk of overselling or

overbuying the raw materials could be reduced as it

involves maintaining stock sheets which records how

much goods have been ordered or are present at the

warehouse.

Cost managerial accounting The managers of Oshodi PLC use cost accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system to ascertain the value of goods associated with

each and every level of production or department. This

helps them to evaluate the price which should be kept

fixed like packaging & labelling charges and variable

such as quantity of juice.

D1 Integration of management accounting systems with reporting:

Both management accounting reports and systems ate interrelated with each other in such

a way that it helps the organisation in preparing both simultaneously. The directors of Oshodi

PLC uses management accounting systems to set price of products & services as per the need

and desire of the user (Fayol, 2016). Since, customer satisfaction is considered to be the main

asset of a firm so the company aims at manufacturing JOJO fruit juices after making

customisations in it as requested by the consumer. For every package of juice manufactured,

funds are required. For that purpose, Oshodi PLC prepares a budget report and allots finances to

each and every functional unit. The company also ensures that performance of its products is

maintained better than its competitors which could be done after assessing ratings given by the

client.

TASK 2

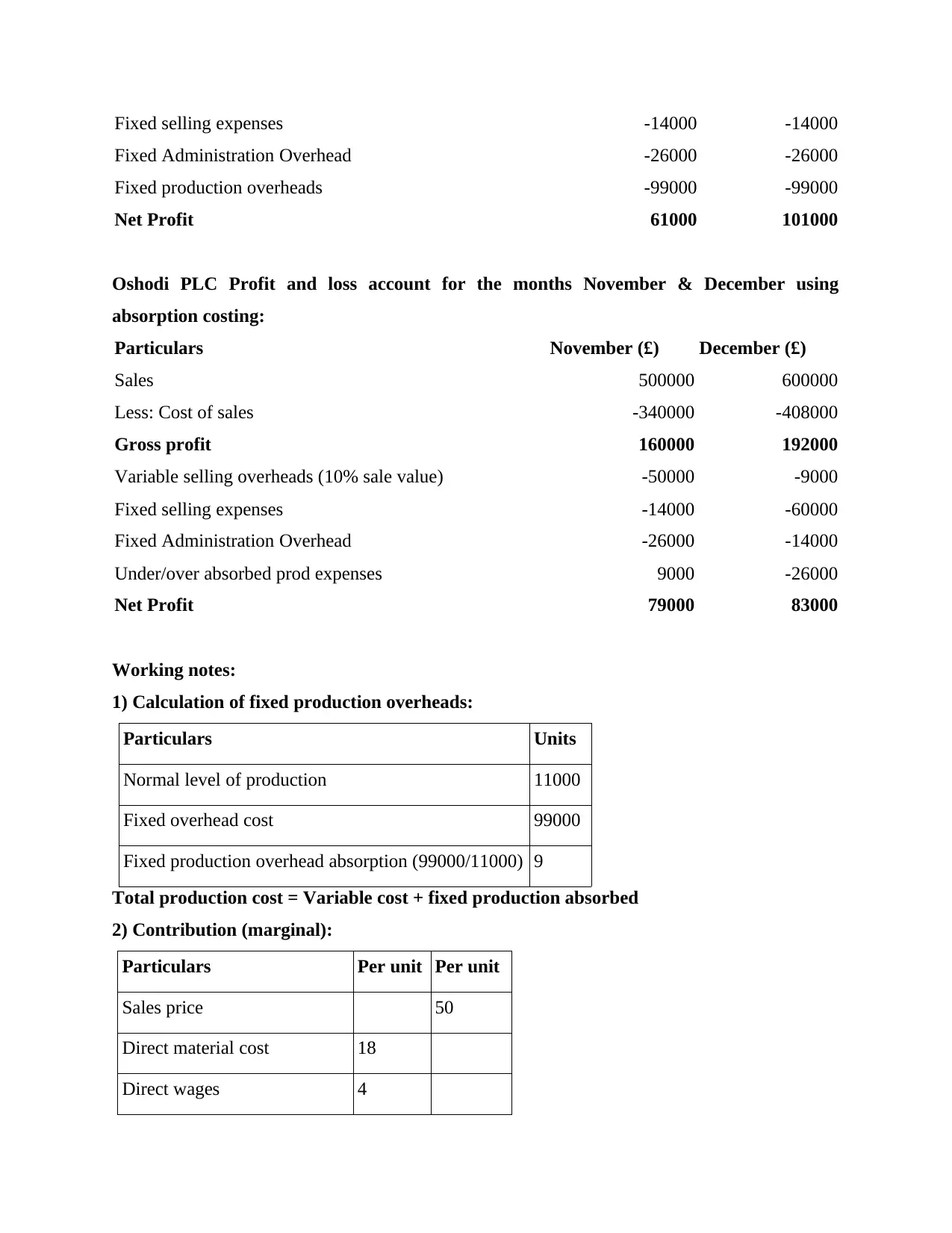

P3 Calculation of net profit with the help of management accounting techniques:

Oshodi PLC Profit and loss account for the months November & December using marginal

costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

Direct Labour costs -40000 -48000

Variable Production Overheads -30000 -36000

Contribution 250000 300000

Less:

Variable selling overheads (10% sale value) -50000 -60000

each and every level of production or department. This

helps them to evaluate the price which should be kept

fixed like packaging & labelling charges and variable

such as quantity of juice.

D1 Integration of management accounting systems with reporting:

Both management accounting reports and systems ate interrelated with each other in such

a way that it helps the organisation in preparing both simultaneously. The directors of Oshodi

PLC uses management accounting systems to set price of products & services as per the need

and desire of the user (Fayol, 2016). Since, customer satisfaction is considered to be the main

asset of a firm so the company aims at manufacturing JOJO fruit juices after making

customisations in it as requested by the consumer. For every package of juice manufactured,

funds are required. For that purpose, Oshodi PLC prepares a budget report and allots finances to

each and every functional unit. The company also ensures that performance of its products is

maintained better than its competitors which could be done after assessing ratings given by the

client.

TASK 2

P3 Calculation of net profit with the help of management accounting techniques:

Oshodi PLC Profit and loss account for the months November & December using marginal

costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

Direct Labour costs -40000 -48000

Variable Production Overheads -30000 -36000

Contribution 250000 300000

Less:

Variable selling overheads (10% sale value) -50000 -60000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed selling expenses -14000 -14000

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Oshodi PLC Profit and loss account for the months November & December using

absorption costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales -340000 -408000

Gross profit 160000 192000

Variable selling overheads (10% sale value) -50000 -9000

Fixed selling expenses -14000 -60000

Fixed Administration Overhead -26000 -14000

Under/over absorbed prod expenses 9000 -26000

Net Profit 79000 83000

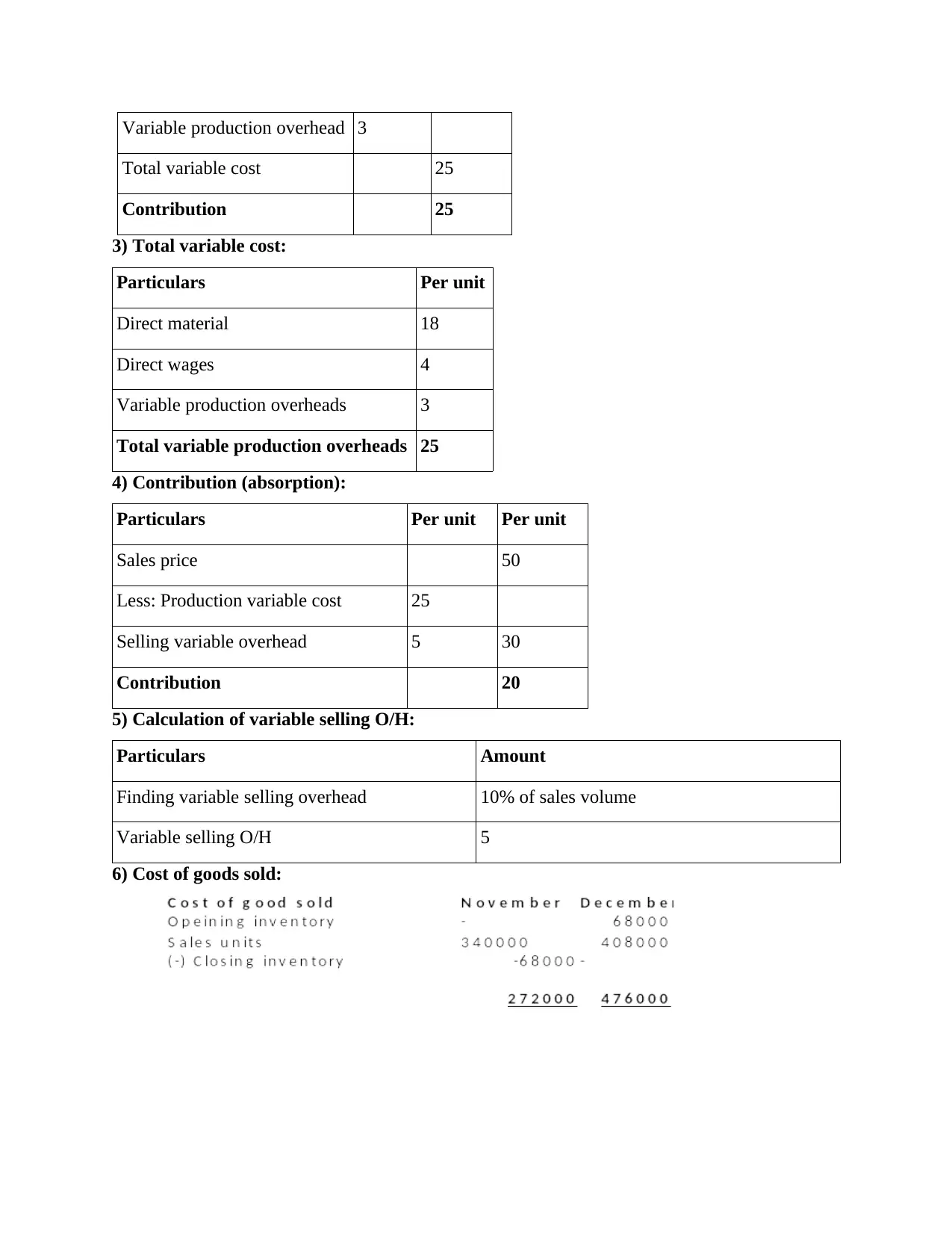

Working notes:

1) Calculation of fixed production overheads:

Particulars Units

Normal level of production 11000

Fixed overhead cost 99000

Fixed production overhead absorption (99000/11000) 9

Total production cost = Variable cost + fixed production absorbed

2) Contribution (marginal):

Particulars Per unit Per unit

Sales price 50

Direct material cost 18

Direct wages 4

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Oshodi PLC Profit and loss account for the months November & December using

absorption costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales -340000 -408000

Gross profit 160000 192000

Variable selling overheads (10% sale value) -50000 -9000

Fixed selling expenses -14000 -60000

Fixed Administration Overhead -26000 -14000

Under/over absorbed prod expenses 9000 -26000

Net Profit 79000 83000

Working notes:

1) Calculation of fixed production overheads:

Particulars Units

Normal level of production 11000

Fixed overhead cost 99000

Fixed production overhead absorption (99000/11000) 9

Total production cost = Variable cost + fixed production absorbed

2) Contribution (marginal):

Particulars Per unit Per unit

Sales price 50

Direct material cost 18

Direct wages 4

Variable production overhead 3

Total variable cost 25

Contribution 25

3) Total variable cost:

Particulars Per unit

Direct material 18

Direct wages 4

Variable production overheads 3

Total variable production overheads 25

4) Contribution (absorption):

Particulars Per unit Per unit

Sales price 50

Less: Production variable cost 25

Selling variable overhead 5 30

Contribution 20

5) Calculation of variable selling O/H:

Particulars Amount

Finding variable selling overhead 10% of sales volume

Variable selling O/H 5

6) Cost of goods sold:

Total variable cost 25

Contribution 25

3) Total variable cost:

Particulars Per unit

Direct material 18

Direct wages 4

Variable production overheads 3

Total variable production overheads 25

4) Contribution (absorption):

Particulars Per unit Per unit

Sales price 50

Less: Production variable cost 25

Selling variable overhead 5 30

Contribution 20

5) Calculation of variable selling O/H:

Particulars Amount

Finding variable selling overhead 10% of sales volume

Variable selling O/H 5

6) Cost of goods sold:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Application of various management accounting techniques:

Standard costing: It is a type of costing method used to determine price, material

variance etc. between cost of goods which are actually produced and the value which should

have been occurred. For Oshodi PLC, this comprises of direct material, labour, production

overheads as well as valuation of inventory (Wilson, 2014).

ABC costing: This is an approach where cost is assigned among various activities

happening in a firm. It ensures that each cost driver has been allotted funds in order to work

productively. The managers of Oshodi PLC allocate funds to each department for the

manufacturing of JOJO fruit juice.

D2 Interpretation of financial reports:

From the above financial reports i.e. marginal and absorption costing it can be interpreted

that in the first profit & loss account, valuation of inventory is not considered. Therefore, there is

a gap in net profit for both the years i.e. November and December. Also, fixed absorption

overheads are not deducted from cost of sales. Although, if we see the net profit figure calculated

by absorption costing, the rise in profit figure is much less as compared with marginal approach.

It is because this considers inventory calculation as well as deducts fixed overheads.

TASK 3

P4 Advantages and disadvantages of planning tools used for budgetary control:

Budget: It is a plan of action in the form of preparing a forecast for the future expenses &

losses during an accounting year (Fleischman and Parker, 2017). In Oshodi PLC, the managers

prepare budget which helps them in analysing and allocating finances to each functional unit of

the organisation. For the manufacturing of JOJO fruit juice, the company usually prepares a cash

forecast to analyse the financial performance of each department i.e. marketing, sales, R&D etc.

Budgetary control: This refers to a control procedure wherein various budgets are

prepared by the organisations for several purpose. It includes master, operational, fixed, flexible,

cash, capital budget etc. In order to achieve organisational growth and success, Oshodi PLC

follows a budgetary control procedure wherein forecasts are produced by the managers to get an

estimation of gains & losses associate with each department.

Following explained are the different types of budgets:

Standard costing: It is a type of costing method used to determine price, material

variance etc. between cost of goods which are actually produced and the value which should

have been occurred. For Oshodi PLC, this comprises of direct material, labour, production

overheads as well as valuation of inventory (Wilson, 2014).

ABC costing: This is an approach where cost is assigned among various activities

happening in a firm. It ensures that each cost driver has been allotted funds in order to work

productively. The managers of Oshodi PLC allocate funds to each department for the

manufacturing of JOJO fruit juice.

D2 Interpretation of financial reports:

From the above financial reports i.e. marginal and absorption costing it can be interpreted

that in the first profit & loss account, valuation of inventory is not considered. Therefore, there is

a gap in net profit for both the years i.e. November and December. Also, fixed absorption

overheads are not deducted from cost of sales. Although, if we see the net profit figure calculated

by absorption costing, the rise in profit figure is much less as compared with marginal approach.

It is because this considers inventory calculation as well as deducts fixed overheads.

TASK 3

P4 Advantages and disadvantages of planning tools used for budgetary control:

Budget: It is a plan of action in the form of preparing a forecast for the future expenses &

losses during an accounting year (Fleischman and Parker, 2017). In Oshodi PLC, the managers

prepare budget which helps them in analysing and allocating finances to each functional unit of

the organisation. For the manufacturing of JOJO fruit juice, the company usually prepares a cash

forecast to analyse the financial performance of each department i.e. marketing, sales, R&D etc.

Budgetary control: This refers to a control procedure wherein various budgets are

prepared by the organisations for several purpose. It includes master, operational, fixed, flexible,

cash, capital budget etc. In order to achieve organisational growth and success, Oshodi PLC

follows a budgetary control procedure wherein forecasts are produced by the managers to get an

estimation of gains & losses associate with each department.

Following explained are the different types of budgets:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash budget: It is an estimation of cash inflows and outflows during an accounting year.

Every organisation needs to prepare cash flow forecast in order to assess cost associated with

different type of products & services (Galliers and Leidner, 2014). The management of Oshodi

PLC requires an estimation of how much funds should be allocated within each functional unit of

the organisation like production, marketing, sales, R&D etc. For better understanding of a cash

budget, some of the advantages and disadvantages are stated below:

Advantages:

It help the managers of Oshodi PLC to stay in touch with reality by only spending the

allocated amount on raw materials for production of JOJO fruit juice.

Any debts or uncertain expenses can be easily dealt with by maintaining a reserve out of

the profits which can be used in case of emergencies.

Disadvantages:

There are higher chances of manipulation in this types of budget as it deals with cash on a

daily basis.

It eliminates non-financial factors while preparing a cash budget as only monetary

transactions are considered.

Capital budget: These budgets are generally used when large expenses need to be

incurred. A capital budget helps management of Oshodi PLC to achieve organisational goals and

objectives by estimating how much funds are required by various departments in the company.

Usually, directors prepare these forecasts to identify potential projects with the help of

investment appraisal techniques like net present value, internal rate of return, pay-back period

etc. For better understanding of a capital budget, listed below are some of the advantages and

disadvantages:

Advantages:

It helps the manufacturing company i.e. Oshodi PLC in better understanding of risks

involved in an investment project and what will be the outcome of it.

With he help of various capital budgeting techniques like NPV, IRR, ARR, pay-back

period, it becomes an easy task for the company to invest in a potential project which will

provide efficient results in the future.

Disadvantages:

Every organisation needs to prepare cash flow forecast in order to assess cost associated with

different type of products & services (Galliers and Leidner, 2014). The management of Oshodi

PLC requires an estimation of how much funds should be allocated within each functional unit of

the organisation like production, marketing, sales, R&D etc. For better understanding of a cash

budget, some of the advantages and disadvantages are stated below:

Advantages:

It help the managers of Oshodi PLC to stay in touch with reality by only spending the

allocated amount on raw materials for production of JOJO fruit juice.

Any debts or uncertain expenses can be easily dealt with by maintaining a reserve out of

the profits which can be used in case of emergencies.

Disadvantages:

There are higher chances of manipulation in this types of budget as it deals with cash on a

daily basis.

It eliminates non-financial factors while preparing a cash budget as only monetary

transactions are considered.

Capital budget: These budgets are generally used when large expenses need to be

incurred. A capital budget helps management of Oshodi PLC to achieve organisational goals and

objectives by estimating how much funds are required by various departments in the company.

Usually, directors prepare these forecasts to identify potential projects with the help of

investment appraisal techniques like net present value, internal rate of return, pay-back period

etc. For better understanding of a capital budget, listed below are some of the advantages and

disadvantages:

Advantages:

It helps the manufacturing company i.e. Oshodi PLC in better understanding of risks

involved in an investment project and what will be the outcome of it.

With he help of various capital budgeting techniques like NPV, IRR, ARR, pay-back

period, it becomes an easy task for the company to invest in a potential project which will

provide efficient results in the future.

Disadvantages:

Any wrong implementation of decision can affect in the long-term durability of Oshodi

PLC.

It is introspective in nature due to subjective risk & discounting factor undertaken by

company to measure cash flows.

Zero-based budget: It is a type of budget which is prepared from zero values i.e. scratch.

This requires the forecast to be produced from a zero-base without considering any previous

year's records (Gupta, 2016). In the selected company i.e. Oshodi PLC, all the cost associated

with manufacturing of JOJO fruit juice needs to be justified in order to get effective & efficient

output. The advantages and disadvantages are mentioned below:

Advantages:

This emphasises on co-ordination as well as communication among all the members of

Oshodi PLC.

It boosts up staff motivation as this gives them more authority towards decision-making.

Disadvantages:

Since this budget is prepared from a zero-base so it becomes a time-consuming process

for the managers at Oshodi PLC.

This requires well-equipped personnels who carry a detailed understanding about each

individual business transaction involves in the preparation of the budget.

M3 Use of planning tools for forecasting budgets:

Planning tools play a crucial role in estimating the requirement of budgets. Different

types of forecasts like zero-based, fixed, flexible, capital, master operational etc. are prepared by

Oshodi PLC for different purpose to assign & allocate cost associated with production of JOJO

fruit juice. These planning tools help the company in producing forecast for income and

expenditure which may result in the future by analysing previous year's records so that there is

no misappropriation of funds. In relation to this, the company also chooses to opt some capital

budgeting techniques in case there is a need to invest in any potential projects.

TASK 4

P5 Ways in which management accounting systems are used to resolve financial problems:

On a day-to-day basis, every organisation needs to comply with some techniques in order

to respond through financial problems. Some of the issues are mentioned below:

PLC.

It is introspective in nature due to subjective risk & discounting factor undertaken by

company to measure cash flows.

Zero-based budget: It is a type of budget which is prepared from zero values i.e. scratch.

This requires the forecast to be produced from a zero-base without considering any previous

year's records (Gupta, 2016). In the selected company i.e. Oshodi PLC, all the cost associated

with manufacturing of JOJO fruit juice needs to be justified in order to get effective & efficient

output. The advantages and disadvantages are mentioned below:

Advantages:

This emphasises on co-ordination as well as communication among all the members of

Oshodi PLC.

It boosts up staff motivation as this gives them more authority towards decision-making.

Disadvantages:

Since this budget is prepared from a zero-base so it becomes a time-consuming process

for the managers at Oshodi PLC.

This requires well-equipped personnels who carry a detailed understanding about each

individual business transaction involves in the preparation of the budget.

M3 Use of planning tools for forecasting budgets:

Planning tools play a crucial role in estimating the requirement of budgets. Different

types of forecasts like zero-based, fixed, flexible, capital, master operational etc. are prepared by

Oshodi PLC for different purpose to assign & allocate cost associated with production of JOJO

fruit juice. These planning tools help the company in producing forecast for income and

expenditure which may result in the future by analysing previous year's records so that there is

no misappropriation of funds. In relation to this, the company also chooses to opt some capital

budgeting techniques in case there is a need to invest in any potential projects.

TASK 4

P5 Ways in which management accounting systems are used to resolve financial problems:

On a day-to-day basis, every organisation needs to comply with some techniques in order

to respond through financial problems. Some of the issues are mentioned below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.