Management Accounting Techniques and Financial Problems Report

VerifiedAdded on 2021/02/19

|14

|4928

|121

Report

AI Summary

This report provides a detailed overview of management accounting, encompassing its definition, various types, and the benefits of different systems like inventory, price optimization, and cost accounting. It delves into management accounting reporting methods, including budgets, variance analysis, and cost schedules, along with their integration with organizational processes. The report analyzes the application of management accounting techniques such as marginal and absorption costing, providing practical examples and calculations. Furthermore, it explores the use of planning tools in forecasting budgets and addressing financial problems, evaluating how these tools contribute to sustainable success within an organization. The report uses ABC Ltd., a medium-sized manufacturing company, as a case study to illustrate these concepts.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and its types....................................................................................1

Different method of management accounting reporting........................................................2

Benefits of different management accounting systems..........................................................3

Management accounting system and reporting is integrated with organisational processes. 3

TASK 2............................................................................................................................................3

Applying a range of management accounting techniques:.....................................................3

TASK 3............................................................................................................................................6

Planning tools used in management accounting:....................................................................6

Uses of different planing tools in forecasting budget.............................................................8

TASK 4............................................................................................................................................8

Comparison of how organisations are adapting management accounting systems to respond to

financial problems:.................................................................................................................8

Analysis about how responding to financial problems, management accounting lead

organisation to sustainable success:.....................................................................................10

Evaluation of how planning tools for accounting respond appropriately for solving financial

problems to lead organisations to sustainable success:........................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and its types....................................................................................1

Different method of management accounting reporting........................................................2

Benefits of different management accounting systems..........................................................3

Management accounting system and reporting is integrated with organisational processes. 3

TASK 2............................................................................................................................................3

Applying a range of management accounting techniques:.....................................................3

TASK 3............................................................................................................................................6

Planning tools used in management accounting:....................................................................6

Uses of different planing tools in forecasting budget.............................................................8

TASK 4............................................................................................................................................8

Comparison of how organisations are adapting management accounting systems to respond to

financial problems:.................................................................................................................8

Analysis about how responding to financial problems, management accounting lead

organisation to sustainable success:.....................................................................................10

Evaluation of how planning tools for accounting respond appropriately for solving financial

problems to lead organisations to sustainable success:........................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is a kind of accounting system which is related to internal

management of companies(Ward, 2012). It consists a wide range of reports, tools and techniques

which are required for overcoming the various financial issues. This process provide raw data to

managerial personnels for decision making activities. It provide a systematic framework for

business organisation for achievement of organisation goals and objectives. The project report

contains detailed explanation about the management accounting and its types as well as benefits,

various aspects of management accounting reporting, advantage and disadvantage of various

planning tools along with their application to respond financial problems of ABC Ltd, an a

medium sized manufacturing company. This report also exhibits integration of management

accounting system and reporting within organisational processes, practical application of

management accounting techniques and an explanation about how responding to financial

problem leads organisation to sustainable success.

TASK 1

Management accounting and its types.

Management accounting may be defined as an accounting system which plays a crucial

role for internal management as well as for controlling the financial performance of companies.

This accounting system contains all kind of information including financial and non financial

information which becomes basis for the managers to take important decisions. This accounting

system is used by the ABC limited company for enhancing the management of their

manufacturing system. Herein, some types of management accounting system are mentioned

below:

Inventory management system- Inventory management system is a kind of system that

is related to management of raw material as well as of finished products. It is required for

track the quantity of available stock the warehouses and with the help of this companies

make decisions for the production. The ABC limited company use this system to analyse

about the quantity of raw material and prepared products.

Price optimisation system- Price optimisation system provides a framework for

determining the price of products and services. Apart from this, it is required in analyse

the reaction of customers on different pricing levels(DRURY, 2013). Due to this

1

Management accounting is a kind of accounting system which is related to internal

management of companies(Ward, 2012). It consists a wide range of reports, tools and techniques

which are required for overcoming the various financial issues. This process provide raw data to

managerial personnels for decision making activities. It provide a systematic framework for

business organisation for achievement of organisation goals and objectives. The project report

contains detailed explanation about the management accounting and its types as well as benefits,

various aspects of management accounting reporting, advantage and disadvantage of various

planning tools along with their application to respond financial problems of ABC Ltd, an a

medium sized manufacturing company. This report also exhibits integration of management

accounting system and reporting within organisational processes, practical application of

management accounting techniques and an explanation about how responding to financial

problem leads organisation to sustainable success.

TASK 1

Management accounting and its types.

Management accounting may be defined as an accounting system which plays a crucial

role for internal management as well as for controlling the financial performance of companies.

This accounting system contains all kind of information including financial and non financial

information which becomes basis for the managers to take important decisions. This accounting

system is used by the ABC limited company for enhancing the management of their

manufacturing system. Herein, some types of management accounting system are mentioned

below:

Inventory management system- Inventory management system is a kind of system that

is related to management of raw material as well as of finished products. It is required for

track the quantity of available stock the warehouses and with the help of this companies

make decisions for the production. The ABC limited company use this system to analyse

about the quantity of raw material and prepared products.

Price optimisation system- Price optimisation system provides a framework for

determining the price of products and services. Apart from this, it is required in analyse

the reaction of customers on different pricing levels(DRURY, 2013). Due to this

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies can assign an accurate price of their products which is affordable for both to

the customers and company. The ABC limited company sets the price of their products

with the help of this system which satisfy their customers as well as they can earn profit

too.

Cost accounting system- Cost accounting system is a kind of system which is related to

the estimation of cost of products and services. Due to this companies can analyse their

profitability by the selling of product and services. The main requirement of this

accounting system is to control the cost which occurs during the production. The above

company ABC limited implements this system for right estimation of cost of products.

Different method of management accounting reporting.

Management accounting reports are those reports which consists all kind of information

that is necessary for internal management of the companies. Due to these reports organisations

can evaluate their financial and non financial performance(Wickramasinghe and Alawattage,

2012). The ABC limited prepares different kind of management accounting reports on the basis

of various methods which are as follows:

Budgets- Budgets are the estimation of income and expenses for a particular time period.

Eventually, these are helpful in making comparison of actual performance with the budgeted

targets. It is an important method of the preparing management accounting reports. The ABC

limited company prepares the budgetary reports with the help of different types of budgets

because these consists all needed financial informations.

Variance analysis- Variance analysis is a kind of method which compares the actual

performance with the standard goals. If any difference occurs then it take appropriate actions to

resolve the difference. With the help of this method companies prepares the management

accounting reports because it provides a basis for that. Herein, the above company ABC limited

apply this method of preparation of the various kind of reports.

Cost schedules- Cost schedules are the estimation of cost in any kind of budgets. While

preparing the management accounting reports, these cost schedules help a lot. This is why

because if actual cost is below the cost schedule then it will be a positive mark in the reports.

Same as if occurred cost is more then the estimated cost, it will be negative aspect for the

performance reports. The ABC limited company use this method for making accounting reports.

2

the customers and company. The ABC limited company sets the price of their products

with the help of this system which satisfy their customers as well as they can earn profit

too.

Cost accounting system- Cost accounting system is a kind of system which is related to

the estimation of cost of products and services. Due to this companies can analyse their

profitability by the selling of product and services. The main requirement of this

accounting system is to control the cost which occurs during the production. The above

company ABC limited implements this system for right estimation of cost of products.

Different method of management accounting reporting.

Management accounting reports are those reports which consists all kind of information

that is necessary for internal management of the companies. Due to these reports organisations

can evaluate their financial and non financial performance(Wickramasinghe and Alawattage,

2012). The ABC limited prepares different kind of management accounting reports on the basis

of various methods which are as follows:

Budgets- Budgets are the estimation of income and expenses for a particular time period.

Eventually, these are helpful in making comparison of actual performance with the budgeted

targets. It is an important method of the preparing management accounting reports. The ABC

limited company prepares the budgetary reports with the help of different types of budgets

because these consists all needed financial informations.

Variance analysis- Variance analysis is a kind of method which compares the actual

performance with the standard goals. If any difference occurs then it take appropriate actions to

resolve the difference. With the help of this method companies prepares the management

accounting reports because it provides a basis for that. Herein, the above company ABC limited

apply this method of preparation of the various kind of reports.

Cost schedules- Cost schedules are the estimation of cost in any kind of budgets. While

preparing the management accounting reports, these cost schedules help a lot. This is why

because if actual cost is below the cost schedule then it will be a positive mark in the reports.

Same as if occurred cost is more then the estimated cost, it will be negative aspect for the

performance reports. The ABC limited company use this method for making accounting reports.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits of different management accounting systems.

Different types of management accounting systems are very crucial in the context of

organisations. Benefits of these accounting systems are as follows:

Benefits of inventory management system- The inventory management system is

important because it helps in the tracking of raw material and prepared products in the

warehouses. Herein, the ABC limited company it is important for evaluate the quantity of

available material for the production. This helps them in tracking the movement of goods

in entire supply chain system.

Benefits of price optimisation system- This system helps to the ABC limited company

in assigning the accurate price of their manufactured products. Additionally, it provides

them a framework to analyse the customer's reaction at different price levels.

Benefits of cost accounting system- Cost accounting system is beneficial for the above

mentioned company in making prediction about the cost. Further, it becomes a basis for

evaluation of profitability.

Management accounting system and reporting is integrated with organisational processes.

Management accounting system and reporting both have a link with organisational

process. Basically, this is possible because different kind of accounting systems become basis for

the preparation of the accounting reports (Otley and Emmanuel, 2013). Due to this integration,

various functions of companies can implement smoothly. Herein, the ABC limited company they

use different kind of accounting systems like price optimisation system, inventory management

systems which plays an important role for the effective use of different available sources. Same

as different methods of management accounting reporting like variance analysis, budgets etc. are

linked with the organisational process as well as with the success.

TASK 2

Applying a range of management accounting techniques:

A business organisation while operating its day to day activities incur various costs which

are necessary to operate. Cost simply refers to monetary amount which organisation is ready to

pay for performing any activity or to acquire some thing. Proper management of cost is essential

for proper utilisation of organisation's resources (Jakobsen, 2012). Following are some major

management accounting techniques that assist in calculation of cost effectively, as follows:

3

Different types of management accounting systems are very crucial in the context of

organisations. Benefits of these accounting systems are as follows:

Benefits of inventory management system- The inventory management system is

important because it helps in the tracking of raw material and prepared products in the

warehouses. Herein, the ABC limited company it is important for evaluate the quantity of

available material for the production. This helps them in tracking the movement of goods

in entire supply chain system.

Benefits of price optimisation system- This system helps to the ABC limited company

in assigning the accurate price of their manufactured products. Additionally, it provides

them a framework to analyse the customer's reaction at different price levels.

Benefits of cost accounting system- Cost accounting system is beneficial for the above

mentioned company in making prediction about the cost. Further, it becomes a basis for

evaluation of profitability.

Management accounting system and reporting is integrated with organisational processes.

Management accounting system and reporting both have a link with organisational

process. Basically, this is possible because different kind of accounting systems become basis for

the preparation of the accounting reports (Otley and Emmanuel, 2013). Due to this integration,

various functions of companies can implement smoothly. Herein, the ABC limited company they

use different kind of accounting systems like price optimisation system, inventory management

systems which plays an important role for the effective use of different available sources. Same

as different methods of management accounting reporting like variance analysis, budgets etc. are

linked with the organisational process as well as with the success.

TASK 2

Applying a range of management accounting techniques:

A business organisation while operating its day to day activities incur various costs which

are necessary to operate. Cost simply refers to monetary amount which organisation is ready to

pay for performing any activity or to acquire some thing. Proper management of cost is essential

for proper utilisation of organisation's resources (Jakobsen, 2012). Following are some major

management accounting techniques that assist in calculation of cost effectively, as follows:

3

Marginal costing : It is technique under which variable costs concerned with

manufacturing and production of product, is charged to cost of units, whereas fixed costs are

considered as period cost so completely written off against net contribution. Marginal cost refers

to additional cost incurred by manufacturer in producing an traditional or extra unit. Under this

technique costs are classified as fixed and variable on the basis of variability. Here price are

calculated as per marginal contribution and marginal cost. While computing the the amount of

finished goods and closing stock, only variable costs are considered. Although variable

distribution and selling overheads are not added in valuation of stock.

Marginal cost = Direct labour + Direct Material + direct expense + other variable

overheads

Absorption costing : It is techniques in which all manufacturing costs whether fixed or

variable are assigned to cost of units manufactured. Absorption cost includes direct labour, direct

material, fixed and variable manufacturing overheads (Gibassier, 2017). This technique is

required for external financial reporting. It provide more accurate calculation of profit as

compare to variable costing. It do not classify costs into variable and fixed costs which is not

possible practically. It presents efficient and inefficient utilisation of various production

resources by indicating over or under absorption of factory overheads. It provide calculation of

net profit and gross profit separately under income statement.

Calculation Of Costs:

A. Marginal Costing

Statement Of Profit Or Loss For

January2019

Per

Unit Budgeted Actual

Sales Revenue 50 800000 800000

Cost Of Sales

Cost Of Production: Variables

Direct Material 10 180000 190000

Direct Labour 20 360000 380000

4

manufacturing and production of product, is charged to cost of units, whereas fixed costs are

considered as period cost so completely written off against net contribution. Marginal cost refers

to additional cost incurred by manufacturer in producing an traditional or extra unit. Under this

technique costs are classified as fixed and variable on the basis of variability. Here price are

calculated as per marginal contribution and marginal cost. While computing the the amount of

finished goods and closing stock, only variable costs are considered. Although variable

distribution and selling overheads are not added in valuation of stock.

Marginal cost = Direct labour + Direct Material + direct expense + other variable

overheads

Absorption costing : It is techniques in which all manufacturing costs whether fixed or

variable are assigned to cost of units manufactured. Absorption cost includes direct labour, direct

material, fixed and variable manufacturing overheads (Gibassier, 2017). This technique is

required for external financial reporting. It provide more accurate calculation of profit as

compare to variable costing. It do not classify costs into variable and fixed costs which is not

possible practically. It presents efficient and inefficient utilisation of various production

resources by indicating over or under absorption of factory overheads. It provide calculation of

net profit and gross profit separately under income statement.

Calculation Of Costs:

A. Marginal Costing

Statement Of Profit Or Loss For

January2019

Per

Unit Budgeted Actual

Sales Revenue 50 800000 800000

Cost Of Sales

Cost Of Production: Variables

Direct Material 10 180000 190000

Direct Labour 20 360000 380000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

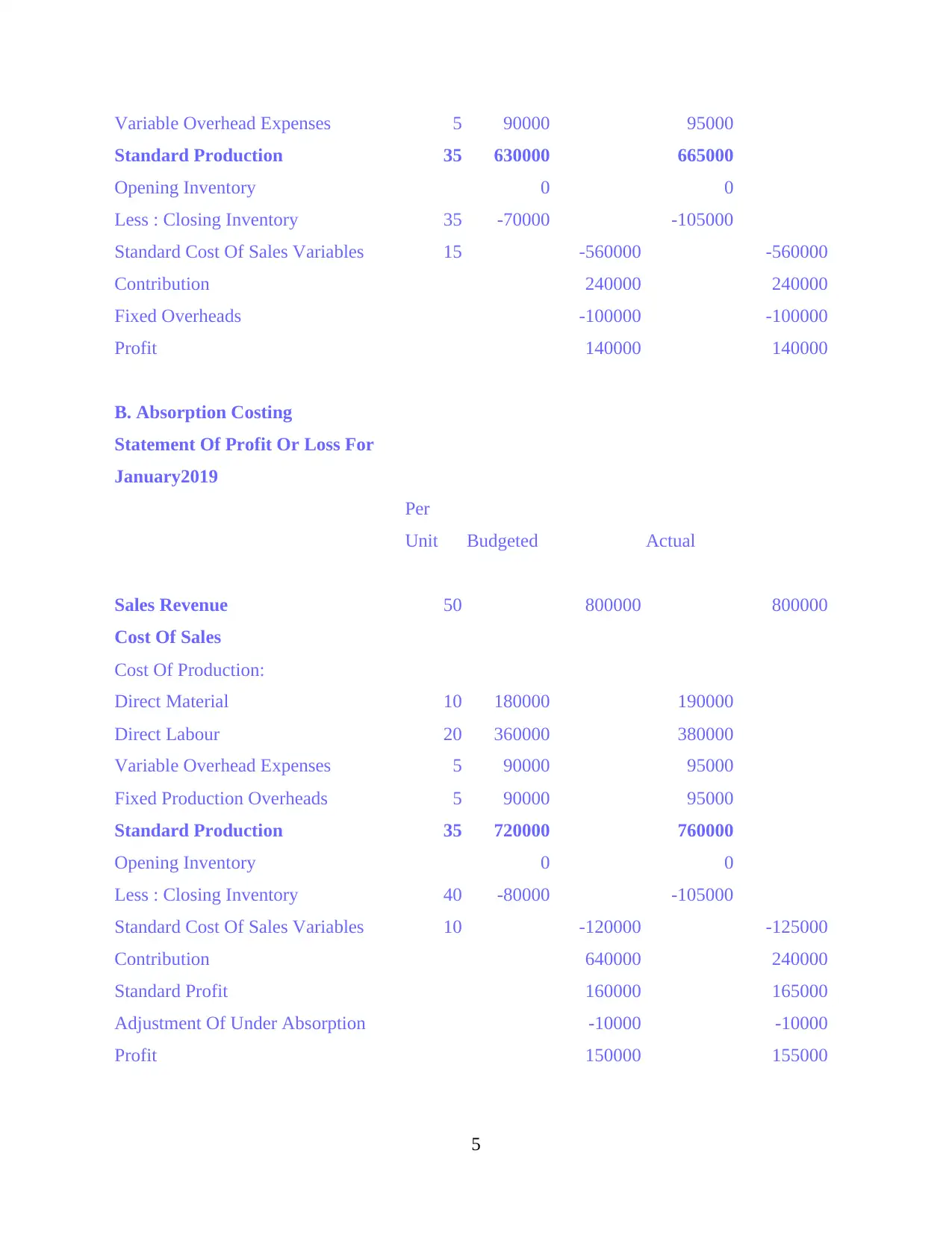

Variable Overhead Expenses 5 90000 95000

Standard Production 35 630000 665000

Opening Inventory 0 0

Less : Closing Inventory 35 -70000 -105000

Standard Cost Of Sales Variables 15 -560000 -560000

Contribution 240000 240000

Fixed Overheads -100000 -100000

Profit 140000 140000

B. Absorption Costing

Statement Of Profit Or Loss For

January2019

Per

Unit Budgeted Actual

Sales Revenue 50 800000 800000

Cost Of Sales

Cost Of Production:

Direct Material 10 180000 190000

Direct Labour 20 360000 380000

Variable Overhead Expenses 5 90000 95000

Fixed Production Overheads 5 90000 95000

Standard Production 35 720000 760000

Opening Inventory 0 0

Less : Closing Inventory 40 -80000 -105000

Standard Cost Of Sales Variables 10 -120000 -125000

Contribution 640000 240000

Standard Profit 160000 165000

Adjustment Of Under Absorption -10000 -10000

Profit 150000 155000

5

Standard Production 35 630000 665000

Opening Inventory 0 0

Less : Closing Inventory 35 -70000 -105000

Standard Cost Of Sales Variables 15 -560000 -560000

Contribution 240000 240000

Fixed Overheads -100000 -100000

Profit 140000 140000

B. Absorption Costing

Statement Of Profit Or Loss For

January2019

Per

Unit Budgeted Actual

Sales Revenue 50 800000 800000

Cost Of Sales

Cost Of Production:

Direct Material 10 180000 190000

Direct Labour 20 360000 380000

Variable Overhead Expenses 5 90000 95000

Fixed Production Overheads 5 90000 95000

Standard Production 35 720000 760000

Opening Inventory 0 0

Less : Closing Inventory 40 -80000 -105000

Standard Cost Of Sales Variables 10 -120000 -125000

Contribution 640000 240000

Standard Profit 160000 165000

Adjustment Of Under Absorption -10000 -10000

Profit 150000 155000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

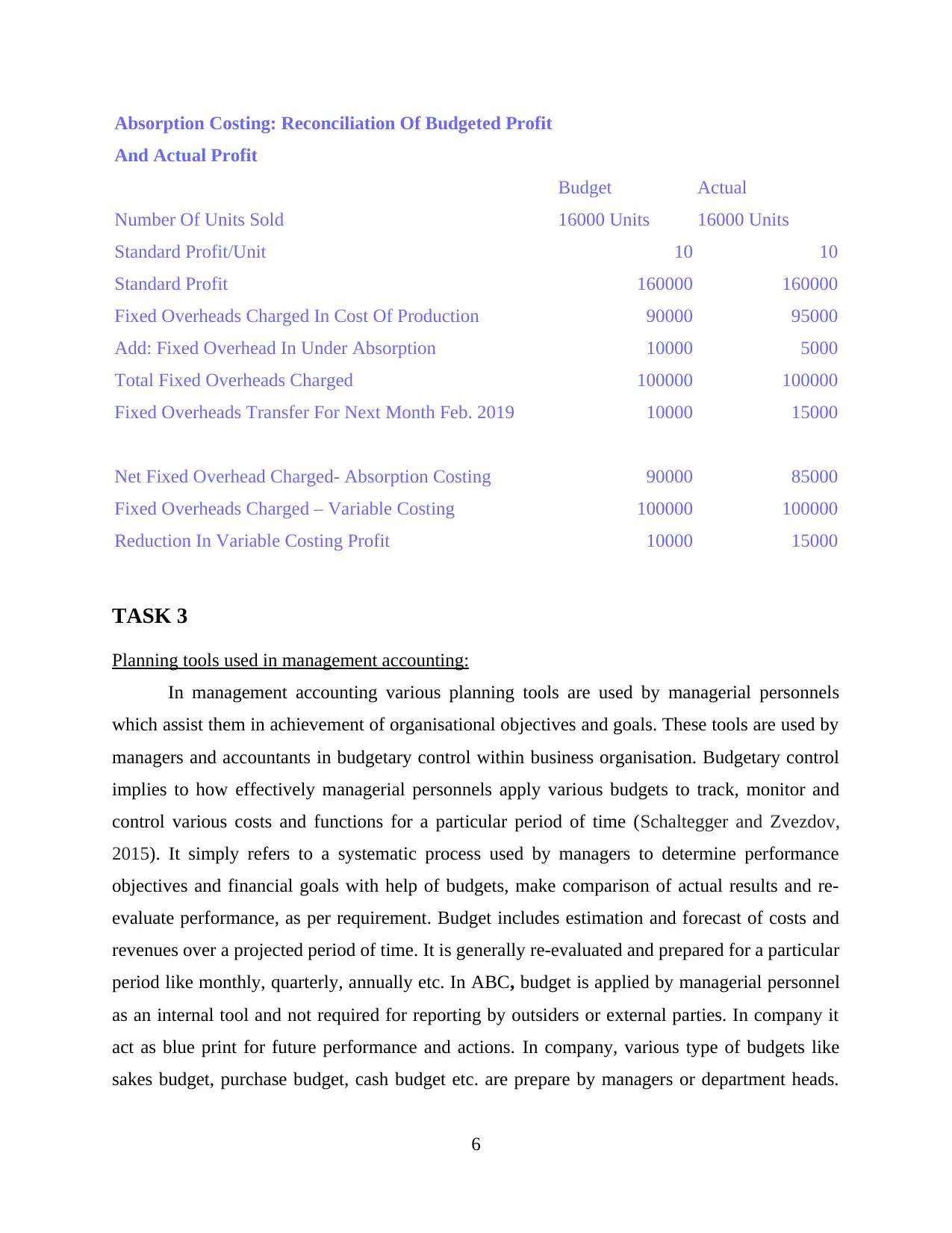

Absorption Costing: Reconciliation Of Budgeted Profit

And Actual Profit

Budget Actual

Number Of Units Sold 16000 Units 16000 Units

Standard Profit/Unit 10 10

Standard Profit 160000 160000

Fixed Overheads Charged In Cost Of Production 90000 95000

Add: Fixed Overhead In Under Absorption 10000 5000

Total Fixed Overheads Charged 100000 100000

Fixed Overheads Transfer For Next Month Feb. 2019 10000 15000

Net Fixed Overhead Charged- Absorption Costing 90000 85000

Fixed Overheads Charged – Variable Costing 100000 100000

Reduction In Variable Costing Profit 10000 15000

TASK 3

Planning tools used in management accounting:

In management accounting various planning tools are used by managerial personnels

which assist them in achievement of organisational objectives and goals. These tools are used by

managers and accountants in budgetary control within business organisation. Budgetary control

implies to how effectively managerial personnels apply various budgets to track, monitor and

control various costs and functions for a particular period of time (Schaltegger and Zvezdov,

2015). It simply refers to a systematic process used by managers to determine performance

objectives and financial goals with help of budgets, make comparison of actual results and re-

evaluate performance, as per requirement. Budget includes estimation and forecast of costs and

revenues over a projected period of time. It is generally re-evaluated and prepared for a particular

period like monthly, quarterly, annually etc. In ABC, budget is applied by managerial personnel

as an internal tool and not required for reporting by outsiders or external parties. In company it

act as blue print for future performance and actions. In company, various type of budgets like

sakes budget, purchase budget, cash budget etc. are prepare by managers or department heads.

6

And Actual Profit

Budget Actual

Number Of Units Sold 16000 Units 16000 Units

Standard Profit/Unit 10 10

Standard Profit 160000 160000

Fixed Overheads Charged In Cost Of Production 90000 95000

Add: Fixed Overhead In Under Absorption 10000 5000

Total Fixed Overheads Charged 100000 100000

Fixed Overheads Transfer For Next Month Feb. 2019 10000 15000

Net Fixed Overhead Charged- Absorption Costing 90000 85000

Fixed Overheads Charged – Variable Costing 100000 100000

Reduction In Variable Costing Profit 10000 15000

TASK 3

Planning tools used in management accounting:

In management accounting various planning tools are used by managerial personnels

which assist them in achievement of organisational objectives and goals. These tools are used by

managers and accountants in budgetary control within business organisation. Budgetary control

implies to how effectively managerial personnels apply various budgets to track, monitor and

control various costs and functions for a particular period of time (Schaltegger and Zvezdov,

2015). It simply refers to a systematic process used by managers to determine performance

objectives and financial goals with help of budgets, make comparison of actual results and re-

evaluate performance, as per requirement. Budget includes estimation and forecast of costs and

revenues over a projected period of time. It is generally re-evaluated and prepared for a particular

period like monthly, quarterly, annually etc. In ABC, budget is applied by managerial personnel

as an internal tool and not required for reporting by outsiders or external parties. In company it

act as blue print for future performance and actions. In company, various type of budgets like

sakes budget, purchase budget, cash budget etc. are prepare by managers or department heads.

6

Then these budgets are used by company's top management in order to take strategic decisions.

Budgets are prepared by companies for internal analysis, normally there is no statutory

requirement for preparation. It help to identify any irregularities or problem that may arise in

near future.

Cash Budget

Cash budget is a significant budget which is prepared by companies to forecast or

estimate the cash in flow and out flow during a specific period of time. This budget assist

managerial personnel to track the actual movement of cash within business organisation. This

budget is also used by business enterprises to ensure the availability of cash to operate. This

budget is normally prepare by mangers after purchase, sale and capital expense budget. In ABC

Ltd, cash budget is prepare by management to manage the movement of cash of company. It

also used to assess the actual liquidity position of company (Amoako, 2013). Management with

help of cash budget also assess the requirement of cash within company. A detailed and

systematic cash budget assist in tracking any loss or theft of cash in company.

Advantages: It is advantageous for ABC, as it assist in determining whether remaining

cash balance is sufficient or adequate to pay their daily working expenses and whether minimum

threshold limit of cash requirement lay down by banks or internal policies are keep up,

Disadvantages: Cash budgets may lead to distortions or misinterpretations, because cash

inflow always do not relate or equate to gain or profits. Cash inflows arise due to capital receipts

like sale of any fixed asset, fines or penalties, deposits etc. are non-sustainable activities, these

are not considered as ongoing and reliable sources of revenue to assess actual profitability.

Operating Budget

It is planning tool which is used by business enterprises to maintain operating and

functioning. For instance, a normal operational budget includes labour and material costs that are

required to operate activities related to manufacturing of product or to provide services. This

budget exhibits company's estimated or forecasted income and expenses during near future

period (Brewer, Sorensen and Stout. 2018). In ABC, this budget is part of income statements

which is prepare by company to assess the operating profit or loss company during the whole

year. It includes a summary schedule which included all items related operating income and

expense. This budget is prepared while considering all variable and revenue expenses but not

includes capital expenditure due to their long term nature.

7

Budgets are prepared by companies for internal analysis, normally there is no statutory

requirement for preparation. It help to identify any irregularities or problem that may arise in

near future.

Cash Budget

Cash budget is a significant budget which is prepared by companies to forecast or

estimate the cash in flow and out flow during a specific period of time. This budget assist

managerial personnel to track the actual movement of cash within business organisation. This

budget is also used by business enterprises to ensure the availability of cash to operate. This

budget is normally prepare by mangers after purchase, sale and capital expense budget. In ABC

Ltd, cash budget is prepare by management to manage the movement of cash of company. It

also used to assess the actual liquidity position of company (Amoako, 2013). Management with

help of cash budget also assess the requirement of cash within company. A detailed and

systematic cash budget assist in tracking any loss or theft of cash in company.

Advantages: It is advantageous for ABC, as it assist in determining whether remaining

cash balance is sufficient or adequate to pay their daily working expenses and whether minimum

threshold limit of cash requirement lay down by banks or internal policies are keep up,

Disadvantages: Cash budgets may lead to distortions or misinterpretations, because cash

inflow always do not relate or equate to gain or profits. Cash inflows arise due to capital receipts

like sale of any fixed asset, fines or penalties, deposits etc. are non-sustainable activities, these

are not considered as ongoing and reliable sources of revenue to assess actual profitability.

Operating Budget

It is planning tool which is used by business enterprises to maintain operating and

functioning. For instance, a normal operational budget includes labour and material costs that are

required to operate activities related to manufacturing of product or to provide services. This

budget exhibits company's estimated or forecasted income and expenses during near future

period (Brewer, Sorensen and Stout. 2018). In ABC, this budget is part of income statements

which is prepare by company to assess the operating profit or loss company during the whole

year. It includes a summary schedule which included all items related operating income and

expense. This budget is prepared while considering all variable and revenue expenses but not

includes capital expenditure due to their long term nature.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages: This budget is prepare by ABC Ltd, to manage their day to day operations

and activities in order to achieve predetermined profitability level. It assist in enhancing the

accountability within a business organisation. It assist in monitoring and tracing the daily

operations of business organisation to minimise additional day to day expenses.

Disadvantages: Operating budgets is kind of short term budgets and prepared by

companies on daily basis which is a time consuming task and also enhance the complexity. In

business organisation that have seasonal business, operating budget does not show true results.

Master Budget

In business organisations, various functional division prepare their own budgets. A

master budget is tool which presents aggregate amount an value of all such divisional budgets. It

assist managerial personnel in decision making and financial planning. It combines all functional

or divisional budgets to provide an overall assessment of company's performance during a

particular period. It determine goals or target for business enterprise to achieve a level within a

specific period (JOSHI and et. al., 2011). In ABC, for preparation of this budget managerial

personnel gather the information of budgets prepared by different functional or divisional

managers, than such information is consolidated to prepare a master budget while considering

organisation's overall objectives and goals. various budgets are prepared by different project

managers and at last a master budget is prepared by mangers to develop a complete picture of

company's performance.

Advantages: It assist business organisation to analyse the complete and detailed

performance and growth during a particular period of time. It provide a framework for master

planning and for identification of any potential problem or issue.

Disadvantages: Through master budget is hard to identify and analyse value of any

specific business item. For intense, it one would not be able to determine or analyse how much

administration department is incurring expense during a particular period.

Uses of different planing tools in forecasting budget

Planning tools are a systematic set of tools that are applied by managerial personnels to

efficiently manage and plan different business activities. Planning tool play a vital role in

preparation and forecasting various budgets. Different – different planning tool assist in

preparation of effective budgets with more accurate and reliable figures (Klemstine and Maher,

2014). Managers in ABC, can apply these tools to identify and assess various problems which

8

and activities in order to achieve predetermined profitability level. It assist in enhancing the

accountability within a business organisation. It assist in monitoring and tracing the daily

operations of business organisation to minimise additional day to day expenses.

Disadvantages: Operating budgets is kind of short term budgets and prepared by

companies on daily basis which is a time consuming task and also enhance the complexity. In

business organisation that have seasonal business, operating budget does not show true results.

Master Budget

In business organisations, various functional division prepare their own budgets. A

master budget is tool which presents aggregate amount an value of all such divisional budgets. It

assist managerial personnel in decision making and financial planning. It combines all functional

or divisional budgets to provide an overall assessment of company's performance during a

particular period. It determine goals or target for business enterprise to achieve a level within a

specific period (JOSHI and et. al., 2011). In ABC, for preparation of this budget managerial

personnel gather the information of budgets prepared by different functional or divisional

managers, than such information is consolidated to prepare a master budget while considering

organisation's overall objectives and goals. various budgets are prepared by different project

managers and at last a master budget is prepared by mangers to develop a complete picture of

company's performance.

Advantages: It assist business organisation to analyse the complete and detailed

performance and growth during a particular period of time. It provide a framework for master

planning and for identification of any potential problem or issue.

Disadvantages: Through master budget is hard to identify and analyse value of any

specific business item. For intense, it one would not be able to determine or analyse how much

administration department is incurring expense during a particular period.

Uses of different planing tools in forecasting budget

Planning tools are a systematic set of tools that are applied by managerial personnels to

efficiently manage and plan different business activities. Planning tool play a vital role in

preparation and forecasting various budgets. Different – different planning tool assist in

preparation of effective budgets with more accurate and reliable figures (Klemstine and Maher,

2014). Managers in ABC, can apply these tools to identify and assess various problems which

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

may occur in near future. Company by using these tools, can increase their efficiency and

effectiveness in forecasting and projecting the amounts and values of items of budgets. Overall

objective of these planning tool is to provide assistance to manager and accountants in

preparation of most reliable and accurate budget. These different tool help in enhancing the

accountability in budgets. Planning tools provide a data or information which point out towards

the a particular trend and scenario in values or amount of various financial items, which assist in

find out most accurate figure for preparation of budgets.

TASK 4

Comparison of how organisations are adapting management accounting systems to respond to

financial problems:

In current business environment, various financial and other problem arise before

business organisation. Sometime, these problems may put question mark on survival of business

enterprises. So early identification and solution of these problem is crucial for business

organisation to sustain success in market. Financial problems refers to circumstances where

lack of money or monetary resources can affect the organisation's operations and functions.

Financial problems develops adverse situation for a business organisation which directly or

indirectly leads to decrease in overall performance, growth and probability of business

organisation (Lim, 2011). Management and owners always wants to avoid or resolve the

financial problem. Following are some major financial problem, in the context of ABC Ltd, as

follows:

Increasing Debts: This is one of the major financial problem for company which affects

overall efficiency of company to generate profit or gains. Increase in shore term and long term

debt indicates that company is not able to generate adequate income to pay its debts. It directly

affects the working capital requirement of company, which is a sign of liquidation. Continuous

increase in debt affects the whole capital structure of company.

Increase in costs: A continuous increase in costs and expenses within a business

organisation is a financial problem which leads to decrease in overall profitability. Increase in

cost indicates various issues like mismanagement of inventories or other material item, decrease

in efficiency of worker, decline in product demand, ineffective management etc (Boyns and

9

effectiveness in forecasting and projecting the amounts and values of items of budgets. Overall

objective of these planning tool is to provide assistance to manager and accountants in

preparation of most reliable and accurate budget. These different tool help in enhancing the

accountability in budgets. Planning tools provide a data or information which point out towards

the a particular trend and scenario in values or amount of various financial items, which assist in

find out most accurate figure for preparation of budgets.

TASK 4

Comparison of how organisations are adapting management accounting systems to respond to

financial problems:

In current business environment, various financial and other problem arise before

business organisation. Sometime, these problems may put question mark on survival of business

enterprises. So early identification and solution of these problem is crucial for business

organisation to sustain success in market. Financial problems refers to circumstances where

lack of money or monetary resources can affect the organisation's operations and functions.

Financial problems develops adverse situation for a business organisation which directly or

indirectly leads to decrease in overall performance, growth and probability of business

organisation (Lim, 2011). Management and owners always wants to avoid or resolve the

financial problem. Following are some major financial problem, in the context of ABC Ltd, as

follows:

Increasing Debts: This is one of the major financial problem for company which affects

overall efficiency of company to generate profit or gains. Increase in shore term and long term

debt indicates that company is not able to generate adequate income to pay its debts. It directly

affects the working capital requirement of company, which is a sign of liquidation. Continuous

increase in debt affects the whole capital structure of company.

Increase in costs: A continuous increase in costs and expenses within a business

organisation is a financial problem which leads to decrease in overall profitability. Increase in

cost indicates various issues like mismanagement of inventories or other material item, decrease

in efficiency of worker, decline in product demand, ineffective management etc (Boyns and

9

Edwards, 2013). it is essential for company to identify the main reason of increasing cost on

early basis.

To avoid or resolve these financial problems, management accounting system is

necessary. Management accounting system propose some methods and techniques to solve or

handle financial problems. Following are some significant methods and techniques which assist

in handling financial problem in ABC Ltd, as follows:

Key financial indicators: KPI or key financial indicators refers to collection of various

quantifiable measures which business enterprise can use to measure its performance over a

particular period. KPI indicates towards any issue that may rise in near future and assist in

resolving these issues. In ABC Ltd, KPI's like net profit, gross profit, account receivable or

payable turnover etc. are applied by managers to analyse the main reason of increasing debts and

area of excessive costs or expenses.

Benchmarking: It includes a set of activities that assist in making comparison of

company's performance against a certain level of performance which may be based on industry

average. Under benchmarking process management first determine the benchmark level, after

that they critically analyse the variance if any to identify cause of financial problem (Tessier and

Otley, 2012). In ABC Ltd, management by applying this method identifies and analyse the main

reason of increase in cost or expenses during a particular problem.

Comparison:

Basis ABC Ltd BCM construction

Financial issue Company is facing financial

problem of increasing debts and

excessive costs which leads to

decrease in profitability (Van der

Stede, 2015).

For BCM construction major financial

problem is high cost of its projects

which forces clients to shift towards

competitors.

Decision making Company is applying management

accounting system to take business

and strategic decisions. Most of the

decisions of company emphasises

on resolving financial problems.

BCM is medium size company and

engaged in construction of buildings,

rail projects and commercial

properties, company's focus towards

taking decisions regarding expansion

10

early basis.

To avoid or resolve these financial problems, management accounting system is

necessary. Management accounting system propose some methods and techniques to solve or

handle financial problems. Following are some significant methods and techniques which assist

in handling financial problem in ABC Ltd, as follows:

Key financial indicators: KPI or key financial indicators refers to collection of various

quantifiable measures which business enterprise can use to measure its performance over a

particular period. KPI indicates towards any issue that may rise in near future and assist in

resolving these issues. In ABC Ltd, KPI's like net profit, gross profit, account receivable or

payable turnover etc. are applied by managers to analyse the main reason of increasing debts and

area of excessive costs or expenses.

Benchmarking: It includes a set of activities that assist in making comparison of

company's performance against a certain level of performance which may be based on industry

average. Under benchmarking process management first determine the benchmark level, after

that they critically analyse the variance if any to identify cause of financial problem (Tessier and

Otley, 2012). In ABC Ltd, management by applying this method identifies and analyse the main

reason of increase in cost or expenses during a particular problem.

Comparison:

Basis ABC Ltd BCM construction

Financial issue Company is facing financial

problem of increasing debts and

excessive costs which leads to

decrease in profitability (Van der

Stede, 2015).

For BCM construction major financial

problem is high cost of its projects

which forces clients to shift towards

competitors.

Decision making Company is applying management

accounting system to take business

and strategic decisions. Most of the

decisions of company emphasises

on resolving financial problems.

BCM is medium size company and

engaged in construction of buildings,

rail projects and commercial

properties, company's focus towards

taking decisions regarding expansion

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.