Management Accounting Report: Techniques and Analysis

VerifiedAdded on 2020/12/29

|18

|5909

|166

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role in financial decision-making within a business context. It begins by defining management accounting and differentiating it from financial accounting, highlighting its importance for internal analysis and strategic planning. The report then delves into various management accounting systems such as inventory management, cost accounting, and price optimization, explaining their functions and benefits. It also explores different management accounting reports, including budget reports, performance reports, and cost management reports, detailing their significance in evaluating performance and guiding business strategies. Furthermore, the report examines costing techniques, such as marginal costing and absorption costing, used to prepare income statements, and discusses various planning tools along with their advantages and disadvantages. Finally, the report analyzes how management accounting systems adapt to respond to financial problems, using examples like TESCO and LOREAL to illustrate its practical applications, ultimately emphasizing its role in achieving sustainable success. The report is structured to provide insights into the practical application of management accounting principles and techniques.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain Management Accounting and different type of management accounting system....1

P2 Different methods of management accounting reports..........................................................3

M1 Evaluate the benefit of management accounting system......................................................4

D1 How management accounting system or management accounting report integrated with

each other.....................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Various costing techniques to prepare an income statement................................................5

M2 Range of management accounting techniques......................................................................9

D2 Financial reports which applies to interpret many business activities..................................9

TASK 3..........................................................................................................................................10

P4 Various kind of planning tool with its advantages and disadvantage..................................10

M3 Analyse different planning tools and their applications......................................................12

TASK 4..........................................................................................................................................12

P5 Adapting of management accounting systems to respond to financial problems................12

Comparison between TESCO and LOREAL............................................................................14

M4 Management accounting response to financial problem can lead organisations to

sustainable success.....................................................................................................................14

D3 Various Planning tool to resolve financial problems...........................................................15

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain Management Accounting and different type of management accounting system....1

P2 Different methods of management accounting reports..........................................................3

M1 Evaluate the benefit of management accounting system......................................................4

D1 How management accounting system or management accounting report integrated with

each other.....................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Various costing techniques to prepare an income statement................................................5

M2 Range of management accounting techniques......................................................................9

D2 Financial reports which applies to interpret many business activities..................................9

TASK 3..........................................................................................................................................10

P4 Various kind of planning tool with its advantages and disadvantage..................................10

M3 Analyse different planning tools and their applications......................................................12

TASK 4..........................................................................................................................................12

P5 Adapting of management accounting systems to respond to financial problems................12

Comparison between TESCO and LOREAL............................................................................14

M4 Management accounting response to financial problem can lead organisations to

sustainable success.....................................................................................................................14

D3 Various Planning tool to resolve financial problems...........................................................15

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is process of analysing the cost of business and prepare financial

statements for the operational work. It include various reports, financial transaction which help

the manager to take decision that further help to achieve their business objectives & goals

(Sisaye and Birnberg, 2012). Management accounting used for the internal purpose and it is not

regulated by law or it helps the manager to take internal or important decision. To be understand

better, Equilibrium Assets Management (EAM) is charted wealth management company and it's

headquarter in Wilmslow. This company established in the year 1995 and they provide experts to

their client regarding wealth and investment management. This report include the management

accounting, it's requirement or different types of management accounting system and the

methods used by the manager for preparing management accounting report. Along with this, it

includes approaches of cost analysis, planning tools and other accounting system with help the

organisation to solve their financial problems.

TASK 1

P1 Explain Management Accounting and different type of management accounting system

Management accounting used by the manager of the company for the identification of

transaction, recording and analysis which help the organisation to take effective decision in

respect of business goal & objectives. It helps the manager to collect financial information to

build different policies which help the management to manage their day to activity in the

Equilibrium Assets Management organisation.

Difference between management accounting and financial accounting.

Management accounting Financial accounting

It is a part of management level and senior

level.

It is one of the mandatory system that is

required to adhere by every organisation for

better financial management.

It assist managers in assessing the requirements

in decision-making.

There are rules related to financial reporting

and accounting principles used in effective

manner.

It is not mandatory to enterprises to imply It is essential for organisations to maintain the

1

Management accounting is process of analysing the cost of business and prepare financial

statements for the operational work. It include various reports, financial transaction which help

the manager to take decision that further help to achieve their business objectives & goals

(Sisaye and Birnberg, 2012). Management accounting used for the internal purpose and it is not

regulated by law or it helps the manager to take internal or important decision. To be understand

better, Equilibrium Assets Management (EAM) is charted wealth management company and it's

headquarter in Wilmslow. This company established in the year 1995 and they provide experts to

their client regarding wealth and investment management. This report include the management

accounting, it's requirement or different types of management accounting system and the

methods used by the manager for preparing management accounting report. Along with this, it

includes approaches of cost analysis, planning tools and other accounting system with help the

organisation to solve their financial problems.

TASK 1

P1 Explain Management Accounting and different type of management accounting system

Management accounting used by the manager of the company for the identification of

transaction, recording and analysis which help the organisation to take effective decision in

respect of business goal & objectives. It helps the manager to collect financial information to

build different policies which help the management to manage their day to activity in the

Equilibrium Assets Management organisation.

Difference between management accounting and financial accounting.

Management accounting Financial accounting

It is a part of management level and senior

level.

It is one of the mandatory system that is

required to adhere by every organisation for

better financial management.

It assist managers in assessing the requirements

in decision-making.

There are rules related to financial reporting

and accounting principles used in effective

manner.

It is not mandatory to enterprises to imply It is essential for organisations to maintain the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management accounting system with in the

organisation.

financial records as income statement, balance

sheet and cash flow statement.

Different Type of management accounting system:

Management accounting system help the organisation to perform their duty effectively in

all department such as It, Finance, Marketing etc. Basically it is useful for the internal analysis

by use of financial information. It is focused on preparing strategies regarding operational

functions, cost of product & services or in decision making process (Sedevich Fons, 2012).

There are some different types of management accounting system which adopt by the manager of

Equilibrium Assets Management company that further helps in decision making process.

Inventory management system: It is a software which help to track inventory level or it

is very complex system to manage their inventory in the organisation but it help the business to

regularly track. It is beneficial for the medium or large size company. Manager of EAM

Company follow this system to manage their products through regular tracking of their supply

chain. This system help the business to identify the availability of their financial products. So it

is beneficial for the manager of EAM company to follow inventory management system or

software. For example: Company can manage their products such as investment, retirement, tax,

intergeneration planning etc. Manager of EAM follow this system to manage their product

information and provide their clients when it required. Inventory management system required to

manage the whole service products through this software which provide the accurate information

regarding this.

Cost accounting system: It is a costing framework which help the organisation to

identify the cost of each unit or it is beneficial or the business of not. Cost accounting system

helps in inventory valuation, profitability and cost analysis. It help the manager to identify the

accurate cost of product which further helpful for the decision making process or develop various

strategies. Manager of EAM company follow this cost accounting system for controlling cost and

increase the profit margin (Schneider, 2015). For example: Manager prepare a retirement policy

for their clients so they fix the monthly premium of that particular plan and identify that whether

it is beneficial or not for the both parties. Manager identify that cost of policy can recover from

premium amount paid by the customer. Cost accounting system required to identify the product

& service cost which further helps in fixing product price of their financial services.

2

organisation.

financial records as income statement, balance

sheet and cash flow statement.

Different Type of management accounting system:

Management accounting system help the organisation to perform their duty effectively in

all department such as It, Finance, Marketing etc. Basically it is useful for the internal analysis

by use of financial information. It is focused on preparing strategies regarding operational

functions, cost of product & services or in decision making process (Sedevich Fons, 2012).

There are some different types of management accounting system which adopt by the manager of

Equilibrium Assets Management company that further helps in decision making process.

Inventory management system: It is a software which help to track inventory level or it

is very complex system to manage their inventory in the organisation but it help the business to

regularly track. It is beneficial for the medium or large size company. Manager of EAM

Company follow this system to manage their products through regular tracking of their supply

chain. This system help the business to identify the availability of their financial products. So it

is beneficial for the manager of EAM company to follow inventory management system or

software. For example: Company can manage their products such as investment, retirement, tax,

intergeneration planning etc. Manager of EAM follow this system to manage their product

information and provide their clients when it required. Inventory management system required to

manage the whole service products through this software which provide the accurate information

regarding this.

Cost accounting system: It is a costing framework which help the organisation to

identify the cost of each unit or it is beneficial or the business of not. Cost accounting system

helps in inventory valuation, profitability and cost analysis. It help the manager to identify the

accurate cost of product which further helpful for the decision making process or develop various

strategies. Manager of EAM company follow this cost accounting system for controlling cost and

increase the profit margin (Schneider, 2015). For example: Manager prepare a retirement policy

for their clients so they fix the monthly premium of that particular plan and identify that whether

it is beneficial or not for the both parties. Manager identify that cost of policy can recover from

premium amount paid by the customer. Cost accounting system required to identify the product

& service cost which further helps in fixing product price of their financial services.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price Optimization system: It is the process of identifying product price or increase the

willingness of consumers to pay more for their products. If product price is high then it is

conform that people will not buy their product & services. So it's a manager's responsibility to set

price of particular Goods & services which increase the sale with nominal profit margin. Price

optimization will be calculated according to the demand of their product, cost of each unit and

their competitors product & price level. Manager of EAM adopt this system and set the price of

their products such as different investment plans according to customer's will power to pay.

Requirement of price optimization system is to fix price of the services provided by the EAM

company to their customers.

P2 Different methods of management accounting reports

Management accounting report help the business to collect information from different

financial statement and prepare a report for the further decision making process. These reports

help the manager to build some effective strategies which help to achieve in business goals &

objectives. There are various report prepared by the manager of EAM company which is

discussed below:

Budget report: - It is an managerial accounting report which is used by the organisation

to measure their performance and build the report for the whole department wise (Schaltegger

and Zvezdov, 2015). Company prepare budget for the estimation of their project and after this

they will compare performances with the actual achievement for that particular duration.

Equilibrium Assets Management company prepare this budget report and it will include the

whole information regarding their project. Such as operational, sales or marketing activities

along with their estimated fund allotted to particular activity of functions. Manager of EAM

company build budget report which include the all activities and the time duration which

required to complete the task and they have fixed amount to spend on particular function. This

report build with the help of previous budget report and it will help the manager to compare their

actual performance with the standard one.

Performance report: - This report help the manager to measure the individual

performance of employee as well as organisation. In the business department performance report

also prepare by the manager for the identification of effective department work. Manager prepare

various strategies regarding with the help of performance report. EAM company build this report

and identify individual performance of their staff members as well as growth of the company in

3

willingness of consumers to pay more for their products. If product price is high then it is

conform that people will not buy their product & services. So it's a manager's responsibility to set

price of particular Goods & services which increase the sale with nominal profit margin. Price

optimization will be calculated according to the demand of their product, cost of each unit and

their competitors product & price level. Manager of EAM adopt this system and set the price of

their products such as different investment plans according to customer's will power to pay.

Requirement of price optimization system is to fix price of the services provided by the EAM

company to their customers.

P2 Different methods of management accounting reports

Management accounting report help the business to collect information from different

financial statement and prepare a report for the further decision making process. These reports

help the manager to build some effective strategies which help to achieve in business goals &

objectives. There are various report prepared by the manager of EAM company which is

discussed below:

Budget report: - It is an managerial accounting report which is used by the organisation

to measure their performance and build the report for the whole department wise (Schaltegger

and Zvezdov, 2015). Company prepare budget for the estimation of their project and after this

they will compare performances with the actual achievement for that particular duration.

Equilibrium Assets Management company prepare this budget report and it will include the

whole information regarding their project. Such as operational, sales or marketing activities

along with their estimated fund allotted to particular activity of functions. Manager of EAM

company build budget report which include the all activities and the time duration which

required to complete the task and they have fixed amount to spend on particular function. This

report build with the help of previous budget report and it will help the manager to compare their

actual performance with the standard one.

Performance report: - This report help the manager to measure the individual

performance of employee as well as organisation. In the business department performance report

also prepare by the manager for the identification of effective department work. Manager prepare

various strategies regarding with the help of performance report. EAM company build this report

and identify individual performance of their staff members as well as growth of the company in

3

the market on the basis on their operational functions. Such as investment or tax planning

services provided by the company to their clients and how effectively they perform their duty to

satisfy the customer's needs. After this report manager appropriate employees due to their good

performance to achieve business objectives & goals.

Other managerial accounting report: - It will include the project, competitor or other

reports which help the organisation to perform their task. This report prepare by the professionals

and it can be prepare through inter or outsider sources. Best way to use this report according to

the requirement of capability to handle the information. Manager of EAS prepare various report

to analyse competitors strategy with the comparison of their own company's strategies. It is

beneficial for the company to prepare different reports and compare with their rival firms. It will

provide the idea to manager to change their decision according to this report and develop

effective strategies which the organisation to achieve their business goals & objectives.

Cost managerial accounting report: - In this report organisation identify the cost of

their product & services and it include the all cost such as material, labour, overhead and any

other cost occur at the time of providing product & services (Rieckhof, Bergmann and Guenther,

2015). Manager of Equilibrium Assets Management company provide the financial services to

their customers. So company make sure that, the price of their product such as securities or

investment policies are cost effective in comparison to their competitors. This report help the

manager to reduce cost or control on regular basis which help them to achieve their business

objectives & task. Manager of EAM compare their policies price with their competitors and

build their strategies on the basis on this report.

M1 Evaluate the benefit of management accounting system

Management accounting system Benefits

Inventory management system Business can achieve high efficiency or

productivity by using this system.

By using this system manager save the

time as well as money that further

contribute in the growth of the

organisation.

Cost accounting system With the help of this manager can

4

services provided by the company to their clients and how effectively they perform their duty to

satisfy the customer's needs. After this report manager appropriate employees due to their good

performance to achieve business objectives & goals.

Other managerial accounting report: - It will include the project, competitor or other

reports which help the organisation to perform their task. This report prepare by the professionals

and it can be prepare through inter or outsider sources. Best way to use this report according to

the requirement of capability to handle the information. Manager of EAS prepare various report

to analyse competitors strategy with the comparison of their own company's strategies. It is

beneficial for the company to prepare different reports and compare with their rival firms. It will

provide the idea to manager to change their decision according to this report and develop

effective strategies which the organisation to achieve their business goals & objectives.

Cost managerial accounting report: - In this report organisation identify the cost of

their product & services and it include the all cost such as material, labour, overhead and any

other cost occur at the time of providing product & services (Rieckhof, Bergmann and Guenther,

2015). Manager of Equilibrium Assets Management company provide the financial services to

their customers. So company make sure that, the price of their product such as securities or

investment policies are cost effective in comparison to their competitors. This report help the

manager to reduce cost or control on regular basis which help them to achieve their business

objectives & task. Manager of EAM compare their policies price with their competitors and

build their strategies on the basis on this report.

M1 Evaluate the benefit of management accounting system

Management accounting system Benefits

Inventory management system Business can achieve high efficiency or

productivity by using this system.

By using this system manager save the

time as well as money that further

contribute in the growth of the

organisation.

Cost accounting system With the help of this manager can

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

easily identify the cost of each unit or

the overall expense of that particular

product & services.

Manger can identify the area of

inefficiency which will be improve by

controlling cost.

Price Optimization system This system work according to the

willingness of customer to pay product

price.

Manager have control all over the

pricing policy so they can take effective

decision regarding price and it will be

in favour if customer.

D1 How management accounting system or management accounting report integrated with each

other

Management accounting system or reporting both are linked with each other the business

process such as cost accounting, price optimization etc. they all integrated with different

accounting reports such as performance report, cost managerial accounting report etc. system or

report both are linked with each other due to the various functions or activities perform by the

employees in the organisation. For example budget report required various financial information

through accounting systems. Same as accounting system required different managerial reports

which help them to perform. So basically in the EAM company, management accounting system

or report linked with each other because of their functions.

TASK 2

P3 Various costing techniques to prepare an income statement

Marginal costing: This type of costing means the total cost of the additional or the

marginal unit produced by companies in a specific time frame (Ratnatunga, Michael and

Balachandran, 2012.). In accounting term, it is defined as cost of one more unit of product

besides the existing level of manufacture. The marginal cost basically varies with the direct

5

the overall expense of that particular

product & services.

Manger can identify the area of

inefficiency which will be improve by

controlling cost.

Price Optimization system This system work according to the

willingness of customer to pay product

price.

Manager have control all over the

pricing policy so they can take effective

decision regarding price and it will be

in favour if customer.

D1 How management accounting system or management accounting report integrated with each

other

Management accounting system or reporting both are linked with each other the business

process such as cost accounting, price optimization etc. they all integrated with different

accounting reports such as performance report, cost managerial accounting report etc. system or

report both are linked with each other due to the various functions or activities perform by the

employees in the organisation. For example budget report required various financial information

through accounting systems. Same as accounting system required different managerial reports

which help them to perform. So basically in the EAM company, management accounting system

or report linked with each other because of their functions.

TASK 2

P3 Various costing techniques to prepare an income statement

Marginal costing: This type of costing means the total cost of the additional or the

marginal unit produced by companies in a specific time frame (Ratnatunga, Michael and

Balachandran, 2012.). In accounting term, it is defined as cost of one more unit of product

besides the existing level of manufacture. The marginal cost basically varies with the direct

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

impact of level of goods produced. Fox example, cost related to direct material, variable cost and

direct labour. Thus this cost do not consists any elements of fixed cost.

Absorption costing: This kind of costing comprises of cost of goods manufactured such

as direct material, labour, fixed and variable factory overheads. With the help of this methods

cost to product are charge fairly as it support to cover all relevant manufacturing cost.

Actual costing system- Actual costing is a method of calculating the cost that occurs in

the final production including the actual cost like labour cost, material cost etc.

Normal costing system- Normal costing system is used to compute the cost of product

with the use of material, labour and manufacturing overhead. Herein, these three costs referred as

the product cost and use for further purposes like inventory evaluation etc.

Standard costing system- Standard costing system is also known by the target costing

system. In this system future cost of products and services are estimated on the basis of past

historical data. The purpose of this system is to control over the cost.

Cost system differs from the job costing, process costing, batch and process costing.

Cost system Job costing Process costing Batch costing Contract costing

Cost system is a

kind of system

which is related

to calculating the

cost of different

products and

services. It

includes various

systems in itself.

Job costing

system is a

method

calculating the

each unit of cost

on the basis of the

each job assigned

in the production

process.

Process costing

system is useful

in calculating the

costs which

occurs in the

different process

of production. It

is suitable for

those

organisations

which offers a

wide range of

products and

services.

Batch costing

system is similar

to the job costing

system in which

products are

categorised into

different batches.

This helps in

calculating the

cost of each unit

on the basis of

each batch.

Contract costing

is a tool of

computing the

cost of different

projects.

Basically, this

costing system is

useful for the

civil projects,

railway projects

etc. Main purpose

of this system is

to control the cost

of contract or

6

direct labour. Thus this cost do not consists any elements of fixed cost.

Absorption costing: This kind of costing comprises of cost of goods manufactured such

as direct material, labour, fixed and variable factory overheads. With the help of this methods

cost to product are charge fairly as it support to cover all relevant manufacturing cost.

Actual costing system- Actual costing is a method of calculating the cost that occurs in

the final production including the actual cost like labour cost, material cost etc.

Normal costing system- Normal costing system is used to compute the cost of product

with the use of material, labour and manufacturing overhead. Herein, these three costs referred as

the product cost and use for further purposes like inventory evaluation etc.

Standard costing system- Standard costing system is also known by the target costing

system. In this system future cost of products and services are estimated on the basis of past

historical data. The purpose of this system is to control over the cost.

Cost system differs from the job costing, process costing, batch and process costing.

Cost system Job costing Process costing Batch costing Contract costing

Cost system is a

kind of system

which is related

to calculating the

cost of different

products and

services. It

includes various

systems in itself.

Job costing

system is a

method

calculating the

each unit of cost

on the basis of the

each job assigned

in the production

process.

Process costing

system is useful

in calculating the

costs which

occurs in the

different process

of production. It

is suitable for

those

organisations

which offers a

wide range of

products and

services.

Batch costing

system is similar

to the job costing

system in which

products are

categorised into

different batches.

This helps in

calculating the

cost of each unit

on the basis of

each batch.

Contract costing

is a tool of

computing the

cost of different

projects.

Basically, this

costing system is

useful for the

civil projects,

railway projects

etc. Main purpose

of this system is

to control the cost

of contract or

6

projects.

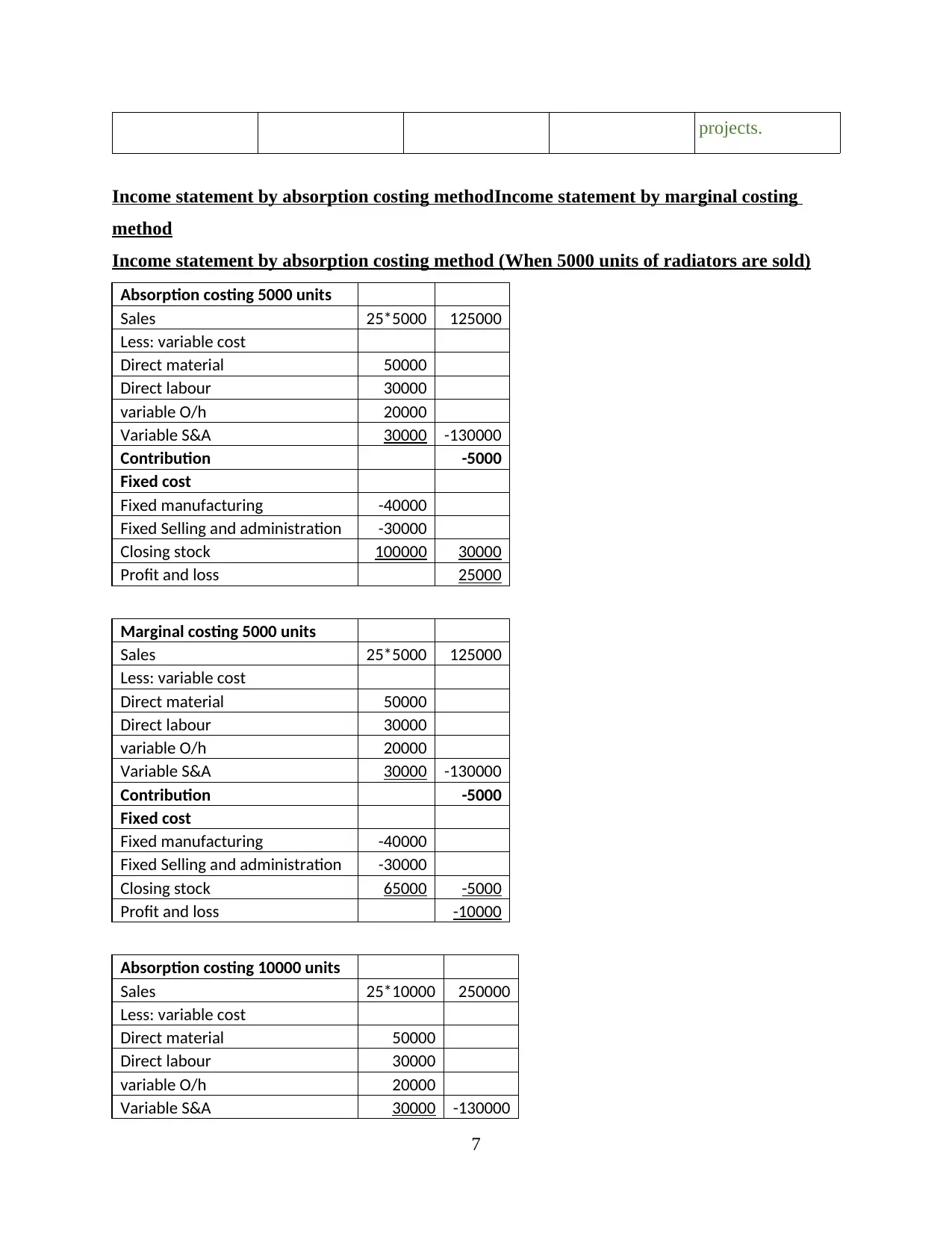

Income statement by absorption costing methodIncome statement by marginal costing

method

Income statement by absorption costing method (When 5000 units of radiators are sold)

Absorption costing 5000 units

Sales 25*5000 125000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution -5000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000

Closing stock 100000 30000

Profit and loss 25000

Marginal costing 5000 units

Sales 25*5000 125000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution -5000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000

Closing stock 65000 -5000

Profit and loss -10000

Absorption costing 10000 units

Sales 25*10000 250000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

7

Income statement by absorption costing methodIncome statement by marginal costing

method

Income statement by absorption costing method (When 5000 units of radiators are sold)

Absorption costing 5000 units

Sales 25*5000 125000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution -5000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000

Closing stock 100000 30000

Profit and loss 25000

Marginal costing 5000 units

Sales 25*5000 125000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution -5000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000

Closing stock 65000 -5000

Profit and loss -10000

Absorption costing 10000 units

Sales 25*10000 250000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

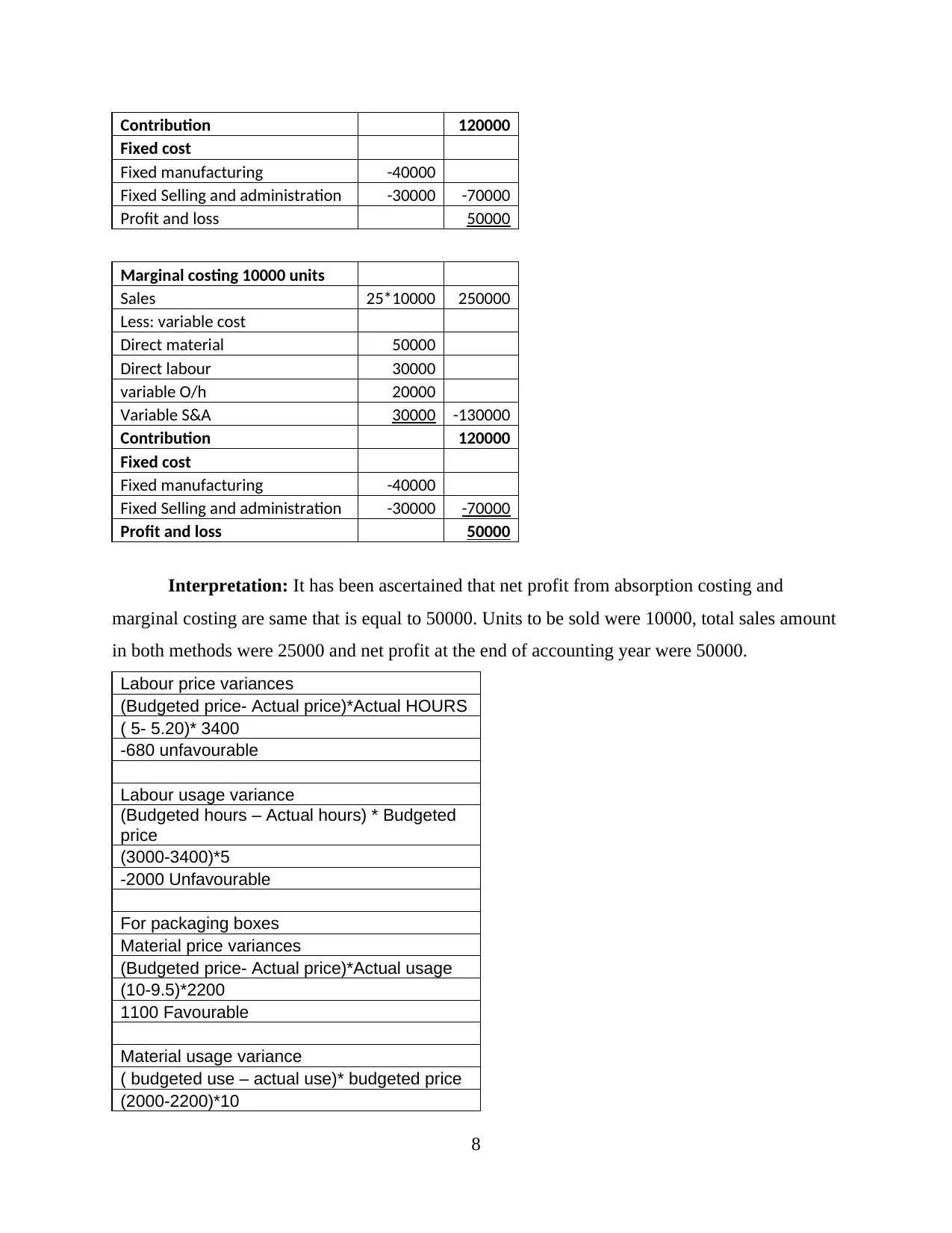

Contribution 120000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000 -70000

Profit and loss 50000

Marginal costing 10000 units

Sales 25*10000 250000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution 120000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000 -70000

Profit and loss 50000

Interpretation: It has been ascertained that net profit from absorption costing and

marginal costing are same that is equal to 50000. Units to be sold were 10000, total sales amount

in both methods were 25000 and net profit at the end of accounting year were 50000.

Labour price variances

(Budgeted price- Actual price)*Actual HOURS

( 5- 5.20)* 3400

-680 unfavourable

Labour usage variance

(Budgeted hours – Actual hours) * Budgeted

price

(3000-3400)*5

-2000 Unfavourable

For packaging boxes

Material price variances

(Budgeted price- Actual price)*Actual usage

(10-9.5)*2200

1100 Favourable

Material usage variance

( budgeted use – actual use)* budgeted price

(2000-2200)*10

8

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000 -70000

Profit and loss 50000

Marginal costing 10000 units

Sales 25*10000 250000

Less: variable cost

Direct material 50000

Direct labour 30000

variable O/h 20000

Variable S&A 30000 -130000

Contribution 120000

Fixed cost

Fixed manufacturing -40000

Fixed Selling and administration -30000 -70000

Profit and loss 50000

Interpretation: It has been ascertained that net profit from absorption costing and

marginal costing are same that is equal to 50000. Units to be sold were 10000, total sales amount

in both methods were 25000 and net profit at the end of accounting year were 50000.

Labour price variances

(Budgeted price- Actual price)*Actual HOURS

( 5- 5.20)* 3400

-680 unfavourable

Labour usage variance

(Budgeted hours – Actual hours) * Budgeted

price

(3000-3400)*5

-2000 Unfavourable

For packaging boxes

Material price variances

(Budgeted price- Actual price)*Actual usage

(10-9.5)*2200

1100 Favourable

Material usage variance

( budgeted use – actual use)* budgeted price

(2000-2200)*10

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-2000 Unfavourable

M2 Range of management accounting techniques

Management accounting techniques help the business to identify the potential area to

increase their profit margin. It will include the various management technique which used by the

Equilibrium Assets Management company in their organisation for the effectiveness of work. It

will help the business to achieve their business objectives or goals. Some of the techniques

discussed below:

Historical cost accounting: - In this accounting technique identify the value which is

originally listed in the balance sheet of the company (Mussnig, 2013). So manager of the

company can take important decision on the basis of historical value of assets. Manager of the

EAM company follow this technique to measure the asset value that further help in decision

making process.

Financial planning: - It required analytical skills to reduce the risk by using this

techniques. It will include the planning of the business finance. It is the important technique

because it include the planning regarding money which is confidential information of the

business. So manager of EAM use this financial planning techniques which help the company to

build their future plan on the basis of this techniques.

D2 Financial reports which applies to interpret many business activities

Financial report include the all business activities in the terms of financial statements

such as profit & loss account or balance sheet. It is important for the organisation because it

include the all business activities or functions. Income statement or balance sheet help the

organisation to interpret data in profitable way. Without this information, manager not able to

take any decision and the users of these financial reports not showing their interest in the

organisation. So basically without financial reports organisation not able to interpret their

activities or functions. Equilibrium Assets Management company use the various financial

reports which help the interpret data such as use of profit and loss statements provide accurate

information regarding business earn profit or loss. Further it will help the manger to build other

financial statements such as balance sheet or cash flow (Moore, 2014).

9

M2 Range of management accounting techniques

Management accounting techniques help the business to identify the potential area to

increase their profit margin. It will include the various management technique which used by the

Equilibrium Assets Management company in their organisation for the effectiveness of work. It

will help the business to achieve their business objectives or goals. Some of the techniques

discussed below:

Historical cost accounting: - In this accounting technique identify the value which is

originally listed in the balance sheet of the company (Mussnig, 2013). So manager of the

company can take important decision on the basis of historical value of assets. Manager of the

EAM company follow this technique to measure the asset value that further help in decision

making process.

Financial planning: - It required analytical skills to reduce the risk by using this

techniques. It will include the planning of the business finance. It is the important technique

because it include the planning regarding money which is confidential information of the

business. So manager of EAM use this financial planning techniques which help the company to

build their future plan on the basis of this techniques.

D2 Financial reports which applies to interpret many business activities

Financial report include the all business activities in the terms of financial statements

such as profit & loss account or balance sheet. It is important for the organisation because it

include the all business activities or functions. Income statement or balance sheet help the

organisation to interpret data in profitable way. Without this information, manager not able to

take any decision and the users of these financial reports not showing their interest in the

organisation. So basically without financial reports organisation not able to interpret their

activities or functions. Equilibrium Assets Management company use the various financial

reports which help the interpret data such as use of profit and loss statements provide accurate

information regarding business earn profit or loss. Further it will help the manger to build other

financial statements such as balance sheet or cash flow (Moore, 2014).

9

TASK 3

P4 Various kind of planning tool with its advantages and disadvantage

Budgetary control: This method support in creating and implementing different plans,

strategies in order to run business operation in effective manner so that long term financial

sustainability can be maintained. With the use of formulated budgets management are able to

measure actual result in order to determine the negative reasons if any. Thus the internal manager

of equilibrium assets management use to prepare budgets to improve the budgetary control

process and improve the business operation. There are various planning tool that are used in

budgetary control process these are discussed below:

Budgets: It is a methods used by business organisation in order to estimate incomes and

expenses within a certain time frame. Budgets provides clarification to internal manager to

forecast result and financial status in future time. It is observed that budgets are embattled by

using last year data and actual market trends that is use to set the targets for upcoming time.

Various advantages and disadvantage of budgets are discussed below:

Advantages:

It support to provide proper guidelines that are connected with cost further linked with

different transactions.

It is an effective tool so that income and expenses are controlled in future time.

Disadvantages:

The main disadvantage is that it is based on assumptions that sometime lead to wrong

decision.

Sometime there are unplanned expenses within organisation that are not budgeted and

reduces profitability (Modell, 2012).

Flexible budgets: This type of budgets mainly varies with the change in the volume or

production of activity. It is termed as variable budgets as it is prepared for activities that are

variable in nature. Management of EAM makes modification in flexible budgets as per the

requirements to manage the variable activities and makes changes in order to improve the

performance. Some benefits and drawbacks are discussed below:

Advantages:

The main strength of this budgets is that it support an organisation to brings coordination

between assorted activities.

10

P4 Various kind of planning tool with its advantages and disadvantage

Budgetary control: This method support in creating and implementing different plans,

strategies in order to run business operation in effective manner so that long term financial

sustainability can be maintained. With the use of formulated budgets management are able to

measure actual result in order to determine the negative reasons if any. Thus the internal manager

of equilibrium assets management use to prepare budgets to improve the budgetary control

process and improve the business operation. There are various planning tool that are used in

budgetary control process these are discussed below:

Budgets: It is a methods used by business organisation in order to estimate incomes and

expenses within a certain time frame. Budgets provides clarification to internal manager to

forecast result and financial status in future time. It is observed that budgets are embattled by

using last year data and actual market trends that is use to set the targets for upcoming time.

Various advantages and disadvantage of budgets are discussed below:

Advantages:

It support to provide proper guidelines that are connected with cost further linked with

different transactions.

It is an effective tool so that income and expenses are controlled in future time.

Disadvantages:

The main disadvantage is that it is based on assumptions that sometime lead to wrong

decision.

Sometime there are unplanned expenses within organisation that are not budgeted and

reduces profitability (Modell, 2012).

Flexible budgets: This type of budgets mainly varies with the change in the volume or

production of activity. It is termed as variable budgets as it is prepared for activities that are

variable in nature. Management of EAM makes modification in flexible budgets as per the

requirements to manage the variable activities and makes changes in order to improve the

performance. Some benefits and drawbacks are discussed below:

Advantages:

The main strength of this budgets is that it support an organisation to brings coordination

between assorted activities.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.