Comprehensive Management Accounting Report: Ryder Architecture

VerifiedAdded on 2021/02/19

|15

|4917

|147

Report

AI Summary

This report delves into the realm of management accounting, focusing on its practical application within Ryder Architecture, a construction company. It begins by defining management accounting and its essential requirements, emphasizing its role in internal decision-making and financial performance analysis. The report then explores various management accounting systems implemented at Ryder Architecture, including cost accounting, inventory management, price optimization, and job order costing systems. It also examines different management accounting reporting methods, such as performance reports, budget reports, account receivable reports, and inventory management reports, highlighting their benefits and applications. Furthermore, the report analyzes the advantages and disadvantages of planning tools used for budgetary control, providing insights into their effectiveness in forecasting and budget preparation. The study further covers the calculation of costs using marginal costing techniques and the application of different costing methods. Finally, the report discusses how organizations adapt management accounting systems to respond to financial problems and achieve sustainable success, along with an evaluation of these systems and their reporting methods.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Management accounting and essential requirements of its systems.......................................4

P2 Different methods used for management accounting reporting.............................................6

M1 benefits of management accounting systems and their application......................................7

D1 Evaluation of management accounting systems and management accounting reporting......7

TASK 2............................................................................................................................................8

P3 Calculation of cost using different costing techniques...........................................................8

M2 Range of management accounting techniques......................................................................9

D2 Financial reports that accurately apply and interpret data ....................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different planning tool used for budgetary control..........9

M3 Use of different planning tools and their application for preparing and forecasting budgets

....................................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................10

M4 Responding to financial problems that lead organisations to sustainable success..............11

D3 Planning tools for accounting respond appropriately to solving financial problems...........12

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Management accounting and essential requirements of its systems.......................................4

P2 Different methods used for management accounting reporting.............................................6

M1 benefits of management accounting systems and their application......................................7

D1 Evaluation of management accounting systems and management accounting reporting......7

TASK 2............................................................................................................................................8

P3 Calculation of cost using different costing techniques...........................................................8

M2 Range of management accounting techniques......................................................................9

D2 Financial reports that accurately apply and interpret data ....................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different planning tool used for budgetary control..........9

M3 Use of different planning tools and their application for preparing and forecasting budgets

....................................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................10

M4 Responding to financial problems that lead organisations to sustainable success..............11

D3 Planning tools for accounting respond appropriately to solving financial problems...........12

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION

Management accounting can be described as the method of maintaining the company's

inner data records in order to develop policy decisions for organizational improvement. In simple

words, it is recognized as the scheme of recoding, analysing and using financial and non-

financial information as concentrates on skills and enables the organization increase its profit by

reducing general operating costs and other activities (Abernethy, Bouwens and Van Lent, 2010).

It also allows executives to expand businesses by discovering fresh methods to boost revenues.

Management accounting also helps internal stakeholders in a way executives, staff might easily

analyse the performance of a company within the market and support external stakeholders in

order to determine the actual and real financial status of company. In order to recognise the

importance of management accounting Ryder Architecture have been selected that is a

construction company in UK and is client Equilibrium Asset Management the famous medium-

sized consultancy firm.

This reports includes multiple subjects like management accounting system and

importance, reporting, structures and using multiple costing techniques to measure cost of

production. Apart this benefits and drawbacks of planning instruments which are part of

budgetary control are also being discussed. This study also covers the manner businesses use

management accounting schemes to react to economic issues.

TASK 1

P1 Management accounting and essential requirements of its systems.

Management Accounting is a method of analysing and sharing crucial organizational

information with manager and responsible executives which enable them to monitor business

performance and to develop approaches to improve their efficiency. It has several advantages

that help in projections and serve a vital part in deciding on the purchase or selling of certain

investments that are beneficial for company. There have been number of management

accounting system that are used by the manager of company in order to maintain a proper record

of various crucial operational and functional section (Arena, Arnaboldi and Azzone, 2010). In

Ryder Architecture several types of system have been implemented which help their stakeholders

to easily assess the overall financial stability and strength. These system are elaborated

underneath:

Management accounting can be described as the method of maintaining the company's

inner data records in order to develop policy decisions for organizational improvement. In simple

words, it is recognized as the scheme of recoding, analysing and using financial and non-

financial information as concentrates on skills and enables the organization increase its profit by

reducing general operating costs and other activities (Abernethy, Bouwens and Van Lent, 2010).

It also allows executives to expand businesses by discovering fresh methods to boost revenues.

Management accounting also helps internal stakeholders in a way executives, staff might easily

analyse the performance of a company within the market and support external stakeholders in

order to determine the actual and real financial status of company. In order to recognise the

importance of management accounting Ryder Architecture have been selected that is a

construction company in UK and is client Equilibrium Asset Management the famous medium-

sized consultancy firm.

This reports includes multiple subjects like management accounting system and

importance, reporting, structures and using multiple costing techniques to measure cost of

production. Apart this benefits and drawbacks of planning instruments which are part of

budgetary control are also being discussed. This study also covers the manner businesses use

management accounting schemes to react to economic issues.

TASK 1

P1 Management accounting and essential requirements of its systems.

Management Accounting is a method of analysing and sharing crucial organizational

information with manager and responsible executives which enable them to monitor business

performance and to develop approaches to improve their efficiency. It has several advantages

that help in projections and serve a vital part in deciding on the purchase or selling of certain

investments that are beneficial for company. There have been number of management

accounting system that are used by the manager of company in order to maintain a proper record

of various crucial operational and functional section (Arena, Arnaboldi and Azzone, 2010). In

Ryder Architecture several types of system have been implemented which help their stakeholders

to easily assess the overall financial stability and strength. These system are elaborated

underneath:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: This system helping the company managers to analyse various

costs associated with different operations of manufacturing that directly support the company to

increase overall profit by a good margin by determining and eliminating wastage or unnecessary

activities. In Ryder Architecture manager uses this system to keeps records of immediate and

indirect company costs to maintain detail information on all expenditures linked to construction

and other facilities. With the support of this system company is able to add value to their

operation and activities by making decision related to reducing of expenses utilised within a

specific year.

Inventory management system: It is used primarily in manufacturing businesses to

properly handle inventory. This system also provides data on the correct amount of products to

be stored by an organization to help resolve supply chain issues. In Ryder Architecture manager,

this scheme is being used to keep track of all materials which is use for the constructing different

products. There have been three distinct kinds of LIFO, FIFO and AVCO inventory management

systems. In respective firm FIFO method is being used for building purposes because contracting

things are always on the need of customer and according to the latest trend of market.

Price optimisation system: As name suggests, it is primarily used to fix best possible

rates for all the goods the organization manufactures. This process performs a main part in

creating price-related decisions for different products that demonstrate to be the greatest for both

clients and business. This have been observed that consumers never purchase a product it the

prices are higher for them. In Ryder Architecture manager uses this system for the purpose to

establish the most appropriate and suitable prices for each and every buildings that are build for

the purpose of trading to customers. This system is essential and adds importance to the

respective firm as it helps to analyse whether or not the cost fixed can satisfy customer

expectations.

Job order costing system: This scheme used to allocate and collect costs that are

incurred by company on different valuable jobs which are involved in various operation. With

the help of this system, management of Ryder Architecture are able to assign cost to each and

every job related with constructing different building. It is very essential for organization to

analyse the price of various products that are being produced as per the consumer specifications.

This system helps to add value to respective firm because it helps to determine cost of each and

costs associated with different operations of manufacturing that directly support the company to

increase overall profit by a good margin by determining and eliminating wastage or unnecessary

activities. In Ryder Architecture manager uses this system to keeps records of immediate and

indirect company costs to maintain detail information on all expenditures linked to construction

and other facilities. With the support of this system company is able to add value to their

operation and activities by making decision related to reducing of expenses utilised within a

specific year.

Inventory management system: It is used primarily in manufacturing businesses to

properly handle inventory. This system also provides data on the correct amount of products to

be stored by an organization to help resolve supply chain issues. In Ryder Architecture manager,

this scheme is being used to keep track of all materials which is use for the constructing different

products. There have been three distinct kinds of LIFO, FIFO and AVCO inventory management

systems. In respective firm FIFO method is being used for building purposes because contracting

things are always on the need of customer and according to the latest trend of market.

Price optimisation system: As name suggests, it is primarily used to fix best possible

rates for all the goods the organization manufactures. This process performs a main part in

creating price-related decisions for different products that demonstrate to be the greatest for both

clients and business. This have been observed that consumers never purchase a product it the

prices are higher for them. In Ryder Architecture manager uses this system for the purpose to

establish the most appropriate and suitable prices for each and every buildings that are build for

the purpose of trading to customers. This system is essential and adds importance to the

respective firm as it helps to analyse whether or not the cost fixed can satisfy customer

expectations.

Job order costing system: This scheme used to allocate and collect costs that are

incurred by company on different valuable jobs which are involved in various operation. With

the help of this system, management of Ryder Architecture are able to assign cost to each and

every job related with constructing different building. It is very essential for organization to

analyse the price of various products that are being produced as per the consumer specifications.

This system helps to add value to respective firm because it helps to determine cost of each and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

every jobs that are part of constructing operation so that actual price can be disclosed to customer

by considering to recover the total job cost (Jiang, Petroni and Wang, 2010).

P2 Different methods used for management accounting reporting

Management accounting reporting can be described as the method of producing various

significant reports covering reliable and authentic data about the overall performance of the

organization. There have been different method of reporting that are being used in Ryder

Architecture recommended by Equilibrium Asset Management which support in preserving

useful report of company. These are discussed underneath:

Performance report: This report is produced primarily used to maintain record related

with company's activities and employees performance during a specific time period. It is used by

the manager of Ryder Architecture to record, measure and make advance steps to improve the

performance of staff and businesses if its is necessary. It's used in organization to provide

bonuses and rewards to employees in accordance to their attempts to achieve the specific task

they have been assigned. This report is helpful to the company as it allows to create effective

methods to enhance its effectiveness. In case if this report is not made by the company, they

would never understand how their staff perform certain task and what error they make within

specific span of moment.

Budget report: From reporting perspective the budget report is most prevalent. This

report is essential as it provides all the data about the job and results of the company as well as

reveals both anticipated and real revenue and expense (Kallunki, Laitinen and Silvola, 2011). It

is an internal document that organizations use to allocate revenue to the various practical and

administrative departments. Managers use it to compare Ryder Architecture's real and normal

expenditure in order to evaluate its efficiency. It is useful for the company as it enables them to

allocate budget that ease to perform all company operations.

Account receivable report: This report is designed to find the actual and total amount

debtors are going to deliver to the business. It includes complete information of how much cash

is outstanding for company that has to be received up to a specific date and what is the origin of

these resources. This report aid to create to list of different customer those owed amount

company. It is produced primarily by companies offering goods on credit to clients in order to

increase sales for that specific period. It is used by staff in the corresponding company to

maintain track of all the outstanding amount that is needed to be collected from customers. With

by considering to recover the total job cost (Jiang, Petroni and Wang, 2010).

P2 Different methods used for management accounting reporting

Management accounting reporting can be described as the method of producing various

significant reports covering reliable and authentic data about the overall performance of the

organization. There have been different method of reporting that are being used in Ryder

Architecture recommended by Equilibrium Asset Management which support in preserving

useful report of company. These are discussed underneath:

Performance report: This report is produced primarily used to maintain record related

with company's activities and employees performance during a specific time period. It is used by

the manager of Ryder Architecture to record, measure and make advance steps to improve the

performance of staff and businesses if its is necessary. It's used in organization to provide

bonuses and rewards to employees in accordance to their attempts to achieve the specific task

they have been assigned. This report is helpful to the company as it allows to create effective

methods to enhance its effectiveness. In case if this report is not made by the company, they

would never understand how their staff perform certain task and what error they make within

specific span of moment.

Budget report: From reporting perspective the budget report is most prevalent. This

report is essential as it provides all the data about the job and results of the company as well as

reveals both anticipated and real revenue and expense (Kallunki, Laitinen and Silvola, 2011). It

is an internal document that organizations use to allocate revenue to the various practical and

administrative departments. Managers use it to compare Ryder Architecture's real and normal

expenditure in order to evaluate its efficiency. It is useful for the company as it enables them to

allocate budget that ease to perform all company operations.

Account receivable report: This report is designed to find the actual and total amount

debtors are going to deliver to the business. It includes complete information of how much cash

is outstanding for company that has to be received up to a specific date and what is the origin of

these resources. This report aid to create to list of different customer those owed amount

company. It is produced primarily by companies offering goods on credit to clients in order to

increase sales for that specific period. It is used by staff in the corresponding company to

maintain track of all the outstanding amount that is needed to be collected from customers. With

the assistance of it, the company can strengthen its credit strategies so that customers can

overlook the condition of early payment.

Inventory management report: This report is mainly produced to maintain record total

inventory that is being hold and preserve by manufacturing firm to meet the certain demand of

customer. It Ryder Architecture manager use to create inventory report with the intention to

keep a valid record of total material required to construct building for customers and goods that

has been put in production process. The main benefit of this report is that it can overcome some

of the significant problems associated with overstocking and under-stocking products. It is

beneficial for respective company as it aids to verify inventory position whether it is in

warehouse, service or supplied to customers.

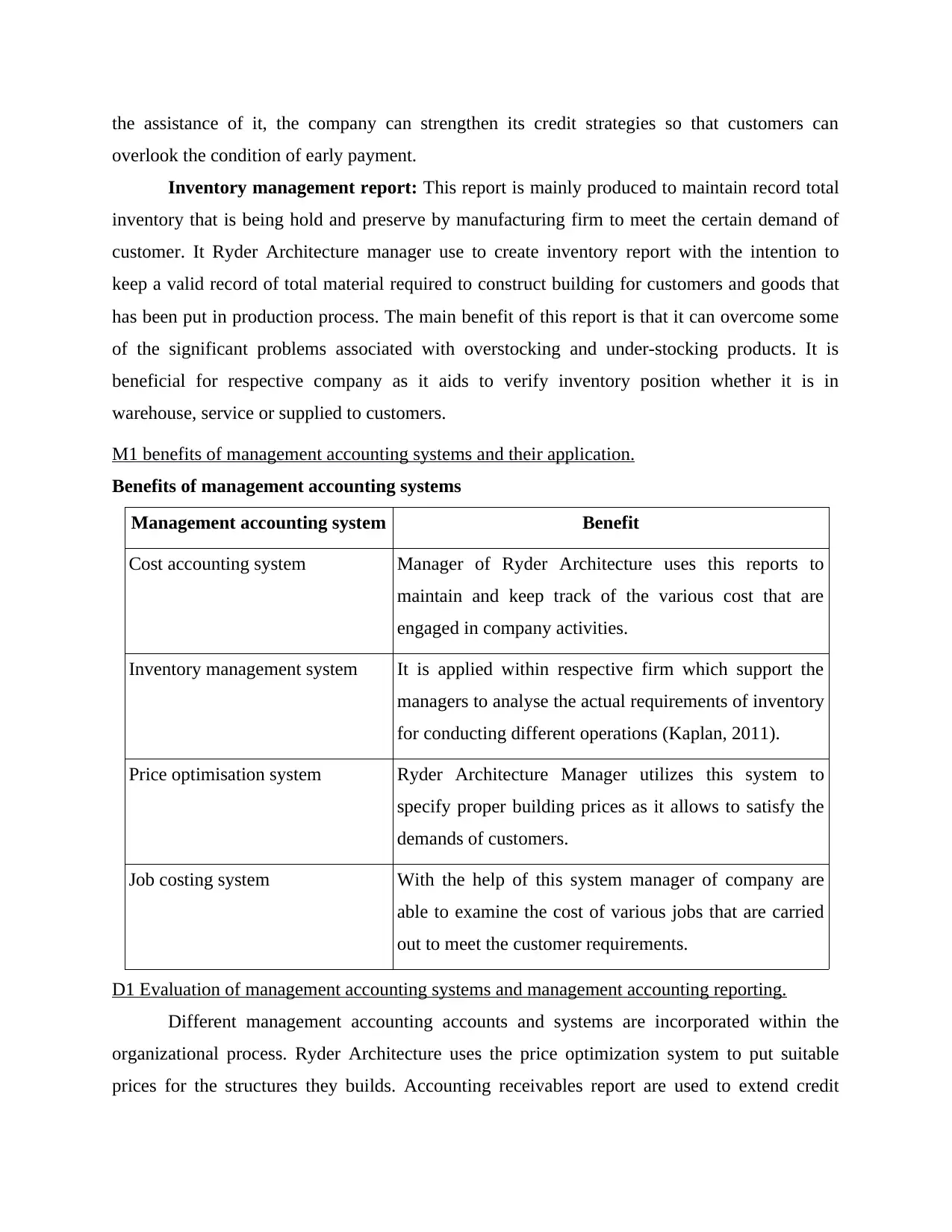

M1 benefits of management accounting systems and their application.

Benefits of management accounting systems

Management accounting system Benefit

Cost accounting system Manager of Ryder Architecture uses this reports to

maintain and keep track of the various cost that are

engaged in company activities.

Inventory management system It is applied within respective firm which support the

managers to analyse the actual requirements of inventory

for conducting different operations (Kaplan, 2011).

Price optimisation system Ryder Architecture Manager utilizes this system to

specify proper building prices as it allows to satisfy the

demands of customers.

Job costing system With the help of this system manager of company are

able to examine the cost of various jobs that are carried

out to meet the customer requirements.

D1 Evaluation of management accounting systems and management accounting reporting.

Different management accounting accounts and systems are incorporated within the

organizational process. Ryder Architecture uses the price optimization system to put suitable

prices for the structures they builds. Accounting receivables report are used to extend credit

overlook the condition of early payment.

Inventory management report: This report is mainly produced to maintain record total

inventory that is being hold and preserve by manufacturing firm to meet the certain demand of

customer. It Ryder Architecture manager use to create inventory report with the intention to

keep a valid record of total material required to construct building for customers and goods that

has been put in production process. The main benefit of this report is that it can overcome some

of the significant problems associated with overstocking and under-stocking products. It is

beneficial for respective company as it aids to verify inventory position whether it is in

warehouse, service or supplied to customers.

M1 benefits of management accounting systems and their application.

Benefits of management accounting systems

Management accounting system Benefit

Cost accounting system Manager of Ryder Architecture uses this reports to

maintain and keep track of the various cost that are

engaged in company activities.

Inventory management system It is applied within respective firm which support the

managers to analyse the actual requirements of inventory

for conducting different operations (Kaplan, 2011).

Price optimisation system Ryder Architecture Manager utilizes this system to

specify proper building prices as it allows to satisfy the

demands of customers.

Job costing system With the help of this system manager of company are

able to examine the cost of various jobs that are carried

out to meet the customer requirements.

D1 Evaluation of management accounting systems and management accounting reporting.

Different management accounting accounts and systems are incorporated within the

organizational process. Ryder Architecture uses the price optimization system to put suitable

prices for the structures they builds. Accounting receivables report are used to extend credit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

strategies by evaluating separate customers complete quantity due. It has been also critically

evaluated that performance report is also used to record and improve the performance of

employees which support to search the desired target.

TASK 2

P3 Calculation of cost using different costing techniques.

In general, the cost is defined as anything that have been spent by an individual to get

something. In business term the word cost defines the total expenses an organisation incurred in

producing useful product or services. In Ryder Architecture, the manager spend huge amount on

constructing different building as per the needs of customer. There are various costing methods

that have been used by the manager of company in order to calculate the total cost incurred by

company on different operation. This also support to prepare income statements for the specific

accounting year so that actual net profit for the year can be calculated. Some of these methods

are as follows:

Marginal costing: The cost that have been spend on producing an extra unit of output

and it support in making short term decision is known as marginal costing. It is determined as the

percentage by which overall expenses are altered at any specified production volume if the

production volume is improved or reduced by one unit.

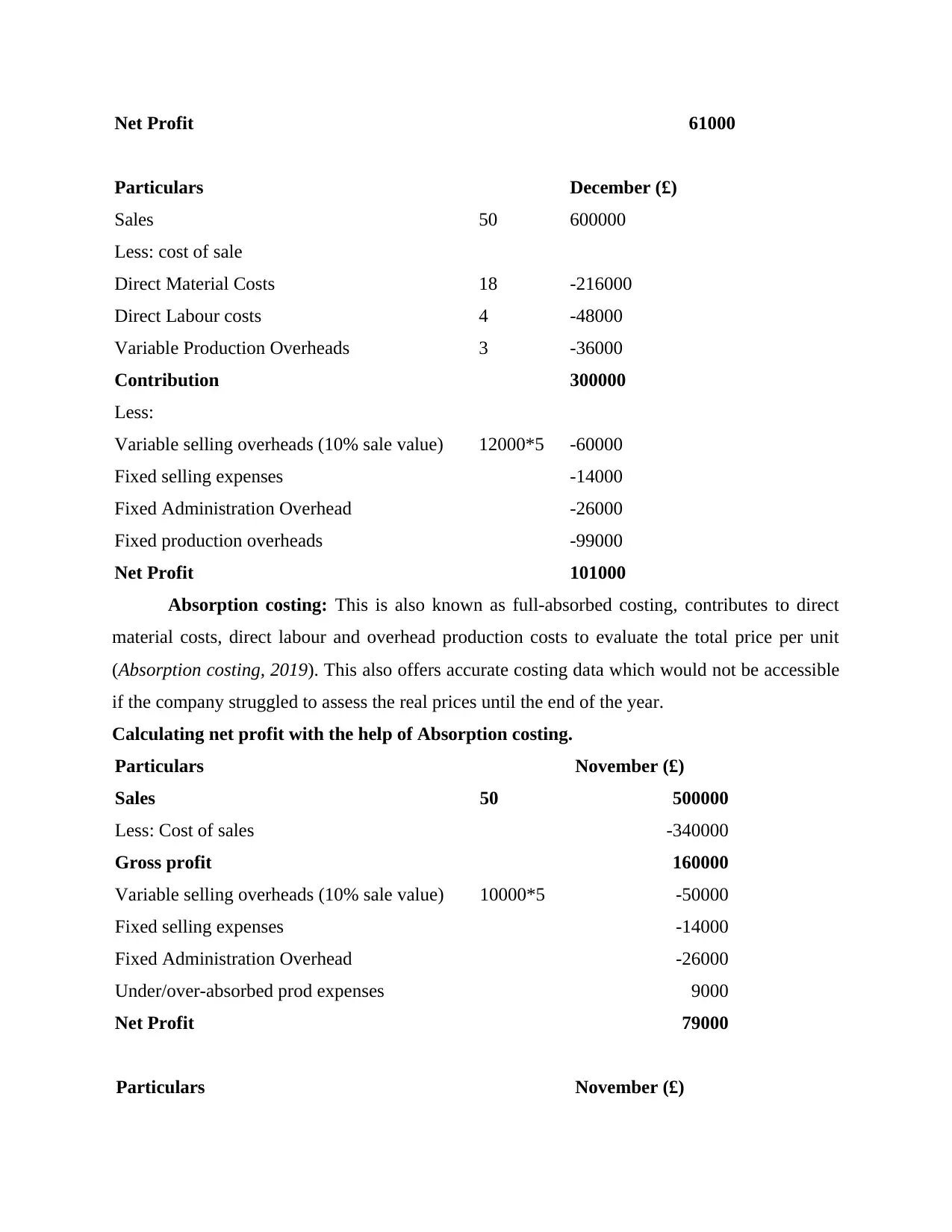

Calculating net profit with the help of Marginal costing.

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

evaluated that performance report is also used to record and improve the performance of

employees which support to search the desired target.

TASK 2

P3 Calculation of cost using different costing techniques.

In general, the cost is defined as anything that have been spent by an individual to get

something. In business term the word cost defines the total expenses an organisation incurred in

producing useful product or services. In Ryder Architecture, the manager spend huge amount on

constructing different building as per the needs of customer. There are various costing methods

that have been used by the manager of company in order to calculate the total cost incurred by

company on different operation. This also support to prepare income statements for the specific

accounting year so that actual net profit for the year can be calculated. Some of these methods

are as follows:

Marginal costing: The cost that have been spend on producing an extra unit of output

and it support in making short term decision is known as marginal costing. It is determined as the

percentage by which overall expenses are altered at any specified production volume if the

production volume is improved or reduced by one unit.

Calculating net profit with the help of Marginal costing.

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit 61000

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing: This is also known as full-absorbed costing, contributes to direct

material costs, direct labour and overhead production costs to evaluate the total price per unit

(Absorption costing, 2019). This also offers accurate costing data which would not be accessible

if the company struggled to assess the real prices until the end of the year.

Calculating net profit with the help of Absorption costing.

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over-absorbed prod expenses 9000

Net Profit 79000

Particulars November (£)

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing: This is also known as full-absorbed costing, contributes to direct

material costs, direct labour and overhead production costs to evaluate the total price per unit

(Absorption costing, 2019). This also offers accurate costing data which would not be accessible

if the company struggled to assess the real prices until the end of the year.

Calculating net profit with the help of Absorption costing.

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over-absorbed prod expenses 9000

Net Profit 79000

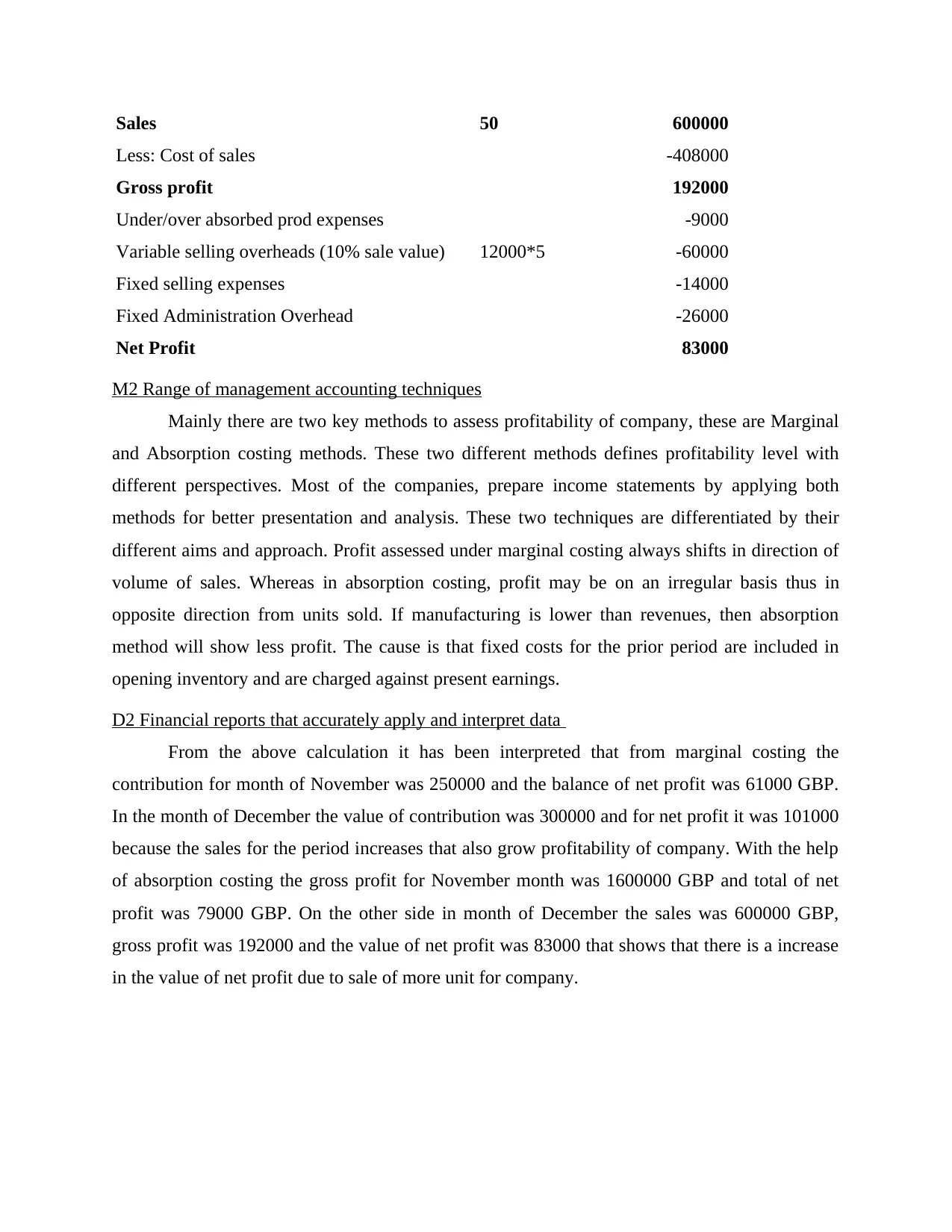

Particulars November (£)

Sales 50 600000

Less: Cost of sales -408000

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

M2 Range of management accounting techniques

Mainly there are two key methods to assess profitability of company, these are Marginal

and Absorption costing methods. These two different methods defines profitability level with

different perspectives. Most of the companies, prepare income statements by applying both

methods for better presentation and analysis. These two techniques are differentiated by their

different aims and approach. Profit assessed under marginal costing always shifts in direction of

volume of sales. Whereas in absorption costing, profit may be on an irregular basis thus in

opposite direction from units sold. If manufacturing is lower than revenues, then absorption

method will show less profit. The cause is that fixed costs for the prior period are included in

opening inventory and are charged against present earnings.

D2 Financial reports that accurately apply and interpret data

From the above calculation it has been interpreted that from marginal costing the

contribution for month of November was 250000 and the balance of net profit was 61000 GBP.

In the month of December the value of contribution was 300000 and for net profit it was 101000

because the sales for the period increases that also grow profitability of company. With the help

of absorption costing the gross profit for November month was 1600000 GBP and total of net

profit was 79000 GBP. On the other side in month of December the sales was 600000 GBP,

gross profit was 192000 and the value of net profit was 83000 that shows that there is a increase

in the value of net profit due to sale of more unit for company.

Less: Cost of sales -408000

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

M2 Range of management accounting techniques

Mainly there are two key methods to assess profitability of company, these are Marginal

and Absorption costing methods. These two different methods defines profitability level with

different perspectives. Most of the companies, prepare income statements by applying both

methods for better presentation and analysis. These two techniques are differentiated by their

different aims and approach. Profit assessed under marginal costing always shifts in direction of

volume of sales. Whereas in absorption costing, profit may be on an irregular basis thus in

opposite direction from units sold. If manufacturing is lower than revenues, then absorption

method will show less profit. The cause is that fixed costs for the prior period are included in

opening inventory and are charged against present earnings.

D2 Financial reports that accurately apply and interpret data

From the above calculation it has been interpreted that from marginal costing the

contribution for month of November was 250000 and the balance of net profit was 61000 GBP.

In the month of December the value of contribution was 300000 and for net profit it was 101000

because the sales for the period increases that also grow profitability of company. With the help

of absorption costing the gross profit for November month was 1600000 GBP and total of net

profit was 79000 GBP. On the other side in month of December the sales was 600000 GBP,

gross profit was 192000 and the value of net profit was 83000 that shows that there is a increase

in the value of net profit due to sale of more unit for company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4 Advantages and disadvantages of different planning tool used for budgetary control.

Budget: These are known as financial plan that constitutes transactions related to

resource quantities, assets, liabilities,sales volumes, expenses as well as flows of cash for defined

period (Northcott and Linacre, 2010). Families, companies and government authorities uses such

concept to describe strategic plans associated with different events addition to activities in

measurable terms. Budgets ensures that all the spendings are to be made within the set limit so

that available resources are used to attain more productive results. Creating and sticking towards

budgetary estimates helps in overcoming from precarious positions. Budgets helps in building

successful action plan shows where cash is to be spend and from where it is to be earned. Ryder

Architecture creates as well as manages budgets so to regularly monitor business performance

together with financial situations.

Budgetary control: These enables administrators in conducting business with adequate

spendings. There are various budgetary control mechanisms that plays significant functions at

Ryder Architecture in monitoring spendings and earnings through distinct operational activities.

The controls makes sure that cash inflows addition to cash outflow resides within adequate

limits. Planning tools are described beneath:

Balanced budget: Organisational budget comes into category of balanced budget when

the receipts are equal to expected expenditure throughout the financial year. While financial

planning, it is estimated that total revenues will be equal or greater that expenses. Management

of Ryder Architecture also prepares such budget where they make estimations to attain budget

surplus with ongoing business activities (Otley and Emmanuel, 2013).

Advantages: Balanced budgets ensures stability of business when implemented

successfully. They ensures to Ryder Architecture that organisation can withhold cash from

incautious expenditures.

Disadvantages: The budget does not offer solutions to various problems such as inflation

or deflation. It is very difficult to manage such budget when various changes as experienced by

an organisation.

Sales budget: the budget provides estimations related to total sales revenue addition to

selling expenses of a company. It is considered as backbone of business. Sales budget provides

P4 Advantages and disadvantages of different planning tool used for budgetary control.

Budget: These are known as financial plan that constitutes transactions related to

resource quantities, assets, liabilities,sales volumes, expenses as well as flows of cash for defined

period (Northcott and Linacre, 2010). Families, companies and government authorities uses such

concept to describe strategic plans associated with different events addition to activities in

measurable terms. Budgets ensures that all the spendings are to be made within the set limit so

that available resources are used to attain more productive results. Creating and sticking towards

budgetary estimates helps in overcoming from precarious positions. Budgets helps in building

successful action plan shows where cash is to be spend and from where it is to be earned. Ryder

Architecture creates as well as manages budgets so to regularly monitor business performance

together with financial situations.

Budgetary control: These enables administrators in conducting business with adequate

spendings. There are various budgetary control mechanisms that plays significant functions at

Ryder Architecture in monitoring spendings and earnings through distinct operational activities.

The controls makes sure that cash inflows addition to cash outflow resides within adequate

limits. Planning tools are described beneath:

Balanced budget: Organisational budget comes into category of balanced budget when

the receipts are equal to expected expenditure throughout the financial year. While financial

planning, it is estimated that total revenues will be equal or greater that expenses. Management

of Ryder Architecture also prepares such budget where they make estimations to attain budget

surplus with ongoing business activities (Otley and Emmanuel, 2013).

Advantages: Balanced budgets ensures stability of business when implemented

successfully. They ensures to Ryder Architecture that organisation can withhold cash from

incautious expenditures.

Disadvantages: The budget does not offer solutions to various problems such as inflation

or deflation. It is very difficult to manage such budget when various changes as experienced by

an organisation.

Sales budget: the budget provides estimations related to total sales revenue addition to

selling expenses of a company. It is considered as backbone of business. Sales budget provides

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actual forecasting of sales of various products of Ryder Architecture for defined period in

context to values and quantities.

Advantages: Sales budget guides management of the company to identify weak links as

well as taking appropriate actions to eliminate hurdles in attaining forecasted sales.

Disadvantages: Various unforeseen circumstances are not forecasted properly through

such budget that can limit earning of Ryder Architecture through sales (Parker, 2012).

Activity based budget: It is prepared after analysing overhead costs associated with each

activity. It is prepared without considering previous year budget instead current activities are

deeply analysed as well as researched so to arrive at proper estimate.

Advantages: Activity based budget helps in eliminating unnecessary activities at Ryder

Architecture through focusing each activities and making final estimate decision. It also helps in

saving costs to strengthen competitive edges.

Disadvantages: The budget requires deep understanding of each activity which is only

done by professional accountant and appointing professionals for such adds extra cost to selected

business. It many times results in incapability to understand as well as evaluate activities that

leads to budget preparation in accurate manner.

M3 Use of different planning tools and their application for preparing and forecasting budgets

In business world, the different planning tools are used to prepare and forecast budgets so

that expenses can be reduces and overall profit margin can be grown in specific accounting year.

The common planning tool used by Ryder Architecture are balanced budget, Sales budget and

Activity based budget that plays a significant role in forecasting budgets for number of effective

activities of company. All these budgets are important because they contain financial information

which help to make framework for accurate projection of future expenses and income (Qian,

Burritt and Monroe, 2011).

TASK 4

P5 Comparison of the way in which organisations are adapting management accounting systems.

Financial issue can be described as the scenario in which an organization experiences

problems owing to a absence of financial assets. These problem can be internal which happen

due to wrong decision made by manager and external issues that arise due to sudden changes

occurring within environment. Identifying the sources of such kinds of issues and then using

context to values and quantities.

Advantages: Sales budget guides management of the company to identify weak links as

well as taking appropriate actions to eliminate hurdles in attaining forecasted sales.

Disadvantages: Various unforeseen circumstances are not forecasted properly through

such budget that can limit earning of Ryder Architecture through sales (Parker, 2012).

Activity based budget: It is prepared after analysing overhead costs associated with each

activity. It is prepared without considering previous year budget instead current activities are

deeply analysed as well as researched so to arrive at proper estimate.

Advantages: Activity based budget helps in eliminating unnecessary activities at Ryder

Architecture through focusing each activities and making final estimate decision. It also helps in

saving costs to strengthen competitive edges.

Disadvantages: The budget requires deep understanding of each activity which is only

done by professional accountant and appointing professionals for such adds extra cost to selected

business. It many times results in incapability to understand as well as evaluate activities that

leads to budget preparation in accurate manner.

M3 Use of different planning tools and their application for preparing and forecasting budgets

In business world, the different planning tools are used to prepare and forecast budgets so

that expenses can be reduces and overall profit margin can be grown in specific accounting year.

The common planning tool used by Ryder Architecture are balanced budget, Sales budget and

Activity based budget that plays a significant role in forecasting budgets for number of effective

activities of company. All these budgets are important because they contain financial information

which help to make framework for accurate projection of future expenses and income (Qian,

Burritt and Monroe, 2011).

TASK 4

P5 Comparison of the way in which organisations are adapting management accounting systems.

Financial issue can be described as the scenario in which an organization experiences

problems owing to a absence of financial assets. These problem can be internal which happen

due to wrong decision made by manager and external issues that arise due to sudden changes

occurring within environment. Identifying the sources of such kinds of issues and then using

efficient policies to solve them is really crucial for all businesses. Ryder Architecture also faces

the following economic difficulties due to which they are unable to perform important activities.

Some of these are discussed below:

Unexpected Expenses: For Ryder Architecture, this financial issue occurs owing to the

absence of efficient planning in which an unforeseen expenses occurs and executives have to use

reserve resources to handle that expenses. It further causes the problem of lack of funds to run

crucial operation of company.

Late payment from clients: In a selfishness to boost sales quantity for that era, Ryder

Architecture offers its clients with credit facility. It often leads to late payouts by consumers

resulting in the unavailability of financial funds that is mainly required to run companies day-to-

day operations (Renz, 2016).

As Ryder Architecture's financial consultant manager is accountable for identifying the

factors of such above-mentioned issues and finding suitable alternatives to them which help to

improve the overall performance during specific year. The advisors use various methods in the

for this purpose. Some of them are explained in detail below:

KPIs (Key Performance Indicators): These are primarily used to measure the

company's efficiency. There have been two primary types of KPI, financial key performance

indicator which is used to discover all the useless costs the organization makes and the other is

non-financial, that is used to analyse issues in the procedure, supply chain, etc. of the

organization. In Ryder Architecture manager uses financial KPI to identify problem of

unexpected expenses due to which planned activities and expenses gets hampered.

Benchmarking: It is a measuring tool that companies are using to measure their

efficiency with rivals in the same sector (Scapens and Bromwich, 2010). This tool is used by

respective firm to identify the major financial problem that is related with late payment by

customer due to which company do not have enough cash flow to run and manage other

activities. They can make changes within their strategies by making valid comparison and

modification to its credit strategies with rivals.

Financial governance: It can be described as the collection of various economic values

that businesses need to adopt to cope with money-related issues. Management tries to solve

challenges faced by Ryder Architecture by identifying suitable alternatives for all of them with

the assistance of this tool. It is also used to track organisational approach by examining whether

the following economic difficulties due to which they are unable to perform important activities.

Some of these are discussed below:

Unexpected Expenses: For Ryder Architecture, this financial issue occurs owing to the

absence of efficient planning in which an unforeseen expenses occurs and executives have to use

reserve resources to handle that expenses. It further causes the problem of lack of funds to run

crucial operation of company.

Late payment from clients: In a selfishness to boost sales quantity for that era, Ryder

Architecture offers its clients with credit facility. It often leads to late payouts by consumers

resulting in the unavailability of financial funds that is mainly required to run companies day-to-

day operations (Renz, 2016).

As Ryder Architecture's financial consultant manager is accountable for identifying the

factors of such above-mentioned issues and finding suitable alternatives to them which help to

improve the overall performance during specific year. The advisors use various methods in the

for this purpose. Some of them are explained in detail below:

KPIs (Key Performance Indicators): These are primarily used to measure the

company's efficiency. There have been two primary types of KPI, financial key performance

indicator which is used to discover all the useless costs the organization makes and the other is

non-financial, that is used to analyse issues in the procedure, supply chain, etc. of the

organization. In Ryder Architecture manager uses financial KPI to identify problem of

unexpected expenses due to which planned activities and expenses gets hampered.

Benchmarking: It is a measuring tool that companies are using to measure their

efficiency with rivals in the same sector (Scapens and Bromwich, 2010). This tool is used by

respective firm to identify the major financial problem that is related with late payment by

customer due to which company do not have enough cash flow to run and manage other

activities. They can make changes within their strategies by making valid comparison and

modification to its credit strategies with rivals.

Financial governance: It can be described as the collection of various economic values

that businesses need to adopt to cope with money-related issues. Management tries to solve

challenges faced by Ryder Architecture by identifying suitable alternatives for all of them with

the assistance of this tool. It is also used to track organisational approach by examining whether

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.