Management Accounting Report: Financial Analysis of Tech Ltd (M1)

VerifiedAdded on 2020/07/22

|22

|6820

|48

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA) and its application to Tech Limited, an electronics company. It begins by defining MA, differentiating it from financial accounting, and highlighting its significance in internal decision-making. The report delves into various MA systems, including cost accounting, inventory management, job costing, and price optimization. It then explores the presentation of financial information through different reports, such as account receivables, budget, sales revenue, and production reports. The report analyzes the importance of presenting information in an understandable manner. The report then presents profit and loss statements based on absorption and marginal costing, along with a reconciliation statement. Furthermore, it examines different types of budgets, their merits, demerits, and the procedure for budget preparation, including pricing determination and different costing systems. The significance of budgeting is also discussed. The report also delves into the Balanced Scorecard (BSC) approach, explaining how it can be used to address financial shortfalls, connecting key performance indicators (KPIs) with Tech Ltd's financial issues. The report concludes by summarizing how MA contributes to a firm's sustainable success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Explaining MA as well as its key requirements................................................................1

I. Difference among MA and financial accounting (FA).......................................................1

II. Significant of MA for making business decisions.............................................................2

III. Cost accounting systems...................................................................................................3

IV. Inventory management systems.......................................................................................3

V. Job costing systems...........................................................................................................3

Price optimisation system.......................................................................................................4

B) Presenting the financial information.................................................................................4

I. Various reports of managerial accounting..........................................................................4

II. Importance of presenting information in an understandable manner................................5

M1 Evaluating benefits of MA systems.................................................................................5

TASK 2............................................................................................................................................6

I. Statement of P&L on the basis of absorption costing.........................................................6

II. Statement of P&L on the basis of marginal costing..........................................................6

M2 Reconciliation statement..................................................................................................7

TASK 3............................................................................................................................................8

A) Various budgets and their merits as well as demerits.......................................................8

Financial budgets....................................................................................................................8

Operating budgets...................................................................................................................9

B) Procedure of budget preparation.....................................................................................11

Determination of pricing......................................................................................................12

Different costing system:......................................................................................................12

C) Significant of budget.......................................................................................................12

M3 Use of various planning tools and application to prepare and forecast budgets............13

TASK 4..........................................................................................................................................14

Ways through which BSC approach is used for responding financial shortfalls.................14

Connection of KPI with Tech Ltd's financial issues............................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Explaining MA as well as its key requirements................................................................1

I. Difference among MA and financial accounting (FA).......................................................1

II. Significant of MA for making business decisions.............................................................2

III. Cost accounting systems...................................................................................................3

IV. Inventory management systems.......................................................................................3

V. Job costing systems...........................................................................................................3

Price optimisation system.......................................................................................................4

B) Presenting the financial information.................................................................................4

I. Various reports of managerial accounting..........................................................................4

II. Importance of presenting information in an understandable manner................................5

M1 Evaluating benefits of MA systems.................................................................................5

TASK 2............................................................................................................................................6

I. Statement of P&L on the basis of absorption costing.........................................................6

II. Statement of P&L on the basis of marginal costing..........................................................6

M2 Reconciliation statement..................................................................................................7

TASK 3............................................................................................................................................8

A) Various budgets and their merits as well as demerits.......................................................8

Financial budgets....................................................................................................................8

Operating budgets...................................................................................................................9

B) Procedure of budget preparation.....................................................................................11

Determination of pricing......................................................................................................12

Different costing system:......................................................................................................12

C) Significant of budget.......................................................................................................12

M3 Use of various planning tools and application to prepare and forecast budgets............13

TASK 4..........................................................................................................................................14

Ways through which BSC approach is used for responding financial shortfalls.................14

Connection of KPI with Tech Ltd's financial issues............................................................16

Comparing BSC used within another business organisation................................................16

M4 Ways through which MA helps to firm in sustainable success.....................................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

M4 Ways through which MA helps to firm in sustainable success.....................................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A system which is used in the firm for making financial plan, implementing, controlling,

monitoring as well as taking effective actions is known as management accounting (MA). The

present report is based on Tech Limited company which has presence in the electronic industry.

Main products offered by it are special mobile phone's charger as well as other carry-on gadgets.

The study reflects about the management accounting along with its essential needs within the

workplace of Tech Ltd in order to make internal financial decisions. Apart from this, various

systems involved in the MA like reporting etc. are explained. The current project focuses on

marginal and absorption costing which are supportive to frame income statements. In additional

to this, budgets, their benefits and limitations as well as importance within Tech Limited are

described. At the end of present assignment, BSC approach is explained which helps to eliminate

financial issues incurred in Tech Limited.

TASK 1

A) Explaining MA as well as its key requirements

A procedure of an entity which helps to make an effective schedule of financial expenses,

control and monitor them within workplace is considered as the management accounting (MA).

It is highly required for taking only internal decisions because not works at the external level.

When Tech Limited will consider this approach in proper and high manner then easily able to

fulfil and accomplish goals of the firm. Apart from this, it consists with wide range of systems

and methods due to which it is an essential part (Klemstine and Maher, 2014). Due to lack of

availability and proper use of MA, businesses cannot meet the objectives framed. The below

sections are giving information about different systems of MA and their basic needs.

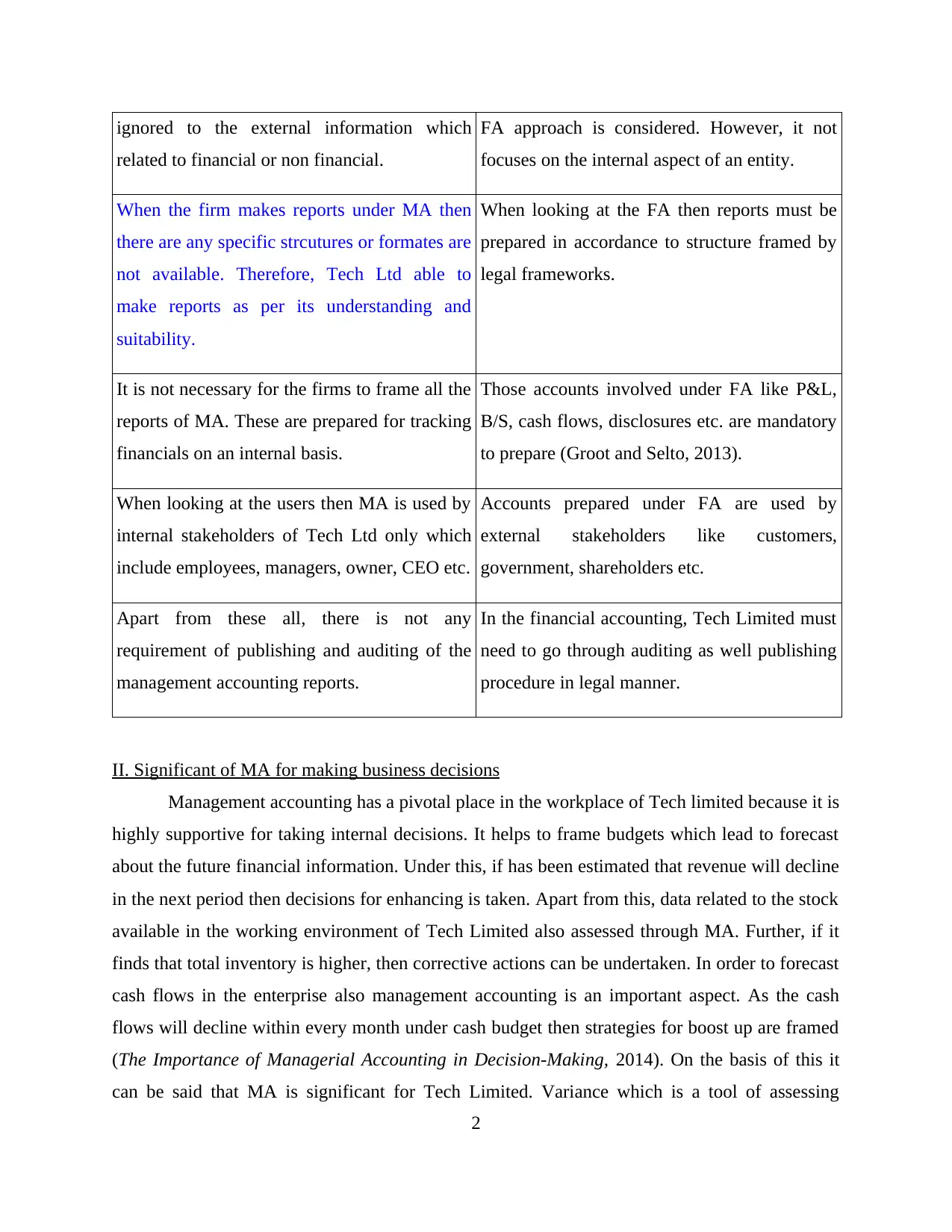

I. Difference among MA and financial accounting (FA)

In the accounting branch of knowledge, basically two aspects involved which are like

management and financial. Both are used by the firms but in different level and criteria.

Therefore, distinguish of these both the systems i.e. MA and FA is mentioned below:

Management accounting Financial accounting

MA is a system used by the company in order

to make internal business only. It totally

On the other side, in order to make highly

effectual kind of external business decisions,

1

A system which is used in the firm for making financial plan, implementing, controlling,

monitoring as well as taking effective actions is known as management accounting (MA). The

present report is based on Tech Limited company which has presence in the electronic industry.

Main products offered by it are special mobile phone's charger as well as other carry-on gadgets.

The study reflects about the management accounting along with its essential needs within the

workplace of Tech Ltd in order to make internal financial decisions. Apart from this, various

systems involved in the MA like reporting etc. are explained. The current project focuses on

marginal and absorption costing which are supportive to frame income statements. In additional

to this, budgets, their benefits and limitations as well as importance within Tech Limited are

described. At the end of present assignment, BSC approach is explained which helps to eliminate

financial issues incurred in Tech Limited.

TASK 1

A) Explaining MA as well as its key requirements

A procedure of an entity which helps to make an effective schedule of financial expenses,

control and monitor them within workplace is considered as the management accounting (MA).

It is highly required for taking only internal decisions because not works at the external level.

When Tech Limited will consider this approach in proper and high manner then easily able to

fulfil and accomplish goals of the firm. Apart from this, it consists with wide range of systems

and methods due to which it is an essential part (Klemstine and Maher, 2014). Due to lack of

availability and proper use of MA, businesses cannot meet the objectives framed. The below

sections are giving information about different systems of MA and their basic needs.

I. Difference among MA and financial accounting (FA)

In the accounting branch of knowledge, basically two aspects involved which are like

management and financial. Both are used by the firms but in different level and criteria.

Therefore, distinguish of these both the systems i.e. MA and FA is mentioned below:

Management accounting Financial accounting

MA is a system used by the company in order

to make internal business only. It totally

On the other side, in order to make highly

effectual kind of external business decisions,

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ignored to the external information which

related to financial or non financial.

FA approach is considered. However, it not

focuses on the internal aspect of an entity.

When the firm makes reports under MA then

there are any specific strcutures or formates are

not available. Therefore, Tech Ltd able to

make reports as per its understanding and

suitability.

When looking at the FA then reports must be

prepared in accordance to structure framed by

legal frameworks.

It is not necessary for the firms to frame all the

reports of MA. These are prepared for tracking

financials on an internal basis.

Those accounts involved under FA like P&L,

B/S, cash flows, disclosures etc. are mandatory

to prepare (Groot and Selto, 2013).

When looking at the users then MA is used by

internal stakeholders of Tech Ltd only which

include employees, managers, owner, CEO etc.

Accounts prepared under FA are used by

external stakeholders like customers,

government, shareholders etc.

Apart from these all, there is not any

requirement of publishing and auditing of the

management accounting reports.

In the financial accounting, Tech Limited must

need to go through auditing as well publishing

procedure in legal manner.

II. Significant of MA for making business decisions

Management accounting has a pivotal place in the workplace of Tech limited because it is

highly supportive for taking internal decisions. It helps to frame budgets which lead to forecast

about the future financial information. Under this, if has been estimated that revenue will decline

in the next period then decisions for enhancing is taken. Apart from this, data related to the stock

available in the working environment of Tech Limited also assessed through MA. Further, if it

finds that total inventory is higher, then corrective actions can be undertaken. In order to forecast

cash flows in the enterprise also management accounting is an important aspect. As the cash

flows will decline within every month under cash budget then strategies for boost up are framed

(The Importance of Managerial Accounting in Decision-Making, 2014). On the basis of this it

can be said that MA is significant for Tech Limited. Variance which is a tool of assessing

2

related to financial or non financial.

FA approach is considered. However, it not

focuses on the internal aspect of an entity.

When the firm makes reports under MA then

there are any specific strcutures or formates are

not available. Therefore, Tech Ltd able to

make reports as per its understanding and

suitability.

When looking at the FA then reports must be

prepared in accordance to structure framed by

legal frameworks.

It is not necessary for the firms to frame all the

reports of MA. These are prepared for tracking

financials on an internal basis.

Those accounts involved under FA like P&L,

B/S, cash flows, disclosures etc. are mandatory

to prepare (Groot and Selto, 2013).

When looking at the users then MA is used by

internal stakeholders of Tech Ltd only which

include employees, managers, owner, CEO etc.

Accounts prepared under FA are used by

external stakeholders like customers,

government, shareholders etc.

Apart from these all, there is not any

requirement of publishing and auditing of the

management accounting reports.

In the financial accounting, Tech Limited must

need to go through auditing as well publishing

procedure in legal manner.

II. Significant of MA for making business decisions

Management accounting has a pivotal place in the workplace of Tech limited because it is

highly supportive for taking internal decisions. It helps to frame budgets which lead to forecast

about the future financial information. Under this, if has been estimated that revenue will decline

in the next period then decisions for enhancing is taken. Apart from this, data related to the stock

available in the working environment of Tech Limited also assessed through MA. Further, if it

finds that total inventory is higher, then corrective actions can be undertaken. In order to forecast

cash flows in the enterprise also management accounting is an important aspect. As the cash

flows will decline within every month under cash budget then strategies for boost up are framed

(The Importance of Managerial Accounting in Decision-Making, 2014). On the basis of this it

can be said that MA is significant for Tech Limited. Variance which is a tool of assessing

2

business performance is also a part of MA. It helps to known that at which aspect like material,

labour, cost, profit etc. Tech Ltd not able to meet budgeted data. Therefore, an effective decision

to grab and eliminate the issues can be taken in the firm properly. Further, it comprises with

several systems and leads to generate reports of different financial transactions like cost,

receivables, budget etc. Therefore, performance of the firm within relevant industry cam be

assessed and effective decisions made accordingly.

III. Cost accounting systems

Expense or cost is a very sensitive aspect for each and every business entity. While

producing chargers and any electronic gadgets when costing enhanced over the years then

directly create negative impact on profit generation capacity. Further, in order to manage this

situation and boost up profitability, cost accounting system is used by the management. It is

taken into consideration in order to assess actual expenditures involved within working

environment of Tech Ltd firm. When looking at the requirements then, used for estimating costs

of production (Bryer, 2013). On the basis of total expenses, decisions for determining pricing

level of that product are made. For instance: if cost of special chargers is high at the end of year

then price will be charged as per the situation. In addition to this, in order to frame strategies for

managing and reducing costing this system is needed to cited entity. Along with this, profitability

analysis is also done by on the basis of cost accounting system in a proper direction.

IV. Inventory management systems

Stock is a big matter of concern for the company because when it remains in the

workplace with higher level then influence to the sales revenue. Therefore, inventory is required

to manage and reduce in proper way within Tech Limited. Apart from managing, it helps to cited

firm in order to track orders, deliveries as well as sales of the stock in the firm. On the basis of

this it can be easily identified that how much stock or products manufactured are sold at the end

of year. It is required for the organisation for assessing as well as tracking levels, sales, orders

and deliveries of stock. In addition to this, for creating order for specific work in the

manufacturing company as well as generate bill of materials also this is used (Soheilirad and

Sofian, 2016). Under this, valuation of stock level is also done by considering major three

methods like LIFO, FIFO and weighted average.

3

labour, cost, profit etc. Tech Ltd not able to meet budgeted data. Therefore, an effective decision

to grab and eliminate the issues can be taken in the firm properly. Further, it comprises with

several systems and leads to generate reports of different financial transactions like cost,

receivables, budget etc. Therefore, performance of the firm within relevant industry cam be

assessed and effective decisions made accordingly.

III. Cost accounting systems

Expense or cost is a very sensitive aspect for each and every business entity. While

producing chargers and any electronic gadgets when costing enhanced over the years then

directly create negative impact on profit generation capacity. Further, in order to manage this

situation and boost up profitability, cost accounting system is used by the management. It is

taken into consideration in order to assess actual expenditures involved within working

environment of Tech Ltd firm. When looking at the requirements then, used for estimating costs

of production (Bryer, 2013). On the basis of total expenses, decisions for determining pricing

level of that product are made. For instance: if cost of special chargers is high at the end of year

then price will be charged as per the situation. In addition to this, in order to frame strategies for

managing and reducing costing this system is needed to cited entity. Along with this, profitability

analysis is also done by on the basis of cost accounting system in a proper direction.

IV. Inventory management systems

Stock is a big matter of concern for the company because when it remains in the

workplace with higher level then influence to the sales revenue. Therefore, inventory is required

to manage and reduce in proper way within Tech Limited. Apart from managing, it helps to cited

firm in order to track orders, deliveries as well as sales of the stock in the firm. On the basis of

this it can be easily identified that how much stock or products manufactured are sold at the end

of year. It is required for the organisation for assessing as well as tracking levels, sales, orders

and deliveries of stock. In addition to this, for creating order for specific work in the

manufacturing company as well as generate bill of materials also this is used (Soheilirad and

Sofian, 2016). Under this, valuation of stock level is also done by considering major three

methods like LIFO, FIFO and weighted average.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

V. Job costing systems

In the firm when products and services manufactured are different from each other in

sufficient way then job costing system is considered. In order to assess level of expenses

occurred at each job products it is highly used. In the present case study, Tech (UK) Limited

company is producing two goods in two batches like special charger and electronic gadgets.

Further, to known that in which batch, cost level incurred up to which extent the job costing

approach is used. It consists with basically three kinds of information which involve direct

material, direct labour as well as overhead expenses (The job costing system, 2015). When

production procedures is accomplished within workplace then implemented properly. The cost

accounting shows whole expenses of the products manufactured. On the other side, the present

explained system gives information about each product produced in every batch which leads to

support for taking profitable pricing decisions.

Price optimisation system

A system of MA by which an enterprise makes pricing decisions of goods and services is

known as price optimisation system. Further, it is generally used by Tech Ltd in order to opt an

attractive price of the special mobile chargers as well as electronic gadgets.

B) Presenting the financial information

I. Various reports of managerial accounting

In order to present information related to financials there are some reports prepared by

the management. The reason is that it helps to make all the financial statements and publish in

the market properly. Under the part of managerial accounting, various reports involved which are

explained below:

Account receivables report: The Tech limited firm selling its special chargers and other

electronic gadgets on credit. Further, amount will be received in the future which known

as credit sales. Further, under this report, those products which are sold at the credit to

consumers, that amount is recorded. At the end of an accounting period, total credits are

recorded in the account receivables reports which transacted in liabilities side of balance

sheet.

Budget report: Another system of reporting which is budget helps to estimate financial

information for next year. There is different kind of data forecasted under budget which

4

In the firm when products and services manufactured are different from each other in

sufficient way then job costing system is considered. In order to assess level of expenses

occurred at each job products it is highly used. In the present case study, Tech (UK) Limited

company is producing two goods in two batches like special charger and electronic gadgets.

Further, to known that in which batch, cost level incurred up to which extent the job costing

approach is used. It consists with basically three kinds of information which involve direct

material, direct labour as well as overhead expenses (The job costing system, 2015). When

production procedures is accomplished within workplace then implemented properly. The cost

accounting shows whole expenses of the products manufactured. On the other side, the present

explained system gives information about each product produced in every batch which leads to

support for taking profitable pricing decisions.

Price optimisation system

A system of MA by which an enterprise makes pricing decisions of goods and services is

known as price optimisation system. Further, it is generally used by Tech Ltd in order to opt an

attractive price of the special mobile chargers as well as electronic gadgets.

B) Presenting the financial information

I. Various reports of managerial accounting

In order to present information related to financials there are some reports prepared by

the management. The reason is that it helps to make all the financial statements and publish in

the market properly. Under the part of managerial accounting, various reports involved which are

explained below:

Account receivables report: The Tech limited firm selling its special chargers and other

electronic gadgets on credit. Further, amount will be received in the future which known

as credit sales. Further, under this report, those products which are sold at the credit to

consumers, that amount is recorded. At the end of an accounting period, total credits are

recorded in the account receivables reports which transacted in liabilities side of balance

sheet.

Budget report: Another system of reporting which is budget helps to estimate financial

information for next year. There is different kind of data forecasted under budget which

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

include sales, cash position, production, material, direct labour etc (Khodzytska and

Ivchenko, 2014). It is used in the firm for framing strategies for achieving desired

objectives in an appropriate manner. Base taken for preparing different budgets is past

financial statements like P&L, B/S, cash flows etc.

Sales revenue report: According to this reporting system, company able to know that

how much amount generated by the firm excluding all the costs. Further, it shows

capabilities of the Tech Limited company in order to know level of financials. Under this,

those amounts included which are earned from selling the chargers and gadgets. In the

accounting it is known as turnover as well. Total of the sales is recorded in the profit and

loss account and considered as a base for assessing profitability position.

Production report: Apart from the above, a report in which level or units included

which are manufactured at the end of year is known as production report (Joshi and Li,

2016). On the basis of this, Tech Limited able to assess that, company is how much

capable for producing products utilising required resources as well as raw materials.

II. Importance of presenting information in an understandable manner

In order to analyse financial performance of a particular organisation, statements and

accounts related to financial transactions are considered by people and stakeholders. When these

are proper and easily understandable by the local communities then they can make decisions for

this. On the other hand, if financials of the business entity like Tech Limited are not presented

appropriately then they cannot analyse its performance. Apart from this, in order to make

investment in Tech Limited firm shareholders or investors always consider to the profitability

position. At the time of making investment decisions if overall financials are not properly

presented then unable to know that whether it will be profitable or not. In addition to this, a

candidate when going to apply in the firm for job then also consider various financials. The

reason is that, higher the level of profit at the end of year leads to provide more salary and

allowances (Bertz and Quinn, 2014). Henceforth, it can be said that to present financial

statements in proper structure is supportive for stakeholders for making suitable decisions

towards the Tech firm.

5

Ivchenko, 2014). It is used in the firm for framing strategies for achieving desired

objectives in an appropriate manner. Base taken for preparing different budgets is past

financial statements like P&L, B/S, cash flows etc.

Sales revenue report: According to this reporting system, company able to know that

how much amount generated by the firm excluding all the costs. Further, it shows

capabilities of the Tech Limited company in order to know level of financials. Under this,

those amounts included which are earned from selling the chargers and gadgets. In the

accounting it is known as turnover as well. Total of the sales is recorded in the profit and

loss account and considered as a base for assessing profitability position.

Production report: Apart from the above, a report in which level or units included

which are manufactured at the end of year is known as production report (Joshi and Li,

2016). On the basis of this, Tech Limited able to assess that, company is how much

capable for producing products utilising required resources as well as raw materials.

II. Importance of presenting information in an understandable manner

In order to analyse financial performance of a particular organisation, statements and

accounts related to financial transactions are considered by people and stakeholders. When these

are proper and easily understandable by the local communities then they can make decisions for

this. On the other hand, if financials of the business entity like Tech Limited are not presented

appropriately then they cannot analyse its performance. Apart from this, in order to make

investment in Tech Limited firm shareholders or investors always consider to the profitability

position. At the time of making investment decisions if overall financials are not properly

presented then unable to know that whether it will be profitable or not. In addition to this, a

candidate when going to apply in the firm for job then also consider various financials. The

reason is that, higher the level of profit at the end of year leads to provide more salary and

allowances (Bertz and Quinn, 2014). Henceforth, it can be said that to present financial

statements in proper structure is supportive for stakeholders for making suitable decisions

towards the Tech firm.

5

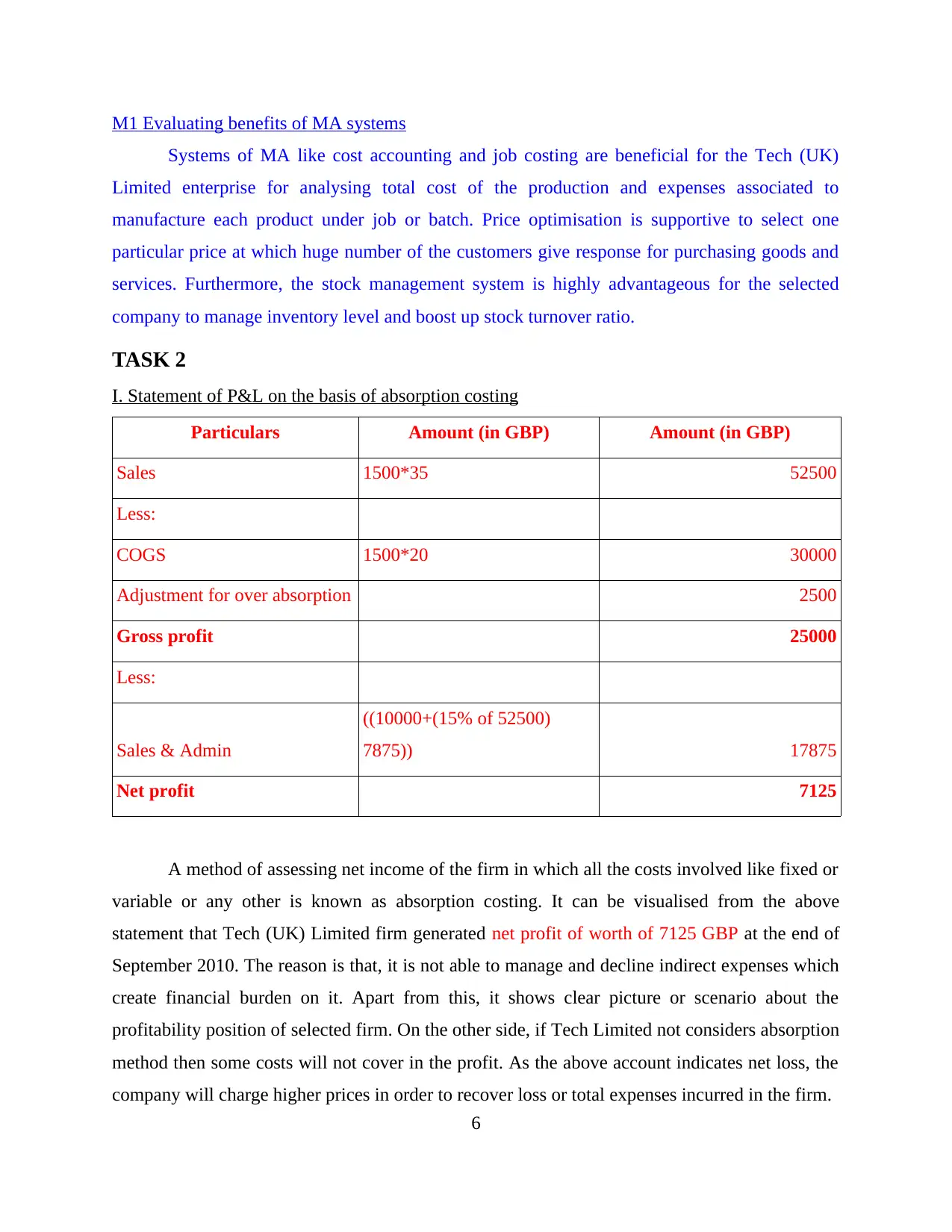

M1 Evaluating benefits of MA systems

Systems of MA like cost accounting and job costing are beneficial for the Tech (UK)

Limited enterprise for analysing total cost of the production and expenses associated to

manufacture each product under job or batch. Price optimisation is supportive to select one

particular price at which huge number of the customers give response for purchasing goods and

services. Furthermore, the stock management system is highly advantageous for the selected

company to manage inventory level and boost up stock turnover ratio.

TASK 2

I. Statement of P&L on the basis of absorption costing

Particulars Amount (in GBP) Amount (in GBP)

Sales 1500*35 52500

Less:

COGS 1500*20 30000

Adjustment for over absorption 2500

Gross profit 25000

Less:

Sales & Admin

((10000+(15% of 52500)

7875)) 17875

Net profit 7125

A method of assessing net income of the firm in which all the costs involved like fixed or

variable or any other is known as absorption costing. It can be visualised from the above

statement that Tech (UK) Limited firm generated net profit of worth of 7125 GBP at the end of

September 2010. The reason is that, it is not able to manage and decline indirect expenses which

create financial burden on it. Apart from this, it shows clear picture or scenario about the

profitability position of selected firm. On the other side, if Tech Limited not considers absorption

method then some costs will not cover in the profit. As the above account indicates net loss, the

company will charge higher prices in order to recover loss or total expenses incurred in the firm.

6

Systems of MA like cost accounting and job costing are beneficial for the Tech (UK)

Limited enterprise for analysing total cost of the production and expenses associated to

manufacture each product under job or batch. Price optimisation is supportive to select one

particular price at which huge number of the customers give response for purchasing goods and

services. Furthermore, the stock management system is highly advantageous for the selected

company to manage inventory level and boost up stock turnover ratio.

TASK 2

I. Statement of P&L on the basis of absorption costing

Particulars Amount (in GBP) Amount (in GBP)

Sales 1500*35 52500

Less:

COGS 1500*20 30000

Adjustment for over absorption 2500

Gross profit 25000

Less:

Sales & Admin

((10000+(15% of 52500)

7875)) 17875

Net profit 7125

A method of assessing net income of the firm in which all the costs involved like fixed or

variable or any other is known as absorption costing. It can be visualised from the above

statement that Tech (UK) Limited firm generated net profit of worth of 7125 GBP at the end of

September 2010. The reason is that, it is not able to manage and decline indirect expenses which

create financial burden on it. Apart from this, it shows clear picture or scenario about the

profitability position of selected firm. On the other side, if Tech Limited not considers absorption

method then some costs will not cover in the profit. As the above account indicates net loss, the

company will charge higher prices in order to recover loss or total expenses incurred in the firm.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

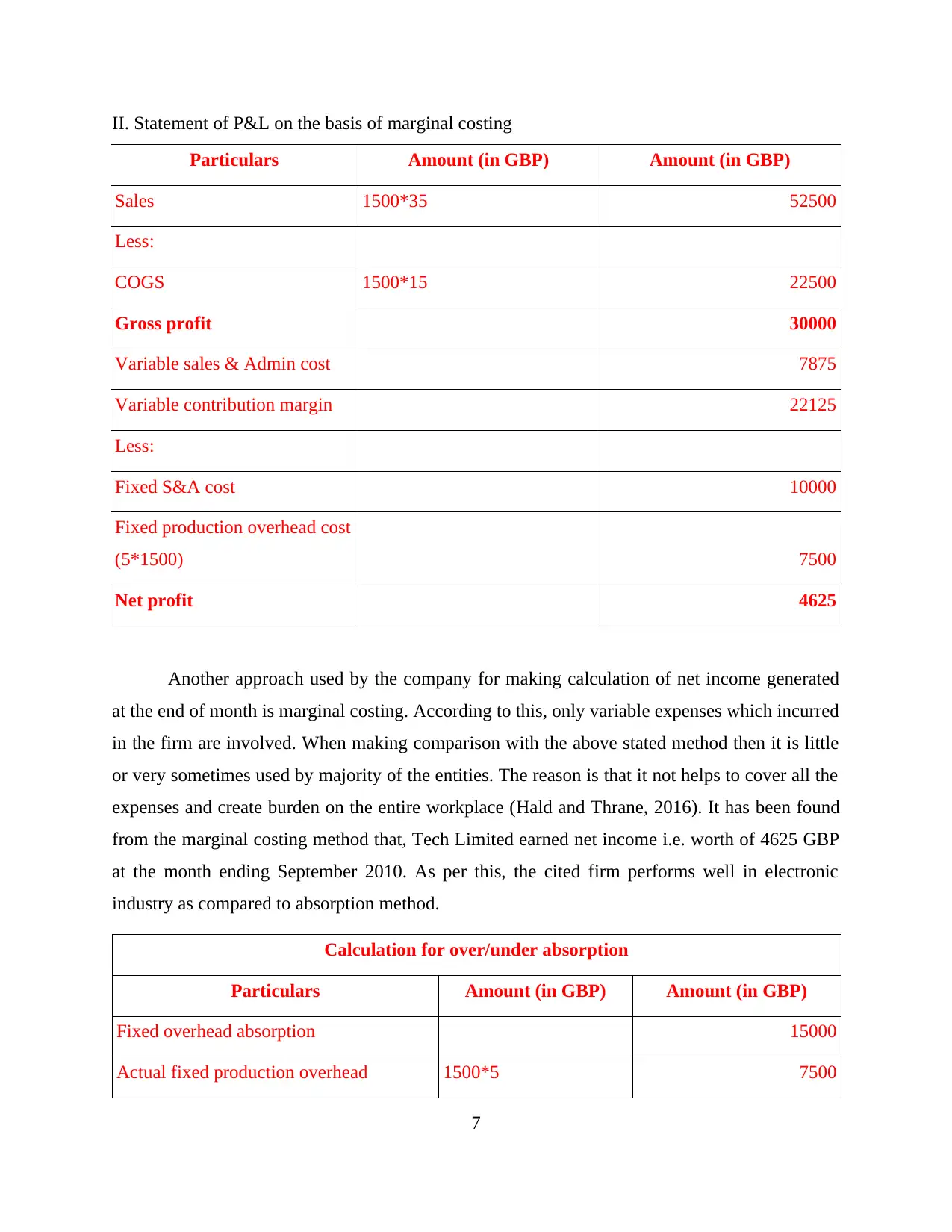

II. Statement of P&L on the basis of marginal costing

Particulars Amount (in GBP) Amount (in GBP)

Sales 1500*35 52500

Less:

COGS 1500*15 22500

Gross profit 30000

Variable sales & Admin cost 7875

Variable contribution margin 22125

Less:

Fixed S&A cost 10000

Fixed production overhead cost

(5*1500) 7500

Net profit 4625

Another approach used by the company for making calculation of net income generated

at the end of month is marginal costing. According to this, only variable expenses which incurred

in the firm are involved. When making comparison with the above stated method then it is little

or very sometimes used by majority of the entities. The reason is that it not helps to cover all the

expenses and create burden on the entire workplace (Hald and Thrane, 2016). It has been found

from the marginal costing method that, Tech Limited earned net income i.e. worth of 4625 GBP

at the month ending September 2010. As per this, the cited firm performs well in electronic

industry as compared to absorption method.

Calculation for over/under absorption

Particulars Amount (in GBP) Amount (in GBP)

Fixed overhead absorption 15000

Actual fixed production overhead 1500*5 7500

7

Particulars Amount (in GBP) Amount (in GBP)

Sales 1500*35 52500

Less:

COGS 1500*15 22500

Gross profit 30000

Variable sales & Admin cost 7875

Variable contribution margin 22125

Less:

Fixed S&A cost 10000

Fixed production overhead cost

(5*1500) 7500

Net profit 4625

Another approach used by the company for making calculation of net income generated

at the end of month is marginal costing. According to this, only variable expenses which incurred

in the firm are involved. When making comparison with the above stated method then it is little

or very sometimes used by majority of the entities. The reason is that it not helps to cover all the

expenses and create burden on the entire workplace (Hald and Thrane, 2016). It has been found

from the marginal costing method that, Tech Limited earned net income i.e. worth of 4625 GBP

at the month ending September 2010. As per this, the cited firm performs well in electronic

industry as compared to absorption method.

Calculation for over/under absorption

Particulars Amount (in GBP) Amount (in GBP)

Fixed overhead absorption 15000

Actual fixed production overhead 1500*5 7500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

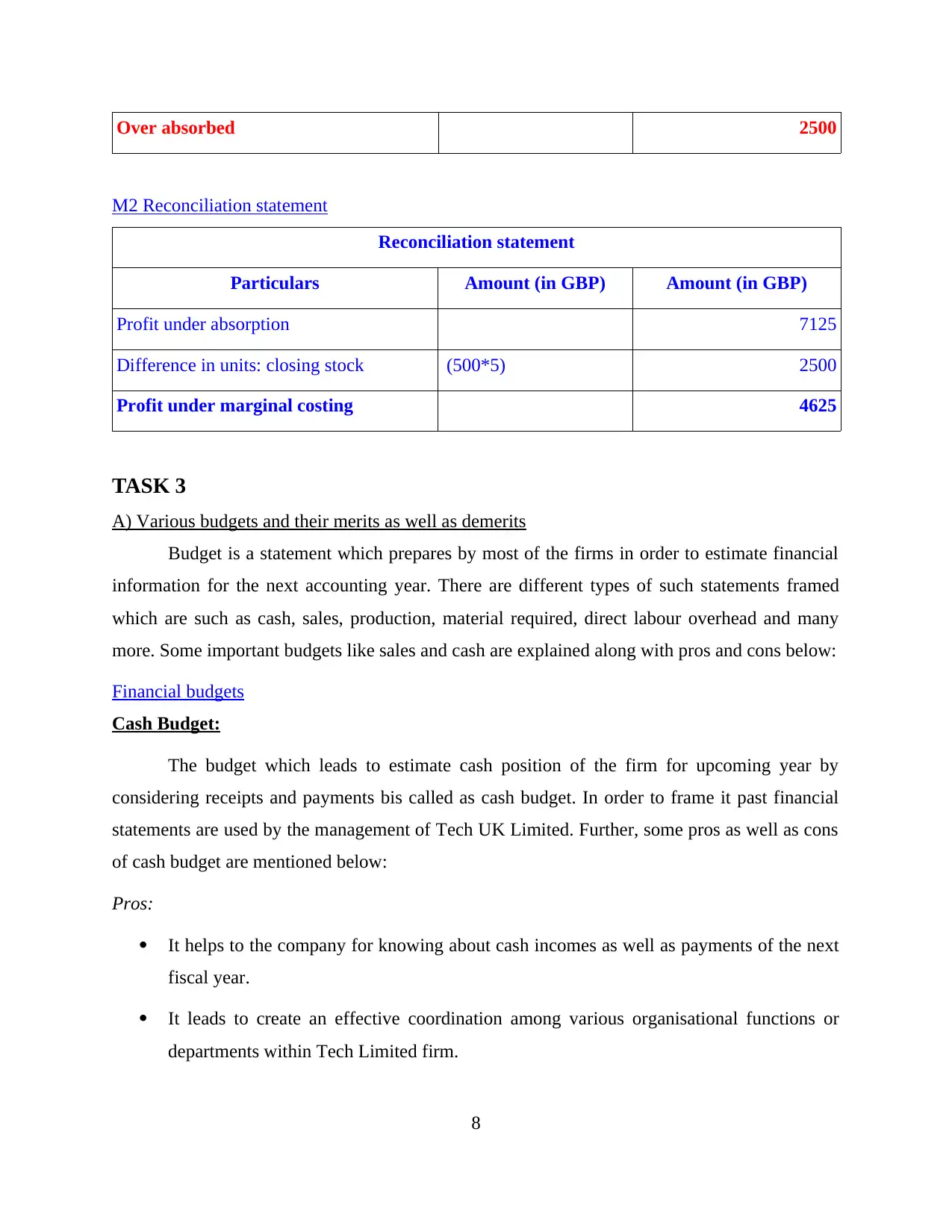

Over absorbed 2500

M2 Reconciliation statement

Reconciliation statement

Particulars Amount (in GBP) Amount (in GBP)

Profit under absorption 7125

Difference in units: closing stock (500*5) 2500

Profit under marginal costing 4625

TASK 3

A) Various budgets and their merits as well as demerits

Budget is a statement which prepares by most of the firms in order to estimate financial

information for the next accounting year. There are different types of such statements framed

which are such as cash, sales, production, material required, direct labour overhead and many

more. Some important budgets like sales and cash are explained along with pros and cons below:

Financial budgets

Cash Budget:

The budget which leads to estimate cash position of the firm for upcoming year by

considering receipts and payments bis called as cash budget. In order to frame it past financial

statements are used by the management of Tech UK Limited. Further, some pros as well as cons

of cash budget are mentioned below:

Pros:

It helps to the company for knowing about cash incomes as well as payments of the next

fiscal year.

It leads to create an effective coordination among various organisational functions or

departments within Tech Limited firm.

8

M2 Reconciliation statement

Reconciliation statement

Particulars Amount (in GBP) Amount (in GBP)

Profit under absorption 7125

Difference in units: closing stock (500*5) 2500

Profit under marginal costing 4625

TASK 3

A) Various budgets and their merits as well as demerits

Budget is a statement which prepares by most of the firms in order to estimate financial

information for the next accounting year. There are different types of such statements framed

which are such as cash, sales, production, material required, direct labour overhead and many

more. Some important budgets like sales and cash are explained along with pros and cons below:

Financial budgets

Cash Budget:

The budget which leads to estimate cash position of the firm for upcoming year by

considering receipts and payments bis called as cash budget. In order to frame it past financial

statements are used by the management of Tech UK Limited. Further, some pros as well as cons

of cash budget are mentioned below:

Pros:

It helps to the company for knowing about cash incomes as well as payments of the next

fiscal year.

It leads to create an effective coordination among various organisational functions or

departments within Tech Limited firm.

8

Apart from this, to assess that in upcoming times how much level of cash will be

available with the entity, cash budget is useful tool.

It is a helpful technique for the management in order to think for upcoming situation and

make the entire company highly efficient (Merits and Demerits of Cash Budget, 2016). Further, for minimising costing aspect as well as maximising level of profitability the

cash budget considered by Tech Limited.

Cons:

On the other side, if various functions of the firm are not coordinated with each other

properly then budgeted data cannot achieved.

It totally focused on the subjective estimations only and ignores to other aspects.

In order to frame and operate cash budget in Tech Limited firm, creates high financial

burden. Hence, it is costly or expensive method for the businesses.

Moreover, in order to meet estimated cash position high time frame required which affect

productivity of Tech Limited entity.

Capital expenditure budget:

A budget which reflects amounts as well as timing of the fixed assets in order to purchase

by a company is known as capital expenditure budget. It is usually considered to make expenses

on long term or fixed assets like plant, machinery, equipments etc. On the basis of this the firm

easily able to analyse rate of return at the end of completing the whole project. It helps to the

Tech Ltd for making decisions of the long-term strategic investments at the workplace (Capital

expenditure budget, 2017.).

However, it is not helpful to cited company in order to make short-term investment

judgements at the workplace. It takes huge time for preparing budget along with applying in the

firm which create negative impact on the efficiency and productivity of the Tech Ltd.

Balance sheet budget:

A report which is used by the management accountants in order to forecast assets,

liabilities and shareholder's equity for the next year is known as balance sheet budget. On the

9

available with the entity, cash budget is useful tool.

It is a helpful technique for the management in order to think for upcoming situation and

make the entire company highly efficient (Merits and Demerits of Cash Budget, 2016). Further, for minimising costing aspect as well as maximising level of profitability the

cash budget considered by Tech Limited.

Cons:

On the other side, if various functions of the firm are not coordinated with each other

properly then budgeted data cannot achieved.

It totally focused on the subjective estimations only and ignores to other aspects.

In order to frame and operate cash budget in Tech Limited firm, creates high financial

burden. Hence, it is costly or expensive method for the businesses.

Moreover, in order to meet estimated cash position high time frame required which affect

productivity of Tech Limited entity.

Capital expenditure budget:

A budget which reflects amounts as well as timing of the fixed assets in order to purchase

by a company is known as capital expenditure budget. It is usually considered to make expenses

on long term or fixed assets like plant, machinery, equipments etc. On the basis of this the firm

easily able to analyse rate of return at the end of completing the whole project. It helps to the

Tech Ltd for making decisions of the long-term strategic investments at the workplace (Capital

expenditure budget, 2017.).

However, it is not helpful to cited company in order to make short-term investment

judgements at the workplace. It takes huge time for preparing budget along with applying in the

firm which create negative impact on the efficiency and productivity of the Tech Ltd.

Balance sheet budget:

A report which is used by the management accountants in order to forecast assets,

liabilities and shareholder's equity for the next year is known as balance sheet budget. On the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.