Management Accounting Systems, Reporting, and Financial Analysis

VerifiedAdded on 2020/10/22

|16

|4923

|134

Report

AI Summary

This report delves into the realm of management accounting, exploring its various systems and techniques within the context of a business like Asda Limited. It begins by defining management accounting and highlighting the need for different systems such as product costing, cost accounting, job costing, process costing, inventory management, activity-based costing, and price optimization. The report then discusses the benefits and applications of these systems, emphasizing their role in effective decision-making and improved organizational efficiency. Furthermore, it critically evaluates accounting system reporting, analyzing different managerial accounting reports like budget reports, accounts receivable reports, and job cost reports. The report also examines the relevance of information gathered from these reports, particularly in the context of decision-making and cost reduction. The report covers techniques used in managerial accounting reporting, including budget reports, accounts receivable reports, and job cost reports. Finally, it explores the application of planning tools for forecasting and budget analysis, and the use of management accounting systems in responding to financial issues. This analysis provides a comprehensive overview of management accounting principles and their practical application in a business setting, offering insights into financial problem-solving and strategic decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and requirement of various management accounting systems.....1

M1: Benefits and applications of management accounting systems...........................................3

D1: Critically evaluate accounting system reporting..................................................................4

P2: Explain various methods used in managerial accounting reporting.....................................4

TASK 2 ...........................................................................................................................................6

P3: Calculation of cost using techniques and preparation of statement of profit and loss..........6

M2: Different types of management accounting techniques.......................................................8

TASK 3 ...........................................................................................................................................9

P4: Advantages and Disadvantages of different types of budgetary controls.............................9

M3: Application of planning tools for forecasting preparing and analysing budgets...............10

D3: Evaluation to deal with planning tools used in resolving financial problems....................11

TASK 4..........................................................................................................................................11

P5: Use of management accounting systems in responding to financial issues.......................11

M4: Analysing management accounting techniques.................................................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and requirement of various management accounting systems.....1

M1: Benefits and applications of management accounting systems...........................................3

D1: Critically evaluate accounting system reporting..................................................................4

P2: Explain various methods used in managerial accounting reporting.....................................4

TASK 2 ...........................................................................................................................................6

P3: Calculation of cost using techniques and preparation of statement of profit and loss..........6

M2: Different types of management accounting techniques.......................................................8

TASK 3 ...........................................................................................................................................9

P4: Advantages and Disadvantages of different types of budgetary controls.............................9

M3: Application of planning tools for forecasting preparing and analysing budgets...............10

D3: Evaluation to deal with planning tools used in resolving financial problems....................11

TASK 4..........................................................................................................................................11

P5: Use of management accounting systems in responding to financial issues.......................11

M4: Analysing management accounting techniques.................................................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Accounting process is related with recording, classifying and summarising the

transactions of business into the financial accounts of business such as journal, ledger and trial

balance in a manner that is easily understandable and comparable to the stakeholders of the

company. This project will discuss about the branch of accounting, which is management

accounting. Management accounting is the process of summarising the details of the financial

statements of the company as well as about the future economic and non economic activities of

the market that will be prevalent in future.( Alleyne, and Weekes-Marshall, 2011) These reports

are then used by the internal management of the Asda Limited so that they can make decision

regarding the formulation of policies and defining objectives in the company. This project will

discuss about the various management accounting systems that are adopted by the organisations

and how different management accounting techniques range are applied in the companies. Uses

of different planning tools in the management accounting process. The report will also perform a

comparison about the ways in which companies like Asda limited use the techniques of

managerial accounting in responding to financial problems.

TASK 1

P1: Management accounting and requirement of various management accounting systems

Management accounting is a process of preparing managerial accounts and reports by the

financial managers to provide reliable and accurate financial and costing data which can be

further used by managers to understand and handle day to day operations of the organisation.

Management accounting also includes translating the financial data into understandable

information which can be used for effective decision making.

Asda limited is a leading supermarket retailer based in United Kingdom, Asda is diverse

in its activities and due to their efficient management accounting system they have a advantage

of reliable management accounts and effective decision making process.( Baldvinsdottir,

Mitchell, and Nørreklit, 2010)

Types of management accounting systems and their need in an organisation

1

Accounting process is related with recording, classifying and summarising the

transactions of business into the financial accounts of business such as journal, ledger and trial

balance in a manner that is easily understandable and comparable to the stakeholders of the

company. This project will discuss about the branch of accounting, which is management

accounting. Management accounting is the process of summarising the details of the financial

statements of the company as well as about the future economic and non economic activities of

the market that will be prevalent in future.( Alleyne, and Weekes-Marshall, 2011) These reports

are then used by the internal management of the Asda Limited so that they can make decision

regarding the formulation of policies and defining objectives in the company. This project will

discuss about the various management accounting systems that are adopted by the organisations

and how different management accounting techniques range are applied in the companies. Uses

of different planning tools in the management accounting process. The report will also perform a

comparison about the ways in which companies like Asda limited use the techniques of

managerial accounting in responding to financial problems.

TASK 1

P1: Management accounting and requirement of various management accounting systems

Management accounting is a process of preparing managerial accounts and reports by the

financial managers to provide reliable and accurate financial and costing data which can be

further used by managers to understand and handle day to day operations of the organisation.

Management accounting also includes translating the financial data into understandable

information which can be used for effective decision making.

Asda limited is a leading supermarket retailer based in United Kingdom, Asda is diverse

in its activities and due to their efficient management accounting system they have a advantage

of reliable management accounts and effective decision making process.( Baldvinsdottir,

Mitchell, and Nørreklit, 2010)

Types of management accounting systems and their need in an organisation

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting systems provides a framework to the organisation to help

managers to prepare accurate management accounts and reports so that sound decisions can be

made.

Product Costing – Product costing management accounting system helps in identifying

all costs involved in production of the products, so that manager of an organisation like

Asda limited can analyse all the expenditures and can manage the allocation of

overheads. This management accounting system is ideal for business of small scale which

has simplicity in their activities and can easily handle allocation of overheads and can

determine profitability, this system also helps to analyse organisational position that at

what point business can face break even condition or no profit no loss condition.

Cost accounting system – Cost accounting system also referred as product costing

system provides a framework to estimate or forecast future costs which can be incurred

by the organisation. Organisations like Asda is beneficial by this management accounting

system as they can analyse their future costs and profitability, Cost accounting system

also forecasts costs of individual functions like costs of inventory, cost of direct material,

direct labour and other variable and fixed costs. Cost accounting system does not gives

accurate costing estimates but the budgeted costs helps in allocation of various

overheads.( Chenhall, and Moers, 2015)

Job Costing – Job costing or job order costing is a method of determining costs for every

manufactured unit, organisations which are engaged in manufacturing unique single units

can get benefited by this management accounting method as it helps in estimating

separate costs involved in each job of manufacturing. This method is appropriate for

those business entities which perform their manufacturing tasks upon order requests.

Asda is a supermarket retail company which is mainly engaged in delivering the goods

and not m,manufacturing it, due to which job order costing unit is not followed by this

company.

Process costing – Process costing is a management accounting system which is similar to

job order costing but it estimates all costs separately involved in various processes, this

type of system or method is appropriate for the organisations which has various

departments or processes like Asda limited. Asda limited is a supermarket retail store

2

managers to prepare accurate management accounts and reports so that sound decisions can be

made.

Product Costing – Product costing management accounting system helps in identifying

all costs involved in production of the products, so that manager of an organisation like

Asda limited can analyse all the expenditures and can manage the allocation of

overheads. This management accounting system is ideal for business of small scale which

has simplicity in their activities and can easily handle allocation of overheads and can

determine profitability, this system also helps to analyse organisational position that at

what point business can face break even condition or no profit no loss condition.

Cost accounting system – Cost accounting system also referred as product costing

system provides a framework to estimate or forecast future costs which can be incurred

by the organisation. Organisations like Asda is beneficial by this management accounting

system as they can analyse their future costs and profitability, Cost accounting system

also forecasts costs of individual functions like costs of inventory, cost of direct material,

direct labour and other variable and fixed costs. Cost accounting system does not gives

accurate costing estimates but the budgeted costs helps in allocation of various

overheads.( Chenhall, and Moers, 2015)

Job Costing – Job costing or job order costing is a method of determining costs for every

manufactured unit, organisations which are engaged in manufacturing unique single units

can get benefited by this management accounting method as it helps in estimating

separate costs involved in each job of manufacturing. This method is appropriate for

those business entities which perform their manufacturing tasks upon order requests.

Asda is a supermarket retail company which is mainly engaged in delivering the goods

and not m,manufacturing it, due to which job order costing unit is not followed by this

company.

Process costing – Process costing is a management accounting system which is similar to

job order costing but it estimates all costs separately involved in various processes, this

type of system or method is appropriate for the organisations which has various

departments or processes like Asda limited. Asda limited is a supermarket retail store

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which has various departments like customer care support department, grocery

department, clothing department, home appliances department etc., where separate costs

are involved and with the help of process costing all these costs can be identified and

profitability can be estimated. Few organisations uses process costing and job order

costing simultaneously which is referred s hybrid management accounting system.

Inventory management system – Inventory management system is a management

accounting system which monitor and maintain the inventory of the organisation either

raw material or goods engaged in work in progress, an efficient inventory management

accounting system maintains the stock through out the manufacturing process from raw

material to finished goods. This management system is ideal for organisations which has

a lot inventories stocked like Asda limited, organisations like Asda is a retail store which

manages and maintains its inventories by the processes involved in inventory

management system.( Dillard, and Roslender, 2011)

Activity based costing – Activity based costing is a management system which

determines cost involved in every activity, this costing system involves two types of costs

that is variable or marginal cost and absorption costs. All variable costs are allocated to

variable or marginal costing overheads whereas in absorption costing overhead all costs

either variable or fixed are included, variable costing is used to determine contribution

and net profits, while absorption costing is used to determine gross profit and net income.

Price optimisation system – Price optimisation system is a method of price

determination for different products; managers of organisations like Asda limited

allocates a price to certain products and also analyse how customers are going to react on

those prices. An effective price optimisation system helps an organisation to earn more

profit by allocating correct prices to the products, if a product's price is too high or too

low it either be undesirable for the customers or non profitable for the organisation,

maintaining a balance between these prices is the real task for managers.

M1: Benefits and applications of management accounting systems

Management accounting systems like job costing or price optimisation system has

universal applicability, these systems are used by every organisation for effective decision

making process. Management accounting system such as job costing or process costing are used

3

department, clothing department, home appliances department etc., where separate costs

are involved and with the help of process costing all these costs can be identified and

profitability can be estimated. Few organisations uses process costing and job order

costing simultaneously which is referred s hybrid management accounting system.

Inventory management system – Inventory management system is a management

accounting system which monitor and maintain the inventory of the organisation either

raw material or goods engaged in work in progress, an efficient inventory management

accounting system maintains the stock through out the manufacturing process from raw

material to finished goods. This management system is ideal for organisations which has

a lot inventories stocked like Asda limited, organisations like Asda is a retail store which

manages and maintains its inventories by the processes involved in inventory

management system.( Dillard, and Roslender, 2011)

Activity based costing – Activity based costing is a management system which

determines cost involved in every activity, this costing system involves two types of costs

that is variable or marginal cost and absorption costs. All variable costs are allocated to

variable or marginal costing overheads whereas in absorption costing overhead all costs

either variable or fixed are included, variable costing is used to determine contribution

and net profits, while absorption costing is used to determine gross profit and net income.

Price optimisation system – Price optimisation system is a method of price

determination for different products; managers of organisations like Asda limited

allocates a price to certain products and also analyse how customers are going to react on

those prices. An effective price optimisation system helps an organisation to earn more

profit by allocating correct prices to the products, if a product's price is too high or too

low it either be undesirable for the customers or non profitable for the organisation,

maintaining a balance between these prices is the real task for managers.

M1: Benefits and applications of management accounting systems

Management accounting systems like job costing or price optimisation system has

universal applicability, these systems are used by every organisation for effective decision

making process. Management accounting system such as job costing or process costing are used

3

to determine costs of specific process or unit whereas systems like product costing or cost

accounting are used determine costs of all the manufactured products. These systems are

appropriate for various kinds of organisations depending on their nature of size, scope and

inventory control. These systems are beneficial for the organisations as they increases efficiency

and profitability of the organisation along with it improves transparency of the cost accounts and

enables flexibility in accounting reports so that it can be changed according to the fluctuations in

the business, it also facilitates the organisation in goal achievement which are pre determined by

the mangers.

D1: Critically evaluate accounting system reporting

As per the accounting reports that are discussed above, it has been observed that all of

them has assisted in providing the maximum outcomes for Asda limited. If the internal

management of the company utilise these reports then these are the reason behind generation of

accurate and reliable outcomes within a less period of time. The main objective of the company

is to achieve all the objectives and aims of the organisation that is been set by the company.

According to this, the performance reports are analysed in much effective manner such the

details of the financial position of the company can be analysed easily.( Endenich, Brandau, and

Hoffjan, 2011)

P2: Explain various methods used in managerial accounting reporting

Management accounting reports are prepared so that the internal management of the

company can formulate policies and define objectives for the efficient functioning of the

company. These reports use the financial as well as non financial transactions that has been

occurred in the companies and these reports also require future economic and non economic

activities that will be implemented in the market in the near future. This is why is becomes very

crucial for the company to prepare these various reports so that managers can easily formulate

and define the policies and objectives of the company. The different types of menagerial

accounting reports include:

Budget reports: Budget reports are formulated by the companies in every area of the

organisation and in every department so that the managers can estimate about the amount of

expenses and revenues that will be reported in undertaking certain activities. The budgets reprots

assists the internal management of the company in financing the funds and formulating the

objectives for each department and overall organisations. These reports also set the performance

4

accounting are used determine costs of all the manufactured products. These systems are

appropriate for various kinds of organisations depending on their nature of size, scope and

inventory control. These systems are beneficial for the organisations as they increases efficiency

and profitability of the organisation along with it improves transparency of the cost accounts and

enables flexibility in accounting reports so that it can be changed according to the fluctuations in

the business, it also facilitates the organisation in goal achievement which are pre determined by

the mangers.

D1: Critically evaluate accounting system reporting

As per the accounting reports that are discussed above, it has been observed that all of

them has assisted in providing the maximum outcomes for Asda limited. If the internal

management of the company utilise these reports then these are the reason behind generation of

accurate and reliable outcomes within a less period of time. The main objective of the company

is to achieve all the objectives and aims of the organisation that is been set by the company.

According to this, the performance reports are analysed in much effective manner such the

details of the financial position of the company can be analysed easily.( Endenich, Brandau, and

Hoffjan, 2011)

P2: Explain various methods used in managerial accounting reporting

Management accounting reports are prepared so that the internal management of the

company can formulate policies and define objectives for the efficient functioning of the

company. These reports use the financial as well as non financial transactions that has been

occurred in the companies and these reports also require future economic and non economic

activities that will be implemented in the market in the near future. This is why is becomes very

crucial for the company to prepare these various reports so that managers can easily formulate

and define the policies and objectives of the company. The different types of menagerial

accounting reports include:

Budget reports: Budget reports are formulated by the companies in every area of the

organisation and in every department so that the managers can estimate about the amount of

expenses and revenues that will be reported in undertaking certain activities. The budgets reprots

assists the internal management of the company in financing the funds and formulating the

objectives for each department and overall organisations. These reports also set the performance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

standards for individual employees and the departments regarding the objectives they are

required to achieve. The managers then use these report in the end of the financial year in

measuring the performances of the employees and analysing whether the set objectives were met

or not and if not what are issues that occurred in achieving the targets and accordingly taking

corrective measures to resolve those issues. The budget reports are formulated at the starting of

the accounting period which helps the concerned person in getting a know-how about what the

organisation is going to do in the coming period.

Accounts receivable reports: This reports are prepared by the managers so that they can

get a idea regarding the total number of debtors that the company have in the current period.

These reports keep a check on the companies accounts receivables regarding when the amount is

to be received from these debtors and which debtors are not paying there amount on due dates.

The report also keep a track record of the amount of bad and doubtful debts of the company. The

main assistance that this report provides to the managers of the company is that it helps in

tightening or loosening the collection period of the company in the upcoming periods.( Gond,

and et. al. 2012)

Job cost reports: In the job cost reports the estimation regarding the information about

the total revenues or total cost that is incurred in producing batch of products or a specific

product. This reports assists the internal management in estimating the total profitability that the

company is making in undertaking a particular job function. This report makes a comparison of

total revenues with the total cost that is incurred in the production of particular product. The

manager uses this in choosing those project which are most profitable and invest more funds in

the projects which are more profitable then other ones.

Relevance of information gathered from management accounting reports:

Decision making: The managerial reports assists the internal management in the decision

making process. The managerial reports provides the information about the financial and non

financial transactions of the company as well as about economic and non economic activities of

the market that will be be prevalent in future. The managers considers all these information in

formulating the policies of the company and defining the objectives so that no hindrance is

occurred in the operations of business in future.

Cost reduction: The managerial accounting reports helps the management in formulating

policies and objectives by considering all the factors and thus does not cause any form of issues

5

required to achieve. The managers then use these report in the end of the financial year in

measuring the performances of the employees and analysing whether the set objectives were met

or not and if not what are issues that occurred in achieving the targets and accordingly taking

corrective measures to resolve those issues. The budget reports are formulated at the starting of

the accounting period which helps the concerned person in getting a know-how about what the

organisation is going to do in the coming period.

Accounts receivable reports: This reports are prepared by the managers so that they can

get a idea regarding the total number of debtors that the company have in the current period.

These reports keep a check on the companies accounts receivables regarding when the amount is

to be received from these debtors and which debtors are not paying there amount on due dates.

The report also keep a track record of the amount of bad and doubtful debts of the company. The

main assistance that this report provides to the managers of the company is that it helps in

tightening or loosening the collection period of the company in the upcoming periods.( Gond,

and et. al. 2012)

Job cost reports: In the job cost reports the estimation regarding the information about

the total revenues or total cost that is incurred in producing batch of products or a specific

product. This reports assists the internal management in estimating the total profitability that the

company is making in undertaking a particular job function. This report makes a comparison of

total revenues with the total cost that is incurred in the production of particular product. The

manager uses this in choosing those project which are most profitable and invest more funds in

the projects which are more profitable then other ones.

Relevance of information gathered from management accounting reports:

Decision making: The managerial reports assists the internal management in the decision

making process. The managerial reports provides the information about the financial and non

financial transactions of the company as well as about economic and non economic activities of

the market that will be be prevalent in future. The managers considers all these information in

formulating the policies of the company and defining the objectives so that no hindrance is

occurred in the operations of business in future.

Cost reduction: The managerial accounting reports helps the management in formulating

policies and objectives by considering all the factors and thus does not cause any form of issues

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the future operation which in turn reduces the cost of resolving these problems if they have

occurred in future.

Increasing Financial returns: The reports that are made under management accounting

such as budget reports assists the management in getting a summary of the financial reports of

the company and thus helps in analysing projects which are suitable and profitable of the

company as per future trends of the market. ( Lavia López, and Hiebl, 2014)

TASK 2

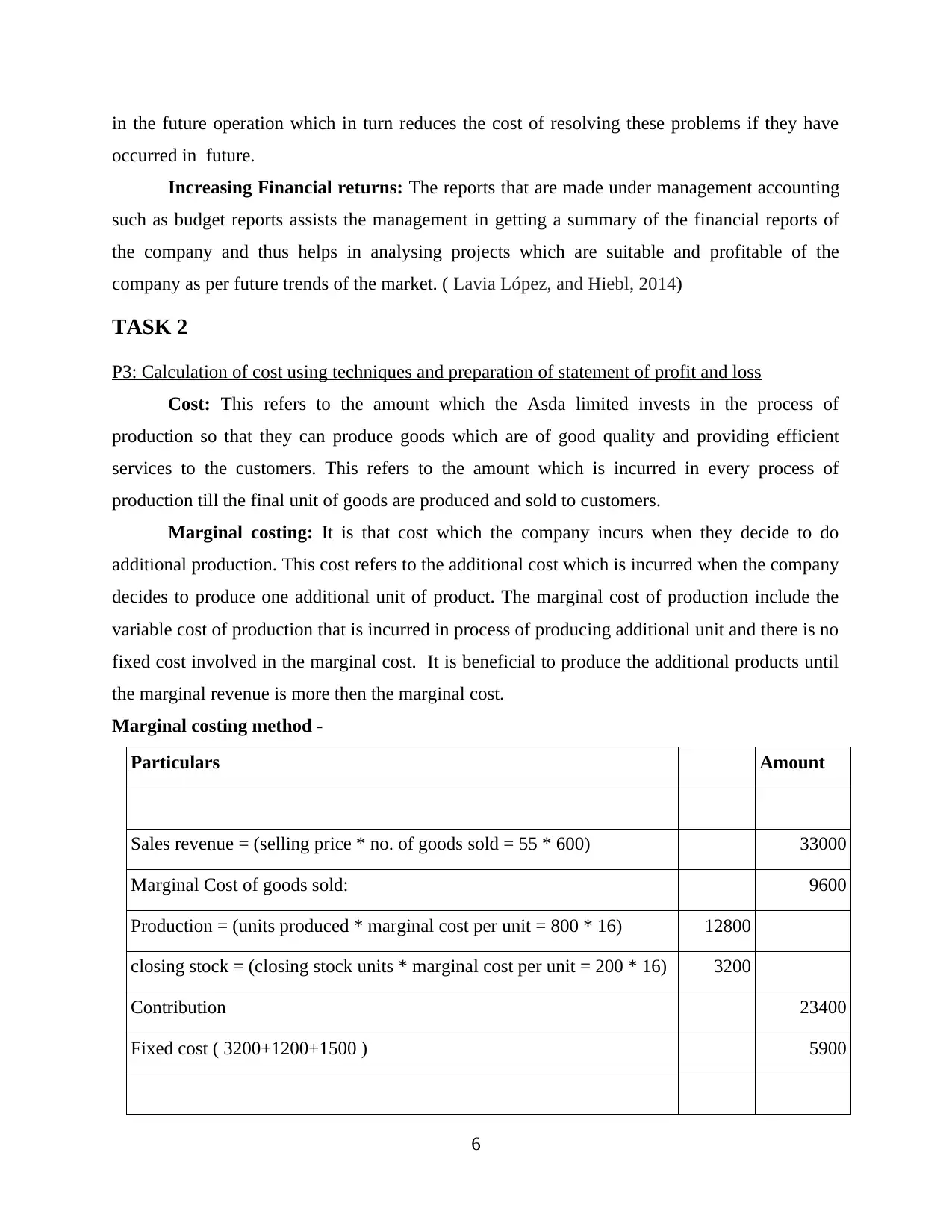

P3: Calculation of cost using techniques and preparation of statement of profit and loss

Cost: This refers to the amount which the Asda limited invests in the process of

production so that they can produce goods which are of good quality and providing efficient

services to the customers. This refers to the amount which is incurred in every process of

production till the final unit of goods are produced and sold to customers.

Marginal costing: It is that cost which the company incurs when they decide to do

additional production. This cost refers to the additional cost which is incurred when the company

decides to produce one additional unit of product. The marginal cost of production include the

variable cost of production that is incurred in process of producing additional unit and there is no

fixed cost involved in the marginal cost. It is beneficial to produce the additional products until

the marginal revenue is more then the marginal cost.

Marginal costing method -

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

6

occurred in future.

Increasing Financial returns: The reports that are made under management accounting

such as budget reports assists the management in getting a summary of the financial reports of

the company and thus helps in analysing projects which are suitable and profitable of the

company as per future trends of the market. ( Lavia López, and Hiebl, 2014)

TASK 2

P3: Calculation of cost using techniques and preparation of statement of profit and loss

Cost: This refers to the amount which the Asda limited invests in the process of

production so that they can produce goods which are of good quality and providing efficient

services to the customers. This refers to the amount which is incurred in every process of

production till the final unit of goods are produced and sold to customers.

Marginal costing: It is that cost which the company incurs when they decide to do

additional production. This cost refers to the additional cost which is incurred when the company

decides to produce one additional unit of product. The marginal cost of production include the

variable cost of production that is incurred in process of producing additional unit and there is no

fixed cost involved in the marginal cost. It is beneficial to produce the additional products until

the marginal revenue is more then the marginal cost.

Marginal costing method -

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

6

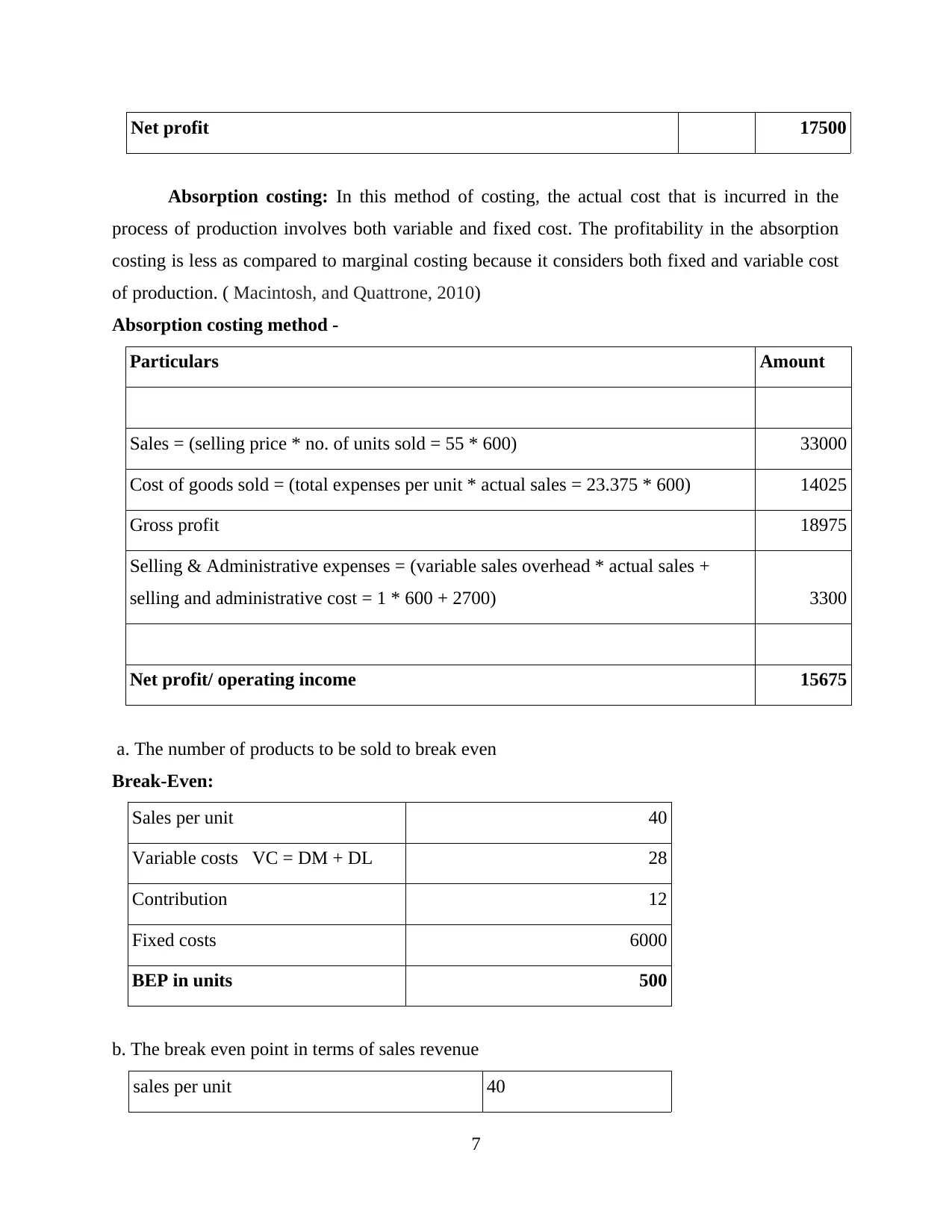

Net profit 17500

Absorption costing: In this method of costing, the actual cost that is incurred in the

process of production involves both variable and fixed cost. The profitability in the absorption

costing is less as compared to marginal costing because it considers both fixed and variable cost

of production. ( Macintosh, and Quattrone, 2010)

Absorption costing method -

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

a. The number of products to be sold to break even

Break-Even:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. The break even point in terms of sales revenue

sales per unit 40

7

Absorption costing: In this method of costing, the actual cost that is incurred in the

process of production involves both variable and fixed cost. The profitability in the absorption

costing is less as compared to marginal costing because it considers both fixed and variable cost

of production. ( Macintosh, and Quattrone, 2010)

Absorption costing method -

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

a. The number of products to be sold to break even

Break-Even:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. The break even point in terms of sales revenue

sales per unit 40

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

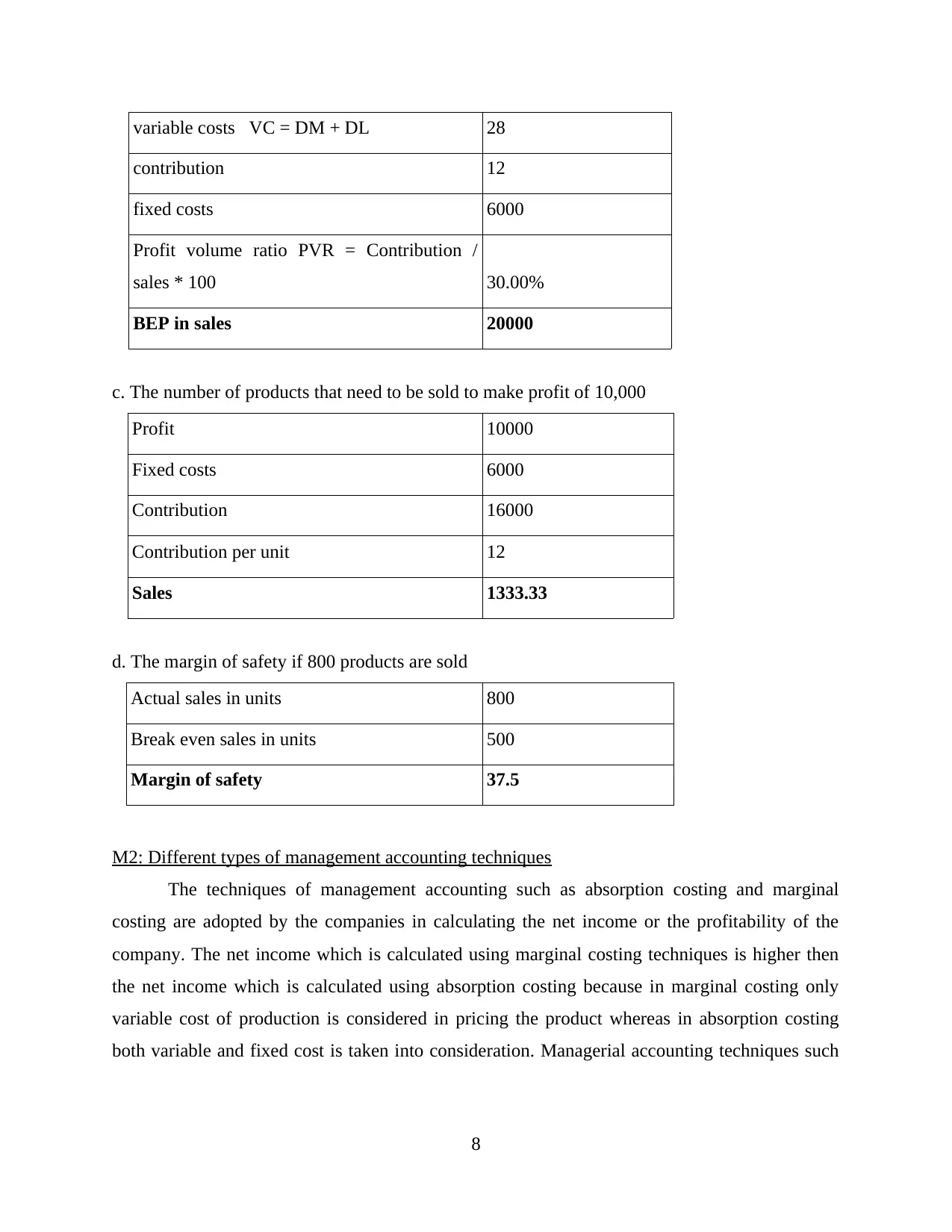

variable costs VC = DM + DL 28

contribution 12

fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Different types of management accounting techniques

The techniques of management accounting such as absorption costing and marginal

costing are adopted by the companies in calculating the net income or the profitability of the

company. The net income which is calculated using marginal costing techniques is higher then

the net income which is calculated using absorption costing because in marginal costing only

variable cost of production is considered in pricing the product whereas in absorption costing

both variable and fixed cost is taken into consideration. Managerial accounting techniques such

8

contribution 12

fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Different types of management accounting techniques

The techniques of management accounting such as absorption costing and marginal

costing are adopted by the companies in calculating the net income or the profitability of the

company. The net income which is calculated using marginal costing techniques is higher then

the net income which is calculated using absorption costing because in marginal costing only

variable cost of production is considered in pricing the product whereas in absorption costing

both variable and fixed cost is taken into consideration. Managerial accounting techniques such

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as historical costing and standard costing are not considered by the Asda limited as the marginal

and absorption methods seems more suitable to the company as per its production capacity.

D2: Interpretation:

As per the above calculations, it has been observed that organisation can earn a profit on

their sales if they produce goods more then 500 units as at this point the company achieves break

even point, which is a situation of no profit and no loss. The above mentioned organisation needs

to sell a minimum of 1334 units in order to earn a profit on the total sales of 10000. with the use

of these techniques the organisation can easily determine the profits of the company.

TASK 3

P4: Advantages and Disadvantages of different types of budgetary controls

The different types of budgets which are prepared by the internal management of the

company in order to increase the efficiency of the company. The budgets that are prepared by the

companies include operational budget, master budget, cash flow budget etc. Descriptions of

these budgets are as under:

Operational budget: The operational budget of the companies include the cost and revenue that

is incurred in the day to day operations of the company. The costs that are taken into

consideration are administrative and overheads costs that are required to be ascertained by the

management of the company. ( Otley, and Emmanuel, 2013)

Advantages: The advantage of this budget is that it covers the revenue and cost that is

incurred in daily operations. It helps in minimising the expenses that may be incurred in

future business operations.

Disadvantages: Preparation of operational budgets require a lot of time.

Cash flow Budget: The cash flow budget helps the management of company in managing the

cash of the organisation. This budget helps in determining the daily outflow and inflow of the

company in its daily operations. Hence, for managing the daily cash requirements in an effective

and efficient manner the managers acquire funds from only those sources where there is capacity

of repayment.

Advantages: This budget helps the management in maintaining sufficient amount of

cash in the company so the operations of company does not get hindered.

9

and absorption methods seems more suitable to the company as per its production capacity.

D2: Interpretation:

As per the above calculations, it has been observed that organisation can earn a profit on

their sales if they produce goods more then 500 units as at this point the company achieves break

even point, which is a situation of no profit and no loss. The above mentioned organisation needs

to sell a minimum of 1334 units in order to earn a profit on the total sales of 10000. with the use

of these techniques the organisation can easily determine the profits of the company.

TASK 3

P4: Advantages and Disadvantages of different types of budgetary controls

The different types of budgets which are prepared by the internal management of the

company in order to increase the efficiency of the company. The budgets that are prepared by the

companies include operational budget, master budget, cash flow budget etc. Descriptions of

these budgets are as under:

Operational budget: The operational budget of the companies include the cost and revenue that

is incurred in the day to day operations of the company. The costs that are taken into

consideration are administrative and overheads costs that are required to be ascertained by the

management of the company. ( Otley, and Emmanuel, 2013)

Advantages: The advantage of this budget is that it covers the revenue and cost that is

incurred in daily operations. It helps in minimising the expenses that may be incurred in

future business operations.

Disadvantages: Preparation of operational budgets require a lot of time.

Cash flow Budget: The cash flow budget helps the management of company in managing the

cash of the organisation. This budget helps in determining the daily outflow and inflow of the

company in its daily operations. Hence, for managing the daily cash requirements in an effective

and efficient manner the managers acquire funds from only those sources where there is capacity

of repayment.

Advantages: This budget helps the management in maintaining sufficient amount of

cash in the company so the operations of company does not get hindered.

9

Disadvantages: Maintaining the cash outflow and inflow of the company becomes

critical for the managers.

Fixed Budget: These budgets are prepared at the starting of the financial year for recording the

expenses and costs of business which are fixed in nature. The fixed budgets are not modified if

the company decided to do more production or sales in the upcoming period. The modifications

are not allowed in financial plans according to this budget.

Advantages: This budget helps the small organisation in measuring their growth and

profitability.

Disadvantages: The only demerit of this budget is that it can not be modified according

to the needs of the management in the future if they try to change the production of the

company.

Master Budget: The master budget is prepared by the managers so that they can forecast

the amount of sales in future, production level, required capital investment in the execution of

future operations of business. The budgets are formulated for the purpose of setting the

performance standards and creating effective plans.

Advantages: this budget assist in determining the overall cost that will be incurred in the

production process.

Disadvantages: master budgets are formulated for a specific production process and

thus accuracy and reliability of information is decreased.( Qian, Burritt,and Monroe,

2011)

Various pricing Systems:

Full cost pricing: According to this strategy of pricing the organisations determine the

value of the services and product on the basis of all types of direct cost such as direct material,

direct labour etc. that is incurred in the process of production.

Cost plus pricing: this pricing method takes into consideration the cost of factors of

productions such as direct labour, direct material and other overheads for the the determination

of the prices of products and services.

Marginal cost pricing: as per this pricing strategy the prices of the products and services

are determined on the basis of the cost that is incurred for the production of additional unit iof

product. The marginal cost only includes variable cost of production.

Different costing systems:

10

critical for the managers.

Fixed Budget: These budgets are prepared at the starting of the financial year for recording the

expenses and costs of business which are fixed in nature. The fixed budgets are not modified if

the company decided to do more production or sales in the upcoming period. The modifications

are not allowed in financial plans according to this budget.

Advantages: This budget helps the small organisation in measuring their growth and

profitability.

Disadvantages: The only demerit of this budget is that it can not be modified according

to the needs of the management in the future if they try to change the production of the

company.

Master Budget: The master budget is prepared by the managers so that they can forecast

the amount of sales in future, production level, required capital investment in the execution of

future operations of business. The budgets are formulated for the purpose of setting the

performance standards and creating effective plans.

Advantages: this budget assist in determining the overall cost that will be incurred in the

production process.

Disadvantages: master budgets are formulated for a specific production process and

thus accuracy and reliability of information is decreased.( Qian, Burritt,and Monroe,

2011)

Various pricing Systems:

Full cost pricing: According to this strategy of pricing the organisations determine the

value of the services and product on the basis of all types of direct cost such as direct material,

direct labour etc. that is incurred in the process of production.

Cost plus pricing: this pricing method takes into consideration the cost of factors of

productions such as direct labour, direct material and other overheads for the the determination

of the prices of products and services.

Marginal cost pricing: as per this pricing strategy the prices of the products and services

are determined on the basis of the cost that is incurred for the production of additional unit iof

product. The marginal cost only includes variable cost of production.

Different costing systems:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.