Analysis of Management Accounting Techniques for AIRDRI Ltd (UK)

VerifiedAdded on 2021/01/02

|17

|5085

|376

Report

AI Summary

This report delves into management accounting, focusing on costing techniques and budgetary control. It examines marginal and absorption costing methods through the analysis of financial data from AIRDRI Ltd. (U.K), an air dryer manufacturing company. The report provides detailed income statements using both costing methods and interprets the financial data to illustrate their application. Furthermore, the report explores the advantages and disadvantages of various planning tools used for budgetary control, including fixed and flexible budgets. The application of management accounting techniques to solve financial problems is also discussed, providing a comprehensive overview of the subject. The report concludes with a summary of the findings and references used.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P3. Cost Accounting techniques of management accounting ...............................................1

M2 Application of range of management accounting techniques..........................................4

D2 Interpretation of financial data regarding the business Activities ..................................4

TASK 2............................................................................................................................................4

P4 Advantages and Disadvantages of different types of planning tools used for Budgetary

Control....................................................................................................................................4

M3 Analysation of different planning tools for preparing and forecasting the budgets........8

P5 Comparison of Organisations adapting management accounting systems to resolve

financial issues........................................................................................................................8

M4 Management accounting helpful in solving the financial problems.............................11

D3 Planning tools are helpful in solving the financial problems of organisation .............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P3. Cost Accounting techniques of management accounting ...............................................1

M2 Application of range of management accounting techniques..........................................4

D2 Interpretation of financial data regarding the business Activities ..................................4

TASK 2............................................................................................................................................4

P4 Advantages and Disadvantages of different types of planning tools used for Budgetary

Control....................................................................................................................................4

M3 Analysation of different planning tools for preparing and forecasting the budgets........8

P5 Comparison of Organisations adapting management accounting systems to resolve

financial issues........................................................................................................................8

M4 Management accounting helpful in solving the financial problems.............................11

D3 Planning tools are helpful in solving the financial problems of organisation .............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting refers to the managerial accounting and also known as cost

accounting, it the process of Identifying, measuring, analysing, interpreting and communicating

information to managers for the achieve the organisational goals. Although, the financial

accounting plays dominant role in functioning of management accounting as on the basis of

financial accounting managers are able to make the business operations decisions, means

financial accounting provides the financial information to managers in order to perform the

management accounting functions. Management accounting comprises with all fields of

accounting with a motive to informing management of business operation metrics. Although it is

related with the costs of products or services acquired by the organisation also budgets are also

decided under the management accounting plans and prepares the organisational performance

reports. (Amidu, Effah and Abor, 2011)

This study pertain the information about the information analyses of Income statement

by marginal and absorption costing method, of AIRDRI Ltd. (U.K) an air dryer manufacturing

company of United Kingdom management accounting system and techniques or costing methods

with appropriate financial statement in order to present systematic analysation. Not only this,

advantages and disadvantages of budgets, planning tools and their applications and an attempt to

solve the financial problems with appropriate planning tools.

TASK 1

P3. Cost Accounting techniques of management accounting

Costing: The term 'costing' also known as cost accountancy, it is the process of

quantifying the costs and it is a technique to assist the management in establishing several

budgets, standards and ascertain the cost of production of any product or services in the business

organisation. The cost accounting is practised at broad level in big manufacturing industries

which produces in thousands of products in very large quantity and spends lot of money on

labour, material and on other overheads. The recording and analysation of these incurred cost in

order to generate the income are comes in context of cost accounting as after the evaluation the

calculation of profit generated from these activities is made. Although the cost accounting or

costing involves some techniques of costing.(Carlsson-Wall, Kraus and Lind, 2015)

1

Management Accounting refers to the managerial accounting and also known as cost

accounting, it the process of Identifying, measuring, analysing, interpreting and communicating

information to managers for the achieve the organisational goals. Although, the financial

accounting plays dominant role in functioning of management accounting as on the basis of

financial accounting managers are able to make the business operations decisions, means

financial accounting provides the financial information to managers in order to perform the

management accounting functions. Management accounting comprises with all fields of

accounting with a motive to informing management of business operation metrics. Although it is

related with the costs of products or services acquired by the organisation also budgets are also

decided under the management accounting plans and prepares the organisational performance

reports. (Amidu, Effah and Abor, 2011)

This study pertain the information about the information analyses of Income statement

by marginal and absorption costing method, of AIRDRI Ltd. (U.K) an air dryer manufacturing

company of United Kingdom management accounting system and techniques or costing methods

with appropriate financial statement in order to present systematic analysation. Not only this,

advantages and disadvantages of budgets, planning tools and their applications and an attempt to

solve the financial problems with appropriate planning tools.

TASK 1

P3. Cost Accounting techniques of management accounting

Costing: The term 'costing' also known as cost accountancy, it is the process of

quantifying the costs and it is a technique to assist the management in establishing several

budgets, standards and ascertain the cost of production of any product or services in the business

organisation. The cost accounting is practised at broad level in big manufacturing industries

which produces in thousands of products in very large quantity and spends lot of money on

labour, material and on other overheads. The recording and analysation of these incurred cost in

order to generate the income are comes in context of cost accounting as after the evaluation the

calculation of profit generated from these activities is made. Although the cost accounting or

costing involves some techniques of costing.(Carlsson-Wall, Kraus and Lind, 2015)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

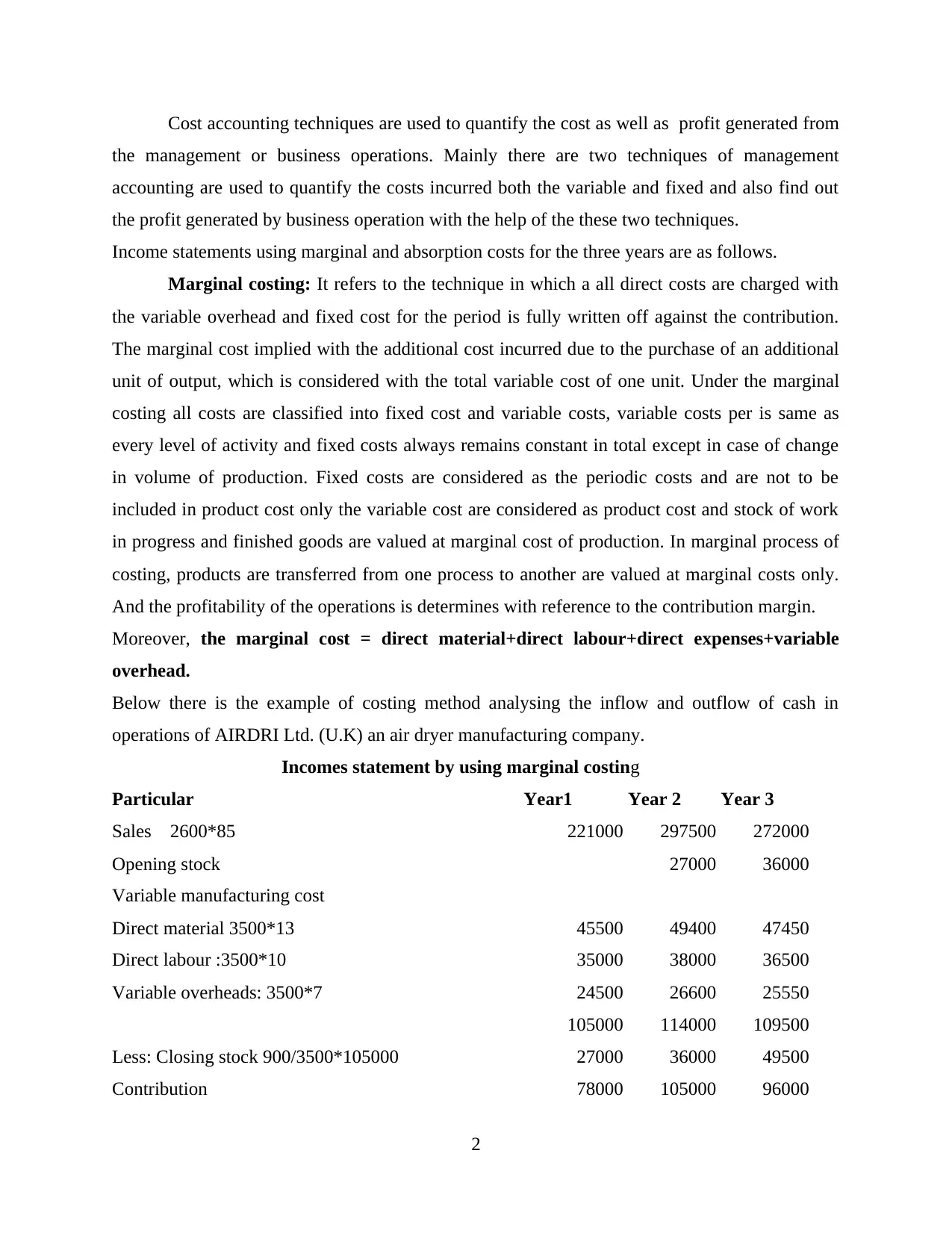

Cost accounting techniques are used to quantify the cost as well as profit generated from

the management or business operations. Mainly there are two techniques of management

accounting are used to quantify the costs incurred both the variable and fixed and also find out

the profit generated by business operation with the help of the these two techniques.

Income statements using marginal and absorption costs for the three years are as follows.

Marginal costing: It refers to the technique in which a all direct costs are charged with

the variable overhead and fixed cost for the period is fully written off against the contribution.

The marginal cost implied with the additional cost incurred due to the purchase of an additional

unit of output, which is considered with the total variable cost of one unit. Under the marginal

costing all costs are classified into fixed cost and variable costs, variable costs per is same as

every level of activity and fixed costs always remains constant in total except in case of change

in volume of production. Fixed costs are considered as the periodic costs and are not to be

included in product cost only the variable cost are considered as product cost and stock of work

in progress and finished goods are valued at marginal cost of production. In marginal process of

costing, products are transferred from one process to another are valued at marginal costs only.

And the profitability of the operations is determines with reference to the contribution margin.

Moreover, the marginal cost = direct material+direct labour+direct expenses+variable

overhead.

Below there is the example of costing method analysing the inflow and outflow of cash in

operations of AIRDRI Ltd. (U.K) an air dryer manufacturing company.

Incomes statement by using marginal costing

Particular Year1 Year 2 Year 3

Sales 2600*85 221000 297500 272000

Opening stock 27000 36000

Variable manufacturing cost

Direct material 3500*13 45500 49400 47450

Direct labour :3500*10 35000 38000 36500

Variable overheads: 3500*7 24500 26600 25550

105000 114000 109500

Less: Closing stock 900/3500*105000 27000 36000 49500

Contribution 78000 105000 96000

2

the management or business operations. Mainly there are two techniques of management

accounting are used to quantify the costs incurred both the variable and fixed and also find out

the profit generated by business operation with the help of the these two techniques.

Income statements using marginal and absorption costs for the three years are as follows.

Marginal costing: It refers to the technique in which a all direct costs are charged with

the variable overhead and fixed cost for the period is fully written off against the contribution.

The marginal cost implied with the additional cost incurred due to the purchase of an additional

unit of output, which is considered with the total variable cost of one unit. Under the marginal

costing all costs are classified into fixed cost and variable costs, variable costs per is same as

every level of activity and fixed costs always remains constant in total except in case of change

in volume of production. Fixed costs are considered as the periodic costs and are not to be

included in product cost only the variable cost are considered as product cost and stock of work

in progress and finished goods are valued at marginal cost of production. In marginal process of

costing, products are transferred from one process to another are valued at marginal costs only.

And the profitability of the operations is determines with reference to the contribution margin.

Moreover, the marginal cost = direct material+direct labour+direct expenses+variable

overhead.

Below there is the example of costing method analysing the inflow and outflow of cash in

operations of AIRDRI Ltd. (U.K) an air dryer manufacturing company.

Incomes statement by using marginal costing

Particular Year1 Year 2 Year 3

Sales 2600*85 221000 297500 272000

Opening stock 27000 36000

Variable manufacturing cost

Direct material 3500*13 45500 49400 47450

Direct labour :3500*10 35000 38000 36500

Variable overheads: 3500*7 24500 26600 25550

105000 114000 109500

Less: Closing stock 900/3500*105000 27000 36000 49500

Contribution 78000 105000 96000

2

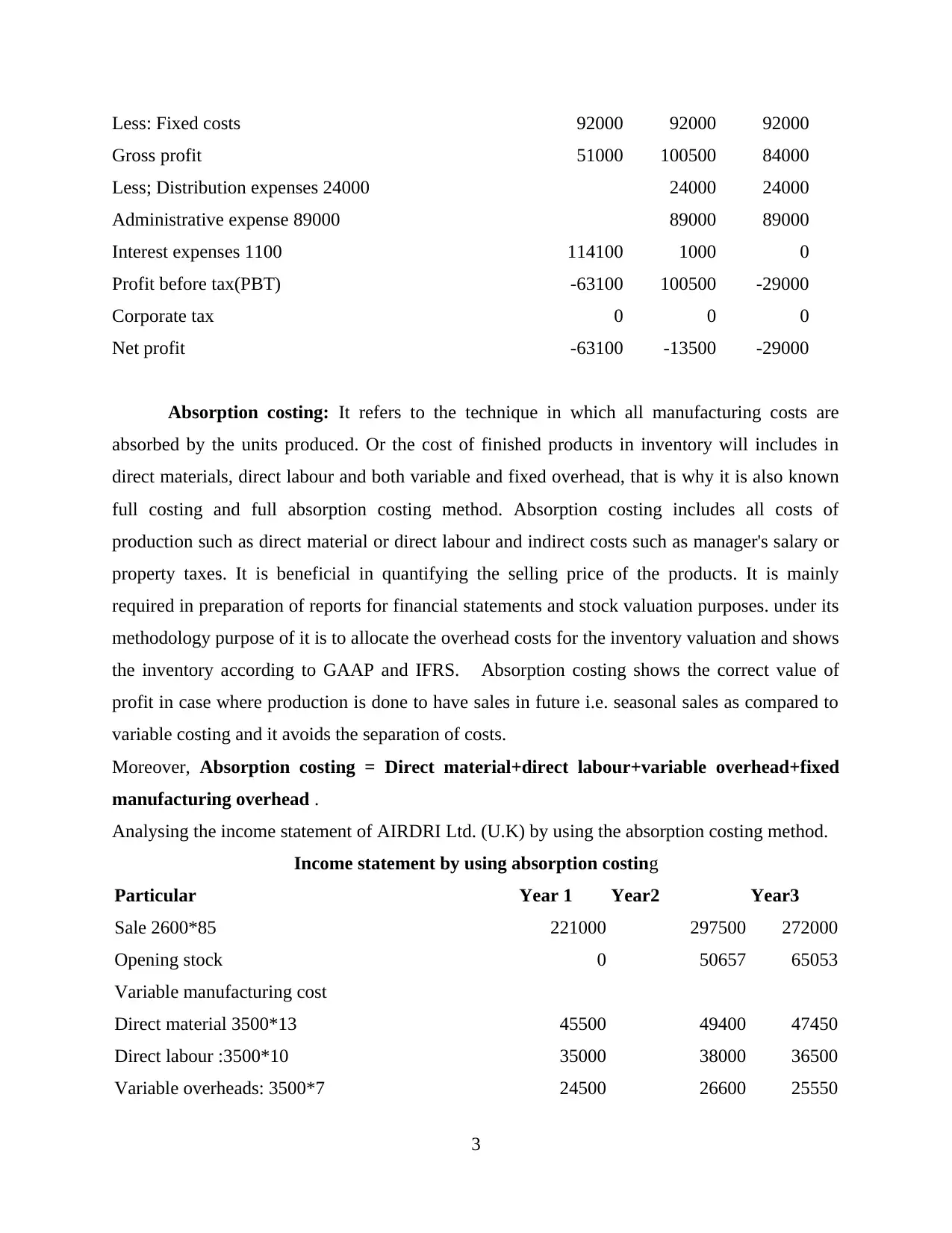

Less: Fixed costs 92000 92000 92000

Gross profit 51000 100500 84000

Less; Distribution expenses 24000 24000 24000

Administrative expense 89000 89000 89000

Interest expenses 1100 114100 1000 0

Profit before tax(PBT) -63100 100500 -29000

Corporate tax 0 0 0

Net profit -63100 -13500 -29000

Absorption costing: It refers to the technique in which all manufacturing costs are

absorbed by the units produced. Or the cost of finished products in inventory will includes in

direct materials, direct labour and both variable and fixed overhead, that is why it is also known

full costing and full absorption costing method. Absorption costing includes all costs of

production such as direct material or direct labour and indirect costs such as manager's salary or

property taxes. It is beneficial in quantifying the selling price of the products. It is mainly

required in preparation of reports for financial statements and stock valuation purposes. under its

methodology purpose of it is to allocate the overhead costs for the inventory valuation and shows

the inventory according to GAAP and IFRS. Absorption costing shows the correct value of

profit in case where production is done to have sales in future i.e. seasonal sales as compared to

variable costing and it avoids the separation of costs.

Moreover, Absorption costing = Direct material+direct labour+variable overhead+fixed

manufacturing overhead .

Analysing the income statement of AIRDRI Ltd. (U.K) by using the absorption costing method.

Income statement by using absorption costing

Particular Year 1 Year2 Year3

Sale 2600*85 221000 297500 272000

Opening stock 0 50657 65053

Variable manufacturing cost

Direct material 3500*13 45500 49400 47450

Direct labour :3500*10 35000 38000 36500

Variable overheads: 3500*7 24500 26600 25550

3

Gross profit 51000 100500 84000

Less; Distribution expenses 24000 24000 24000

Administrative expense 89000 89000 89000

Interest expenses 1100 114100 1000 0

Profit before tax(PBT) -63100 100500 -29000

Corporate tax 0 0 0

Net profit -63100 -13500 -29000

Absorption costing: It refers to the technique in which all manufacturing costs are

absorbed by the units produced. Or the cost of finished products in inventory will includes in

direct materials, direct labour and both variable and fixed overhead, that is why it is also known

full costing and full absorption costing method. Absorption costing includes all costs of

production such as direct material or direct labour and indirect costs such as manager's salary or

property taxes. It is beneficial in quantifying the selling price of the products. It is mainly

required in preparation of reports for financial statements and stock valuation purposes. under its

methodology purpose of it is to allocate the overhead costs for the inventory valuation and shows

the inventory according to GAAP and IFRS. Absorption costing shows the correct value of

profit in case where production is done to have sales in future i.e. seasonal sales as compared to

variable costing and it avoids the separation of costs.

Moreover, Absorption costing = Direct material+direct labour+variable overhead+fixed

manufacturing overhead .

Analysing the income statement of AIRDRI Ltd. (U.K) by using the absorption costing method.

Income statement by using absorption costing

Particular Year 1 Year2 Year3

Sale 2600*85 221000 297500 272000

Opening stock 0 50657 65053

Variable manufacturing cost

Direct material 3500*13 45500 49400 47450

Direct labour :3500*10 35000 38000 36500

Variable overheads: 3500*7 24500 26600 25550

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

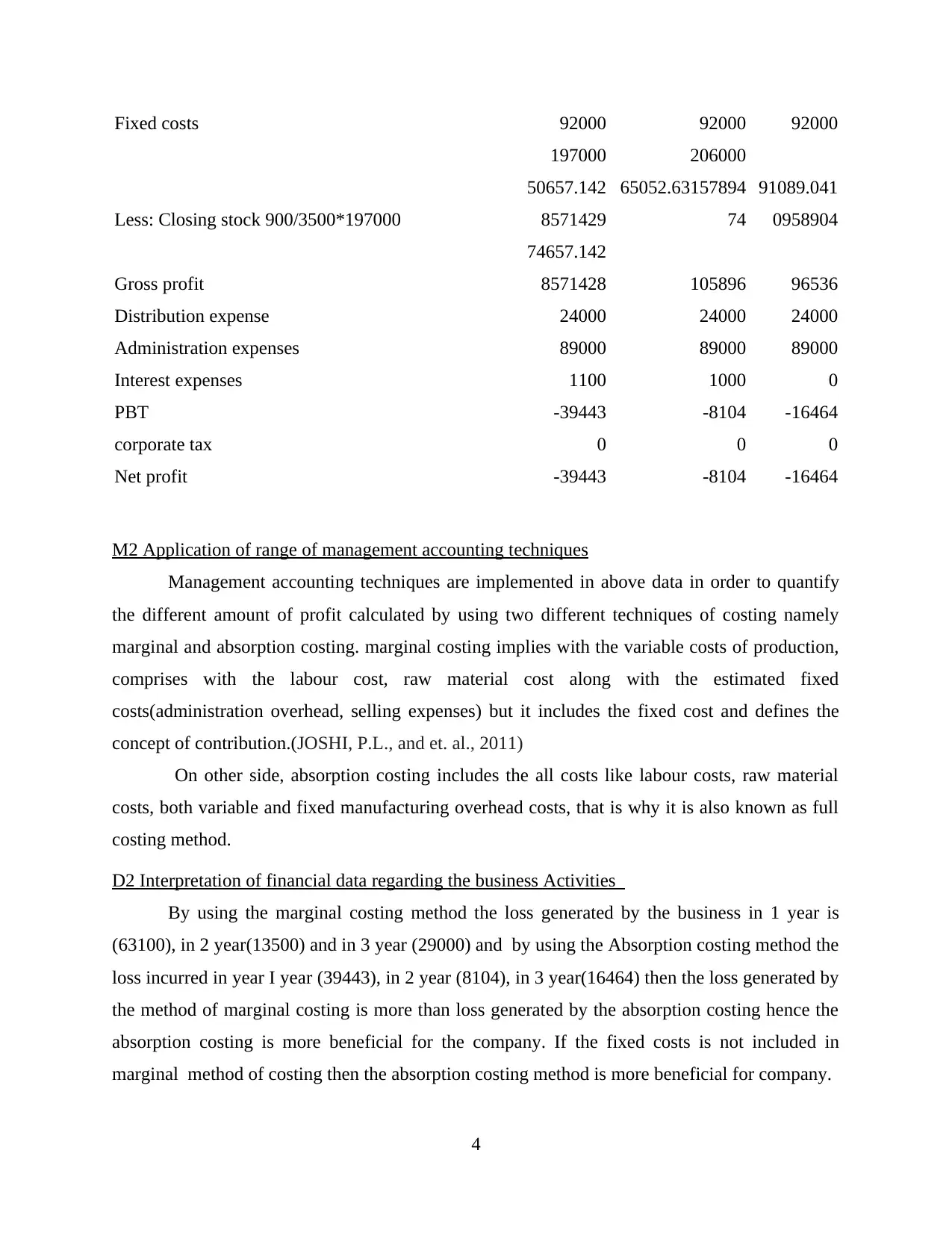

Fixed costs 92000 92000 92000

197000 206000

Less: Closing stock 900/3500*197000

50657.142

8571429

65052.63157894

74

91089.041

0958904

Gross profit

74657.142

8571428 105896 96536

Distribution expense 24000 24000 24000

Administration expenses 89000 89000 89000

Interest expenses 1100 1000 0

PBT -39443 -8104 -16464

corporate tax 0 0 0

Net profit -39443 -8104 -16464

M2 Application of range of management accounting techniques

Management accounting techniques are implemented in above data in order to quantify

the different amount of profit calculated by using two different techniques of costing namely

marginal and absorption costing. marginal costing implies with the variable costs of production,

comprises with the labour cost, raw material cost along with the estimated fixed

costs(administration overhead, selling expenses) but it includes the fixed cost and defines the

concept of contribution.(JOSHI, P.L., and et. al., 2011)

On other side, absorption costing includes the all costs like labour costs, raw material

costs, both variable and fixed manufacturing overhead costs, that is why it is also known as full

costing method.

D2 Interpretation of financial data regarding the business Activities

By using the marginal costing method the loss generated by the business in 1 year is

(63100), in 2 year(13500) and in 3 year (29000) and by using the Absorption costing method the

loss incurred in year I year (39443), in 2 year (8104), in 3 year(16464) then the loss generated by

the method of marginal costing is more than loss generated by the absorption costing hence the

absorption costing is more beneficial for the company. If the fixed costs is not included in

marginal method of costing then the absorption costing method is more beneficial for company.

4

197000 206000

Less: Closing stock 900/3500*197000

50657.142

8571429

65052.63157894

74

91089.041

0958904

Gross profit

74657.142

8571428 105896 96536

Distribution expense 24000 24000 24000

Administration expenses 89000 89000 89000

Interest expenses 1100 1000 0

PBT -39443 -8104 -16464

corporate tax 0 0 0

Net profit -39443 -8104 -16464

M2 Application of range of management accounting techniques

Management accounting techniques are implemented in above data in order to quantify

the different amount of profit calculated by using two different techniques of costing namely

marginal and absorption costing. marginal costing implies with the variable costs of production,

comprises with the labour cost, raw material cost along with the estimated fixed

costs(administration overhead, selling expenses) but it includes the fixed cost and defines the

concept of contribution.(JOSHI, P.L., and et. al., 2011)

On other side, absorption costing includes the all costs like labour costs, raw material

costs, both variable and fixed manufacturing overhead costs, that is why it is also known as full

costing method.

D2 Interpretation of financial data regarding the business Activities

By using the marginal costing method the loss generated by the business in 1 year is

(63100), in 2 year(13500) and in 3 year (29000) and by using the Absorption costing method the

loss incurred in year I year (39443), in 2 year (8104), in 3 year(16464) then the loss generated by

the method of marginal costing is more than loss generated by the absorption costing hence the

absorption costing is more beneficial for the company. If the fixed costs is not included in

marginal method of costing then the absorption costing method is more beneficial for company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P4 Advantages and Disadvantages of different types of planning tools used for Budgetary

Control

Budgetary Control: Budgetary control is a system, which includes preparation of

budgets, establishing responsibilities and coordinating with the department for controlling costs.

Their main motive is to evaluate, control day to day operations with a specified goal.(Johnson,

2013) Moreover it is the process of quantifying several actual results with the budgeted figures

for the enterprise for the future period and standards set after that the comparison is made

between the budgeted figures and actual performance for calculating deviations or differences,

because budgets are prepared first then actual results are recorded and analysed and it focuses on

controlling costs for which several budgets are prepared on the basis of past records, planned

budgets are based on the predictions so after the implementation the actual performance with the

budgeted and acting upon the results to accomplish the key performance indicators and goals,

also helpful in profit maximisation.

Budget: A budget is an estimated value of revenue and expenses for a specified future

date. For an organization it is an internal tool. The firm drawn up their budget for the upcoming

financial year.

Advantages: It is based on achieving financial goals either in short-term, medium-term

and long-term. Goal of a person is in allocating their pay off debt for saving or

retirement. For achieving objectives the company uses accurate accounting systems and

disciplined focus. The benefit of budget is to deal with the unexpected expenses (Ijiri,

2015).

Disadvantages: Slow preparation of budget arises disputes. As increasing use of

budgeting work reduces control from actual results. It emphasises short term benefit

which detriment of long term goals. Their basic disadvantage is time consuming and

costly. They may create conflicts within an organization.

Fixed Budget: Fixed budget is a budget which changes when its sales and other activities

increases or decreases (Chenhall and Morris, 2016). Their main purpose is to sell specific goods

according to financial plan.

It is based on sales and revenues. Fixed budget remains constant or does not flex when sales or

other activities increases or decreases. It is also known as static budget.

5

P4 Advantages and Disadvantages of different types of planning tools used for Budgetary

Control

Budgetary Control: Budgetary control is a system, which includes preparation of

budgets, establishing responsibilities and coordinating with the department for controlling costs.

Their main motive is to evaluate, control day to day operations with a specified goal.(Johnson,

2013) Moreover it is the process of quantifying several actual results with the budgeted figures

for the enterprise for the future period and standards set after that the comparison is made

between the budgeted figures and actual performance for calculating deviations or differences,

because budgets are prepared first then actual results are recorded and analysed and it focuses on

controlling costs for which several budgets are prepared on the basis of past records, planned

budgets are based on the predictions so after the implementation the actual performance with the

budgeted and acting upon the results to accomplish the key performance indicators and goals,

also helpful in profit maximisation.

Budget: A budget is an estimated value of revenue and expenses for a specified future

date. For an organization it is an internal tool. The firm drawn up their budget for the upcoming

financial year.

Advantages: It is based on achieving financial goals either in short-term, medium-term

and long-term. Goal of a person is in allocating their pay off debt for saving or

retirement. For achieving objectives the company uses accurate accounting systems and

disciplined focus. The benefit of budget is to deal with the unexpected expenses (Ijiri,

2015).

Disadvantages: Slow preparation of budget arises disputes. As increasing use of

budgeting work reduces control from actual results. It emphasises short term benefit

which detriment of long term goals. Their basic disadvantage is time consuming and

costly. They may create conflicts within an organization.

Fixed Budget: Fixed budget is a budget which changes when its sales and other activities

increases or decreases (Chenhall and Morris, 2016). Their main purpose is to sell specific goods

according to financial plan.

It is based on sales and revenues. Fixed budget remains constant or does not flex when sales or

other activities increases or decreases. It is also known as static budget.

5

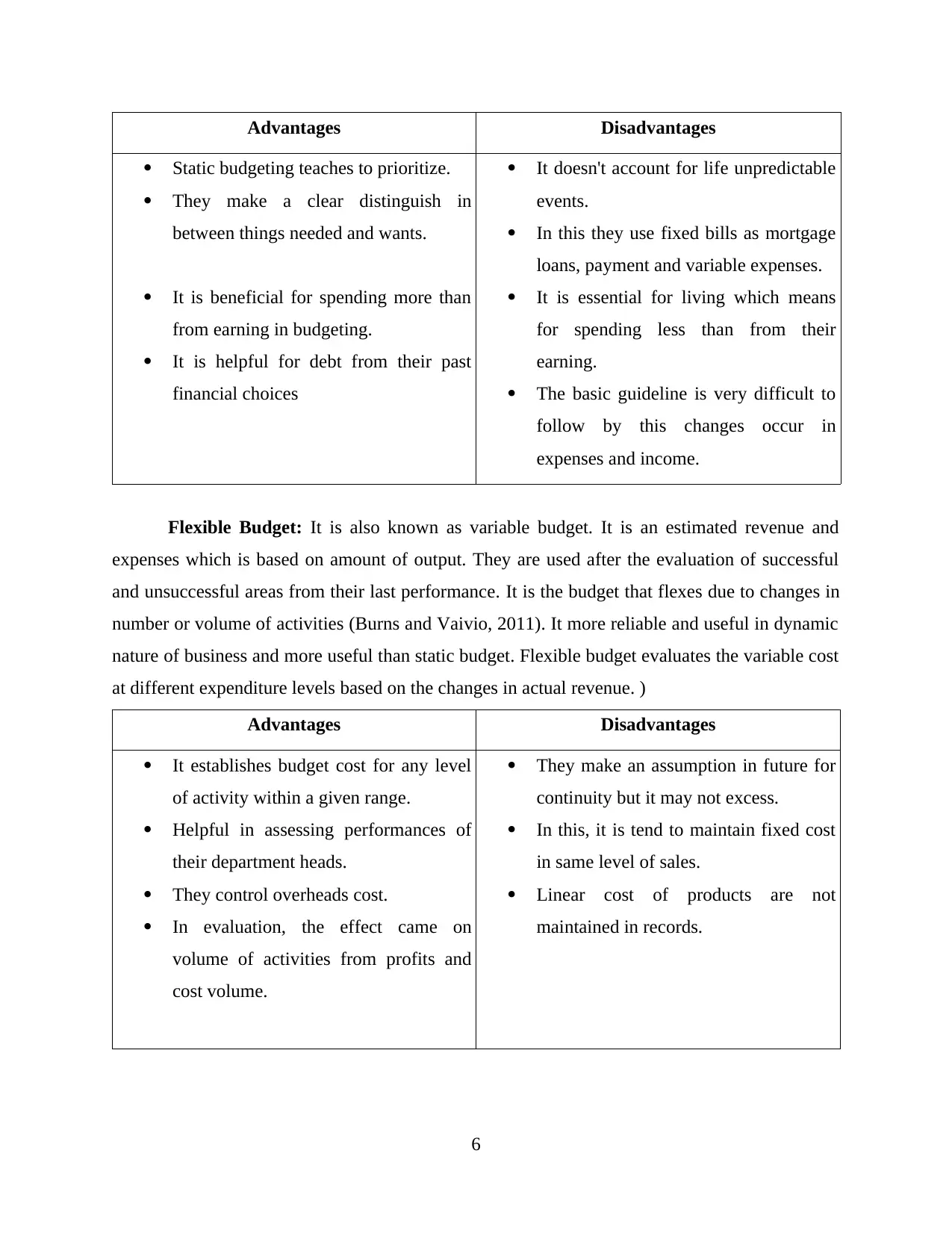

Advantages Disadvantages

Static budgeting teaches to prioritize.

They make a clear distinguish in

between things needed and wants.

It is beneficial for spending more than

from earning in budgeting.

It is helpful for debt from their past

financial choices

It doesn't account for life unpredictable

events.

In this they use fixed bills as mortgage

loans, payment and variable expenses.

It is essential for living which means

for spending less than from their

earning.

The basic guideline is very difficult to

follow by this changes occur in

expenses and income.

Flexible Budget: It is also known as variable budget. It is an estimated revenue and

expenses which is based on amount of output. They are used after the evaluation of successful

and unsuccessful areas from their last performance. It is the budget that flexes due to changes in

number or volume of activities (Burns and Vaivio, 2011). It more reliable and useful in dynamic

nature of business and more useful than static budget. Flexible budget evaluates the variable cost

at different expenditure levels based on the changes in actual revenue. )

Advantages Disadvantages

It establishes budget cost for any level

of activity within a given range.

Helpful in assessing performances of

their department heads.

They control overheads cost.

In evaluation, the effect came on

volume of activities from profits and

cost volume.

They make an assumption in future for

continuity but it may not excess.

In this, it is tend to maintain fixed cost

in same level of sales.

Linear cost of products are not

maintained in records.

6

Static budgeting teaches to prioritize.

They make a clear distinguish in

between things needed and wants.

It is beneficial for spending more than

from earning in budgeting.

It is helpful for debt from their past

financial choices

It doesn't account for life unpredictable

events.

In this they use fixed bills as mortgage

loans, payment and variable expenses.

It is essential for living which means

for spending less than from their

earning.

The basic guideline is very difficult to

follow by this changes occur in

expenses and income.

Flexible Budget: It is also known as variable budget. It is an estimated revenue and

expenses which is based on amount of output. They are used after the evaluation of successful

and unsuccessful areas from their last performance. It is the budget that flexes due to changes in

number or volume of activities (Burns and Vaivio, 2011). It more reliable and useful in dynamic

nature of business and more useful than static budget. Flexible budget evaluates the variable cost

at different expenditure levels based on the changes in actual revenue. )

Advantages Disadvantages

It establishes budget cost for any level

of activity within a given range.

Helpful in assessing performances of

their department heads.

They control overheads cost.

In evaluation, the effect came on

volume of activities from profits and

cost volume.

They make an assumption in future for

continuity but it may not excess.

In this, it is tend to maintain fixed cost

in same level of sales.

Linear cost of products are not

maintained in records.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental Budget: it is a budget used for incrementing from past budgets or in the

basis of actual performances, that increment amount added in new budget formation. The

increment made on best utilisation on allocation of resources (Kaplan, 2014). Moreover, it is the

budget prepared by using the previous year's budget amounts actual performance and quantifies

the difference, as the increment amount will use for next new budget of next accounting period.

This budget is stable and change is gradual increment or decrement and impact of change can be

observed easily and quickly. Some of its advantages and disadvantages are.

Advantages Disadvantages

Budget is always in stability and

changes in gradual basis.

They avoided their conflicts when

department seen treated.

If the changes occur can be seen

quickly.

They are assuming their activities

working in a same way.

No incentives provided for generating

new ideas and reducing costs.

Resources priority changes when

budget were set originally.

Zero Based Budgets: It is the process of creating budget without using any year priority

budget. It involves re-evaluating of items in cash flow statement and justifying expenses incurred

by department (Bromwich and Bhimani, 2015). This budget prepares under the zero based

budgeting (ZBB), without using the previous year's budget or spending numbers. Overall, ZBB

is the method of preparing the budget s which are based on “zero base” by quantifying every cost

and expense incurred in company's operations.

Advantages Disadvantages

The inefficient operations are

discontinued and identified.

They has proper coordination with

other employees and communication.

Allocation of resources should be done

economically and efficiently.

Management skills are not present.

They have lack of expertise employees.

Budgeting process is a time consuming

process by this mangers feel

demotivated.

Budgeting process is too rigid so the

organization is not able to unforeseen

its opportunities and threats.

7

basis of actual performances, that increment amount added in new budget formation. The

increment made on best utilisation on allocation of resources (Kaplan, 2014). Moreover, it is the

budget prepared by using the previous year's budget amounts actual performance and quantifies

the difference, as the increment amount will use for next new budget of next accounting period.

This budget is stable and change is gradual increment or decrement and impact of change can be

observed easily and quickly. Some of its advantages and disadvantages are.

Advantages Disadvantages

Budget is always in stability and

changes in gradual basis.

They avoided their conflicts when

department seen treated.

If the changes occur can be seen

quickly.

They are assuming their activities

working in a same way.

No incentives provided for generating

new ideas and reducing costs.

Resources priority changes when

budget were set originally.

Zero Based Budgets: It is the process of creating budget without using any year priority

budget. It involves re-evaluating of items in cash flow statement and justifying expenses incurred

by department (Bromwich and Bhimani, 2015). This budget prepares under the zero based

budgeting (ZBB), without using the previous year's budget or spending numbers. Overall, ZBB

is the method of preparing the budget s which are based on “zero base” by quantifying every cost

and expense incurred in company's operations.

Advantages Disadvantages

The inefficient operations are

discontinued and identified.

They has proper coordination with

other employees and communication.

Allocation of resources should be done

economically and efficiently.

Management skills are not present.

They have lack of expertise employees.

Budgeting process is a time consuming

process by this mangers feel

demotivated.

Budgeting process is too rigid so the

organization is not able to unforeseen

its opportunities and threats.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

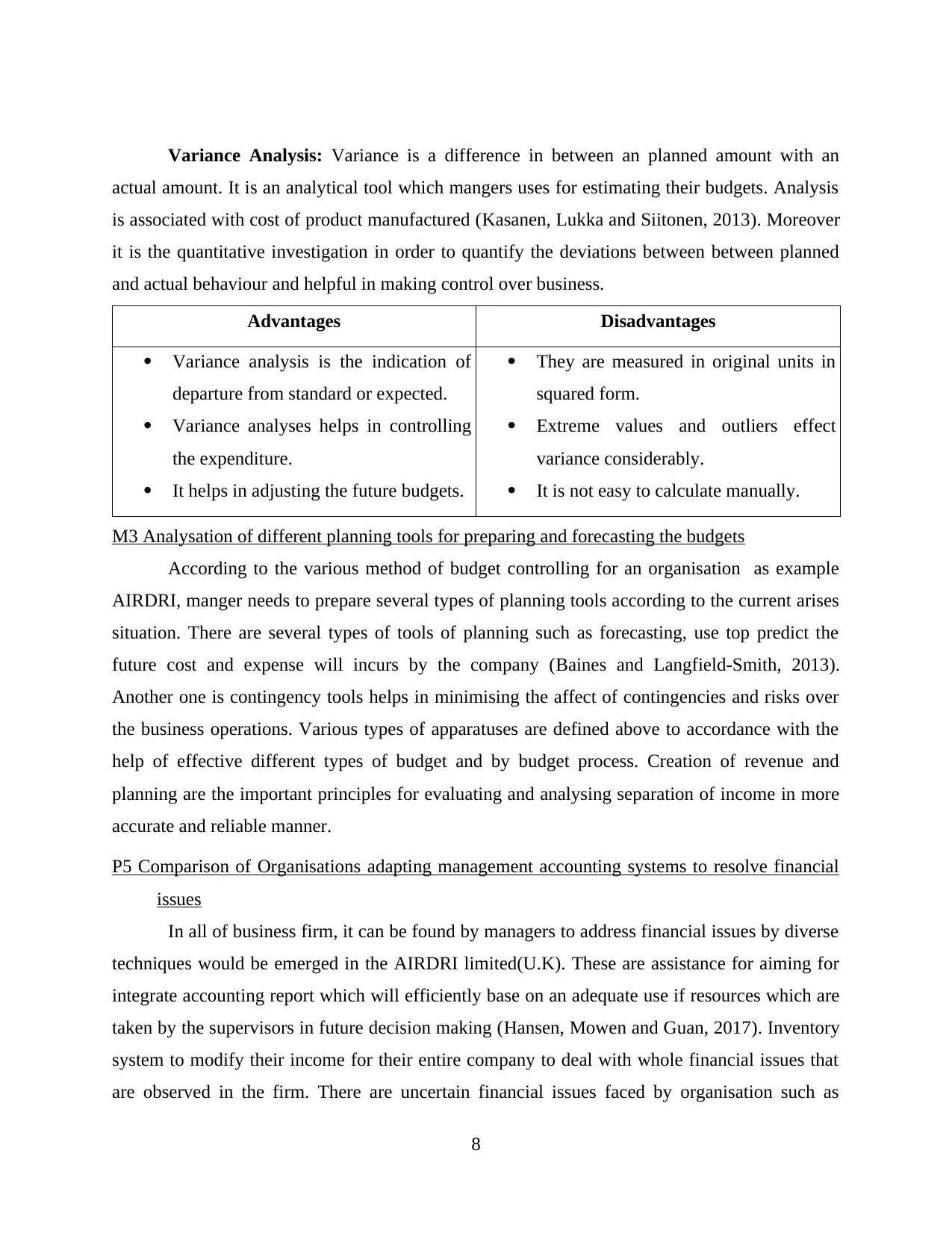

Variance Analysis: Variance is a difference in between an planned amount with an

actual amount. It is an analytical tool which mangers uses for estimating their budgets. Analysis

is associated with cost of product manufactured (Kasanen, Lukka and Siitonen, 2013). Moreover

it is the quantitative investigation in order to quantify the deviations between between planned

and actual behaviour and helpful in making control over business.

Advantages Disadvantages

Variance analysis is the indication of

departure from standard or expected.

Variance analyses helps in controlling

the expenditure.

It helps in adjusting the future budgets.

They are measured in original units in

squared form.

Extreme values and outliers effect

variance considerably.

It is not easy to calculate manually.

M3 Analysation of different planning tools for preparing and forecasting the budgets

According to the various method of budget controlling for an organisation as example

AIRDRI, manger needs to prepare several types of planning tools according to the current arises

situation. There are several types of tools of planning such as forecasting, use top predict the

future cost and expense will incurs by the company (Baines and Langfield-Smith, 2013).

Another one is contingency tools helps in minimising the affect of contingencies and risks over

the business operations. Various types of apparatuses are defined above to accordance with the

help of effective different types of budget and by budget process. Creation of revenue and

planning are the important principles for evaluating and analysing separation of income in more

accurate and reliable manner.

P5 Comparison of Organisations adapting management accounting systems to resolve financial

issues

In all of business firm, it can be found by managers to address financial issues by diverse

techniques would be emerged in the AIRDRI limited(U.K). These are assistance for aiming for

integrate accounting report which will efficiently base on an adequate use if resources which are

taken by the supervisors in future decision making (Hansen, Mowen and Guan, 2017). Inventory

system to modify their income for their entire company to deal with whole financial issues that

are observed in the firm. There are uncertain financial issues faced by organisation such as

8

actual amount. It is an analytical tool which mangers uses for estimating their budgets. Analysis

is associated with cost of product manufactured (Kasanen, Lukka and Siitonen, 2013). Moreover

it is the quantitative investigation in order to quantify the deviations between between planned

and actual behaviour and helpful in making control over business.

Advantages Disadvantages

Variance analysis is the indication of

departure from standard or expected.

Variance analyses helps in controlling

the expenditure.

It helps in adjusting the future budgets.

They are measured in original units in

squared form.

Extreme values and outliers effect

variance considerably.

It is not easy to calculate manually.

M3 Analysation of different planning tools for preparing and forecasting the budgets

According to the various method of budget controlling for an organisation as example

AIRDRI, manger needs to prepare several types of planning tools according to the current arises

situation. There are several types of tools of planning such as forecasting, use top predict the

future cost and expense will incurs by the company (Baines and Langfield-Smith, 2013).

Another one is contingency tools helps in minimising the affect of contingencies and risks over

the business operations. Various types of apparatuses are defined above to accordance with the

help of effective different types of budget and by budget process. Creation of revenue and

planning are the important principles for evaluating and analysing separation of income in more

accurate and reliable manner.

P5 Comparison of Organisations adapting management accounting systems to resolve financial

issues

In all of business firm, it can be found by managers to address financial issues by diverse

techniques would be emerged in the AIRDRI limited(U.K). These are assistance for aiming for

integrate accounting report which will efficiently base on an adequate use if resources which are

taken by the supervisors in future decision making (Hansen, Mowen and Guan, 2017). Inventory

system to modify their income for their entire company to deal with whole financial issues that

are observed in the firm. There are uncertain financial issues faced by organisation such as

8

increase in cost, decrease in revenue and customer satisfaction. These all financial issues relating

to financial statements of the company like as lack of accuracy, untimely preparation and

mismanagement of operating cycle.

KPI

A key performance indicator (KPI) is a countable value that present how effectively a

company is achieving key business objectives. AIRDRI limited use KPIs to evaluate their

success at movement for reference. It is business metrics mostly used by corporate governance

and other managers to analyse and track factors consider important to the success of an

organization (Granlund and Lukka, 2016). KPIs are divided into two types level, first one is high

level and second is low level. High level concentrates of performance of company and low level

consider in individual personnel like department wise – marketing, human resources, operations

and promotions. Effective KPIs focus on the business functions and processes that senior

management sees as most important for measuring progress toward meeting performance targets

and strategic goals. AIRDRI can use KPI to get over financial challenges by using metric which

show how a team and business is performing for action of goals of organisation. It measures

department wise performance to identify best ways to communication of crucial performance and

reduce costs.

Financial Indicators

Financial indicators are statistics extended used foe stability and performance, regarding

of various sectors of the economy. It is establish relationship between financial and economic

statistics such as assets, debt, liabilities and income. These indicators assist to interpretation of

the data contained in the balance sheet of AIRDRI limited. It also provides description of data

for evaluation and monitor. AIRDRI limited including financial indicators are Leverage,

profitability, growth and activity. For solving financial problems regarding financial indicators

through different types ratios are liquidity, debt equity, assets ratio and solvency ratio.

Profitability ratios shows net profit, operating profit and gross profit, efficiency ratios including

accounts receivable, accounts payable and inventory turnover ratio (Chapman, Hopwood and

Shields, 2016). Ratios are prepare on the basis of long term and short term. It helps to show

financial data of company and helping for assist performance. Mostly financial indicators

including cash flow statement, income statement, changes in equity and balance sheet.

Non Financial indicators

9

to financial statements of the company like as lack of accuracy, untimely preparation and

mismanagement of operating cycle.

KPI

A key performance indicator (KPI) is a countable value that present how effectively a

company is achieving key business objectives. AIRDRI limited use KPIs to evaluate their

success at movement for reference. It is business metrics mostly used by corporate governance

and other managers to analyse and track factors consider important to the success of an

organization (Granlund and Lukka, 2016). KPIs are divided into two types level, first one is high

level and second is low level. High level concentrates of performance of company and low level

consider in individual personnel like department wise – marketing, human resources, operations

and promotions. Effective KPIs focus on the business functions and processes that senior

management sees as most important for measuring progress toward meeting performance targets

and strategic goals. AIRDRI can use KPI to get over financial challenges by using metric which

show how a team and business is performing for action of goals of organisation. It measures

department wise performance to identify best ways to communication of crucial performance and

reduce costs.

Financial Indicators

Financial indicators are statistics extended used foe stability and performance, regarding

of various sectors of the economy. It is establish relationship between financial and economic

statistics such as assets, debt, liabilities and income. These indicators assist to interpretation of

the data contained in the balance sheet of AIRDRI limited. It also provides description of data

for evaluation and monitor. AIRDRI limited including financial indicators are Leverage,

profitability, growth and activity. For solving financial problems regarding financial indicators

through different types ratios are liquidity, debt equity, assets ratio and solvency ratio.

Profitability ratios shows net profit, operating profit and gross profit, efficiency ratios including

accounts receivable, accounts payable and inventory turnover ratio (Chapman, Hopwood and

Shields, 2016). Ratios are prepare on the basis of long term and short term. It helps to show

financial data of company and helping for assist performance. Mostly financial indicators

including cash flow statement, income statement, changes in equity and balance sheet.

Non Financial indicators

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.