Management Accounting Report: Costing Techniques and Analysis

VerifiedAdded on 2020/09/08

|17

|4610

|38

Report

AI Summary

This report delves into the realm of management accounting, offering a comprehensive exploration of its systems, methods, and practical applications. It begins by defining management accounting and its role in organizational decision-making, with a focus on various systems like job costing, inventory management, and price optimizing systems. The report then examines different management accounting reporting methods, including inventory and manufacturing reports, accounts receivable aging reports, budget reports, and job cost reports. Furthermore, the report analyzes the benefits of implementing a management accounting system, emphasizing its impact on strategic planning, cost management, and overall financial performance. Finally, the report demonstrates the application of both marginal costing and absorption costing techniques in drafting income statements, providing a practical understanding of their implications. This report aims to provide a detailed overview of management accounting practices, offering valuable insights into financial analysis and decision-making for students and professionals alike.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION

Managerial accounting is also refereed as management accounting and it is considered as

a process of framing management accounting reports which will helps the managers for

justifying the daily short term decisions by giving very perfect and accurate data with the context

of statistical and financial information related to activities of organizations. In the present report

there is brief discussion about management accounting system with its method. Further income

statement has been elaborated by the two techniques of costing

TASK 1

P1. Justifying management accounting system with respect to its type and requirement

Introduction

Management accounting has been referred as a managerial tool which gives all

information which is relevant to internal users and managers who are involved in process of

economic decision for company. In the present scenario, there are various kinds of management

accounting systems which give the entire information related to various segments and role of

business like system which manages inventory (Abrahamson, Berkowitz and Dumez, 2016). The

various management accounting systems function on the basis of objectives and goals within

organization. The Ovation system is using different kinds of management accounting systems

such as:

Job costing system

Inventory management system Types of management

accounting Price optimizing system

Cost accounting system

Job costing system: Usually, this system of management accounting is applied in

concern of manufacturing which helps in assigning the cost to every batch of individual

goods. The specific aim of this system is to gather the information which is purely

associated with the cost of particular service and production job. It helps in measuring the

level of efficiency and accuracy of the company i.e. it monitors each and every expense

or known as expense monitoring system which traces all expenses associated with

various services and products. In the same series, The Ovation system identifies each and

1

Managerial accounting is also refereed as management accounting and it is considered as

a process of framing management accounting reports which will helps the managers for

justifying the daily short term decisions by giving very perfect and accurate data with the context

of statistical and financial information related to activities of organizations. In the present report

there is brief discussion about management accounting system with its method. Further income

statement has been elaborated by the two techniques of costing

TASK 1

P1. Justifying management accounting system with respect to its type and requirement

Introduction

Management accounting has been referred as a managerial tool which gives all

information which is relevant to internal users and managers who are involved in process of

economic decision for company. In the present scenario, there are various kinds of management

accounting systems which give the entire information related to various segments and role of

business like system which manages inventory (Abrahamson, Berkowitz and Dumez, 2016). The

various management accounting systems function on the basis of objectives and goals within

organization. The Ovation system is using different kinds of management accounting systems

such as:

Job costing system

Inventory management system Types of management

accounting Price optimizing system

Cost accounting system

Job costing system: Usually, this system of management accounting is applied in

concern of manufacturing which helps in assigning the cost to every batch of individual

goods. The specific aim of this system is to gather the information which is purely

associated with the cost of particular service and production job. It helps in measuring the

level of efficiency and accuracy of the company i.e. it monitors each and every expense

or known as expense monitoring system which traces all expenses associated with

various services and products. In the same series, The Ovation system identifies each and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

every expense with job costing system such as home delivery services, servicing each

product, replacing the machinery, etc.

Cost accounting system: It is also referred as product costing system and its main

objective is to perform profitability analysis, cost control and inventory valuation by

identifying the cost of various services and products with respect to organization. In the

same series, the operations which are giving advantages as well as determining the actual

cost of each service and product is captious. It is typically used by company which are in

manufacturing to keep record of inventory at different stages. The Ovation system is an

electronic design and manufacturing company and so, it can trace the inventory flow

during production such as recording raw material when they are transforming in finished

goods. It is very essential to identify that which products are contributing more in margin

so that they can be given with special focus (Narasimhan, 2017).

Price optimizing system: It is very essential as management accounting through which

statistical and mathematical analysis is been performed to collect the response of

consumer at various level of price of all goods and services. With this technique, the best

price can be identified of each product and services according to its objective. Its

example can be, if the aim of organization is to increase the sales, then it will adopt the

price where consumers are more attracted to their company and in the same series, if

company wants to raise profit, price will set according to the maximum amount of margin

to the business.

Inventory management system: The overall inventory has been managed by inventory

management system of business organization. For managing and controlling, there are

various traditional methods such as weighted average method, FIFO and LIFO as

improving the level of technology, different software are available in the present scenario

which makes easy for all mangers in process of managing and controlling inventory. In a

manufacturing business, The Ovation system determines inventory which has been

required by them such as magnets, wires and cables, etc. It is very difficult to manage the

inventory flow manually so for resolving this issue various inventory management

software are used by them and for controlling the application of raw material in very

efficient way.

Conclusion

2

product, replacing the machinery, etc.

Cost accounting system: It is also referred as product costing system and its main

objective is to perform profitability analysis, cost control and inventory valuation by

identifying the cost of various services and products with respect to organization. In the

same series, the operations which are giving advantages as well as determining the actual

cost of each service and product is captious. It is typically used by company which are in

manufacturing to keep record of inventory at different stages. The Ovation system is an

electronic design and manufacturing company and so, it can trace the inventory flow

during production such as recording raw material when they are transforming in finished

goods. It is very essential to identify that which products are contributing more in margin

so that they can be given with special focus (Narasimhan, 2017).

Price optimizing system: It is very essential as management accounting through which

statistical and mathematical analysis is been performed to collect the response of

consumer at various level of price of all goods and services. With this technique, the best

price can be identified of each product and services according to its objective. Its

example can be, if the aim of organization is to increase the sales, then it will adopt the

price where consumers are more attracted to their company and in the same series, if

company wants to raise profit, price will set according to the maximum amount of margin

to the business.

Inventory management system: The overall inventory has been managed by inventory

management system of business organization. For managing and controlling, there are

various traditional methods such as weighted average method, FIFO and LIFO as

improving the level of technology, different software are available in the present scenario

which makes easy for all mangers in process of managing and controlling inventory. In a

manufacturing business, The Ovation system determines inventory which has been

required by them such as magnets, wires and cables, etc. It is very difficult to manage the

inventory flow manually so for resolving this issue various inventory management

software are used by them and for controlling the application of raw material in very

efficient way.

Conclusion

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above kinds of management accounting systems are used for increasing the level of

efficiency of the organization.

P2. Various methods of management accounting reporting

Introduction

Managers and owners of every business whether it is large or small prepare the

management accounting report which helps in identifying the performance of business. Financial

and management accounting reports sound similar but they are not as financial reports are

prepared for the external users and accounting reports are framed by organization's internal users.

These are not made yearly like financial reports as these reports are framed frequently on

monthly or weekly basis with the requirement.

Management accounting report gives information which is relevant according to different

segments and role of business (Brown-Liburd, Issa and Lombardi, 2015). The outcomes of these

reports help the organization's internal users for setting the future economic decisions.

Accounts receivable Aging report

Budget report Types of management

accounting system reports Job cost report

Inventory and Manufacturing report

Inventory and Manufacturing Report: The business can use this report along with the

physical inventory to create efficiency in the processes. The main article of this report is

referred as unit overhead cost, waste of inventory and hourly labour cost. Inventory

management system has been supported by this report. The various assembly lines of

organization have been compared to analyse the variations and its ways to improvement

with the bonuses to department who are deserves. There are many organizations that do

not afford any fault in the inventory production. So, this report is applicable. The dead

stock can be identified and fewer prices of that same stock so rotation of dead stock can

be implied in market.

Accounts Receivable Aging Report: The organizations that buy and sell the goods and

services on credit mostly frame this report. It is referred as a critical tool which has been

used by managers for the purpose of cash flow of customers who are on credit. Basically,

3

efficiency of the organization.

P2. Various methods of management accounting reporting

Introduction

Managers and owners of every business whether it is large or small prepare the

management accounting report which helps in identifying the performance of business. Financial

and management accounting reports sound similar but they are not as financial reports are

prepared for the external users and accounting reports are framed by organization's internal users.

These are not made yearly like financial reports as these reports are framed frequently on

monthly or weekly basis with the requirement.

Management accounting report gives information which is relevant according to different

segments and role of business (Brown-Liburd, Issa and Lombardi, 2015). The outcomes of these

reports help the organization's internal users for setting the future economic decisions.

Accounts receivable Aging report

Budget report Types of management

accounting system reports Job cost report

Inventory and Manufacturing report

Inventory and Manufacturing Report: The business can use this report along with the

physical inventory to create efficiency in the processes. The main article of this report is

referred as unit overhead cost, waste of inventory and hourly labour cost. Inventory

management system has been supported by this report. The various assembly lines of

organization have been compared to analyse the variations and its ways to improvement

with the bonuses to department who are deserves. There are many organizations that do

not afford any fault in the inventory production. So, this report is applicable. The dead

stock can be identified and fewer prices of that same stock so rotation of dead stock can

be implied in market.

Accounts Receivable Aging Report: The organizations that buy and sell the goods and

services on credit mostly frame this report. It is referred as a critical tool which has been

used by managers for the purpose of cash flow of customers who are on credit. Basically,

3

it helps in identifying the customer's balance that from what time they have been owned.

This report extracts the information of the customers who are 30, 60 and 90 days late.

The problems have been identified regarding the collection policy and organization's

process. Each and every business has the requirement to tighten the policy of credit if

most of the people are not able to pay their liability within ninety days.

Budget report : For analysing the performance of business, managers and owners of the

organizations prepare this report. For framing this report, primarily budgets are prepared

on the various roles according to expenses which have been incurred in previous year.

The expenses which are incurred in previous year exceeds the average expenses then to

trim the cost has been identified to perform in budget of current year. If the budgets are

prepared and actual outcome are matched with budgeted outcomes or actual performance.

The reasons are identified of all the variances and if any corrective action can be taken

for attaining the specific desired objectives of the organization (Shojaeezand,

Mohammad-Khani and Azmi, 2018).

Job cost report : Job costing system has been supported by this report under the

management accounting system. All the expenses are drawn in this report for some

particular project or job. Expense are been matched with revenue which is estimated from

those particular jobs or projects so that margin can be evaluated. It helps in identifying

the functions of high earning of the organization so that all resource and efforts will be

more focused on the functions which are giving advantage instead of areas which are

wasting resources and giving fewer earnings. This report gives brief analysis of those

expenses when project is on the mode of work in process so that some more costs can be

step up and areas can be determined where something is happening wrong and can be

rectified.

Conclusion

The above report will help Ovation system group for identifying the information which is

relevant and actual performance of the organization has been determined. The variance and its

alterations will be determined by budget report, inventory can be managed efficiently by

inventory and manufacturing report and for determining the huge earnings services so resources

will be utilised properly through job cost report.

4

This report extracts the information of the customers who are 30, 60 and 90 days late.

The problems have been identified regarding the collection policy and organization's

process. Each and every business has the requirement to tighten the policy of credit if

most of the people are not able to pay their liability within ninety days.

Budget report : For analysing the performance of business, managers and owners of the

organizations prepare this report. For framing this report, primarily budgets are prepared

on the various roles according to expenses which have been incurred in previous year.

The expenses which are incurred in previous year exceeds the average expenses then to

trim the cost has been identified to perform in budget of current year. If the budgets are

prepared and actual outcome are matched with budgeted outcomes or actual performance.

The reasons are identified of all the variances and if any corrective action can be taken

for attaining the specific desired objectives of the organization (Shojaeezand,

Mohammad-Khani and Azmi, 2018).

Job cost report : Job costing system has been supported by this report under the

management accounting system. All the expenses are drawn in this report for some

particular project or job. Expense are been matched with revenue which is estimated from

those particular jobs or projects so that margin can be evaluated. It helps in identifying

the functions of high earning of the organization so that all resource and efforts will be

more focused on the functions which are giving advantage instead of areas which are

wasting resources and giving fewer earnings. This report gives brief analysis of those

expenses when project is on the mode of work in process so that some more costs can be

step up and areas can be determined where something is happening wrong and can be

rectified.

Conclusion

The above report will help Ovation system group for identifying the information which is

relevant and actual performance of the organization has been determined. The variance and its

alterations will be determined by budget report, inventory can be managed efficiently by

inventory and manufacturing report and for determining the huge earnings services so resources

will be utilised properly through job cost report.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

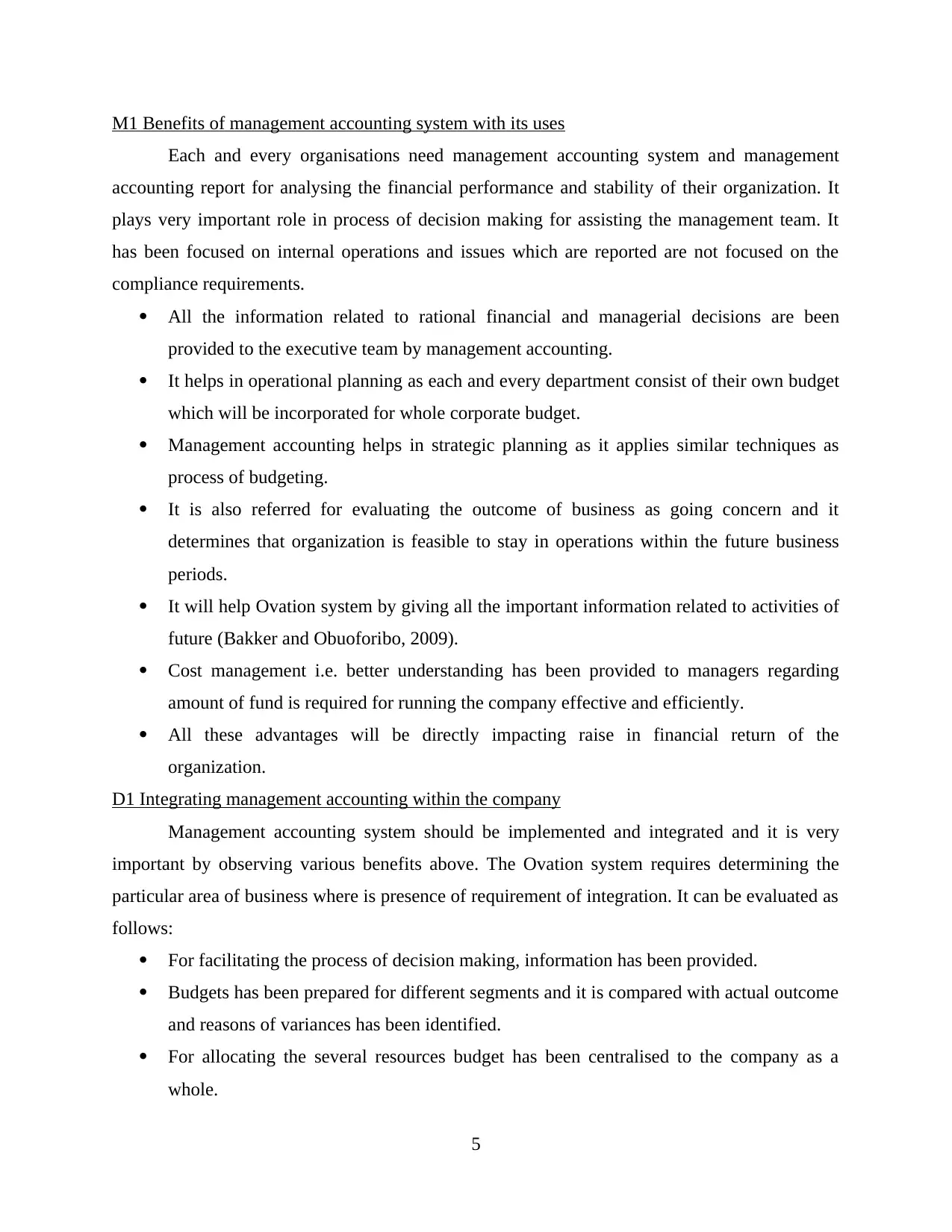

M1 Benefits of management accounting system with its uses

Each and every organisations need management accounting system and management

accounting report for analysing the financial performance and stability of their organization. It

plays very important role in process of decision making for assisting the management team. It

has been focused on internal operations and issues which are reported are not focused on the

compliance requirements.

All the information related to rational financial and managerial decisions are been

provided to the executive team by management accounting.

It helps in operational planning as each and every department consist of their own budget

which will be incorporated for whole corporate budget.

Management accounting helps in strategic planning as it applies similar techniques as

process of budgeting.

It is also referred for evaluating the outcome of business as going concern and it

determines that organization is feasible to stay in operations within the future business

periods.

It will help Ovation system by giving all the important information related to activities of

future (Bakker and Obuoforibo, 2009).

Cost management i.e. better understanding has been provided to managers regarding

amount of fund is required for running the company effective and efficiently.

All these advantages will be directly impacting raise in financial return of the

organization.

D1 Integrating management accounting within the company

Management accounting system should be implemented and integrated and it is very

important by observing various benefits above. The Ovation system requires determining the

particular area of business where is presence of requirement of integration. It can be evaluated as

follows:

For facilitating the process of decision making, information has been provided.

Budgets has been prepared for different segments and it is compared with actual outcome

and reasons of variances has been identified.

For allocating the several resources budget has been centralised to the company as a

whole.

5

Each and every organisations need management accounting system and management

accounting report for analysing the financial performance and stability of their organization. It

plays very important role in process of decision making for assisting the management team. It

has been focused on internal operations and issues which are reported are not focused on the

compliance requirements.

All the information related to rational financial and managerial decisions are been

provided to the executive team by management accounting.

It helps in operational planning as each and every department consist of their own budget

which will be incorporated for whole corporate budget.

Management accounting helps in strategic planning as it applies similar techniques as

process of budgeting.

It is also referred for evaluating the outcome of business as going concern and it

determines that organization is feasible to stay in operations within the future business

periods.

It will help Ovation system by giving all the important information related to activities of

future (Bakker and Obuoforibo, 2009).

Cost management i.e. better understanding has been provided to managers regarding

amount of fund is required for running the company effective and efficiently.

All these advantages will be directly impacting raise in financial return of the

organization.

D1 Integrating management accounting within the company

Management accounting system should be implemented and integrated and it is very

important by observing various benefits above. The Ovation system requires determining the

particular area of business where is presence of requirement of integration. It can be evaluated as

follows:

For facilitating the process of decision making, information has been provided.

Budgets has been prepared for different segments and it is compared with actual outcome

and reasons of variances has been identified.

For allocating the several resources budget has been centralised to the company as a

whole.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The value of integration of management accounting system of Ovation group has been

given by conducting personal interviews and meetings with major personnel.

Task 2

P3 Drafting income statement by using both cost techniques

Introduction

Each and every organization prepares the income statement by applying various

techniques. The techniques are absorption costing technique and marginal costing technique,

both are applicable very differently with different outcome. It is very essential for organization

for selecting the best one of drafting the financial statement so this will create best image in

industry (Shojaeezand, Mohammad-Khani, and Azmi, 2018).

Marginal Costing Techniques

This technique will always consider the variable cost as a cost of goods. For getting

margin it only considers variable cost which are directly linked to goods and fixed cost has been

ignored.

Given:

Selling price 35

Unit cost

Direct materials 6

Direct labour 5

Variable production overhead 2

variable sales overhead 1

Budgeted production for the

period 600

Fixed cost Budgeted cost Actual cost

Production overhead 1800 2000

Administration cost 800 700

Selling cost 400 600

Units

Budgeted sales 450

Actual sales 600

Actual production 700

6

given by conducting personal interviews and meetings with major personnel.

Task 2

P3 Drafting income statement by using both cost techniques

Introduction

Each and every organization prepares the income statement by applying various

techniques. The techniques are absorption costing technique and marginal costing technique,

both are applicable very differently with different outcome. It is very essential for organization

for selecting the best one of drafting the financial statement so this will create best image in

industry (Shojaeezand, Mohammad-Khani, and Azmi, 2018).

Marginal Costing Techniques

This technique will always consider the variable cost as a cost of goods. For getting

margin it only considers variable cost which are directly linked to goods and fixed cost has been

ignored.

Given:

Selling price 35

Unit cost

Direct materials 6

Direct labour 5

Variable production overhead 2

variable sales overhead 1

Budgeted production for the

period 600

Fixed cost Budgeted cost Actual cost

Production overhead 1800 2000

Administration cost 800 700

Selling cost 400 600

Units

Budgeted sales 450

Actual sales 600

Actual production 700

6

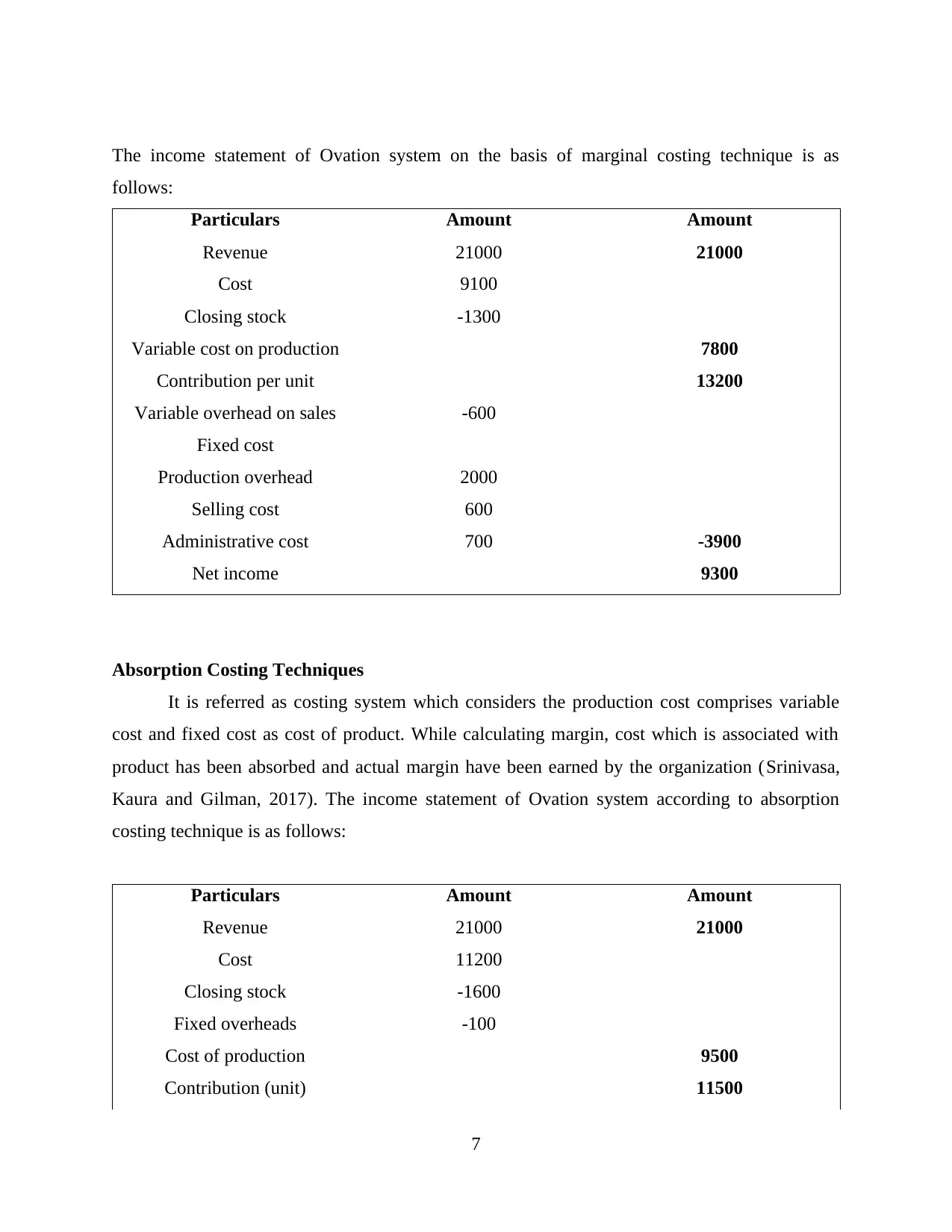

The income statement of Ovation system on the basis of marginal costing technique is as

follows:

Particulars Amount Amount

Revenue 21000 21000

Cost 9100

Closing stock -1300

Variable cost on production 7800

Contribution per unit 13200

Variable overhead on sales -600

Fixed cost

Production overhead 2000

Selling cost 600

Administrative cost 700 -3900

Net income 9300

Absorption Costing Techniques

It is referred as costing system which considers the production cost comprises variable

cost and fixed cost as cost of product. While calculating margin, cost which is associated with

product has been absorbed and actual margin have been earned by the organization (Srinivasa,

Kaura and Gilman, 2017). The income statement of Ovation system according to absorption

costing technique is as follows:

Particulars Amount Amount

Revenue 21000 21000

Cost 11200

Closing stock -1600

Fixed overheads -100

Cost of production 9500

Contribution (unit) 11500

7

follows:

Particulars Amount Amount

Revenue 21000 21000

Cost 9100

Closing stock -1300

Variable cost on production 7800

Contribution per unit 13200

Variable overhead on sales -600

Fixed cost

Production overhead 2000

Selling cost 600

Administrative cost 700 -3900

Net income 9300

Absorption Costing Techniques

It is referred as costing system which considers the production cost comprises variable

cost and fixed cost as cost of product. While calculating margin, cost which is associated with

product has been absorbed and actual margin have been earned by the organization (Srinivasa,

Kaura and Gilman, 2017). The income statement of Ovation system according to absorption

costing technique is as follows:

Particulars Amount Amount

Revenue 21000 21000

Cost 11200

Closing stock -1600

Fixed overheads -100

Cost of production 9500

Contribution (unit) 11500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

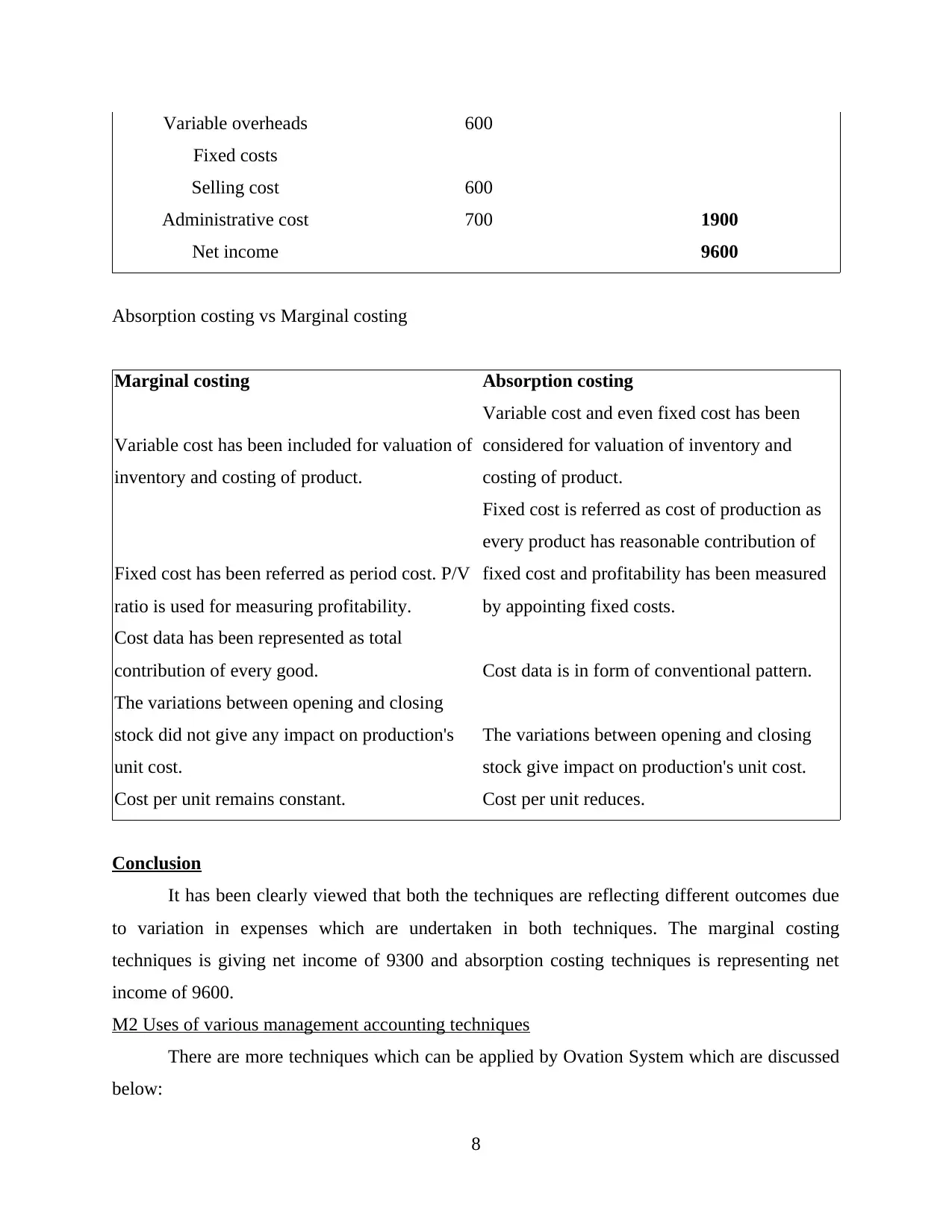

Variable overheads 600

Fixed costs

Selling cost 600

Administrative cost 700 1900

Net income 9600

Absorption costing vs Marginal costing

Marginal costing Absorption costing

Variable cost has been included for valuation of

inventory and costing of product.

Variable cost and even fixed cost has been

considered for valuation of inventory and

costing of product.

Fixed cost has been referred as period cost. P/V

ratio is used for measuring profitability.

Fixed cost is referred as cost of production as

every product has reasonable contribution of

fixed cost and profitability has been measured

by appointing fixed costs.

Cost data has been represented as total

contribution of every good. Cost data is in form of conventional pattern.

The variations between opening and closing

stock did not give any impact on production's

unit cost.

The variations between opening and closing

stock give impact on production's unit cost.

Cost per unit remains constant. Cost per unit reduces.

Conclusion

It has been clearly viewed that both the techniques are reflecting different outcomes due

to variation in expenses which are undertaken in both techniques. The marginal costing

techniques is giving net income of 9300 and absorption costing techniques is representing net

income of 9600.

M2 Uses of various management accounting techniques

There are more techniques which can be applied by Ovation System which are discussed

below:

8

Fixed costs

Selling cost 600

Administrative cost 700 1900

Net income 9600

Absorption costing vs Marginal costing

Marginal costing Absorption costing

Variable cost has been included for valuation of

inventory and costing of product.

Variable cost and even fixed cost has been

considered for valuation of inventory and

costing of product.

Fixed cost has been referred as period cost. P/V

ratio is used for measuring profitability.

Fixed cost is referred as cost of production as

every product has reasonable contribution of

fixed cost and profitability has been measured

by appointing fixed costs.

Cost data has been represented as total

contribution of every good. Cost data is in form of conventional pattern.

The variations between opening and closing

stock did not give any impact on production's

unit cost.

The variations between opening and closing

stock give impact on production's unit cost.

Cost per unit remains constant. Cost per unit reduces.

Conclusion

It has been clearly viewed that both the techniques are reflecting different outcomes due

to variation in expenses which are undertaken in both techniques. The marginal costing

techniques is giving net income of 9300 and absorption costing techniques is representing net

income of 9600.

M2 Uses of various management accounting techniques

There are more techniques which can be applied by Ovation System which are discussed

below:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing : The manufacturing overhead cost has been assigned in this

system for different units of the organization. The cost has been assigned according to the

resource's level which are absorbed by activities. While, comparing it with conventional

costing, indirect cost are purely associated with direct cost.

Standard costing : Different activities of the business are created as standard cost.

Variations are recorded in this technique by comparing expected and actual cost by

eliminating cost which is expected for actual cost in report (Nuhu, Baird and Bala

Appuhamilage, 2017). Huge amount of data has been maintained of historical cost for the

elements which are part of inventory.

D2 Drafting Financial report with justifying the activities related to business.

To : GM

(The Ovation System Group)

From : Management Accounting Officer

(The Ovation System Group)

Subject : Justifying the activities with the prospective of business

Respected Sir,

This report has been drafted for justifying the information which has been identified while

preparing income statement of the organization by applying both the costing techniques such as

Marginal costing and absorption costing technique. It has been viewed that if company goes

with absorption technique then it will be giving net income of 9600 and on its contrary marginal

costing technique will be representing net income of 9300. There is minimal variation which is

because of different expenses which are considered. The application of method will be

identified according to dependency on type of organization's image for pertaining in front of all

stakeholders. For earning more margin absorption costing technique is better in this scenario

and for actual results marginal costing will be given more preference.

Thanks and regards

Task 3

P4 Application of various planning tools in the organisation

Introduction

9

system for different units of the organization. The cost has been assigned according to the

resource's level which are absorbed by activities. While, comparing it with conventional

costing, indirect cost are purely associated with direct cost.

Standard costing : Different activities of the business are created as standard cost.

Variations are recorded in this technique by comparing expected and actual cost by

eliminating cost which is expected for actual cost in report (Nuhu, Baird and Bala

Appuhamilage, 2017). Huge amount of data has been maintained of historical cost for the

elements which are part of inventory.

D2 Drafting Financial report with justifying the activities related to business.

To : GM

(The Ovation System Group)

From : Management Accounting Officer

(The Ovation System Group)

Subject : Justifying the activities with the prospective of business

Respected Sir,

This report has been drafted for justifying the information which has been identified while

preparing income statement of the organization by applying both the costing techniques such as

Marginal costing and absorption costing technique. It has been viewed that if company goes

with absorption technique then it will be giving net income of 9600 and on its contrary marginal

costing technique will be representing net income of 9300. There is minimal variation which is

because of different expenses which are considered. The application of method will be

identified according to dependency on type of organization's image for pertaining in front of all

stakeholders. For earning more margin absorption costing technique is better in this scenario

and for actual results marginal costing will be given more preference.

Thanks and regards

Task 3

P4 Application of various planning tools in the organisation

Introduction

9

There are various planning tools in management accounting system like budgeting is very

essential for managers for determining the future events and plans and decision should be

undertaken according to it. With the perspective of budgetary control, various kinds of planning

tools can be implied by The Ovation System for drafting budget for its different aspect.

Activity Based Budgeting : It is method of budgeting where overhead cost has been considered

for framing budget. Past year expenses are not undertaken in this method for drafting budget of

present year. All the activities are analysed properly and even it has been researched that it

occurs high cost and all resources are purely allocated according to the results (Pratheepkanth,

2018).

Merits

All the unnecessary activities are substituted which be giving advantage for saving cost.

Each cost driver has been undertaken for evaluation.

Demerits

It is very complex method and there is requirement of deep understanding of various

functional areas of organization.

There is requirement of high professionals to be employed and it will consume more

resources.

Zero Based Budgeting : It is method of budgeting in which zero is taken as base and in this

method also past year expenses are not considered. The items are re-evaluated in cash flow and

they are interpreted in the budget.

Merits

Resources are allocated efficiently and actual numbers are undertaken instead of

historical numbers.

All the expenses are re-evaluated and accuracy has been determined while preparing

budgets.

Demerits

It is very time consuming as each and every item has been considered.

It also blocks huge number of employees.

Incremental Budgeting : It is method of budgeting which alters fewer alterations for

accomplishing new budget. Budgets are drafted by considering past year budget for the current

10

essential for managers for determining the future events and plans and decision should be

undertaken according to it. With the perspective of budgetary control, various kinds of planning

tools can be implied by The Ovation System for drafting budget for its different aspect.

Activity Based Budgeting : It is method of budgeting where overhead cost has been considered

for framing budget. Past year expenses are not undertaken in this method for drafting budget of

present year. All the activities are analysed properly and even it has been researched that it

occurs high cost and all resources are purely allocated according to the results (Pratheepkanth,

2018).

Merits

All the unnecessary activities are substituted which be giving advantage for saving cost.

Each cost driver has been undertaken for evaluation.

Demerits

It is very complex method and there is requirement of deep understanding of various

functional areas of organization.

There is requirement of high professionals to be employed and it will consume more

resources.

Zero Based Budgeting : It is method of budgeting in which zero is taken as base and in this

method also past year expenses are not considered. The items are re-evaluated in cash flow and

they are interpreted in the budget.

Merits

Resources are allocated efficiently and actual numbers are undertaken instead of

historical numbers.

All the expenses are re-evaluated and accuracy has been determined while preparing

budgets.

Demerits

It is very time consuming as each and every item has been considered.

It also blocks huge number of employees.

Incremental Budgeting : It is method of budgeting which alters fewer alterations for

accomplishing new budget. Budgets are drafted by considering past year budget for the current

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.