Management Accounting Report: Costing, Planning, and Budgeting

VerifiedAdded on 2020/07/22

|17

|5674

|141

Report

AI Summary

This report, prepared for Rotork PLC, a manufacturing company, delves into various aspects of management accounting. It begins by defining management accounting and exploring different systems like cost accounting, inventory management, and transfer pricing, highlighting their relevance to Rotork PLC. The report then examines several management accounting reporting methods, including budget reports, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, income statements, and cash flow statements, illustrating their applications within the company. The assignment further includes a detailed calculation of an income statement using both marginal and absorption costing methods. Finally, it provides a comprehensive analysis of different planning tools for budgetary control, outlining their advantages and disadvantages, and demonstrates the application of a management accounting system to address financial challenges within the company, offering valuable insights and recommendations for improved financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Report on meaning of management accounting and requirements of different types of

management accounting.........................................................................................................3

P2 Methods of management accounting reporting.................................................................5

TASK 2............................................................................................................................................9

P3 Calculation of Income statement using marginal and absorption costs............................9

TASK 3..........................................................................................................................................12

P4 Report on advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................12

P5 Use of management accounting system to solve financial problem...............................14

CONCLUSION.............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Report on meaning of management accounting and requirements of different types of

management accounting.........................................................................................................3

P2 Methods of management accounting reporting.................................................................5

TASK 2............................................................................................................................................9

P3 Calculation of Income statement using marginal and absorption costs............................9

TASK 3..........................................................................................................................................12

P4 Report on advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................12

P5 Use of management accounting system to solve financial problem...............................14

CONCLUSION.............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Managing accounting system or MAS is a process of continuous organisational learning

and transformation (Anandarajan and Srinivasan, 2012). It is the practical application of

management techniques to report on financial health of a business. This process involves

analysis, planning, implementation and control of designed programs to give financial status

through reporting for management decision making (Bebbington, Unerman and O'Dwyer, 2014).

Rotork plc is a manufacturing company located in British. It's major role is to

manufacture industrial flow control equipment.

In this assignment, different types and methods of management accounting systems has

been explained. Advantages and disadvantages of different types of planning tools for budgetary

control will give the clear picture of how to make proper budget. In this assignment, two

different scenarios has been discussed. In first scenario, as a management accounting officer,

report is made for implementation of different cost accounting techniques. On the basis of

second scenario, a valuable report is written to General manager about how to response to

financial problems.

The purpose of this assignment is to generate report through application of management

accounting techniques such as profit analysis, marginal costing and absorption costing.

TASK 1

P1 Report on meaning of management accounting and requirements of different types of

management accounting

From: Management accounting officer

To: General manager of Rotork plc

Sub: Management accounting system

In this report, as a Management accounting officer, I have explained about types of

management accounting systems which will help Rotork plc in making decisions in choosing

best systems. Traditional, Lean, Throughput and Transfer accounting has been explained as a

types of accounting systems of management.

Meaning of Management accounting system:

Management accounting systems contains of all provisions which provides accounting

information to managers. This informations helps them in deciding issues within organisations.

Managing accounting system or MAS is a process of continuous organisational learning

and transformation (Anandarajan and Srinivasan, 2012). It is the practical application of

management techniques to report on financial health of a business. This process involves

analysis, planning, implementation and control of designed programs to give financial status

through reporting for management decision making (Bebbington, Unerman and O'Dwyer, 2014).

Rotork plc is a manufacturing company located in British. It's major role is to

manufacture industrial flow control equipment.

In this assignment, different types and methods of management accounting systems has

been explained. Advantages and disadvantages of different types of planning tools for budgetary

control will give the clear picture of how to make proper budget. In this assignment, two

different scenarios has been discussed. In first scenario, as a management accounting officer,

report is made for implementation of different cost accounting techniques. On the basis of

second scenario, a valuable report is written to General manager about how to response to

financial problems.

The purpose of this assignment is to generate report through application of management

accounting techniques such as profit analysis, marginal costing and absorption costing.

TASK 1

P1 Report on meaning of management accounting and requirements of different types of

management accounting

From: Management accounting officer

To: General manager of Rotork plc

Sub: Management accounting system

In this report, as a Management accounting officer, I have explained about types of

management accounting systems which will help Rotork plc in making decisions in choosing

best systems. Traditional, Lean, Throughput and Transfer accounting has been explained as a

types of accounting systems of management.

Meaning of Management accounting system:

Management accounting systems contains of all provisions which provides accounting

information to managers. This informations helps them in deciding issues within organisations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overall it is guidelines for financial and non-financial decision making informations process

which supports managers (Chapman, 2011). The main users of management accounting

systems are Investors, creditors and operational managers. Each users have different motives

according to their requirements of accounting informations.

Some of the essential requirements of different types of management accounting are as

follows:

Cost accounting system: According to this particular costing system management can

be able to determine total costs and expenses they are going to incur during the period of

time. It is used specially by managers to record of costs related data is become easy for

individual projects (Damodaran, 2012). Process costing method is suitable for only

those projects which are in the production of homogeneous products.

Inventory management system: This type of management accounting system, involves

revolutionary techniques in which it focuses on strategies to maintain overall stock that

are being kept by an organisation. This system provides immediate informations to

accounting managers whenever it is required for decision-making.

Price optimisation system: This particular system is done to analyse various price of

the products which are being set by the company. This can easily be helpful to

determine overall perception of customers about total products cost which are being set

by the company during the time.

Transfer Pricing method: Here price is added to a product, when there is movement

from one department to another. This method explains that product will become costly,

if it transfers from one department to other.

Application of this types on Rotork plc

Cost accounting system: This type of accounting system is essentially required for

Rotork plc because after application of this method, it can determine allocation of its

costs related to cost of goods sold. For example, It can apply this method in distributing

the cost of raw materials, direct labours and manufacturing overheads separately.

Inventory management system: Rotork plc can apply this method in reducing the costs

of its material by eliminating wastes. For example, companies present revenue is 500000

pounds but profit is only 9300 pounds. This reflects that there are huge unnecessary

expenses. The main reason behind this increases expenses could be wastage of resources

which supports managers (Chapman, 2011). The main users of management accounting

systems are Investors, creditors and operational managers. Each users have different motives

according to their requirements of accounting informations.

Some of the essential requirements of different types of management accounting are as

follows:

Cost accounting system: According to this particular costing system management can

be able to determine total costs and expenses they are going to incur during the period of

time. It is used specially by managers to record of costs related data is become easy for

individual projects (Damodaran, 2012). Process costing method is suitable for only

those projects which are in the production of homogeneous products.

Inventory management system: This type of management accounting system, involves

revolutionary techniques in which it focuses on strategies to maintain overall stock that

are being kept by an organisation. This system provides immediate informations to

accounting managers whenever it is required for decision-making.

Price optimisation system: This particular system is done to analyse various price of

the products which are being set by the company. This can easily be helpful to

determine overall perception of customers about total products cost which are being set

by the company during the time.

Transfer Pricing method: Here price is added to a product, when there is movement

from one department to another. This method explains that product will become costly,

if it transfers from one department to other.

Application of this types on Rotork plc

Cost accounting system: This type of accounting system is essentially required for

Rotork plc because after application of this method, it can determine allocation of its

costs related to cost of goods sold. For example, It can apply this method in distributing

the cost of raw materials, direct labours and manufacturing overheads separately.

Inventory management system: Rotork plc can apply this method in reducing the costs

of its material by eliminating wastes. For example, companies present revenue is 500000

pounds but profit is only 9300 pounds. This reflects that there are huge unnecessary

expenses. The main reason behind this increases expenses could be wastage of resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

like labour hours, money and raw materials. Hence, it can improve its overall profit by

reducing these costs of productions.

Job costing system: This accounting method could help Rotork Plc eliminating pitfalls

in production process after application into business (David, 2011). For example,

Companies budgeted and actual costs and demands were varied. Which indicates that it

has not done analysis of demand properly or it has not estimated for unexpected costs.

Transfer Pricing method: Rotork Plc's net profit very low as compare to its revenue.

Because company has gone through many departments to deliver its product for sale.

This is necessary to a company to add this cost into pricing method otherwise it could

face loss. For example, suppose company has not considered fixed and variable costs

while calculating its net profit, than this could effect business by running out of cash as

it hasn't include costs of different departments in calculating its net profits.

P2 Methods of management accounting reporting

From: Management accounting officer

To: General manager of Rotork plc

Sub: Management accounting report

In this report, different methods of accounting reporting for helping Rotork Plc in decision-

making process have been explained. Also, the uses of this methods according to the

requirement of company is also mentioned.

Meaning of Management accounting report

Management accounting reports helps business in monitoring company's performance (Fowzia,

2011). It is made at the end of every accounting period or it can be present at the time of

requirement of it like managers may request for quarterly, monthly, weekly or even daily

reports.

Importance of Management accounting report

It helps in forecasting the future.

It helps in Make or buy decisions.

It forecasts future cash flows of business from different sources.

It helps in understanding the variance in performance of labour, materials and assets.

reducing these costs of productions.

Job costing system: This accounting method could help Rotork Plc eliminating pitfalls

in production process after application into business (David, 2011). For example,

Companies budgeted and actual costs and demands were varied. Which indicates that it

has not done analysis of demand properly or it has not estimated for unexpected costs.

Transfer Pricing method: Rotork Plc's net profit very low as compare to its revenue.

Because company has gone through many departments to deliver its product for sale.

This is necessary to a company to add this cost into pricing method otherwise it could

face loss. For example, suppose company has not considered fixed and variable costs

while calculating its net profit, than this could effect business by running out of cash as

it hasn't include costs of different departments in calculating its net profits.

P2 Methods of management accounting reporting

From: Management accounting officer

To: General manager of Rotork plc

Sub: Management accounting report

In this report, different methods of accounting reporting for helping Rotork Plc in decision-

making process have been explained. Also, the uses of this methods according to the

requirement of company is also mentioned.

Meaning of Management accounting report

Management accounting reports helps business in monitoring company's performance (Fowzia,

2011). It is made at the end of every accounting period or it can be present at the time of

requirement of it like managers may request for quarterly, monthly, weekly or even daily

reports.

Importance of Management accounting report

It helps in forecasting the future.

It helps in Make or buy decisions.

It forecasts future cash flows of business from different sources.

It helps in understanding the variance in performance of labour, materials and assets.

It supports business in analysing required rate of return to run a business.

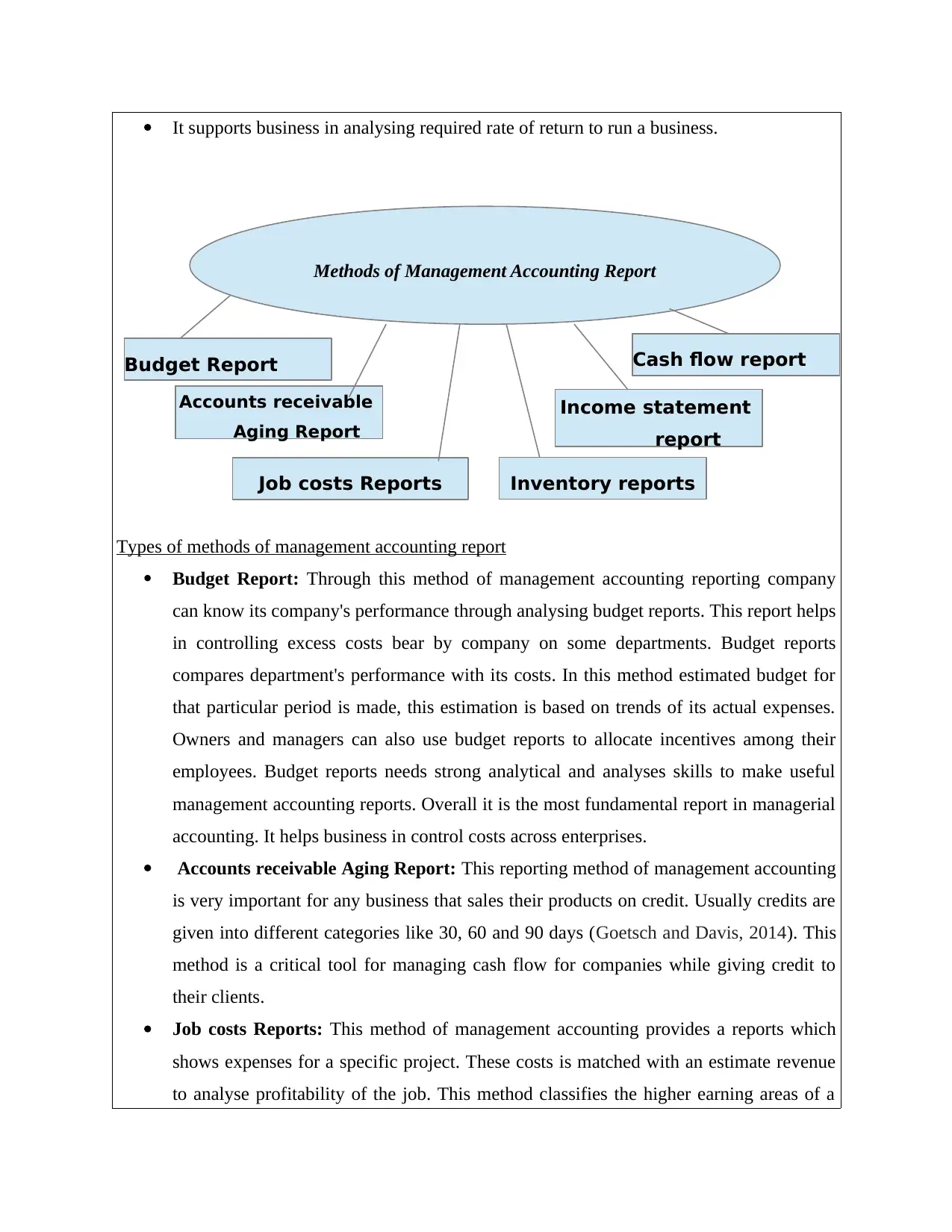

Types of methods of management accounting report

Budget Report: Through this method of management accounting reporting company

can know its company's performance through analysing budget reports. This report helps

in controlling excess costs bear by company on some departments. Budget reports

compares department's performance with its costs. In this method estimated budget for

that particular period is made, this estimation is based on trends of its actual expenses.

Owners and managers can also use budget reports to allocate incentives among their

employees. Budget reports needs strong analytical and analyses skills to make useful

management accounting reports. Overall it is the most fundamental report in managerial

accounting. It helps business in control costs across enterprises.

Accounts receivable Aging Report: This reporting method of management accounting

is very important for any business that sales their products on credit. Usually credits are

given into different categories like 30, 60 and 90 days (Goetsch and Davis, 2014). This

method is a critical tool for managing cash flow for companies while giving credit to

their clients.

Job costs Reports: This method of management accounting provides a reports which

shows expenses for a specific project. These costs is matched with an estimate revenue

to analyse profitability of the job. This method classifies the higher earning areas of a

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

Types of methods of management accounting report

Budget Report: Through this method of management accounting reporting company

can know its company's performance through analysing budget reports. This report helps

in controlling excess costs bear by company on some departments. Budget reports

compares department's performance with its costs. In this method estimated budget for

that particular period is made, this estimation is based on trends of its actual expenses.

Owners and managers can also use budget reports to allocate incentives among their

employees. Budget reports needs strong analytical and analyses skills to make useful

management accounting reports. Overall it is the most fundamental report in managerial

accounting. It helps business in control costs across enterprises.

Accounts receivable Aging Report: This reporting method of management accounting

is very important for any business that sales their products on credit. Usually credits are

given into different categories like 30, 60 and 90 days (Goetsch and Davis, 2014). This

method is a critical tool for managing cash flow for companies while giving credit to

their clients.

Job costs Reports: This method of management accounting provides a reports which

shows expenses for a specific project. These costs is matched with an estimate revenue

to analyse profitability of the job. This method classifies the higher earning areas of a

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business which helps company to focus on allocating its funds among these areas instead

wasting its money and cost in using funds in less earning areas. Job Cost Report is also

used to analyse expenses of work-in-progress projects to control waste before

completing it.

Inventory and manufacturing reports: This method of management accounting is

useful for those companies who produces physical products like manufacturing

industries. Inventory and manufacturing report helps in collecting data's on inventory

costs, labour and other overheads of production process. Manufacturing companies can

use managerial accounting reports to make their operational process more efficient.

Income statement report: This reporting methods helps a company in analysing overall

net profit remaining with the business after payment of all types of expenses like fixed

and variables (Granlund, 2011). This net profit is also concerned as net earnings which

is added to capital of the company.

Cash Flow statement report: This report helps a business in knowing how much cash

is available with a company and how much it can earned in future. Overall it tells about

liquidity of a business.

Application of above reporting methods to Rotork plc

Budget Report: Rotork plc could use budget report in analysing the variance between

estimated and actual figures. More variance reflects inefficiency of a company in

managing its costs where less variance implies that company is effectively utilising its

resources without wasting its resources. For example, in the given illustration, Rotork

Plc's budgeted sales is 450 units while its actual sales if 600 units. It can be called under

budgeted sales. This situation impacts business in facing difficulties in fulfilling the

demands on time.

Accounts receivable Aging Report: Through the application of this type of reports

company can know about duration required to receive amounts from its debtors (Linoff

and Berry, 2011). For example if debtors are increased from previous year than

companies efficiency of working capital would affected due to less cash available to a

business. Hence, this report could be applied to control excess blockage of cash among

debtors.

Job costs Reports: After application of this method, Rotork Plc may know which

wasting its money and cost in using funds in less earning areas. Job Cost Report is also

used to analyse expenses of work-in-progress projects to control waste before

completing it.

Inventory and manufacturing reports: This method of management accounting is

useful for those companies who produces physical products like manufacturing

industries. Inventory and manufacturing report helps in collecting data's on inventory

costs, labour and other overheads of production process. Manufacturing companies can

use managerial accounting reports to make their operational process more efficient.

Income statement report: This reporting methods helps a company in analysing overall

net profit remaining with the business after payment of all types of expenses like fixed

and variables (Granlund, 2011). This net profit is also concerned as net earnings which

is added to capital of the company.

Cash Flow statement report: This report helps a business in knowing how much cash

is available with a company and how much it can earned in future. Overall it tells about

liquidity of a business.

Application of above reporting methods to Rotork plc

Budget Report: Rotork plc could use budget report in analysing the variance between

estimated and actual figures. More variance reflects inefficiency of a company in

managing its costs where less variance implies that company is effectively utilising its

resources without wasting its resources. For example, in the given illustration, Rotork

Plc's budgeted sales is 450 units while its actual sales if 600 units. It can be called under

budgeted sales. This situation impacts business in facing difficulties in fulfilling the

demands on time.

Accounts receivable Aging Report: Through the application of this type of reports

company can know about duration required to receive amounts from its debtors (Linoff

and Berry, 2011). For example if debtors are increased from previous year than

companies efficiency of working capital would affected due to less cash available to a

business. Hence, this report could be applied to control excess blockage of cash among

debtors.

Job costs Reports: After application of this method, Rotork Plc may know which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activity consumes much cash. Like for example, in the given illustration, company has

production, selling and distribution costs. These different costs would generate job

costing reports for the company.

Inventory and manufacturing reports: This reporting method could be applied to

know how much capital of Rotork Plc has been blocked in manufacturing process.

These reports represents the statement of working capital and work-in-progress of a

company. For example, information through reports about opening stock and closing

stock of a company is required to meet the demand of a product.

Income statement report: This report is considered to know how much profit is left

with Rotork Plc after paying all expenses, interests, taxes and payments. For example

company records net profit amount £9300 during a year. Which implies that it has only

managed to earn that much amount.

Cash flow statement report: Rotork Plc can applied this method to find liquidity of its

business through analysing cash flow statement reports. For example, Company's net

profit is £9300 which is accrued. Means it is not earned by business in cash. So, business

could know how much actual cash is left with this report.

CONCLUSION

It's depend on the requirement of Rotork Plc upon which report it requires. Each

reporting methods has its own uses and importance. Cash flow statement report is useful to find

liquidity of a business. Income statement helps business in knowing how much earnings left

with it to invest in expansion activities and maintenance of business. Budget reports are the

forecasts which is based on the estimation. It requires for a Rotork Plc to allocate its funds

among different department accordingly.

TASK 2

P3 Calculation of Income statement using marginal and absorption costs

Marginal Costs: These costs also known as variable costing. In this costing method,

decisions can be taken on the basis of uncertainty of total costs (McNeil, Frey and Embrechts,

2015). For example, determination of fixed and variable cost is done to find out products for

production. Identification of marginal costing is required to know the impact of profit due to

production, selling and distribution costs. These different costs would generate job

costing reports for the company.

Inventory and manufacturing reports: This reporting method could be applied to

know how much capital of Rotork Plc has been blocked in manufacturing process.

These reports represents the statement of working capital and work-in-progress of a

company. For example, information through reports about opening stock and closing

stock of a company is required to meet the demand of a product.

Income statement report: This report is considered to know how much profit is left

with Rotork Plc after paying all expenses, interests, taxes and payments. For example

company records net profit amount £9300 during a year. Which implies that it has only

managed to earn that much amount.

Cash flow statement report: Rotork Plc can applied this method to find liquidity of its

business through analysing cash flow statement reports. For example, Company's net

profit is £9300 which is accrued. Means it is not earned by business in cash. So, business

could know how much actual cash is left with this report.

CONCLUSION

It's depend on the requirement of Rotork Plc upon which report it requires. Each

reporting methods has its own uses and importance. Cash flow statement report is useful to find

liquidity of a business. Income statement helps business in knowing how much earnings left

with it to invest in expansion activities and maintenance of business. Budget reports are the

forecasts which is based on the estimation. It requires for a Rotork Plc to allocate its funds

among different department accordingly.

TASK 2

P3 Calculation of Income statement using marginal and absorption costs

Marginal Costs: These costs also known as variable costing. In this costing method,

decisions can be taken on the basis of uncertainty of total costs (McNeil, Frey and Embrechts,

2015). For example, determination of fixed and variable cost is done to find out products for

production. Identification of marginal costing is required to know the impact of profit due to

change in output units. It also refers to as a movement in total cost with producing additional

output units.

Absorption Costs: It is a method for valuation of inventory. Here, manufacturing

expenses are distributed among different departments to know exactly how much cost of each

department is. For example, suppose Rotork Plc has two departments which is selling and

distribution and production. Let's assume that the employees of these two departments eat in a

canteen. The cost of canteen is bared by company itself. Hence, the cost of canteen is not a direct

cost but it supports both departments to run a business. Therefore, absorption methods suggests

to distribute canteen expenses among these two departments to get actual value.

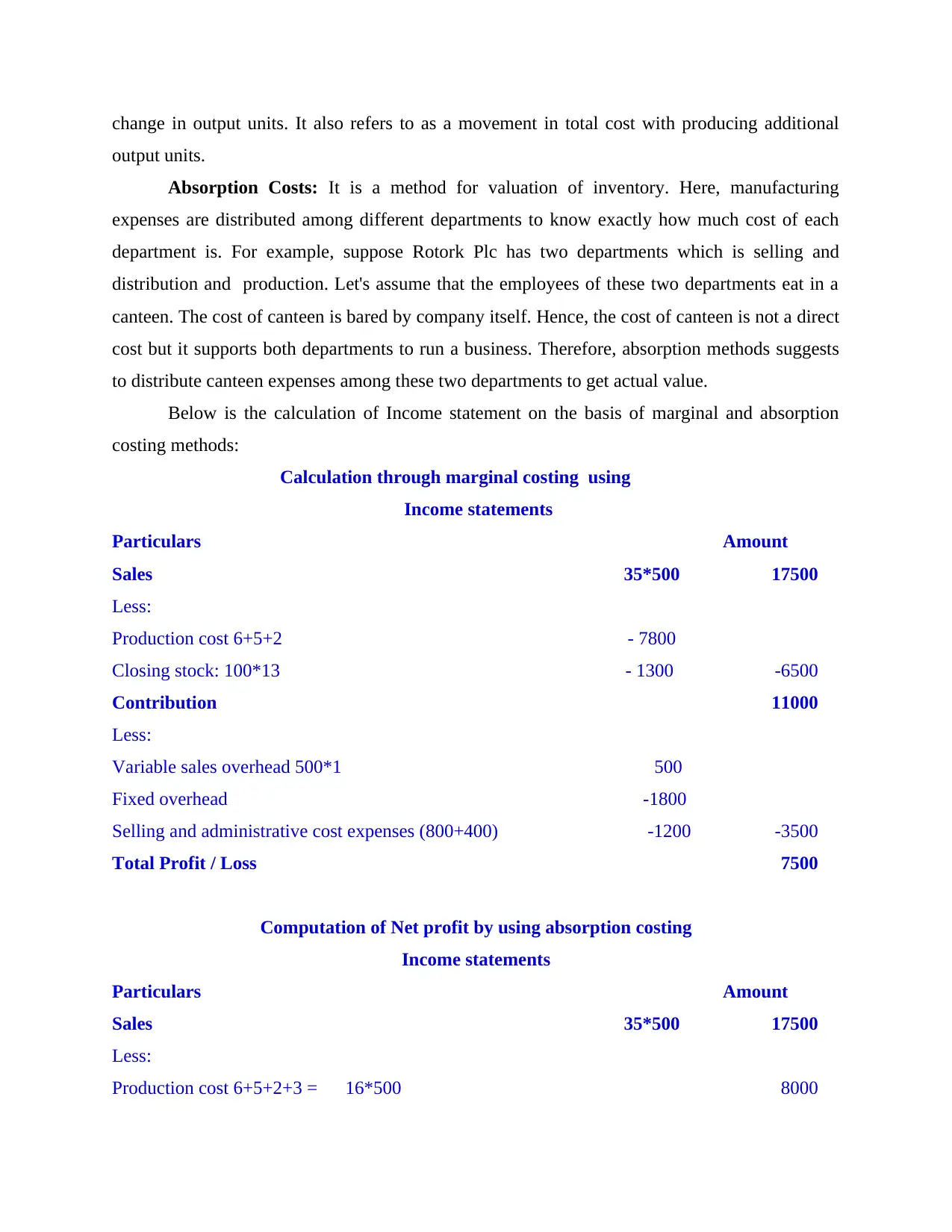

Below is the calculation of Income statement on the basis of marginal and absorption

costing methods:

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000

output units.

Absorption Costs: It is a method for valuation of inventory. Here, manufacturing

expenses are distributed among different departments to know exactly how much cost of each

department is. For example, suppose Rotork Plc has two departments which is selling and

distribution and production. Let's assume that the employees of these two departments eat in a

canteen. The cost of canteen is bared by company itself. Hence, the cost of canteen is not a direct

cost but it supports both departments to run a business. Therefore, absorption methods suggests

to distribute canteen expenses among these two departments to get actual value.

Below is the calculation of Income statement on the basis of marginal and absorption

costing methods:

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

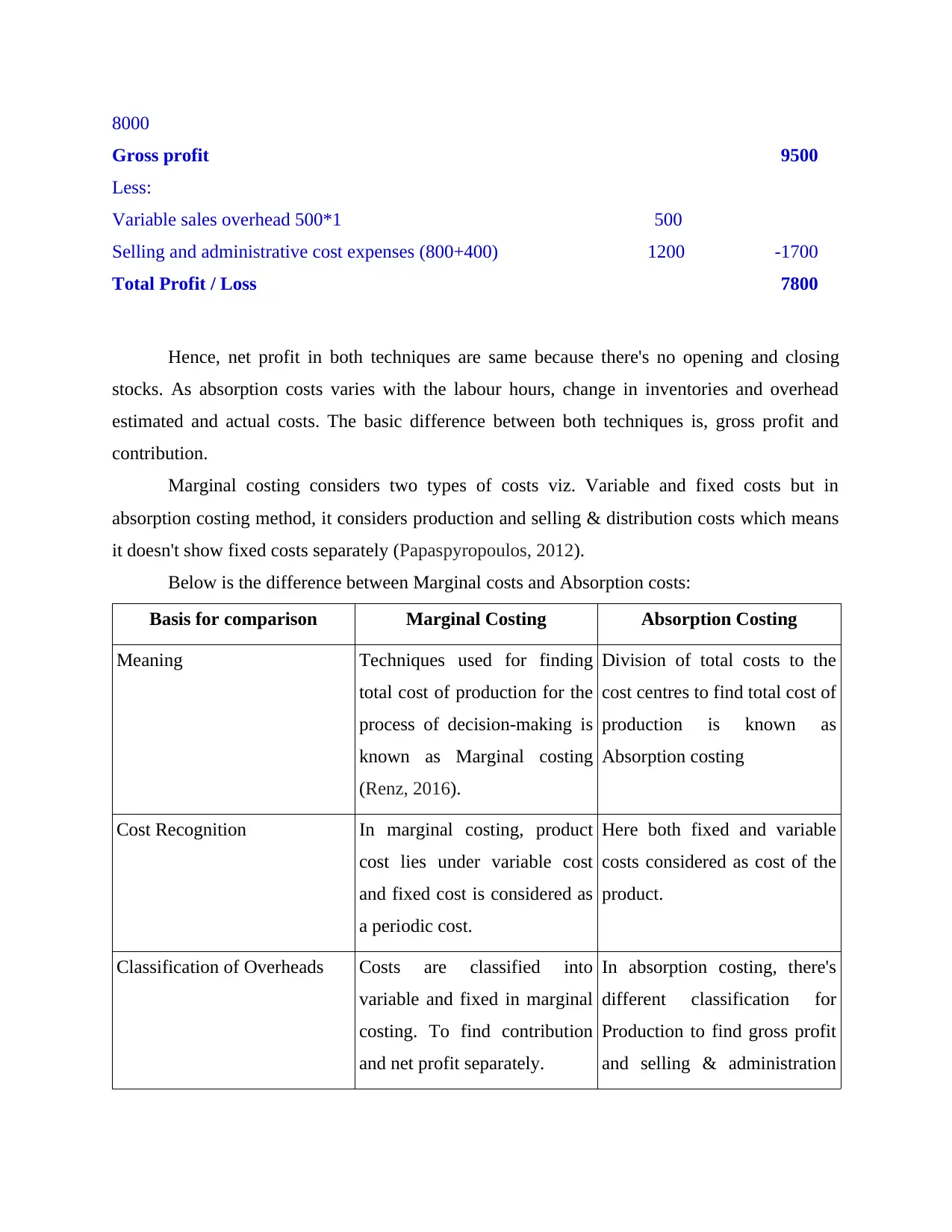

8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Hence, net profit in both techniques are same because there's no opening and closing

stocks. As absorption costs varies with the labour hours, change in inventories and overhead

estimated and actual costs. The basic difference between both techniques is, gross profit and

contribution.

Marginal costing considers two types of costs viz. Variable and fixed costs but in

absorption costing method, it considers production and selling & distribution costs which means

it doesn't show fixed costs separately (Papaspyropoulos, 2012).

Below is the difference between Marginal costs and Absorption costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning Techniques used for finding

total cost of production for the

process of decision-making is

known as Marginal costing

(Renz, 2016).

Division of total costs to the

cost centres to find total cost of

production is known as

Absorption costing

Cost Recognition In marginal costing, product

cost lies under variable cost

and fixed cost is considered as

a periodic cost.

Here both fixed and variable

costs considered as cost of the

product.

Classification of Overheads Costs are classified into

variable and fixed in marginal

costing. To find contribution

and net profit separately.

In absorption costing, there's

different classification for

Production to find gross profit

and selling & administration

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Hence, net profit in both techniques are same because there's no opening and closing

stocks. As absorption costs varies with the labour hours, change in inventories and overhead

estimated and actual costs. The basic difference between both techniques is, gross profit and

contribution.

Marginal costing considers two types of costs viz. Variable and fixed costs but in

absorption costing method, it considers production and selling & distribution costs which means

it doesn't show fixed costs separately (Papaspyropoulos, 2012).

Below is the difference between Marginal costs and Absorption costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning Techniques used for finding

total cost of production for the

process of decision-making is

known as Marginal costing

(Renz, 2016).

Division of total costs to the

cost centres to find total cost of

production is known as

Absorption costing

Cost Recognition In marginal costing, product

cost lies under variable cost

and fixed cost is considered as

a periodic cost.

Here both fixed and variable

costs considered as cost of the

product.

Classification of Overheads Costs are classified into

variable and fixed in marginal

costing. To find contribution

and net profit separately.

In absorption costing, there's

different classification for

Production to find gross profit

and selling & administration

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

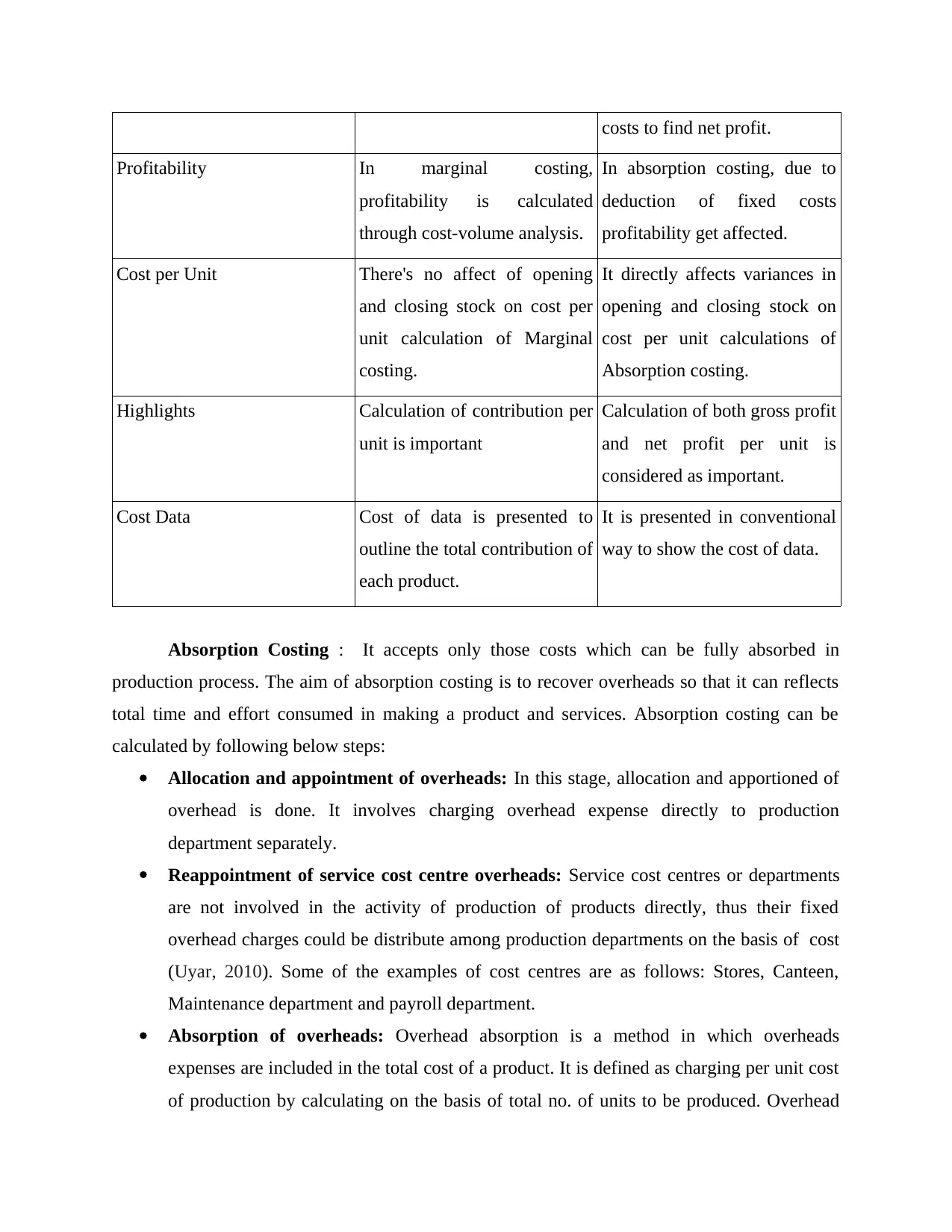

costs to find net profit.

Profitability In marginal costing,

profitability is calculated

through cost-volume analysis.

In absorption costing, due to

deduction of fixed costs

profitability get affected.

Cost per Unit There's no affect of opening

and closing stock on cost per

unit calculation of Marginal

costing.

It directly affects variances in

opening and closing stock on

cost per unit calculations of

Absorption costing.

Highlights Calculation of contribution per

unit is important

Calculation of both gross profit

and net profit per unit is

considered as important.

Cost Data Cost of data is presented to

outline the total contribution of

each product.

It is presented in conventional

way to show the cost of data.

Absorption Costing : It accepts only those costs which can be fully absorbed in

production process. The aim of absorption costing is to recover overheads so that it can reflects

total time and effort consumed in making a product and services. Absorption costing can be

calculated by following below steps:

Allocation and appointment of overheads: In this stage, allocation and apportioned of

overhead is done. It involves charging overhead expense directly to production

department separately.

Reappointment of service cost centre overheads: Service cost centres or departments

are not involved in the activity of production of products directly, thus their fixed

overhead charges could be distribute among production departments on the basis of cost

(Uyar, 2010). Some of the examples of cost centres are as follows: Stores, Canteen,

Maintenance department and payroll department.

Absorption of overheads: Overhead absorption is a method in which overheads

expenses are included in the total cost of a product. It is defined as charging per unit cost

of production by calculating on the basis of total no. of units to be produced. Overhead

Profitability In marginal costing,

profitability is calculated

through cost-volume analysis.

In absorption costing, due to

deduction of fixed costs

profitability get affected.

Cost per Unit There's no affect of opening

and closing stock on cost per

unit calculation of Marginal

costing.

It directly affects variances in

opening and closing stock on

cost per unit calculations of

Absorption costing.

Highlights Calculation of contribution per

unit is important

Calculation of both gross profit

and net profit per unit is

considered as important.

Cost Data Cost of data is presented to

outline the total contribution of

each product.

It is presented in conventional

way to show the cost of data.

Absorption Costing : It accepts only those costs which can be fully absorbed in

production process. The aim of absorption costing is to recover overheads so that it can reflects

total time and effort consumed in making a product and services. Absorption costing can be

calculated by following below steps:

Allocation and appointment of overheads: In this stage, allocation and apportioned of

overhead is done. It involves charging overhead expense directly to production

department separately.

Reappointment of service cost centre overheads: Service cost centres or departments

are not involved in the activity of production of products directly, thus their fixed

overhead charges could be distribute among production departments on the basis of cost

(Uyar, 2010). Some of the examples of cost centres are as follows: Stores, Canteen,

Maintenance department and payroll department.

Absorption of overheads: Overhead absorption is a method in which overheads

expenses are included in the total cost of a product. It is defined as charging per unit cost

of production by calculating on the basis of total no. of units to be produced. Overhead

absorption rate can be identified by dividing total overheads from number of units of

absorption products available. Sometimes number of units is estimated on the basis of

demand or previous trends.

TASK 3

P4 Report on advantages and disadvantages of different types of planning tools for budgetary

control

From: Management accounting officer

To: General manager of Rotork plc

Sub: Types of accounting tools

In this report, issues in management accounting functions like budgeting and budgetary control,

performance indicators and variances have been explained. This report contains advantages and

disadvantages of different types of planning tools to be used by management for budgetary

control.

Meaning of Budgetary control

Budgetary control is a process of managing funds through controlling them in advance on

the basis of future forecasting of sales and expenses in advance (Van Deventer, Imaiand

Mesler, 2013). Here, management controls actual income and expenditure by comparing it with

with their estimated figures for the same. It gives the value that varies with actual figures.

There are different types of tools in budgetary control process, these tools are Financial

Budgets, Operating Budgets, Non- monetary budgets and Fixed and variable Budgets. Below is

the diagram and explanation of these different tools:

Types planning tools of Budgetary

control

Financial Budgets

Fixed and variable

budgets

absorption products available. Sometimes number of units is estimated on the basis of

demand or previous trends.

TASK 3

P4 Report on advantages and disadvantages of different types of planning tools for budgetary

control

From: Management accounting officer

To: General manager of Rotork plc

Sub: Types of accounting tools

In this report, issues in management accounting functions like budgeting and budgetary control,

performance indicators and variances have been explained. This report contains advantages and

disadvantages of different types of planning tools to be used by management for budgetary

control.

Meaning of Budgetary control

Budgetary control is a process of managing funds through controlling them in advance on

the basis of future forecasting of sales and expenses in advance (Van Deventer, Imaiand

Mesler, 2013). Here, management controls actual income and expenditure by comparing it with

with their estimated figures for the same. It gives the value that varies with actual figures.

There are different types of tools in budgetary control process, these tools are Financial

Budgets, Operating Budgets, Non- monetary budgets and Fixed and variable Budgets. Below is

the diagram and explanation of these different tools:

Types planning tools of Budgetary

control

Financial Budgets

Fixed and variable

budgets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.