Detailed Management Accounting Report: Agmet Company, Unit 5 Overview

VerifiedAdded on 2020/07/23

|18

|5320

|45

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on their application within the context of Agmet Company, a chemical manufacturing firm. The report begins by highlighting the importance of management accounting in forecasting business trends and aiding in effective decision-making. It then delves into various types of management accounting, including cost accounting, price optimization, job costing, and inventory management, explaining their significance in controlling costs and optimizing production. Furthermore, the report explores different methods of management accounting reporting, such as segmental reporting, performance reports, inventory management reports, accounts receivables aging reports, job cost reports, and operational budget reports, illustrating their role in providing crucial information for decision-making and financial problem-solving. The report also discusses the benefits of a management accounting system, emphasizing its role in enhancing internal organizational strength and facilitating effective planning for new projects, ultimately leading to improved profitability and operational efficiency. Finally, the report emphasizes the role of planning tools and how management accounting systems help in responding to financial problems within the company.

UNIT 5 MAN ACC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential types of management accounting........................1

P2 Methods for management accounting reporting................................................................3

TASK 2............................................................................................................................................6

P3 Marginal and absorption costing and enumerating differences........................................6

TASK 3............................................................................................................................................8

P4 Kinds of planning tools.....................................................................................................8

P5 How management accounting system help to respond to financial problems................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential types of management accounting........................1

P2 Methods for management accounting reporting................................................................3

TASK 2............................................................................................................................................6

P3 Marginal and absorption costing and enumerating differences........................................6

TASK 3............................................................................................................................................8

P4 Kinds of planning tools.....................................................................................................8

P5 How management accounting system help to respond to financial problems................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting has much importance for management of the company so that

accurate decisions are taken with much ease. The present report deals with Agmet company

which is a chemical manufacturing firm. Management accounting information is required by

firm to strengthen organisation internally. Types of management accounting is discussed in the

report. Moreover, various methods of managerial accounting reports are also discussed in the

report. Planning tools are explained which are helpful in taking viable decisions. Budgeting and

planning are also accomplished with the help of management accounting information. This help

management of company to take better decisions. Moreover, marginal and absorption costing are

discussed. Furthermore, management accounting systems are also discussed so that financial

problems may be resolved quite effectively. Benefits of management accounting is also

discussed and it can be said that management accounting has great role in making enhanced

decisions.

TASK 1

P1 Management accounting and essential types of management accounting

Management accounting help to forecast business trends and as such, management is

benefited by given information for the betterment of the company. Agmet Company also uses

management accounting information so that it may be able to forecast trends in effective way

and take viable decisions. This accounting information is used by management of Agmet

Organisation to enhance internal strength so that operational tasks may be effectively managed

and customers' may be satisfied in the best possible way. Short-term and long-term policies are

taken quite easily with the help of management accounting information. Various sources which

are used in production process such as labour, materials and overheads as well as other

equipment which are required so that business may be successful in the market by satisfying

customer's demand (Otley, 2016).

Stakeholders such as creditors and investors also benefited as firm becomes strong

enough and go ahead of competitors. Various managerial reports are provided to management so

that it may analyse the same to reduce costs in effective way. This is important as business

should concentrate on expenditures so that it may not exceed revenue in any case. Thus,

expenses are reduced and revenue is maximised up to high extent which ultimately led to

1

Management accounting has much importance for management of the company so that

accurate decisions are taken with much ease. The present report deals with Agmet company

which is a chemical manufacturing firm. Management accounting information is required by

firm to strengthen organisation internally. Types of management accounting is discussed in the

report. Moreover, various methods of managerial accounting reports are also discussed in the

report. Planning tools are explained which are helpful in taking viable decisions. Budgeting and

planning are also accomplished with the help of management accounting information. This help

management of company to take better decisions. Moreover, marginal and absorption costing are

discussed. Furthermore, management accounting systems are also discussed so that financial

problems may be resolved quite effectively. Benefits of management accounting is also

discussed and it can be said that management accounting has great role in making enhanced

decisions.

TASK 1

P1 Management accounting and essential types of management accounting

Management accounting help to forecast business trends and as such, management is

benefited by given information for the betterment of the company. Agmet Company also uses

management accounting information so that it may be able to forecast trends in effective way

and take viable decisions. This accounting information is used by management of Agmet

Organisation to enhance internal strength so that operational tasks may be effectively managed

and customers' may be satisfied in the best possible way. Short-term and long-term policies are

taken quite easily with the help of management accounting information. Various sources which

are used in production process such as labour, materials and overheads as well as other

equipment which are required so that business may be successful in the market by satisfying

customer's demand (Otley, 2016).

Stakeholders such as creditors and investors also benefited as firm becomes strong

enough and go ahead of competitors. Various managerial reports are provided to management so

that it may analyse the same to reduce costs in effective way. This is important as business

should concentrate on expenditures so that it may not exceed revenue in any case. Thus,

expenses are reduced and revenue is maximised up to high extent which ultimately led to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achievement of goals and objectives in effectual way. Moreover, it helps to control company's

operations in that way so that it may earn desired profits quite easily. In relation to this, types of

management accounting are as follows-

1. Cost accounting:

Cost accounting is quite helpful as it helps to control costs in effective way so that

revenue may be earned by company in the best possible manner (Renz and Herman, 2016). This

is useful branch of management accounting as it helps to assess costs of various elements in the

production process and as such, take effective measures to reduce expenditures so that adequate

revenue may be earned with much ease. There are expenses which are required to be incurred so

that production may be accomplished in effectual way. As such, various expenditures are direct,

indirect, variable, semi-variable and fixed costs in the production process. Thus, various costs are

ascertained in that way so that steps can be taken by the management to minimise expenditures

in effectual way in order to earn desired revenue.

2. Price optimisation:

Price optimisation is useful technique of management accounting and is essentially

required in Agmet company as well. It is termed as a mathematical analysis which is carried out

to assess how price of a particular product affects customer's behaviour. In simple words, this

technique help management to determine price level of products in that way so customers may

be attracted to buy it. Thus, it is meaningful technique for management to quote price of goods in

the easiest way. Agmet Company also uses price optimisation method so that it may set price of

products by analysing consumer's behaviour. This help to achieve desired profits in accordance

with satisfaction of customers as well. Thus, it is good technique to quote price of commodities

by the organisation (Chenhall and Moers, 2015).

3. Job costing:

The method of job costing is quite useful in the manufacturing sector. In relation to this,

Agmet Company also takes into account job costing as it is engaged in manufacturing of

chemical products. Job costing is recording expenditures incurred on various jobs so that

management may keep track on each of the jobs so that expenses may be reduced so that more

production may be successfully accomplished in the best possible way. Manufacturing sector

2

operations in that way so that it may earn desired profits quite easily. In relation to this, types of

management accounting are as follows-

1. Cost accounting:

Cost accounting is quite helpful as it helps to control costs in effective way so that

revenue may be earned by company in the best possible manner (Renz and Herman, 2016). This

is useful branch of management accounting as it helps to assess costs of various elements in the

production process and as such, take effective measures to reduce expenditures so that adequate

revenue may be earned with much ease. There are expenses which are required to be incurred so

that production may be accomplished in effectual way. As such, various expenditures are direct,

indirect, variable, semi-variable and fixed costs in the production process. Thus, various costs are

ascertained in that way so that steps can be taken by the management to minimise expenditures

in effectual way in order to earn desired revenue.

2. Price optimisation:

Price optimisation is useful technique of management accounting and is essentially

required in Agmet company as well. It is termed as a mathematical analysis which is carried out

to assess how price of a particular product affects customer's behaviour. In simple words, this

technique help management to determine price level of products in that way so customers may

be attracted to buy it. Thus, it is meaningful technique for management to quote price of goods in

the easiest way. Agmet Company also uses price optimisation method so that it may set price of

products by analysing consumer's behaviour. This help to achieve desired profits in accordance

with satisfaction of customers as well. Thus, it is good technique to quote price of commodities

by the organisation (Chenhall and Moers, 2015).

3. Job costing:

The method of job costing is quite useful in the manufacturing sector. In relation to this,

Agmet Company also takes into account job costing as it is engaged in manufacturing of

chemical products. Job costing is recording expenditures incurred on various jobs so that

management may keep track on each of the jobs so that expenses may be reduced so that more

production may be successfully accomplished in the best possible way. Manufacturing sector

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

involves various jobs and as such, it is required to figure out costs incurred on jobs so that

ineffective ones can be opt out for achieving desired production quite easily. Job costs such as

materials, direct, equipments should be analysed in that way so that it may be minimised and

more production may be achieved for meeting customers' demand. Thus, it is effective technique

for controlling costs on various jobs.

4. Inventory management:

Production cannot be achieved by the company if it has not adequate stock in the

warehouse (Cooper, Ezzamel and Qu, 2017). Inventory should be managed in effective manner

so that demand of production department may be achieved with much ease. This is important as

if more than required inventory is purchased then, it leads to incur additional costs of handling it

in the warehouse. Moreover, it leads to spoilage of scarce resources. In contrary to this, if stock

is not in adequate quantity, then production cannot be achieved effectively. Thus, inventory

should be managed so that production may be accomplished in desired way. This method help

management to assess need for production department related to stock and then purchases in

desired quantity to satisfy demand of it and meet timely orders of customers. Thus, above

discussed types of management accounting are useful for company so that it may analyse costs

and reduced the same to accomplish targeted revenue with much ease.

P2 Methods for management accounting reporting

Management accounting has immense importance for management. In addition to this,

various methods of reporting are as follows-

1. Segmental report:

Segmental reporting is quite helpful in company which has many segments. In simple

words, it is much helpful in diversified business which has enough of segments in it. The

information extracted by this report is quite helpful for creditors and investors to assess

company's strengths and weaknesses in the best possible way (Chiarini and Vagnoni, 2015). This

information is required by them so that they may be able to judge company and make decisions

whether to provide funds to it or not. This is important so that funds initiated by them may be

recovered with much ease. Agmet Company provides segmental reports to them so that better

and effective decisions related to profitability and solvency can be taken by them quite

3

ineffective ones can be opt out for achieving desired production quite easily. Job costs such as

materials, direct, equipments should be analysed in that way so that it may be minimised and

more production may be achieved for meeting customers' demand. Thus, it is effective technique

for controlling costs on various jobs.

4. Inventory management:

Production cannot be achieved by the company if it has not adequate stock in the

warehouse (Cooper, Ezzamel and Qu, 2017). Inventory should be managed in effective manner

so that demand of production department may be achieved with much ease. This is important as

if more than required inventory is purchased then, it leads to incur additional costs of handling it

in the warehouse. Moreover, it leads to spoilage of scarce resources. In contrary to this, if stock

is not in adequate quantity, then production cannot be achieved effectively. Thus, inventory

should be managed so that production may be accomplished in desired way. This method help

management to assess need for production department related to stock and then purchases in

desired quantity to satisfy demand of it and meet timely orders of customers. Thus, above

discussed types of management accounting are useful for company so that it may analyse costs

and reduced the same to accomplish targeted revenue with much ease.

P2 Methods for management accounting reporting

Management accounting has immense importance for management. In addition to this,

various methods of reporting are as follows-

1. Segmental report:

Segmental reporting is quite helpful in company which has many segments. In simple

words, it is much helpful in diversified business which has enough of segments in it. The

information extracted by this report is quite helpful for creditors and investors to assess

company's strengths and weaknesses in the best possible way (Chiarini and Vagnoni, 2015). This

information is required by them so that they may be able to judge company and make decisions

whether to provide funds to it or not. This is important so that funds initiated by them may be

recovered with much ease. Agmet Company provides segmental reports to them so that better

and effective decisions related to profitability and solvency can be taken by them quite

3

effectively. As such, operational segments are adequately managed by company. As such, varied

information regarding operational segments are described in the report.

2. Performance report:

Performance report is useful for analysing performance of something in the company.

Generally, performance of employees in the company is observed so that efficiency can be

maintained with much ease. To overcome this problem, performance report is prepared and

imparted to management so that it may carefully assess performance of the workers so that

deficiency in them can be resolved by taking steps and as such, they may be able to perform

much better than earlier (Tappura and et.al, 2015). Agmet Company should use performance

report to determine level of performance so that corrective actions can be taken in the event of

reduced efficiency of employees. Thus, it is effective managerial report which provides much

needed information to management to assess workers' performance to maximise the same up to

high extent.

3. Inventory management report:

Maintaining inventory is difficult task for company so that it may achieve production

with much ease and satisfy customers as well. This is important as over purchasing of stock is

not beneficial for the company and leads to additional costs for managing in the warehouse. To

overcome this problem, inventory management report is prepared. This report is forwarded to

management so that it may analyse quantum of units held by company and assess future

requirements of production department so that inventory can be purchased with reference to

demand of production. This is required as company gets numerous orders on daily basis and as

such, it is required to manage inventory in effective way. This helps to ensure that inventory is

managed in effectual way and this helps to minimise wastage of scarce resources up to high

extent (Nitzl, 2016).

4. Accounts receivables ageing report:

Credit is common thing in the business which is required so that goods and services may

be brought by customers. For maintaining accounts receivables, a report named as accounts

receivables ageing report is prepared to analyse how much credit is outstanding in the business.

The report help management to assess unpaid customer invoices so that outstanding amount may

4

information regarding operational segments are described in the report.

2. Performance report:

Performance report is useful for analysing performance of something in the company.

Generally, performance of employees in the company is observed so that efficiency can be

maintained with much ease. To overcome this problem, performance report is prepared and

imparted to management so that it may carefully assess performance of the workers so that

deficiency in them can be resolved by taking steps and as such, they may be able to perform

much better than earlier (Tappura and et.al, 2015). Agmet Company should use performance

report to determine level of performance so that corrective actions can be taken in the event of

reduced efficiency of employees. Thus, it is effective managerial report which provides much

needed information to management to assess workers' performance to maximise the same up to

high extent.

3. Inventory management report:

Maintaining inventory is difficult task for company so that it may achieve production

with much ease and satisfy customers as well. This is important as over purchasing of stock is

not beneficial for the company and leads to additional costs for managing in the warehouse. To

overcome this problem, inventory management report is prepared. This report is forwarded to

management so that it may analyse quantum of units held by company and assess future

requirements of production department so that inventory can be purchased with reference to

demand of production. This is required as company gets numerous orders on daily basis and as

such, it is required to manage inventory in effective way. This helps to ensure that inventory is

managed in effectual way and this helps to minimise wastage of scarce resources up to high

extent (Nitzl, 2016).

4. Accounts receivables ageing report:

Credit is common thing in the business which is required so that goods and services may

be brought by customers. For maintaining accounts receivables, a report named as accounts

receivables ageing report is prepared to analyse how much credit is outstanding in the business.

The report help management to assess unpaid customer invoices so that outstanding amount may

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be recovered with much ease. This is important as if long credit is allowed then, timely recovery

of payments is interrupted up to maximum possible extent. Thus, management assess amount

which has not paid by the customers and that's why it is known as ageing report. This help

management to recover amount and if unpaid amount is more than, company should make well-

structured strategies and strict measures so that timely payment may be recovered with much

ease. Thus, accounts receivables ageing report provides much needed piece of information

beneficial for the company (Kokubu and Kitada, 2015).

5. Job cost report:

Various jobs are placed in the company so that effective work can be achieved. Job cost

report is useful in this scenario as it provides information to analyse various costs incurred on

jobs and as such, it can be reduced to achieve more production with much ease. Job costing

report is maintained in manufacturing and construction sector as they involve more jobs. The

report determine labour and materials costs and as such, steps are taken by management to

minimise the same to attain desired revenue. As such, when costs are analysed, then management

take measures to control expenditures so that efficiency may be achieved in the best possible

way. As such, costs are assigned to particular job and as a result, overall expenses are cut down

which help to accomplish targeted production in effectual way. Thus, this report is beneficial for

the management of Agmet Company to control costs incurred on jobs.

6. Operational budget report:

Operational budget is prepared in advance so that revenue and expenditures can be

decided so that control can be attained quite effectively. This is important so that business may

come to know future costs in advance and as such, adequate revenue may be earned (Wouters

and Kirchberger, 2015). Operational budget report is prepared on quarterly and annual basis

depending upon the company. Operational activities are assessed by the management and as a

result, measures are taken to control them so that adequate profits may be earned with much

ease. It includes various budgets such as production, sales, overhead which are relevant to

company so that expenditures can be analysed quite effectively and business may flourish as

well. This report is beneficial for the management of company to easily predict future costs.

Benefits of management accounting system

5

of payments is interrupted up to maximum possible extent. Thus, management assess amount

which has not paid by the customers and that's why it is known as ageing report. This help

management to recover amount and if unpaid amount is more than, company should make well-

structured strategies and strict measures so that timely payment may be recovered with much

ease. Thus, accounts receivables ageing report provides much needed piece of information

beneficial for the company (Kokubu and Kitada, 2015).

5. Job cost report:

Various jobs are placed in the company so that effective work can be achieved. Job cost

report is useful in this scenario as it provides information to analyse various costs incurred on

jobs and as such, it can be reduced to achieve more production with much ease. Job costing

report is maintained in manufacturing and construction sector as they involve more jobs. The

report determine labour and materials costs and as such, steps are taken by management to

minimise the same to attain desired revenue. As such, when costs are analysed, then management

take measures to control expenditures so that efficiency may be achieved in the best possible

way. As such, costs are assigned to particular job and as a result, overall expenses are cut down

which help to accomplish targeted production in effectual way. Thus, this report is beneficial for

the management of Agmet Company to control costs incurred on jobs.

6. Operational budget report:

Operational budget is prepared in advance so that revenue and expenditures can be

decided so that control can be attained quite effectively. This is important so that business may

come to know future costs in advance and as such, adequate revenue may be earned (Wouters

and Kirchberger, 2015). Operational budget report is prepared on quarterly and annual basis

depending upon the company. Operational activities are assessed by the management and as a

result, measures are taken to control them so that adequate profits may be earned with much

ease. It includes various budgets such as production, sales, overhead which are relevant to

company so that expenditures can be analysed quite effectively and business may flourish as

well. This report is beneficial for the management of company to easily predict future costs.

Benefits of management accounting system

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting system is quite importance for the management as it help to take

effective and better decisions. The main essence of management accounting information is that

managers can resolve internal problems with much ease. This is useful information as goals can

be achieved quite effectively by strengthening organisation internally. Moreover, planning about

the new project can also be accomplished by relying on such information (Cleary, 2015).

Controlling can also be done in effective manner as various costs are analysed and steps are

taken so that expenditures may not exceed revenue in any case.

TASK 2

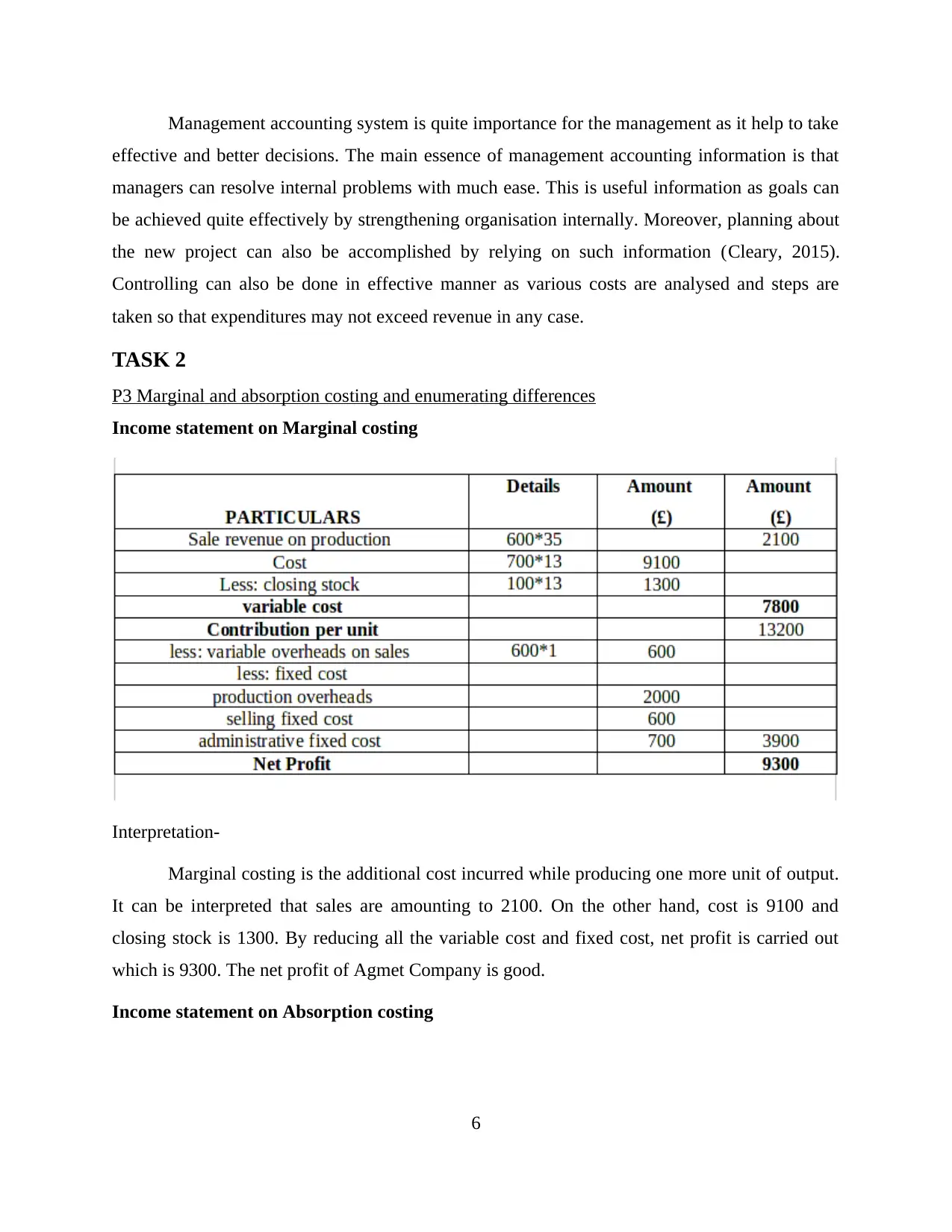

P3 Marginal and absorption costing and enumerating differences

Income statement on Marginal costing

Interpretation-

Marginal costing is the additional cost incurred while producing one more unit of output.

It can be interpreted that sales are amounting to 2100. On the other hand, cost is 9100 and

closing stock is 1300. By reducing all the variable cost and fixed cost, net profit is carried out

which is 9300. The net profit of Agmet Company is good.

Income statement on Absorption costing

6

effective and better decisions. The main essence of management accounting information is that

managers can resolve internal problems with much ease. This is useful information as goals can

be achieved quite effectively by strengthening organisation internally. Moreover, planning about

the new project can also be accomplished by relying on such information (Cleary, 2015).

Controlling can also be done in effective manner as various costs are analysed and steps are

taken so that expenditures may not exceed revenue in any case.

TASK 2

P3 Marginal and absorption costing and enumerating differences

Income statement on Marginal costing

Interpretation-

Marginal costing is the additional cost incurred while producing one more unit of output.

It can be interpreted that sales are amounting to 2100. On the other hand, cost is 9100 and

closing stock is 1300. By reducing all the variable cost and fixed cost, net profit is carried out

which is 9300. The net profit of Agmet Company is good.

Income statement on Absorption costing

6

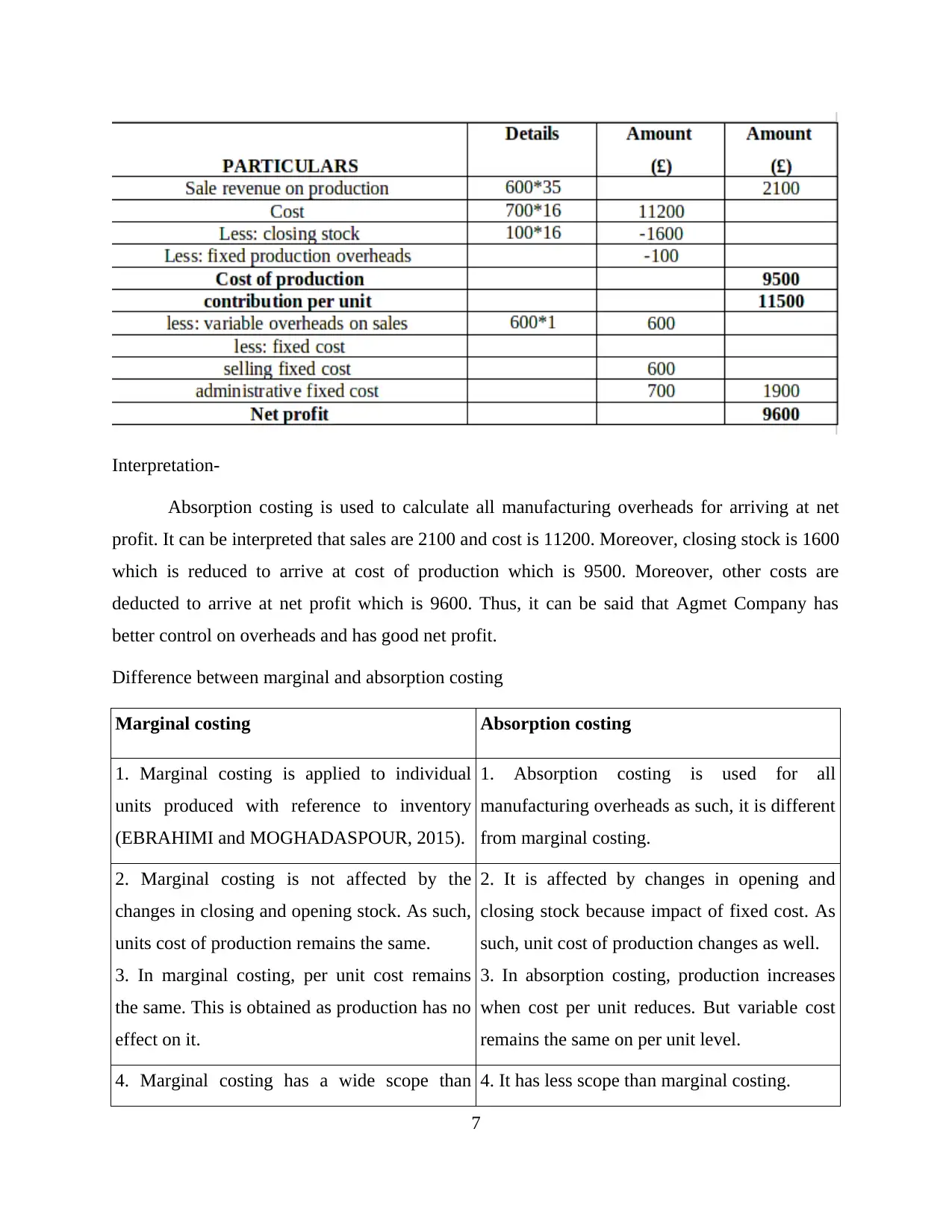

Interpretation-

Absorption costing is used to calculate all manufacturing overheads for arriving at net

profit. It can be interpreted that sales are 2100 and cost is 11200. Moreover, closing stock is 1600

which is reduced to arrive at cost of production which is 9500. Moreover, other costs are

deducted to arrive at net profit which is 9600. Thus, it can be said that Agmet Company has

better control on overheads and has good net profit.

Difference between marginal and absorption costing

Marginal costing Absorption costing

1. Marginal costing is applied to individual

units produced with reference to inventory

(EBRAHIMI and MOGHADASPOUR, 2015).

1. Absorption costing is used for all

manufacturing overheads as such, it is different

from marginal costing.

2. Marginal costing is not affected by the

changes in closing and opening stock. As such,

units cost of production remains the same.

3. In marginal costing, per unit cost remains

the same. This is obtained as production has no

effect on it.

2. It is affected by changes in opening and

closing stock because impact of fixed cost. As

such, unit cost of production changes as well.

3. In absorption costing, production increases

when cost per unit reduces. But variable cost

remains the same on per unit level.

4. Marginal costing has a wide scope than 4. It has less scope than marginal costing.

7

Absorption costing is used to calculate all manufacturing overheads for arriving at net

profit. It can be interpreted that sales are 2100 and cost is 11200. Moreover, closing stock is 1600

which is reduced to arrive at cost of production which is 9500. Moreover, other costs are

deducted to arrive at net profit which is 9600. Thus, it can be said that Agmet Company has

better control on overheads and has good net profit.

Difference between marginal and absorption costing

Marginal costing Absorption costing

1. Marginal costing is applied to individual

units produced with reference to inventory

(EBRAHIMI and MOGHADASPOUR, 2015).

1. Absorption costing is used for all

manufacturing overheads as such, it is different

from marginal costing.

2. Marginal costing is not affected by the

changes in closing and opening stock. As such,

units cost of production remains the same.

3. In marginal costing, per unit cost remains

the same. This is obtained as production has no

effect on it.

2. It is affected by changes in opening and

closing stock because impact of fixed cost. As

such, unit cost of production changes as well.

3. In absorption costing, production increases

when cost per unit reduces. But variable cost

remains the same on per unit level.

4. Marginal costing has a wide scope than 4. It has less scope than marginal costing.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

absorption costing as it calculates each level of

units of produced.

5. The main essence of marginal costing is that

it uses only variable cost for valuing inventory.

5. On the other hand, both variable and fixed

costs are taken for valuing inventory.

Techniques of Management accounting

Revaluation accounting

Revaluation accounting is done to match book value of business's asset with current

market value. This is done so that correct ascertainment of profit may be made with much ease

else cost of acquisition will be over than current market value (Coad, Jack and Kholeif, 2015).

Funds flow statement

This statement is good management accounting technique which shows changes occurred

in financial statements of two years stating the concrete reason listing sources and application of

funds.

Cash flow forecasting

Cash flow forecasting is the prediction technique to analyse operating expenditures and

revenue of firm and to know how much amount of cash to be flowed in and out of the

organisation quite effectively.

TASK 3

P4 Kinds of planning tools

Incremental budgeting

Incremental budgeting is the planning tool which is the easiest way to prepare budget by

taking previous year base and just increment the same. This is helpful as only figures are

increased which will be required by departments in future period (Tucker and Schaltegger,

2016).

Advantages

8

units of produced.

5. The main essence of marginal costing is that

it uses only variable cost for valuing inventory.

5. On the other hand, both variable and fixed

costs are taken for valuing inventory.

Techniques of Management accounting

Revaluation accounting

Revaluation accounting is done to match book value of business's asset with current

market value. This is done so that correct ascertainment of profit may be made with much ease

else cost of acquisition will be over than current market value (Coad, Jack and Kholeif, 2015).

Funds flow statement

This statement is good management accounting technique which shows changes occurred

in financial statements of two years stating the concrete reason listing sources and application of

funds.

Cash flow forecasting

Cash flow forecasting is the prediction technique to analyse operating expenditures and

revenue of firm and to know how much amount of cash to be flowed in and out of the

organisation quite effectively.

TASK 3

P4 Kinds of planning tools

Incremental budgeting

Incremental budgeting is the planning tool which is the easiest way to prepare budget by

taking previous year base and just increment the same. This is helpful as only figures are

increased which will be required by departments in future period (Tucker and Schaltegger,

2016).

Advantages

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. No complex computations are required as only figures are added from previous year to

prepare new budget. As such, it consumes less time as not entire budget needs to be prepared.

2. It is helpful as not large deviations are made by incrementing figures year after year.

Moreover, budget is prepared with much ease as less manpower is required.

Disadvantages

1. Changes are not analysed as it is mere based on increasing amount for each

department. Thus, needs of various departments may be different which is not analysed by

management (Strauss, Kristandl and Quinn, 2015).

2. The main limitation of incremental budgeting as a planning tool is that managers tend

to utilise unnecessary funds for their department and this leads to wastage of resources as well.

In contrary to this, zero based budgeting method should be used.

Zero based Budgeting

This planning tool is different from incremental budgeting. It does not take into account

previous figures and prepare budget for coming period. Instead of this, it prepares budget from

scratch base or zero base. This is effective planning tool as needs of department are analysed

from completely zero base. This leads to optimum utilisation of resources.

Advantages

1. It is effective method as calculations are easier and to arrive at new budget. As it does

not take historical figures, it is leads to effective assessment of needs of department.

2. Budget inflation is not made as company determine demand of departments and as

such, it provides funds that fulfil their requirement. This leads to effective use of resources.

Disadvantages

1. It is not suitable tool for planning as it involves lot of manpower to formulate

completely new budget which is a tedious task for employees involved in the process (Theriou,

2015).

2. Zero based budgeting takes completely new base for ascertaining requirement of

departments which is a time consuming process and not suitable for large organisations.

9

prepare new budget. As such, it consumes less time as not entire budget needs to be prepared.

2. It is helpful as not large deviations are made by incrementing figures year after year.

Moreover, budget is prepared with much ease as less manpower is required.

Disadvantages

1. Changes are not analysed as it is mere based on increasing amount for each

department. Thus, needs of various departments may be different which is not analysed by

management (Strauss, Kristandl and Quinn, 2015).

2. The main limitation of incremental budgeting as a planning tool is that managers tend

to utilise unnecessary funds for their department and this leads to wastage of resources as well.

In contrary to this, zero based budgeting method should be used.

Zero based Budgeting

This planning tool is different from incremental budgeting. It does not take into account

previous figures and prepare budget for coming period. Instead of this, it prepares budget from

scratch base or zero base. This is effective planning tool as needs of department are analysed

from completely zero base. This leads to optimum utilisation of resources.

Advantages

1. It is effective method as calculations are easier and to arrive at new budget. As it does

not take historical figures, it is leads to effective assessment of needs of department.

2. Budget inflation is not made as company determine demand of departments and as

such, it provides funds that fulfil their requirement. This leads to effective use of resources.

Disadvantages

1. It is not suitable tool for planning as it involves lot of manpower to formulate

completely new budget which is a tedious task for employees involved in the process (Theriou,

2015).

2. Zero based budgeting takes completely new base for ascertaining requirement of

departments which is a time consuming process and not suitable for large organisations.

9

NPV

NPV (Net Present Value) is effective planning tool which help management to assess

profitability aspect of new project with much ease. This is effective tool for management so that

most profitable project can be selected among various alternatives. Thus, it assists management

to opt for project depending upon profitability aspect.

Advantages

1. It is important for management to assess profitability of the project. Moreover, it

considers time of value of money as well. Moreover, it contributes in increasing value of

organisation.

2. Another advantage of NPV method is that it also takes cost of capital while evaluating

project and risks are also analysed with much ease. Moreover, calculation of NPV is easier as

well (Carlsson-Wall, Kraus and Lind, 2015).

Disadvantages

1. The main limitation of NPV is that it takes discounting rate for assessing profitability

of project which is difficult to carry out and wrong results are extracted.

2. Another limitation of this method is that it is based on mere projections and as such,

results interpreted may be wrong and not meaningful. This is not effective planning tool as it

does not consider unforeseen events which might affect profitability of the project.

IRR

IRR (Internal Rate of Return) is another useful method for planning purpose. IRR is

effective method for assessing investment by taking discounting rate factor. The main essence of

such method is that it helps NPV of cash flows from investment equal to zero. Higher IRR is

better for company and could invest in the project (Concept, Advantages, Disadvantages,

Calculation And Decision Rules Of Internal Rate Of Return(IRR), 2018).

Advantages

1. IRR is useful as a planning tool as it considers time value of money and as such, it is

quite easy to compute the value of IRR. It is also simple to use and can be easily interpreted quite

effectively.

10

NPV (Net Present Value) is effective planning tool which help management to assess

profitability aspect of new project with much ease. This is effective tool for management so that

most profitable project can be selected among various alternatives. Thus, it assists management

to opt for project depending upon profitability aspect.

Advantages

1. It is important for management to assess profitability of the project. Moreover, it

considers time of value of money as well. Moreover, it contributes in increasing value of

organisation.

2. Another advantage of NPV method is that it also takes cost of capital while evaluating

project and risks are also analysed with much ease. Moreover, calculation of NPV is easier as

well (Carlsson-Wall, Kraus and Lind, 2015).

Disadvantages

1. The main limitation of NPV is that it takes discounting rate for assessing profitability

of project which is difficult to carry out and wrong results are extracted.

2. Another limitation of this method is that it is based on mere projections and as such,

results interpreted may be wrong and not meaningful. This is not effective planning tool as it

does not consider unforeseen events which might affect profitability of the project.

IRR

IRR (Internal Rate of Return) is another useful method for planning purpose. IRR is

effective method for assessing investment by taking discounting rate factor. The main essence of

such method is that it helps NPV of cash flows from investment equal to zero. Higher IRR is

better for company and could invest in the project (Concept, Advantages, Disadvantages,

Calculation And Decision Rules Of Internal Rate Of Return(IRR), 2018).

Advantages

1. IRR is useful as a planning tool as it considers time value of money and as such, it is

quite easy to compute the value of IRR. It is also simple to use and can be easily interpreted quite

effectively.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.