Management Accounting Report: RH Amar Analysis and Strategies

VerifiedAdded on 2021/02/20

|16

|4318

|36

Report

AI Summary

This report examines the application of management accounting principles within the context of RH Amar, a food import and distribution company. It covers essential elements of management accounting, including data collection, analysis, and decision-making processes. The report details various management accounting systems, such as financial, cost, and tax accounting, along with different reporting methods like performance reports, inventory management reports, cash flow statements, and balance sheets. It further explores costing techniques through marginal and absorption costing methods, including the preparation of cost cards and profit and loss statements for different months. Finally, the report discusses the advantages and disadvantages of planning tools like zero-based budgeting and provides an overview of how management accounting systems support the resolution of financial problems within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting as well as its essential requirements.............................................1

P2. Methods used for management accounting reporting...........................................................2

P3. Cost of product by using effective techniques......................................................................4

P4. Advantage or disadvantage of different planning tools........................................................7

P5. Management accounting system support to respond financial problem.............................10

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting as well as its essential requirements.............................................1

P2. Methods used for management accounting reporting...........................................................2

P3. Cost of product by using effective techniques......................................................................4

P4. Advantage or disadvantage of different planning tools........................................................7

P5. Management accounting system support to respond financial problem.............................10

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................14

INTRODUCTION

Management accounting provides sufficient advantages like monitoring day-to-day

operations, analysing data and writing financial statements with the support of everything

collected related to operations (Arunruangsirilert and Chonglerttham, 2017). Manager need detail

and cosine information about each and every business activity that enables them to make better

decision for improving the overall productivity and profit margins. In this report, RH Amar have

been selected that helps to better understand the importance of management accounting. The

company use to import and distribute food item for each and every type of customer such baby

food, capers, Meat and fish, Herbs, spices.

The report cover, different type of management accounting system and reports, costing

techniques to prepare income statements, planning tools to support budgetary control and

resolving of financial problems.

TASK 1

P1. Management accounting as well as its essential requirements.

In business term, management accounting is wider concept that comprise collecting of

useful information, analysing of relevant data, formulation of plans and making decision in order

to increase the overall productivity and profitability of company. The main elements related with

are gathering, preparing, planning and making decision for better results in next financial year

(Barnard and Mostert, 2015).

Key functions of Management accounting system: The process includes different

functions of such as :

Modifies data: This practice relates with organising business activities, evaluating price

level, making available of necessary information for improving productivity of company.

Facilitates control account: It helps in building effective communication network

among entire internal team to work accordingly so that detail summary is given to maintain

ledger free of error.

Different type of accounts

Financial accounting system: This system mainly helps to plans, manages, schedules

different activities, area of an establishment's accounts, finances, division issues,

monitoring and other financial activities within company. For example, in RH Amar this

1

Management accounting provides sufficient advantages like monitoring day-to-day

operations, analysing data and writing financial statements with the support of everything

collected related to operations (Arunruangsirilert and Chonglerttham, 2017). Manager need detail

and cosine information about each and every business activity that enables them to make better

decision for improving the overall productivity and profit margins. In this report, RH Amar have

been selected that helps to better understand the importance of management accounting. The

company use to import and distribute food item for each and every type of customer such baby

food, capers, Meat and fish, Herbs, spices.

The report cover, different type of management accounting system and reports, costing

techniques to prepare income statements, planning tools to support budgetary control and

resolving of financial problems.

TASK 1

P1. Management accounting as well as its essential requirements.

In business term, management accounting is wider concept that comprise collecting of

useful information, analysing of relevant data, formulation of plans and making decision in order

to increase the overall productivity and profitability of company. The main elements related with

are gathering, preparing, planning and making decision for better results in next financial year

(Barnard and Mostert, 2015).

Key functions of Management accounting system: The process includes different

functions of such as :

Modifies data: This practice relates with organising business activities, evaluating price

level, making available of necessary information for improving productivity of company.

Facilitates control account: It helps in building effective communication network

among entire internal team to work accordingly so that detail summary is given to maintain

ledger free of error.

Different type of accounts

Financial accounting system: This system mainly helps to plans, manages, schedules

different activities, area of an establishment's accounts, finances, division issues,

monitoring and other financial activities within company. For example, in RH Amar this

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system is used for conducting auditing such as all the financial book prepared by the

internal department are audited easily to check the authenticity so that true and fair image

of company within an accounting year.

Cost accounting system: This system is useful in collecting and reporting of meaningful

information related to total cost that has been used in managing and controlling valuable

operation of company. For example, in respective firm this system is used for product

costing so that actual requirement of cash that is needed to prepare desired goods and

services for customer can be determined.

Management accounting system: This system is consider to be one of the most crucial

part of business, as it support in making decision about different aspects of company

operation such as setting price, allocating cost, valuation of inventory etc. For instance, in

RH Amar manager use this system in order to calculate the total profit earned within an

accounting year by evaluating cost and revenue earned during that period (Bellanca,

Cultrera and Vermeylen, 2015).

Tax accounting: This is consider to be authorised accounting method that mainly focus

on taxes so that funds can be tracked for a financial year. For example, an employee of

respective firm is liable to pay income tax which is to be calculated on the annual wages

and income. Moreover, tax reporting primarily focuses on aspects such as profits,

qualified deductions, capital unrealized gains as well as other activities impacting the tax

burden of the entity.

P2. Methods used for management accounting reporting.

In present time, it is crucial for an organisation to maintain proper reports so that

information can be analysed and decision are made for better improvement in future time. There

are different type of management accounting reports that are prepared by the manager of

company to record each and every business happening that ease the decision making. In RH

Amar manager use to prepare valuable reports that are effective to provide detail knowledge

about each and every aspect of business to the internal manager. Some of these reports are

discussed underneath:

Performance report: The purpose for updating performance reports is to assess the

actual performance of the company with its employee results during the financial year.

RH Amar's manage people through this report to specifically assess the actual

2

internal department are audited easily to check the authenticity so that true and fair image

of company within an accounting year.

Cost accounting system: This system is useful in collecting and reporting of meaningful

information related to total cost that has been used in managing and controlling valuable

operation of company. For example, in respective firm this system is used for product

costing so that actual requirement of cash that is needed to prepare desired goods and

services for customer can be determined.

Management accounting system: This system is consider to be one of the most crucial

part of business, as it support in making decision about different aspects of company

operation such as setting price, allocating cost, valuation of inventory etc. For instance, in

RH Amar manager use this system in order to calculate the total profit earned within an

accounting year by evaluating cost and revenue earned during that period (Bellanca,

Cultrera and Vermeylen, 2015).

Tax accounting: This is consider to be authorised accounting method that mainly focus

on taxes so that funds can be tracked for a financial year. For example, an employee of

respective firm is liable to pay income tax which is to be calculated on the annual wages

and income. Moreover, tax reporting primarily focuses on aspects such as profits,

qualified deductions, capital unrealized gains as well as other activities impacting the tax

burden of the entity.

P2. Methods used for management accounting reporting.

In present time, it is crucial for an organisation to maintain proper reports so that

information can be analysed and decision are made for better improvement in future time. There

are different type of management accounting reports that are prepared by the manager of

company to record each and every business happening that ease the decision making. In RH

Amar manager use to prepare valuable reports that are effective to provide detail knowledge

about each and every aspect of business to the internal manager. Some of these reports are

discussed underneath:

Performance report: The purpose for updating performance reports is to assess the

actual performance of the company with its employee results during the financial year.

RH Amar's manage people through this report to specifically assess the actual

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of company's and make improvement plans to increase overall productivity.

A performance report is an important method for companies. This enables company to

record and monitor the quality of employees. Making these reports cautiously is critical

since they could be key drivers to inspire more positively or negatively employee

behaviour (Brewer, Garrison and Noreen, 2015). A very well-written report of

performance blends knowledge, observation, integrity and tact.

Inventory management report: This report is mainly prepared by the manager to record

the total inventories. In RH Amar this report is prepared by stock handlers or inventory to

monitor and control different inventories. The inventory report is a description of trade,

company or association. This provides a detailed account of different products ' inventory

or distribution. Report could be presented in different ways and in different lengths. It

must always be transparent, quick and thorough to have a reliable stock report.

Purpose and use of valuable statements for company are discussed below:

Cash flow statement: The main aim of the this statement is to demonstrate across a

given period of time, in which an organization produced money and total cash expended to reach

the desired targets. This statements is consider to be valuable as it help to analyse the actual

liquidity, solvency of company that ease in make future plans for increasing production. In RH

Amar this statements is used to detect the total cash flows from different components such as

operating, financing and investing. This is also used determine the variation between the

projected and actual cash inflows and outflows for a specific period (Christner and Strömsten,

2015).

Balance sheet: This is consider to be valuable financial statements that defines the actual

volume or worth of business within specific period of time. Balance sheet is mainly prepared to

disclose the financial status and strength of company at specific point of time. In respective firm,

manager use to prepare balance sheet that help to show the total total assets and liabilities and

total amount invested within different project. Such data is more useful whenever the financials

are grouped together for many consecutive years so that patterns can be seen in the various line

items.

Management accounting systems

Price optimisation systems: This system is useful to fix the most suitable prices for the

goods which are produced within company to increase profitability. In RH Amar, manager use

3

A performance report is an important method for companies. This enables company to

record and monitor the quality of employees. Making these reports cautiously is critical

since they could be key drivers to inspire more positively or negatively employee

behaviour (Brewer, Garrison and Noreen, 2015). A very well-written report of

performance blends knowledge, observation, integrity and tact.

Inventory management report: This report is mainly prepared by the manager to record

the total inventories. In RH Amar this report is prepared by stock handlers or inventory to

monitor and control different inventories. The inventory report is a description of trade,

company or association. This provides a detailed account of different products ' inventory

or distribution. Report could be presented in different ways and in different lengths. It

must always be transparent, quick and thorough to have a reliable stock report.

Purpose and use of valuable statements for company are discussed below:

Cash flow statement: The main aim of the this statement is to demonstrate across a

given period of time, in which an organization produced money and total cash expended to reach

the desired targets. This statements is consider to be valuable as it help to analyse the actual

liquidity, solvency of company that ease in make future plans for increasing production. In RH

Amar this statements is used to detect the total cash flows from different components such as

operating, financing and investing. This is also used determine the variation between the

projected and actual cash inflows and outflows for a specific period (Christner and Strömsten,

2015).

Balance sheet: This is consider to be valuable financial statements that defines the actual

volume or worth of business within specific period of time. Balance sheet is mainly prepared to

disclose the financial status and strength of company at specific point of time. In respective firm,

manager use to prepare balance sheet that help to show the total total assets and liabilities and

total amount invested within different project. Such data is more useful whenever the financials

are grouped together for many consecutive years so that patterns can be seen in the various line

items.

Management accounting systems

Price optimisation systems: This system is useful to fix the most suitable prices for the

goods which are produced within company to increase profitability. In RH Amar, manager use

3

this system to define the best price for different food items according to the demand and

customer type. This system help to maintain reasonable profit for company by setting the

suitable price of goods that would definitely increaser the overall demand which have a positive

influence profitability.

Inventory management system: This system is helpful in management of actual stock

available for production process. In RH Amar this system is consider to be one of the most

crucial because it help in producing different food stuff as per the needs of customer. By using

this system manager gets the knowledge about the total raw material which can be helpful to

complete the production of food items that are mostly required by clients visiting ion regular

basis. There are mainly three type of Inventory management system such as LIFO, FIFO and

AVCO. LIFO define stock that is recently acquired is first used for operations. In FIFO process

the goods that are previously acquired products are used for producing goods (Englund and

Gerdin, 2018).

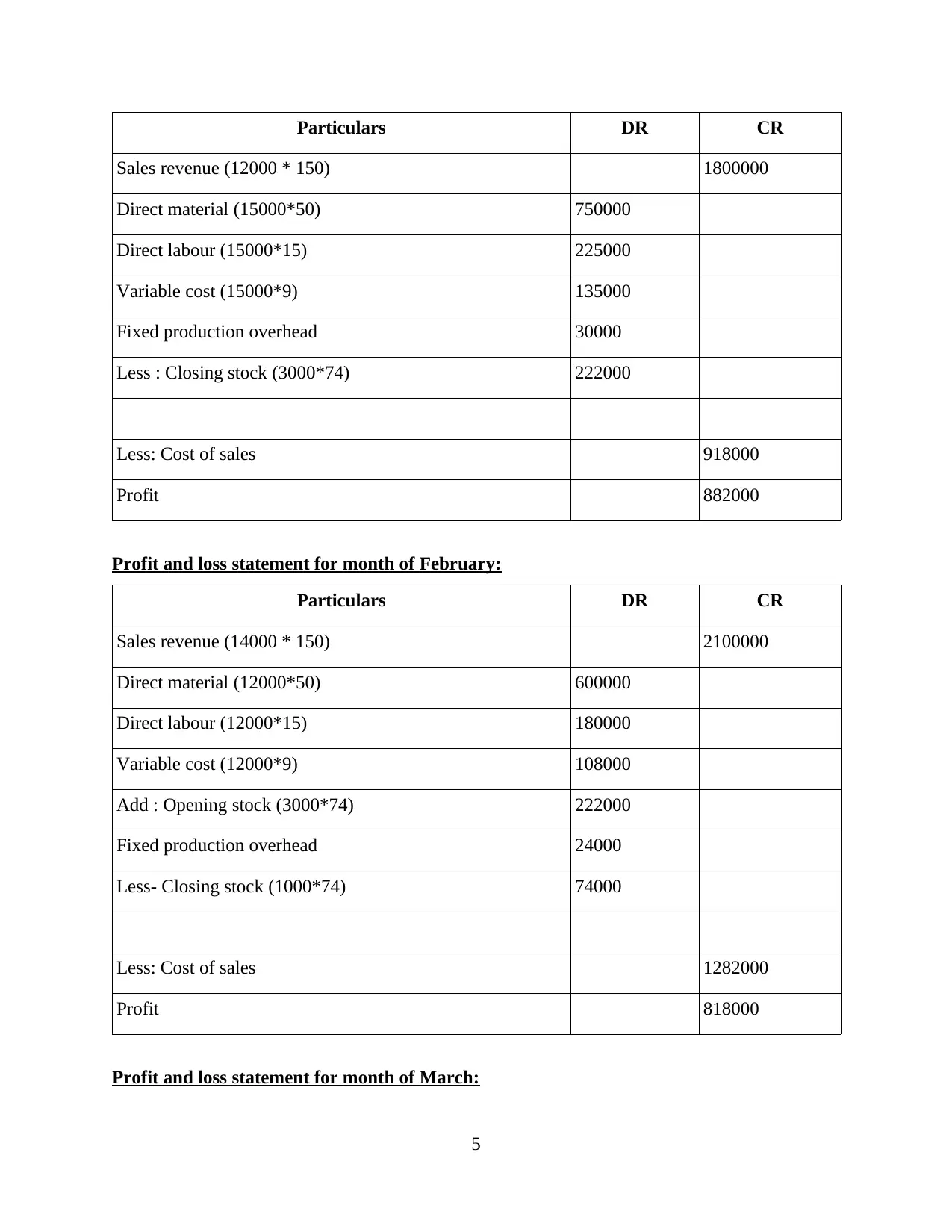

P3. Cost of product by using effective techniques.

CASE 1:

(a) Preparation of cost card:

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 9

Marginal cost 74

Selling price 150

Marginal cost 74

Contribution 76

(b) Profit and loss statement for month of January:

4

customer type. This system help to maintain reasonable profit for company by setting the

suitable price of goods that would definitely increaser the overall demand which have a positive

influence profitability.

Inventory management system: This system is helpful in management of actual stock

available for production process. In RH Amar this system is consider to be one of the most

crucial because it help in producing different food stuff as per the needs of customer. By using

this system manager gets the knowledge about the total raw material which can be helpful to

complete the production of food items that are mostly required by clients visiting ion regular

basis. There are mainly three type of Inventory management system such as LIFO, FIFO and

AVCO. LIFO define stock that is recently acquired is first used for operations. In FIFO process

the goods that are previously acquired products are used for producing goods (Englund and

Gerdin, 2018).

P3. Cost of product by using effective techniques.

CASE 1:

(a) Preparation of cost card:

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 9

Marginal cost 74

Selling price 150

Marginal cost 74

Contribution 76

(b) Profit and loss statement for month of January:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars DR CR

Sales revenue (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*9) 135000

Fixed production overhead 30000

Less : Closing stock (3000*74) 222000

Less: Cost of sales 918000

Profit 882000

Profit and loss statement for month of February:

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*9) 108000

Add : Opening stock (3000*74) 222000

Fixed production overhead 24000

Less- Closing stock (1000*74) 74000

Less: Cost of sales 1282000

Profit 818000

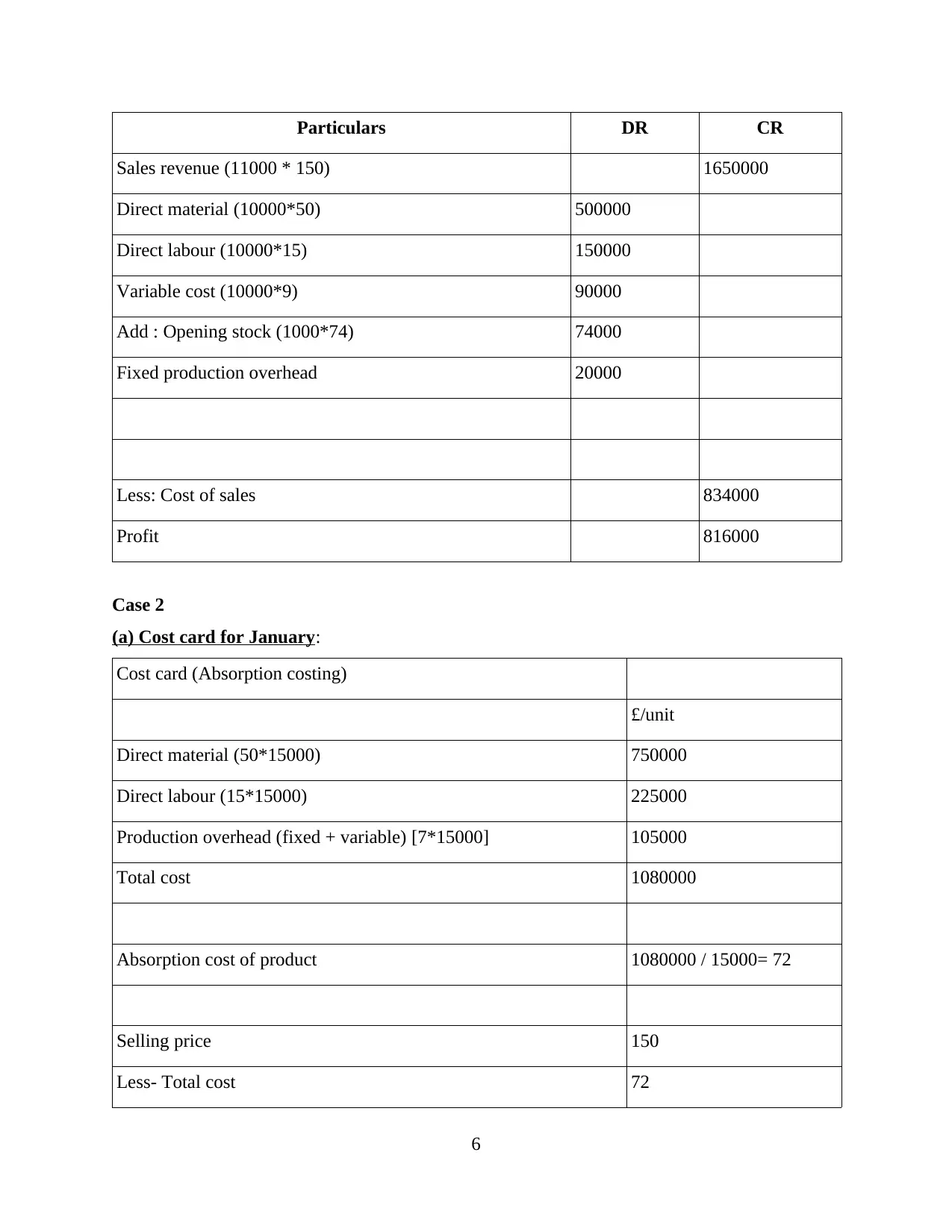

Profit and loss statement for month of March:

5

Sales revenue (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*9) 135000

Fixed production overhead 30000

Less : Closing stock (3000*74) 222000

Less: Cost of sales 918000

Profit 882000

Profit and loss statement for month of February:

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*9) 108000

Add : Opening stock (3000*74) 222000

Fixed production overhead 24000

Less- Closing stock (1000*74) 74000

Less: Cost of sales 1282000

Profit 818000

Profit and loss statement for month of March:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars DR CR

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*9) 90000

Add : Opening stock (1000*74) 74000

Fixed production overhead 20000

Less: Cost of sales 834000

Profit 816000

Case 2

(a) Cost card for January:

Cost card (Absorption costing)

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

Selling price 150

Less- Total cost 72

6

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*9) 90000

Add : Opening stock (1000*74) 74000

Fixed production overhead 20000

Less: Cost of sales 834000

Profit 816000

Case 2

(a) Cost card for January:

Cost card (Absorption costing)

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

Selling price 150

Less- Total cost 72

6

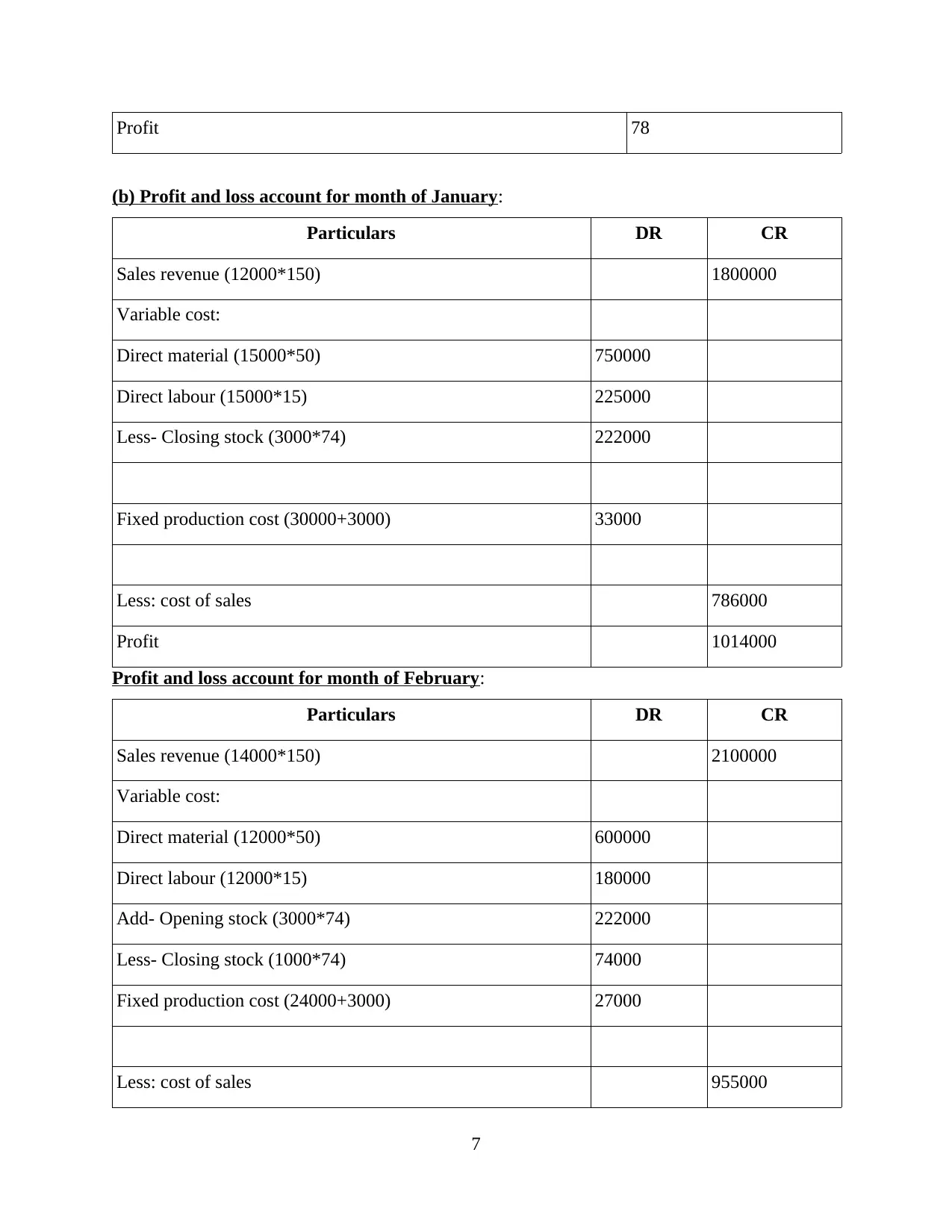

Profit 78

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Less- Closing stock (3000*74) 222000

Fixed production cost (30000+3000) 33000

Less: cost of sales 786000

Profit 1014000

Profit and loss account for month of February:

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*74) 222000

Less- Closing stock (1000*74) 74000

Fixed production cost (24000+3000) 27000

Less: cost of sales 955000

7

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Less- Closing stock (3000*74) 222000

Fixed production cost (30000+3000) 33000

Less: cost of sales 786000

Profit 1014000

Profit and loss account for month of February:

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*74) 222000

Less- Closing stock (1000*74) 74000

Fixed production cost (24000+3000) 27000

Less: cost of sales 955000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

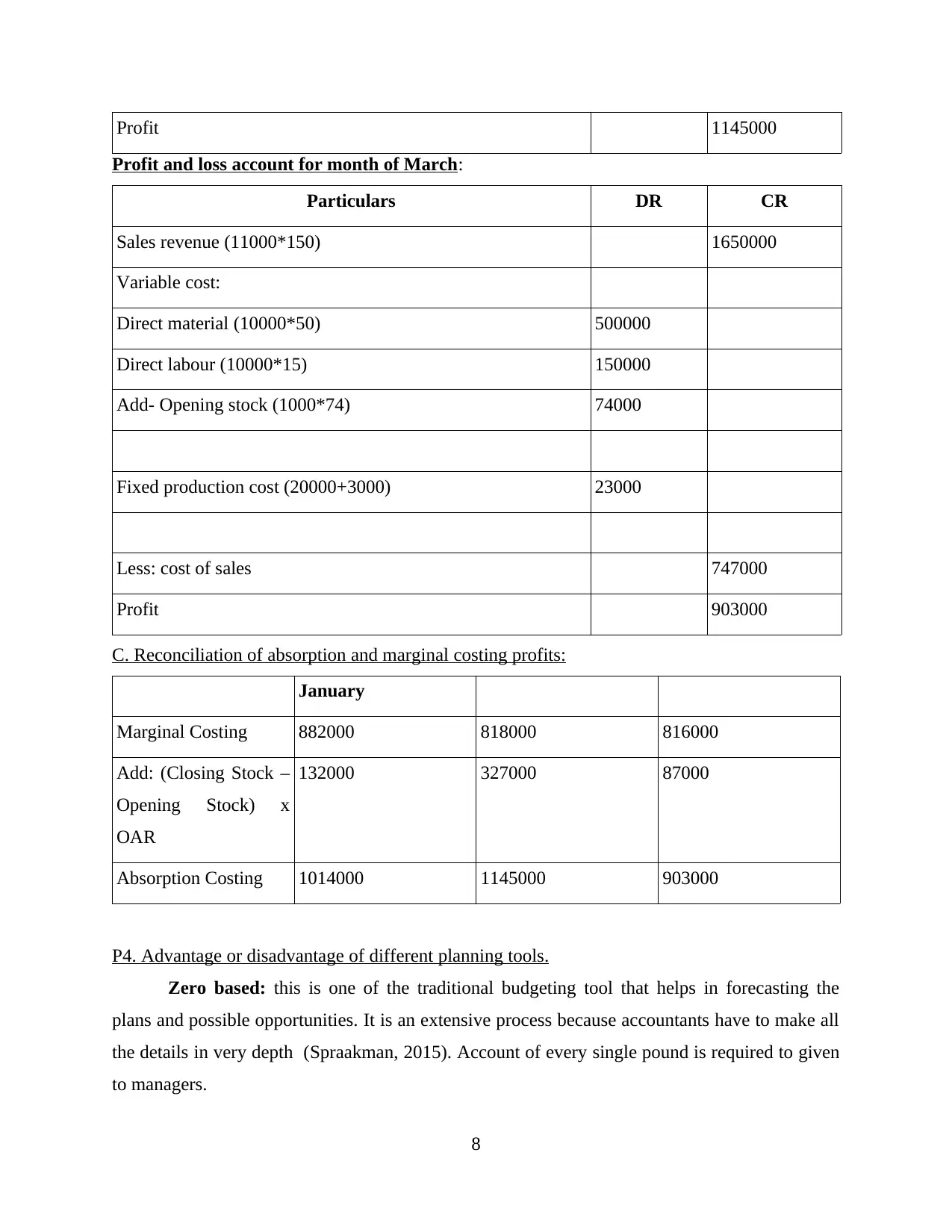

Profit 1145000

Profit and loss account for month of March:

Particulars DR CR

Sales revenue (11000*150) 1650000

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*74) 74000

Fixed production cost (20000+3000) 23000

Less: cost of sales 747000

Profit 903000

C. Reconciliation of absorption and marginal costing profits:

January

Marginal Costing 882000 818000 816000

Add: (Closing Stock –

Opening Stock) x

OAR

132000 327000 87000

Absorption Costing 1014000 1145000 903000

P4. Advantage or disadvantage of different planning tools.

Zero based: this is one of the traditional budgeting tool that helps in forecasting the

plans and possible opportunities. It is an extensive process because accountants have to make all

the details in very depth (Spraakman, 2015). Account of every single pound is required to given

to managers.

8

Profit and loss account for month of March:

Particulars DR CR

Sales revenue (11000*150) 1650000

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*74) 74000

Fixed production cost (20000+3000) 23000

Less: cost of sales 747000

Profit 903000

C. Reconciliation of absorption and marginal costing profits:

January

Marginal Costing 882000 818000 816000

Add: (Closing Stock –

Opening Stock) x

OAR

132000 327000 87000

Absorption Costing 1014000 1145000 903000

P4. Advantage or disadvantage of different planning tools.

Zero based: this is one of the traditional budgeting tool that helps in forecasting the

plans and possible opportunities. It is an extensive process because accountants have to make all

the details in very depth (Spraakman, 2015). Account of every single pound is required to given

to managers.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pros: the budget mainly assist the managers to understand the cost of plan in very detail.

The historical trends make the process of preparing budget more easy. The budgets always

remain centralized around cutting the excessive cost.

Cons: This budget forming process takes too much time and required large amount of

data to produce information in detail. Being a cost cutting nature it is not required that all the sub

departments will agree to reduce their departmental cost.

Cash budgets: This is one of the common budget formation tool that help in analyzing

the cash requirements with in operations. The process also helps in considering the changes and

variations with more strategic manner by making cash budget.

Pros: the debt cost can be controlled by compressing the interest expenses. The actual

results get in more strategic manner. The amount of non-cash items is considered in the cash

budget that can only be used in business.

Cons: Cash budget only remain centralized towards cash items and elements due to

which non cash elements remain avoided in budget (Sugahara, Daidj and Ushio, 2017).

Capital budget: this is one of the process that mainly determine that how much

investment is required in business for a particular time duration.

Pros: These budgets help in framing the budgets for large projects and plans. Capital

expenditures helps in fulfilling the long terms objectives of business.

Cons: These budgets do not forecast the revenue expenditures which is the main

drawback of capital budgets.

Operating budgets: This corresponds to the financial plan in which it allows the

corporation within a financial year to fulfil the different operation of the company. In respective

firm this budgets is beneficial to give stability in different operation and business activity

(Operating Budget, 2019).

Pros: It is useful in long-range preparation, where consumer prices are forecast and

budgets are handled to run business in profitable manner.

Cons: It is a static schedule that determines the results and it also takes time to collect

data and turn it into a comprehensible shape.

CASE 3:

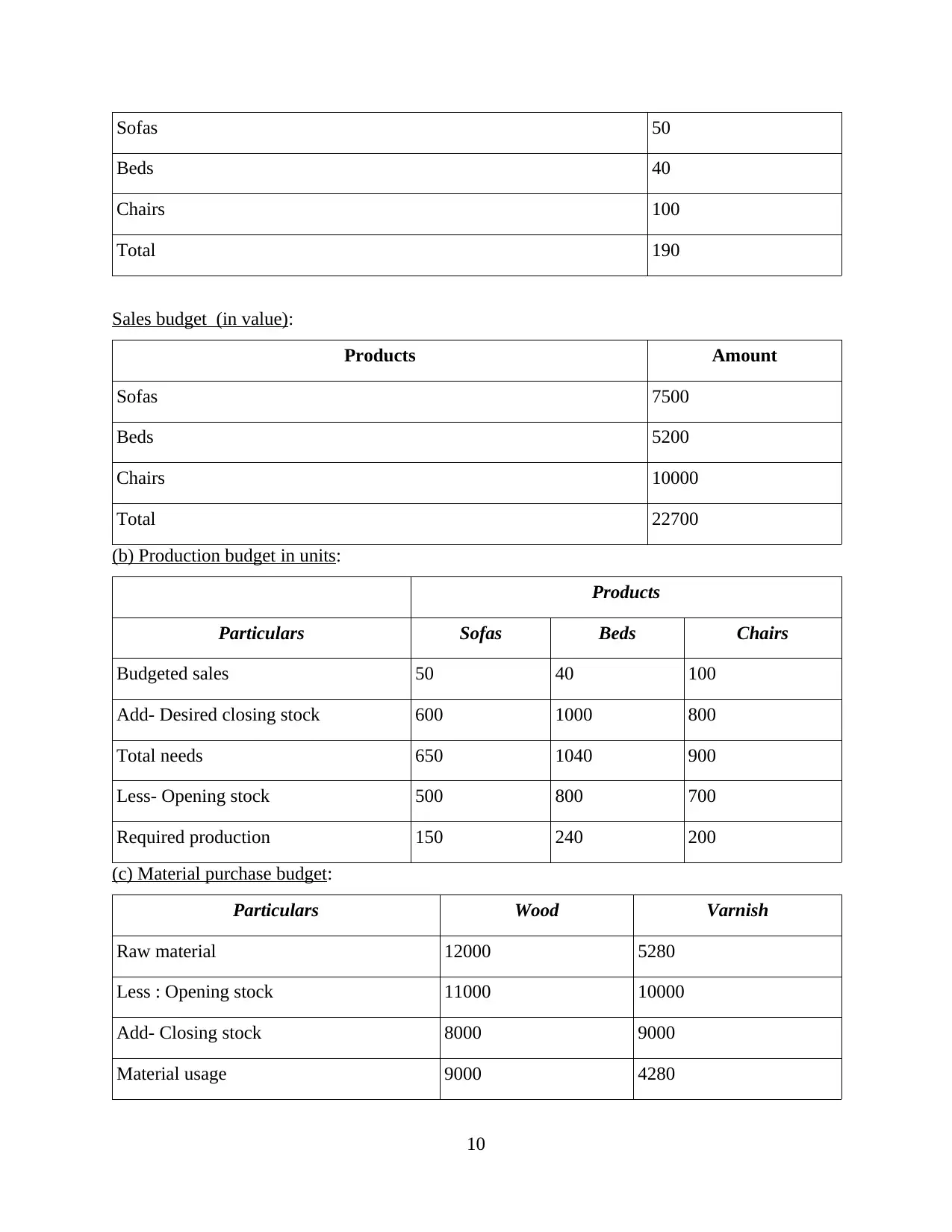

(a) Sales budget (in quantity):

Products Units

9

The historical trends make the process of preparing budget more easy. The budgets always

remain centralized around cutting the excessive cost.

Cons: This budget forming process takes too much time and required large amount of

data to produce information in detail. Being a cost cutting nature it is not required that all the sub

departments will agree to reduce their departmental cost.

Cash budgets: This is one of the common budget formation tool that help in analyzing

the cash requirements with in operations. The process also helps in considering the changes and

variations with more strategic manner by making cash budget.

Pros: the debt cost can be controlled by compressing the interest expenses. The actual

results get in more strategic manner. The amount of non-cash items is considered in the cash

budget that can only be used in business.

Cons: Cash budget only remain centralized towards cash items and elements due to

which non cash elements remain avoided in budget (Sugahara, Daidj and Ushio, 2017).

Capital budget: this is one of the process that mainly determine that how much

investment is required in business for a particular time duration.

Pros: These budgets help in framing the budgets for large projects and plans. Capital

expenditures helps in fulfilling the long terms objectives of business.

Cons: These budgets do not forecast the revenue expenditures which is the main

drawback of capital budgets.

Operating budgets: This corresponds to the financial plan in which it allows the

corporation within a financial year to fulfil the different operation of the company. In respective

firm this budgets is beneficial to give stability in different operation and business activity

(Operating Budget, 2019).

Pros: It is useful in long-range preparation, where consumer prices are forecast and

budgets are handled to run business in profitable manner.

Cons: It is a static schedule that determines the results and it also takes time to collect

data and turn it into a comprehensible shape.

CASE 3:

(a) Sales budget (in quantity):

Products Units

9

Sofas 50

Beds 40

Chairs 100

Total 190

Sales budget (in value):

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

Total 22700

(b) Production budget in units:

Products

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget:

Particulars Wood Varnish

Raw material 12000 5280

Less : Opening stock 11000 10000

Add- Closing stock 8000 9000

Material usage 9000 4280

10

Beds 40

Chairs 100

Total 190

Sales budget (in value):

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

Total 22700

(b) Production budget in units:

Products

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget:

Particulars Wood Varnish

Raw material 12000 5280

Less : Opening stock 11000 10000

Add- Closing stock 8000 9000

Material usage 9000 4280

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.