Management Accounting Report: Jeffrey and Son's Costing and Budgeting

VerifiedAdded on 2020/02/05

|23

|5966

|45

Report

AI Summary

This report delves into the principles of management accounting, specifically focusing on costing and budgeting techniques within the context of Jeffrey and Son's Ltd. It begins with an introduction to management accounting and its significance in business decision-making, emphasizing the importance of financial analysis. The report then explores various cost classifications, including material, labor, and overhead costs, along with different cost behaviors such as fixed, variable, and semi-variable costs. A job cost sheet is presented to determine the total and per-unit cost of a specific job. Furthermore, the report analyzes overhead allocation, calculating overhead absorption rates for different departments using both machine hour and labor hour methods. It also includes a variance analysis to compare budgeted and actual costs, offering insights into the financial performance of the company. The report concludes by highlighting the impact of different costing methods on the overall cost of the product and providing recommendations for Jeffrey and Son's Ltd.

Management Accounting :

Costing & Budgeting

Costing & Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................4

1.3...........................................................................................................................................5

1.4...........................................................................................................................................7

TASK 2............................................................................................................................................8

2.1...........................................................................................................................................8

2.2...........................................................................................................................................9

2.3.........................................................................................................................................10

TASK 3..........................................................................................................................................11

3.1.........................................................................................................................................11

3.2.........................................................................................................................................12

3.3.........................................................................................................................................12

3.4.........................................................................................................................................14

TASK 4..........................................................................................................................................16

4.1.........................................................................................................................................16

4.2.........................................................................................................................................18

4.3.........................................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................4

1.3...........................................................................................................................................5

1.4...........................................................................................................................................7

TASK 2............................................................................................................................................8

2.1...........................................................................................................................................8

2.2...........................................................................................................................................9

2.3.........................................................................................................................................10

TASK 3..........................................................................................................................................11

3.1.........................................................................................................................................11

3.2.........................................................................................................................................12

3.3.........................................................................................................................................12

3.4.........................................................................................................................................14

TASK 4..........................................................................................................................................16

4.1.........................................................................................................................................16

4.2.........................................................................................................................................18

4.3.........................................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Effective decision making is an essential part of business unit if an organization wants to

survive in competitive and continually changing environment. For getting profits sound

judgement, information regarding economic positioning, interpretation, analysis and evaluation

of financial resources are very important aspects. With the use of financial analysis techniques

managers can control the cost of operations and can plan the business activities which can

provide optimistic outcomes to entity (Dechow and Skinner, 2000). For the present report Jeffrey

and Son's Ltd is taken into account, it produces exquisite products. Current report will discuss

the various management tools like budgeting process, cost sheet which can be beneficial for the

enterprise. Purpose of the assignment is to determine importance of management accounting and

cost budgeting in context to Jeffrey and Son's Ltd. Various calculations will be illustrated for

achieving the aim of the report by following given scenario.

TASK 1

1.1

For getting positive results corporations sacrifice resource like for the production of any

electrical product company requires electricity, raw material etc. These are the necessary

expenses for the business unit called as cost of entity. There are various types of costs are

included in the enterprise are described below:

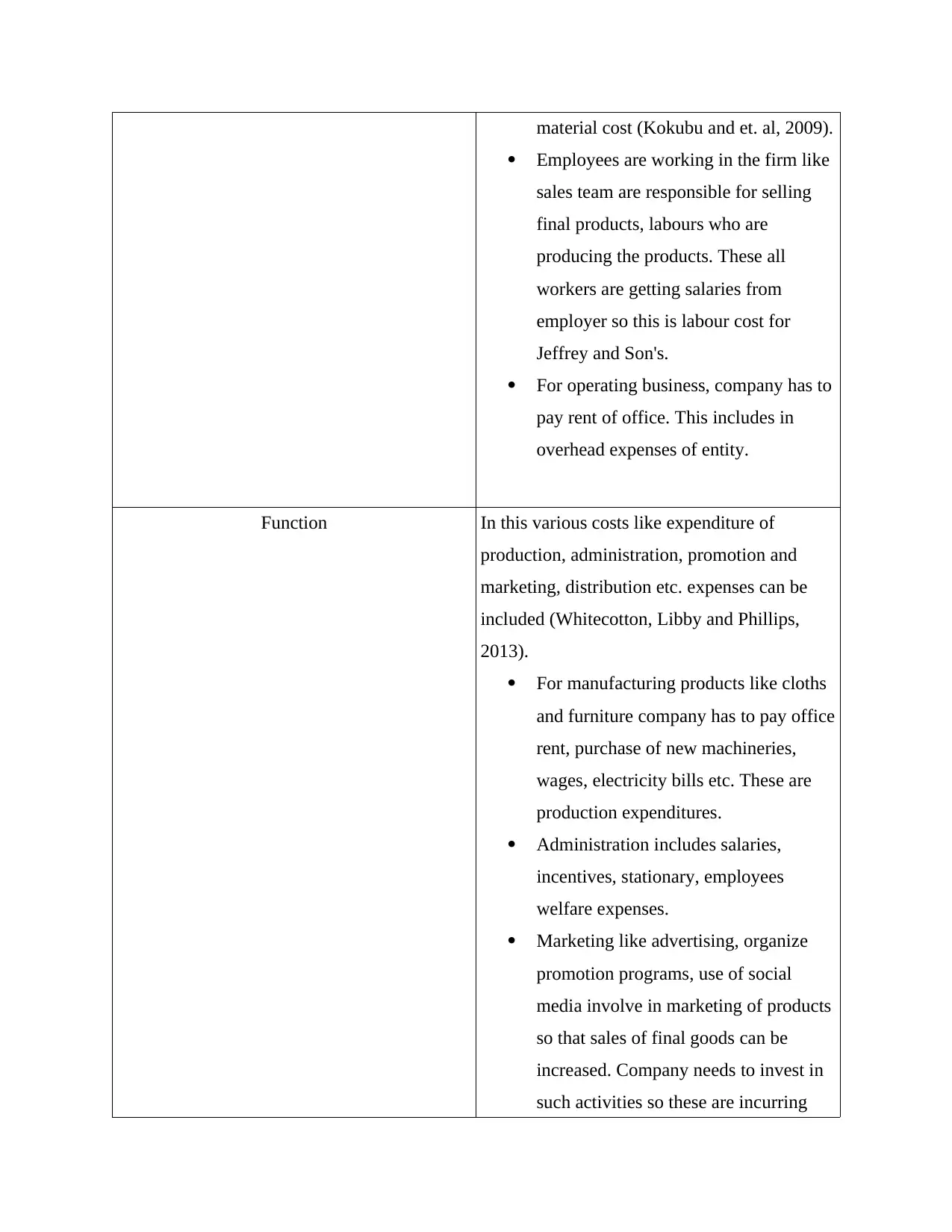

Categorization Type of costs

Elements Material, labour and overhead costs are

included in this element.

In Jeffrey and Son's Ltd material costs

are as raw substantial which are

necessary for producing final good and

services. Like for manufacturing of

furniture company requires timber, this

is the cost of material for the entity.

Enterprise requires to purchase fabrics

for manufacturing of cloths so this also

Effective decision making is an essential part of business unit if an organization wants to

survive in competitive and continually changing environment. For getting profits sound

judgement, information regarding economic positioning, interpretation, analysis and evaluation

of financial resources are very important aspects. With the use of financial analysis techniques

managers can control the cost of operations and can plan the business activities which can

provide optimistic outcomes to entity (Dechow and Skinner, 2000). For the present report Jeffrey

and Son's Ltd is taken into account, it produces exquisite products. Current report will discuss

the various management tools like budgeting process, cost sheet which can be beneficial for the

enterprise. Purpose of the assignment is to determine importance of management accounting and

cost budgeting in context to Jeffrey and Son's Ltd. Various calculations will be illustrated for

achieving the aim of the report by following given scenario.

TASK 1

1.1

For getting positive results corporations sacrifice resource like for the production of any

electrical product company requires electricity, raw material etc. These are the necessary

expenses for the business unit called as cost of entity. There are various types of costs are

included in the enterprise are described below:

Categorization Type of costs

Elements Material, labour and overhead costs are

included in this element.

In Jeffrey and Son's Ltd material costs

are as raw substantial which are

necessary for producing final good and

services. Like for manufacturing of

furniture company requires timber, this

is the cost of material for the entity.

Enterprise requires to purchase fabrics

for manufacturing of cloths so this also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

material cost (Kokubu and et. al, 2009).

Employees are working in the firm like

sales team are responsible for selling

final products, labours who are

producing the products. These all

workers are getting salaries from

employer so this is labour cost for

Jeffrey and Son's.

For operating business, company has to

pay rent of office. This includes in

overhead expenses of entity.

Function In this various costs like expenditure of

production, administration, promotion and

marketing, distribution etc. expenses can be

included (Whitecotton, Libby and Phillips,

2013).

For manufacturing products like cloths

and furniture company has to pay office

rent, purchase of new machineries,

wages, electricity bills etc. These are

production expenditures.

Administration includes salaries,

incentives, stationary, employees

welfare expenses.

Marketing like advertising, organize

promotion programs, use of social

media involve in marketing of products

so that sales of final goods can be

increased. Company needs to invest in

such activities so these are incurring

Employees are working in the firm like

sales team are responsible for selling

final products, labours who are

producing the products. These all

workers are getting salaries from

employer so this is labour cost for

Jeffrey and Son's.

For operating business, company has to

pay rent of office. This includes in

overhead expenses of entity.

Function In this various costs like expenditure of

production, administration, promotion and

marketing, distribution etc. expenses can be

included (Whitecotton, Libby and Phillips,

2013).

For manufacturing products like cloths

and furniture company has to pay office

rent, purchase of new machineries,

wages, electricity bills etc. These are

production expenditures.

Administration includes salaries,

incentives, stationary, employees

welfare expenses.

Marketing like advertising, organize

promotion programs, use of social

media involve in marketing of products

so that sales of final goods can be

increased. Company needs to invest in

such activities so these are incurring

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

high cost (Zimmerman and Yahya-

Zadeh, 2011).

Distribution expenditures like travelling

cost, shipment expenses etc.

Nature This includes direct and indirect costs.

Company has to purchase raw material, has to

pay wages to employees etc. are necessary and

direct expenses. Whereas some expenditure are

indirect, these can not be measured in amount

like labour hours, postage, printing, lighting

etc. So these are indirect costs of the

organization.

Behaviour In this area various fixed, variable and semi

variable costs are attached.

Some expenses are fixed and can not be

changed by changing conditions are

called as fixed expenses. Like company

has to pay building rent to owner of the

building, insurance is needed and can

not be ignored, depreciation of

machinery is fixed, salaries of peon and

watchmen are fixed (Adler, 2013).

Variable expenditures get changed

according to size of production. Like as

per the requirement of production

company purchase raw material and

hire employees according to workload

so related wages will be given by

Zadeh, 2011).

Distribution expenditures like travelling

cost, shipment expenses etc.

Nature This includes direct and indirect costs.

Company has to purchase raw material, has to

pay wages to employees etc. are necessary and

direct expenses. Whereas some expenditure are

indirect, these can not be measured in amount

like labour hours, postage, printing, lighting

etc. So these are indirect costs of the

organization.

Behaviour In this area various fixed, variable and semi

variable costs are attached.

Some expenses are fixed and can not be

changed by changing conditions are

called as fixed expenses. Like company

has to pay building rent to owner of the

building, insurance is needed and can

not be ignored, depreciation of

machinery is fixed, salaries of peon and

watchmen are fixed (Adler, 2013).

Variable expenditures get changed

according to size of production. Like as

per the requirement of production

company purchase raw material and

hire employees according to workload

so related wages will be given by

employer to workers.

Semi variable expenses are constant but

can get changed after certain point.

Like electricity expenses are fixed but it

can be higher when level of production

is high.

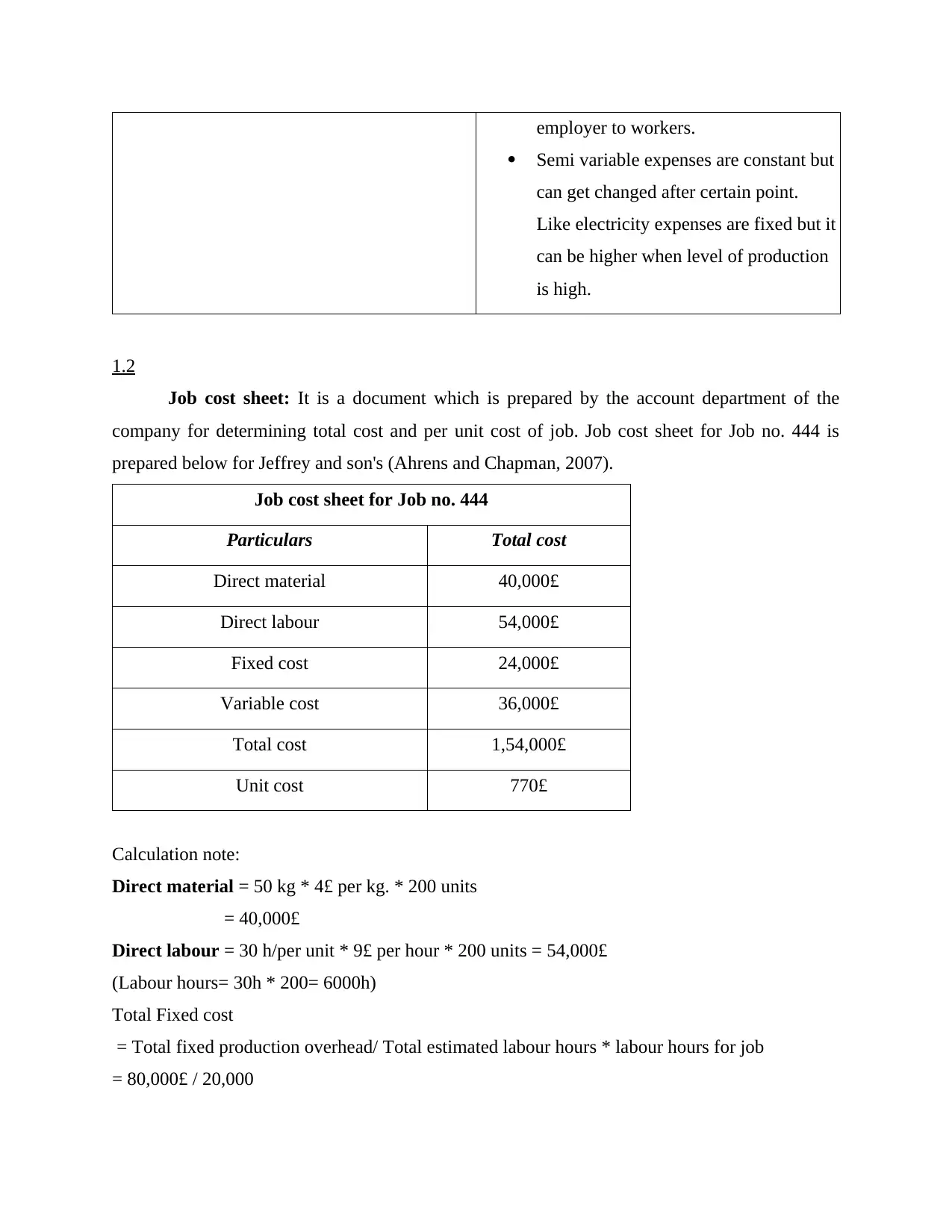

1.2

Job cost sheet: It is a document which is prepared by the account department of the

company for determining total cost and per unit cost of job. Job cost sheet for Job no. 444 is

prepared below for Jeffrey and son's (Ahrens and Chapman, 2007).

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40,000£

Direct labour 54,000£

Fixed cost 24,000£

Variable cost 36,000£

Total cost 1,54,000£

Unit cost 770£

Calculation note:

Direct material = 50 kg * 4£ per kg. * 200 units

= 40,000£

Direct labour = 30 h/per unit * 9£ per hour * 200 units = 54,000£

(Labour hours= 30h * 200= 6000h)

Total Fixed cost

= Total fixed production overhead/ Total estimated labour hours * labour hours for job

= 80,000£ / 20,000

Semi variable expenses are constant but

can get changed after certain point.

Like electricity expenses are fixed but it

can be higher when level of production

is high.

1.2

Job cost sheet: It is a document which is prepared by the account department of the

company for determining total cost and per unit cost of job. Job cost sheet for Job no. 444 is

prepared below for Jeffrey and son's (Ahrens and Chapman, 2007).

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40,000£

Direct labour 54,000£

Fixed cost 24,000£

Variable cost 36,000£

Total cost 1,54,000£

Unit cost 770£

Calculation note:

Direct material = 50 kg * 4£ per kg. * 200 units

= 40,000£

Direct labour = 30 h/per unit * 9£ per hour * 200 units = 54,000£

(Labour hours= 30h * 200= 6000h)

Total Fixed cost

= Total fixed production overhead/ Total estimated labour hours * labour hours for job

= 80,000£ / 20,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 4 £ * 6000 hours

= 24,000£

Total variable cost

= Labour hours for job * Direct labour hours

= 6000 hrs. * 6£ per hours

= 36,000£

Total cost

= direct material + Direct labour + Variable cost + Fixed cost

=40,000£ + 54,000£ + 36,000£ + 24,000£

= 1,54,000£

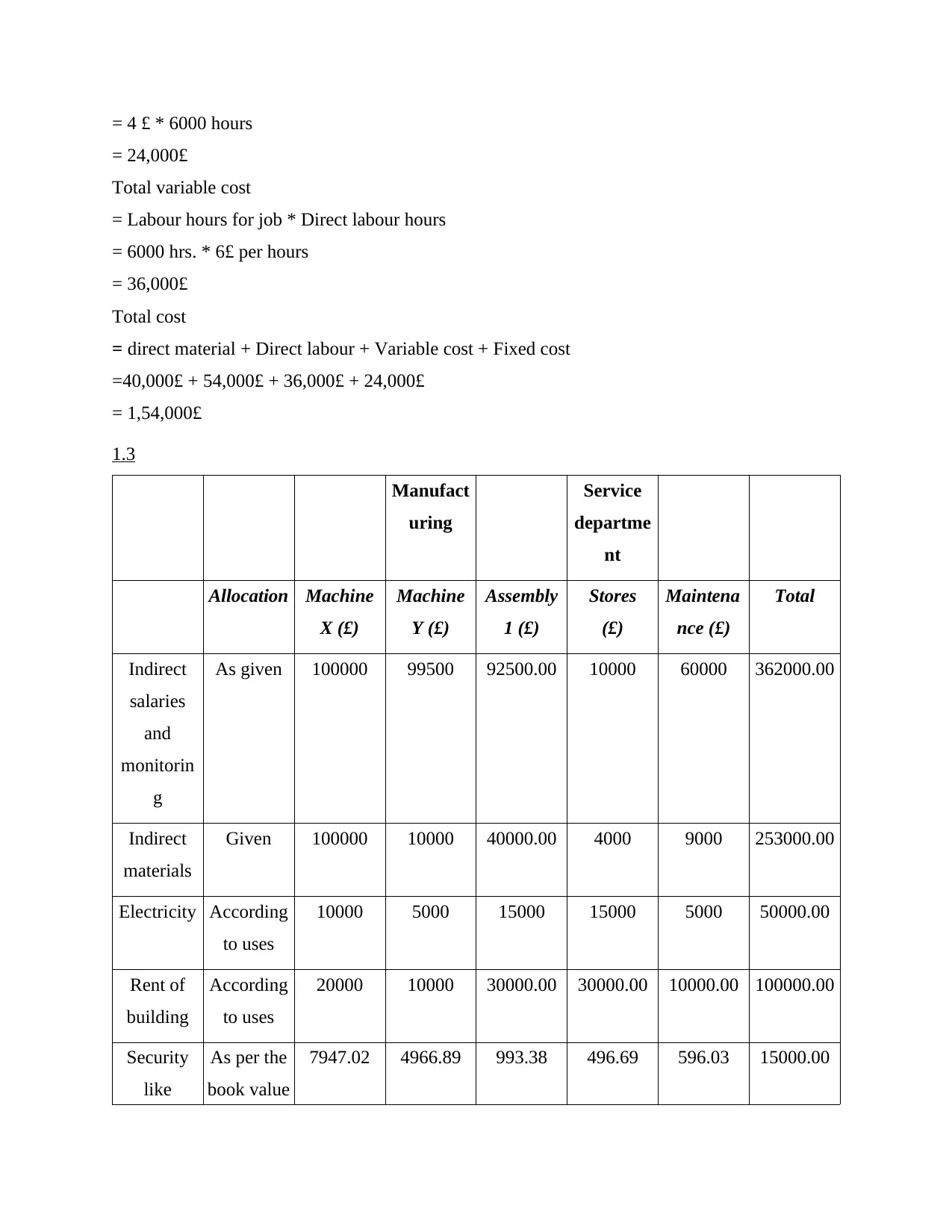

1.3

Manufact

uring

Service

departme

nt

Allocation Machine

X (£)

Machine

Y (£)

Assembly

1 (£)

Stores

(£)

Maintena

nce (£)

Total

Indirect

salaries

and

monitorin

g

As given 100000 99500 92500.00 10000 60000 362000.00

Indirect

materials

Given 100000 10000 40000.00 4000 9000 253000.00

Electricity According

to uses

10000 5000 15000 15000 5000 50000.00

Rent of

building

According

to uses

20000 10000 30000.00 30000.00 10000.00 100000.00

Security

like

As per the

book value

7947.02 4966.89 993.38 496.69 596.03 15000.00

= 24,000£

Total variable cost

= Labour hours for job * Direct labour hours

= 6000 hrs. * 6£ per hours

= 36,000£

Total cost

= direct material + Direct labour + Variable cost + Fixed cost

=40,000£ + 54,000£ + 36,000£ + 24,000£

= 1,54,000£

1.3

Manufact

uring

Service

departme

nt

Allocation Machine

X (£)

Machine

Y (£)

Assembly

1 (£)

Stores

(£)

Maintena

nce (£)

Total

Indirect

salaries

and

monitorin

g

As given 100000 99500 92500.00 10000 60000 362000.00

Indirect

materials

Given 100000 10000 40000.00 4000 9000 253000.00

Electricity According

to uses

10000 5000 15000 15000 5000 50000.00

Rent of

building

According

to uses

20000 10000 30000.00 30000.00 10000.00 100000.00

Security

like

As per the

book value

7947.02 4966.89 993.38 496.69 596.03 15000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

insurance

of

machinery

of

machine

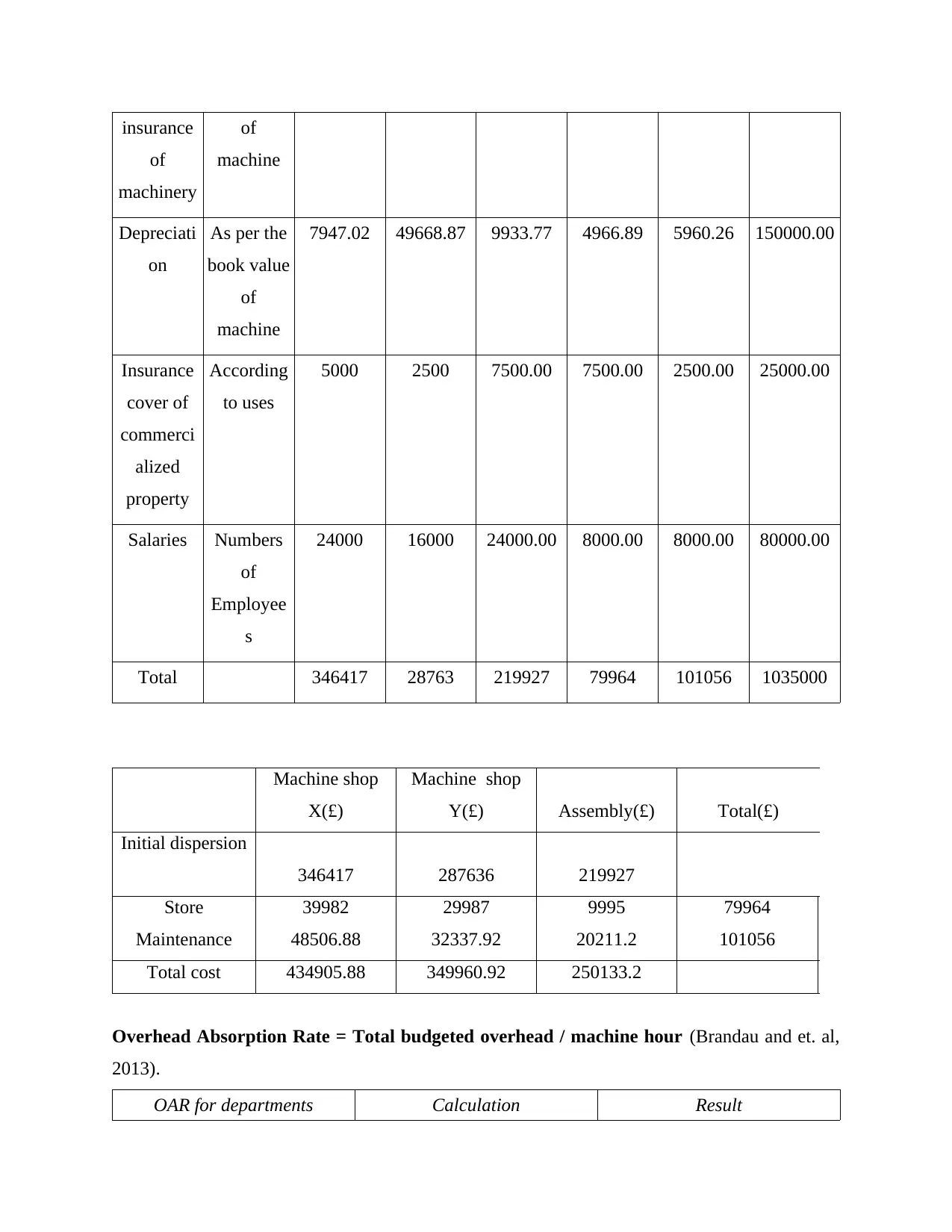

Depreciati

on

As per the

book value

of

machine

7947.02 49668.87 9933.77 4966.89 5960.26 150000.00

Insurance

cover of

commerci

alized

property

According

to uses

5000 2500 7500.00 7500.00 2500.00 25000.00

Salaries Numbers

of

Employee

s

24000 16000 24000.00 8000.00 8000.00 80000.00

Total 346417 28763 219927 79964 101056 1035000

Machine shop

X(£)

Machine shop

Y(£) Assembly(£) Total(£)

Initial dispersion

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

Overhead Absorption Rate = Total budgeted overhead / machine hour (Brandau and et. al,

2013).

OAR for departments Calculation Result

of

machinery

of

machine

Depreciati

on

As per the

book value

of

machine

7947.02 49668.87 9933.77 4966.89 5960.26 150000.00

Insurance

cover of

commerci

alized

property

According

to uses

5000 2500 7500.00 7500.00 2500.00 25000.00

Salaries Numbers

of

Employee

s

24000 16000 24000.00 8000.00 8000.00 80000.00

Total 346417 28763 219927 79964 101056 1035000

Machine shop

X(£)

Machine shop

Y(£) Assembly(£) Total(£)

Initial dispersion

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

Overhead Absorption Rate = Total budgeted overhead / machine hour (Brandau and et. al,

2013).

OAR for departments Calculation Result

Department X 434905.88£ /80000 5.44£

Department Y 349960.92£ /60000 £5.83

Department Assembly 250133.2£ /10000 £25.01

Total overhead cost = (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

4.35£ + 3.50£ + 2.50£ = 10.35£

Total cost = Material cost + labour cost + Overhead cost

= 8£ + 15£ + (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

= 33.35£

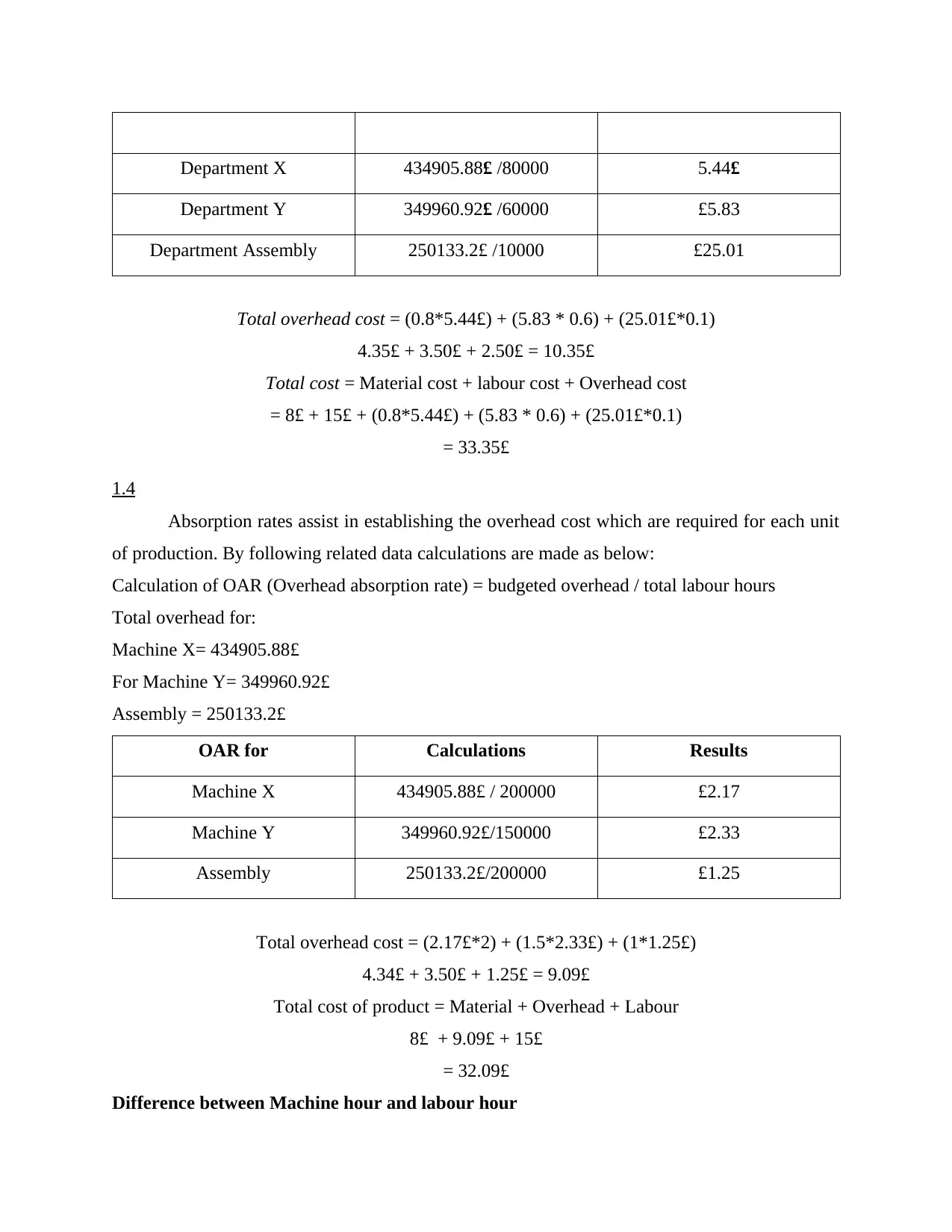

1.4

Absorption rates assist in establishing the overhead cost which are required for each unit

of production. By following related data calculations are made as below:

Calculation of OAR (Overhead absorption rate) = budgeted overhead / total labour hours

Total overhead for:

Machine X= 434905.88£

For Machine Y= 349960.92£

Assembly = 250133.2£

OAR for Calculations Results

Machine X 434905.88£ / 200000 £2.17

Machine Y 349960.92£/150000 £2.33

Assembly 250133.2£/200000 £1.25

Total overhead cost = (2.17£*2) + (1.5*2.33£) + (1*1.25£)

4.34£ + 3.50£ + 1.25£ = 9.09£

Total cost of product = Material + Overhead + Labour

8£ + 9.09£ + 15£

= 32.09£

Difference between Machine hour and labour hour

Department Y 349960.92£ /60000 £5.83

Department Assembly 250133.2£ /10000 £25.01

Total overhead cost = (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

4.35£ + 3.50£ + 2.50£ = 10.35£

Total cost = Material cost + labour cost + Overhead cost

= 8£ + 15£ + (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

= 33.35£

1.4

Absorption rates assist in establishing the overhead cost which are required for each unit

of production. By following related data calculations are made as below:

Calculation of OAR (Overhead absorption rate) = budgeted overhead / total labour hours

Total overhead for:

Machine X= 434905.88£

For Machine Y= 349960.92£

Assembly = 250133.2£

OAR for Calculations Results

Machine X 434905.88£ / 200000 £2.17

Machine Y 349960.92£/150000 £2.33

Assembly 250133.2£/200000 £1.25

Total overhead cost = (2.17£*2) + (1.5*2.33£) + (1*1.25£)

4.34£ + 3.50£ + 1.25£ = 9.09£

Total cost of product = Material + Overhead + Labour

8£ + 9.09£ + 15£

= 32.09£

Difference between Machine hour and labour hour

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above calculation it is found that by using machine hour the overhead cost for

machine X is 5.44£, for machine Y 5.83£ and for assembly is 25.01£. Whereas by using labour

hour apportion, overhead cost for machine X results 2.14£, for Y 2.3£ and for assembly results

1.25£. Total overhead cost of product under machine hour is 10.35£ whereas under labour hour

is 32.09£. So it is found that machine hour cost is higher than labour hour. Hence, cost of product

using labour hour method is comparatively low and get changed to 32.09£ from 33.35£. So it is

good apportionment for Jeffrey and Son's (House and Jackson, 2013).

TASK 2

2.1

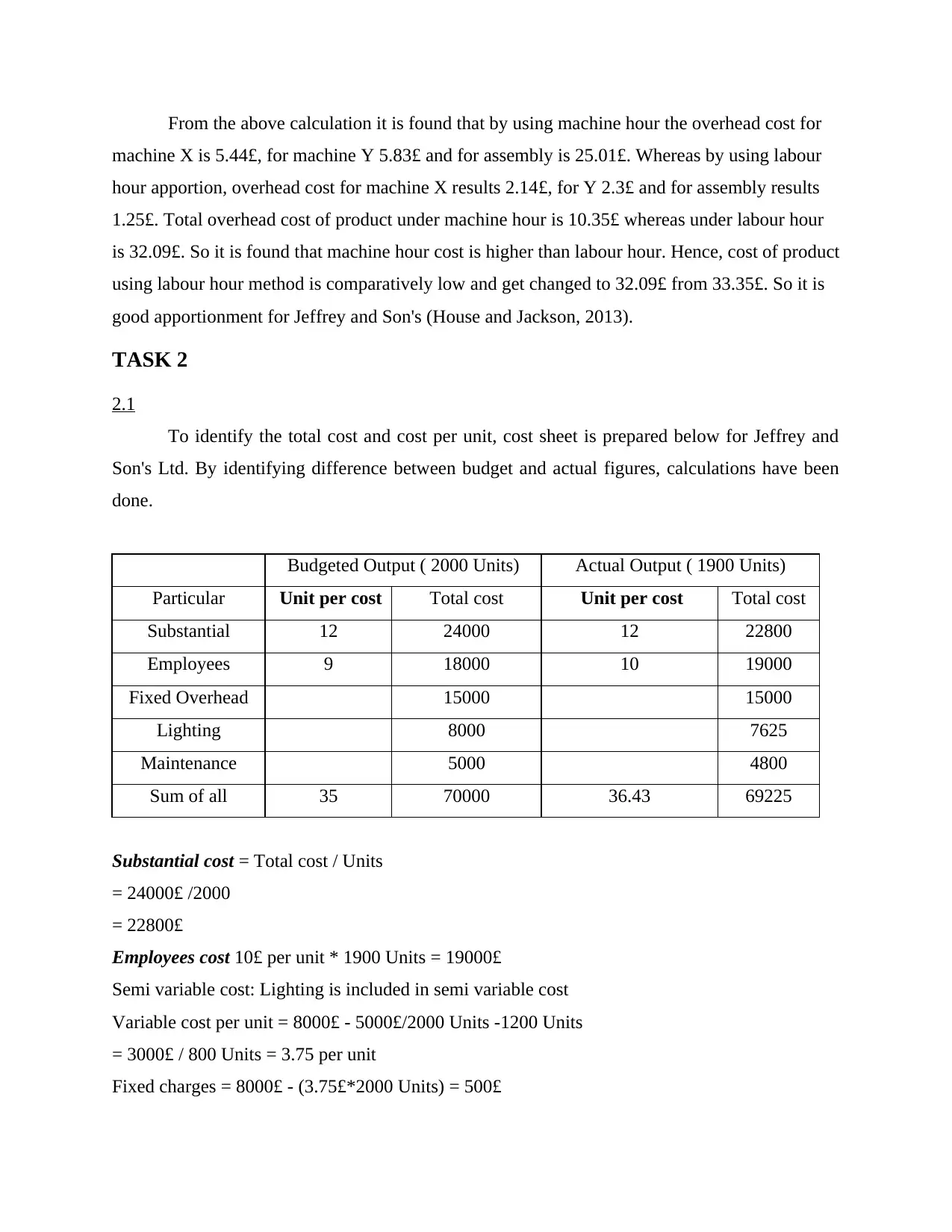

To identify the total cost and cost per unit, cost sheet is prepared below for Jeffrey and

Son's Ltd. By identifying difference between budget and actual figures, calculations have been

done.

Budgeted Output ( 2000 Units) Actual Output ( 1900 Units)

Particular Unit per cost Total cost Unit per cost Total cost

Substantial 12 24000 12 22800

Employees 9 18000 10 19000

Fixed Overhead 15000 15000

Lighting 8000 7625

Maintenance 5000 4800

Sum of all 35 70000 36.43 69225

Substantial cost = Total cost / Units

= 24000£ /2000

= 22800£

Employees cost 10£ per unit * 1900 Units = 19000£

Semi variable cost: Lighting is included in semi variable cost

Variable cost per unit = 8000£ - 5000£/2000 Units -1200 Units

= 3000£ / 800 Units = 3.75 per unit

Fixed charges = 8000£ - (3.75£*2000 Units) = 500£

machine X is 5.44£, for machine Y 5.83£ and for assembly is 25.01£. Whereas by using labour

hour apportion, overhead cost for machine X results 2.14£, for Y 2.3£ and for assembly results

1.25£. Total overhead cost of product under machine hour is 10.35£ whereas under labour hour

is 32.09£. So it is found that machine hour cost is higher than labour hour. Hence, cost of product

using labour hour method is comparatively low and get changed to 32.09£ from 33.35£. So it is

good apportionment for Jeffrey and Son's (House and Jackson, 2013).

TASK 2

2.1

To identify the total cost and cost per unit, cost sheet is prepared below for Jeffrey and

Son's Ltd. By identifying difference between budget and actual figures, calculations have been

done.

Budgeted Output ( 2000 Units) Actual Output ( 1900 Units)

Particular Unit per cost Total cost Unit per cost Total cost

Substantial 12 24000 12 22800

Employees 9 18000 10 19000

Fixed Overhead 15000 15000

Lighting 8000 7625

Maintenance 5000 4800

Sum of all 35 70000 36.43 69225

Substantial cost = Total cost / Units

= 24000£ /2000

= 22800£

Employees cost 10£ per unit * 1900 Units = 19000£

Semi variable cost: Lighting is included in semi variable cost

Variable cost per unit = 8000£ - 5000£/2000 Units -1200 Units

= 3000£ / 800 Units = 3.75 per unit

Fixed charges = 8000£ - (3.75£*2000 Units) = 500£

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable electricity charges = 3.75£*1900 Units

= 7125£

Total charges of lighting = 7125£ + 500£

= 7625£

Maintenance cost = 5000£ - (1000£/500 units*100 Units) = 4800£

Cost per unit = 69225£/1900 Units = 36.43£

Calculation of Variance analysis:

It concerns with the financial performance of deviations, by this calculation company

analysis difference between flexed standards and actual results (Kurichi and et. al, 2013).

Particular Budgeted cost Real cost Variance

Substantial 24000 22800 1200

Employees 18000 19000 -1000

Fixed Overhead 15000 15000 0

Lighting 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

Interpretation: Substantial variance indicates that Jeffrey and Son's Ltd. Actual cost is lower

than budgeted cost. So price variance of material is zero because it is same to 12£. Labour

variance shows that it is higher than budgeted cost. It increased due to the higher labour rate

which is 10£ per unit. As lighting budgeted cost was 8000 but it is getting declined to 7625. So

there is positive variance that is 375. Because of lower production maintenance rate get affected.

Budgeted cost of maintenance was 5000 but actual was 4800 so variance arises to 200£. As fixed

cost remains same therefore fixed cost variance also remains same under the output of 2000 and

1900 Units. Thus, it may be said that labour cost variance, labour rate and material cost variance

impact negatively on business unit. It reduces the profitability margin of the company to the

great extend. For making good profits Jeffrey and Son's has to search alternatives so that these

negative areas can be decreased and enterprise get high profit (Johnson, Pfeiffer and Schneider,

2013).

= 7125£

Total charges of lighting = 7125£ + 500£

= 7625£

Maintenance cost = 5000£ - (1000£/500 units*100 Units) = 4800£

Cost per unit = 69225£/1900 Units = 36.43£

Calculation of Variance analysis:

It concerns with the financial performance of deviations, by this calculation company

analysis difference between flexed standards and actual results (Kurichi and et. al, 2013).

Particular Budgeted cost Real cost Variance

Substantial 24000 22800 1200

Employees 18000 19000 -1000

Fixed Overhead 15000 15000 0

Lighting 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

Interpretation: Substantial variance indicates that Jeffrey and Son's Ltd. Actual cost is lower

than budgeted cost. So price variance of material is zero because it is same to 12£. Labour

variance shows that it is higher than budgeted cost. It increased due to the higher labour rate

which is 10£ per unit. As lighting budgeted cost was 8000 but it is getting declined to 7625. So

there is positive variance that is 375. Because of lower production maintenance rate get affected.

Budgeted cost of maintenance was 5000 but actual was 4800 so variance arises to 200£. As fixed

cost remains same therefore fixed cost variance also remains same under the output of 2000 and

1900 Units. Thus, it may be said that labour cost variance, labour rate and material cost variance

impact negatively on business unit. It reduces the profitability margin of the company to the

great extend. For making good profits Jeffrey and Son's has to search alternatives so that these

negative areas can be decreased and enterprise get high profit (Johnson, Pfeiffer and Schneider,

2013).

2.2

So many indicators used by the business entities for identifying the actual performance of

corporation. In context to Jeffrey and Son's, it uses various indicators, these are as below: Increasing sales: It is the important tool, by improving in sales and enhancing sales of

the products organizations can enhance its profit to great extend. It will affect the overall

revenue of company. For increasing sales of the entity, Jeffrey and Son's has to provide

quality good to consumers at affordable rates. By using several marketing techniques like

promotional activities, advertising, enterprise can achieve its target. Sales promotions and

after sales services can assist in increasing sales of the products. For providing quality

products, company has to adopt advanced technologies so that production may give

quality (Robbins and Simonsen, 2012). Financial statements: By preparing financial statements company can analysed the

performance of the enterprise. By this way accountant can analysis improving areas and

areas where cost can be minimized. By this way profit of the firm will get increased.

These records assist in knowing actual position of competitor. By comparing statements

with rivals enterprise can know sales and profit of respective entity. Customers feed back: By getting consumers feed backs company can identify the actual

point of view of service uses towards the business unit. Satisfy end users increases sales

of the firm. Delivery timing: It is an important tool, by reducing waiting time through delivering

products to consumers soon Jeffrey and Son's can enhance its performance and

profitability. Market share of Jeffrey and Son's: Market share of business unit assists in analysing

actual performance of the company.

Utilization of available resource: By utilizing resources effectively company can

increase its profits because by this way operation cost will be reduces. Thus, business will

earn high profits (Wyatt, 2012).

2.3

For achieving the business goal every organization require to reduce cost and to enhance

value of the company. For Jeffrey and Son's also it is important to look upon cost and quality for

getting positive results.

So many indicators used by the business entities for identifying the actual performance of

corporation. In context to Jeffrey and Son's, it uses various indicators, these are as below: Increasing sales: It is the important tool, by improving in sales and enhancing sales of

the products organizations can enhance its profit to great extend. It will affect the overall

revenue of company. For increasing sales of the entity, Jeffrey and Son's has to provide

quality good to consumers at affordable rates. By using several marketing techniques like

promotional activities, advertising, enterprise can achieve its target. Sales promotions and

after sales services can assist in increasing sales of the products. For providing quality

products, company has to adopt advanced technologies so that production may give

quality (Robbins and Simonsen, 2012). Financial statements: By preparing financial statements company can analysed the

performance of the enterprise. By this way accountant can analysis improving areas and

areas where cost can be minimized. By this way profit of the firm will get increased.

These records assist in knowing actual position of competitor. By comparing statements

with rivals enterprise can know sales and profit of respective entity. Customers feed back: By getting consumers feed backs company can identify the actual

point of view of service uses towards the business unit. Satisfy end users increases sales

of the firm. Delivery timing: It is an important tool, by reducing waiting time through delivering

products to consumers soon Jeffrey and Son's can enhance its performance and

profitability. Market share of Jeffrey and Son's: Market share of business unit assists in analysing

actual performance of the company.

Utilization of available resource: By utilizing resources effectively company can

increase its profits because by this way operation cost will be reduces. Thus, business will

earn high profits (Wyatt, 2012).

2.3

For achieving the business goal every organization require to reduce cost and to enhance

value of the company. For Jeffrey and Son's also it is important to look upon cost and quality for

getting positive results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.