Management Accounting Report: Functions, Systems, and Analysis

VerifiedAdded on 2020/07/22

|13

|4791

|153

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within Imda Tech Limited, an electronic sector company in the UK. The report begins by defining management accounting and differentiating it from financial accounting, emphasizing its role as a decision-making tool for department managers. It then explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimizing systems, detailing their functions and relevance. The report also includes an income statement prepared using marginal costing, discusses different budgeting methods, and analyzes pricing strategies. Finally, it examines the use of a balanced scorecard to measure business performance, offering a holistic view of the company's financial and operational aspects. The analysis aims to identify areas for improvement and provide strategic insights for Imda Tech Limited.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Function of MA......................................................................................................................3

1. Definition of management accounting and difference of it with financial accounting..........3

2. Importance of management accounting as a decision making tool for department managers 4

(b) Different management accounting systems and their use by other departments...................5

TASK 2............................................................................................................................................7

Income statement under the marginal costing method................................................................7

TASK 3............................................................................................................................................9

(a) Different budgets and their advantages as well as disadvantages .........................................9

(b) Process of preparing budget.................................................................................................10

(c) Pricing strategies..................................................................................................................11

TASK 4 .........................................................................................................................................12

(a) Management accounting systems and their use by firms ....................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Function of MA......................................................................................................................3

1. Definition of management accounting and difference of it with financial accounting..........3

2. Importance of management accounting as a decision making tool for department managers 4

(b) Different management accounting systems and their use by other departments...................5

TASK 2............................................................................................................................................7

Income statement under the marginal costing method................................................................7

TASK 3............................................................................................................................................9

(a) Different budgets and their advantages as well as disadvantages .........................................9

(b) Process of preparing budget.................................................................................................10

(c) Pricing strategies..................................................................................................................11

TASK 4 .........................................................................................................................................12

(a) Management accounting systems and their use by firms ....................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting (MA) is the discipline that is widely used by firms to improve

their performance. Under management accounting, there are number of tools used by firms to

identify the weak areas. In order to prepare the present report, Imda Tech Limited business entity

taken into account which operates in the electronic sector within UK. Proper strategy is used to

convert weak points into strong one. In the current report, different functions of management

accounting are explained. Along with this, varied management accounting systems are discussed

in detail. In the middle part of report, income statement is prepared by using marginal and

absorption costing methods. Apart from this, in the report, various budgets are explained and

their advantages disadvantages are discussed briefly. At the end of report, discussion about

balanced scorecard is to be done which one of the very important tool to measure business

performance of Imda Tech.

TASK 1

(a) Function of MA

1. Definition of management accounting and difference of it with financial accounting

Management accounting is one of the main domains that is used to do cost related

computations. There are number of methods of management accounting that are used to control

cost and to monitor the same. Over the past years, it has been observed that use of management

accounting is increasing at a rapid pace as it is very important to maintain a strict control over the

cost in business (Bellah and et. al., 2013). It is observed that in case of many firms, cost

increased to a great extent especially when economic condition of the nation is not good. Thus,

profit has declined but the cost increased. Due to this reason, most of the business firms are

laying down stress on costs that are incurred in business. Some of the methods that are usually

used in management accounting are budget and variance analysis. By using these methods, strict

monitoring of expenses is done in business and actions are taken on time to control the cost.

Variance analysis is another method under which whether expenses increased or decreased in

comparison to cost is identified. It can be said that there is significant importance of management

accounting methods for the business firms (Kaplan and Atkinson, 2015). There is difference

between management and financial accounting in number of ways. Management accounting

refers to the discipline that is used to perform cost related computations with respect to different

Management accounting (MA) is the discipline that is widely used by firms to improve

their performance. Under management accounting, there are number of tools used by firms to

identify the weak areas. In order to prepare the present report, Imda Tech Limited business entity

taken into account which operates in the electronic sector within UK. Proper strategy is used to

convert weak points into strong one. In the current report, different functions of management

accounting are explained. Along with this, varied management accounting systems are discussed

in detail. In the middle part of report, income statement is prepared by using marginal and

absorption costing methods. Apart from this, in the report, various budgets are explained and

their advantages disadvantages are discussed briefly. At the end of report, discussion about

balanced scorecard is to be done which one of the very important tool to measure business

performance of Imda Tech.

TASK 1

(a) Function of MA

1. Definition of management accounting and difference of it with financial accounting

Management accounting is one of the main domains that is used to do cost related

computations. There are number of methods of management accounting that are used to control

cost and to monitor the same. Over the past years, it has been observed that use of management

accounting is increasing at a rapid pace as it is very important to maintain a strict control over the

cost in business (Bellah and et. al., 2013). It is observed that in case of many firms, cost

increased to a great extent especially when economic condition of the nation is not good. Thus,

profit has declined but the cost increased. Due to this reason, most of the business firms are

laying down stress on costs that are incurred in business. Some of the methods that are usually

used in management accounting are budget and variance analysis. By using these methods, strict

monitoring of expenses is done in business and actions are taken on time to control the cost.

Variance analysis is another method under which whether expenses increased or decreased in

comparison to cost is identified. It can be said that there is significant importance of management

accounting methods for the business firms (Kaplan and Atkinson, 2015). There is difference

between management and financial accounting in number of ways. Management accounting

refers to the discipline that is used to perform cost related computations with respect to different

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses like direct, indirect and fixed. In the management accounting, varied calculations are

performed on available cost related data. On the other hand, in case of financial accounting,

different expenses are recorded with respect to its final value. It means that in case of

management accounting, all costs related calculations in terms of aggregate value of specific

expenses is done. On the contrary, in financial accounting, only value of expenses is taken into

account to compute profit or loss in business (Gesimba, Alvar and Mante, 2014). Thus, it can be

said that there is difference between the financial and management accounting in terms of their

use.

The other difference between financial and management accounting is that use of both

the tools of accounting are different from each other. In case of management accounting,

performance of the firm is measured solely in terms of cost but while in the financial accounting

it measured through cash flows, expense and profitability as well as assets and liability. It can be

said that there is difference between financial and management accounting in terms of area of

application.

Another difference between management and financial accounting is in terms of use by

the users. Management accounting is used only by the internal users like managers of

organization. Managers take into consideration cost related data in order to measure the

performance of business firm internally. On the other hand, in case of financial accounting both

internal and external stakeholders make use of accounting statements (Brigham. and Houston,

2011). Thus, it can be said that there is huge difference between financial and management

accounting in terms of use of accounting statements by different stakeholders.

2. Importance of management accounting as a decision making tool for department managers

Management accounting is one of the main tools that is used for decision making by

department managers. Under this, varied tools of management accounting are used by the

managers for decision making. Variance analysis is commonly used by the production manager

in order to identify the extent to which cost increased in business. Relevant tools are used to

identify whether expenses that are made in business are higher than determined range. Thus,

production department receives an input about the direction in which it needs to work. Cost

control strategy is formulated by production department on the basis of results of variance

analysis. Thus, it can be said that there is huge importance of decision making tools for the

managers of business firm. Management accounting tools are also used by the other department

performed on available cost related data. On the other hand, in case of financial accounting,

different expenses are recorded with respect to its final value. It means that in case of

management accounting, all costs related calculations in terms of aggregate value of specific

expenses is done. On the contrary, in financial accounting, only value of expenses is taken into

account to compute profit or loss in business (Gesimba, Alvar and Mante, 2014). Thus, it can be

said that there is difference between the financial and management accounting in terms of their

use.

The other difference between financial and management accounting is that use of both

the tools of accounting are different from each other. In case of management accounting,

performance of the firm is measured solely in terms of cost but while in the financial accounting

it measured through cash flows, expense and profitability as well as assets and liability. It can be

said that there is difference between financial and management accounting in terms of area of

application.

Another difference between management and financial accounting is in terms of use by

the users. Management accounting is used only by the internal users like managers of

organization. Managers take into consideration cost related data in order to measure the

performance of business firm internally. On the other hand, in case of financial accounting both

internal and external stakeholders make use of accounting statements (Brigham. and Houston,

2011). Thus, it can be said that there is huge difference between financial and management

accounting in terms of use of accounting statements by different stakeholders.

2. Importance of management accounting as a decision making tool for department managers

Management accounting is one of the main tools that is used for decision making by

department managers. Under this, varied tools of management accounting are used by the

managers for decision making. Variance analysis is commonly used by the production manager

in order to identify the extent to which cost increased in business. Relevant tools are used to

identify whether expenses that are made in business are higher than determined range. Thus,

production department receives an input about the direction in which it needs to work. Cost

control strategy is formulated by production department on the basis of results of variance

analysis. Thus, it can be said that there is huge importance of decision making tools for the

managers of business firm. Management accounting tools are also used by the other department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managers like marketing. This is because; in case of marketing department also, budget is

prepared with respect to expenses that have incurred with respect to marketing related

operations. Through management accounting tool, managers come to know about the extent to

which they make use of budgeted amount for marketing related operations (Malhotra and

Temponi, 2010). Thus, risk management strategy can be formulated in order to ensure that all

marketing related operations will be performed on time. It can be said that there is significant

importance of management accounting tools for the department managers. Similarly, by using

budget, HR managers come to know about the budgeted amount of employee’s cost that they are

ready to bear. Accordingly, HR manager selects an appropriate number of candidates on the job.

It can be said that there is high importance of management accounting tools for the

managers as same are used by different department managers to ensure that available resources

are used effectively in the business. Apart from this, by using key performance indicator method,

employee’s performance can be measured. Under this, expected performance of employees is

determined and same is compared with actual values in order to identify whether firm’s

employees perform effectual job at the workplace or not. It can be said that there is huge

importance of the management accounting tool for business firms as by using same, it can make

the best use of resources in business. Thus, managers must time to time make use of these tools

in order to manage business operations or functional operations in a proper manner.

(b) Different management accounting systems and their use by other departments

Management accounting systems are those under which all details related to transactions

are recorded in a specific format by the managers of business firm. In specific manner, data is

recorded in the books of accounts according to the management accounting systems. Varied

accounting systems that can be used by Imda tech limited are given as below. Cost accounting systems: Cost accounting system is one under which expenses of

specific category are segregated from each other. For example: variable expenses will be

computed separately and fixed expenses individually in respective accounting system

(Chapman Hopwood and Shields, 2011). Means that it does not matter that which kinds

of product lines are manufactured by the firm in the current time period. All variable

expenses will be summed up by the management accountant of Imda tech limited in order

to identify overall non fixed costs that are made by the business firm. Same thing is

applied in case of the other business firms. It can be said that cost accounting system is

prepared with respect to expenses that have incurred with respect to marketing related

operations. Through management accounting tool, managers come to know about the extent to

which they make use of budgeted amount for marketing related operations (Malhotra and

Temponi, 2010). Thus, risk management strategy can be formulated in order to ensure that all

marketing related operations will be performed on time. It can be said that there is significant

importance of management accounting tools for the department managers. Similarly, by using

budget, HR managers come to know about the budgeted amount of employee’s cost that they are

ready to bear. Accordingly, HR manager selects an appropriate number of candidates on the job.

It can be said that there is high importance of management accounting tools for the

managers as same are used by different department managers to ensure that available resources

are used effectively in the business. Apart from this, by using key performance indicator method,

employee’s performance can be measured. Under this, expected performance of employees is

determined and same is compared with actual values in order to identify whether firm’s

employees perform effectual job at the workplace or not. It can be said that there is huge

importance of the management accounting tool for business firms as by using same, it can make

the best use of resources in business. Thus, managers must time to time make use of these tools

in order to manage business operations or functional operations in a proper manner.

(b) Different management accounting systems and their use by other departments

Management accounting systems are those under which all details related to transactions

are recorded in a specific format by the managers of business firm. In specific manner, data is

recorded in the books of accounts according to the management accounting systems. Varied

accounting systems that can be used by Imda tech limited are given as below. Cost accounting systems: Cost accounting system is one under which expenses of

specific category are segregated from each other. For example: variable expenses will be

computed separately and fixed expenses individually in respective accounting system

(Chapman Hopwood and Shields, 2011). Means that it does not matter that which kinds

of product lines are manufactured by the firm in the current time period. All variable

expenses will be summed up by the management accountant of Imda tech limited in order

to identify overall non fixed costs that are made by the business firm. Same thing is

applied in case of the other business firms. It can be said that cost accounting system is

one of the most important systems. This is because; it gives an overall overview of the

specific sort of expenditure that is made by the firm in its business. It can be said that it

becomes very simple for the chartered accountant to include cost of goods sold in the

income statement as it does not need to add variable expenses of different products to

arrive at specific conclusion. It can be said that cost accounting system is used at wider

level by the business firms. Inventory management systems: Inventory management system is another approach of

management accounting under which all expenses related to stcok are recorded and added

to identify the overall cost of it that is incurred by the firm in the business. One of the

major significance of inventory management system is that by using same cost that is

incurred by different sort of inventories can be computed and added to compute overall

cost of inventory in the business. Inventory management system is used by all business

firms (Chandra, 2011). This is because; each of them has to keep their inventory

separately and there must be information about the amount of inventory that is

specifically at the warehouse. It can be said that by using inventory management system

that company has how much level of stock within an accounting period. Along with this,

changes which are made in the value of stock are also assessed properly over the

financial years. Apart from this, inventory management system also provides firm’s

information about the cost that is associated with storage of different stock. Thus, cost

related decisions are taken by the managers with respect to storage of inventory on the

basis of inventory management system. Job costing systems: Job order costing system is used at a wide level by the business

firms. This is because; under this system, for different product lines, costing is done

separately by the business firm. Under job order costing system, firm produces different

products on the basis of order received from customers. In the mentioned accounting

system, separate costing of each product is done (McKevitt. and Davis, 2013). In this

regard, separate data is gathered for each product line by the management accountant. It

can be said that there are multiple advantages of using mentioned management

accounting systems for the business firms. This is because; it helps the firm in

maintaining records of different orders separately. Relevant data can be used by the cost

accountants for making business decisions. On the basis of past data, prediction can be

specific sort of expenditure that is made by the firm in its business. It can be said that it

becomes very simple for the chartered accountant to include cost of goods sold in the

income statement as it does not need to add variable expenses of different products to

arrive at specific conclusion. It can be said that cost accounting system is used at wider

level by the business firms. Inventory management systems: Inventory management system is another approach of

management accounting under which all expenses related to stcok are recorded and added

to identify the overall cost of it that is incurred by the firm in the business. One of the

major significance of inventory management system is that by using same cost that is

incurred by different sort of inventories can be computed and added to compute overall

cost of inventory in the business. Inventory management system is used by all business

firms (Chandra, 2011). This is because; each of them has to keep their inventory

separately and there must be information about the amount of inventory that is

specifically at the warehouse. It can be said that by using inventory management system

that company has how much level of stock within an accounting period. Along with this,

changes which are made in the value of stock are also assessed properly over the

financial years. Apart from this, inventory management system also provides firm’s

information about the cost that is associated with storage of different stock. Thus, cost

related decisions are taken by the managers with respect to storage of inventory on the

basis of inventory management system. Job costing systems: Job order costing system is used at a wide level by the business

firms. This is because; under this system, for different product lines, costing is done

separately by the business firm. Under job order costing system, firm produces different

products on the basis of order received from customers. In the mentioned accounting

system, separate costing of each product is done (McKevitt. and Davis, 2013). In this

regard, separate data is gathered for each product line by the management accountant. It

can be said that there are multiple advantages of using mentioned management

accounting systems for the business firms. This is because; it helps the firm in

maintaining records of different orders separately. Relevant data can be used by the cost

accountants for making business decisions. On the basis of past data, prediction can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

made about the future and according to change in environment, adjustments can be made

in the decision. It can be said that there is significant importance of the job order costing

for managers.

Price optimizing systems: It is one of the important information systems and in this, price

of different products is identified and number of customers that make purchase at specific

price level are find out. Price level at which most of the customers make purchase is

identified and it is declared as the final sales price by firm. Under price optimizing

system, data related to cost of different product categories is identified. On the basis of

analysis of data, it is identified that whether cost can be reduced or not.

TASK 2

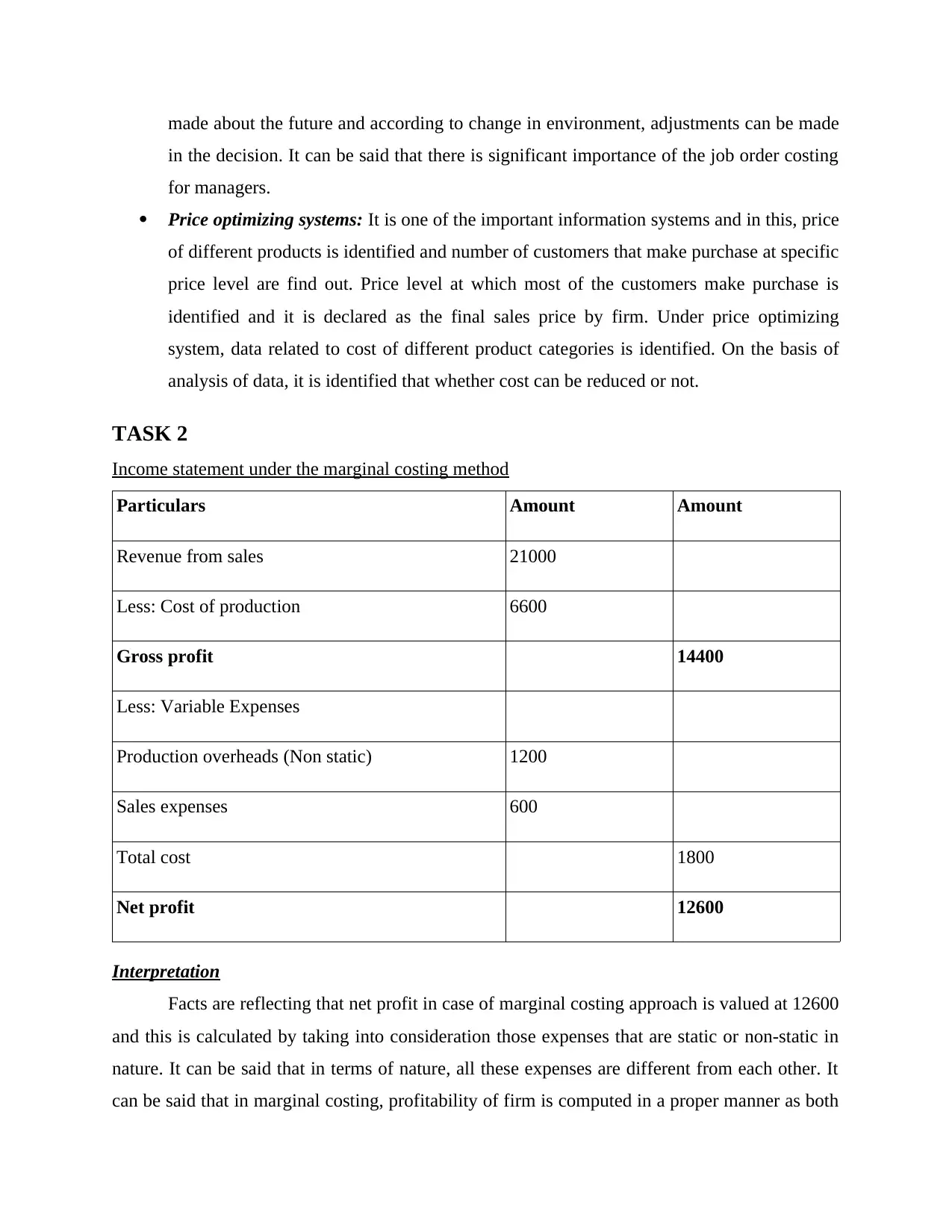

Income statement under the marginal costing method

Particulars Amount Amount

Revenue from sales 21000

Less: Cost of production 6600

Gross profit 14400

Less: Variable Expenses

Production overheads (Non static) 1200

Sales expenses 600

Total cost 1800

Net profit 12600

Interpretation

Facts are reflecting that net profit in case of marginal costing approach is valued at 12600

and this is calculated by taking into consideration those expenses that are static or non-static in

nature. It can be said that in terms of nature, all these expenses are different from each other. It

can be said that in marginal costing, profitability of firm is computed in a proper manner as both

in the decision. It can be said that there is significant importance of the job order costing

for managers.

Price optimizing systems: It is one of the important information systems and in this, price

of different products is identified and number of customers that make purchase at specific

price level are find out. Price level at which most of the customers make purchase is

identified and it is declared as the final sales price by firm. Under price optimizing

system, data related to cost of different product categories is identified. On the basis of

analysis of data, it is identified that whether cost can be reduced or not.

TASK 2

Income statement under the marginal costing method

Particulars Amount Amount

Revenue from sales 21000

Less: Cost of production 6600

Gross profit 14400

Less: Variable Expenses

Production overheads (Non static) 1200

Sales expenses 600

Total cost 1800

Net profit 12600

Interpretation

Facts are reflecting that net profit in case of marginal costing approach is valued at 12600

and this is calculated by taking into consideration those expenses that are static or non-static in

nature. It can be said that in terms of nature, all these expenses are different from each other. It

can be said that in marginal costing, profitability of firm is computed in a proper manner as both

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

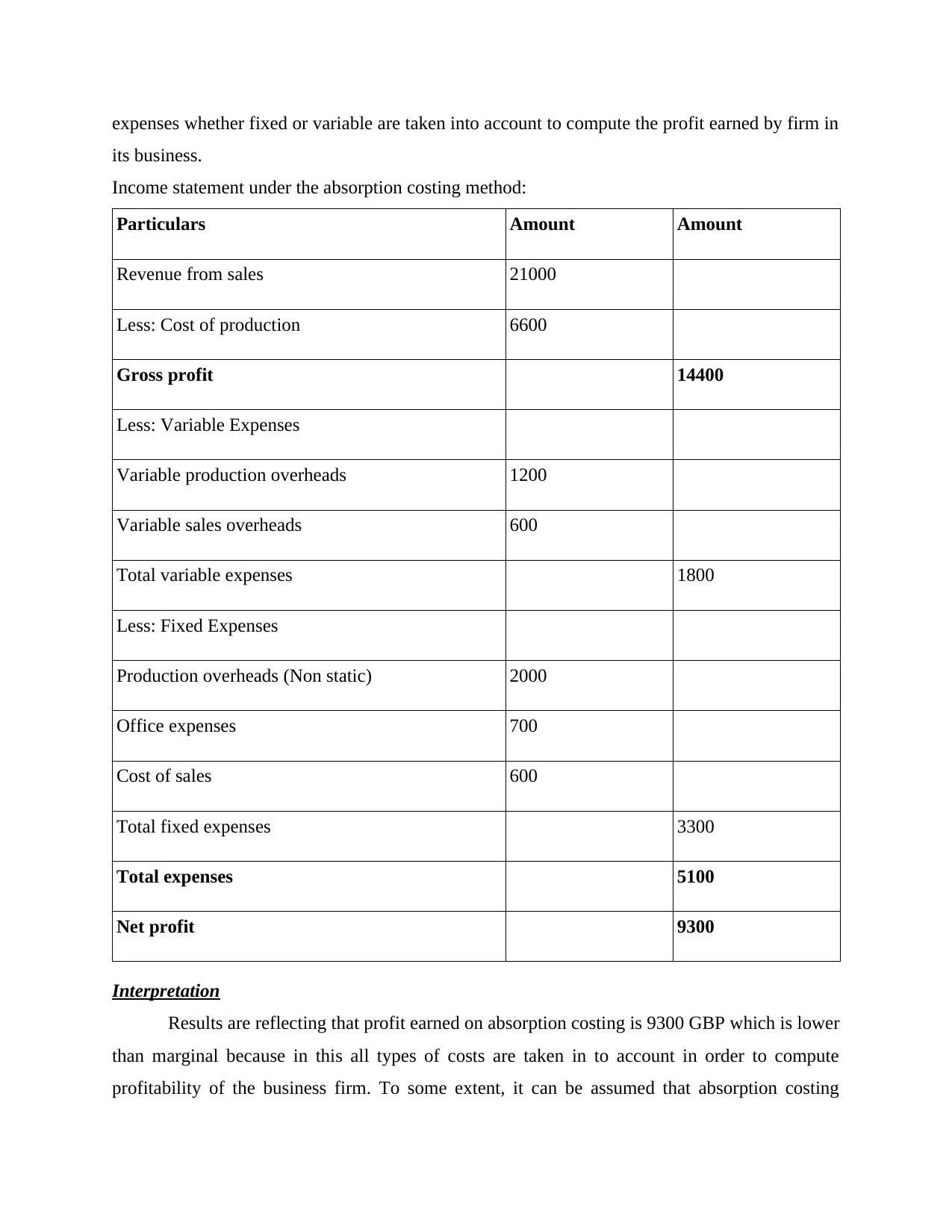

expenses whether fixed or variable are taken into account to compute the profit earned by firm in

its business.

Income statement under the absorption costing method:

Particulars Amount Amount

Revenue from sales 21000

Less: Cost of production 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overheads (Non static) 2000

Office expenses 700

Cost of sales 600

Total fixed expenses 3300

Total expenses 5100

Net profit 9300

Interpretation

Results are reflecting that profit earned on absorption costing is 9300 GBP which is lower

than marginal because in this all types of costs are taken in to account in order to compute

profitability of the business firm. To some extent, it can be assumed that absorption costing

its business.

Income statement under the absorption costing method:

Particulars Amount Amount

Revenue from sales 21000

Less: Cost of production 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overheads (Non static) 2000

Office expenses 700

Cost of sales 600

Total fixed expenses 3300

Total expenses 5100

Net profit 9300

Interpretation

Results are reflecting that profit earned on absorption costing is 9300 GBP which is lower

than marginal because in this all types of costs are taken in to account in order to compute

profitability of the business firm. To some extent, it can be assumed that absorption costing

method gives better overview of the profitability position of Imda Tech company.. It can be said

that there is huge importance of both marginal and absorption costing method for the business

firms.

TASK 3

(a) Different budgets and their advantages as well as disadvantages

Budget refers to the statement under which projections are made by the business firm

with respect to expenses and income for specific duration. Actual values which are generated by

firm are compared with the standard value and on that basis, firm’s performance is accessed

(Hult, Craighead and Ketchen Jr, 2010). In case it is identified that performance is not excellent

then strict action is taken on time to control the situation. Different budgets that are prepared by

the business firm are given as below along with their advantages and disadvantages:

Fixed budget

Fixed budget is one under which values of all variables is kept constant and does not

change with passage of time period. This means that even if business conditions are changed, no

alteration will be made to the values of budget variables. There are number of advantages and

disadvantages of fixed budget for the business firms and same are given as below.

Advantages of fixed budget

One of the main advantages of fixed budget is that under the same, values of all variables

is kept as fixed. Thus, same budget is used by the business firm and this leads to save a

lot of time of the business firm. Managers do not need to do brainstorming on work

through which their time saved and they able to become more productive. It can be said

that there is significant importance of the fixed budget for business firms. Other main advantage of fixed budget is that in case business environment get changed

then due to fluctuation, they does not need to change the budget frequently (Shelby,

2013). This is because; in the fixed budget, all values are fixed and does not change.

Disadvantages of fixed budget

One of the main disadvantages of fixed budget is that in this, values are kept to be

constant. With change in business environment, conditions get changed sharply. Firm that

prepares or follows fixed budget makes all decisions by considering the fixed values

irrespective of changes that are taking place in business environment. Hence, sometimes,

that there is huge importance of both marginal and absorption costing method for the business

firms.

TASK 3

(a) Different budgets and their advantages as well as disadvantages

Budget refers to the statement under which projections are made by the business firm

with respect to expenses and income for specific duration. Actual values which are generated by

firm are compared with the standard value and on that basis, firm’s performance is accessed

(Hult, Craighead and Ketchen Jr, 2010). In case it is identified that performance is not excellent

then strict action is taken on time to control the situation. Different budgets that are prepared by

the business firm are given as below along with their advantages and disadvantages:

Fixed budget

Fixed budget is one under which values of all variables is kept constant and does not

change with passage of time period. This means that even if business conditions are changed, no

alteration will be made to the values of budget variables. There are number of advantages and

disadvantages of fixed budget for the business firms and same are given as below.

Advantages of fixed budget

One of the main advantages of fixed budget is that under the same, values of all variables

is kept as fixed. Thus, same budget is used by the business firm and this leads to save a

lot of time of the business firm. Managers do not need to do brainstorming on work

through which their time saved and they able to become more productive. It can be said

that there is significant importance of the fixed budget for business firms. Other main advantage of fixed budget is that in case business environment get changed

then due to fluctuation, they does not need to change the budget frequently (Shelby,

2013). This is because; in the fixed budget, all values are fixed and does not change.

Disadvantages of fixed budget

One of the main disadvantages of fixed budget is that in this, values are kept to be

constant. With change in business environment, conditions get changed sharply. Firm that

prepares or follows fixed budget makes all decisions by considering the fixed values

irrespective of changes that are taking place in business environment. Hence, sometimes,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business firm makes decisions in wrong directions. This leads to heavy elevation in cost

of the business and thus, there is sharp decline in the profit of business.

Disadvantage of the fixed budget is that it is possible same values in terms of percentage

are considered over the many periods. If same will happen then in that case, every time

wrong decisions will be made by the managers (Swayne, Duncan and Ginter, 2012).

Along with this, appropriate decisions to generate profit and make expenses are not taken

bt the managers.

Flexible budget

Flexible budget is the one whose values keep on changing consistently because in this

values are not remain constant. With change in the business environment, values of budget also

get changed at a rapid pace. Advantages and disadvantages of flexible budget are given as below.

Advantages Main advantage of flexible budget is that with change in business conditions, values are

changed. Hence, according to change in situation, decisions are made by the business

firms.Other main advantage of flexible budget is that the best use of resources is made by

business firm in every situation. It can be said that there is significant importance of the

flexible budget for business firm.

Disadvantages

Main disadvantage of flexible budget is that changes are made in the values of elements

of budget according to estimation (Talke, Salomo and Rost, 2010). In case if one makes

wrong estimation then budget will be prepared in a wrong manner. Hence, it can be stated

that wrong decisions can be made on the basis of flexible budget.

(b) Process of preparing budget Updating budget assumptions: In this stage, budget assumptions are changed according

to expectations that management has about changes that can be observed with respect to

business environment. Available funding: In this stage, funding is made available and those who prepare budget

obtain an information about fund that is required in the business. Creating budget package: after receipt of the funds entire budget package is prepared

and under this it is determined that how much amount of fund will be available to the

business firm?

of the business and thus, there is sharp decline in the profit of business.

Disadvantage of the fixed budget is that it is possible same values in terms of percentage

are considered over the many periods. If same will happen then in that case, every time

wrong decisions will be made by the managers (Swayne, Duncan and Ginter, 2012).

Along with this, appropriate decisions to generate profit and make expenses are not taken

bt the managers.

Flexible budget

Flexible budget is the one whose values keep on changing consistently because in this

values are not remain constant. With change in the business environment, values of budget also

get changed at a rapid pace. Advantages and disadvantages of flexible budget are given as below.

Advantages Main advantage of flexible budget is that with change in business conditions, values are

changed. Hence, according to change in situation, decisions are made by the business

firms.Other main advantage of flexible budget is that the best use of resources is made by

business firm in every situation. It can be said that there is significant importance of the

flexible budget for business firm.

Disadvantages

Main disadvantage of flexible budget is that changes are made in the values of elements

of budget according to estimation (Talke, Salomo and Rost, 2010). In case if one makes

wrong estimation then budget will be prepared in a wrong manner. Hence, it can be stated

that wrong decisions can be made on the basis of flexible budget.

(b) Process of preparing budget Updating budget assumptions: In this stage, budget assumptions are changed according

to expectations that management has about changes that can be observed with respect to

business environment. Available funding: In this stage, funding is made available and those who prepare budget

obtain an information about fund that is required in the business. Creating budget package: after receipt of the funds entire budget package is prepared

and under this it is determined that how much amount of fund will be available to the

business firm?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue forecast: In this stage, forecast of revenue is done by the business firm by

considering future business environment and its growth strategies. Advises and

comments are received from other important internal stakeholders to ensure that forecsted

values are proper or not (Cash Budget. 2016). Receiving capital budget forecast: After forecast of revenue from different departments,

capital budget requirements are received and same is taken into consideration by the

project manager. Allocation of funds: In this stage, allocation of funds is done across different

departments in order to ensure that needs of all of them will be fulfilled in a proper

manner.

Updating budget: After allocation of budget across departments, same is updated

according to decisions that are taken by the top management.

(c) Pricing strategies

There are number of pricing strategies that can be followed by the business firms and

some of them are given as below. Skimming price strategy: It is the pricing strategy that is followed by the business firm

and under this, product is sold at higher price relative to other firms. This strategy is

followed when firm launches innovative product in the market. Penetration price strategy: Penetration pricing strategy is one under which product is

sold at a low price in the market. By doing so, firm tries to capture the market at a rapid

rate. This kind of strategy is used by most of the firms because it supports to increase

market share in the industry. Competition based pricing: Competition based pricing is one under which firm takes into

consideration the price that is determined by rival firms (Shelby, 2013). By considering

such price, product pricing is done. Moreover, within the market if rivals charge 50 GBP

price of the every mobile charger then selected firm will take pricing decisions lower than

50 GBP

Cost plus pricing: Cost plus pricing is one under which cost of product is determined

with the help of basically two factors like cost of per unit and agreed percentage of profit.

considering future business environment and its growth strategies. Advises and

comments are received from other important internal stakeholders to ensure that forecsted

values are proper or not (Cash Budget. 2016). Receiving capital budget forecast: After forecast of revenue from different departments,

capital budget requirements are received and same is taken into consideration by the

project manager. Allocation of funds: In this stage, allocation of funds is done across different

departments in order to ensure that needs of all of them will be fulfilled in a proper

manner.

Updating budget: After allocation of budget across departments, same is updated

according to decisions that are taken by the top management.

(c) Pricing strategies

There are number of pricing strategies that can be followed by the business firms and

some of them are given as below. Skimming price strategy: It is the pricing strategy that is followed by the business firm

and under this, product is sold at higher price relative to other firms. This strategy is

followed when firm launches innovative product in the market. Penetration price strategy: Penetration pricing strategy is one under which product is

sold at a low price in the market. By doing so, firm tries to capture the market at a rapid

rate. This kind of strategy is used by most of the firms because it supports to increase

market share in the industry. Competition based pricing: Competition based pricing is one under which firm takes into

consideration the price that is determined by rival firms (Shelby, 2013). By considering

such price, product pricing is done. Moreover, within the market if rivals charge 50 GBP

price of the every mobile charger then selected firm will take pricing decisions lower than

50 GBP

Cost plus pricing: Cost plus pricing is one under which cost of product is determined

with the help of basically two factors like cost of per unit and agreed percentage of profit.

TASK 4

(a) Management accounting systems and their use by firms

Balance scorecard is an approach under which financial and non-financial performance of

the firm is measured. There are four different segments of balance scorecard which are used to

access the firm’s performance. Balance scorecard can be used by the business firm and under

this, it can measure its performance in different ways like customers, internal business process,

financial etc. Balance score card can be used to identify and solve the financial problems. In this

segment, it can be observed that there are four parts like objectives, measures, targets and

initiatives. Actual results can be compared with determined objectives and on that basis, it can be

identified that whether performance was good or bad. On the basis of results, it can be identified

whether measures that are taken by the firm are effective in nature or not (Chandra, 2011).

Effectiveness of initiatives taken by the business firm is also identified by using balance score

card. All these things reflect the finance related issue that is currently faced by business firm and

areas where there is need to take strict actions. Balance score card is used to improve the

financial governance because areas where there is need to improve performance is identified by

using KPI or balance scorecard. By formulating an appropriate strategy, governance is improved

to a high extent. It can be said that there is huge importance of the balance scorecard for business

firms.

CONCLUSION

On the basis of above discussion, it is concluded that there is significant importance of

the management accounting for business firms. There are number of methods that are used by the

firms under management accounting by business organisation. These tools help managers in

evaluating business performance in a systematic way. Strategy is prepared on time to resolve

issues that are currently being faced by the business firm. It can be said that there is huge

importance of the management accounting for business firm. Budget is one of the main tools that

help firms in controlling expenses in business. Time to time actual performance is compared

with project’s performance in order to identify time when there is need to take action.

(a) Management accounting systems and their use by firms

Balance scorecard is an approach under which financial and non-financial performance of

the firm is measured. There are four different segments of balance scorecard which are used to

access the firm’s performance. Balance scorecard can be used by the business firm and under

this, it can measure its performance in different ways like customers, internal business process,

financial etc. Balance score card can be used to identify and solve the financial problems. In this

segment, it can be observed that there are four parts like objectives, measures, targets and

initiatives. Actual results can be compared with determined objectives and on that basis, it can be

identified that whether performance was good or bad. On the basis of results, it can be identified

whether measures that are taken by the firm are effective in nature or not (Chandra, 2011).

Effectiveness of initiatives taken by the business firm is also identified by using balance score

card. All these things reflect the finance related issue that is currently faced by business firm and

areas where there is need to take strict actions. Balance score card is used to improve the

financial governance because areas where there is need to improve performance is identified by

using KPI or balance scorecard. By formulating an appropriate strategy, governance is improved

to a high extent. It can be said that there is huge importance of the balance scorecard for business

firms.

CONCLUSION

On the basis of above discussion, it is concluded that there is significant importance of

the management accounting for business firms. There are number of methods that are used by the

firms under management accounting by business organisation. These tools help managers in

evaluating business performance in a systematic way. Strategy is prepared on time to resolve

issues that are currently being faced by the business firm. It can be said that there is huge

importance of the management accounting for business firm. Budget is one of the main tools that

help firms in controlling expenses in business. Time to time actual performance is compared

with project’s performance in order to identify time when there is need to take action.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.