Management Accounting Report: Assessment 1 Analysis and Evaluation

VerifiedAdded on 2019/10/31

|18

|4083

|495

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles. It begins with an examination of key concepts such as the role of reliable accounting information systems, data coding, and manufacturing overhead. The report then delves into business performance analysis, exploring tools like variance analysis and key performance indicators, and also covers the analysis of leverage ratios and budget implementation. The report further investigates the importance of variance analysis in identifying and addressing discrepancies between planned and actual figures. The report also includes an assessment of manufacturing costs, differentiating between prime, direct, and indirect costs. The analysis extends to cost sheets, providing an understanding of cost variances related to furniture manufacturing. Overall, the report aims to provide a deep understanding of management accounting practices and their application in business operations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Assessment 1 (A).......................................................................................................................4

Question 1..............................................................................................................................4

Question 2..............................................................................................................................4

Question 3..............................................................................................................................5

Question 4..............................................................................................................................5

Question 5..............................................................................................................................6

Question 7..............................................................................................................................7

Question 8..............................................................................................................................7

Assessment 1 (B)........................................................................................................................8

Task 1 – Cost of Manufacture Analysis.................................................................................8

Task 2- Production cost worksheet..........................................................................................10

Part A...................................................................................................................................10

Part B....................................................................................................................................11

Part C....................................................................................................................................11

Part D...................................................................................................................................12

Part E....................................................................................................................................13

Part F....................................................................................................................................13

Part G...................................................................................................................................14

Part H...................................................................................................................................14

Part I.....................................................................................................................................15

References................................................................................................................................16

Assessment 1 (A).......................................................................................................................4

Question 1..............................................................................................................................4

Question 2..............................................................................................................................4

Question 3..............................................................................................................................5

Question 4..............................................................................................................................5

Question 5..............................................................................................................................6

Question 7..............................................................................................................................7

Question 8..............................................................................................................................7

Assessment 1 (B)........................................................................................................................8

Task 1 – Cost of Manufacture Analysis.................................................................................8

Task 2- Production cost worksheet..........................................................................................10

Part A...................................................................................................................................10

Part B....................................................................................................................................11

Part C....................................................................................................................................11

Part D...................................................................................................................................12

Part E....................................................................................................................................13

Part F....................................................................................................................................13

Part G...................................................................................................................................14

Part H...................................................................................................................................14

Part I.....................................................................................................................................15

References................................................................................................................................16

TABLE OF FIGURES

Figure 1: Total Product Curve..................................................................................................12

Figure 2: Total Cost Curve.......................................................................................................14

Figure 3: Graph representing marginal curve..........................................................................15

Figure 1: Total Product Curve..................................................................................................12

Figure 2: Total Cost Curve.......................................................................................................14

Figure 3: Graph representing marginal curve..........................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT 1 (A)

Question 1

According to Haynes and et al. (2014), reliable accounting information systems

generate and record costing information reliably by considering viability and accuracy of

data1. The computerized system will be able to generate accounting documents such as bills,

memo and invoices. It will also record transactions of daily costing and business transactions

via computer software. The further computerized system will assist costing information by

preparing financial statements and trial balance in order to check authenticity and accuracy.

Computerized system comprises a primary stage that is the Transaction processing system,

which records and store transactions held in different operational areas of business. TPS

engages these following steps in addressing a transaction; data validation and entry, recording

and storage, processing and re-validation, data and reporting. If the system is able to generate

and record cited data, then it will be cost-effective and assist in smooth management, while

ensuring speed, security and easy access to data.

Question 2

The legislative and organizational requirement prescribe that a single code should

apply to an only individual category of data coding and all the categories should be wide-

ranging. As per Drury and Colin (2013), there are clear rules for coders which are to be

followed so that the process of coding is consistent in all fields related to particular data2. For

the purpose of quantitative analysis, data coding is usually done into a variable that is capable

of being measured as nominal or ordinal. Quantitative analysis-data is-

Pre-coded that is specific codes are assigned to expected answers,

field-coded (codes are available during fieldwork),

Post-coded (coding are available when the coding is complete )

Office-coded (done after fieldwork).

According to words of Bryman, Alan and Emma Bell, (2015), in this aspect business are

required to comply with the legislation such as AMX Software and Program Code License

1 Haynes, Ian Frederick, Bradley Jason Schultz, Stephen Conway Larkin, and Sean David Rogers.

"Computerized information collection and training method and apparatus." U.S. Patent 8,633,985, issued

January 21, 2014.

2 DRURY, COLIN M. Management and cost accounting. Springer, 2013.

Question 1

According to Haynes and et al. (2014), reliable accounting information systems

generate and record costing information reliably by considering viability and accuracy of

data1. The computerized system will be able to generate accounting documents such as bills,

memo and invoices. It will also record transactions of daily costing and business transactions

via computer software. The further computerized system will assist costing information by

preparing financial statements and trial balance in order to check authenticity and accuracy.

Computerized system comprises a primary stage that is the Transaction processing system,

which records and store transactions held in different operational areas of business. TPS

engages these following steps in addressing a transaction; data validation and entry, recording

and storage, processing and re-validation, data and reporting. If the system is able to generate

and record cited data, then it will be cost-effective and assist in smooth management, while

ensuring speed, security and easy access to data.

Question 2

The legislative and organizational requirement prescribe that a single code should

apply to an only individual category of data coding and all the categories should be wide-

ranging. As per Drury and Colin (2013), there are clear rules for coders which are to be

followed so that the process of coding is consistent in all fields related to particular data2. For

the purpose of quantitative analysis, data coding is usually done into a variable that is capable

of being measured as nominal or ordinal. Quantitative analysis-data is-

Pre-coded that is specific codes are assigned to expected answers,

field-coded (codes are available during fieldwork),

Post-coded (coding are available when the coding is complete )

Office-coded (done after fieldwork).

According to words of Bryman, Alan and Emma Bell, (2015), in this aspect business are

required to comply with the legislation such as AMX Software and Program Code License

1 Haynes, Ian Frederick, Bradley Jason Schultz, Stephen Conway Larkin, and Sean David Rogers.

"Computerized information collection and training method and apparatus." U.S. Patent 8,633,985, issued

January 21, 2014.

2 DRURY, COLIN M. Management and cost accounting. Springer, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Agreement; Amendment (Moral Rights) Act; 2001; Privacy Regulation 2013; Electronic

Transactions Act 1999 and Fair Work Regulations 20093. In addition to this; they are required

to satisfy standards cited under AS ISO 15489 Records Management; FOI guidelines and

guidance notes.

For areas, which require a qualitative format like phenomenological psychology (for

example, formulating a motivational theory at the organizational level), a varied approach to

coding can be used. A two-step process is outlined by the legislation which begins with basic

coding in order to differentiate between the overall themes which are followed in depth. This

basic coding is interpretive code which has more specific trends and patterns. As per the

words of Halling and et al., (2016), most of the qualitative coding is either grounded or a

priori coding4.

Grounded coding is the one that allows notable themes and patterns which

become known from the document themselves.

Priori coding applies pre-existing theoretical frameworks for analyzing the

documents.

Since the methods of coding are applied across various fields, the researcher

applies axial coding. This is the process in which core thematic categories are

presented in several documents for discovering common patterns and relations

between various fields.

Before formulating categories, a researcher should implement first cycle method of

coding. There are many methods available out of which the researcher has to pick one that is

suitable for the format and nature of the information to be coded.

Question 3

Manufacturing overhead is inclusive of things like utilization of electricity in order to

function the equipment of factory, property and equipment depreciation, factory workers and

supplies exclusive of direct labour. Manufacturing overhead is totally engaged in operational

activities of the company. According to the views of McDonald, Malcolm and Hugh Wilson,

3 Bryman, Alan, and Emma Bell. Business research methods. Oxford University Press, USA, 2015.

4 Halling, Michael, Jin Yu, and Josef Zechner. "Leverage dynamics over the business cycle." Journal of

Financial Economics 122, no. 1 (2016): 21-41.

Transactions Act 1999 and Fair Work Regulations 20093. In addition to this; they are required

to satisfy standards cited under AS ISO 15489 Records Management; FOI guidelines and

guidance notes.

For areas, which require a qualitative format like phenomenological psychology (for

example, formulating a motivational theory at the organizational level), a varied approach to

coding can be used. A two-step process is outlined by the legislation which begins with basic

coding in order to differentiate between the overall themes which are followed in depth. This

basic coding is interpretive code which has more specific trends and patterns. As per the

words of Halling and et al., (2016), most of the qualitative coding is either grounded or a

priori coding4.

Grounded coding is the one that allows notable themes and patterns which

become known from the document themselves.

Priori coding applies pre-existing theoretical frameworks for analyzing the

documents.

Since the methods of coding are applied across various fields, the researcher

applies axial coding. This is the process in which core thematic categories are

presented in several documents for discovering common patterns and relations

between various fields.

Before formulating categories, a researcher should implement first cycle method of

coding. There are many methods available out of which the researcher has to pick one that is

suitable for the format and nature of the information to be coded.

Question 3

Manufacturing overhead is inclusive of things like utilization of electricity in order to

function the equipment of factory, property and equipment depreciation, factory workers and

supplies exclusive of direct labour. Manufacturing overhead is totally engaged in operational

activities of the company. According to the views of McDonald, Malcolm and Hugh Wilson,

3 Bryman, Alan, and Emma Bell. Business research methods. Oxford University Press, USA, 2015.

4 Halling, Michael, Jin Yu, and Josef Zechner. "Leverage dynamics over the business cycle." Journal of

Financial Economics 122, no. 1 (2016): 21-41.

(2016), it involves the cost held in the factory other than the direct labour and material costs5.

For this reason, manufacturing overhead is considered as an indirect cost. Some examples for

manufacturing overhead are rent and depreciation on factory premises and equipment, factory

supervisors, a quality segment of factory, electricity, employees, gas and maintenance of the

factory etc.

Question 4

The aim of business performance analysis is to determine the opportunities for

development, interpreting their causes and further taking action. Opportunities can be spotted

in many ways, like in performance issues and business areas that conduct well and could be

controlled additionally. Businesses make use of various tools such as variance analysis; this

analysis makes a prediction of how an organization will conduct from a financial position. As

per the views of Tereanu and et al., (2014), the comparison of financial results is made in

order to forecast. Once the reasons are determined, business identifies if or if not the changes

in their own aspects within operations are needed to drive the company towards its forecasted

goals6. A key performance indicator is also a tool for analysing business performance; it

assists the organization to identify whether the parts are effectively working or not. It is

helpful in monitoring better market strategies in order to attain available opportunities.

Business performance analysis also involves customer satisfaction measurement, as this

aspect is considered considerable for any business; it is because happy customers are always

likely to engage with business in near future. One other tool is employee satisfaction;

business is required to determine whether the human resources are satisfied with their

salaries, compensation, working environment or opportunities in order to motivate and

encourage them.

Question 5

Organizations are based on the combination of owner’s equity and finance in their

operational activities. The leverage ratio is considered as one of the various measurements of

financial operations that keeps an eye upon how capital incurred in term of loan, debts or

considers the company’s capability to meet the financial requirements. A leverage ratio, in

essence, means to determine the debts levels of a company. Most general leverage ratios used

are a debt to equity and debt ratios. According to the opinion of Braun and et al., (2014), the

5 McDonald, Malcolm, and Hugh Wilson. Marketing Plans: How to prepare them, how to profit from them. John

Wiley & Sons, 2016.

6 Tereanu, Eugen, Anita Tuladhar, and Alejandro S. Simone. "Structural balance targeting and output gap

uncertainty." (2014).

For this reason, manufacturing overhead is considered as an indirect cost. Some examples for

manufacturing overhead are rent and depreciation on factory premises and equipment, factory

supervisors, a quality segment of factory, electricity, employees, gas and maintenance of the

factory etc.

Question 4

The aim of business performance analysis is to determine the opportunities for

development, interpreting their causes and further taking action. Opportunities can be spotted

in many ways, like in performance issues and business areas that conduct well and could be

controlled additionally. Businesses make use of various tools such as variance analysis; this

analysis makes a prediction of how an organization will conduct from a financial position. As

per the views of Tereanu and et al., (2014), the comparison of financial results is made in

order to forecast. Once the reasons are determined, business identifies if or if not the changes

in their own aspects within operations are needed to drive the company towards its forecasted

goals6. A key performance indicator is also a tool for analysing business performance; it

assists the organization to identify whether the parts are effectively working or not. It is

helpful in monitoring better market strategies in order to attain available opportunities.

Business performance analysis also involves customer satisfaction measurement, as this

aspect is considered considerable for any business; it is because happy customers are always

likely to engage with business in near future. One other tool is employee satisfaction;

business is required to determine whether the human resources are satisfied with their

salaries, compensation, working environment or opportunities in order to motivate and

encourage them.

Question 5

Organizations are based on the combination of owner’s equity and finance in their

operational activities. The leverage ratio is considered as one of the various measurements of

financial operations that keeps an eye upon how capital incurred in term of loan, debts or

considers the company’s capability to meet the financial requirements. A leverage ratio, in

essence, means to determine the debts levels of a company. Most general leverage ratios used

are a debt to equity and debt ratios. According to the opinion of Braun and et al., (2014), the

5 McDonald, Malcolm, and Hugh Wilson. Marketing Plans: How to prepare them, how to profit from them. John

Wiley & Sons, 2016.

6 Tereanu, Eugen, Anita Tuladhar, and Alejandro S. Simone. "Structural balance targeting and output gap

uncertainty." (2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

leverage ratio is a type of financial ratio that shows the debt level held by a business

enterprise in opposition to various other accounts cited in profit and loss statement, balance

sheet or cash flow statement7. It offers and keeps a record of incoming assets from loans to

finance business operations.

Question 6

Before implementing a budget, an organization must consider these questions. First is

the strategic plan, this will ensure that resources are used in such a manner that they promote

strategic development of the organization. Next step is to realise the goals of the

organization; goals are required to be developed and achieved. Organizations must implement

revenue projections, and it must be based on past financial performance plus the estimated

growth income of the business. The further organization has to consider fixed and variable

cost projections for controlling the budgeting and making it cost effective. As per the opinion

of Brei, Michael and Leonardo Gambacorta, (2014), evaluation of payroll expenses must be

done on a timely basis prior to making a budget. Target profit margin must be conducted in

any organization, as they allow for returns on investment8. Next is the budget approved by

the CEO, president or the owner of the organization in order to examine the budget

performance and for controlling the all the expenses. The organization must nest step on to

review the budget for monitoring the performance in opposition to the goals. This step must

be performed by the committee on a timely basis so that corrections can be done if there are

any. The last step is to address with the budget variances, and it must be reviewed by a

responsible manager, and queries must be raised as to know why the variance took place.

Hence, a good process of budgeting can improve and progress organizational activities while

ensuring long-term growth and financial health.

Question 7

Variance analysis is a method of analyzing and determining the variation between two

figures. It can also be defined as an accounting or numerical tool that assists in identifying the

root cause of variance in the operational and functional activities of business. In accountancy,

use of variation analysis is done to consider the productivity of the project. It also assists in

analyzing the difference between total and proposed costs of the project. Variance analysis

7 Braun, Karen Wilken, Wendy M. Tietz, Walter T. Harrison, Linda Smith Bamber, and Charles T.

Horngren. Managerial accounting. Pearson, 2014.

8 Brei, Michael, and Leonardo Gambacorta. "The leverage ratio over the cycle." (2014).

enterprise in opposition to various other accounts cited in profit and loss statement, balance

sheet or cash flow statement7. It offers and keeps a record of incoming assets from loans to

finance business operations.

Question 6

Before implementing a budget, an organization must consider these questions. First is

the strategic plan, this will ensure that resources are used in such a manner that they promote

strategic development of the organization. Next step is to realise the goals of the

organization; goals are required to be developed and achieved. Organizations must implement

revenue projections, and it must be based on past financial performance plus the estimated

growth income of the business. The further organization has to consider fixed and variable

cost projections for controlling the budgeting and making it cost effective. As per the opinion

of Brei, Michael and Leonardo Gambacorta, (2014), evaluation of payroll expenses must be

done on a timely basis prior to making a budget. Target profit margin must be conducted in

any organization, as they allow for returns on investment8. Next is the budget approved by

the CEO, president or the owner of the organization in order to examine the budget

performance and for controlling the all the expenses. The organization must nest step on to

review the budget for monitoring the performance in opposition to the goals. This step must

be performed by the committee on a timely basis so that corrections can be done if there are

any. The last step is to address with the budget variances, and it must be reviewed by a

responsible manager, and queries must be raised as to know why the variance took place.

Hence, a good process of budgeting can improve and progress organizational activities while

ensuring long-term growth and financial health.

Question 7

Variance analysis is a method of analyzing and determining the variation between two

figures. It can also be defined as an accounting or numerical tool that assists in identifying the

root cause of variance in the operational and functional activities of business. In accountancy,

use of variation analysis is done to consider the productivity of the project. It also assists in

analyzing the difference between total and proposed costs of the project. Variance analysis

7 Braun, Karen Wilken, Wendy M. Tietz, Walter T. Harrison, Linda Smith Bamber, and Charles T.

Horngren. Managerial accounting. Pearson, 2014.

8 Brei, Michael, and Leonardo Gambacorta. "The leverage ratio over the cycle." (2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assists the managers to manage and control those differences. In accordance to Roberts,

Maxwell and Riccardo Russo, (2014), project managers are required to perform variance

analysis at each target of the business project in order to evaluate the financial data. Along

with this, it also spots actual differences between actual against proposed costs9. By following

this path, managers will be able to measure the quantitative data as regards with the expenses,

income and stock level regarding the project that will consequently assist managing and

achieve the business goals.

Question 8

Variance analysis is an investigation based on a quantitative analysis which indicates

the difference of actual with planned behaviour. Variance analysis is used to manage and

maintain control of the business management. For instance, is a company makes a budget for

sales of $10,000 and the total sales were $8,000 further the variance analysis yields $2,000

which was the difference amount. Particularly, Variance analysis will be effective if an entity

reviews the variance amount over the trend line, that the unexpected changes in this level

from monthly basis can be apparently clear. In accordance with the words of Montgomery

and Douglas, (2017), variance analysis is also inclusive of examination of these considered

differences, so the outcome is as a report becomes the difference from potential, and an

understanding of the occurrence of variance10. Variance analysis is used to determine and

clarify the reasons due to which there was a difference between budgeted and actual figures.

ASSESSMENT 1 (B)

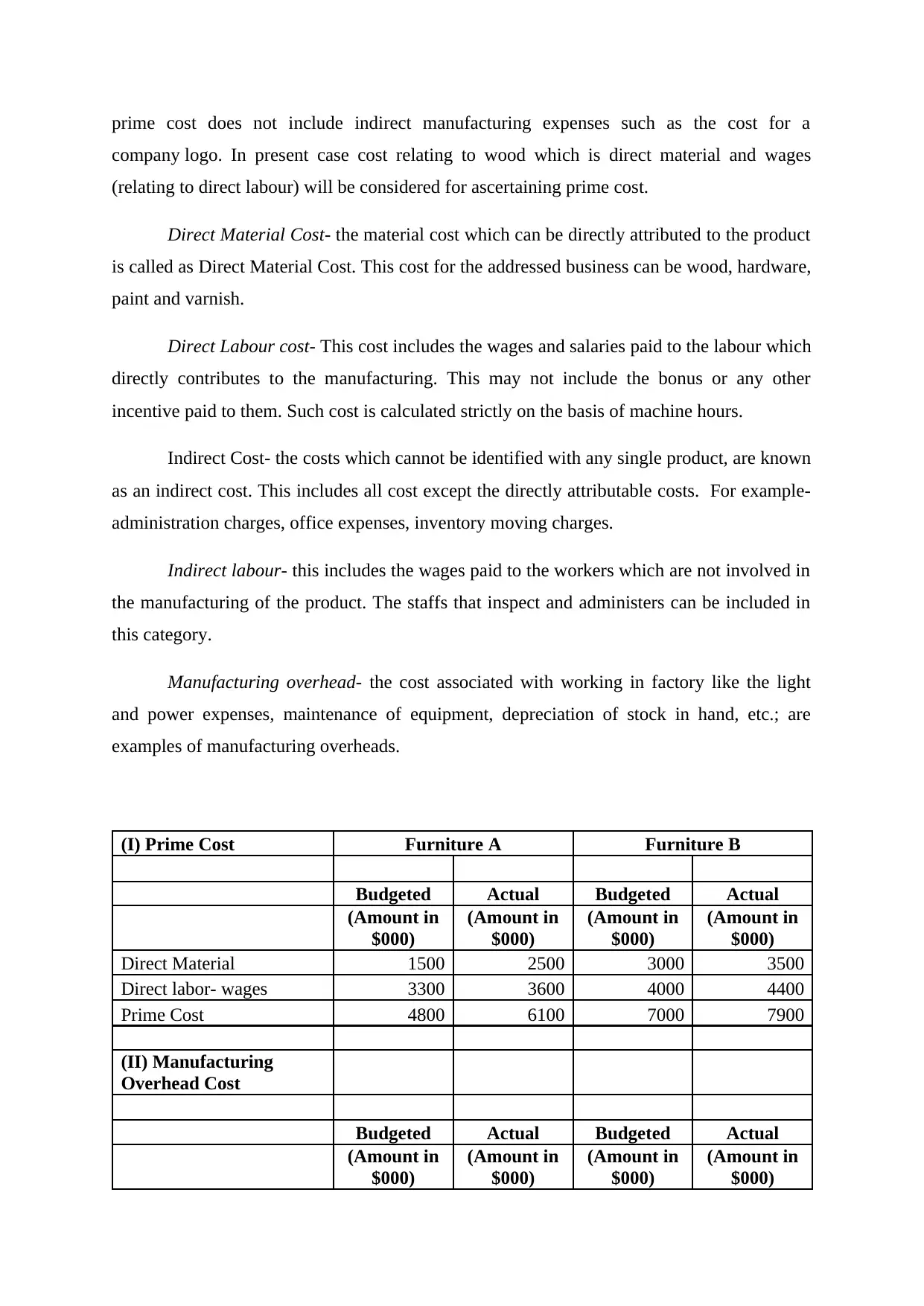

Task 1 – Cost of Manufacture Analysis

In present case manufacturing cost of business relating to furniture making is assessed in

which uniform furniture is manufactured in bulk. Further, two kinds of furniture are being

prepared Furniture A, and Furniture B. Cost sheet relating to this furniture have been

provided with both estimated and budgeted figures to assess the existing variance relating to

cost.

Prime cost- In accordance with the views of Weygandt and et al. (2015), refers to the

cost of the manufactured product which reveals the best profit margin of a company11. The

9 Roberts, Maxwell, and Riccardo Russo. A student's guide to analysis of variance. Routledge, 2014.

10 Montgomery, Douglas C. Design and analysis of experiments. John Wiley & Sons, 2017.

11 Weygandt and et.al. Kieso. Financial & Managerial Accounting. John Wiley & Sons, 2015.

Maxwell and Riccardo Russo, (2014), project managers are required to perform variance

analysis at each target of the business project in order to evaluate the financial data. Along

with this, it also spots actual differences between actual against proposed costs9. By following

this path, managers will be able to measure the quantitative data as regards with the expenses,

income and stock level regarding the project that will consequently assist managing and

achieve the business goals.

Question 8

Variance analysis is an investigation based on a quantitative analysis which indicates

the difference of actual with planned behaviour. Variance analysis is used to manage and

maintain control of the business management. For instance, is a company makes a budget for

sales of $10,000 and the total sales were $8,000 further the variance analysis yields $2,000

which was the difference amount. Particularly, Variance analysis will be effective if an entity

reviews the variance amount over the trend line, that the unexpected changes in this level

from monthly basis can be apparently clear. In accordance with the words of Montgomery

and Douglas, (2017), variance analysis is also inclusive of examination of these considered

differences, so the outcome is as a report becomes the difference from potential, and an

understanding of the occurrence of variance10. Variance analysis is used to determine and

clarify the reasons due to which there was a difference between budgeted and actual figures.

ASSESSMENT 1 (B)

Task 1 – Cost of Manufacture Analysis

In present case manufacturing cost of business relating to furniture making is assessed in

which uniform furniture is manufactured in bulk. Further, two kinds of furniture are being

prepared Furniture A, and Furniture B. Cost sheet relating to this furniture have been

provided with both estimated and budgeted figures to assess the existing variance relating to

cost.

Prime cost- In accordance with the views of Weygandt and et al. (2015), refers to the

cost of the manufactured product which reveals the best profit margin of a company11. The

9 Roberts, Maxwell, and Riccardo Russo. A student's guide to analysis of variance. Routledge, 2014.

10 Montgomery, Douglas C. Design and analysis of experiments. John Wiley & Sons, 2017.

11 Weygandt and et.al. Kieso. Financial & Managerial Accounting. John Wiley & Sons, 2015.

prime cost does not include indirect manufacturing expenses such as the cost for a

company logo. In present case cost relating to wood which is direct material and wages

(relating to direct labour) will be considered for ascertaining prime cost.

Direct Material Cost- the material cost which can be directly attributed to the product

is called as Direct Material Cost. This cost for the addressed business can be wood, hardware,

paint and varnish.

Direct Labour cost- This cost includes the wages and salaries paid to the labour which

directly contributes to the manufacturing. This may not include the bonus or any other

incentive paid to them. Such cost is calculated strictly on the basis of machine hours.

Indirect Cost- the costs which cannot be identified with any single product, are known

as an indirect cost. This includes all cost except the directly attributable costs. For example-

administration charges, office expenses, inventory moving charges.

Indirect labour- this includes the wages paid to the workers which are not involved in

the manufacturing of the product. The staffs that inspect and administers can be included in

this category.

Manufacturing overhead- the cost associated with working in factory like the light

and power expenses, maintenance of equipment, depreciation of stock in hand, etc.; are

examples of manufacturing overheads.

(I) Prime Cost Furniture A Furniture B

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

Direct Material 1500 2500 3000 3500

Direct labor- wages 3300 3600 4000 4400

Prime Cost 4800 6100 7000 7900

(II) Manufacturing

Overhead Cost

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

company logo. In present case cost relating to wood which is direct material and wages

(relating to direct labour) will be considered for ascertaining prime cost.

Direct Material Cost- the material cost which can be directly attributed to the product

is called as Direct Material Cost. This cost for the addressed business can be wood, hardware,

paint and varnish.

Direct Labour cost- This cost includes the wages and salaries paid to the labour which

directly contributes to the manufacturing. This may not include the bonus or any other

incentive paid to them. Such cost is calculated strictly on the basis of machine hours.

Indirect Cost- the costs which cannot be identified with any single product, are known

as an indirect cost. This includes all cost except the directly attributable costs. For example-

administration charges, office expenses, inventory moving charges.

Indirect labour- this includes the wages paid to the workers which are not involved in

the manufacturing of the product. The staffs that inspect and administers can be included in

this category.

Manufacturing overhead- the cost associated with working in factory like the light

and power expenses, maintenance of equipment, depreciation of stock in hand, etc.; are

examples of manufacturing overheads.

(I) Prime Cost Furniture A Furniture B

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

Direct Material 1500 2500 3000 3500

Direct labor- wages 3300 3600 4000 4400

Prime Cost 4800 6100 7000 7900

(II) Manufacturing

Overhead Cost

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

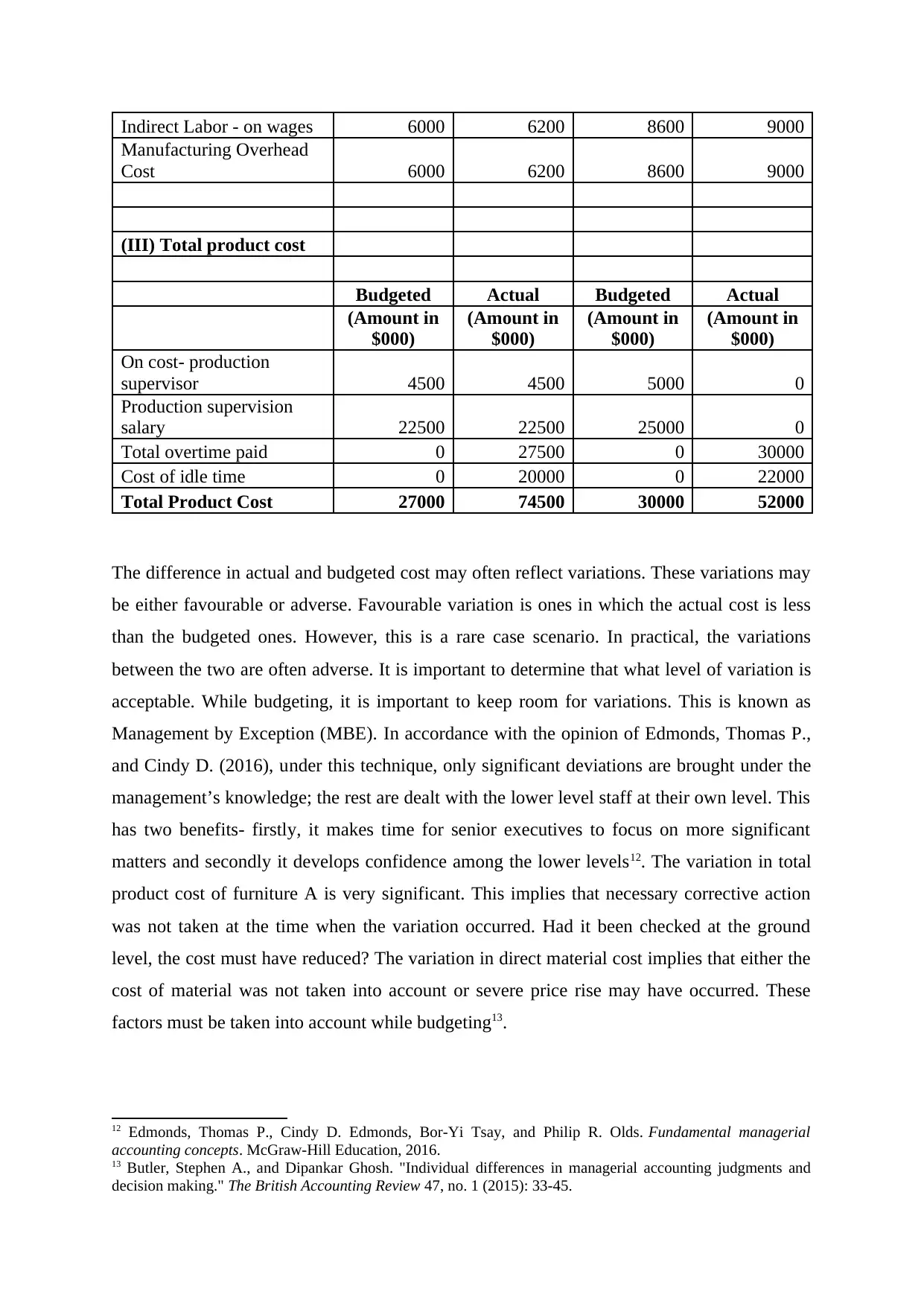

Indirect Labor - on wages 6000 6200 8600 9000

Manufacturing Overhead

Cost 6000 6200 8600 9000

(III) Total product cost

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

On cost- production

supervisor 4500 4500 5000 0

Production supervision

salary 22500 22500 25000 0

Total overtime paid 0 27500 0 30000

Cost of idle time 0 20000 0 22000

Total Product Cost 27000 74500 30000 52000

The difference in actual and budgeted cost may often reflect variations. These variations may

be either favourable or adverse. Favourable variation is ones in which the actual cost is less

than the budgeted ones. However, this is a rare case scenario. In practical, the variations

between the two are often adverse. It is important to determine that what level of variation is

acceptable. While budgeting, it is important to keep room for variations. This is known as

Management by Exception (MBE). In accordance with the opinion of Edmonds, Thomas P.,

and Cindy D. (2016), under this technique, only significant deviations are brought under the

management’s knowledge; the rest are dealt with the lower level staff at their own level. This

has two benefits- firstly, it makes time for senior executives to focus on more significant

matters and secondly it develops confidence among the lower levels12. The variation in total

product cost of furniture A is very significant. This implies that necessary corrective action

was not taken at the time when the variation occurred. Had it been checked at the ground

level, the cost must have reduced? The variation in direct material cost implies that either the

cost of material was not taken into account or severe price rise may have occurred. These

factors must be taken into account while budgeting13.

12 Edmonds, Thomas P., Cindy D. Edmonds, Bor-Yi Tsay, and Philip R. Olds. Fundamental managerial

accounting concepts. McGraw-Hill Education, 2016.

13 Butler, Stephen A., and Dipankar Ghosh. "Individual differences in managerial accounting judgments and

decision making." The British Accounting Review 47, no. 1 (2015): 33-45.

Manufacturing Overhead

Cost 6000 6200 8600 9000

(III) Total product cost

Budgeted Actual Budgeted Actual

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

(Amount in

$000)

On cost- production

supervisor 4500 4500 5000 0

Production supervision

salary 22500 22500 25000 0

Total overtime paid 0 27500 0 30000

Cost of idle time 0 20000 0 22000

Total Product Cost 27000 74500 30000 52000

The difference in actual and budgeted cost may often reflect variations. These variations may

be either favourable or adverse. Favourable variation is ones in which the actual cost is less

than the budgeted ones. However, this is a rare case scenario. In practical, the variations

between the two are often adverse. It is important to determine that what level of variation is

acceptable. While budgeting, it is important to keep room for variations. This is known as

Management by Exception (MBE). In accordance with the opinion of Edmonds, Thomas P.,

and Cindy D. (2016), under this technique, only significant deviations are brought under the

management’s knowledge; the rest are dealt with the lower level staff at their own level. This

has two benefits- firstly, it makes time for senior executives to focus on more significant

matters and secondly it develops confidence among the lower levels12. The variation in total

product cost of furniture A is very significant. This implies that necessary corrective action

was not taken at the time when the variation occurred. Had it been checked at the ground

level, the cost must have reduced? The variation in direct material cost implies that either the

cost of material was not taken into account or severe price rise may have occurred. These

factors must be taken into account while budgeting13.

12 Edmonds, Thomas P., Cindy D. Edmonds, Bor-Yi Tsay, and Philip R. Olds. Fundamental managerial

accounting concepts. McGraw-Hill Education, 2016.

13 Butler, Stephen A., and Dipankar Ghosh. "Individual differences in managerial accounting judgments and

decision making." The British Accounting Review 47, no. 1 (2015): 33-45.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2- PRODUCTION COST WORKSHEET

Part A

The output, in this case, will be weaved rugs. Output is said as something which the

end product of a manufacturing process. The output is the final product of the input. In this

case, the rough rugs are woven to produced fine weaved rugs. Fixed input is the product

which remains constant at any number of units14. In this case, rough rags will be the fixed

unit. However, it must be noted at here each unit of input produces a single output. Thus, the

fixed input in this regard will be one labour that is Coretta. The Woking hours of Coretta is

fixed for any unit of output. The variable input will be the additional worker which increases

the level of output up to a certain level.

14 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance. Pearson Higher

Education AU, 2015.

Part A

The output, in this case, will be weaved rugs. Output is said as something which the

end product of a manufacturing process. The output is the final product of the input. In this

case, the rough rugs are woven to produced fine weaved rugs. Fixed input is the product

which remains constant at any number of units14. In this case, rough rags will be the fixed

unit. However, it must be noted at here each unit of input produces a single output. Thus, the

fixed input in this regard will be one labour that is Coretta. The Woking hours of Coretta is

fixed for any unit of output. The variable input will be the additional worker which increases

the level of output up to a certain level.

14 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance. Pearson Higher

Education AU, 2015.

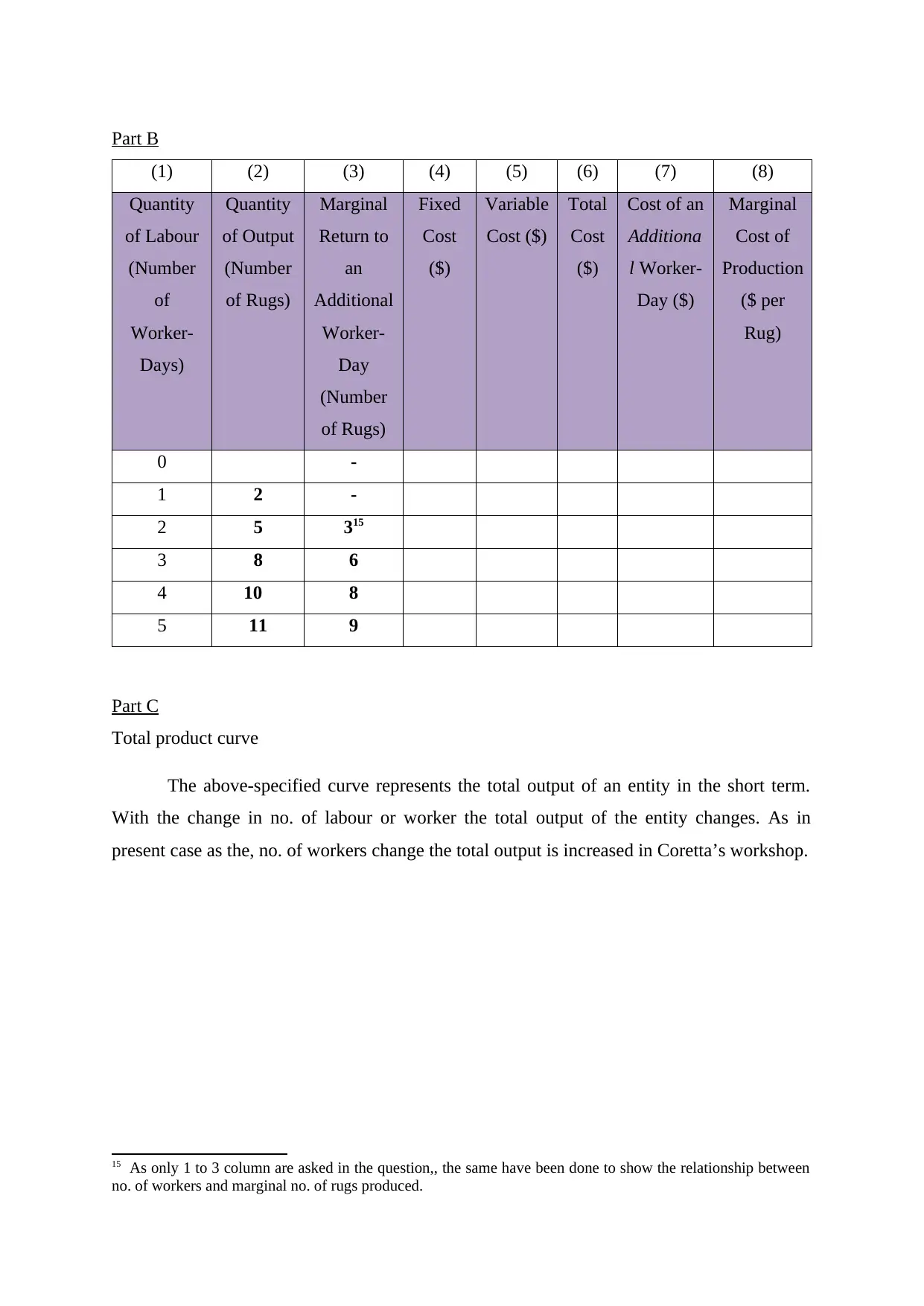

Part B

(1) (2) (3) (4) (5) (6) (7) (8)

Quantity

of Labour

(Number

of

Worker-

Days)

Quantity

of Output

(Number

of Rugs)

Marginal

Return to

an

Additional

Worker-

Day

(Number

of Rugs)

Fixed

Cost

($)

Variable

Cost ($)

Total

Cost

($)

Cost of an

Additiona

l Worker-

Day ($)

Marginal

Cost of

Production

($ per

Rug)

0 -

1 2 -

2 5 315

3 8 6

4 10 8

5 11 9

Part C

Total product curve

The above-specified curve represents the total output of an entity in the short term.

With the change in no. of labour or worker the total output of the entity changes. As in

present case as the, no. of workers change the total output is increased in Coretta’s workshop.

15 As only 1 to 3 column are asked in the question,, the same have been done to show the relationship between

no. of workers and marginal no. of rugs produced.

(1) (2) (3) (4) (5) (6) (7) (8)

Quantity

of Labour

(Number

of

Worker-

Days)

Quantity

of Output

(Number

of Rugs)

Marginal

Return to

an

Additional

Worker-

Day

(Number

of Rugs)

Fixed

Cost

($)

Variable

Cost ($)

Total

Cost

($)

Cost of an

Additiona

l Worker-

Day ($)

Marginal

Cost of

Production

($ per

Rug)

0 -

1 2 -

2 5 315

3 8 6

4 10 8

5 11 9

Part C

Total product curve

The above-specified curve represents the total output of an entity in the short term.

With the change in no. of labour or worker the total output of the entity changes. As in

present case as the, no. of workers change the total output is increased in Coretta’s workshop.

15 As only 1 to 3 column are asked in the question,, the same have been done to show the relationship between

no. of workers and marginal no. of rugs produced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.