Management Accounting Report for Merlin Financial Consultants Analysis

VerifiedAdded on 2020/10/05

|19

|5663

|433

Report

AI Summary

This comprehensive report delves into the realm of management accounting, using Merlin Financial Consultants as a case study. It meticulously examines the core principles of management accounting, contrasting it with financial accounting, and explores the essential requirements of various management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report details different management accounting reporting methods, emphasizing information relevancy and the types of reports such as budget reports, credit control reports, and job cost reports. A key focus is on cost analysis techniques, with a detailed comparison between absorption costing and marginal costing, illustrated through income statement examples. Furthermore, the report analyzes the advantages of different planning tools and their application within a management accounting framework and concludes by addressing how organizations use management accounting to respond to financial problems, ultimately leading to sustainable success. The report provides a well-structured analysis of management accounting principles and their practical application.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and the essential requirements of different types of management

accounting system..................................................................................................................1

P2. Different methods used for management accounting reporting.......................................3

M1. Evaluation of benefits of management accounting systems...........................................4

D1. Management accounting system and management accounting reporting integrated within

organisational processes.........................................................................................................5

TASK 2 ...........................................................................................................................................5

P3. Appropriate techniques of cost analysis to prepare an income statement........................5

M2. Range of management accounting techniques and producing appropriate financial

reporting documents...............................................................................................................9

D2. Financial reports which are applied to interpret data for business activities...................9

TASK 3............................................................................................................................................9

P4. Uses of different planning tools in management accounting...........................................9

M3. Analysing different planning tools and their applications............................................13

TASK 4..........................................................................................................................................13

P5. The way organisation use management accounting system to respond to financial

problems...............................................................................................................................13

M4. Management accounting in response to financial problems which leads organisation to

sustainable success...............................................................................................................16

D3. Various planning tools to resolve financial problems...................................................16

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and the essential requirements of different types of management

accounting system..................................................................................................................1

P2. Different methods used for management accounting reporting.......................................3

M1. Evaluation of benefits of management accounting systems...........................................4

D1. Management accounting system and management accounting reporting integrated within

organisational processes.........................................................................................................5

TASK 2 ...........................................................................................................................................5

P3. Appropriate techniques of cost analysis to prepare an income statement........................5

M2. Range of management accounting techniques and producing appropriate financial

reporting documents...............................................................................................................9

D2. Financial reports which are applied to interpret data for business activities...................9

TASK 3............................................................................................................................................9

P4. Uses of different planning tools in management accounting...........................................9

M3. Analysing different planning tools and their applications............................................13

TASK 4..........................................................................................................................................13

P5. The way organisation use management accounting system to respond to financial

problems...............................................................................................................................13

M4. Management accounting in response to financial problems which leads organisation to

sustainable success...............................................................................................................16

D3. Various planning tools to resolve financial problems...................................................16

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION

Management accounting is a system which helps in analysing costs and operations for the

purpose of preparing the internal reports and maintaining the records. Such reports and records

are used by the managers to take critical decisions and formulate day to day plans. Such

accounting is required in any firm to present all the financial as well as non financial

informations for assisting for preparing strategies for future along with growth. To understand

the accounting techniques, Merlin Financial Consultants is selected. The selected consultancy

firm is located at Eagle Street, London, UK and catering its services from the year 1988 which

provides financial services along with assistance and formulates financial future plans for

individual as well as small companies (Banerjee, 2012).

This report consists of detailed information related to management accounting, different

types of management accounting systems, management accounting reports. Further, it includes

cost analysis using appropriate technique for preparing income statement. In addition,

advantages and disadvantages of different types of planning tools for budgetary control and

management accounting approaches used to respond towards the financial problems leading

towards sustainable success.

TASK 1

P1 Management accounting and the essential requirements of different types of management

accounting system

Management accounting: Management accounting is a process of identification,

analysis, measurement, recording, interpretation as well as communication of the financial and

non financial information in the organisation for the purpose of preparing financial statements

and taking decisions for the future along with day to day operations.

Management accounting system: It is framework of preparing the internal reports and

keeping record of financial statements to provide timely as well as accurate information for

planning and controlling the activities to achieve profitability.

Origin, role and principles of management accounting:

Origin: Management accounting has first started its functions during the industrial

revolution in the 19th century. During such period, there was little control of stakeholders and

financial debts along with little need of internal reports. Management accounting acted as an

1

Management accounting is a system which helps in analysing costs and operations for the

purpose of preparing the internal reports and maintaining the records. Such reports and records

are used by the managers to take critical decisions and formulate day to day plans. Such

accounting is required in any firm to present all the financial as well as non financial

informations for assisting for preparing strategies for future along with growth. To understand

the accounting techniques, Merlin Financial Consultants is selected. The selected consultancy

firm is located at Eagle Street, London, UK and catering its services from the year 1988 which

provides financial services along with assistance and formulates financial future plans for

individual as well as small companies (Banerjee, 2012).

This report consists of detailed information related to management accounting, different

types of management accounting systems, management accounting reports. Further, it includes

cost analysis using appropriate technique for preparing income statement. In addition,

advantages and disadvantages of different types of planning tools for budgetary control and

management accounting approaches used to respond towards the financial problems leading

towards sustainable success.

TASK 1

P1 Management accounting and the essential requirements of different types of management

accounting system

Management accounting: Management accounting is a process of identification,

analysis, measurement, recording, interpretation as well as communication of the financial and

non financial information in the organisation for the purpose of preparing financial statements

and taking decisions for the future along with day to day operations.

Management accounting system: It is framework of preparing the internal reports and

keeping record of financial statements to provide timely as well as accurate information for

planning and controlling the activities to achieve profitability.

Origin, role and principles of management accounting:

Origin: Management accounting has first started its functions during the industrial

revolution in the 19th century. During such period, there was little control of stakeholders and

financial debts along with little need of internal reports. Management accounting acted as an

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

essential tool for providing necessary information. With the passage of time, such accounting

speed up its practices and new innovations are formed in their usage.

Role: Management accounting plays significant role in performing the series of various

tasks related to planing, organising, coordinating, controlling, communicating, and interpreting

the financial information for decision making.

Principles: Management accounting includes the following principles:

Influence: Communicates the information which influences the working.

Relevance: Scans the available resources which are relevant to decision making.

Value: Analyses of information which generates value.

Trust: Administration helps in building trust.

Distinguish between management accounting and financial accounting

Basis of distinguish Management accounting Financial accounting

Purpose To provide accurate and timely

information to the managers

for planning, controlling along

with decision making.

To provide the financial

position of the organisation

with other firms.

Focus of information It focuses on financial as well

as non financial information.

Only focuses on financial

information.

Nature Reports are prepared after

considering all the past along

with current performances.

Prepares reports on the basis

of past information.

Different types of management accounting systems

Management accounting systems are the tools which are used for measuring and

evaluating the management operations (Contrafatto and Burns, 2013). Various types of

management accounting systems are the following:

Cost accounting systems: Such system is used to estimate the different costs associated

with the production process. It helps in identifying different ways to reduce these costs

for achieving profits. The essential requirement Merlin Financial Consultants is to record

2

speed up its practices and new innovations are formed in their usage.

Role: Management accounting plays significant role in performing the series of various

tasks related to planing, organising, coordinating, controlling, communicating, and interpreting

the financial information for decision making.

Principles: Management accounting includes the following principles:

Influence: Communicates the information which influences the working.

Relevance: Scans the available resources which are relevant to decision making.

Value: Analyses of information which generates value.

Trust: Administration helps in building trust.

Distinguish between management accounting and financial accounting

Basis of distinguish Management accounting Financial accounting

Purpose To provide accurate and timely

information to the managers

for planning, controlling along

with decision making.

To provide the financial

position of the organisation

with other firms.

Focus of information It focuses on financial as well

as non financial information.

Only focuses on financial

information.

Nature Reports are prepared after

considering all the past along

with current performances.

Prepares reports on the basis

of past information.

Different types of management accounting systems

Management accounting systems are the tools which are used for measuring and

evaluating the management operations (Contrafatto and Burns, 2013). Various types of

management accounting systems are the following:

Cost accounting systems: Such system is used to estimate the different costs associated

with the production process. It helps in identifying different ways to reduce these costs

for achieving profits. The essential requirement Merlin Financial Consultants is to record

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and examine the cost structure by divide the costs of various commodities with different

clients.

Inventory management system: This system is used to monitor and manage the

available inventory or stock with the firm. The essential requirement in chosen

organisation is to implement various strategies for effectively management of the

available stock of capital with its clients by recording of all activities related to inventory

at each level.

Job costing system: Respective system is used by managers to optimize and allocate the

associated costs of different jobs. The essential requirement in the respective firm is to

keep an account of the information related to work completed by an individual along with

team performance.

Price optimising system: Such system is used for determining and optimizing the prices

of products for fulfilling the objective of the business. The essential requirement in the

chosen entity is to understand the perceptions of the clients in relation to prices of the

securities or investment for the purpose of formulating policies.

P2. Different methods used for management accounting reporting

Information relevancy: It is very important for the selected consultancy firm to present the

information according to the requirements of different users. If they are unable to gather and

provide the relevant information then it it is worthless to waste the time. All the information

should be presented to the users must be reliable, accurate, up to date and relevant for decision

making.

The way in which information presented must be understandable because the understandability

helps in preventing any confusions and clearly interpreting the information to others.

Different types of management accounting reports:

Budget report: These are the internal reports prepared by the accountants of selected

organisation for recording, controlling, comparing as well as evaluating the estimated

results with the actual performance during the projected period for taking important

decisions (DRURY, 2013).

Credit control reports: These report are used by the respective business to evaluate

credit limit provided to different in any accounting period. Such reports helps in

highlighting the information of clients to whom more credit is provided for the purpose of

3

clients.

Inventory management system: This system is used to monitor and manage the

available inventory or stock with the firm. The essential requirement in chosen

organisation is to implement various strategies for effectively management of the

available stock of capital with its clients by recording of all activities related to inventory

at each level.

Job costing system: Respective system is used by managers to optimize and allocate the

associated costs of different jobs. The essential requirement in the respective firm is to

keep an account of the information related to work completed by an individual along with

team performance.

Price optimising system: Such system is used for determining and optimizing the prices

of products for fulfilling the objective of the business. The essential requirement in the

chosen entity is to understand the perceptions of the clients in relation to prices of the

securities or investment for the purpose of formulating policies.

P2. Different methods used for management accounting reporting

Information relevancy: It is very important for the selected consultancy firm to present the

information according to the requirements of different users. If they are unable to gather and

provide the relevant information then it it is worthless to waste the time. All the information

should be presented to the users must be reliable, accurate, up to date and relevant for decision

making.

The way in which information presented must be understandable because the understandability

helps in preventing any confusions and clearly interpreting the information to others.

Different types of management accounting reports:

Budget report: These are the internal reports prepared by the accountants of selected

organisation for recording, controlling, comparing as well as evaluating the estimated

results with the actual performance during the projected period for taking important

decisions (DRURY, 2013).

Credit control reports: These report are used by the respective business to evaluate

credit limit provided to different in any accounting period. Such reports helps in

highlighting the information of clients to whom more credit is provided for the purpose of

3

controlling the credit to increase the sales and decreasing debt by improving the cash

flow.

Job cost reports: Such reports are prepared by the managers of chosen entity to exhibit

the actual amount spent for completing any job. The actual amount is compared with the

budgeted value to find any deviations to control cost and increasing the margins of profits

from the jobs with the objective of meeting the overall profitability targets.

Inventory and manufacturing reports: These reports are prepared by the Merlin

Financial Consultants to keep a proper track record the available inventory or stock of

capital with the firm to provide distinct consultancy services to its clients to manufacture

their products and highlighting the hurdles which waste the management time to

understand the breakdown situations.

M1. Evaluation of benefits of management accounting systems

The benefits of management accounting system in context to the Merlin Financial Consultants

are as follows:

Benefits of cost accounting system:

Helps in controlling costs of associated products in the operational processes.

Identifying different ways to reduce these costs for achieving profits.

Benefits of Inventory management system:

Benefits the clients by maintaining and managing the available inventory.

Keeping a proper record helps in achieving efficiency along with productivity in the

working of an organisation.

Benefits of Job costing system:

Tracking the performance of different clients in completion of different job.

Such system helps in assigning the costs in completion of any job.

Benefits of Price optimising system:

It benefits by overall management of prices of different financial products for achieving

profits.

This system helps in understanding the perceptions of the clients towards the securities or

investment for formulation of policies (Fullerton, Kennedy and Widener, 2013).

4

flow.

Job cost reports: Such reports are prepared by the managers of chosen entity to exhibit

the actual amount spent for completing any job. The actual amount is compared with the

budgeted value to find any deviations to control cost and increasing the margins of profits

from the jobs with the objective of meeting the overall profitability targets.

Inventory and manufacturing reports: These reports are prepared by the Merlin

Financial Consultants to keep a proper track record the available inventory or stock of

capital with the firm to provide distinct consultancy services to its clients to manufacture

their products and highlighting the hurdles which waste the management time to

understand the breakdown situations.

M1. Evaluation of benefits of management accounting systems

The benefits of management accounting system in context to the Merlin Financial Consultants

are as follows:

Benefits of cost accounting system:

Helps in controlling costs of associated products in the operational processes.

Identifying different ways to reduce these costs for achieving profits.

Benefits of Inventory management system:

Benefits the clients by maintaining and managing the available inventory.

Keeping a proper record helps in achieving efficiency along with productivity in the

working of an organisation.

Benefits of Job costing system:

Tracking the performance of different clients in completion of different job.

Such system helps in assigning the costs in completion of any job.

Benefits of Price optimising system:

It benefits by overall management of prices of different financial products for achieving

profits.

This system helps in understanding the perceptions of the clients towards the securities or

investment for formulation of policies (Fullerton, Kennedy and Widener, 2013).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

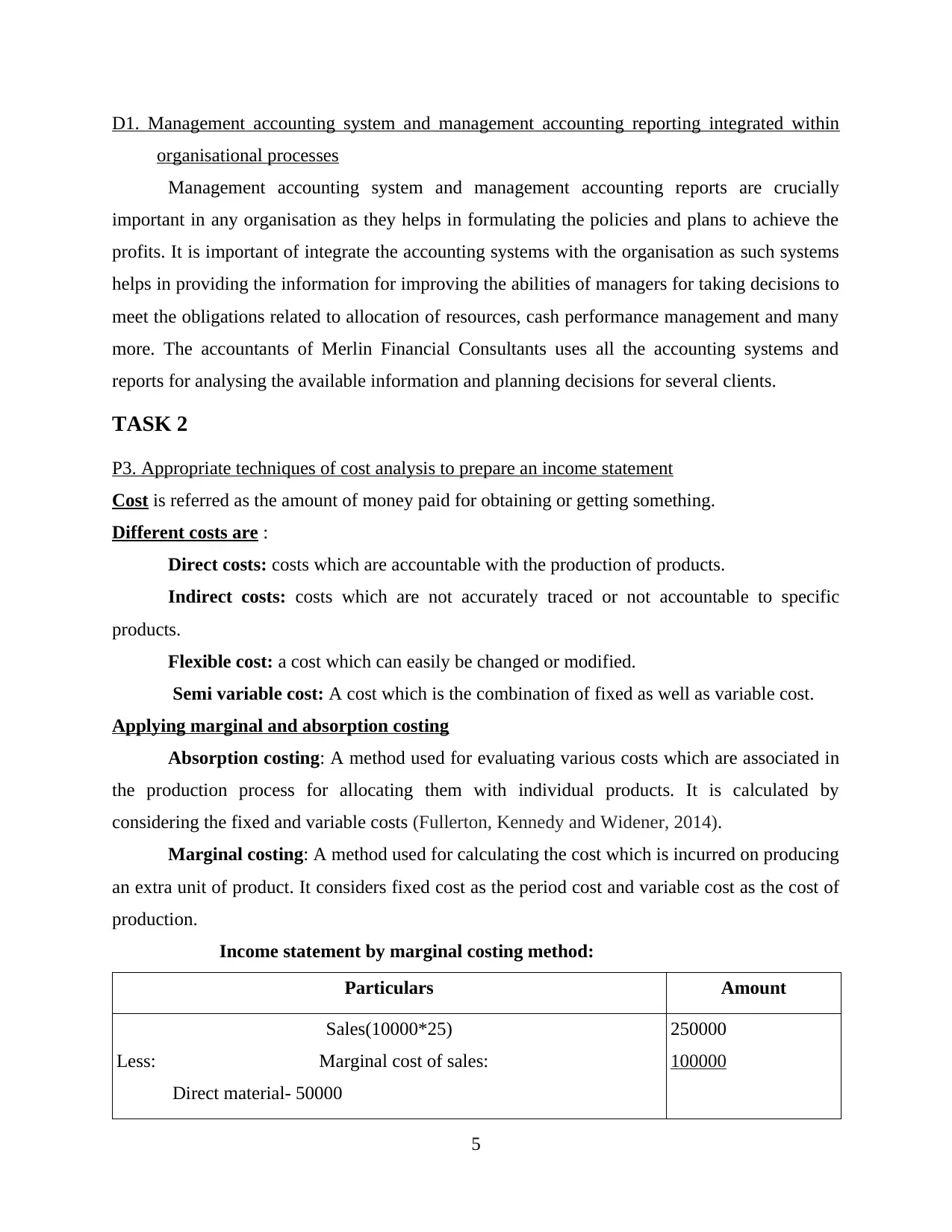

D1. Management accounting system and management accounting reporting integrated within

organisational processes

Management accounting system and management accounting reports are crucially

important in any organisation as they helps in formulating the policies and plans to achieve the

profits. It is important of integrate the accounting systems with the organisation as such systems

helps in providing the information for improving the abilities of managers for taking decisions to

meet the obligations related to allocation of resources, cash performance management and many

more. The accountants of Merlin Financial Consultants uses all the accounting systems and

reports for analysing the available information and planning decisions for several clients.

TASK 2

P3. Appropriate techniques of cost analysis to prepare an income statement

Cost is referred as the amount of money paid for obtaining or getting something.

Different costs are :

Direct costs: costs which are accountable with the production of products.

Indirect costs: costs which are not accurately traced or not accountable to specific

products.

Flexible cost: a cost which can easily be changed or modified.

Semi variable cost: A cost which is the combination of fixed as well as variable cost.

Applying marginal and absorption costing

Absorption costing: A method used for evaluating various costs which are associated in

the production process for allocating them with individual products. It is calculated by

considering the fixed and variable costs (Fullerton, Kennedy and Widener, 2014).

Marginal costing: A method used for calculating the cost which is incurred on producing

an extra unit of product. It considers fixed cost as the period cost and variable cost as the cost of

production.

Income statement by marginal costing method:

Particulars Amount

Sales(10000*25)

Less: Marginal cost of sales:

Direct material- 50000

250000

100000

5

organisational processes

Management accounting system and management accounting reports are crucially

important in any organisation as they helps in formulating the policies and plans to achieve the

profits. It is important of integrate the accounting systems with the organisation as such systems

helps in providing the information for improving the abilities of managers for taking decisions to

meet the obligations related to allocation of resources, cash performance management and many

more. The accountants of Merlin Financial Consultants uses all the accounting systems and

reports for analysing the available information and planning decisions for several clients.

TASK 2

P3. Appropriate techniques of cost analysis to prepare an income statement

Cost is referred as the amount of money paid for obtaining or getting something.

Different costs are :

Direct costs: costs which are accountable with the production of products.

Indirect costs: costs which are not accurately traced or not accountable to specific

products.

Flexible cost: a cost which can easily be changed or modified.

Semi variable cost: A cost which is the combination of fixed as well as variable cost.

Applying marginal and absorption costing

Absorption costing: A method used for evaluating various costs which are associated in

the production process for allocating them with individual products. It is calculated by

considering the fixed and variable costs (Fullerton, Kennedy and Widener, 2014).

Marginal costing: A method used for calculating the cost which is incurred on producing

an extra unit of product. It considers fixed cost as the period cost and variable cost as the cost of

production.

Income statement by marginal costing method:

Particulars Amount

Sales(10000*25)

Less: Marginal cost of sales:

Direct material- 50000

250000

100000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

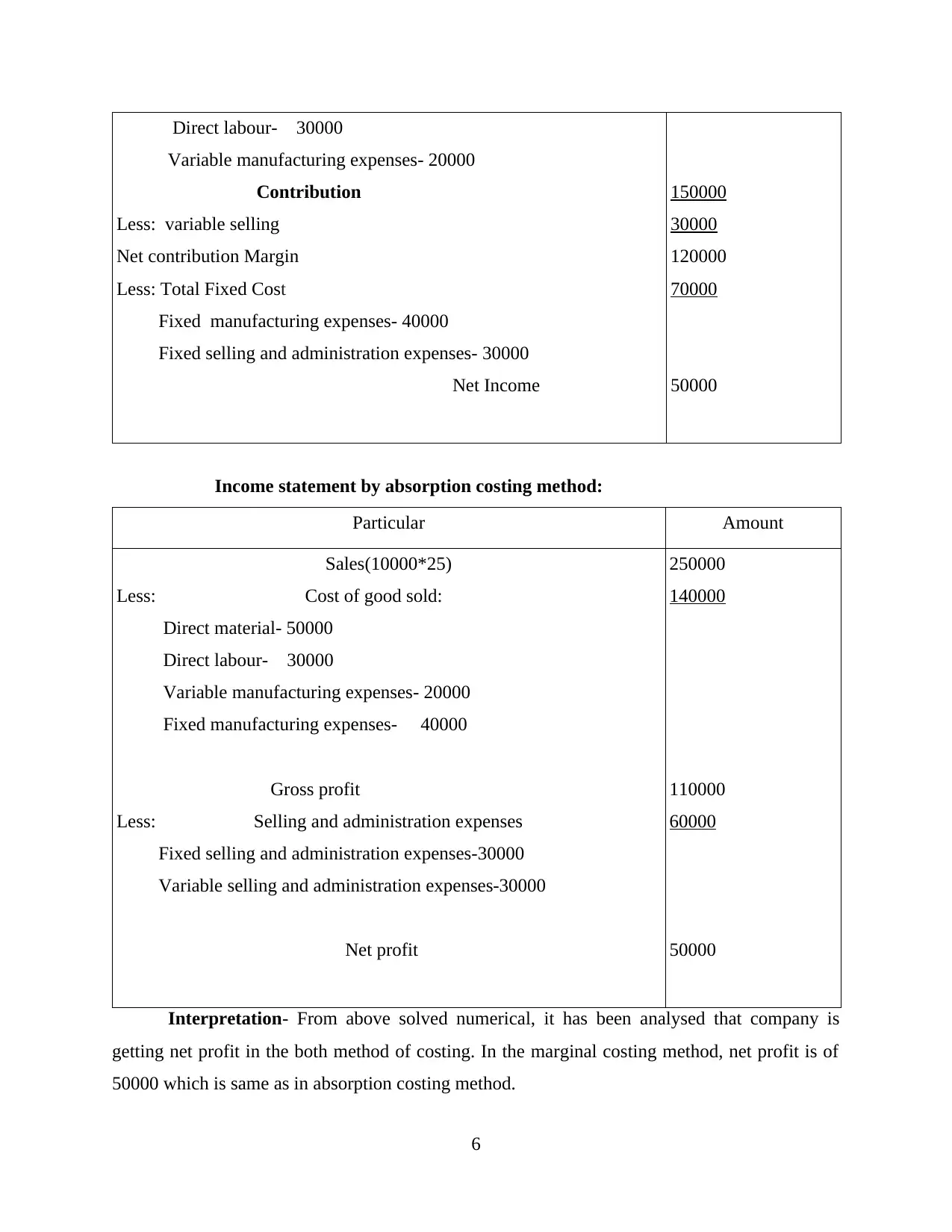

Direct labour- 30000

Variable manufacturing expenses- 20000

Contribution

Less: variable selling

Net contribution Margin

Less: Total Fixed Cost

Fixed manufacturing expenses- 40000

Fixed selling and administration expenses- 30000

Net Income

150000

30000

120000

70000

50000

Income statement by absorption costing method:

Particular Amount

Sales(10000*25)

Less: Cost of good sold:

Direct material- 50000

Direct labour- 30000

Variable manufacturing expenses- 20000

Fixed manufacturing expenses- 40000

Gross profit

Less: Selling and administration expenses

Fixed selling and administration expenses-30000

Variable selling and administration expenses-30000

Net profit

250000

140000

110000

60000

50000

Interpretation- From above solved numerical, it has been analysed that company is

getting net profit in the both method of costing. In the marginal costing method, net profit is of

50000 which is same as in absorption costing method.

6

Variable manufacturing expenses- 20000

Contribution

Less: variable selling

Net contribution Margin

Less: Total Fixed Cost

Fixed manufacturing expenses- 40000

Fixed selling and administration expenses- 30000

Net Income

150000

30000

120000

70000

50000

Income statement by absorption costing method:

Particular Amount

Sales(10000*25)

Less: Cost of good sold:

Direct material- 50000

Direct labour- 30000

Variable manufacturing expenses- 20000

Fixed manufacturing expenses- 40000

Gross profit

Less: Selling and administration expenses

Fixed selling and administration expenses-30000

Variable selling and administration expenses-30000

Net profit

250000

140000

110000

60000

50000

Interpretation- From above solved numerical, it has been analysed that company is

getting net profit in the both method of costing. In the marginal costing method, net profit is of

50000 which is same as in absorption costing method.

6

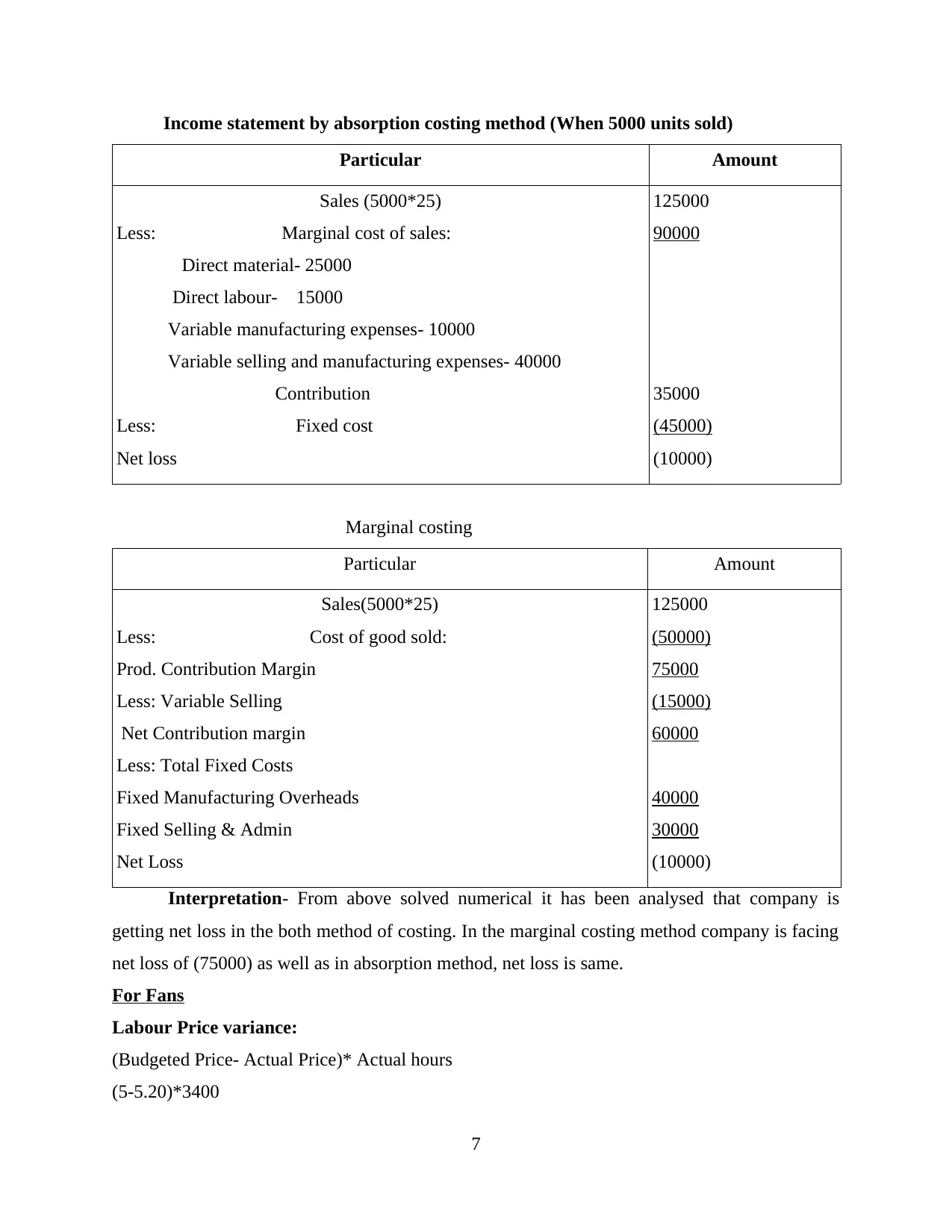

Income statement by absorption costing method (When 5000 units sold)

Particular Amount

Sales (5000*25)

Less: Marginal cost of sales:

Direct material- 25000

Direct labour- 15000

Variable manufacturing expenses- 10000

Variable selling and manufacturing expenses- 40000

Contribution

Less: Fixed cost

Net loss

125000

90000

35000

(45000)

(10000)

Marginal costing

Particular Amount

Sales(5000*25)

Less: Cost of good sold:

Prod. Contribution Margin

Less: Variable Selling

Net Contribution margin

Less: Total Fixed Costs

Fixed Manufacturing Overheads

Fixed Selling & Admin

Net Loss

125000

(50000)

75000

(15000)

60000

40000

30000

(10000)

Interpretation- From above solved numerical it has been analysed that company is

getting net loss in the both method of costing. In the marginal costing method company is facing

net loss of (75000) as well as in absorption method, net loss is same.

For Fans

Labour Price variance:

(Budgeted Price- Actual Price)* Actual hours

(5-5.20)*3400

7

Particular Amount

Sales (5000*25)

Less: Marginal cost of sales:

Direct material- 25000

Direct labour- 15000

Variable manufacturing expenses- 10000

Variable selling and manufacturing expenses- 40000

Contribution

Less: Fixed cost

Net loss

125000

90000

35000

(45000)

(10000)

Marginal costing

Particular Amount

Sales(5000*25)

Less: Cost of good sold:

Prod. Contribution Margin

Less: Variable Selling

Net Contribution margin

Less: Total Fixed Costs

Fixed Manufacturing Overheads

Fixed Selling & Admin

Net Loss

125000

(50000)

75000

(15000)

60000

40000

30000

(10000)

Interpretation- From above solved numerical it has been analysed that company is

getting net loss in the both method of costing. In the marginal costing method company is facing

net loss of (75000) as well as in absorption method, net loss is same.

For Fans

Labour Price variance:

(Budgeted Price- Actual Price)* Actual hours

(5-5.20)*3400

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=-680 (Unfavourable)

Labour usage variance:

(Budgeted Hour -Actual Hours)* Budgeted price

(3000-3400)*5

-2000 (Unfavourable)

For Packaging boxes

Material price variances

(Budgeted price- actual prices)* Actual usage

(10-9.5)*2200

1100 (Favourable)

Material usage variances

(Budgeted use- Actual use)* Budgeted Price

(2000-2200)*10

-2000 (Unfavourable)

Product costing: It can be defined as the cost incurred on producing any product.

Fixed costs: A cost which do not change with the change in production activity.

Variable costs: A cost which changes with the change in the level of activity.

Cost allocation helps in financial reporting and it is used to spread the costs among departments

or inventory items. It is used for calculating profitability.

Normal costing helps in valuation of manufactured products with respect to direct material cost,

the direct labour cost and manufacturing overhead on the basis of predetermination

manufacturing overhead rate (Habib and Hasan, 2018).

Standard costing is used for valuation of manufactured products with a determined material

cost, a planned direct labour cost and planned manufacturing overhead cost.

All the costs plays an crucial role in setting the prices. The prices of any product are set after

considering the costs which are incurred on production of a product.

Inventory cost- such cost is associated with various expenses incurred in production process as

well as for the purpose of sale. There are three types of inventory costs:-

Inventory purchase cost- It is related to procurement of raw materials for producing

new product.

8

Labour usage variance:

(Budgeted Hour -Actual Hours)* Budgeted price

(3000-3400)*5

-2000 (Unfavourable)

For Packaging boxes

Material price variances

(Budgeted price- actual prices)* Actual usage

(10-9.5)*2200

1100 (Favourable)

Material usage variances

(Budgeted use- Actual use)* Budgeted Price

(2000-2200)*10

-2000 (Unfavourable)

Product costing: It can be defined as the cost incurred on producing any product.

Fixed costs: A cost which do not change with the change in production activity.

Variable costs: A cost which changes with the change in the level of activity.

Cost allocation helps in financial reporting and it is used to spread the costs among departments

or inventory items. It is used for calculating profitability.

Normal costing helps in valuation of manufactured products with respect to direct material cost,

the direct labour cost and manufacturing overhead on the basis of predetermination

manufacturing overhead rate (Habib and Hasan, 2018).

Standard costing is used for valuation of manufactured products with a determined material

cost, a planned direct labour cost and planned manufacturing overhead cost.

All the costs plays an crucial role in setting the prices. The prices of any product are set after

considering the costs which are incurred on production of a product.

Inventory cost- such cost is associated with various expenses incurred in production process as

well as for the purpose of sale. There are three types of inventory costs:-

Inventory purchase cost- It is related to procurement of raw materials for producing

new product.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory processing costs- These are related to modifying the existing inventory for the

purpose of further selling.

Inventory distribution cost- It is concerned with expenses incurred in providing the

products for shipping and storing inventory at warehouses before actual sales.

Benefits of reducing inventory costs: It helps in reducing the warehousing storage cost, re

ordering cost which leads to overall cost management.

Valuation methods: It is a way to determine the values of different products of any

organisation.

Cost variances: It is the cost which which determines the differences between actual cost

incurred and planned cost.

Overhead Costs: These are the costs related to the expenses incurred while performing the

operations of any business.

M2. Range of management accounting techniques and producing appropriate financial reporting

documents.

Management accounting techniques are used for the preparation of the management

accounting reports and financial statements. Various techniques helps in accurately forecasting

the practices in present for the future and accordingly formulates strategies. The managers of

respective consultancy firm uses management accounting techniques related to forecasting

planning and historical cost accounting (Herbert and Seal, 2012). Both the techniques plays

crucial function in preparing the financial ass well as non financial reports and important

documents which helps in future financial planning.

D2. Financial reports which are applied to interpret data for business activities

Financial reports are the records of all the tasks and activities performed to achieve the

financial position in the competitive environment. Such reports are presented in systematic

manner to present all business activities in numerical form. The accountants of the chosen

business prepares various financial reports such as inventory and manufacturing reports, job cost

reports, credit control reports, budget report. All these reports helps in formulating the future

plans by interpreting the data or information of the business activities.

9

purpose of further selling.

Inventory distribution cost- It is concerned with expenses incurred in providing the

products for shipping and storing inventory at warehouses before actual sales.

Benefits of reducing inventory costs: It helps in reducing the warehousing storage cost, re

ordering cost which leads to overall cost management.

Valuation methods: It is a way to determine the values of different products of any

organisation.

Cost variances: It is the cost which which determines the differences between actual cost

incurred and planned cost.

Overhead Costs: These are the costs related to the expenses incurred while performing the

operations of any business.

M2. Range of management accounting techniques and producing appropriate financial reporting

documents.

Management accounting techniques are used for the preparation of the management

accounting reports and financial statements. Various techniques helps in accurately forecasting

the practices in present for the future and accordingly formulates strategies. The managers of

respective consultancy firm uses management accounting techniques related to forecasting

planning and historical cost accounting (Herbert and Seal, 2012). Both the techniques plays

crucial function in preparing the financial ass well as non financial reports and important

documents which helps in future financial planning.

D2. Financial reports which are applied to interpret data for business activities

Financial reports are the records of all the tasks and activities performed to achieve the

financial position in the competitive environment. Such reports are presented in systematic

manner to present all business activities in numerical form. The accountants of the chosen

business prepares various financial reports such as inventory and manufacturing reports, job cost

reports, credit control reports, budget report. All these reports helps in formulating the future

plans by interpreting the data or information of the business activities.

9

TASK 3

P4. Uses of different planning tools in management accounting

Planning tools are the means that helps in managing different aspects of business

operations through effective planning. One such tool is Budget which is used by the organisation

in forecasting the expenditure needed to be made for the completion of project and programme.

It also helps in assessing income that will be generated within the certified period. Managers of

Merlin set goals related to finance and performance of organisation and ensures that such

objectives are achieved with in the boundaries of set budget. This process is known as budgetary

control where actual performance is compared with predefined budget and corrections are made

in order to control excessive expenditure (Kotas, 2014).

Process of preparing budget:

Forecasting- This is the first step where incomes and expenditure regarding project is

predicted.

Market research- under this detailed analysis of market is done to identify the potential

threats and opportunities.

Standard costs- This is concerned with estimation of product or process manufacturing

costs.

Reviewing bottlenecks- Problems which can occur during the production process can be

identified and changes can be made.

Software- An effective software needed to be installed so that comparison and analysis

can be made based on past budget.

Different types of budget:-

Capital budget- Such budgets are prepared to assess the expenditure incurred on large

scale projects in order to minimise the losses. It is used to evaluate whether investing on certain

programme with huge amounts would be beneficial or not.

Advantages

It helps in controlling excess expenditure which are of no use. Controlling finances is

necessary as it is the vital requirement for running the business.

Potential threats can be identified which can affect the growth of business.

Evaluation of alternatives will lead to improved decision-making and prospective

alternatives can be selected.

10

P4. Uses of different planning tools in management accounting

Planning tools are the means that helps in managing different aspects of business

operations through effective planning. One such tool is Budget which is used by the organisation

in forecasting the expenditure needed to be made for the completion of project and programme.

It also helps in assessing income that will be generated within the certified period. Managers of

Merlin set goals related to finance and performance of organisation and ensures that such

objectives are achieved with in the boundaries of set budget. This process is known as budgetary

control where actual performance is compared with predefined budget and corrections are made

in order to control excessive expenditure (Kotas, 2014).

Process of preparing budget:

Forecasting- This is the first step where incomes and expenditure regarding project is

predicted.

Market research- under this detailed analysis of market is done to identify the potential

threats and opportunities.

Standard costs- This is concerned with estimation of product or process manufacturing

costs.

Reviewing bottlenecks- Problems which can occur during the production process can be

identified and changes can be made.

Software- An effective software needed to be installed so that comparison and analysis

can be made based on past budget.

Different types of budget:-

Capital budget- Such budgets are prepared to assess the expenditure incurred on large

scale projects in order to minimise the losses. It is used to evaluate whether investing on certain

programme with huge amounts would be beneficial or not.

Advantages

It helps in controlling excess expenditure which are of no use. Controlling finances is

necessary as it is the vital requirement for running the business.

Potential threats can be identified which can affect the growth of business.

Evaluation of alternatives will lead to improved decision-making and prospective

alternatives can be selected.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.