Management Accounting Report: Analysis of C&K Developments Limited

VerifiedAdded on 2020/10/22

|15

|4616

|160

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within C&K Developments Limited, a construction company. It begins with an introduction to management accounting, exploring its concept and essential systems, including inventory management, job order costing, and price planning. The report then delves into various reporting methods, such as item cost reports, budget reports, and pro forma cash flow statements. A significant portion is dedicated to cost analysis techniques, specifically marginal and absorption costing, with detailed calculations of net profit using each method. Furthermore, the report examines the benefits of management accounting systems, their integration within organizational processes, and the advantages and disadvantages of planning tools used in budgetary control. The analysis includes an evaluation of these tools and their application in preparing forecasting budgets and solving financial issues, concluding with a discussion on the role of planning tools in addressing financial problems. The report provides a practical understanding of how management accounting aids decision-making and financial management within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting and essential requirements of its systems....................1

P2 Methods of management accounting reporting......................................................................2

M1 Benefits of management accounting systems and their applications...................................3

D1 Integration of management accounting system and its reports in organisational process....4

TASK 2............................................................................................................................................4

P3 Ascertainment of costs using techniques of cost analysis.....................................................4

M2 Range of management accounting techniques......................................................................6

D2 Interpret data for a range of business activities.....................................................................7

TASK3.............................................................................................................................................7

P4 Advantages and disadvantages of planning tools used in budgetary control.........................7

M3 Analyses of planning tools and their application for preparing forecasting budgets...........8

D3 Evaluation of planning tools.................................................................................................9

TASK 4............................................................................................................................................9

P5 Financial problem and techniques to solve these problem...................................................9

M4 Benefit of management accounting to solve financial problems..........................................9

D3 Planning tools for solving financial issues............................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting and essential requirements of its systems....................1

P2 Methods of management accounting reporting......................................................................2

M1 Benefits of management accounting systems and their applications...................................3

D1 Integration of management accounting system and its reports in organisational process....4

TASK 2............................................................................................................................................4

P3 Ascertainment of costs using techniques of cost analysis.....................................................4

M2 Range of management accounting techniques......................................................................6

D2 Interpret data for a range of business activities.....................................................................7

TASK3.............................................................................................................................................7

P4 Advantages and disadvantages of planning tools used in budgetary control.........................7

M3 Analyses of planning tools and their application for preparing forecasting budgets...........8

D3 Evaluation of planning tools.................................................................................................9

TASK 4............................................................................................................................................9

P5 Financial problem and techniques to solve these problem...................................................9

M4 Benefit of management accounting to solve financial problems..........................................9

D3 Planning tools for solving financial issues............................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a special branch of accounting which deals with managerial

operations and functions performed in an organisation. To better understand the topic of

management accounting, a construction company is selected that is C & K developments limited.

This organisation is a small private limited company which deals in constructing domestic

buildings. Main aim of this report is to identify significance of management accounting concept

by analysing its various techniques and systems. In this project report, various management

accounting systems are analysed along with methods of reporting. Costing techniques such as

marginal and absorption are used to ascertain net profit and break even point. Budgetary control

and its several planning tools are evaluated in order to solve financial issues. Techniques of

producing financial reports are also discussed in this report. Planning tools are analysed along

with their advantages and disadvantages to ensure better treatment of financial issues (Amidu,

Effah and Abor, 2011).

TASK 1

P1 Concept of management accounting and essential requirements of its systems

C & K developments limited is a construction company and as their management

accounting officer, the concept of management accounting and its systems are discussed below

in order to provide reliable information to their general manager.

Management accounting:

It is a process of preparing and presenting managerial accounting information in form of

reports. These accounting operations are the day to day activities which are performed by

personnel of an organisation. This process helps management to analyse business costs which are

incurred in managerial operations. This concept is an aid to managers as it plays a significant

role in decision making. This process is concerned with internal management of a company

(Carlsson-Wall, Kraus and Lind, 2015).

Types of management accounting systems and their essential requirements

Management accounting systems are a framework which provides an overview about

internal information of a company. These systems assists in developing and interpreting this

information so that in can be served to various stakeholders such as employees, directors and

shareholders. Some of these systems along with their requirements are given below:

1

Management accounting is a special branch of accounting which deals with managerial

operations and functions performed in an organisation. To better understand the topic of

management accounting, a construction company is selected that is C & K developments limited.

This organisation is a small private limited company which deals in constructing domestic

buildings. Main aim of this report is to identify significance of management accounting concept

by analysing its various techniques and systems. In this project report, various management

accounting systems are analysed along with methods of reporting. Costing techniques such as

marginal and absorption are used to ascertain net profit and break even point. Budgetary control

and its several planning tools are evaluated in order to solve financial issues. Techniques of

producing financial reports are also discussed in this report. Planning tools are analysed along

with their advantages and disadvantages to ensure better treatment of financial issues (Amidu,

Effah and Abor, 2011).

TASK 1

P1 Concept of management accounting and essential requirements of its systems

C & K developments limited is a construction company and as their management

accounting officer, the concept of management accounting and its systems are discussed below

in order to provide reliable information to their general manager.

Management accounting:

It is a process of preparing and presenting managerial accounting information in form of

reports. These accounting operations are the day to day activities which are performed by

personnel of an organisation. This process helps management to analyse business costs which are

incurred in managerial operations. This concept is an aid to managers as it plays a significant

role in decision making. This process is concerned with internal management of a company

(Carlsson-Wall, Kraus and Lind, 2015).

Types of management accounting systems and their essential requirements

Management accounting systems are a framework which provides an overview about

internal information of a company. These systems assists in developing and interpreting this

information so that in can be served to various stakeholders such as employees, directors and

shareholders. Some of these systems along with their requirements are given below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system – This system helps in managing all the inventory and

stock which is available to the company. Inventory involves raw material, warehoused material,

stock in work in progress and finished goods. In the case of C & K developments limited,

inventory is raw material which is used by company to construct buildings. All the materials of

this company is managed by managers by using techniques of LIFO. Under LIFO technique, last

in stock is used first and under FIFO, first in stock is used first. This system is essentially

required by companies which has ample of inventories (Dražić Lutilsky, 2012).

Job order costing system – This system helps an organisations to record every order

which is received by the organisation. In the case of C & K developments limited, management

of this organisation records all their orders in order to maintain records for cost involvement in

each order and profit acquired from each order.

Price planning system – Under this system, organisations allocate prices to their

different products which are manufactured or distributed by them. In case of C & K

developments limited, this system is essentially required by them as it helps to determine suitable

pricing strategy which should be allocated by them in order to earn profit and satisfy their

clients. This sytem enables planning of prices of products which are manufactured by the

company.

Cost accounting system – This system is concerned with ascertaining various costs

which are involved in organisational operations and activities. Determining cost involvement is a

critical task to perform as this cost is classified into variable, semi variable and fixed cost. C & K

developments limited uses this system to determine cost involved in their operations related to

construction. This system is essentially required by a company as it helps in ascertaining cost in

various activities and projects along with conducting profitability analysis. . This system consists

three types of cost that is normal, standard and actual. Standard costing helps in predicting future

cost involvement whereas normal and actual cost helps in ascertain cost which is actually

incurred by the company.

P2 Methods of management accounting reporting

Management accounting reporting is a process of preparing various reports which consist

information about management and its operations. These reports are prepared by the manager of

C & K developments limited in order to serve them to internal stakeholders such as directors,

snior executives, employees and more. Some of these reporting methods are mentioned below:

2

stock which is available to the company. Inventory involves raw material, warehoused material,

stock in work in progress and finished goods. In the case of C & K developments limited,

inventory is raw material which is used by company to construct buildings. All the materials of

this company is managed by managers by using techniques of LIFO. Under LIFO technique, last

in stock is used first and under FIFO, first in stock is used first. This system is essentially

required by companies which has ample of inventories (Dražić Lutilsky, 2012).

Job order costing system – This system helps an organisations to record every order

which is received by the organisation. In the case of C & K developments limited, management

of this organisation records all their orders in order to maintain records for cost involvement in

each order and profit acquired from each order.

Price planning system – Under this system, organisations allocate prices to their

different products which are manufactured or distributed by them. In case of C & K

developments limited, this system is essentially required by them as it helps to determine suitable

pricing strategy which should be allocated by them in order to earn profit and satisfy their

clients. This sytem enables planning of prices of products which are manufactured by the

company.

Cost accounting system – This system is concerned with ascertaining various costs

which are involved in organisational operations and activities. Determining cost involvement is a

critical task to perform as this cost is classified into variable, semi variable and fixed cost. C & K

developments limited uses this system to determine cost involved in their operations related to

construction. This system is essentially required by a company as it helps in ascertaining cost in

various activities and projects along with conducting profitability analysis. . This system consists

three types of cost that is normal, standard and actual. Standard costing helps in predicting future

cost involvement whereas normal and actual cost helps in ascertain cost which is actually

incurred by the company.

P2 Methods of management accounting reporting

Management accounting reporting is a process of preparing various reports which consist

information about management and its operations. These reports are prepared by the manager of

C & K developments limited in order to serve them to internal stakeholders such as directors,

snior executives, employees and more. Some of these reporting methods are mentioned below:

2

Item cost report – This report is prepared by the management accounting officer of a

company which consists all records for inventories such as opening stock, closing stock and

inventory involved in work in progress. Cost of all the items used in manufacturing the finished

products are recorded in this reporrt. This report even has cost of stock which is incurred by an

organisation. Main aim behind developing this report is to transact all inventories in a report so

that it can be easily accessible whenver it is needed by top management staff of the C & K

developments limited. By developing this report, managers can get access to all the stock which

is avalible to the company to conduct their organisational operations.

Budget report – This report includes all the budgeted and predicted information which is

estimated by managerial acountants of a company. Under this report, various budgets are

prepared in order to ascertain future events, expenses and incomes. In case of C & K

developments limited, management accountants set financial goals which are based on their

projections and estimates. These budgets are prepared by using trend analysis and past

experiences. Main aim behind preparing this report is to serve reliable information to internal

stakeholders about future projections.

Pro forma cash flow - Pro forma cash flow is essential to analyse the shortage of cash in

the future so that company can prepare by obtaining additional debt or equity fund to offset the

estimated shortfall. It is the estimated amount of cash outflows and cash inflows in one or more

period of time in future. C& K development Limited can use this information to develop annual

budgeting and forecasting process and it is prepared for the cash flow information (Granlund,

2011).

Performance report – This report is mainly focused to performance of the company. In

this report performance of employees and overall company is determined in order to determine

efficiency and effectiveness of an organisation. Performance is reffered as efficiency of a

particular employee along with overall performance of a company. In case of C & K

developments limited, manager and HR manager prepares this report in order to serve it to

internal stakeholders such as directors and senior executives.

M1 Benefits of management accounting systems and their applications

System Benefits

Cost accounting system C & K developments limited is benefitted by this system as

3

company which consists all records for inventories such as opening stock, closing stock and

inventory involved in work in progress. Cost of all the items used in manufacturing the finished

products are recorded in this reporrt. This report even has cost of stock which is incurred by an

organisation. Main aim behind developing this report is to transact all inventories in a report so

that it can be easily accessible whenver it is needed by top management staff of the C & K

developments limited. By developing this report, managers can get access to all the stock which

is avalible to the company to conduct their organisational operations.

Budget report – This report includes all the budgeted and predicted information which is

estimated by managerial acountants of a company. Under this report, various budgets are

prepared in order to ascertain future events, expenses and incomes. In case of C & K

developments limited, management accountants set financial goals which are based on their

projections and estimates. These budgets are prepared by using trend analysis and past

experiences. Main aim behind preparing this report is to serve reliable information to internal

stakeholders about future projections.

Pro forma cash flow - Pro forma cash flow is essential to analyse the shortage of cash in

the future so that company can prepare by obtaining additional debt or equity fund to offset the

estimated shortfall. It is the estimated amount of cash outflows and cash inflows in one or more

period of time in future. C& K development Limited can use this information to develop annual

budgeting and forecasting process and it is prepared for the cash flow information (Granlund,

2011).

Performance report – This report is mainly focused to performance of the company. In

this report performance of employees and overall company is determined in order to determine

efficiency and effectiveness of an organisation. Performance is reffered as efficiency of a

particular employee along with overall performance of a company. In case of C & K

developments limited, manager and HR manager prepares this report in order to serve it to

internal stakeholders such as directors and senior executives.

M1 Benefits of management accounting systems and their applications

System Benefits

Cost accounting system C & K developments limited is benefitted by this system as

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

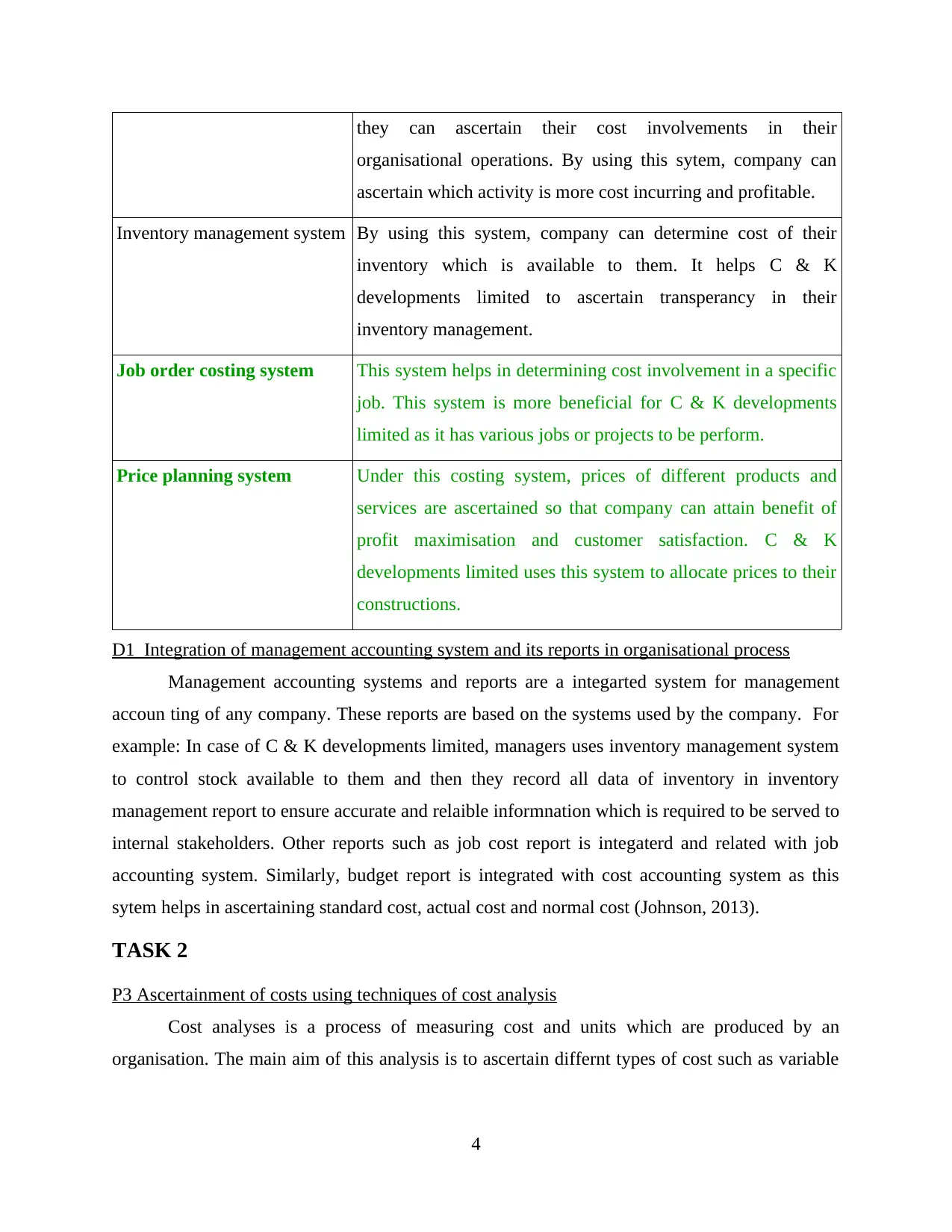

they can ascertain their cost involvements in their

organisational operations. By using this sytem, company can

ascertain which activity is more cost incurring and profitable.

Inventory management system By using this system, company can determine cost of their

inventory which is available to them. It helps C & K

developments limited to ascertain transperancy in their

inventory management.

Job order costing system This system helps in determining cost involvement in a specific

job. This system is more beneficial for C & K developments

limited as it has various jobs or projects to be perform.

Price planning system Under this costing system, prices of different products and

services are ascertained so that company can attain benefit of

profit maximisation and customer satisfaction. C & K

developments limited uses this system to allocate prices to their

constructions.

D1 Integration of management accounting system and its reports in organisational process

Management accounting systems and reports are a integarted system for management

accoun ting of any company. These reports are based on the systems used by the company. For

example: In case of C & K developments limited, managers uses inventory management system

to control stock available to them and then they record all data of inventory in inventory

management report to ensure accurate and relaible informnation which is required to be served to

internal stakeholders. Other reports such as job cost report is integaterd and related with job

accounting system. Similarly, budget report is integrated with cost accounting system as this

sytem helps in ascertaining standard cost, actual cost and normal cost (Johnson, 2013).

TASK 2

P3 Ascertainment of costs using techniques of cost analysis

Cost analyses is a process of measuring cost and units which are produced by an

organisation. The main aim of this analysis is to ascertain differnt types of cost such as variable

4

organisational operations. By using this sytem, company can

ascertain which activity is more cost incurring and profitable.

Inventory management system By using this system, company can determine cost of their

inventory which is available to them. It helps C & K

developments limited to ascertain transperancy in their

inventory management.

Job order costing system This system helps in determining cost involvement in a specific

job. This system is more beneficial for C & K developments

limited as it has various jobs or projects to be perform.

Price planning system Under this costing system, prices of different products and

services are ascertained so that company can attain benefit of

profit maximisation and customer satisfaction. C & K

developments limited uses this system to allocate prices to their

constructions.

D1 Integration of management accounting system and its reports in organisational process

Management accounting systems and reports are a integarted system for management

accoun ting of any company. These reports are based on the systems used by the company. For

example: In case of C & K developments limited, managers uses inventory management system

to control stock available to them and then they record all data of inventory in inventory

management report to ensure accurate and relaible informnation which is required to be served to

internal stakeholders. Other reports such as job cost report is integaterd and related with job

accounting system. Similarly, budget report is integrated with cost accounting system as this

sytem helps in ascertaining standard cost, actual cost and normal cost (Johnson, 2013).

TASK 2

P3 Ascertainment of costs using techniques of cost analysis

Cost analyses is a process of measuring cost and units which are produced by an

organisation. The main aim of this analysis is to ascertain differnt types of cost such as variable

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and fixed which are incurred by a company. Cost analysis has various techniques which helps C

& K developments limited to determine cost involvement such as marginal and variable.

Managers of C & K developments limited uses two types of cost analysis technique.

Using these techniques, cost and net profit is calculated below:

Marginal costing – This costing technique helps a company to determine marginal or

varib ale cost which is incurred by a company in a specific period of time. This technique

completely writes off all fixed assets against contribution. Marginal cost can be determined with

the combination of direct material, direct labout, direct expenses and variable overheads. This

technique helps in classifying fixed and variable cost and alos helps in valuation of inventory.

Main aim behind using this technique is to determine price of their products and ascertain

profitability (Marginal costing. 2018).

Absorption costing – Under this costing technique, manufacturing costs are abosrbed by

units which are produced. In this costing technique, manufacturing costs are deducted from

selling price and all selling and distribution costs are deducted from gross profit earned by the

company. Main aim behind using this costing technique is to ascertain all the costs which are

incurred by the company.

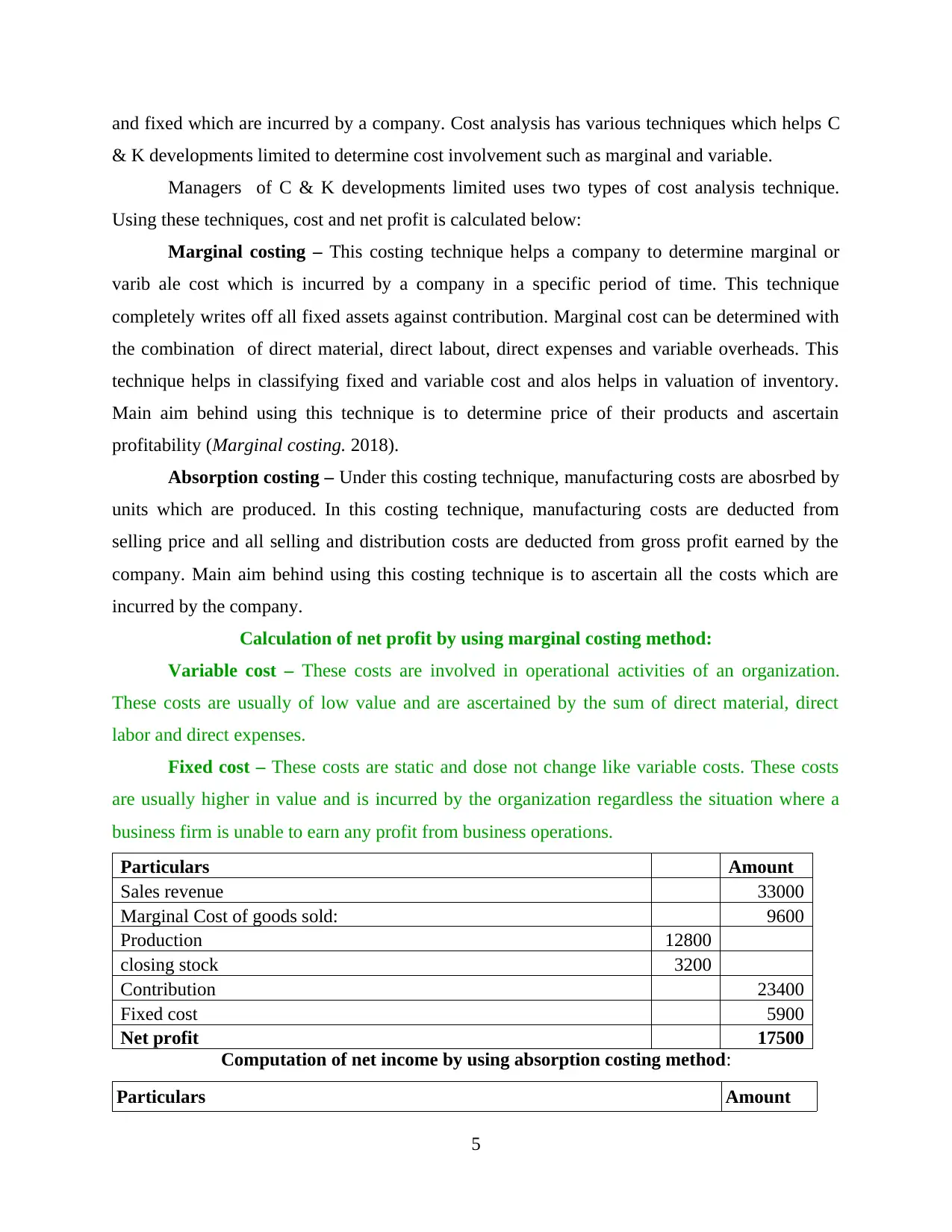

Calculation of net profit by using marginal costing method:

Variable cost – These costs are involved in operational activities of an organization.

These costs are usually of low value and are ascertained by the sum of direct material, direct

labor and direct expenses.

Fixed cost – These costs are static and dose not change like variable costs. These costs

are usually higher in value and is incurred by the organization regardless the situation where a

business firm is unable to earn any profit from business operations.

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

closing stock 3200

Contribution 23400

Fixed cost 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

5

& K developments limited to determine cost involvement such as marginal and variable.

Managers of C & K developments limited uses two types of cost analysis technique.

Using these techniques, cost and net profit is calculated below:

Marginal costing – This costing technique helps a company to determine marginal or

varib ale cost which is incurred by a company in a specific period of time. This technique

completely writes off all fixed assets against contribution. Marginal cost can be determined with

the combination of direct material, direct labout, direct expenses and variable overheads. This

technique helps in classifying fixed and variable cost and alos helps in valuation of inventory.

Main aim behind using this technique is to determine price of their products and ascertain

profitability (Marginal costing. 2018).

Absorption costing – Under this costing technique, manufacturing costs are abosrbed by

units which are produced. In this costing technique, manufacturing costs are deducted from

selling price and all selling and distribution costs are deducted from gross profit earned by the

company. Main aim behind using this costing technique is to ascertain all the costs which are

incurred by the company.

Calculation of net profit by using marginal costing method:

Variable cost – These costs are involved in operational activities of an organization.

These costs are usually of low value and are ascertained by the sum of direct material, direct

labor and direct expenses.

Fixed cost – These costs are static and dose not change like variable costs. These costs

are usually higher in value and is incurred by the organization regardless the situation where a

business firm is unable to earn any profit from business operations.

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

closing stock 3200

Contribution 23400

Fixed cost 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

5

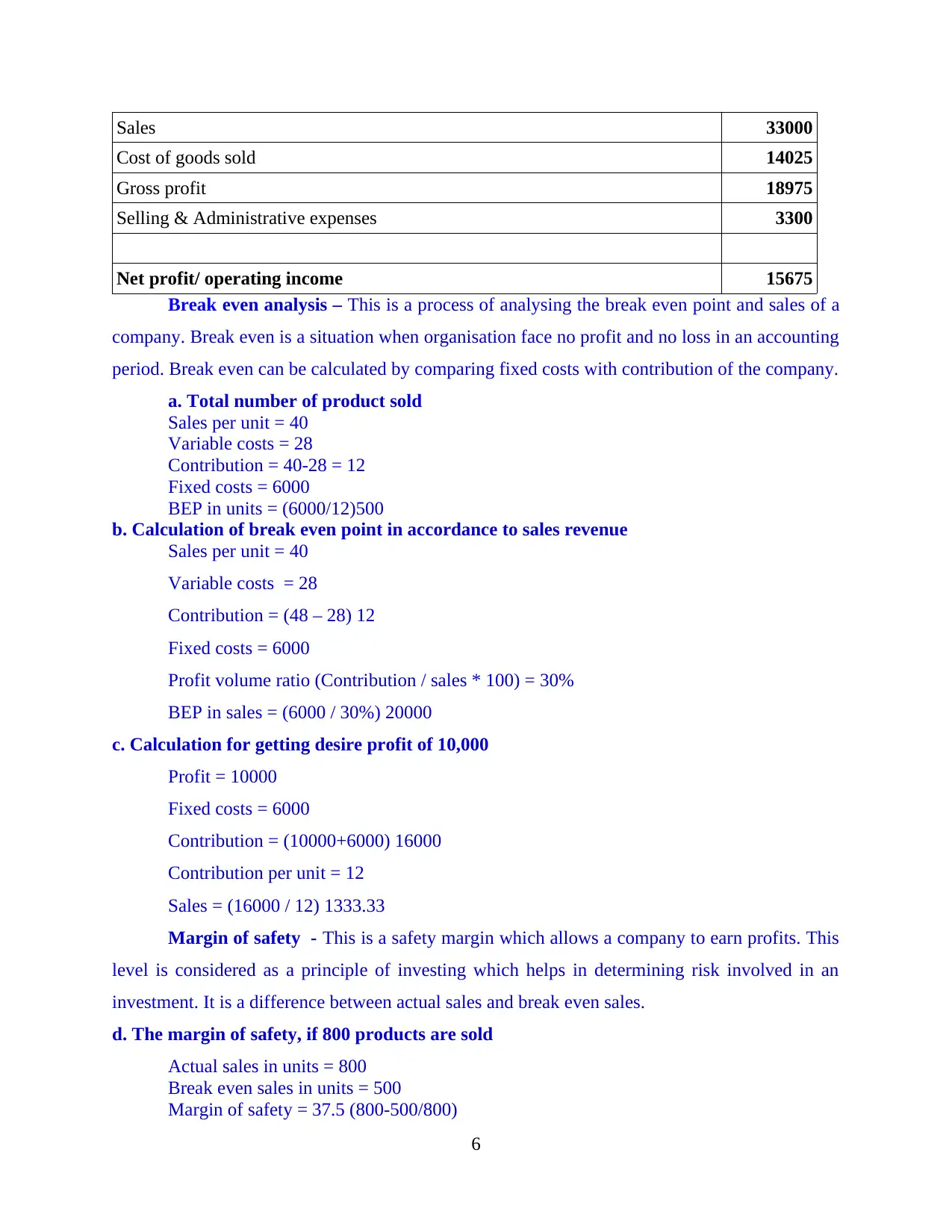

Sales 33000

Cost of goods sold 14025

Gross profit 18975

Selling & Administrative expenses 3300

Net profit/ operating income 15675

Break even analysis – This is a process of analysing the break even point and sales of a

company. Break even is a situation when organisation face no profit and no loss in an accounting

period. Break even can be calculated by comparing fixed costs with contribution of the company.

a. Total number of product sold

Sales per unit = 40

Variable costs = 28

Contribution = 40-28 = 12

Fixed costs = 6000

BEP in units = (6000/12)500

b. Calculation of break even point in accordance to sales revenue

Sales per unit = 40

Variable costs = 28

Contribution = (48 – 28) 12

Fixed costs = 6000

Profit volume ratio (Contribution / sales * 100) = 30%

BEP in sales = (6000 / 30%) 20000

c. Calculation for getting desire profit of 10,000

Profit = 10000

Fixed costs = 6000

Contribution = (10000+6000) 16000

Contribution per unit = 12

Sales = (16000 / 12) 1333.33

Margin of safety - This is a safety margin which allows a company to earn profits. This

level is considered as a principle of investing which helps in determining risk involved in an

investment. It is a difference between actual sales and break even sales.

d. The margin of safety, if 800 products are sold

Actual sales in units = 800

Break even sales in units = 500

Margin of safety = 37.5 (800-500/800)

6

Cost of goods sold 14025

Gross profit 18975

Selling & Administrative expenses 3300

Net profit/ operating income 15675

Break even analysis – This is a process of analysing the break even point and sales of a

company. Break even is a situation when organisation face no profit and no loss in an accounting

period. Break even can be calculated by comparing fixed costs with contribution of the company.

a. Total number of product sold

Sales per unit = 40

Variable costs = 28

Contribution = 40-28 = 12

Fixed costs = 6000

BEP in units = (6000/12)500

b. Calculation of break even point in accordance to sales revenue

Sales per unit = 40

Variable costs = 28

Contribution = (48 – 28) 12

Fixed costs = 6000

Profit volume ratio (Contribution / sales * 100) = 30%

BEP in sales = (6000 / 30%) 20000

c. Calculation for getting desire profit of 10,000

Profit = 10000

Fixed costs = 6000

Contribution = (10000+6000) 16000

Contribution per unit = 12

Sales = (16000 / 12) 1333.33

Margin of safety - This is a safety margin which allows a company to earn profits. This

level is considered as a principle of investing which helps in determining risk involved in an

investment. It is a difference between actual sales and break even sales.

d. The margin of safety, if 800 products are sold

Actual sales in units = 800

Break even sales in units = 500

Margin of safety = 37.5 (800-500/800)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Range of management accounting techniques

Management accounting technqiues are the tools which are used to record and

determine cost which is incurred by a company. C & K developments limited uses marginal cost

which is decsibed below along with historical cost:

Marginal cost – Marginal cost is a tool which helps C & K developments limited to determine

their variable cost and also helps in classifying fixed and marginal cost. By using this tool

company can calculate their cost involvement in organisational operations and activities.

Historical cost – Under this type of management accounting technique, C & K developments

limited records all their assets on historical cost in order to ascertain reliable cost of acquisitions

and depreciation. This technique is used to against replacement cost.

D2 Interpret data for a range of business activities

Cost is determined using two costing methods which is marginal and absorptional. Under

marginal costing technique, net profit is calculated as 17500 whereas according to absorptional

technique, net profit is ascetained as 15675. This difference between the profits of same firm is a

result of abosrption of cost. As in only absorptional costing, both variable and fixed costs are

absorbed.

Break even analysis of this company is also conducted which reflects that break even

point o f this company is 500 units with sales of 20000 dollars. Margin of safety of this company

is 37.5. In order to earn profit of 10000 this company has to manufacture 1333.33 units.

TASK3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget - It is known as the estimation of total cost, earnings and resources that are going

to be incurred in near future time. A budget used to work administrative tools, as it works as

effective plan of action in order to attain organisation aims and objectives in more effective

manner. There are various types of budgets which will be taken into account for the purpose of

managing overall operations of the department. Some of them are operating, cash, sales and

production budgets. A forecasts the financial results and financial performance of a company for

one or more future periods (JOSHI and et. al., 2011).

Budgetary Control:

7

Management accounting technqiues are the tools which are used to record and

determine cost which is incurred by a company. C & K developments limited uses marginal cost

which is decsibed below along with historical cost:

Marginal cost – Marginal cost is a tool which helps C & K developments limited to determine

their variable cost and also helps in classifying fixed and marginal cost. By using this tool

company can calculate their cost involvement in organisational operations and activities.

Historical cost – Under this type of management accounting technique, C & K developments

limited records all their assets on historical cost in order to ascertain reliable cost of acquisitions

and depreciation. This technique is used to against replacement cost.

D2 Interpret data for a range of business activities

Cost is determined using two costing methods which is marginal and absorptional. Under

marginal costing technique, net profit is calculated as 17500 whereas according to absorptional

technique, net profit is ascetained as 15675. This difference between the profits of same firm is a

result of abosrption of cost. As in only absorptional costing, both variable and fixed costs are

absorbed.

Break even analysis of this company is also conducted which reflects that break even

point o f this company is 500 units with sales of 20000 dollars. Margin of safety of this company

is 37.5. In order to earn profit of 10000 this company has to manufacture 1333.33 units.

TASK3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget - It is known as the estimation of total cost, earnings and resources that are going

to be incurred in near future time. A budget used to work administrative tools, as it works as

effective plan of action in order to attain organisation aims and objectives in more effective

manner. There are various types of budgets which will be taken into account for the purpose of

managing overall operations of the department. Some of them are operating, cash, sales and

production budgets. A forecasts the financial results and financial performance of a company for

one or more future periods (JOSHI and et. al., 2011).

Budgetary Control:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is a system of management control in which, actual income and spending are compared

with the standard spending and incomes. It helped C & K developments limited company to

determine whether the arrangement are working according to the set standard. There is certain

useful centre that consists of effective procedure to cop-up with different budget needs.

Production budget:

Production budget can help C&K Development Limited to analyse that how much units

can be produced in one day, one month or year. It is prepared on the basis of sales budget.

Advantages:

It is helpful to ascertain the cost of production.

By analysing and estimating the production budget wastages in production can be

minimise.

Disadvantages:

Accurate cost of production can not be identified through the production budget.

If sales budget of C & KA Development Limited is not appropriate then production

budget can be prepare accurately.

Financial budget:

Financial budget can help C&K Development Limited to estimates the requirements of

finance in the organisation.

Advantages:

It helps to analyse the need of finance for the short and long term in the company.

Disadvantages:

It is not estimated accurately if C&K Development Limited does not know how much amount of

fund is require by the organisation

Planning is one of the necessary tools and techniques that can be taken into consideration

for controlling various issues that are arises in an C & K developments limited. The company

need to control their budget by the help of using various planning tools such as:

Forecasting tools:

It is said to be one of the reliable process of formulating estimated data and their

outcomes for the purpose of evaluating the current trend in the market. It has been found that

estimating for future cannot be too easy because it is uncertain. It is essential for an organisation

to design their future project effectively.

8

with the standard spending and incomes. It helped C & K developments limited company to

determine whether the arrangement are working according to the set standard. There is certain

useful centre that consists of effective procedure to cop-up with different budget needs.

Production budget:

Production budget can help C&K Development Limited to analyse that how much units

can be produced in one day, one month or year. It is prepared on the basis of sales budget.

Advantages:

It is helpful to ascertain the cost of production.

By analysing and estimating the production budget wastages in production can be

minimise.

Disadvantages:

Accurate cost of production can not be identified through the production budget.

If sales budget of C & KA Development Limited is not appropriate then production

budget can be prepare accurately.

Financial budget:

Financial budget can help C&K Development Limited to estimates the requirements of

finance in the organisation.

Advantages:

It helps to analyse the need of finance for the short and long term in the company.

Disadvantages:

It is not estimated accurately if C&K Development Limited does not know how much amount of

fund is require by the organisation

Planning is one of the necessary tools and techniques that can be taken into consideration

for controlling various issues that are arises in an C & K developments limited. The company

need to control their budget by the help of using various planning tools such as:

Forecasting tools:

It is said to be one of the reliable process of formulating estimated data and their

outcomes for the purpose of evaluating the current trend in the market. It has been found that

estimating for future cannot be too easy because it is uncertain. It is essential for an organisation

to design their future project effectively.

8

Advantages - The primary benefits of using this tool is to deliver C & K developments

limited valuable information to business which will be effectively helpful in future

decision making.

Disadvantage - It is entirely relying upon qualitative estimation which will be depend on

subjective inputs thus, not been accountable for long term process.

Contingency tool:

It refers to a course of action designed to assist C & K developments limited respond

effectively to an important future activity that may or may not occur. These types of plans are

general considered as plan B, because it can also be helpful as an alternative for action in case of

any contingent situation arises in an organisation. Like, unexpected requirement for a bandage on

a hike (Klychova, Faskhutdinova and Sadrieva, 2014).

Advantage - It is basically recognising company limitation and formulating to deal with

things that cannot be avoided such as hardware failures and other events.

Disadvantage - Contingency method being complex used to present issues in testing the

precepts of the theory. Like, it is essential that some methodology is available with the

managers in order to make empirical testing.

Scenario tools:

It is an effective management tool that is framed in order to allow an organisation to

analyse the efficacy of various strategies, tactic and plan under a wide range of better future

environments. By this analysis, manager can see how to take actions on the additional costs,

human resource and supply availability within an organisation (Handy and Polimeni, 2017).

M3 Analyses of planning tools and their application for preparing forecasting budgets

Planning tools such as forecasting, contingency and scenario planning tools helps in

preparing budgets for C & K developments limited. Forecating tool is technique which is based

in trend analysis and it helps in estimating future expenses and revebnues which are required to

develop budgets. Other tools such as contingency and scenerio helps in developing future plans

for prevention.

D3 Evaluation of planning tools

Planning tools such as scenario, contingency and forecasting helps in solving financial

issues such as quality of products and performance of employees. C & K developments limited

has a issue with their employees performance due to which they use scenerio planning so that

9

limited valuable information to business which will be effectively helpful in future

decision making.

Disadvantage - It is entirely relying upon qualitative estimation which will be depend on

subjective inputs thus, not been accountable for long term process.

Contingency tool:

It refers to a course of action designed to assist C & K developments limited respond

effectively to an important future activity that may or may not occur. These types of plans are

general considered as plan B, because it can also be helpful as an alternative for action in case of

any contingent situation arises in an organisation. Like, unexpected requirement for a bandage on

a hike (Klychova, Faskhutdinova and Sadrieva, 2014).

Advantage - It is basically recognising company limitation and formulating to deal with

things that cannot be avoided such as hardware failures and other events.

Disadvantage - Contingency method being complex used to present issues in testing the

precepts of the theory. Like, it is essential that some methodology is available with the

managers in order to make empirical testing.

Scenario tools:

It is an effective management tool that is framed in order to allow an organisation to

analyse the efficacy of various strategies, tactic and plan under a wide range of better future

environments. By this analysis, manager can see how to take actions on the additional costs,

human resource and supply availability within an organisation (Handy and Polimeni, 2017).

M3 Analyses of planning tools and their application for preparing forecasting budgets

Planning tools such as forecasting, contingency and scenario planning tools helps in

preparing budgets for C & K developments limited. Forecating tool is technique which is based

in trend analysis and it helps in estimating future expenses and revebnues which are required to

develop budgets. Other tools such as contingency and scenerio helps in developing future plans

for prevention.

D3 Evaluation of planning tools

Planning tools such as scenario, contingency and forecasting helps in solving financial

issues such as quality of products and performance of employees. C & K developments limited

has a issue with their employees performance due to which they use scenerio planning so that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.