Management Accounting Report: Jeffrey & Son's Ltd Analysis

VerifiedAdded on 2020/01/28

|21

|5954

|97

Report

AI Summary

This management accounting report analyzes various costing techniques and budgeting processes using the case of Jeffrey & Son's Ltd. It covers different types of cost classification, including material, labor, and overhead, as well as direct and indirect costs. The report calculates job costs using the job costing method and determines costs using absorption costing. It also prepares and analyzes routine cost reports, applying performance indicators to identify areas for improvement and recommending cost reduction and value enhancement strategies. Furthermore, the report explains the purpose and nature of the budgeting process, selects appropriate budgeting methods, and prepares production, material purchase, and cash budgets. Finally, it computes variances, identifies possible causes, and provides recommendations for corrective actions, along with a reconciliation operating statement and a management report.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Different types of cost classification......................................................................................4

1.2 Calculating of job cost for 200 units using job costing method............................................5

1.3 Determination of Exquisite cost using Absorption Costing Technique.................................6

1.4 Analyzing cost data using appropriate techniques.................................................................8

TASK 2............................................................................................................................................9

2.1 Preparation and analysis of routine cost reports....................................................................9

2.2 Application of performance indicators in order to identify potential improvements in

business......................................................................................................................................11

2.3 Recommendation for cost reduction and value enhancement for business.........................12

TASK 3..........................................................................................................................................13

3.1 Explaining of purpose and nature of the budgeting process................................................13

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

....................................................................................................................................................13

3.3 Preparation of production and material purchase budget....................................................14

3.4 Preparation of cash budget...................................................................................................15

TASK 4..........................................................................................................................................16

4.1 Computation of variances along with the identification of possible causes and

recommendation for corrective actions......................................................................................16

4.2 Preparation of reconciliation operating statement...............................................................17

4.3 Management report in accordance with the identified responsibility centers......................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Different types of cost classification......................................................................................4

1.2 Calculating of job cost for 200 units using job costing method............................................5

1.3 Determination of Exquisite cost using Absorption Costing Technique.................................6

1.4 Analyzing cost data using appropriate techniques.................................................................8

TASK 2............................................................................................................................................9

2.1 Preparation and analysis of routine cost reports....................................................................9

2.2 Application of performance indicators in order to identify potential improvements in

business......................................................................................................................................11

2.3 Recommendation for cost reduction and value enhancement for business.........................12

TASK 3..........................................................................................................................................13

3.1 Explaining of purpose and nature of the budgeting process................................................13

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

....................................................................................................................................................13

3.3 Preparation of production and material purchase budget....................................................14

3.4 Preparation of cash budget...................................................................................................15

TASK 4..........................................................................................................................................16

4.1 Computation of variances along with the identification of possible causes and

recommendation for corrective actions......................................................................................16

4.2 Preparation of reconciliation operating statement...............................................................17

4.3 Management report in accordance with the identified responsibility centers......................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INDEX OF TABLES

Table 1: Calculating of job cost for 200 units..................................................................................6

Table 2: Allocation and apportion of overheads..............................................................................7

Table 3: Reapportion of service departments..................................................................................7

Table 4: Calculation of overhead absorption rates..........................................................................8

Table 5: Routine cost report of September......................................................................................9

Table 6: Computation of standard budget at 1900 units..................................................................9

Table 7: Production budget of Jeffrey and Son's .........................................................................14

Table 8: Material purchase budget of Jeffrey and Son's ...............................................................14

Table 9: Cash budget of Jeffrey and Son's ....................................................................................15

Table 10: Computation of amount receivable from debtors..........................................................15

Table 11: Computation of amount of overhead payment..............................................................15

Table 12: Computation of production cost ...................................................................................15

Table 13: Sales budget...................................................................................................................16

Table 14: Computation of variances of Jeffrey and Son's ............................................................16

Table 15: Reconciliation operating statement of Jeffrey and Son's ..............................................17

Table 1: Calculating of job cost for 200 units..................................................................................6

Table 2: Allocation and apportion of overheads..............................................................................7

Table 3: Reapportion of service departments..................................................................................7

Table 4: Calculation of overhead absorption rates..........................................................................8

Table 5: Routine cost report of September......................................................................................9

Table 6: Computation of standard budget at 1900 units..................................................................9

Table 7: Production budget of Jeffrey and Son's .........................................................................14

Table 8: Material purchase budget of Jeffrey and Son's ...............................................................14

Table 9: Cash budget of Jeffrey and Son's ....................................................................................15

Table 10: Computation of amount receivable from debtors..........................................................15

Table 11: Computation of amount of overhead payment..............................................................15

Table 12: Computation of production cost ...................................................................................15

Table 13: Sales budget...................................................................................................................16

Table 14: Computation of variances of Jeffrey and Son's ............................................................16

Table 15: Reconciliation operating statement of Jeffrey and Son's ..............................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is identified as the important part of business accounting. It

provides significant assistance to management of an organization while handling various tasks

and business operations associated with costing and budgeting. These tools play vital role in

evaluation of wide range of data which is related with cost of production. The rationale behind

the same is to apply cost control and production management strategies that are having

significant impact on the profitability and growth of business entity. By applying different

budgeting approaches, management is able to forecast profitability of company and expenditures

on several business operations (Drury, 2013). By using different type of management accounting

tools such as costing, overhead management, etc., an organization can take appropriate decisions

related to pricing and quality management. It also supports management for developing

appropriate business practices through which effectiveness of different business operations can

be enhanced. Present study carried out is a detail evaluation of wide range of costing techniques

by considering the case of Jeffrey and Son's Ltd. This report is going to evaluate different aspects

of management accounting that are associated with cost and budgets as well as their

implementation as per the given case scenario. This report also determines the role of different

elements of management accounting in decision making process.

TASK 1

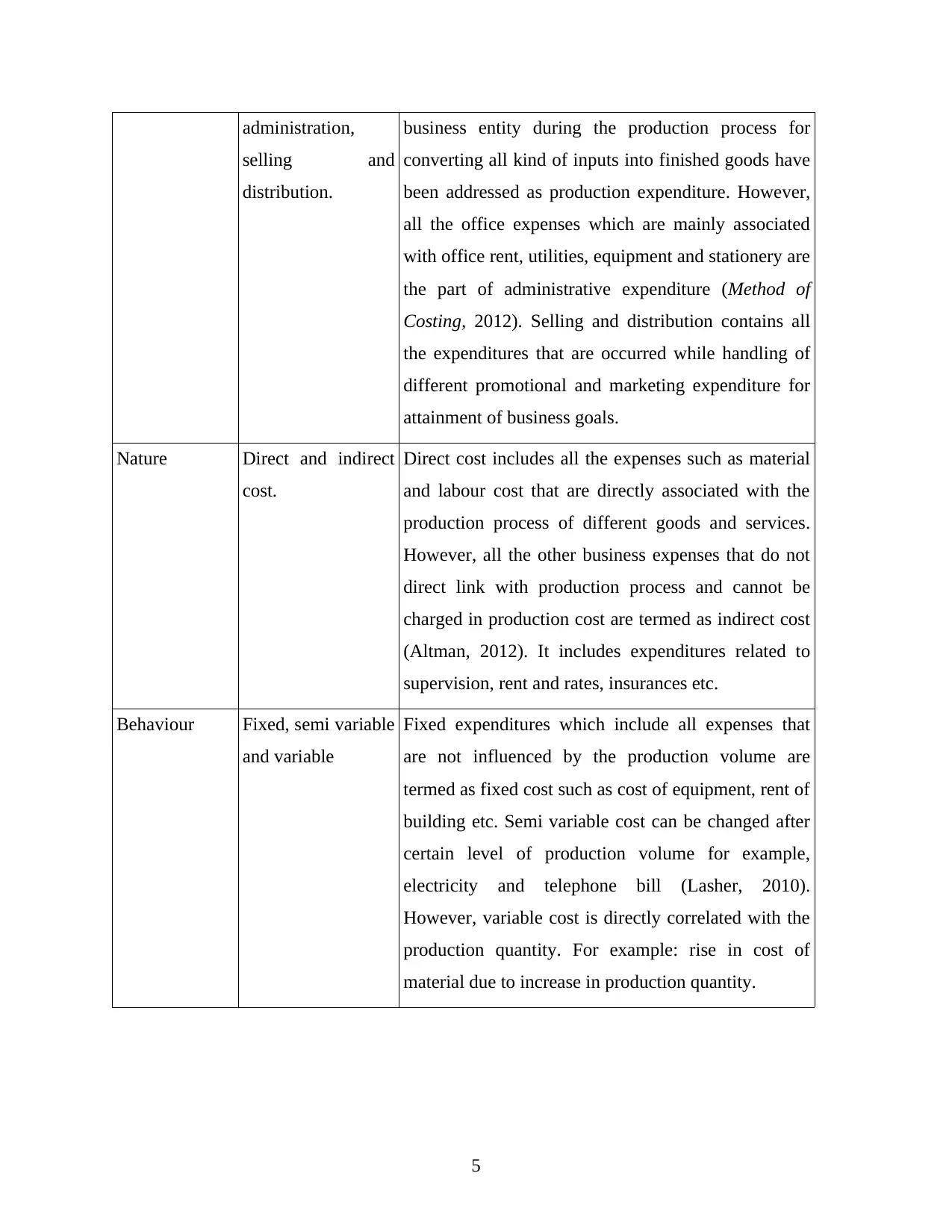

1.1 Different types of cost classification

Basis of

classification

Type of cost Meaning

Elements Material, Labour

and overhead

Material cost is determined as expenditure made by

company for purchasing the raw material. In addition

to that payment of salary, wages and other benefits

are considered as labour cost for organization

(Bennouna, Meredith and Marchant, 201). Apart from

the material and labour cost, all the other expenses

such as factory rent insurance, utilities expenditure

etc. are considered as overhead for company.

Functions Production, All the production expenses which are managed by

4

Management accounting is identified as the important part of business accounting. It

provides significant assistance to management of an organization while handling various tasks

and business operations associated with costing and budgeting. These tools play vital role in

evaluation of wide range of data which is related with cost of production. The rationale behind

the same is to apply cost control and production management strategies that are having

significant impact on the profitability and growth of business entity. By applying different

budgeting approaches, management is able to forecast profitability of company and expenditures

on several business operations (Drury, 2013). By using different type of management accounting

tools such as costing, overhead management, etc., an organization can take appropriate decisions

related to pricing and quality management. It also supports management for developing

appropriate business practices through which effectiveness of different business operations can

be enhanced. Present study carried out is a detail evaluation of wide range of costing techniques

by considering the case of Jeffrey and Son's Ltd. This report is going to evaluate different aspects

of management accounting that are associated with cost and budgets as well as their

implementation as per the given case scenario. This report also determines the role of different

elements of management accounting in decision making process.

TASK 1

1.1 Different types of cost classification

Basis of

classification

Type of cost Meaning

Elements Material, Labour

and overhead

Material cost is determined as expenditure made by

company for purchasing the raw material. In addition

to that payment of salary, wages and other benefits

are considered as labour cost for organization

(Bennouna, Meredith and Marchant, 201). Apart from

the material and labour cost, all the other expenses

such as factory rent insurance, utilities expenditure

etc. are considered as overhead for company.

Functions Production, All the production expenses which are managed by

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

administration,

selling and

distribution.

business entity during the production process for

converting all kind of inputs into finished goods have

been addressed as production expenditure. However,

all the office expenses which are mainly associated

with office rent, utilities, equipment and stationery are

the part of administrative expenditure (Method of

Costing, 2012). Selling and distribution contains all

the expenditures that are occurred while handling of

different promotional and marketing expenditure for

attainment of business goals.

Nature Direct and indirect

cost.

Direct cost includes all the expenses such as material

and labour cost that are directly associated with the

production process of different goods and services.

However, all the other business expenses that do not

direct link with production process and cannot be

charged in production cost are termed as indirect cost

(Altman, 2012). It includes expenditures related to

supervision, rent and rates, insurances etc.

Behaviour Fixed, semi variable

and variable

Fixed expenditures which include all expenses that

are not influenced by the production volume are

termed as fixed cost such as cost of equipment, rent of

building etc. Semi variable cost can be changed after

certain level of production volume for example,

electricity and telephone bill (Lasher, 2010).

However, variable cost is directly correlated with the

production quantity. For example: rise in cost of

material due to increase in production quantity.

5

selling and

distribution.

business entity during the production process for

converting all kind of inputs into finished goods have

been addressed as production expenditure. However,

all the office expenses which are mainly associated

with office rent, utilities, equipment and stationery are

the part of administrative expenditure (Method of

Costing, 2012). Selling and distribution contains all

the expenditures that are occurred while handling of

different promotional and marketing expenditure for

attainment of business goals.

Nature Direct and indirect

cost.

Direct cost includes all the expenses such as material

and labour cost that are directly associated with the

production process of different goods and services.

However, all the other business expenses that do not

direct link with production process and cannot be

charged in production cost are termed as indirect cost

(Altman, 2012). It includes expenditures related to

supervision, rent and rates, insurances etc.

Behaviour Fixed, semi variable

and variable

Fixed expenditures which include all expenses that

are not influenced by the production volume are

termed as fixed cost such as cost of equipment, rent of

building etc. Semi variable cost can be changed after

certain level of production volume for example,

electricity and telephone bill (Lasher, 2010).

However, variable cost is directly correlated with the

production quantity. For example: rise in cost of

material due to increase in production quantity.

5

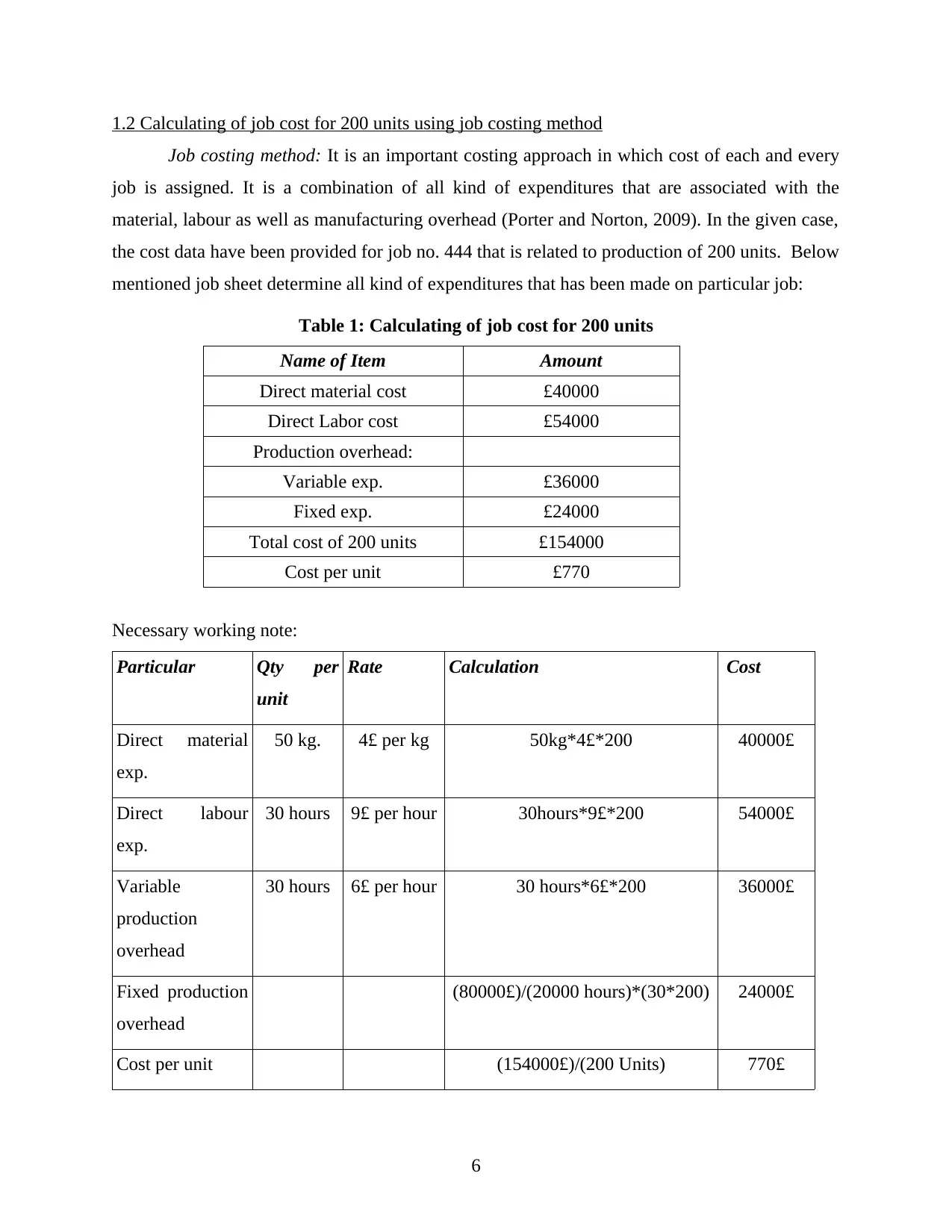

1.2 Calculating of job cost for 200 units using job costing method

Job costing method: It is an important costing approach in which cost of each and every

job is assigned. It is a combination of all kind of expenditures that are associated with the

material, labour as well as manufacturing overhead (Porter and Norton, 2009). In the given case,

the cost data have been provided for job no. 444 that is related to production of 200 units. Below

mentioned job sheet determine all kind of expenditures that has been made on particular job:

Table 1: Calculating of job cost for 200 units

Name of Item Amount

Direct material cost £40000

Direct Labor cost £54000

Production overhead:

Variable exp. £36000

Fixed exp. £24000

Total cost of 200 units £154000

Cost per unit £770

Necessary working note:

Particular Qty per

unit

Rate Calculation Cost

Direct material

exp.

50 kg. 4£ per kg 50kg*4£*200 40000£

Direct labour

exp.

30 hours 9£ per hour 30hours*9£*200 54000£

Variable

production

overhead

30 hours 6£ per hour 30 hours*6£*200 36000£

Fixed production

overhead

(80000£)/(20000 hours)*(30*200) 24000£

Cost per unit (154000£)/(200 Units) 770£

6

Job costing method: It is an important costing approach in which cost of each and every

job is assigned. It is a combination of all kind of expenditures that are associated with the

material, labour as well as manufacturing overhead (Porter and Norton, 2009). In the given case,

the cost data have been provided for job no. 444 that is related to production of 200 units. Below

mentioned job sheet determine all kind of expenditures that has been made on particular job:

Table 1: Calculating of job cost for 200 units

Name of Item Amount

Direct material cost £40000

Direct Labor cost £54000

Production overhead:

Variable exp. £36000

Fixed exp. £24000

Total cost of 200 units £154000

Cost per unit £770

Necessary working note:

Particular Qty per

unit

Rate Calculation Cost

Direct material

exp.

50 kg. 4£ per kg 50kg*4£*200 40000£

Direct labour

exp.

30 hours 9£ per hour 30hours*9£*200 54000£

Variable

production

overhead

30 hours 6£ per hour 30 hours*6£*200 36000£

Fixed production

overhead

(80000£)/(20000 hours)*(30*200) 24000£

Cost per unit (154000£)/(200 Units) 770£

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

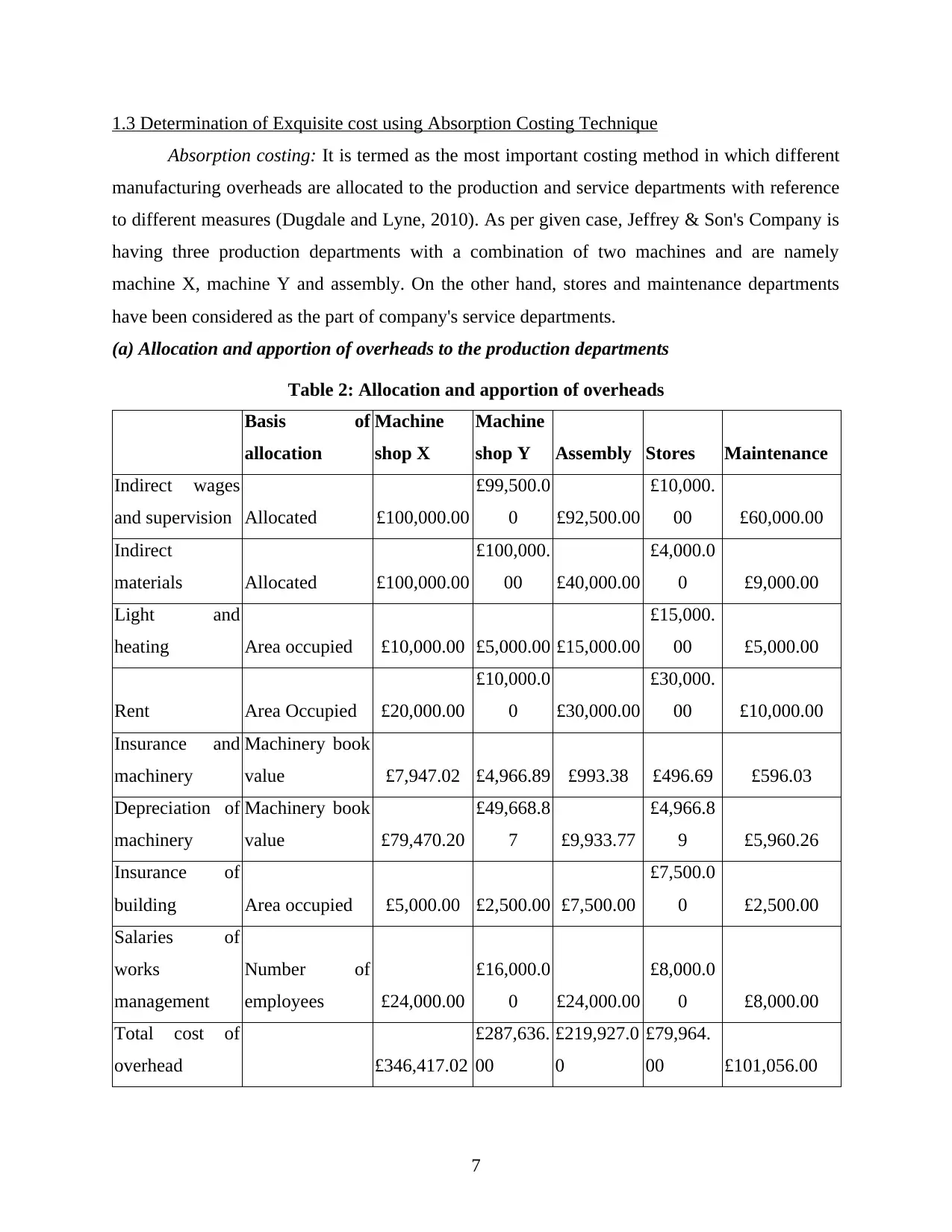

1.3 Determination of Exquisite cost using Absorption Costing Technique

Absorption costing: It is termed as the most important costing method in which different

manufacturing overheads are allocated to the production and service departments with reference

to different measures (Dugdale and Lyne, 2010). As per given case, Jeffrey & Son's Company is

having three production departments with a combination of two machines and are namely

machine X, machine Y and assembly. On the other hand, stores and maintenance departments

have been considered as the part of company's service departments.

(a) Allocation and apportion of overheads to the production departments

Table 2: Allocation and apportion of overheads

Basis of

allocation

Machine

shop X

Machine

shop Y Assembly Stores Maintenance

Indirect wages

and supervision Allocated £100,000.00

£99,500.0

0 £92,500.00

£10,000.

00 £60,000.00

Indirect

materials Allocated £100,000.00

£100,000.

00 £40,000.00

£4,000.0

0 £9,000.00

Light and

heating Area occupied £10,000.00 £5,000.00 £15,000.00

£15,000.

00 £5,000.00

Rent Area Occupied £20,000.00

£10,000.0

0 £30,000.00

£30,000.

00 £10,000.00

Insurance and

machinery

Machinery book

value £7,947.02 £4,966.89 £993.38 £496.69 £596.03

Depreciation of

machinery

Machinery book

value £79,470.20

£49,668.8

7 £9,933.77

£4,966.8

9 £5,960.26

Insurance of

building Area occupied £5,000.00 £2,500.00 £7,500.00

£7,500.0

0 £2,500.00

Salaries of

works

management

Number of

employees £24,000.00

£16,000.0

0 £24,000.00

£8,000.0

0 £8,000.00

Total cost of

overhead £346,417.02

£287,636.

00

£219,927.0

0

£79,964.

00 £101,056.00

7

Absorption costing: It is termed as the most important costing method in which different

manufacturing overheads are allocated to the production and service departments with reference

to different measures (Dugdale and Lyne, 2010). As per given case, Jeffrey & Son's Company is

having three production departments with a combination of two machines and are namely

machine X, machine Y and assembly. On the other hand, stores and maintenance departments

have been considered as the part of company's service departments.

(a) Allocation and apportion of overheads to the production departments

Table 2: Allocation and apportion of overheads

Basis of

allocation

Machine

shop X

Machine

shop Y Assembly Stores Maintenance

Indirect wages

and supervision Allocated £100,000.00

£99,500.0

0 £92,500.00

£10,000.

00 £60,000.00

Indirect

materials Allocated £100,000.00

£100,000.

00 £40,000.00

£4,000.0

0 £9,000.00

Light and

heating Area occupied £10,000.00 £5,000.00 £15,000.00

£15,000.

00 £5,000.00

Rent Area Occupied £20,000.00

£10,000.0

0 £30,000.00

£30,000.

00 £10,000.00

Insurance and

machinery

Machinery book

value £7,947.02 £4,966.89 £993.38 £496.69 £596.03

Depreciation of

machinery

Machinery book

value £79,470.20

£49,668.8

7 £9,933.77

£4,966.8

9 £5,960.26

Insurance of

building Area occupied £5,000.00 £2,500.00 £7,500.00

£7,500.0

0 £2,500.00

Salaries of

works

management

Number of

employees £24,000.00

£16,000.0

0 £24,000.00

£8,000.0

0 £8,000.00

Total cost of

overhead £346,417.02

£287,636.

00

£219,927.0

0

£79,964.

00 £101,056.00

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

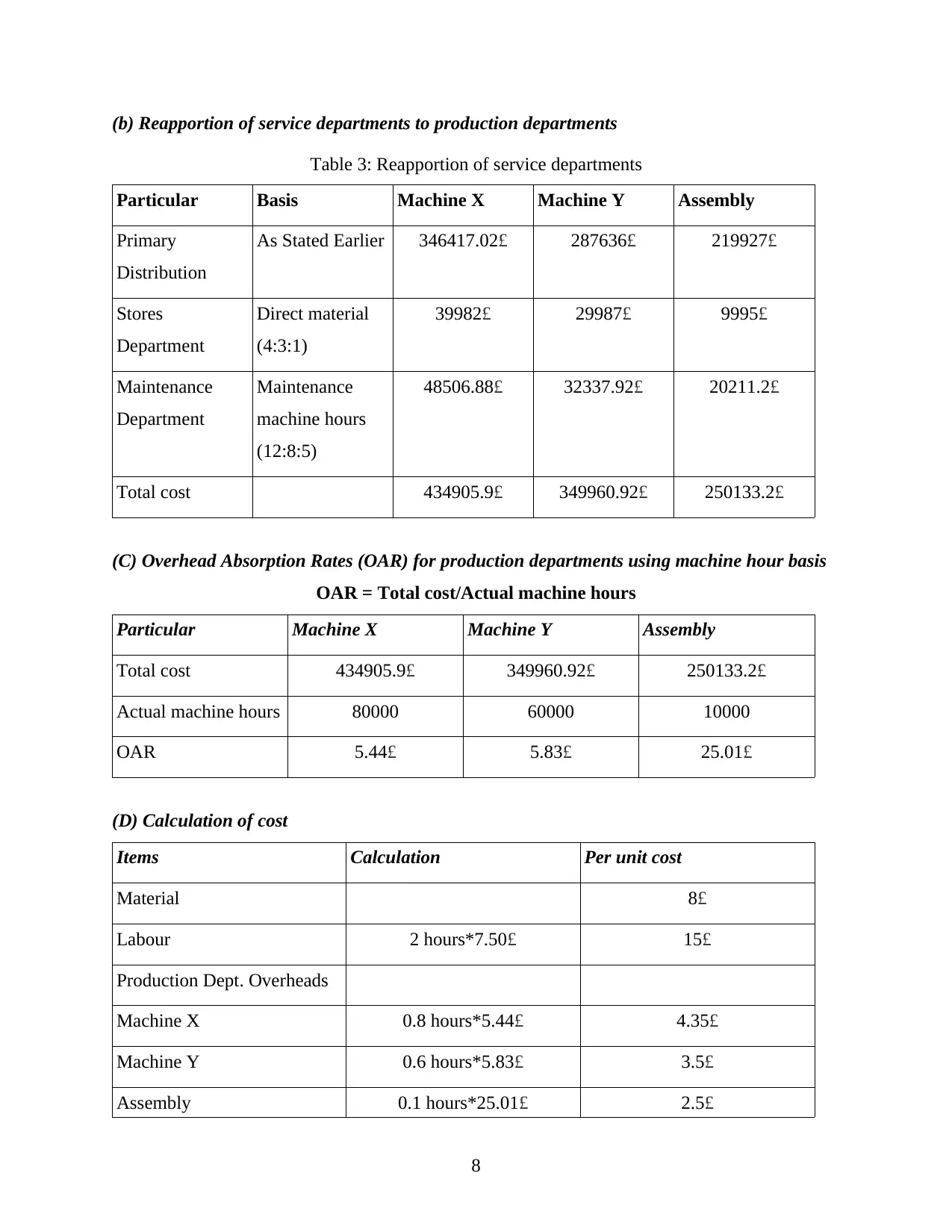

(b) Reapportion of service departments to production departments

Table 3: Reapportion of service departments

Particular Basis Machine X Machine Y Assembly

Primary

Distribution

As Stated Earlier 346417.02£ 287636£ 219927£

Stores

Department

Direct material

(4:3:1)

39982£ 29987£ 9995£

Maintenance

Department

Maintenance

machine hours

(12:8:5)

48506.88£ 32337.92£ 20211.2£

Total cost 434905.9£ 349960.92£ 250133.2£

(C) Overhead Absorption Rates (OAR) for production departments using machine hour basis

OAR = Total cost/Actual machine hours

Particular Machine X Machine Y Assembly

Total cost 434905.9£ 349960.92£ 250133.2£

Actual machine hours 80000 60000 10000

OAR 5.44£ 5.83£ 25.01£

(D) Calculation of cost

Items Calculation Per unit cost

Material 8£

Labour 2 hours*7.50£ 15£

Production Dept. Overheads

Machine X 0.8 hours*5.44£ 4.35£

Machine Y 0.6 hours*5.83£ 3.5£

Assembly 0.1 hours*25.01£ 2.5£

8

Table 3: Reapportion of service departments

Particular Basis Machine X Machine Y Assembly

Primary

Distribution

As Stated Earlier 346417.02£ 287636£ 219927£

Stores

Department

Direct material

(4:3:1)

39982£ 29987£ 9995£

Maintenance

Department

Maintenance

machine hours

(12:8:5)

48506.88£ 32337.92£ 20211.2£

Total cost 434905.9£ 349960.92£ 250133.2£

(C) Overhead Absorption Rates (OAR) for production departments using machine hour basis

OAR = Total cost/Actual machine hours

Particular Machine X Machine Y Assembly

Total cost 434905.9£ 349960.92£ 250133.2£

Actual machine hours 80000 60000 10000

OAR 5.44£ 5.83£ 25.01£

(D) Calculation of cost

Items Calculation Per unit cost

Material 8£

Labour 2 hours*7.50£ 15£

Production Dept. Overheads

Machine X 0.8 hours*5.44£ 4.35£

Machine Y 0.6 hours*5.83£ 3.5£

Assembly 0.1 hours*25.01£ 2.5£

8

Total cost 33.35£

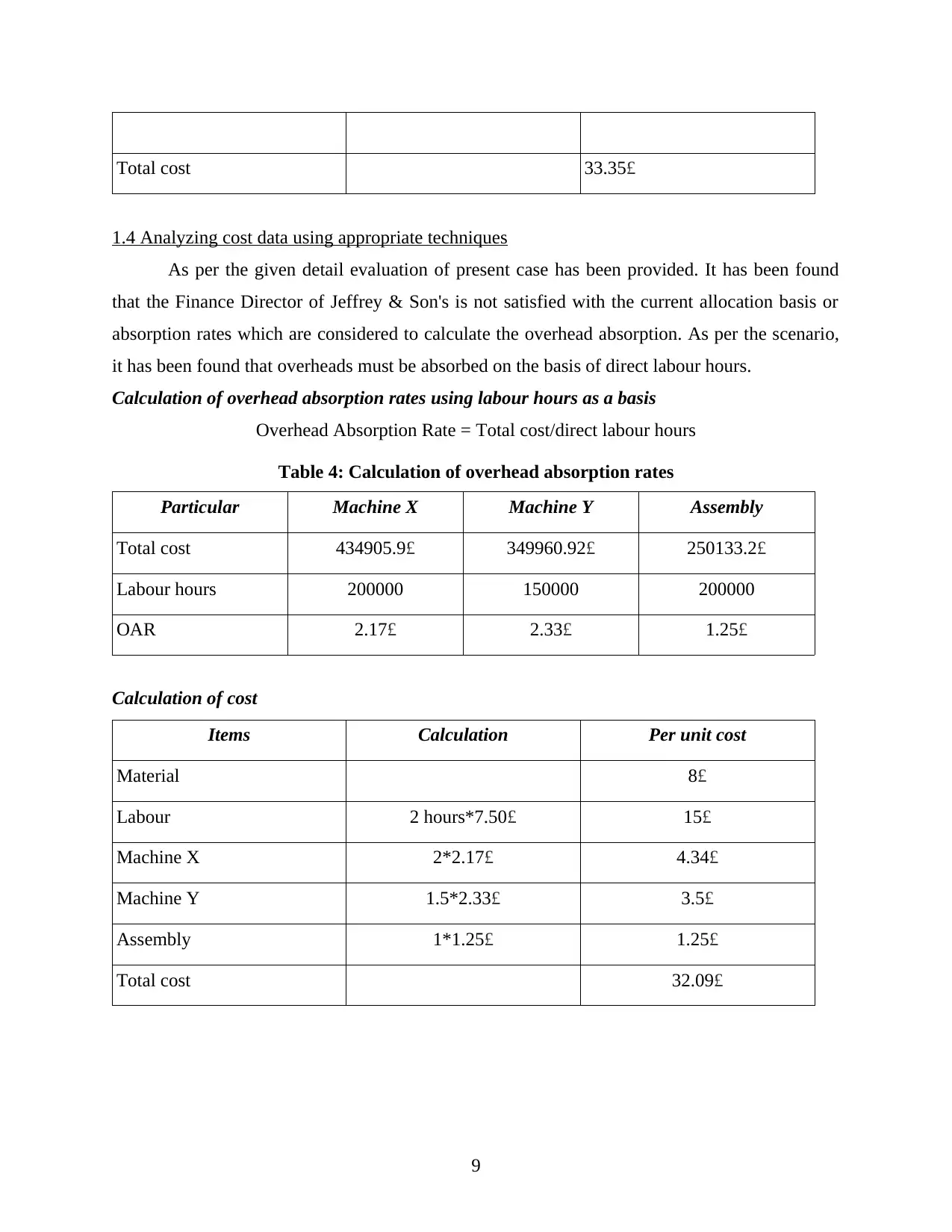

1.4 Analyzing cost data using appropriate techniques

As per the given detail evaluation of present case has been provided. It has been found

that the Finance Director of Jeffrey & Son's is not satisfied with the current allocation basis or

absorption rates which are considered to calculate the overhead absorption. As per the scenario,

it has been found that overheads must be absorbed on the basis of direct labour hours.

Calculation of overhead absorption rates using labour hours as a basis

Overhead Absorption Rate = Total cost/direct labour hours

Table 4: Calculation of overhead absorption rates

Particular Machine X Machine Y Assembly

Total cost 434905.9£ 349960.92£ 250133.2£

Labour hours 200000 150000 200000

OAR 2.17£ 2.33£ 1.25£

Calculation of cost

Items Calculation Per unit cost

Material 8£

Labour 2 hours*7.50£ 15£

Machine X 2*2.17£ 4.34£

Machine Y 1.5*2.33£ 3.5£

Assembly 1*1.25£ 1.25£

Total cost 32.09£

9

1.4 Analyzing cost data using appropriate techniques

As per the given detail evaluation of present case has been provided. It has been found

that the Finance Director of Jeffrey & Son's is not satisfied with the current allocation basis or

absorption rates which are considered to calculate the overhead absorption. As per the scenario,

it has been found that overheads must be absorbed on the basis of direct labour hours.

Calculation of overhead absorption rates using labour hours as a basis

Overhead Absorption Rate = Total cost/direct labour hours

Table 4: Calculation of overhead absorption rates

Particular Machine X Machine Y Assembly

Total cost 434905.9£ 349960.92£ 250133.2£

Labour hours 200000 150000 200000

OAR 2.17£ 2.33£ 1.25£

Calculation of cost

Items Calculation Per unit cost

Material 8£

Labour 2 hours*7.50£ 15£

Machine X 2*2.17£ 4.34£

Machine Y 1.5*2.33£ 3.5£

Assembly 1*1.25£ 1.25£

Total cost 32.09£

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the above assessment, it has been found that labor hour is identified as a good

basis of allocation of overheads. As a result of such decision, the cost per unit gets declined to

32.09£. This is beneficial for the company to reduce its product cost.

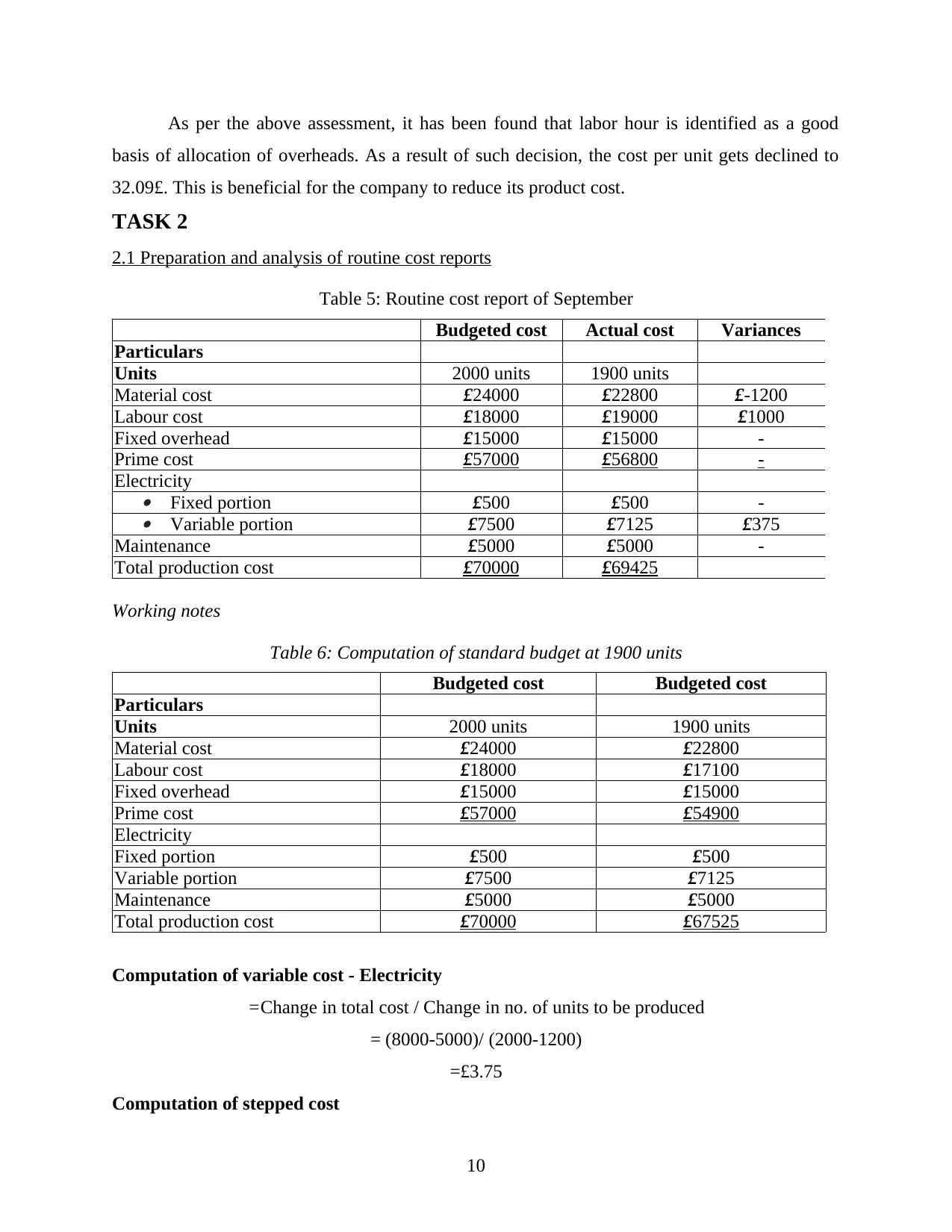

TASK 2

2.1 Preparation and analysis of routine cost reports

Table 5: Routine cost report of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost £24000 £22800 £-1200

Labour cost £18000 £19000 £1000

Fixed overhead £15000 £15000 -

Prime cost £57000 £56800 -

Electricity

Fixed portion £500 £500 -

Variable portion £7500 £7125 £375

Maintenance £5000 £5000 -

Total production cost £70000 £69425

Working notes

Table 6: Computation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

Material cost £24000 £22800

Labour cost £18000 £17100

Fixed overhead £15000 £15000

Prime cost £57000 £54900

Electricity

Fixed portion £500 £500

Variable portion £7500 £7125

Maintenance £5000 £5000

Total production cost £70000 £67525

Computation of variable cost - Electricity

=Change in total cost / Change in no. of units to be produced

= (8000-5000)/ (2000-1200)

=£3.75

Computation of stepped cost

10

basis of allocation of overheads. As a result of such decision, the cost per unit gets declined to

32.09£. This is beneficial for the company to reduce its product cost.

TASK 2

2.1 Preparation and analysis of routine cost reports

Table 5: Routine cost report of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost £24000 £22800 £-1200

Labour cost £18000 £19000 £1000

Fixed overhead £15000 £15000 -

Prime cost £57000 £56800 -

Electricity

Fixed portion £500 £500 -

Variable portion £7500 £7125 £375

Maintenance £5000 £5000 -

Total production cost £70000 £69425

Working notes

Table 6: Computation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

Material cost £24000 £22800

Labour cost £18000 £17100

Fixed overhead £15000 £15000

Prime cost £57000 £54900

Electricity

Fixed portion £500 £500

Variable portion £7500 £7125

Maintenance £5000 £5000

Total production cost £70000 £67525

Computation of variable cost - Electricity

=Change in total cost / Change in no. of units to be produced

= (8000-5000)/ (2000-1200)

=£3.75

Computation of stepped cost

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Maintenance cost can be altered due to it is indentified in the slot of 500. As per the

aspect, it can be stated that there is not significant reduction in cost addressed if company

reduces 100 units.

Comment on variance

Material cost- By considering the outcomes of above calculation, it has been found

favourable variance in amount of material. This reason behind this is that there has not

been any significant alteration addressed in the per unit cost along as well as the nature of

material is also variable so as reduction in production unit is going to create significant

impact on the cost of production (Variance Analysis, 2010).

Labour cost- The above evaluation has found the negative variance in labour cost of 1000

with reference to actual variance which is 1900. Therefore, it can be stated that estimated

per unit cost of labour is 9 that is lower than actual labour cost of 10. As per the variation,

the management of Jeffrey and Son's Ltd should have to manage some extra expenditure

of 1 on each unit. Therefore, the Amount of 900 has to manage in the variance because

computation of budget for 20000 units is carried out with a rate of 9 and actual

computation of 18000 units has been addressed on 10.

Fixed overhead- There is not any kind of variation addressed in the value of fixed

overhead due to fixed overhead are never change as per the production quantity.

Electricity- It is considered as semi variable cost as per the nature. Therefore, this amount

of electricity bills has been evaluated in the form of fixed and variable expense. As per

the above computation, it has been addressed that there is not any kind of change in fixed

portion (Berger, 2011). In the contrary, the value of variable cost is also reduced with

reference to production volume.

Maintenance- Maintenance charges are being applied as a stepped cost that has enhanced

due to increase in slot of 500. Therefore, reduction in production unit by 100 has not

created any huge impact on the maintenance cost.

2.2 Application of performance indicators in order to identify potential improvements in business

There is wide range of performance indicators available for the management of Jeffrey

and Son's through which business entity is able to assess different scope in which advancement

can be made.

11

aspect, it can be stated that there is not significant reduction in cost addressed if company

reduces 100 units.

Comment on variance

Material cost- By considering the outcomes of above calculation, it has been found

favourable variance in amount of material. This reason behind this is that there has not

been any significant alteration addressed in the per unit cost along as well as the nature of

material is also variable so as reduction in production unit is going to create significant

impact on the cost of production (Variance Analysis, 2010).

Labour cost- The above evaluation has found the negative variance in labour cost of 1000

with reference to actual variance which is 1900. Therefore, it can be stated that estimated

per unit cost of labour is 9 that is lower than actual labour cost of 10. As per the variation,

the management of Jeffrey and Son's Ltd should have to manage some extra expenditure

of 1 on each unit. Therefore, the Amount of 900 has to manage in the variance because

computation of budget for 20000 units is carried out with a rate of 9 and actual

computation of 18000 units has been addressed on 10.

Fixed overhead- There is not any kind of variation addressed in the value of fixed

overhead due to fixed overhead are never change as per the production quantity.

Electricity- It is considered as semi variable cost as per the nature. Therefore, this amount

of electricity bills has been evaluated in the form of fixed and variable expense. As per

the above computation, it has been addressed that there is not any kind of change in fixed

portion (Berger, 2011). In the contrary, the value of variable cost is also reduced with

reference to production volume.

Maintenance- Maintenance charges are being applied as a stepped cost that has enhanced

due to increase in slot of 500. Therefore, reduction in production unit by 100 has not

created any huge impact on the maintenance cost.

2.2 Application of performance indicators in order to identify potential improvements in business

There is wide range of performance indicators available for the management of Jeffrey

and Son's through which business entity is able to assess different scope in which advancement

can be made.

11

Evaluation of the product quality- The quality of product and services is termed as most

important element of organizational success that is having direct impact on the growth

and profitability of firm. By carrying out detail evaluation of the product quality and

production process, business entity is able to monitor different operational activities in

which improvements are required as per the current market trends (Hooks and et. al.

2012). This evaluation plays important role in assessment of negative elements of

production process which are hampering overall quality of different kinds of goods and

services. Accounting statements- A systematic evaluation of a variety of accounting statements

such as income statements, balance sheet etc., provides significant assistance to

management of Jeffrey and Son's in assessment of alternation in the financial position of

business entity. If management finds some reduction in the amount of sales as well as

profitability then business entity has to select appropriate strategies in order to increase

profitability (Menifield, 2010). In the contrary, increment in business expenditure is

influenced managers for implementation of changes in business operations. In the process

of change management, accounting statements have played important role for increasing

effectiveness of business decision and monitoring organization performance.

Customer satisfaction- It is one the most essential element for ensuring long term

sustainability of business. By assessing views and suggestion of buyers, business entity

will be able to make appropriate improvements in the product quality as well as service

rendering process. It also supports the management of Jeffrey and Son's for developing

appropriate strategies through which management is able to adapt to appropriate

strategies to increase efficiency of the production process as per the distinct needs of

consumers.

2.3 Recommendation for cost reduction and value enhancement for business

The below mentioned approaches will help management of Jeffrey and Son's in

attainment of the business objectives associated with the cost reduction and profit

enhancement for business-

Techniques Details

Total quality

management

By applying these tools, management will be able to improve all aspects

of business operations that are having direct impact on the quality of

12

important element of organizational success that is having direct impact on the growth

and profitability of firm. By carrying out detail evaluation of the product quality and

production process, business entity is able to monitor different operational activities in

which improvements are required as per the current market trends (Hooks and et. al.

2012). This evaluation plays important role in assessment of negative elements of

production process which are hampering overall quality of different kinds of goods and

services. Accounting statements- A systematic evaluation of a variety of accounting statements

such as income statements, balance sheet etc., provides significant assistance to

management of Jeffrey and Son's in assessment of alternation in the financial position of

business entity. If management finds some reduction in the amount of sales as well as

profitability then business entity has to select appropriate strategies in order to increase

profitability (Menifield, 2010). In the contrary, increment in business expenditure is

influenced managers for implementation of changes in business operations. In the process

of change management, accounting statements have played important role for increasing

effectiveness of business decision and monitoring organization performance.

Customer satisfaction- It is one the most essential element for ensuring long term

sustainability of business. By assessing views and suggestion of buyers, business entity

will be able to make appropriate improvements in the product quality as well as service

rendering process. It also supports the management of Jeffrey and Son's for developing

appropriate strategies through which management is able to adapt to appropriate

strategies to increase efficiency of the production process as per the distinct needs of

consumers.

2.3 Recommendation for cost reduction and value enhancement for business

The below mentioned approaches will help management of Jeffrey and Son's in

attainment of the business objectives associated with the cost reduction and profit

enhancement for business-

Techniques Details

Total quality

management

By applying these tools, management will be able to improve all aspects

of business operations that are having direct impact on the quality of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.