Management Accounting Report: Oakwood Guest House Financial Analysis

VerifiedAdded on 2019/12/18

|17

|5025

|36

Report

AI Summary

This report delves into management accounting practices, specifically focusing on the Oakwood guest house. It begins by outlining different management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report then presents various types of management accounting reports such as budget reports, account receivable aging, inventory and manufacturing reports, job cost reports, and sales reports. The analysis further explores cost calculation techniques, including traditional cost accounting and transfer pricing. Finally, it discusses the merits and demerits of different budgetary planning techniques and the application of management accounting systems to address financial problems within the guest house. The report emphasizes the importance of these tools for decision-making, financial control, and strategic planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different systems of management accounting which are necessary to implement..........1

P2 Different kind of reports used by management accountant...............................................4

TASK 2............................................................................................................................................6

P3 Calculation of costs through appropriate techniques and differences between them.......6

TASK 3..........................................................................................................................................10

P4 Merits and demerits of various budgetary plan techniques.............................................10

P5 Management accounting system used by business to deal with financial problems.......11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different systems of management accounting which are necessary to implement..........1

P2 Different kind of reports used by management accountant...............................................4

TASK 2............................................................................................................................................6

P3 Calculation of costs through appropriate techniques and differences between them.......6

TASK 3..........................................................................................................................................10

P4 Merits and demerits of various budgetary plan techniques.............................................10

P5 Management accounting system used by business to deal with financial problems.......11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a process that is adopted in each small and big firms to make

a report on various activities of business. The report made under management accounting is

formed after making an analysis and detailed interpretation because of which the top level

management cam take decisions after having an overview from the management accounting

reports. The report is usually prepared on monthly basis for all departments and sections of

company so as to take decision on overall basis for entire organisation. The present report is

made on the management accounting in which the chosen company is Oakwood guest house in

which there are maximum 50 members in its workforce where annual turnover is below

£500,000. The report will have a discussion over management accounting and various essential

requirement to make it (Baldvinsdottir, Mitchell and Nørreklit, 2010). Further, the report is going

to make a discussion over the range of methods that are used for management accounting reports.

Besides this, the calculation of costs will be done with the help of different techniques of

absorption and marginal costing ways. Apart from this, the report has the description of merits

and demerits of planning tools have been done which will help in knowing different tools and

methods of planning process.

TASK 1

1.1 Different systems of management accounting which are necessary to implement

To: General Manager, Aron Smith, Oakwood

From: Management Accounting Officer, Marius Marin Iosif

Date: 6th October 2017

Subject: Different types of management accounting systems

The management accounting is a report that is used extensively by the managers and

owners of the business so as to have the information about position of business. These reports

are made on the basis of monthly to weekly basis on which a number of information regarding

cash flows, revenue earnings through sales and outputs, purchase and sell of materials, stocks

etc. Thus, the management accounting is helpful in providing a lot of information to the internal

parties and managers so as to take right decision over various matters (Lukka and Modell,

2010). Here, it is vital to mention that it is opposite to the financial accounting in which the

reports are made to be analysed by the manager in which most of the information is based on

1

Management accounting is a process that is adopted in each small and big firms to make

a report on various activities of business. The report made under management accounting is

formed after making an analysis and detailed interpretation because of which the top level

management cam take decisions after having an overview from the management accounting

reports. The report is usually prepared on monthly basis for all departments and sections of

company so as to take decision on overall basis for entire organisation. The present report is

made on the management accounting in which the chosen company is Oakwood guest house in

which there are maximum 50 members in its workforce where annual turnover is below

£500,000. The report will have a discussion over management accounting and various essential

requirement to make it (Baldvinsdottir, Mitchell and Nørreklit, 2010). Further, the report is going

to make a discussion over the range of methods that are used for management accounting reports.

Besides this, the calculation of costs will be done with the help of different techniques of

absorption and marginal costing ways. Apart from this, the report has the description of merits

and demerits of planning tools have been done which will help in knowing different tools and

methods of planning process.

TASK 1

1.1 Different systems of management accounting which are necessary to implement

To: General Manager, Aron Smith, Oakwood

From: Management Accounting Officer, Marius Marin Iosif

Date: 6th October 2017

Subject: Different types of management accounting systems

The management accounting is a report that is used extensively by the managers and

owners of the business so as to have the information about position of business. These reports

are made on the basis of monthly to weekly basis on which a number of information regarding

cash flows, revenue earnings through sales and outputs, purchase and sell of materials, stocks

etc. Thus, the management accounting is helpful in providing a lot of information to the internal

parties and managers so as to take right decision over various matters (Lukka and Modell,

2010). Here, it is vital to mention that it is opposite to the financial accounting in which the

reports are made to be analysed by the manager in which most of the information is based on

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

historical data. While on other hand, the management accounting report contains the most

recent data because of which it is more relevant in taking decisions for future time period.

Further, it helps the firm in getting the information regarding operating expenses as well

because of which, if the expenses are more, the management will take decision regarding

reduction in the expenditure. The Oakwood guest house employ this method of accounting

extensively so as to make use of available information in preparing budgets and taking other

significant decisions. In addition to this, it acts as a foundation for making different

anticipations related to cost and minimise different types of risk (Garrison and et.al., 2010).

Management accounting: It is the process used by enterprise because it helps the

management in decision making, planning and organising organisational functions in order to

increase effectiveness and efficiency in business operations. The management of Oakwood can

implementing the management accounting as it is beneficial in various processing of business

such as,

Determining the goals and objectives

Increasing cost effectiveness

It helps the organisation in increasing financial returns

It will also help the Oakwood in making changes and maximizing return and

profitability.

The ultimate objectives behind implementing this system in Oakwood in establish the

coordination and cooperation between business operations. Further, it helps the manager in

planning and communication with all the departments of the firm. Thus, the system assist in

making appropriate decision and strategies regarding fluctuations in policies and procedures.

Management accounting system: The system can be useful for the guest house because it

assist in converting the financial data of raw materials, sales, and inventory into an analysis

which helps in determining the accurate information about the company’s position. There are

various types of accounting system which can be implemented by the Oakwood to make its data

reliable and accurate. Some of the system are as follows:

Cost Accounting system: This system is used by management to evaluate the cost of

products and services in order to forecast company’s profitability. This is done to set prices in

order to control the cost functions and to value the inventory appropriately.

Inventory Management system: It helps the company in keeping record of inventory

2

recent data because of which it is more relevant in taking decisions for future time period.

Further, it helps the firm in getting the information regarding operating expenses as well

because of which, if the expenses are more, the management will take decision regarding

reduction in the expenditure. The Oakwood guest house employ this method of accounting

extensively so as to make use of available information in preparing budgets and taking other

significant decisions. In addition to this, it acts as a foundation for making different

anticipations related to cost and minimise different types of risk (Garrison and et.al., 2010).

Management accounting: It is the process used by enterprise because it helps the

management in decision making, planning and organising organisational functions in order to

increase effectiveness and efficiency in business operations. The management of Oakwood can

implementing the management accounting as it is beneficial in various processing of business

such as,

Determining the goals and objectives

Increasing cost effectiveness

It helps the organisation in increasing financial returns

It will also help the Oakwood in making changes and maximizing return and

profitability.

The ultimate objectives behind implementing this system in Oakwood in establish the

coordination and cooperation between business operations. Further, it helps the manager in

planning and communication with all the departments of the firm. Thus, the system assist in

making appropriate decision and strategies regarding fluctuations in policies and procedures.

Management accounting system: The system can be useful for the guest house because it

assist in converting the financial data of raw materials, sales, and inventory into an analysis

which helps in determining the accurate information about the company’s position. There are

various types of accounting system which can be implemented by the Oakwood to make its data

reliable and accurate. Some of the system are as follows:

Cost Accounting system: This system is used by management to evaluate the cost of

products and services in order to forecast company’s profitability. This is done to set prices in

order to control the cost functions and to value the inventory appropriately.

Inventory Management system: It helps the company in keeping record of inventory

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

like, work order bill, raw material, finished product and all the documents regarding production

operations.

Job Costing: It is the process of determining products and services according to its batch

of production. For example, In oakwood when the company will launch its new service it will

cost them differently as per the demand.

Price optimisation System: With the use of this accounting system, company will

determine consumer response towards the pricing of it services which helps the firm in setting

consumer friendly prices. For instance, when Oakwood will change and formulate its services,

it can assume the consumer response by using this which can help the manager in formulating

its price strategy according to customer requirement.

Essential requirements of different types of management accounting systems

It is important for Oakwood to make use of management accounting system in order to

establish stability between management and staff members.

It assists the organisation in serving best services to its customers.

It is required to make effective planning and decisions regarding business functions.

In context of Oakwood guest house, the management accounting systems applied within firm

are:

Traditional cost accounting: The traditional costing method is an accounting method

which is generally used for making a prediction of the profits. For doing calculation, it

takes into account various direct and indirect costs in the business. This methods use to

make a monitoring over the expenditures of the firm and it is generally taken as a

simpler system to be applied for making decisions (Van der Stede, 2011). Besides this, it

is extensively used by those entities who are engaged in the production and similar

activities of a single product. For calculation purpose, in this method, the costs are

allotted to the products on an average basis. Thus, it considers all the indirect costs as

well in the calculation process so as to consider proper cost driver (Weißenberger and

Angelkort, 2011).

Transfer pricing: the transfer pricing attempts to explain various rules and ways for

pricing the transactions that take place between different entities who use to share a

common ownership and control. Thus, when different divisions have to make a

transaction between each other, they use to take help of transfer pricing so as to

3

operations.

Job Costing: It is the process of determining products and services according to its batch

of production. For example, In oakwood when the company will launch its new service it will

cost them differently as per the demand.

Price optimisation System: With the use of this accounting system, company will

determine consumer response towards the pricing of it services which helps the firm in setting

consumer friendly prices. For instance, when Oakwood will change and formulate its services,

it can assume the consumer response by using this which can help the manager in formulating

its price strategy according to customer requirement.

Essential requirements of different types of management accounting systems

It is important for Oakwood to make use of management accounting system in order to

establish stability between management and staff members.

It assists the organisation in serving best services to its customers.

It is required to make effective planning and decisions regarding business functions.

In context of Oakwood guest house, the management accounting systems applied within firm

are:

Traditional cost accounting: The traditional costing method is an accounting method

which is generally used for making a prediction of the profits. For doing calculation, it

takes into account various direct and indirect costs in the business. This methods use to

make a monitoring over the expenditures of the firm and it is generally taken as a

simpler system to be applied for making decisions (Van der Stede, 2011). Besides this, it

is extensively used by those entities who are engaged in the production and similar

activities of a single product. For calculation purpose, in this method, the costs are

allotted to the products on an average basis. Thus, it considers all the indirect costs as

well in the calculation process so as to consider proper cost driver (Weißenberger and

Angelkort, 2011).

Transfer pricing: the transfer pricing attempts to explain various rules and ways for

pricing the transactions that take place between different entities who use to share a

common ownership and control. Thus, when different divisions have to make a

transaction between each other, they use to take help of transfer pricing so as to

3

determine the right cost. The rules and regulations that are applied in transfer pricing

give an opportunity for having better and more transparent pricing so as to give fairness

in all deals and transactions (Modell, 2010). Apart from this, it is evident that in such

types of pricing, the rules applied ion this give provisions for making adjustments in

case of cross border transactions.

P2 Different kind of reports used by management accountant

To: General Manager, Aron Smith, Oakwood

From: Management Accounting Officer, Marius Marin Iosif

Date: 6th October 2017

Subject: Different types of management accounting reports

Oakwood adopts a number of methods for to prepare the management accounting reports

which are as follows:

Budget report: The budget reports are the most commonly used methods that are used by

various business firms of different sectors. The budgets are prepared by the organisations in the

beginning of a month or a year on the basis of predictions related to different incomes and

expenses. In case of small and medium size firms, the manager use to make an analysis of

performance in each department. On the basis of this analysis, estimations are made for incomes

and expenses for a specific time period. This analysis is used for making a budget so that cost

can be controlled. The budgets can be prepared for the present as well as for future time which

also helps in keeping a control over the expenses of the firm. Thus, the budgets are prepared to

keep a track of different cash inflows and outflows so as to prepare the plan for performing

various types of activities (Ward, 2012). The stated enterprise also take help of this approach to

make plans and undertake various activities accordingly.

Account receivable Aging: It is used by the organisation to manage the cash flow for

which company extends the credit limit for its buyers. It assists in identifying from how much

time the customers owe to business. It is used by accountant when the firm faces' difficulty in

cash collection process. Further, it determines that what individual are unable to pay on time

which helps the management in formulating more strict policies accordingly.

Inventory and manufacturing: It is used by Oakwood to make its accounting reports more

efficient because it includes, labour cost, overhead and inventory waste management. It is used

by business to compare assembly lines which can assist the management in improving internal

4

give an opportunity for having better and more transparent pricing so as to give fairness

in all deals and transactions (Modell, 2010). Apart from this, it is evident that in such

types of pricing, the rules applied ion this give provisions for making adjustments in

case of cross border transactions.

P2 Different kind of reports used by management accountant

To: General Manager, Aron Smith, Oakwood

From: Management Accounting Officer, Marius Marin Iosif

Date: 6th October 2017

Subject: Different types of management accounting reports

Oakwood adopts a number of methods for to prepare the management accounting reports

which are as follows:

Budget report: The budget reports are the most commonly used methods that are used by

various business firms of different sectors. The budgets are prepared by the organisations in the

beginning of a month or a year on the basis of predictions related to different incomes and

expenses. In case of small and medium size firms, the manager use to make an analysis of

performance in each department. On the basis of this analysis, estimations are made for incomes

and expenses for a specific time period. This analysis is used for making a budget so that cost

can be controlled. The budgets can be prepared for the present as well as for future time which

also helps in keeping a control over the expenses of the firm. Thus, the budgets are prepared to

keep a track of different cash inflows and outflows so as to prepare the plan for performing

various types of activities (Ward, 2012). The stated enterprise also take help of this approach to

make plans and undertake various activities accordingly.

Account receivable Aging: It is used by the organisation to manage the cash flow for

which company extends the credit limit for its buyers. It assists in identifying from how much

time the customers owe to business. It is used by accountant when the firm faces' difficulty in

cash collection process. Further, it determines that what individual are unable to pay on time

which helps the management in formulating more strict policies accordingly.

Inventory and manufacturing: It is used by Oakwood to make its accounting reports more

efficient because it includes, labour cost, overhead and inventory waste management. It is used

by business to compare assembly lines which can assist the management in improving internal

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of firm.

Job cost reports: The job cost reports are made as per the particular projects and

expresses various expenses related to that project. The estimations that are made on advance

basis is used for making a comparison so that the particular job's profitability can be measured.

On this basis, the managers can easily identify all the profitable areas of business on which the

organisation can make investments to get various profits. Besides this, it helps in getting major

improvements in the business as the managers will save their time by shifting their focus on

more gainful areas rather than wasting time and efforts on the less productive areas. In addition

to this, the job cost reports can also be used as a tool to examine various types of expenses while

the project is in progress. On this basis, the managers can point out all those areas that are

moving in wrong direction so as top correct the deviations.

Sales report: The sales report gives an overview of the total sales that have been made by

the company within a specific period which may be yearly, quarterly or half yearly. The report

contains information regarding the sales volume that is made at a specific time period along with

information on the costs that have been made in a particular duration. Further, the management

takes decision on the basis of sales report regarding the opportunities that are available in the

market (Lazonick, 2012). Thus, the said company keeps all the accurate information on the sales

report and keeps themselves informed regarding the market conditions so as to increase their

sales output. In addition to this, the report also contains information regarding demands of the

product. Thus, a trend can be determined and on this basis, the manager can also have the

knowledge regarding any issue that is making sales of firm less. Apart from this, the market price

can also be determined from this report by the manager.

Cost accounting: The cost accounting reports helps in collecting detailed information on

the cost related activities of the business. The report has all the details which are made on the

basis of classification and evaluation of different alternatives that can be used for putting a

control over costs. On the basis of various reports, the manager keeps a control over operational

budgeting, transfer pricing etc. Thus, the decisions can be made in relation to all those areas

which are required to be modified according to the standard cost structure. This accounting is

also helpful in measuring the performances of the company. Thus, the decisions are made

accordingly by comparing the performance of current year with the previous years' profits (Li,

and Chi, 2013). Moreover, improvements can be made in the cost structure and all those

5

Job cost reports: The job cost reports are made as per the particular projects and

expresses various expenses related to that project. The estimations that are made on advance

basis is used for making a comparison so that the particular job's profitability can be measured.

On this basis, the managers can easily identify all the profitable areas of business on which the

organisation can make investments to get various profits. Besides this, it helps in getting major

improvements in the business as the managers will save their time by shifting their focus on

more gainful areas rather than wasting time and efforts on the less productive areas. In addition

to this, the job cost reports can also be used as a tool to examine various types of expenses while

the project is in progress. On this basis, the managers can point out all those areas that are

moving in wrong direction so as top correct the deviations.

Sales report: The sales report gives an overview of the total sales that have been made by

the company within a specific period which may be yearly, quarterly or half yearly. The report

contains information regarding the sales volume that is made at a specific time period along with

information on the costs that have been made in a particular duration. Further, the management

takes decision on the basis of sales report regarding the opportunities that are available in the

market (Lazonick, 2012). Thus, the said company keeps all the accurate information on the sales

report and keeps themselves informed regarding the market conditions so as to increase their

sales output. In addition to this, the report also contains information regarding demands of the

product. Thus, a trend can be determined and on this basis, the manager can also have the

knowledge regarding any issue that is making sales of firm less. Apart from this, the market price

can also be determined from this report by the manager.

Cost accounting: The cost accounting reports helps in collecting detailed information on

the cost related activities of the business. The report has all the details which are made on the

basis of classification and evaluation of different alternatives that can be used for putting a

control over costs. On the basis of various reports, the manager keeps a control over operational

budgeting, transfer pricing etc. Thus, the decisions can be made in relation to all those areas

which are required to be modified according to the standard cost structure. This accounting is

also helpful in measuring the performances of the company. Thus, the decisions are made

accordingly by comparing the performance of current year with the previous years' profits (Li,

and Chi, 2013). Moreover, improvements can be made in the cost structure and all those

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transactions that involve some pricing so as to manage changes in the inventory.

TASK 2

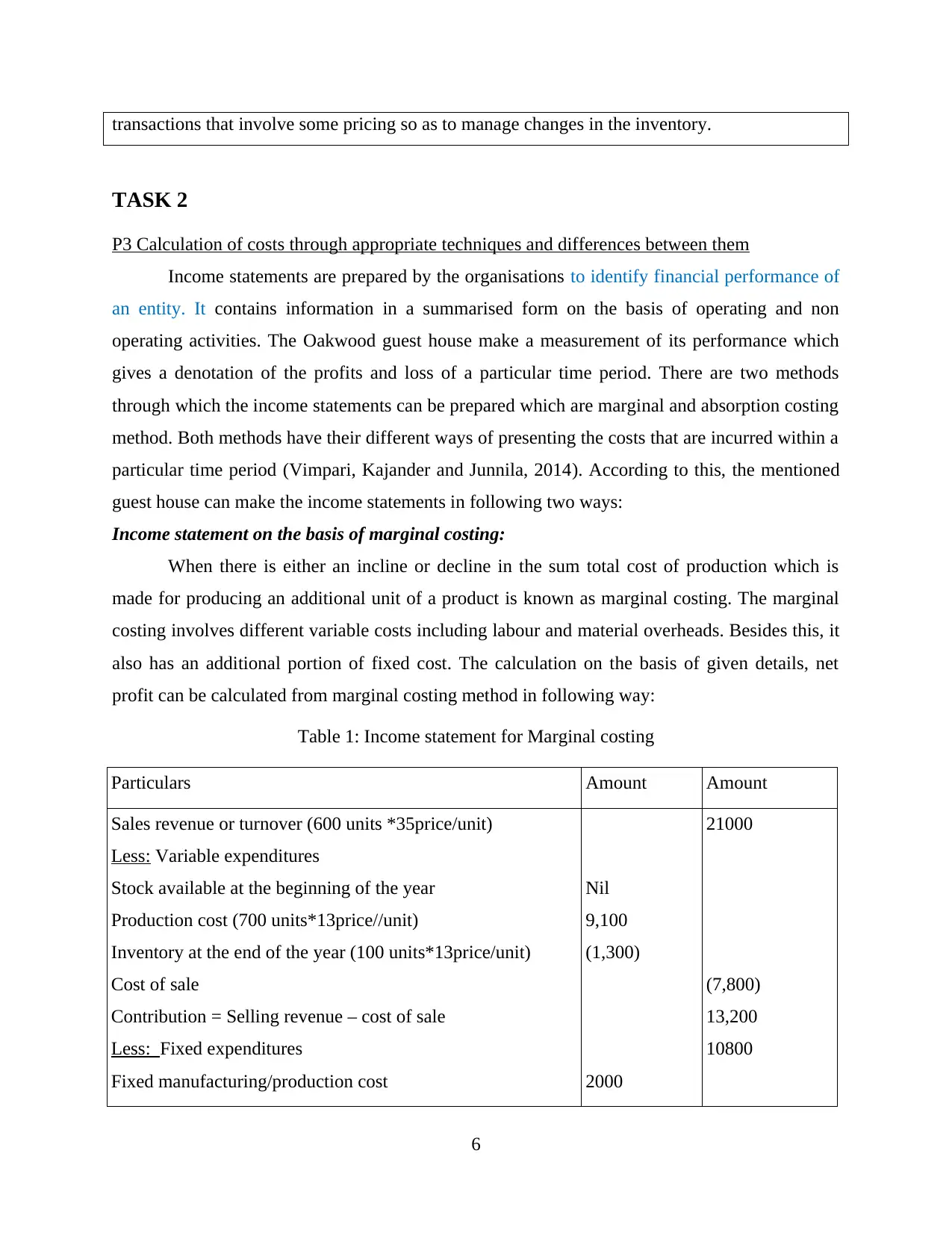

P3 Calculation of costs through appropriate techniques and differences between them

Income statements are prepared by the organisations to identify financial performance of

an entity. It contains information in a summarised form on the basis of operating and non

operating activities. The Oakwood guest house make a measurement of its performance which

gives a denotation of the profits and loss of a particular time period. There are two methods

through which the income statements can be prepared which are marginal and absorption costing

method. Both methods have their different ways of presenting the costs that are incurred within a

particular time period (Vimpari, Kajander and Junnila, 2014). According to this, the mentioned

guest house can make the income statements in following two ways:

Income statement on the basis of marginal costing:

When there is either an incline or decline in the sum total cost of production which is

made for producing an additional unit of a product is known as marginal costing. The marginal

costing involves different variable costs including labour and material overheads. Besides this, it

also has an additional portion of fixed cost. The calculation on the basis of given details, net

profit can be calculated from marginal costing method in following way:

Table 1: Income statement for Marginal costing

Particulars Amount Amount

Sales revenue or turnover (600 units *35price/unit)

Less: Variable expenditures

Stock available at the beginning of the year

Production cost (700 units*13price//unit)

Inventory at the end of the year (100 units*13price/unit)

Cost of sale

Contribution = Selling revenue – cost of sale

Less: Fixed expenditures

Fixed manufacturing/production cost

Nil

9,100

(1,300)

2000

21000

(7,800)

13,200

10800

6

TASK 2

P3 Calculation of costs through appropriate techniques and differences between them

Income statements are prepared by the organisations to identify financial performance of

an entity. It contains information in a summarised form on the basis of operating and non

operating activities. The Oakwood guest house make a measurement of its performance which

gives a denotation of the profits and loss of a particular time period. There are two methods

through which the income statements can be prepared which are marginal and absorption costing

method. Both methods have their different ways of presenting the costs that are incurred within a

particular time period (Vimpari, Kajander and Junnila, 2014). According to this, the mentioned

guest house can make the income statements in following two ways:

Income statement on the basis of marginal costing:

When there is either an incline or decline in the sum total cost of production which is

made for producing an additional unit of a product is known as marginal costing. The marginal

costing involves different variable costs including labour and material overheads. Besides this, it

also has an additional portion of fixed cost. The calculation on the basis of given details, net

profit can be calculated from marginal costing method in following way:

Table 1: Income statement for Marginal costing

Particulars Amount Amount

Sales revenue or turnover (600 units *35price/unit)

Less: Variable expenditures

Stock available at the beginning of the year

Production cost (700 units*13price//unit)

Inventory at the end of the year (100 units*13price/unit)

Cost of sale

Contribution = Selling revenue – cost of sale

Less: Fixed expenditures

Fixed manufacturing/production cost

Nil

9,100

(1,300)

2000

21000

(7,800)

13,200

10800

6

Administration cost

Selling costs

Overheads of sales

Net Profitability / Net loss

700

600

600 (3,900)

9,300

Particulars Cost per unit (In GBP)

Cost of material 6

Cost of labor 5

Cost of variable expenditures 2

Cost each unit 13

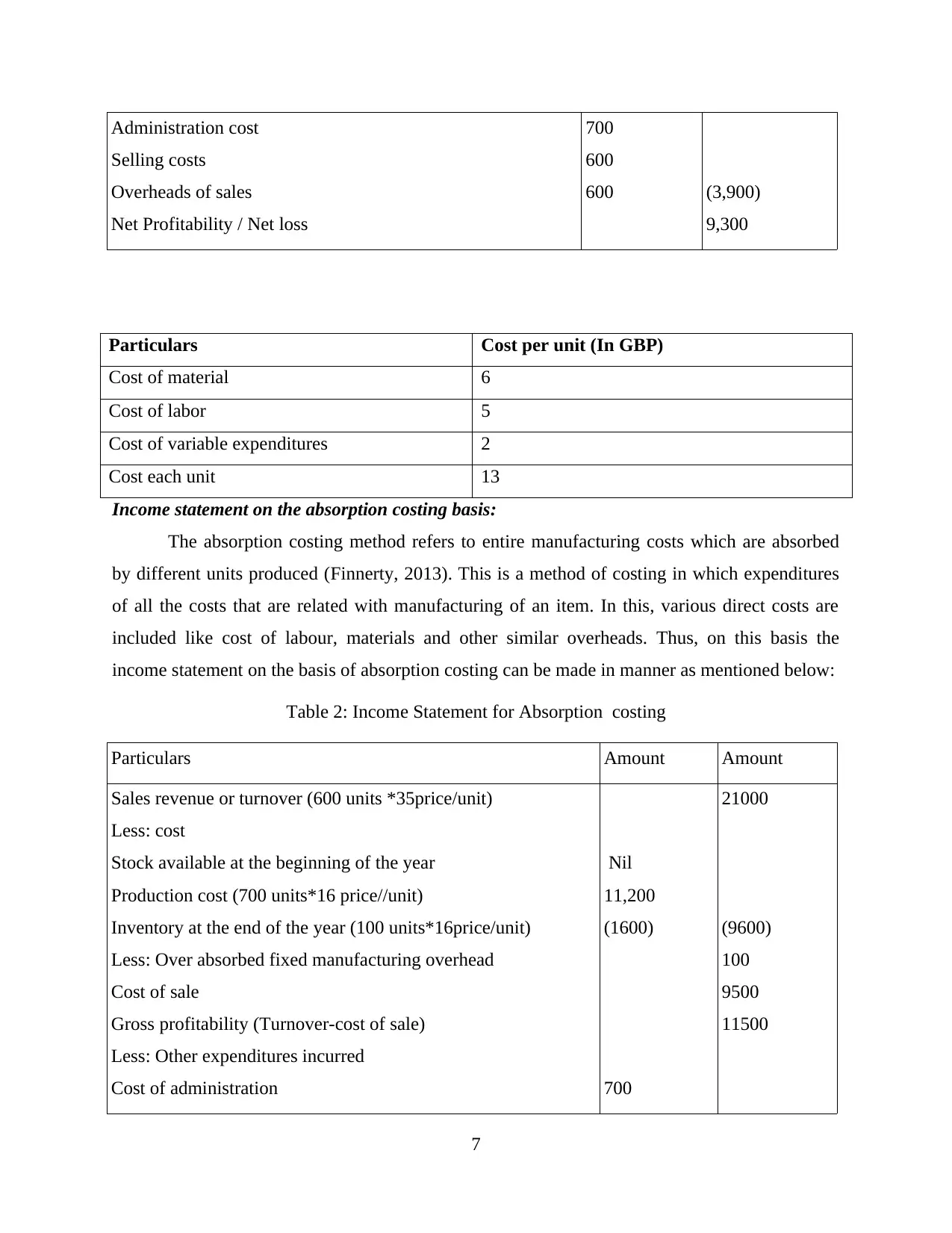

Income statement on the absorption costing basis:

The absorption costing method refers to entire manufacturing costs which are absorbed

by different units produced (Finnerty, 2013). This is a method of costing in which expenditures

of all the costs that are related with manufacturing of an item. In this, various direct costs are

included like cost of labour, materials and other similar overheads. Thus, on this basis the

income statement on the basis of absorption costing can be made in manner as mentioned below:

Table 2: Income Statement for Absorption costing

Particulars Amount Amount

Sales revenue or turnover (600 units *35price/unit)

Less: cost

Stock available at the beginning of the year

Production cost (700 units*16 price//unit)

Inventory at the end of the year (100 units*16price/unit)

Less: Over absorbed fixed manufacturing overhead

Cost of sale

Gross profitability (Turnover-cost of sale)

Less: Other expenditures incurred

Cost of administration

Nil

11,200

(1600)

700

21000

(9600)

100

9500

11500

7

Selling costs

Overheads of sales

Net Profitability / Net loss

700

600

600 (3,900)

9,300

Particulars Cost per unit (In GBP)

Cost of material 6

Cost of labor 5

Cost of variable expenditures 2

Cost each unit 13

Income statement on the absorption costing basis:

The absorption costing method refers to entire manufacturing costs which are absorbed

by different units produced (Finnerty, 2013). This is a method of costing in which expenditures

of all the costs that are related with manufacturing of an item. In this, various direct costs are

included like cost of labour, materials and other similar overheads. Thus, on this basis the

income statement on the basis of absorption costing can be made in manner as mentioned below:

Table 2: Income Statement for Absorption costing

Particulars Amount Amount

Sales revenue or turnover (600 units *35price/unit)

Less: cost

Stock available at the beginning of the year

Production cost (700 units*16 price//unit)

Inventory at the end of the year (100 units*16price/unit)

Less: Over absorbed fixed manufacturing overhead

Cost of sale

Gross profitability (Turnover-cost of sale)

Less: Other expenditures incurred

Cost of administration

Nil

11,200

(1600)

700

21000

(9600)

100

9500

11500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

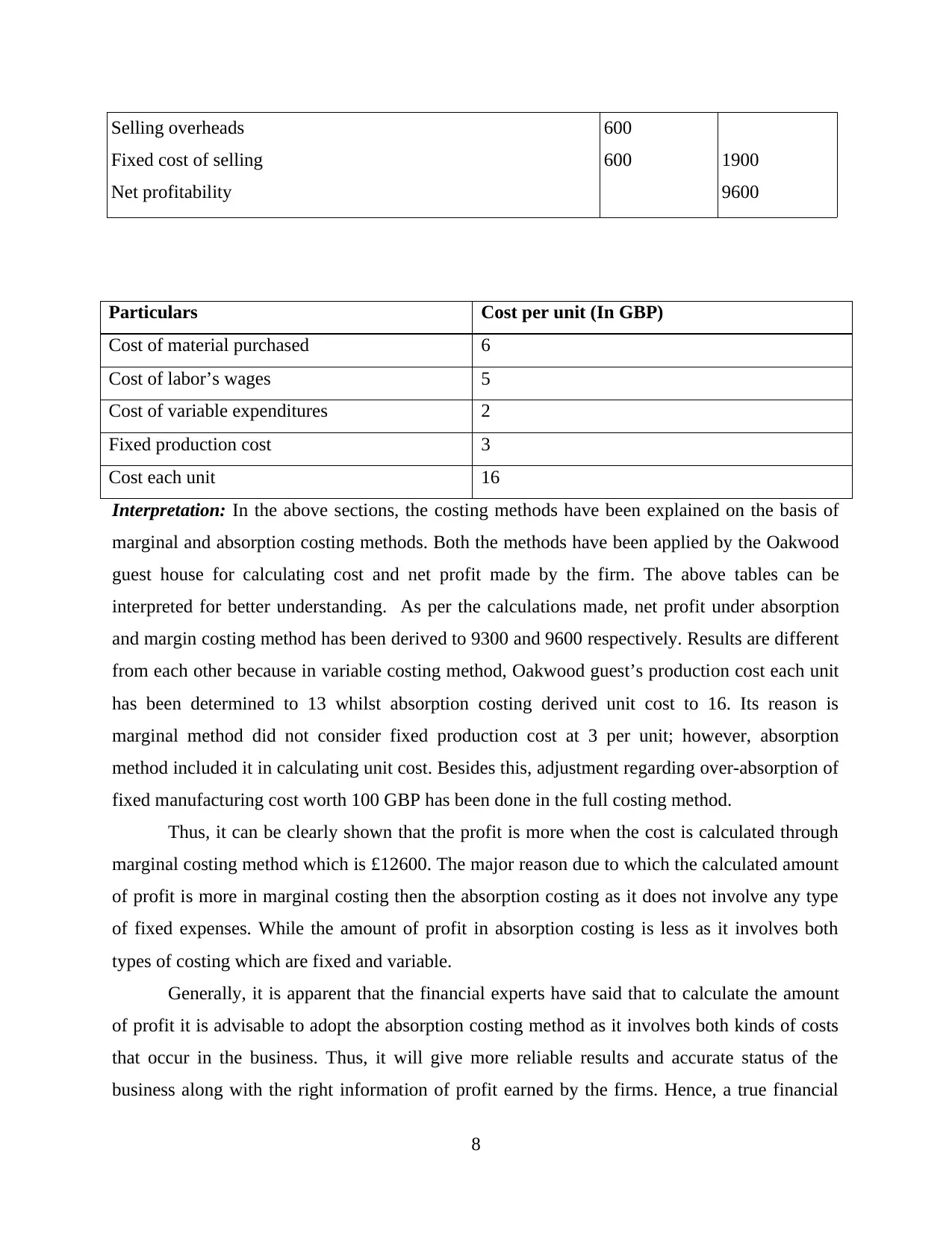

Selling overheads

Fixed cost of selling

Net profitability

600

600 1900

9600

Particulars Cost per unit (In GBP)

Cost of material purchased 6

Cost of labor’s wages 5

Cost of variable expenditures 2

Fixed production cost 3

Cost each unit 16

Interpretation: In the above sections, the costing methods have been explained on the basis of

marginal and absorption costing methods. Both the methods have been applied by the Oakwood

guest house for calculating cost and net profit made by the firm. The above tables can be

interpreted for better understanding. As per the calculations made, net profit under absorption

and margin costing method has been derived to 9300 and 9600 respectively. Results are different

from each other because in variable costing method, Oakwood guest’s production cost each unit

has been determined to 13 whilst absorption costing derived unit cost to 16. Its reason is

marginal method did not consider fixed production cost at 3 per unit; however, absorption

method included it in calculating unit cost. Besides this, adjustment regarding over-absorption of

fixed manufacturing cost worth 100 GBP has been done in the full costing method.

Thus, it can be clearly shown that the profit is more when the cost is calculated through

marginal costing method which is £12600. The major reason due to which the calculated amount

of profit is more in marginal costing then the absorption costing as it does not involve any type

of fixed expenses. While the amount of profit in absorption costing is less as it involves both

types of costing which are fixed and variable.

Generally, it is apparent that the financial experts have said that to calculate the amount

of profit it is advisable to adopt the absorption costing method as it involves both kinds of costs

that occur in the business. Thus, it will give more reliable results and accurate status of the

business along with the right information of profit earned by the firms. Hence, a true financial

8

Fixed cost of selling

Net profitability

600

600 1900

9600

Particulars Cost per unit (In GBP)

Cost of material purchased 6

Cost of labor’s wages 5

Cost of variable expenditures 2

Fixed production cost 3

Cost each unit 16

Interpretation: In the above sections, the costing methods have been explained on the basis of

marginal and absorption costing methods. Both the methods have been applied by the Oakwood

guest house for calculating cost and net profit made by the firm. The above tables can be

interpreted for better understanding. As per the calculations made, net profit under absorption

and margin costing method has been derived to 9300 and 9600 respectively. Results are different

from each other because in variable costing method, Oakwood guest’s production cost each unit

has been determined to 13 whilst absorption costing derived unit cost to 16. Its reason is

marginal method did not consider fixed production cost at 3 per unit; however, absorption

method included it in calculating unit cost. Besides this, adjustment regarding over-absorption of

fixed manufacturing cost worth 100 GBP has been done in the full costing method.

Thus, it can be clearly shown that the profit is more when the cost is calculated through

marginal costing method which is £12600. The major reason due to which the calculated amount

of profit is more in marginal costing then the absorption costing as it does not involve any type

of fixed expenses. While the amount of profit in absorption costing is less as it involves both

types of costing which are fixed and variable.

Generally, it is apparent that the financial experts have said that to calculate the amount

of profit it is advisable to adopt the absorption costing method as it involves both kinds of costs

that occur in the business. Thus, it will give more reliable results and accurate status of the

business along with the right information of profit earned by the firms. Hence, a true financial

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

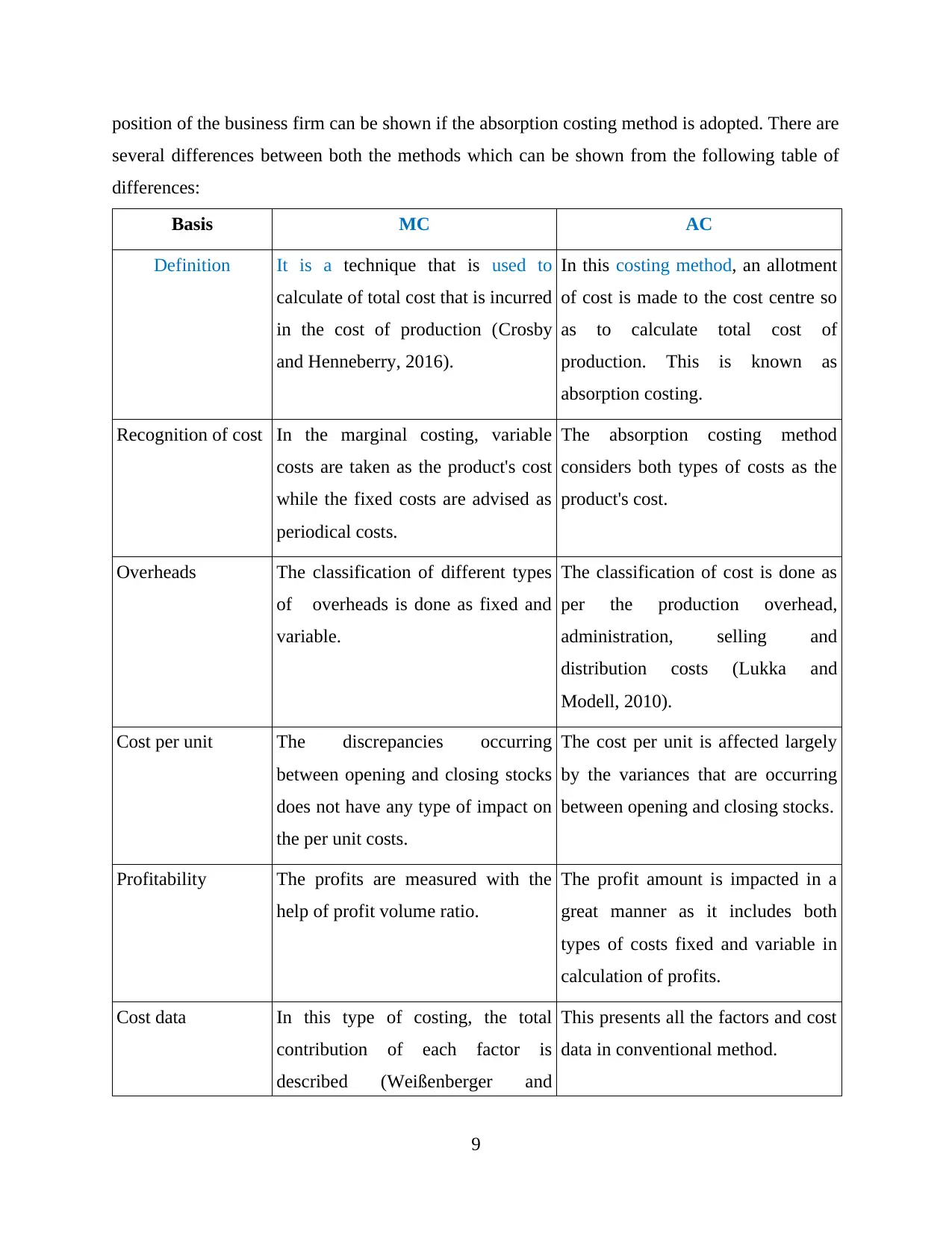

position of the business firm can be shown if the absorption costing method is adopted. There are

several differences between both the methods which can be shown from the following table of

differences:

Basis MC AC

Definition It is a technique that is used to

calculate of total cost that is incurred

in the cost of production (Crosby

and Henneberry, 2016).

In this costing method, an allotment

of cost is made to the cost centre so

as to calculate total cost of

production. This is known as

absorption costing.

Recognition of cost In the marginal costing, variable

costs are taken as the product's cost

while the fixed costs are advised as

periodical costs.

The absorption costing method

considers both types of costs as the

product's cost.

Overheads The classification of different types

of overheads is done as fixed and

variable.

The classification of cost is done as

per the production overhead,

administration, selling and

distribution costs (Lukka and

Modell, 2010).

Cost per unit The discrepancies occurring

between opening and closing stocks

does not have any type of impact on

the per unit costs.

The cost per unit is affected largely

by the variances that are occurring

between opening and closing stocks.

Profitability The profits are measured with the

help of profit volume ratio.

The profit amount is impacted in a

great manner as it includes both

types of costs fixed and variable in

calculation of profits.

Cost data In this type of costing, the total

contribution of each factor is

described (Weißenberger and

This presents all the factors and cost

data in conventional method.

9

several differences between both the methods which can be shown from the following table of

differences:

Basis MC AC

Definition It is a technique that is used to

calculate of total cost that is incurred

in the cost of production (Crosby

and Henneberry, 2016).

In this costing method, an allotment

of cost is made to the cost centre so

as to calculate total cost of

production. This is known as

absorption costing.

Recognition of cost In the marginal costing, variable

costs are taken as the product's cost

while the fixed costs are advised as

periodical costs.

The absorption costing method

considers both types of costs as the

product's cost.

Overheads The classification of different types

of overheads is done as fixed and

variable.

The classification of cost is done as

per the production overhead,

administration, selling and

distribution costs (Lukka and

Modell, 2010).

Cost per unit The discrepancies occurring

between opening and closing stocks

does not have any type of impact on

the per unit costs.

The cost per unit is affected largely

by the variances that are occurring

between opening and closing stocks.

Profitability The profits are measured with the

help of profit volume ratio.

The profit amount is impacted in a

great manner as it includes both

types of costs fixed and variable in

calculation of profits.

Cost data In this type of costing, the total

contribution of each factor is

described (Weißenberger and

This presents all the factors and cost

data in conventional method.

9

Angelkort, 2011).

TASK 3

P4 Merits and demerits of various budgetary plan techniques

The budgetary method involves the procedure in which at first, the managers and other

top level managers use to fix a standard according to which they can compare the actual

performance of the company. Thus, the budgetary tools and can be used as a measure to have a

control over various deviations that may occur in the performance. Thus, the best utilisation of

available sources can be done through this process of budgetary control. Thus, there are various

advantages and disadvantages of various methods adopted for budgeting which are mentioned in

the below section:

Incremental budgeting: This budgetary method makes use of past budgets for the upcoming

year because the organisation believes that the expenses and amounts are added in the new

budget according to the changes.

Advantages

It helps the manager in removing complex calculation

It establishes smooth flow of funds in all the departments of the organisation.

It assists the organisation in making stable budget for complete year.

The business uses this method because it identifies the risk and changes immediately.

Disadvantages:

This budgeting method is not reliable as it is prepared on the basis of assumption.

It is an expensive process and disconnects the firm from reality.

Sometimes it leads to risk as it is made on the assumption of last year expenses and it is

possible that the departments need more funds according to the changes.

Zero based budgeting: In this budgeting method the organisation makes budget from the

start by assuming all the figures as zero. In this all the cost and expenses are made on the basis of

present calculation. Moreover, in this while preparing and expense need to be explained in order

to make optimum utilisation of resources.

Advantages

The management uses this method as it demonstrate accurate and reliable figures.

10

TASK 3

P4 Merits and demerits of various budgetary plan techniques

The budgetary method involves the procedure in which at first, the managers and other

top level managers use to fix a standard according to which they can compare the actual

performance of the company. Thus, the budgetary tools and can be used as a measure to have a

control over various deviations that may occur in the performance. Thus, the best utilisation of

available sources can be done through this process of budgetary control. Thus, there are various

advantages and disadvantages of various methods adopted for budgeting which are mentioned in

the below section:

Incremental budgeting: This budgetary method makes use of past budgets for the upcoming

year because the organisation believes that the expenses and amounts are added in the new

budget according to the changes.

Advantages

It helps the manager in removing complex calculation

It establishes smooth flow of funds in all the departments of the organisation.

It assists the organisation in making stable budget for complete year.

The business uses this method because it identifies the risk and changes immediately.

Disadvantages:

This budgeting method is not reliable as it is prepared on the basis of assumption.

It is an expensive process and disconnects the firm from reality.

Sometimes it leads to risk as it is made on the assumption of last year expenses and it is

possible that the departments need more funds according to the changes.

Zero based budgeting: In this budgeting method the organisation makes budget from the

start by assuming all the figures as zero. In this all the cost and expenses are made on the basis of

present calculation. Moreover, in this while preparing and expense need to be explained in order

to make optimum utilisation of resources.

Advantages

The management uses this method as it demonstrate accurate and reliable figures.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.