Management Accounting Report: Systems, Approaches and Planning Tools

VerifiedAdded on 2020/06/06

|15

|4329

|48

Report

AI Summary

This report delves into the realm of management accounting, offering a comprehensive analysis of various systems and approaches. It begins by outlining different management accounting systems, including cost accounting, job costing, process costing, and throughput accounting, detailing their essential requirements and applications. The report then explores diverse reporting approaches, such as job cost reporting, sales and profit reports, and budget reports, emphasizing their significance in managerial decision-making. Furthermore, it incorporates practical applications through the preparation of income statements using marginal and absorption costing methods, providing a comparative analysis of their impact on profit calculation. Finally, the report examines different planning tools and their advantages and disadvantages in budgetary control, along with strategies for adopting management accounting systems to address financial problems. The report is written in the context of Bristol Commercial Vehicles (BCV).

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION....................................................................................................................................3

P1 Management accounting systems and essential requirements of different management accounting

systems........................................................................................................................................................3

P2 Varied approaches availability for management accounting reporting...................................................5

P3 Marginal and absorption costing method................................................................................................8

P4 Different types of planning tools and their advantages as well as disadvantages for budgetary control. 8

P5 Adoption of management accounting system in order to respond to financial problems......................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

Table 1Profit calculation by using marginal costing method.......................................................................8

Table 2Profit calculation by using absorption costing method....................................................................8

INTRODUCTION....................................................................................................................................3

P1 Management accounting systems and essential requirements of different management accounting

systems........................................................................................................................................................3

P2 Varied approaches availability for management accounting reporting...................................................5

P3 Marginal and absorption costing method................................................................................................8

P4 Different types of planning tools and their advantages as well as disadvantages for budgetary control. 8

P5 Adoption of management accounting system in order to respond to financial problems......................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

Table 1Profit calculation by using marginal costing method.......................................................................8

Table 2Profit calculation by using absorption costing method....................................................................8

INTRODUCTION

Management accounting is the one of the important area which helps firm in measuring

its performance and business condition. In the current research study, varied management

accounting systems are explained along with essential requirements associated with them. In

middle part of the report, varied reporting approaches are explained and along with this income

statement is prepared by using marginal and absorption costing method. At end of the report,

varied planning tools are discussed and tools that can be used to deal with financial problem are

explained in detail.

P1 Management accounting systems and essential requirements of different

management accounting systems

To

The Board of Directors of Bristol commercial vehicles(BCV) Date: 25-2-2017

Subject: Management accounting systems and essential requirements

Management accounting system refers to the system under which by following specific

process transactions are recorded by the firms in their books of accounts. Before understanding

management accounting system it is important to understand relevant domain. Management

accounting is the domain wherein facts related to costing of products are recorded in proper

manner and varied calculations are performed in respect to cost and profit for the business firm.

It can be observed that there are varied approaches in management accounting like variance

analysis by using which useful management decisions can be taken by the managers. Usually, in

the business in respect to costing of products varied standards are determined which need to be

fulfilled in order to access firm performance in proper manner (Kothari, Mizik and

Roychowdhury, 2015). Management accounting assist managers in keeping track record of

expenses that are incurred in the business and help them in identifying areas where actually work

need to be done in the business. Varied management accounting systems that are used by the

firms in their business are explained below. Cost accounting system: Cost accounting system is one that is accepted by the firms to

great extent. Under this system overall costing for the business firm is done in terms of

fixed, variable and semi variable expenses. There is wide difference between these

Management accounting is the one of the important area which helps firm in measuring

its performance and business condition. In the current research study, varied management

accounting systems are explained along with essential requirements associated with them. In

middle part of the report, varied reporting approaches are explained and along with this income

statement is prepared by using marginal and absorption costing method. At end of the report,

varied planning tools are discussed and tools that can be used to deal with financial problem are

explained in detail.

P1 Management accounting systems and essential requirements of different

management accounting systems

To

The Board of Directors of Bristol commercial vehicles(BCV) Date: 25-2-2017

Subject: Management accounting systems and essential requirements

Management accounting system refers to the system under which by following specific

process transactions are recorded by the firms in their books of accounts. Before understanding

management accounting system it is important to understand relevant domain. Management

accounting is the domain wherein facts related to costing of products are recorded in proper

manner and varied calculations are performed in respect to cost and profit for the business firm.

It can be observed that there are varied approaches in management accounting like variance

analysis by using which useful management decisions can be taken by the managers. Usually, in

the business in respect to costing of products varied standards are determined which need to be

fulfilled in order to access firm performance in proper manner (Kothari, Mizik and

Roychowdhury, 2015). Management accounting assist managers in keeping track record of

expenses that are incurred in the business and help them in identifying areas where actually work

need to be done in the business. Varied management accounting systems that are used by the

firms in their business are explained below. Cost accounting system: Cost accounting system is one that is accepted by the firms to

great extent. Under this system overall costing for the business firm is done in terms of

fixed, variable and semi variable expenses. There is wide difference between these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing systems in nature. In cost accounting system simply all products fixed

components and variable expenses are added separately. Thus, cost accounting system

reflects overall fixed cost that is incurred in the business. In same way cost accounting

system indicate overall variable expenses in the business. So, by comparing variable

expenses that are computed for different time period it can be identified whether variable

expenses increased or decreased in the business. It can be said that cost accounting

system help managers in identifying areas they need to do hard work to improve

company performance (Luft 2016). Thus, there is huge importance of the cost accounting

system for the business firms. There is easy to use feature in cost accounting systems and

due to this reason it is widely used by the firms in their business. Thus, in upcoming time

period more use of cost accounting systems can be observed in respect to the business

firms. Job costing system: Job costing system is another important accounting system where for

different jobs separately costing is done by the BCV. There are many business firms that

manufacture goods on basis of received order. In other words, it can be said that many

firms manufacture products by considering orders that different companies give to them

in respect to manufacturing products at their workplace. For example many firms like

BVC manufacture care steering for car manufacturing firms. So, different orders that are

received by the company are considered as jobs. For these different jobs costing is done

separately. Hence, it can be said that job costing system is one under which for each job

or order cost is calculated separately. Computations that are done for each job reflect

managers that which of received order is proving costly to the company and which one is

cheaper in nature. Managers take strict action to control cost for those jobs where cost is

high. It can be said that there is huge importance of the job costing system for the

companies because by same in proper manner in right direction decisions can be taken by

the managers. Job costing system is used on large scale by the companies. This is because

it give managers an overview of costing of each and every product line. This flexibility is

not available in the other costing systems. Hence, this is the reason due to which job

costing system is widely used by the firms in their business (Bromiley and et.al,, 2015).

Importance of the job costing system increased to great extent in past couple of years and

its great assistance in problem solving is the one of the important feature that is usually

components and variable expenses are added separately. Thus, cost accounting system

reflects overall fixed cost that is incurred in the business. In same way cost accounting

system indicate overall variable expenses in the business. So, by comparing variable

expenses that are computed for different time period it can be identified whether variable

expenses increased or decreased in the business. It can be said that cost accounting

system help managers in identifying areas they need to do hard work to improve

company performance (Luft 2016). Thus, there is huge importance of the cost accounting

system for the business firms. There is easy to use feature in cost accounting systems and

due to this reason it is widely used by the firms in their business. Thus, in upcoming time

period more use of cost accounting systems can be observed in respect to the business

firms. Job costing system: Job costing system is another important accounting system where for

different jobs separately costing is done by the BCV. There are many business firms that

manufacture goods on basis of received order. In other words, it can be said that many

firms manufacture products by considering orders that different companies give to them

in respect to manufacturing products at their workplace. For example many firms like

BVC manufacture care steering for car manufacturing firms. So, different orders that are

received by the company are considered as jobs. For these different jobs costing is done

separately. Hence, it can be said that job costing system is one under which for each job

or order cost is calculated separately. Computations that are done for each job reflect

managers that which of received order is proving costly to the company and which one is

cheaper in nature. Managers take strict action to control cost for those jobs where cost is

high. It can be said that there is huge importance of the job costing system for the

companies because by same in proper manner in right direction decisions can be taken by

the managers. Job costing system is used on large scale by the companies. This is because

it give managers an overview of costing of each and every product line. This flexibility is

not available in the other costing systems. Hence, this is the reason due to which job

costing system is widely used by the firms in their business (Bromiley and et.al,, 2015).

Importance of the job costing system increased to great extent in past couple of years and

its great assistance in problem solving is the one of the important feature that is usually

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered by the firms for making decisions. Thus, it can be expected that in the

upcoming time period also usage of job order costing system will increase in the

business. Process costing system: Process costing system is the different approach under which for

each process costing is done. Means that while any product is produced a specific process

is followed and under this there are several stages that need to be performed in order to

do costing of products. In the process costing system for each stage of production

separately costing of product is done by the business firm which is BVC. Process costing

proved beneficial for the companies when they want to evaluate cost of varied stages of

production. It can be said that there is huge importance of the process costing method for

the companies. This is because mentioned approach assists managers in identifying stages

of production where cost was very high and need strict action for control purpose. It can

be said that process costing process have significant importance for the business firms.

So, cost control and wastage minimization objective can be easily achieved by using

process costing method by the business firms (Järvinen, 2016). Process costing is used

specially by those firms where product production process is larger and it is difficult to

track points where cost is skyrocketing which ultimately lead to increase in production

cost in the business. It can be said that process costing is the one of the management

accounting system that assists firms in achieving multiple objectives in the business. Throughput accounting system: Throughput accounting system is another one that is

widely used by the firms. in above section varied management accounting systems are

discussed in detail but they are traditional approaches. In category of modern approach of

management accounting throughput accounting system comes. Mentioned approach was

evolved by one of the Israeli businessman. These costing systems help firms in

minimizing wastage in the business (Zheng and Alver, 2015). There are many companies

that are commonly facing problem where wastage increases consistently in the business.

Throughput accounting system is one which assists firms in tacking such kind of

problems to great extent. Thus, it can be said that throughput accounting system have due

importance for the companies and its adoption is also increasing with passage of time by

the business firms.

upcoming time period also usage of job order costing system will increase in the

business. Process costing system: Process costing system is the different approach under which for

each process costing is done. Means that while any product is produced a specific process

is followed and under this there are several stages that need to be performed in order to

do costing of products. In the process costing system for each stage of production

separately costing of product is done by the business firm which is BVC. Process costing

proved beneficial for the companies when they want to evaluate cost of varied stages of

production. It can be said that there is huge importance of the process costing method for

the companies. This is because mentioned approach assists managers in identifying stages

of production where cost was very high and need strict action for control purpose. It can

be said that process costing process have significant importance for the business firms.

So, cost control and wastage minimization objective can be easily achieved by using

process costing method by the business firms (Järvinen, 2016). Process costing is used

specially by those firms where product production process is larger and it is difficult to

track points where cost is skyrocketing which ultimately lead to increase in production

cost in the business. It can be said that process costing is the one of the management

accounting system that assists firms in achieving multiple objectives in the business. Throughput accounting system: Throughput accounting system is another one that is

widely used by the firms. in above section varied management accounting systems are

discussed in detail but they are traditional approaches. In category of modern approach of

management accounting throughput accounting system comes. Mentioned approach was

evolved by one of the Israeli businessman. These costing systems help firms in

minimizing wastage in the business (Zheng and Alver, 2015). There are many companies

that are commonly facing problem where wastage increases consistently in the business.

Throughput accounting system is one which assists firms in tacking such kind of

problems to great extent. Thus, it can be said that throughput accounting system have due

importance for the companies and its adoption is also increasing with passage of time by

the business firms.

P2 Varied approaches availability for management accounting reporting

To

The Board of Directors of Bristol commercial vehicles Date: 25-2-2017

Subject: Management accounting systems and essential requirements

Reporting is the one of the most important function of management because it assists managers

in making business decisions. In these reports varied facts are provided by the assistants that help

manages in taking idea of situation that is going on in the business and making decisions.

Different sort of reporting approaches that are used by the firms in their day to day business are

explained below.

Job cost reporting: Under job costing reporting approach for different jobs cost reporting

is done separately by BVC managers. In these reports separately sheets are prepared for

each product line. Costing is shown individually for these product lines in reports.

Hence, it can be said that through job cost reporting managers get a better overview of

the product costing. Job costing have due importance for the firms because for each

product line managers comes to know that which are the products where cost is high

(Watson, 2015). With passage of time some of changes comes in the job cost reporting

system as firms according to their requirements make changes in reporting approaches in

order to view inside facts with more granularity and making sound business decisions.

There are multiple advantages of the job cost reporting approach for the firms and due to

this reason this approach of reporting is widely preferred by the companies. In many

business firms software’s like Tableau is used and under this charting of variables is

done. Through visualization managers get clear information about product line costing.

Thus, it can be said that use of advanced software or technology is underpinning decision

making process that managers follow in respect to cost control at the workplace. In

upcoming time period large size corporate can make many changes in their accounting

system in order to make wise decisions at fast rate in the business. Not even large

corporate but small companies also prefer to use job order costing reporting because there

are multiple product lines that are operated by the firms in the market. Thus, with passage

of time job costing reporting may gain wide popularity then other accounting system due

to its some of the important characteristics. Out of all characteristics one of the main

features of job cost reporting is that it is informative in nature about costing of product

To

The Board of Directors of Bristol commercial vehicles Date: 25-2-2017

Subject: Management accounting systems and essential requirements

Reporting is the one of the most important function of management because it assists managers

in making business decisions. In these reports varied facts are provided by the assistants that help

manages in taking idea of situation that is going on in the business and making decisions.

Different sort of reporting approaches that are used by the firms in their day to day business are

explained below.

Job cost reporting: Under job costing reporting approach for different jobs cost reporting

is done separately by BVC managers. In these reports separately sheets are prepared for

each product line. Costing is shown individually for these product lines in reports.

Hence, it can be said that through job cost reporting managers get a better overview of

the product costing. Job costing have due importance for the firms because for each

product line managers comes to know that which are the products where cost is high

(Watson, 2015). With passage of time some of changes comes in the job cost reporting

system as firms according to their requirements make changes in reporting approaches in

order to view inside facts with more granularity and making sound business decisions.

There are multiple advantages of the job cost reporting approach for the firms and due to

this reason this approach of reporting is widely preferred by the companies. In many

business firms software’s like Tableau is used and under this charting of variables is

done. Through visualization managers get clear information about product line costing.

Thus, it can be said that use of advanced software or technology is underpinning decision

making process that managers follow in respect to cost control at the workplace. In

upcoming time period large size corporate can make many changes in their accounting

system in order to make wise decisions at fast rate in the business. Not even large

corporate but small companies also prefer to use job order costing reporting because there

are multiple product lines that are operated by the firms in the market. Thus, with passage

of time job costing reporting may gain wide popularity then other accounting system due

to its some of the important characteristics. Out of all characteristics one of the main

features of job cost reporting is that it is informative in nature about costing of product

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Bui and De Villiers, 2017). Through job cost reporting managers get more information

about cost of product than any other approach of cost reporting. This is the reason due to

which job cost reporting is gaining wide popularity among large, medium and small size

corporate.

Sales and profit report: It is another reporting approach that is used by the firms in their

business. Under this reporting approach sales and profit report is prepared individually. In

sales report, entire sales amount is classified among different categories which are varied

product lines or different geographic areas. In case of profit report sales amount is listed

and varied expenses are taken in to account. From sales value expenses are subtracted

and in this way net profit amount is computed by the business firm (Young and et.al.,

2015). Thus, it can be said that sales and profit report both have significant importance

for the firms. This is because through sales report managers come to know about

contribution that is given by varied geographic areas in revenue earning of the business

firm. Thus, managers easily identify that which are the fastest growing markets and

which are one that are growing at slow rate. By preparing strategy areas where firm

performance is weak is identified and effort is made to generate more revenue from that

area if there is huge growth potential in that area. Profit report is another one that like

sales report reflects lots of things to the firms. In profit report last five years income and

expenditure are reflected and by making comparison between them it is identified

whether firm performance is excellent or worst. On basis of obtained results tactic is

prepared to improve company performance. It can be said that sales and profit report

have due importance for the firms. Company managers must make best use of these

statements or reports and must work in relevant area to improve condition of the

company.

Budget report: It is another method that is used for reporting purpose by the BVC. In the

budget report actual and estimated values are compared with each other and on that basis

company performance is accessed. In budget report, quarter wise budget and actual

values are given and results are also presented in the report. Thus, managers are always

interested in identifying areas where consistently firm performance is poor. By taking

strict action against relevant areas performance of the firm is improved to great extent. It

can be said that budget report have due importance for the firms. There are different sort

about cost of product than any other approach of cost reporting. This is the reason due to

which job cost reporting is gaining wide popularity among large, medium and small size

corporate.

Sales and profit report: It is another reporting approach that is used by the firms in their

business. Under this reporting approach sales and profit report is prepared individually. In

sales report, entire sales amount is classified among different categories which are varied

product lines or different geographic areas. In case of profit report sales amount is listed

and varied expenses are taken in to account. From sales value expenses are subtracted

and in this way net profit amount is computed by the business firm (Young and et.al.,

2015). Thus, it can be said that sales and profit report both have significant importance

for the firms. This is because through sales report managers come to know about

contribution that is given by varied geographic areas in revenue earning of the business

firm. Thus, managers easily identify that which are the fastest growing markets and

which are one that are growing at slow rate. By preparing strategy areas where firm

performance is weak is identified and effort is made to generate more revenue from that

area if there is huge growth potential in that area. Profit report is another one that like

sales report reflects lots of things to the firms. In profit report last five years income and

expenditure are reflected and by making comparison between them it is identified

whether firm performance is excellent or worst. On basis of obtained results tactic is

prepared to improve company performance. It can be said that sales and profit report

have due importance for the firms. Company managers must make best use of these

statements or reports and must work in relevant area to improve condition of the

company.

Budget report: It is another method that is used for reporting purpose by the BVC. In the

budget report actual and estimated values are compared with each other and on that basis

company performance is accessed. In budget report, quarter wise budget and actual

values are given and results are also presented in the report. Thus, managers are always

interested in identifying areas where consistently firm performance is poor. By taking

strict action against relevant areas performance of the firm is improved to great extent. It

can be said that budget report have due importance for the firms. There are different sort

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of budgets that are prepared by the firms like fixed and flexible budget (Erkan, 2015).

There is wide difference between these budgeting approaches. In case of fixed budget

values that are determined for specific element of budget remain certain and does not

change over the time period. It can be said that there is huge importance of the budget

report for the business firms. There is much other approach that is used for preparing

budget like zero based budgeting. In this approach each department manager prepare

budget for its department separately. If that budget is passed by the top manager then

budget amount is allocated to the department. In this way, budget is prepared under zero

based budgeting. In order to make reporting procedure more accurate zero based budgets

must be used. This is because in this method first of all department heads are making

estimations and then top managers carry out detail discussion with them. Hence, budget

is prepared accurately and due to this reason reporting of performance become more

accurate in case of zero based budget in budget report.

P3 Marginal and absorption costing method

Marginal and absorption costing methods are commonly used by the business firms. In

case of marginal costing approach variable costs are taken in to account and deducted from sales

revenue. On other hand, in case of absorption costing method fixed expenses and variable

expenses are taken in to account and deducted from the sales revenue amount. Thus, it can be

said that there is difference between marginal and absorption costing method (Kalpan financial

knowledge bank, 2017). There is importance of the both marginal and absorption costing method

for the firms. Usually, it is observed that companies are using both these methods to make

business decisions. If managers wants to know firm profitability level if fixed expenses are not

taken in to account then marginal costing approach is better for the firm.

Table 1Profit calculation by using marginal costing method

Sales revenue 52500

Less: COGS

Opening stock -

Variable cost of production (2000 * 15) 30000

Closing inventory (500* 15) 7500 22500

30000

There is wide difference between these budgeting approaches. In case of fixed budget

values that are determined for specific element of budget remain certain and does not

change over the time period. It can be said that there is huge importance of the budget

report for the business firms. There is much other approach that is used for preparing

budget like zero based budgeting. In this approach each department manager prepare

budget for its department separately. If that budget is passed by the top manager then

budget amount is allocated to the department. In this way, budget is prepared under zero

based budgeting. In order to make reporting procedure more accurate zero based budgets

must be used. This is because in this method first of all department heads are making

estimations and then top managers carry out detail discussion with them. Hence, budget

is prepared accurately and due to this reason reporting of performance become more

accurate in case of zero based budget in budget report.

P3 Marginal and absorption costing method

Marginal and absorption costing methods are commonly used by the business firms. In

case of marginal costing approach variable costs are taken in to account and deducted from sales

revenue. On other hand, in case of absorption costing method fixed expenses and variable

expenses are taken in to account and deducted from the sales revenue amount. Thus, it can be

said that there is difference between marginal and absorption costing method (Kalpan financial

knowledge bank, 2017). There is importance of the both marginal and absorption costing method

for the firms. Usually, it is observed that companies are using both these methods to make

business decisions. If managers wants to know firm profitability level if fixed expenses are not

taken in to account then marginal costing approach is better for the firm.

Table 1Profit calculation by using marginal costing method

Sales revenue 52500

Less: COGS

Opening stock -

Variable cost of production (2000 * 15) 30000

Closing inventory (500* 15) 7500 22500

30000

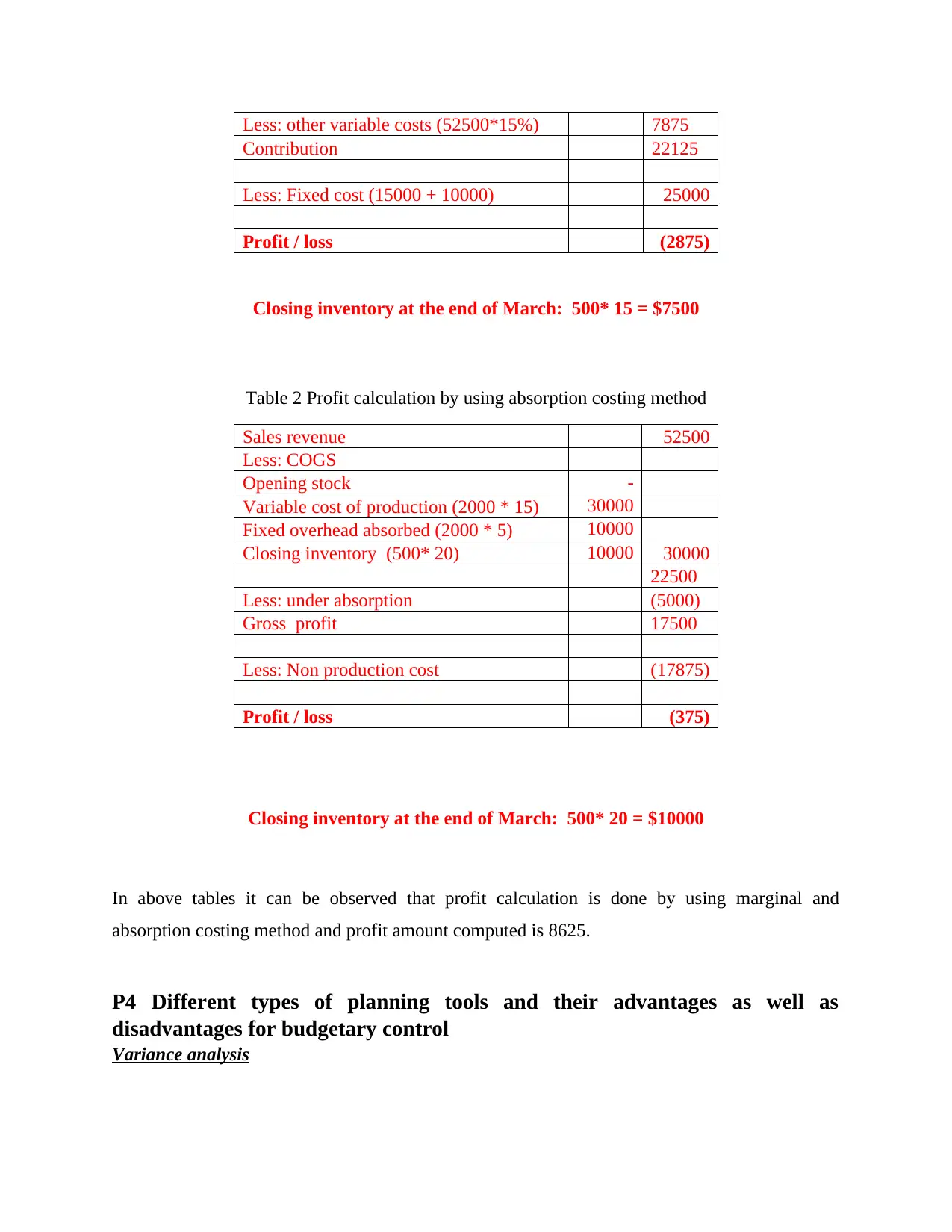

Less: other variable costs (52500*15%) 7875

Contribution 22125

Less: Fixed cost (15000 + 10000) 25000

Profit / loss (2875)

Closing inventory at the end of March: 500* 15 = $7500

Table 2 Profit calculation by using absorption costing method

Sales revenue 52500

Less: COGS

Opening stock -

Variable cost of production (2000 * 15) 30000

Fixed overhead absorbed (2000 * 5) 10000

Closing inventory (500* 20) 10000 30000

22500

Less: under absorption (5000)

Gross profit 17500

Less: Non production cost (17875)

Profit / loss (375)

Closing inventory at the end of March: 500* 20 = $10000

In above tables it can be observed that profit calculation is done by using marginal and

absorption costing method and profit amount computed is 8625.

P4 Different types of planning tools and their advantages as well as

disadvantages for budgetary control

Variance analysis

Contribution 22125

Less: Fixed cost (15000 + 10000) 25000

Profit / loss (2875)

Closing inventory at the end of March: 500* 15 = $7500

Table 2 Profit calculation by using absorption costing method

Sales revenue 52500

Less: COGS

Opening stock -

Variable cost of production (2000 * 15) 30000

Fixed overhead absorbed (2000 * 5) 10000

Closing inventory (500* 20) 10000 30000

22500

Less: under absorption (5000)

Gross profit 17500

Less: Non production cost (17875)

Profit / loss (375)

Closing inventory at the end of March: 500* 20 = $10000

In above tables it can be observed that profit calculation is done by using marginal and

absorption costing method and profit amount computed is 8625.

P4 Different types of planning tools and their advantages as well as

disadvantages for budgetary control

Variance analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variance analysis is the method under which current and determined standard are

compared with each other and by doing so performance of the firm is measured. There is huge

importance of the variance analysis method for the firms. Advantages and disadvantages of the

variance analysis method is explained below.

Advantages

One of the major advantage of the variance analysis approach is that by using performance of the

BVC can be measured accurately. Weak areas can be find out and by working on that area

performance can be improved to great extent.

Short term and long term performance of the company can be measured in proper manner by

using variance analysis method. Thus, usage of mentioned method ensured that cost will be

measured in proper manner in the business.

Disadvantages

One of the major disadvantage of variance analysis is that estimations are made in order to

prepare budget. Many times managers wrongly forecast future time period and due to this reason

wrong predictions are made (Rieckhof, Bergmann and Guenther, 2015). Hence, if budget is

prepared in wrong way business decisions are also made in wrong direction. This is one of the

major disadvantage of the variance analysis method.

Zero based budgeting

It is one of the approach under which departments prepare their own budget and same get

approve from top manager. Accordingly, budget amount is allocated to all departments.

Advantage

One of the major advantage of zero based budgeting is that from bottom to top estimations are

made and there are little chances of their inaccuracy. Due to this reason there is high reliability of

results that are obtained in zero based budgeting method.

Disadvantage

One of major disadvantage of zero based budgeting is that many times top managers does not

pay much attention and due to this reason even middle level managers make a mistake error in

compared with each other and by doing so performance of the firm is measured. There is huge

importance of the variance analysis method for the firms. Advantages and disadvantages of the

variance analysis method is explained below.

Advantages

One of the major advantage of the variance analysis approach is that by using performance of the

BVC can be measured accurately. Weak areas can be find out and by working on that area

performance can be improved to great extent.

Short term and long term performance of the company can be measured in proper manner by

using variance analysis method. Thus, usage of mentioned method ensured that cost will be

measured in proper manner in the business.

Disadvantages

One of the major disadvantage of variance analysis is that estimations are made in order to

prepare budget. Many times managers wrongly forecast future time period and due to this reason

wrong predictions are made (Rieckhof, Bergmann and Guenther, 2015). Hence, if budget is

prepared in wrong way business decisions are also made in wrong direction. This is one of the

major disadvantage of the variance analysis method.

Zero based budgeting

It is one of the approach under which departments prepare their own budget and same get

approve from top manager. Accordingly, budget amount is allocated to all departments.

Advantage

One of the major advantage of zero based budgeting is that from bottom to top estimations are

made and there are little chances of their inaccuracy. Due to this reason there is high reliability of

results that are obtained in zero based budgeting method.

Disadvantage

One of major disadvantage of zero based budgeting is that many times top managers does not

pay much attention and due to this reason even middle level managers make a mistake error in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budget is not detected (Erkan, 2015). Hence, actions can be taken in wrong direction. This is one

of major disadvantage of zero based budgeting for the BVC.

Incremental budgeting

It is the budget under which increase is made in the previous year budget values. This

approach is commonly followed by the firms in their business. Some of advantage and

disadvantage of incremental budgeting are as follows.

Advantage

Usually on yearly basis business of firms grow at specific percentage level and due to this reason

expenses also increase. Hence, it is not hard to make estimation of cash flows and due to this

reason in incremental budget formation there are less chances of error.

Disadvantage

One of major disadvantage is that business certainly cannot every year and due to this reason it is

possible that values in budget increased but actually its value get declined due to downturn in

economic condition of the nation (Bui and De Villiers, 2017). In such kind of situation business

performance can be wrongly accessed. This is one of major disadvantage of incremental budget

for the firm.

P5 Adoption of management accounting system in order to respond to

financial problems

Financial problems are commonly faced by the firms in their business and in order to deal

with such kind of situations there is need to follow specific management accounting system.

Some of the system that can be followed by the firm are given below. KPI: Cost control is one of the problem that is faced by the firm in its business. Under

KPI some of the standards can be determined for varied indicators and by comparing

actual performance with same performance can be accessed. Benchmarking: It is the approach under which like KPI standard is determined and

current performance is compared. Weak areas are identified and preparing tactics that

weak area is converted in to strong domain.

of major disadvantage of zero based budgeting for the BVC.

Incremental budgeting

It is the budget under which increase is made in the previous year budget values. This

approach is commonly followed by the firms in their business. Some of advantage and

disadvantage of incremental budgeting are as follows.

Advantage

Usually on yearly basis business of firms grow at specific percentage level and due to this reason

expenses also increase. Hence, it is not hard to make estimation of cash flows and due to this

reason in incremental budget formation there are less chances of error.

Disadvantage

One of major disadvantage is that business certainly cannot every year and due to this reason it is

possible that values in budget increased but actually its value get declined due to downturn in

economic condition of the nation (Bui and De Villiers, 2017). In such kind of situation business

performance can be wrongly accessed. This is one of major disadvantage of incremental budget

for the firm.

P5 Adoption of management accounting system in order to respond to

financial problems

Financial problems are commonly faced by the firms in their business and in order to deal

with such kind of situations there is need to follow specific management accounting system.

Some of the system that can be followed by the firm are given below. KPI: Cost control is one of the problem that is faced by the firm in its business. Under

KPI some of the standards can be determined for varied indicators and by comparing

actual performance with same performance can be accessed. Benchmarking: It is the approach under which like KPI standard is determined and

current performance is compared. Weak areas are identified and preparing tactics that

weak area is converted in to strong domain.

Financial governance : Under financial governance some rules and regulations are

prepared which are followed while performing any operation (Erkan, 2015). In case it is

identified that there was any mistake that was made by an employee then in that case

culprit entity can be easily identified and action can be taken against it for making

mistake. Such kind of practices create fear among employees and ensure that mistakes

will never made from their side in respect to performance of operation. Ratio analysis: Ratio analysis is the another approach that is used to measure firm

performance. Under this company condition is evaluated on varied parameters and an

area where performance is poor is identified. By taking corrective action weak area is

converted into strong one.

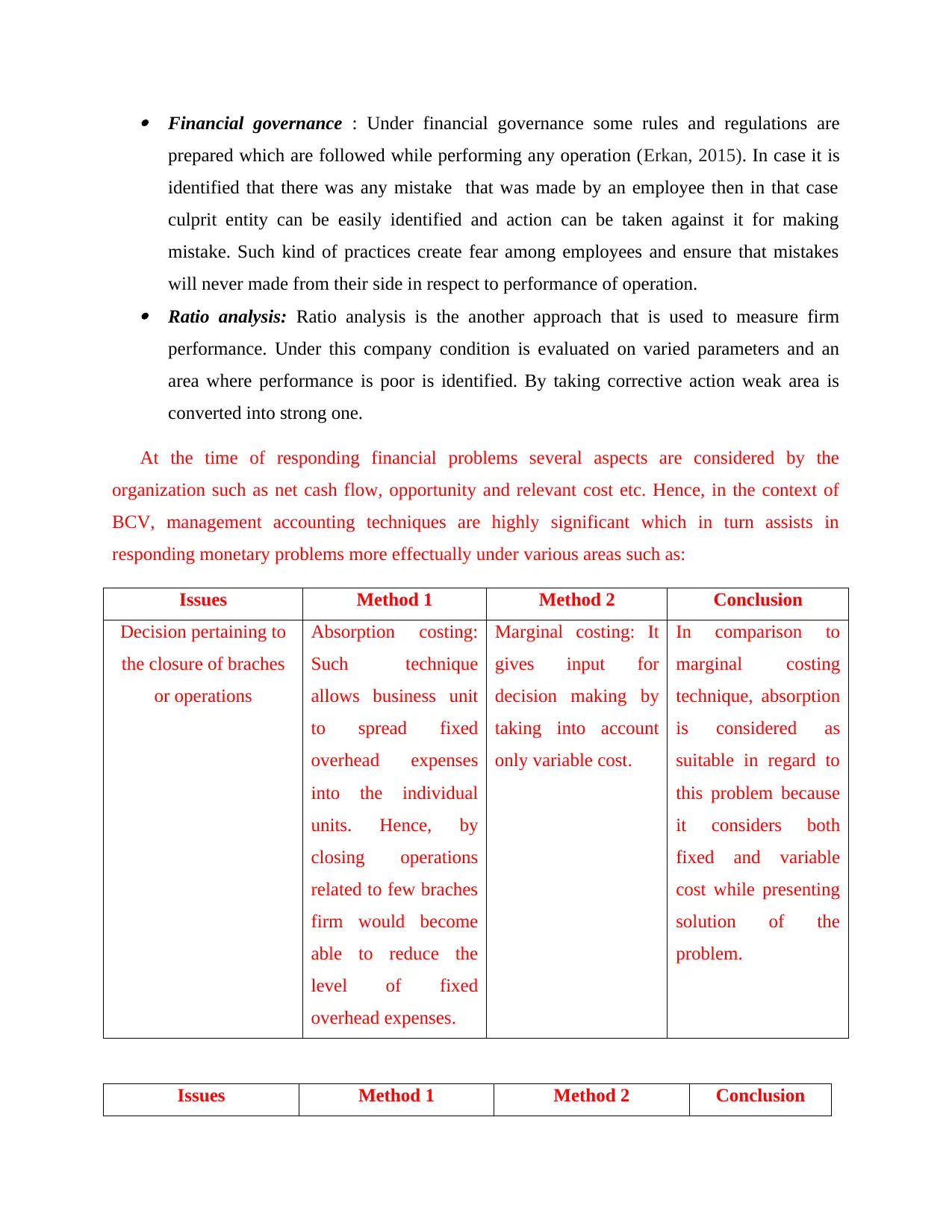

At the time of responding financial problems several aspects are considered by the

organization such as net cash flow, opportunity and relevant cost etc. Hence, in the context of

BCV, management accounting techniques are highly significant which in turn assists in

responding monetary problems more effectually under various areas such as:

Issues Method 1 Method 2 Conclusion

Decision pertaining to

the closure of braches

or operations

Absorption costing:

Such technique

allows business unit

to spread fixed

overhead expenses

into the individual

units. Hence, by

closing operations

related to few braches

firm would become

able to reduce the

level of fixed

overhead expenses.

Marginal costing: It

gives input for

decision making by

taking into account

only variable cost.

In comparison to

marginal costing

technique, absorption

is considered as

suitable in regard to

this problem because

it considers both

fixed and variable

cost while presenting

solution of the

problem.

Issues Method 1 Method 2 Conclusion

prepared which are followed while performing any operation (Erkan, 2015). In case it is

identified that there was any mistake that was made by an employee then in that case

culprit entity can be easily identified and action can be taken against it for making

mistake. Such kind of practices create fear among employees and ensure that mistakes

will never made from their side in respect to performance of operation. Ratio analysis: Ratio analysis is the another approach that is used to measure firm

performance. Under this company condition is evaluated on varied parameters and an

area where performance is poor is identified. By taking corrective action weak area is

converted into strong one.

At the time of responding financial problems several aspects are considered by the

organization such as net cash flow, opportunity and relevant cost etc. Hence, in the context of

BCV, management accounting techniques are highly significant which in turn assists in

responding monetary problems more effectually under various areas such as:

Issues Method 1 Method 2 Conclusion

Decision pertaining to

the closure of braches

or operations

Absorption costing:

Such technique

allows business unit

to spread fixed

overhead expenses

into the individual

units. Hence, by

closing operations

related to few braches

firm would become

able to reduce the

level of fixed

overhead expenses.

Marginal costing: It

gives input for

decision making by

taking into account

only variable cost.

In comparison to

marginal costing

technique, absorption

is considered as

suitable in regard to

this problem because

it considers both

fixed and variable

cost while presenting

solution of the

problem.

Issues Method 1 Method 2 Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.