Management Accounting Report: Analysis and Planning Tools

VerifiedAdded on 2021/02/20

|22

|4756

|43

Report

AI Summary

This report on management accounting for ABC Ltd. explores various facets of managerial accounting. It defines management accounting, differentiating it from financial accounting, and discusses different management accounting systems such as job costing, inventory management, price optimization, and cost accounting. The report then delves into the integration of these systems within an organization and their impact on operational efficiency, using ABC Ltd as a case study. It further compares costing techniques, including marginal and absorption costing, with detailed calculations of cost per unit, cost of production, and profitability statements. The report also examines planning tools in budgetary control, outlining their benefits and drawbacks, and how they are used in preparing and forecasting budgets. Finally, it compares how companies adapt management accounting systems to address financial problems and concludes that management accounting is essential for sustainable success, highlighting planning tools for solving financial issues.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

Meaning of management accounting system...............................................................................3

Different types of management accounting systems and their essentials and benefits................4

Integration of management accounting systems and management accounting reporting within

organization..................................................................................................................................6

TASK 2............................................................................................................................................6

Different costing techniques........................................................................................................6

Cost per unit, cost of production and total cost of sales.............................................................7

TASK 3............................................................................................................................................9

Benefits and drawbacks of various kinds of planning tools applied in budgetary control..........9

Use of planning tools for preparing and forecasting budgets....................................................10

TASK 4..........................................................................................................................................12

Comparison regarding how companies are adapting management accounting systems for

confronting financial problems..................................................................................................12

Management accounting leads organizations towards sustainable success...............................14

Planning tools for accounting for solving financial issues........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

Meaning of management accounting system...............................................................................3

Different types of management accounting systems and their essentials and benefits................4

Integration of management accounting systems and management accounting reporting within

organization..................................................................................................................................6

TASK 2............................................................................................................................................6

Different costing techniques........................................................................................................6

Cost per unit, cost of production and total cost of sales.............................................................7

TASK 3............................................................................................................................................9

Benefits and drawbacks of various kinds of planning tools applied in budgetary control..........9

Use of planning tools for preparing and forecasting budgets....................................................10

TASK 4..........................................................................................................................................12

Comparison regarding how companies are adapting management accounting systems for

confronting financial problems..................................................................................................12

Management accounting leads organizations towards sustainable success...............................14

Planning tools for accounting for solving financial issues........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is defined as a procedure of applying professional knowledge,

skills and techniques in order to prepare accounting information in such a way, which assists the

managers of a business organization in their decision-making process, formulation of strategies,

plan, polices relating operations, rational use of limited resources, safeguarding of assets and

disclosure to company's management (Agrawal, 2018). In the present report, concept of

management accounting will be studied in the context of ABC Ltd which is a medium-sized

business entity operating in manufacturing sector.

Different types of management accounting system along with their benefits will be

discussed in the report. It will also include how management accounting reporting is integrated

within the company. Further, a comparison will be done regarding how various companies

applies the techniques and tools of management accounting for responding to the financial

problems. Moreover, various planning tools of budgetary control will be highlighted in this

project report and how such management accounting leads an organization towards the

sustainable success.

TASK 1

Meaning of management accounting system

Management accounting also called as managerial accounting is described as a process of

presenting the financial and cost information for the purpose of helping the management of a

company in the formulation of policies and strategies that are to be adopted by the entire

organization. In simpler language, it is that field of accounting which assists the managers of

ABC limited in performing their core functions such as planning, organizing, monitoring and

controlling the activities of the business entity (Management accounting - What is management

accounting, 2019).

The primary thing which distinguish management accounting from financial accounting

is that managerial accounting is concerned with preparation of financial report for the purpose of

aiding the internal team of the organization in their decision-making process while financial

accounting is a process of preparing financial statements of the company for the purpose of

communicating it same to the interested parties or stakeholders. Management accounting

considers monetary and non monetary information while financial accounting considers only

Management accounting is defined as a procedure of applying professional knowledge,

skills and techniques in order to prepare accounting information in such a way, which assists the

managers of a business organization in their decision-making process, formulation of strategies,

plan, polices relating operations, rational use of limited resources, safeguarding of assets and

disclosure to company's management (Agrawal, 2018). In the present report, concept of

management accounting will be studied in the context of ABC Ltd which is a medium-sized

business entity operating in manufacturing sector.

Different types of management accounting system along with their benefits will be

discussed in the report. It will also include how management accounting reporting is integrated

within the company. Further, a comparison will be done regarding how various companies

applies the techniques and tools of management accounting for responding to the financial

problems. Moreover, various planning tools of budgetary control will be highlighted in this

project report and how such management accounting leads an organization towards the

sustainable success.

TASK 1

Meaning of management accounting system

Management accounting also called as managerial accounting is described as a process of

presenting the financial and cost information for the purpose of helping the management of a

company in the formulation of policies and strategies that are to be adopted by the entire

organization. In simpler language, it is that field of accounting which assists the managers of

ABC limited in performing their core functions such as planning, organizing, monitoring and

controlling the activities of the business entity (Management accounting - What is management

accounting, 2019).

The primary thing which distinguish management accounting from financial accounting

is that managerial accounting is concerned with preparation of financial report for the purpose of

aiding the internal team of the organization in their decision-making process while financial

accounting is a process of preparing financial statements of the company for the purpose of

communicating it same to the interested parties or stakeholders. Management accounting

considers monetary and non monetary information while financial accounting considers only

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information relating to financial nature (Amanollah Nejad Kalkhouran, Hossein Nezhad Nedaei,

and Abdul Rasid, 2017).

Different types of management accounting systems and their essentials and benefits

Managerial accounting consist of various kinds of other systems which aids the managers

in adding value to the organization. Managers use different systems of management accounting

for the purpose of obtaining efficiency in the operations within the business. These are as

follows:

Job costing system:

This is referred to as a expenditure monitoring system which is concerned with assigning

manufacturing expenses to each product separately. This makes the managers to keep the track

of company's costs and expenditures. Job costing is related with ascertainment of manufacturing

expenses by segmenting them in direct material, labour and manufacturing overheads (Azmitov

and Korabelnikova, 2015).

Essentials and benefits:

This system is required in the business as it enables the management in calculating the

profit earned on individual jobs which in turns facilitates them in their decision-making that a

particular job is profitable enough to continue it in the future or shall it be closed down.

Inventory management system:

In the simpler words, inventory management is keeping a track of company's non

capitalized assets such as inventory and stock items. It is a systematic procedure of attaining,

storing and creating profits from the non capital assets. Availability of adequate inventory at all

times is the main motive of inventory management system. This facilitates a smooth flow in the

production process (What is inventory management, 2019). There are inventory management

systems such as:

LIFO

FIFO Just in time purchase

Essentials and benefits:

The main advantage of employing inventory management system within the business is

that it helps in reducing the unnecessary inventory carrying and holding costs. This in turn assist

and Abdul Rasid, 2017).

Different types of management accounting systems and their essentials and benefits

Managerial accounting consist of various kinds of other systems which aids the managers

in adding value to the organization. Managers use different systems of management accounting

for the purpose of obtaining efficiency in the operations within the business. These are as

follows:

Job costing system:

This is referred to as a expenditure monitoring system which is concerned with assigning

manufacturing expenses to each product separately. This makes the managers to keep the track

of company's costs and expenditures. Job costing is related with ascertainment of manufacturing

expenses by segmenting them in direct material, labour and manufacturing overheads (Azmitov

and Korabelnikova, 2015).

Essentials and benefits:

This system is required in the business as it enables the management in calculating the

profit earned on individual jobs which in turns facilitates them in their decision-making that a

particular job is profitable enough to continue it in the future or shall it be closed down.

Inventory management system:

In the simpler words, inventory management is keeping a track of company's non

capitalized assets such as inventory and stock items. It is a systematic procedure of attaining,

storing and creating profits from the non capital assets. Availability of adequate inventory at all

times is the main motive of inventory management system. This facilitates a smooth flow in the

production process (What is inventory management, 2019). There are inventory management

systems such as:

LIFO

FIFO Just in time purchase

Essentials and benefits:

The main advantage of employing inventory management system within the business is

that it helps in reducing the unnecessary inventory carrying and holding costs. This in turn assist

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in reducing the requirements of working capital of the organization. Moreover, it helps in

preventing loss from theft, inventory manipulation, returns and spoilage.

Price Optimizing systems:

It refers to a systematic procedure of ascertaining a rational retail value of the products

and services of the company. It is basically a process of finding such a price at which company

gets maximum profits and which the consumer are willing to pay. For example, if the price is

fixed too high, then consumers will not buy the product and if the prices are fixed too low, then

company will not be able to earn profits (Christ and Burritt, 2015). Thus, price optimization

system assists the managers in setting an optimum prices of products and services on the basis of

market demand of the products.

Essentials and benefits:

Prize optimization system requires; cost models, analysis of competitive management,

models of customers elasticity and optimization techniques. The advantage of this system is that

proper price for the product or service is determined scientifically in accordance with the market

forces. This helps in increasing the profitability of the company.

Cost accounting system:

It is defined as a process which is concerned with anticipation of costs of company's

products for the purpose of analysis of profitability, cost control and inventory valuation.

Estimation of the costs of activities of business accurately is the essence of profitability of the

company. This indicates that ABC company shall know which of its operations are profiterole

while which operations are consuming more of resources and does not live up to the expectations

of business.

Essentials and benefits:

The advantages of cost accounting system is that enables the management in reducing the

,cost, wastage, losses and loopholes by setting standards/bench-marks for every activity within

the organization. It facilitates the managers in identifying the reasons behind profit or loss with

the help of which they take remedial steps for keeping the profitability of company on right

track.

preventing loss from theft, inventory manipulation, returns and spoilage.

Price Optimizing systems:

It refers to a systematic procedure of ascertaining a rational retail value of the products

and services of the company. It is basically a process of finding such a price at which company

gets maximum profits and which the consumer are willing to pay. For example, if the price is

fixed too high, then consumers will not buy the product and if the prices are fixed too low, then

company will not be able to earn profits (Christ and Burritt, 2015). Thus, price optimization

system assists the managers in setting an optimum prices of products and services on the basis of

market demand of the products.

Essentials and benefits:

Prize optimization system requires; cost models, analysis of competitive management,

models of customers elasticity and optimization techniques. The advantage of this system is that

proper price for the product or service is determined scientifically in accordance with the market

forces. This helps in increasing the profitability of the company.

Cost accounting system:

It is defined as a process which is concerned with anticipation of costs of company's

products for the purpose of analysis of profitability, cost control and inventory valuation.

Estimation of the costs of activities of business accurately is the essence of profitability of the

company. This indicates that ABC company shall know which of its operations are profiterole

while which operations are consuming more of resources and does not live up to the expectations

of business.

Essentials and benefits:

The advantages of cost accounting system is that enables the management in reducing the

,cost, wastage, losses and loopholes by setting standards/bench-marks for every activity within

the organization. It facilitates the managers in identifying the reasons behind profit or loss with

the help of which they take remedial steps for keeping the profitability of company on right

track.

Integration of management accounting systems and management accounting reporting within

organization

Management accounting systems and reporting integration with the other aspects of the

business is necessary because it helps in achieving the efficiencies in the operations. Since, the

information provided by management accounting reports are of qualitative and quantitative

nature, therefore, managers are able to form more quality decisions relating to cost, pricing,

inventory management and cost control. Managerial accounting is integrated with the quality

management in the sense that systems of management accounting assists in measuring and

monitoring the quality related costs which leads to continuous improvement in the processes of

the organization (Francioli and Quagli, 2016). Like inventory management system adopted by

ABC limited helps in managing the inventory in the best way possible. This increases the

efficiency in the production processes by making available the raw material at all time. This

helps in avoiding the stoppage in production process that ultimately results in higher

productivity. Moreover, proper management of inventory also helps in establishing a loyal

customer base by offering the consistent products and services. Thus, this is how the

management accounting systems integrates with the other processes of the business and

improves them for achieving higher efficiency.

TASK 2

Different costing techniques

Marginal costing:

It is defined as a technique of cost accounting in which the marginal cost meaning of

which only variable cost is considered for calculating the unit cost of production. This means that

fixed costs for the relative accounting period is entirely written off against contribution.

Marginal costs of a product is calculated by adding up the direct material& labour, direct

expenses and variable overheads.

Absorption costing:

It refers to a technique of cost accounting in which all the manufacturing expenses

including both fixed and variable are considered for calculating unit cost of production. This

method is required to be adopted by the companies as it is needed for external financial and

income tax reporting (Ghasemi and et.al., 2016).

organization

Management accounting systems and reporting integration with the other aspects of the

business is necessary because it helps in achieving the efficiencies in the operations. Since, the

information provided by management accounting reports are of qualitative and quantitative

nature, therefore, managers are able to form more quality decisions relating to cost, pricing,

inventory management and cost control. Managerial accounting is integrated with the quality

management in the sense that systems of management accounting assists in measuring and

monitoring the quality related costs which leads to continuous improvement in the processes of

the organization (Francioli and Quagli, 2016). Like inventory management system adopted by

ABC limited helps in managing the inventory in the best way possible. This increases the

efficiency in the production processes by making available the raw material at all time. This

helps in avoiding the stoppage in production process that ultimately results in higher

productivity. Moreover, proper management of inventory also helps in establishing a loyal

customer base by offering the consistent products and services. Thus, this is how the

management accounting systems integrates with the other processes of the business and

improves them for achieving higher efficiency.

TASK 2

Different costing techniques

Marginal costing:

It is defined as a technique of cost accounting in which the marginal cost meaning of

which only variable cost is considered for calculating the unit cost of production. This means that

fixed costs for the relative accounting period is entirely written off against contribution.

Marginal costs of a product is calculated by adding up the direct material& labour, direct

expenses and variable overheads.

Absorption costing:

It refers to a technique of cost accounting in which all the manufacturing expenses

including both fixed and variable are considered for calculating unit cost of production. This

method is required to be adopted by the companies as it is needed for external financial and

income tax reporting (Ghasemi and et.al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

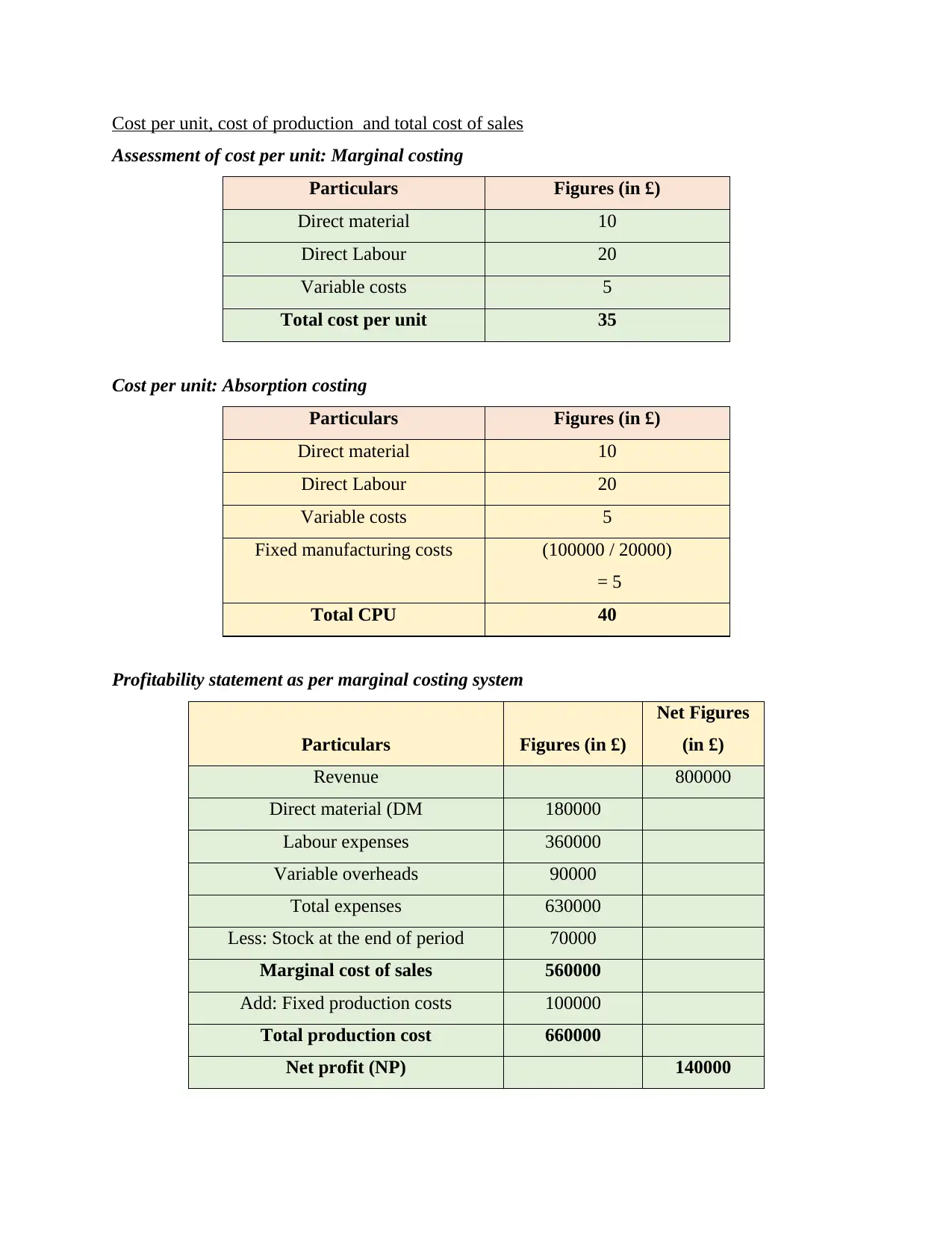

Cost per unit, cost of production and total cost of sales

Assessment of cost per unit: Marginal costing

Particulars Figures (in £)

Direct material 10

Direct Labour 20

Variable costs 5

Total cost per unit 35

Cost per unit: Absorption costing

Particulars Figures (in £)

Direct material 10

Direct Labour 20

Variable costs 5

Fixed manufacturing costs (100000 / 20000)

= 5

Total CPU 40

Profitability statement as per marginal costing system

Particulars Figures (in £)

Net Figures

(in £)

Revenue 800000

Direct material (DM 180000

Labour expenses 360000

Variable overheads 90000

Total expenses 630000

Less: Stock at the end of period 70000

Marginal cost of sales 560000

Add: Fixed production costs 100000

Total production cost 660000

Net profit (NP) 140000

Assessment of cost per unit: Marginal costing

Particulars Figures (in £)

Direct material 10

Direct Labour 20

Variable costs 5

Total cost per unit 35

Cost per unit: Absorption costing

Particulars Figures (in £)

Direct material 10

Direct Labour 20

Variable costs 5

Fixed manufacturing costs (100000 / 20000)

= 5

Total CPU 40

Profitability statement as per marginal costing system

Particulars Figures (in £)

Net Figures

(in £)

Revenue 800000

Direct material (DM 180000

Labour expenses 360000

Variable overheads 90000

Total expenses 630000

Less: Stock at the end of period 70000

Marginal cost of sales 560000

Add: Fixed production costs 100000

Total production cost 660000

Net profit (NP) 140000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

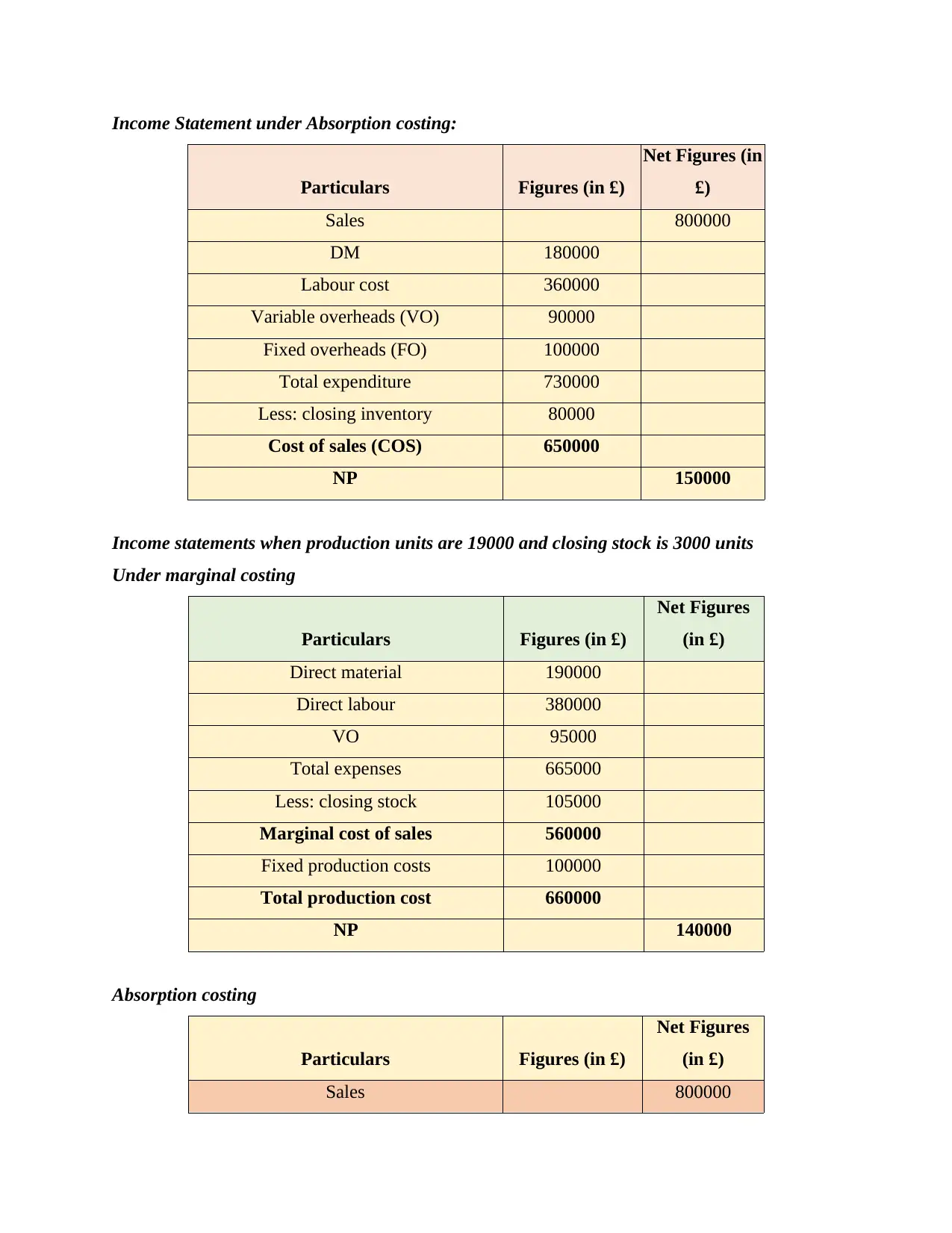

Income Statement under Absorption costing:

Particulars Figures (in £)

Net Figures (in

£)

Sales 800000

DM 180000

Labour cost 360000

Variable overheads (VO) 90000

Fixed overheads (FO) 100000

Total expenditure 730000

Less: closing inventory 80000

Cost of sales (COS) 650000

NP 150000

Income statements when production units are 19000 and closing stock is 3000 units

Under marginal costing

Particulars Figures (in £)

Net Figures

(in £)

Direct material 190000

Direct labour 380000

VO 95000

Total expenses 665000

Less: closing stock 105000

Marginal cost of sales 560000

Fixed production costs 100000

Total production cost 660000

NP 140000

Absorption costing

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

Particulars Figures (in £)

Net Figures (in

£)

Sales 800000

DM 180000

Labour cost 360000

Variable overheads (VO) 90000

Fixed overheads (FO) 100000

Total expenditure 730000

Less: closing inventory 80000

Cost of sales (COS) 650000

NP 150000

Income statements when production units are 19000 and closing stock is 3000 units

Under marginal costing

Particulars Figures (in £)

Net Figures

(in £)

Direct material 190000

Direct labour 380000

VO 95000

Total expenses 665000

Less: closing stock 105000

Marginal cost of sales 560000

Fixed production costs 100000

Total production cost 660000

NP 140000

Absorption costing

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

DM 190000

DL 380000

VO 95000

FO 100000

Total expenses 765000

Less: closing stock 80000

COS 685000

NP 800000

Interpretation :

It can be observed that profits when production units were 18000 and when it 19000 are

same under both the methods. This is due to fact that as production units increased by 1000 units,

closing stock also increased by 1000 units which nullify the effect of each other.

Reasons for change in the profit or loss under both the methods :

The primary reason is that closing stock under the marginal costing method is valued at a

price which is exclusive of fixed manufacturing fixed overheads while in the absorption costing,

the closing stock is valued at a price which is inclusive of all the expenses that is both variable

and fixed overheads.

TASK 3

Benefits and drawbacks of various kinds of planning tools applied in budgetary control

Budgetary control is described as a process of formulation of budgets for various

operations of the business and comparison of anticipated figures with the actual results for the

purpose of arriving at some deviations or variances. The object is to identify the variances and

correct them for attaining the efficiencies in the operations of the ABC Limited. There are

different types of planning tools which the managers of the company uses for controlling the

activities of business (Johnstone, 2018). These are as follows:

Static budget:

In the simpler terms, a static budget is referred to a budget which does not variate with

the change in sales. This budget incorporates the estimated values relating to expenses and

income which are conceived before the beginning of budget period.

Benefits:

DL 380000

VO 95000

FO 100000

Total expenses 765000

Less: closing stock 80000

COS 685000

NP 800000

Interpretation :

It can be observed that profits when production units were 18000 and when it 19000 are

same under both the methods. This is due to fact that as production units increased by 1000 units,

closing stock also increased by 1000 units which nullify the effect of each other.

Reasons for change in the profit or loss under both the methods :

The primary reason is that closing stock under the marginal costing method is valued at a

price which is exclusive of fixed manufacturing fixed overheads while in the absorption costing,

the closing stock is valued at a price which is inclusive of all the expenses that is both variable

and fixed overheads.

TASK 3

Benefits and drawbacks of various kinds of planning tools applied in budgetary control

Budgetary control is described as a process of formulation of budgets for various

operations of the business and comparison of anticipated figures with the actual results for the

purpose of arriving at some deviations or variances. The object is to identify the variances and

correct them for attaining the efficiencies in the operations of the ABC Limited. There are

different types of planning tools which the managers of the company uses for controlling the

activities of business (Johnstone, 2018). These are as follows:

Static budget:

In the simpler terms, a static budget is referred to a budget which does not variate with

the change in sales. This budget incorporates the estimated values relating to expenses and

income which are conceived before the beginning of budget period.

Benefits:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The foremost advantage of this kind of budget is that is easy to form, understand and

implement due to the fact no continuous changes are to be made throughout the intended

accounting period. It is also helpful in the sense that preparation of static budget makes it easier

for the management in determining the anticipated taxes which are paid in the future accounting

period (What Are the Advantages and Disadvantages of Using a Static Budget, 2019).

Drawbacks:

The biggest drawback of static or fixed budget is that it does not allow any flexibility.

This means that no changes can be done in the static budget for extracting the benefits of

changes in revenues and expense as the time period progress. For example, if by the of

comparing the budgets with actual results, the organization finds any area which is

underperforming, it can not re-allocate the resources for bringing the efficiency in such areas.

Flexible budget:

This budgets are those budgets which allows the managers to adjust the anticipated

amounts as the time period progress. In other words, this method allows room for budget

inflation which depicts more realistic forecasting through which more reliable results could be

drawn.

Benefits:

More reliable and realistic forecasting is done by this type of budgeting since it takes into

consideration the budget inflation. This leads to better monitoring and controlling of the

activities of the business. Moreover, the budgets are updated with the latest data.

Drawbacks:

The main limitation of this type of budgeting is that it is confusing. This is because these

budgets requires continuous planning for keeping the track of expenditures and making

adjustments for the variations for the intended time period (Kalkhouran and et.al., 2015). Further,

such budgets allows managers to spend more than the boundaries set for the specific time period.

Zero base budgeting:

It is a type of budgeting in which the managers start with scratch or zero base for each of

item or activity that is to be included in the budget list. Each of the activity is comprehensively

evaluated and analysed. The main objective of this zero base budgeting is to reduce the

unnecessary expenses or costs by looking closely in what areas, the costs can be cut in order to

bring efficiency in the business processes.

implement due to the fact no continuous changes are to be made throughout the intended

accounting period. It is also helpful in the sense that preparation of static budget makes it easier

for the management in determining the anticipated taxes which are paid in the future accounting

period (What Are the Advantages and Disadvantages of Using a Static Budget, 2019).

Drawbacks:

The biggest drawback of static or fixed budget is that it does not allow any flexibility.

This means that no changes can be done in the static budget for extracting the benefits of

changes in revenues and expense as the time period progress. For example, if by the of

comparing the budgets with actual results, the organization finds any area which is

underperforming, it can not re-allocate the resources for bringing the efficiency in such areas.

Flexible budget:

This budgets are those budgets which allows the managers to adjust the anticipated

amounts as the time period progress. In other words, this method allows room for budget

inflation which depicts more realistic forecasting through which more reliable results could be

drawn.

Benefits:

More reliable and realistic forecasting is done by this type of budgeting since it takes into

consideration the budget inflation. This leads to better monitoring and controlling of the

activities of the business. Moreover, the budgets are updated with the latest data.

Drawbacks:

The main limitation of this type of budgeting is that it is confusing. This is because these

budgets requires continuous planning for keeping the track of expenditures and making

adjustments for the variations for the intended time period (Kalkhouran and et.al., 2015). Further,

such budgets allows managers to spend more than the boundaries set for the specific time period.

Zero base budgeting:

It is a type of budgeting in which the managers start with scratch or zero base for each of

item or activity that is to be included in the budget list. Each of the activity is comprehensively

evaluated and analysed. The main objective of this zero base budgeting is to reduce the

unnecessary expenses or costs by looking closely in what areas, the costs can be cut in order to

bring efficiency in the business processes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits:

The biggest advantage of this budgeting is that it does not create a budget on the basis of

past or previous budget data. Rather, the budget is prepared from a zero base which helps in

optimal allocation of resources within the various departments of the business. Since, budget

inflation and other changes relating to sales, expense are taken into consideration in between the

time period, the forecasting made by applying this technique is more accurate and correct (Luft,

Shields and Thomas, 2016).

Drawbacks:

Although zero based budgeting offers many advantages to the organization, it has some

drawbacks which makes its application more difficult within the business. This budgeting suffers

from the limitation that it requires large number of skilled employees who can perform this type

of budgeting. Moreover, zero based budgeting requires huge amount of time which is sometimes

not feasible for the smaller or medium size organization.

Use of planning tools for preparing and forecasting budgets

Managers of ABC Ltd applies different planning tools for preparing and forecasting of its

expenditures and income. For example, cash flow statements helps in assessing the pattern of

how company generates its cash inflows and what are the activities which takes up the most of

the financial resources. Below is a cash budget by which ABC Ltd., management ascertains how

cash inflows and outflows would take place within the business over a specific period of time:

CASH BUDGET

(For the next three months)

Particulars Initial

investment August September October

Sales of financial products

Number of consumers 28000 30800 33880

Average cost 38 38 38

Total revenue from products (1) 1065167 1171683 1288852

The biggest advantage of this budgeting is that it does not create a budget on the basis of

past or previous budget data. Rather, the budget is prepared from a zero base which helps in

optimal allocation of resources within the various departments of the business. Since, budget

inflation and other changes relating to sales, expense are taken into consideration in between the

time period, the forecasting made by applying this technique is more accurate and correct (Luft,

Shields and Thomas, 2016).

Drawbacks:

Although zero based budgeting offers many advantages to the organization, it has some

drawbacks which makes its application more difficult within the business. This budgeting suffers

from the limitation that it requires large number of skilled employees who can perform this type

of budgeting. Moreover, zero based budgeting requires huge amount of time which is sometimes

not feasible for the smaller or medium size organization.

Use of planning tools for preparing and forecasting budgets

Managers of ABC Ltd applies different planning tools for preparing and forecasting of its

expenditures and income. For example, cash flow statements helps in assessing the pattern of

how company generates its cash inflows and what are the activities which takes up the most of

the financial resources. Below is a cash budget by which ABC Ltd., management ascertains how

cash inflows and outflows would take place within the business over a specific period of time:

CASH BUDGET

(For the next three months)

Particulars Initial

investment August September October

Sales of financial products

Number of consumers 28000 30800 33880

Average cost 38 38 38

Total revenue from products (1) 1065167 1171683 1288852

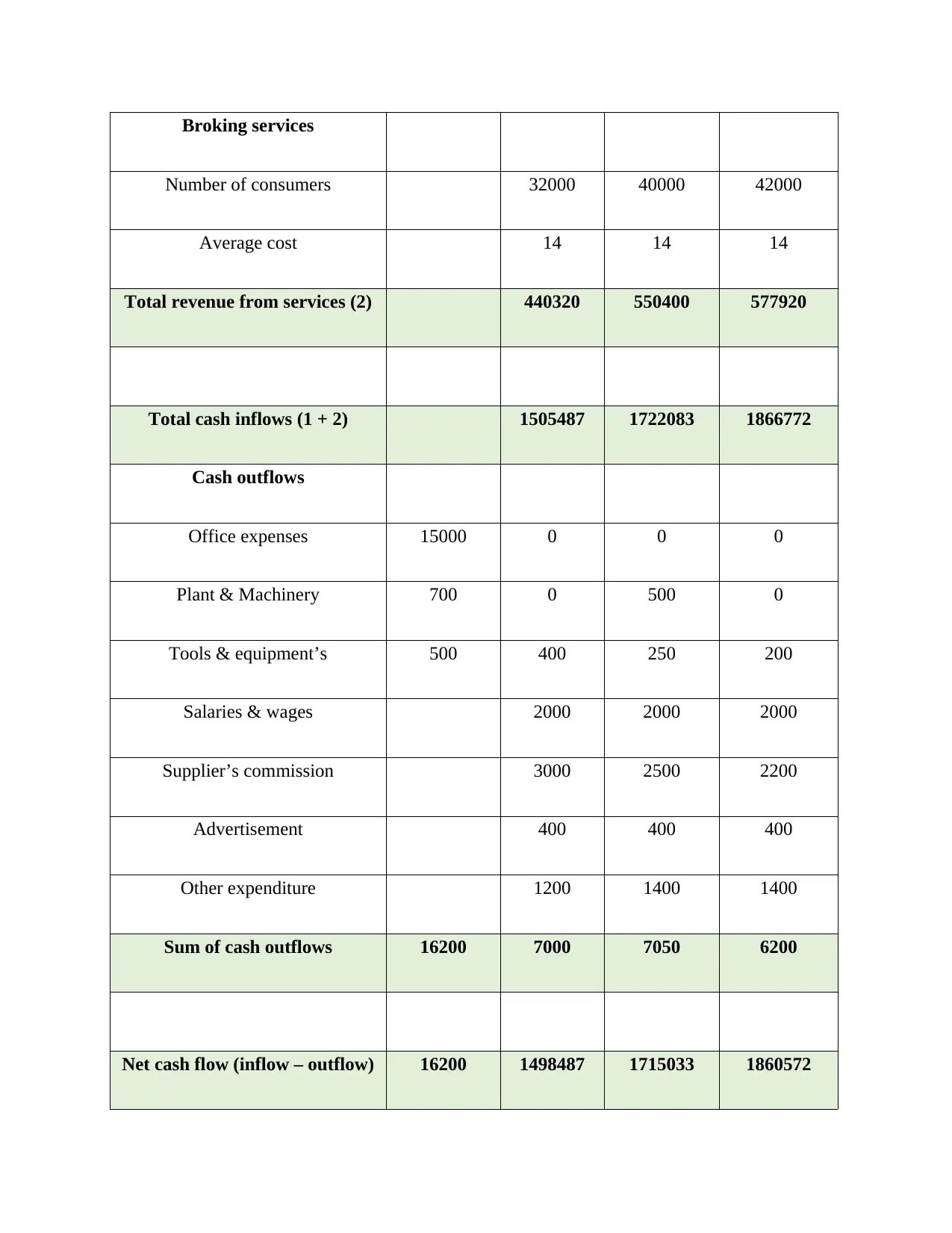

Broking services

Number of consumers 32000 40000 42000

Average cost 14 14 14

Total revenue from services (2) 440320 550400 577920

Total cash inflows (1 + 2) 1505487 1722083 1866772

Cash outflows

Office expenses 15000 0 0 0

Plant & Machinery 700 0 500 0

Tools & equipment’s 500 400 250 200

Salaries & wages 2000 2000 2000

Supplier’s commission 3000 2500 2200

Advertisement 400 400 400

Other expenditure 1200 1400 1400

Sum of cash outflows 16200 7000 7050 6200

Net cash flow (inflow – outflow) 16200 1498487 1715033 1860572

Number of consumers 32000 40000 42000

Average cost 14 14 14

Total revenue from services (2) 440320 550400 577920

Total cash inflows (1 + 2) 1505487 1722083 1866772

Cash outflows

Office expenses 15000 0 0 0

Plant & Machinery 700 0 500 0

Tools & equipment’s 500 400 250 200

Salaries & wages 2000 2000 2000

Supplier’s commission 3000 2500 2200

Advertisement 400 400 400

Other expenditure 1200 1400 1400

Sum of cash outflows 16200 7000 7050 6200

Net cash flow (inflow – outflow) 16200 1498487 1715033 1860572

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.