Management Accounting Report: Mittelstand Case Study Analysis

VerifiedAdded on 2020/06/04

|18

|5179

|316

Report

AI Summary

This report provides a comprehensive overview of management accounting, emphasizing its crucial role in business decision-making, particularly for small and medium-sized enterprises (SMEs) like Mittelstand. It differentiates between management and financial accounting, highlighting the significance of management accounting in generating timely and accurate financial and statistical information. The report delves into the importance of management accounting in cost analysis, production decisions, and data utilization. It explores three key management accounting systems: budgeting and budgeting, marginal costing, and ratio analysis, outlining their advantages and disadvantages. The report also critically evaluates the benefits of management accounting systems, including budgeting control, marginal costing, and standard costing. The report examines the effectiveness of management accounting in dealing with financial problems and contributing to business success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

1 Importance of management accounting in decision-making process for improve

performances...............................................................................................................................1

2. Three types of management accounting system used for report of management accounting.2

3. Critically evaluates benefits of management accounting system............................................3

4. (a) Absorption costing and marginal costing techniques........................................................4

4. (b) Supportive calculation and demonstrate profit in each method........................................7

4. (c) Produce reconciled statements of profit and loss..............................................................8

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

(a) Compare different management accounting methods...........................................................8

Comparison among the different three tools.............................................................................11

PART B..........................................................................................................................................12

Effectiveness of management accounting to deal with financial problems..............................12

Assess problem to respond towards financial problem, management accounting to lead with

business success........................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

1 Importance of management accounting in decision-making process for improve

performances...............................................................................................................................1

2. Three types of management accounting system used for report of management accounting.2

3. Critically evaluates benefits of management accounting system............................................3

4. (a) Absorption costing and marginal costing techniques........................................................4

4. (b) Supportive calculation and demonstrate profit in each method........................................7

4. (c) Produce reconciled statements of profit and loss..............................................................8

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

(a) Compare different management accounting methods...........................................................8

Comparison among the different three tools.............................................................................11

PART B..........................................................................................................................................12

Effectiveness of management accounting to deal with financial problems..............................12

Assess problem to respond towards financial problem, management accounting to lead with

business success........................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Management accounting is the important part of every business which include procedure

for develop report and account. It helps to managers to make effective financial statements to

take day to day operations (Otley and Emmanuel, 2013). Further, short term plan can also be

made in successful way for ascertain more effective results. In this context, report based on the

Mittelstand which is small and medium enterprise which deals in machinery, auto parts,

chemicals and many electrical equipment’s. For gaining insight knowledge of the company,

present report covers understanding of the management accounting system. Furthermore, it

includes use of planning tools that are used in management accounting. Moreover, it discusses

about ways of management accounting which applied on effectiveness of financial outcomes.

SECTION 1

PART A

1 Importance of management accounting in decision-making process for improve performances

Management Accounting-management accounting involves the process of preparing

various reports and account in order to get timely and accurate financial and statistical

information for making various short as well as long term decisions (Bebbington, Unerman and

O'Dwyer, 2014). For instance sales report generated buy using management accounting is

utilised by various stakeholder in order to gain knowledge about profitability of organisations.

These reports typically present data related to cash receivable, payable, cash in hand, raw

material, stock in hand etc.

Financial accounting-Financial accounting is the process which is conducted to keep

track in firm financial transaction. Financial report is produced by financial accounting system in

which various transaction are recorded in summarised way and presented in systematic manner

as well in proper format. Example of financial report are income and expenditure account,

balance sheet etc.

Difference between management accounting and financial accounting

Financial accounting Management accounting

Financial accounting is focussed on financial 1. Management accounting has focus on

1

Management accounting is the important part of every business which include procedure

for develop report and account. It helps to managers to make effective financial statements to

take day to day operations (Otley and Emmanuel, 2013). Further, short term plan can also be

made in successful way for ascertain more effective results. In this context, report based on the

Mittelstand which is small and medium enterprise which deals in machinery, auto parts,

chemicals and many electrical equipment’s. For gaining insight knowledge of the company,

present report covers understanding of the management accounting system. Furthermore, it

includes use of planning tools that are used in management accounting. Moreover, it discusses

about ways of management accounting which applied on effectiveness of financial outcomes.

SECTION 1

PART A

1 Importance of management accounting in decision-making process for improve performances

Management Accounting-management accounting involves the process of preparing

various reports and account in order to get timely and accurate financial and statistical

information for making various short as well as long term decisions (Bebbington, Unerman and

O'Dwyer, 2014). For instance sales report generated buy using management accounting is

utilised by various stakeholder in order to gain knowledge about profitability of organisations.

These reports typically present data related to cash receivable, payable, cash in hand, raw

material, stock in hand etc.

Financial accounting-Financial accounting is the process which is conducted to keep

track in firm financial transaction. Financial report is produced by financial accounting system in

which various transaction are recorded in summarised way and presented in systematic manner

as well in proper format. Example of financial report are income and expenditure account,

balance sheet etc.

Difference between management accounting and financial accounting

Financial accounting Management accounting

Financial accounting is focussed on financial 1. Management accounting has focus on

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities carried out by organisations.

2.Some set standard are required to be

followed in financial accounting.

3.Financial accounting aim at providing only

quantitative data.

4.It helps manager in analysing financial

position of company.

operational reports which are distributed within

a company.

2. There are no set standards in management

accounting.

3. Management accounting provide\s both

quantitative and qualitative data.

4.It provides assistance to manger in making

various decision (Otley and Emmanuel, 2013).

Management accounting profession involves partnering in the management for decision-

making. In addition to this, it is the system of devising plans and performance that provides

expertise for financial reporting and formulate management plans (Bebbington, Unerman and

O'Dwyer, 2014). In order to contributing development, competent framework has been taken

significant in Mittelstand for decision-making. They are as follows:

Cost analysis: In the management accounting information system, there are different

types of important elements helps in business to perform functions of cost assessment. With the

help of this method, Mittelstand can take decisions to sell specific type or product and services.

Moreover, it also serves information for cost level and extent relevant results on it (Ammar,

2017). For example, management accounting system helps in to take decisions for marketing

efforts and plans as well. In this the chosen organisation, manager has aim to take decisions to

use alternative mode of the advertisement. It will assist to assess common cost which can be

helps in conducting research (Otley, 2016).

Ascertain decision to produce or buying: Another importance of management

accounting is ascertained decision to face several problems and issues that relate to buying

product or its production (Freedman, 2017). In this aspect, Mittelstand need to assess cost for

production and compare it with purchasing product. Therefore, it will help to take decisions for

select the best alternative from several points. In this using system, management accounting

business also decide to produce cost component that needed for buying products from others.

Data utilization: With the help of different tools and techniques of the management

accounting, budget, variance and many other things will be calculated that helps to take decision

for future outcomes (Northcott, 2014). In this aspect, employees of Mittelstand need to take

2

2.Some set standard are required to be

followed in financial accounting.

3.Financial accounting aim at providing only

quantitative data.

4.It helps manager in analysing financial

position of company.

operational reports which are distributed within

a company.

2. There are no set standards in management

accounting.

3. Management accounting provide\s both

quantitative and qualitative data.

4.It provides assistance to manger in making

various decision (Otley and Emmanuel, 2013).

Management accounting profession involves partnering in the management for decision-

making. In addition to this, it is the system of devising plans and performance that provides

expertise for financial reporting and formulate management plans (Bebbington, Unerman and

O'Dwyer, 2014). In order to contributing development, competent framework has been taken

significant in Mittelstand for decision-making. They are as follows:

Cost analysis: In the management accounting information system, there are different

types of important elements helps in business to perform functions of cost assessment. With the

help of this method, Mittelstand can take decisions to sell specific type or product and services.

Moreover, it also serves information for cost level and extent relevant results on it (Ammar,

2017). For example, management accounting system helps in to take decisions for marketing

efforts and plans as well. In this the chosen organisation, manager has aim to take decisions to

use alternative mode of the advertisement. It will assist to assess common cost which can be

helps in conducting research (Otley, 2016).

Ascertain decision to produce or buying: Another importance of management

accounting is ascertained decision to face several problems and issues that relate to buying

product or its production (Freedman, 2017). In this aspect, Mittelstand need to assess cost for

production and compare it with purchasing product. Therefore, it will help to take decisions for

select the best alternative from several points. In this using system, management accounting

business also decide to produce cost component that needed for buying products from others.

Data utilization: With the help of different tools and techniques of the management

accounting, budget, variance and many other things will be calculated that helps to take decision

for future outcomes (Northcott, 2014). In this aspect, employees of Mittelstand need to take

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

participation to collect information. For example, with comparing actual performance and

standards, monetary aspects can be measures. Therefore, it will be helpful to find cause for

assess deviations that occurred in financial aspects. With taking consideration in this process,

business unit will easily able to enhance strategies and policies for financial performances

(Soderstrom, Soderstrom and Stewart, 2017).

Technique activity based costing: Activity based costing helps in the organisation to

assess activities which needed to perform functions for manufacturing industry. Specific

products and services can be develop in systematic way in Mittelstand through getting

information about individual customers. In addition to this, it is the good method in which

awareness can be created that are highly profitable for sales and profits as well (Avery, 2016).

2. Three types of management accounting system used for report of management accounting

There are different types of management accounting system can be used by the enterprise

which explained under here:

Budget and budgeting: In the present aspect, each enterprise place very important place

to prepare their budget plan with estimating expenses and income. In the budget,

managers allocate fund to perform activity that required for smooth functions (Taylor and

Scapens, 2016). However, it also demonstrates direction for employees to create way for

investment. Budgeting is the most important method which helps in management to

ensure optimum utilization of resources. In addition to this, in Mittelstand budgeting also

provide deeper knowledge towards management about the several areas which suitable to

take action for improvements. In this aspect, budgeting tools and techniques helps in

respect to ascertain high profitable outcomes to prepare suitable framework (Jazayeri and

Ahmed, 2016). In the inflationary condition, budget also prepare for future outcomes and

results in successful manner. It is highly possible for the firm to predict effective future

situation into the right direction. Further, uncertainties can also be cater which influence

to utility of budget. Success of budgetary system also affect to the top management.

Therefore, higher management fails to provide enough fund to each department

(Hyndman, 2016).

Advantages of budgets

Budgeting system plays an important role in efficient allocation of resources such as it

helps in planning investment.

3

standards, monetary aspects can be measures. Therefore, it will be helpful to find cause for

assess deviations that occurred in financial aspects. With taking consideration in this process,

business unit will easily able to enhance strategies and policies for financial performances

(Soderstrom, Soderstrom and Stewart, 2017).

Technique activity based costing: Activity based costing helps in the organisation to

assess activities which needed to perform functions for manufacturing industry. Specific

products and services can be develop in systematic way in Mittelstand through getting

information about individual customers. In addition to this, it is the good method in which

awareness can be created that are highly profitable for sales and profits as well (Avery, 2016).

2. Three types of management accounting system used for report of management accounting

There are different types of management accounting system can be used by the enterprise

which explained under here:

Budget and budgeting: In the present aspect, each enterprise place very important place

to prepare their budget plan with estimating expenses and income. In the budget,

managers allocate fund to perform activity that required for smooth functions (Taylor and

Scapens, 2016). However, it also demonstrates direction for employees to create way for

investment. Budgeting is the most important method which helps in management to

ensure optimum utilization of resources. In addition to this, in Mittelstand budgeting also

provide deeper knowledge towards management about the several areas which suitable to

take action for improvements. In this aspect, budgeting tools and techniques helps in

respect to ascertain high profitable outcomes to prepare suitable framework (Jazayeri and

Ahmed, 2016). In the inflationary condition, budget also prepare for future outcomes and

results in successful manner. It is highly possible for the firm to predict effective future

situation into the right direction. Further, uncertainties can also be cater which influence

to utility of budget. Success of budgetary system also affect to the top management.

Therefore, higher management fails to provide enough fund to each department

(Hyndman, 2016).

Advantages of budgets

Budgeting system plays an important role in efficient allocation of resources such as it

helps in planning investment.

3

It enables management to identify various risk and analyse various opportunities and

provides the way to capture such opportunities. For example it provides the prevention

and cure for various risk (Otley and Emmanuel, 2013).

Budgetary-control system provides the various method to control various activities and it

assists organisation in various planning process. For instance it assists management in

planning various expenses.

Budget provides direction to convert various resources into profitable channel.

Budgetary system provide opportunity to management to decentralise their authority

without losing any control.

Disadvantages

The limitation of budgetary system is that it is based on estimation.

This system consumes lot of time and its is cost consuming too.

Marginal cost: Marginal cost analysis used in the business to assess effective pricing

strategy to assess break-even point and assess actual profit as well. With conducting break-even

analysis, Mittelstand can easily assess actual profits and loss which encounter in the business. It

also drives number of units that needed to produce and sell to assess desired profits (Quinn,

2014). In this way, marginal costing method provides high freedom over and under the

absorption of overhead.

Advantages

This system is simple and easy to operate.

This system assist enterprise in comparing various cost.

It enables organisation to make effective decisions.

It helps in analysing the contribution of various product in generating profit.

Disadvantages

It only provides data related to total cost, it does not provide separate data related to fixed

and variable cost (Otley and Emmanuel, 2013).

This system do not include evaluation of variable overheads.

Ratio analysis: This tool helps to the organisation to assess financial health and performances in

effective aspect. This will help to forecast, making plan and performing many other activities in

Mittelstand. Ratio analysis assists to getting information to generate more profits by the

enterprise over the expenses (Hiebl, 2017). In addition to this, liquidity ratio entails extent in

4

provides the way to capture such opportunities. For example it provides the prevention

and cure for various risk (Otley and Emmanuel, 2013).

Budgetary-control system provides the various method to control various activities and it

assists organisation in various planning process. For instance it assists management in

planning various expenses.

Budget provides direction to convert various resources into profitable channel.

Budgetary system provide opportunity to management to decentralise their authority

without losing any control.

Disadvantages

The limitation of budgetary system is that it is based on estimation.

This system consumes lot of time and its is cost consuming too.

Marginal cost: Marginal cost analysis used in the business to assess effective pricing

strategy to assess break-even point and assess actual profit as well. With conducting break-even

analysis, Mittelstand can easily assess actual profits and loss which encounter in the business. It

also drives number of units that needed to produce and sell to assess desired profits (Quinn,

2014). In this way, marginal costing method provides high freedom over and under the

absorption of overhead.

Advantages

This system is simple and easy to operate.

This system assist enterprise in comparing various cost.

It enables organisation to make effective decisions.

It helps in analysing the contribution of various product in generating profit.

Disadvantages

It only provides data related to total cost, it does not provide separate data related to fixed

and variable cost (Otley and Emmanuel, 2013).

This system do not include evaluation of variable overheads.

Ratio analysis: This tool helps to the organisation to assess financial health and performances in

effective aspect. This will help to forecast, making plan and performing many other activities in

Mittelstand. Ratio analysis assists to getting information to generate more profits by the

enterprise over the expenses (Hiebl, 2017). In addition to this, liquidity ratio entails extent in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which organisation has enough amount of money to meet with current liabilities and obligations

as well. Ratio analysis performances in term of controlling directly measures expenses so that it

is the main method which used for analysis performance in cost control (DRURY, 2013).

Advantages

This system helps in identifying the efficiency of working capital.

It assists business unit in examining its current financial position.

This system provide aid to management in preparing various financial estimations for

future.

This system facilitates task managerial control (Jazayeri and Ahmed, 2016).

This system is very useful for bench marking purpose, to compare working performance

of organisation with its competitors performance.

Disadvantages

The ratio analysis system may have narrow focus on certain elements of enterprise

financial performance.

Certain ratios may get influenced by the accounting methodology used by firm.

3. Critically evaluates benefits of management accounting system

In this aspect, following are certain benefits of management accounting information

system in Mittelstand:

Budgeting control: This technique of the management accounting assist to encourage

each personal to work in effective manner and accomplish predetermined goals as well. With the

help of performing several activities in different department, Mittelstand can control their

operations to pursue it in the large extent (Mokhtar, Jusoh and Zulkifli, 2016). However,

budgeting control tool is very helpful to provide effective assistance in the firm enhance

coordination in different personnel in each department (Venkatesh, 2017). Therefore,

performances level can be assessed as per the expectation level to management to find

responsibility level. In addition to this, tool and techniques also assists to ensure smooth

functioning in business activities and operations.

Marginal costing: This costing helps in the business to exerting control over the cost

level in the large extent. In the marginal costing, arbitrary allocations of fixed cost easily

ignored. In addition to this, it is the easiest method to determine number of units which

Mittelstand offers to customers for recover initial amount. When level exceeded so that

5

as well. Ratio analysis performances in term of controlling directly measures expenses so that it

is the main method which used for analysis performance in cost control (DRURY, 2013).

Advantages

This system helps in identifying the efficiency of working capital.

It assists business unit in examining its current financial position.

This system provide aid to management in preparing various financial estimations for

future.

This system facilitates task managerial control (Jazayeri and Ahmed, 2016).

This system is very useful for bench marking purpose, to compare working performance

of organisation with its competitors performance.

Disadvantages

The ratio analysis system may have narrow focus on certain elements of enterprise

financial performance.

Certain ratios may get influenced by the accounting methodology used by firm.

3. Critically evaluates benefits of management accounting system

In this aspect, following are certain benefits of management accounting information

system in Mittelstand:

Budgeting control: This technique of the management accounting assist to encourage

each personal to work in effective manner and accomplish predetermined goals as well. With the

help of performing several activities in different department, Mittelstand can control their

operations to pursue it in the large extent (Mokhtar, Jusoh and Zulkifli, 2016). However,

budgeting control tool is very helpful to provide effective assistance in the firm enhance

coordination in different personnel in each department (Venkatesh, 2017). Therefore,

performances level can be assessed as per the expectation level to management to find

responsibility level. In addition to this, tool and techniques also assists to ensure smooth

functioning in business activities and operations.

Marginal costing: This costing helps in the business to exerting control over the cost

level in the large extent. In the marginal costing, arbitrary allocations of fixed cost easily

ignored. In addition to this, it is the easiest method to determine number of units which

Mittelstand offers to customers for recover initial amount. When level exceeded so that

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation able to accomplish their profit margin. This type of technique assists to create

relationship between cost and volume of profit margin (Bebbington, Unerman and O'Dwyer,

2014). With assessment of break-even point, the chosen enterprise will easily focus on efficiency

and sales efforts for development.

Standard costing-It refers to the tool for preparing, managing, controlling cost and

calculating cost management performance. Standard accounting process includes estimating

various cost of material and other fixed and variable cost that might be required in production

process. For instance setting standards regarding particular amount of money required in product

process of specific item (Bebbington, Unerman and O'Dwyer, 2014). This process is required to

prepare budget for production process.

Advantages :

This method can be used fir reducing various cost and also for controlling various

expenses.

It assists manger in taking various decision related to production process.

Disadvantages

It is time consuming process

This costing system require regular update.

There are number of resources required by this costing system such as labour, time.

This system of costing is quite expensive.

Ratio analysis: Ratio analysis is the most important method that used for assessment of

facts and figures that present in financial statements such as income. Further, it could be

observed that income statements is the direct cost that evaluates cost of production that covered

in the enterprise (Soderstrom, Soderstrom and Stewart, 2017).

4. (a) Absorption costing and marginal costing techniques

Absorption costing: It is the costing which known as the different names such as

complete the full costing. In this method, there are different types of sort of costs which taken in

account namely on fixed and variable cost. Beside this, variable expenses also gather valued

which get changed with variations that are observed in manufacturing of products in Mittelstand.

In the present costing, there are different kinds of things has been used for absorption costing for

specific job at the production place (Mokhtar, Jusoh and Zulkifli, 2016). It laid down to the

6

relationship between cost and volume of profit margin (Bebbington, Unerman and O'Dwyer,

2014). With assessment of break-even point, the chosen enterprise will easily focus on efficiency

and sales efforts for development.

Standard costing-It refers to the tool for preparing, managing, controlling cost and

calculating cost management performance. Standard accounting process includes estimating

various cost of material and other fixed and variable cost that might be required in production

process. For instance setting standards regarding particular amount of money required in product

process of specific item (Bebbington, Unerman and O'Dwyer, 2014). This process is required to

prepare budget for production process.

Advantages :

This method can be used fir reducing various cost and also for controlling various

expenses.

It assists manger in taking various decision related to production process.

Disadvantages

It is time consuming process

This costing system require regular update.

There are number of resources required by this costing system such as labour, time.

This system of costing is quite expensive.

Ratio analysis: Ratio analysis is the most important method that used for assessment of

facts and figures that present in financial statements such as income. Further, it could be

observed that income statements is the direct cost that evaluates cost of production that covered

in the enterprise (Soderstrom, Soderstrom and Stewart, 2017).

4. (a) Absorption costing and marginal costing techniques

Absorption costing: It is the costing which known as the different names such as

complete the full costing. In this method, there are different types of sort of costs which taken in

account namely on fixed and variable cost. Beside this, variable expenses also gather valued

which get changed with variations that are observed in manufacturing of products in Mittelstand.

In the present costing, there are different kinds of things has been used for absorption costing for

specific job at the production place (Mokhtar, Jusoh and Zulkifli, 2016). It laid down to the

6

major attention on several minor distribution of the varied sort of the expenses in business unit. It

is the best method to cater effective results.

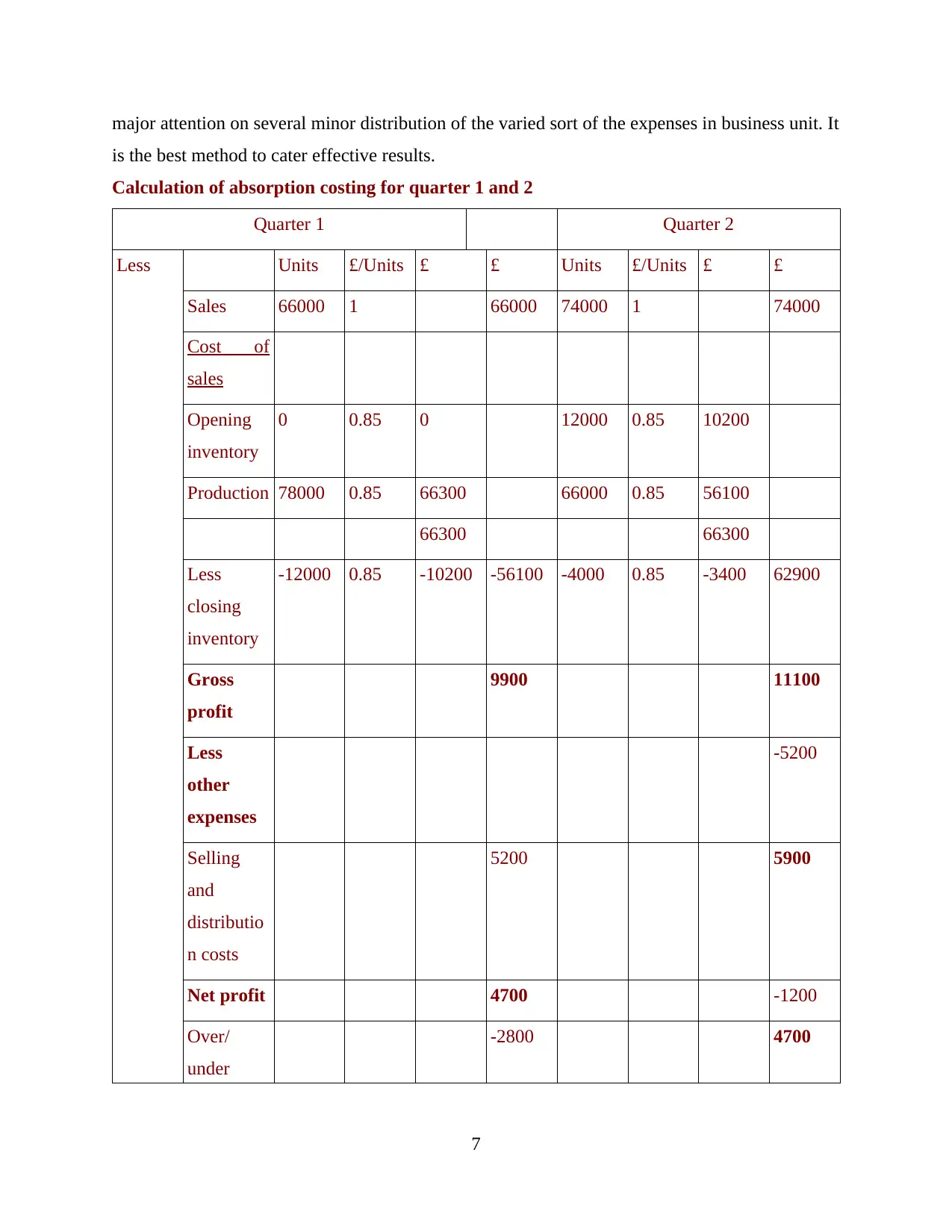

Calculation of absorption costing for quarter 1 and 2

Quarter 1 Quarter 2

Less Units £/Units £ £ Units £/Units £ £

Sales 66000 1 66000 74000 1 74000

Cost of

sales

Opening

inventory

0 0.85 0 12000 0.85 10200

Production 78000 0.85 66300 66000 0.85 56100

66300 66300

Less

closing

inventory

-12000 0.85 -10200 -56100 -4000 0.85 -3400 62900

Gross

profit

9900 11100

Less

other

expenses

-5200

Selling

and

distributio

n costs

5200 5900

Net profit 4700 -1200

Over/

under

-2800 4700

7

is the best method to cater effective results.

Calculation of absorption costing for quarter 1 and 2

Quarter 1 Quarter 2

Less Units £/Units £ £ Units £/Units £ £

Sales 66000 1 66000 74000 1 74000

Cost of

sales

Opening

inventory

0 0.85 0 12000 0.85 10200

Production 78000 0.85 66300 66000 0.85 56100

66300 66300

Less

closing

inventory

-12000 0.85 -10200 -56100 -4000 0.85 -3400 62900

Gross

profit

9900 11100

Less

other

expenses

-5200

Selling

and

distributio

n costs

5200 5900

Net profit 4700 -1200

Over/

under

-2800 4700

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

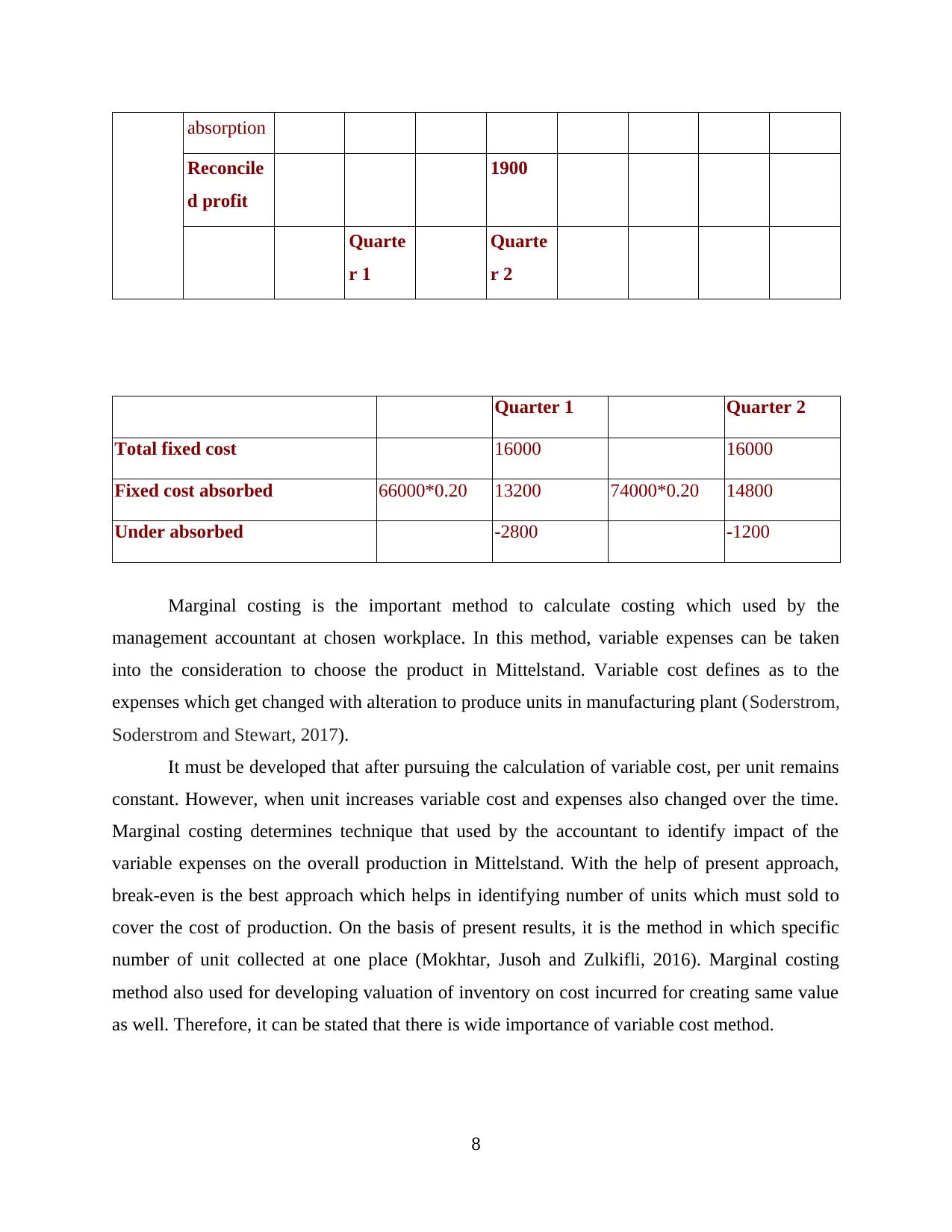

absorption

Reconcile

d profit

1900

Quarte

r 1

Quarte

r 2

Quarter 1 Quarter 2

Total fixed cost 16000 16000

Fixed cost absorbed 66000*0.20 13200 74000*0.20 14800

Under absorbed -2800 -1200

Marginal costing is the important method to calculate costing which used by the

management accountant at chosen workplace. In this method, variable expenses can be taken

into the consideration to choose the product in Mittelstand. Variable cost defines as to the

expenses which get changed with alteration to produce units in manufacturing plant (Soderstrom,

Soderstrom and Stewart, 2017).

It must be developed that after pursuing the calculation of variable cost, per unit remains

constant. However, when unit increases variable cost and expenses also changed over the time.

Marginal costing determines technique that used by the accountant to identify impact of the

variable expenses on the overall production in Mittelstand. With the help of present approach,

break-even is the best approach which helps in identifying number of units which must sold to

cover the cost of production. On the basis of present results, it is the method in which specific

number of unit collected at one place (Mokhtar, Jusoh and Zulkifli, 2016). Marginal costing

method also used for developing valuation of inventory on cost incurred for creating same value

as well. Therefore, it can be stated that there is wide importance of variable cost method.

8

Reconcile

d profit

1900

Quarte

r 1

Quarte

r 2

Quarter 1 Quarter 2

Total fixed cost 16000 16000

Fixed cost absorbed 66000*0.20 13200 74000*0.20 14800

Under absorbed -2800 -1200

Marginal costing is the important method to calculate costing which used by the

management accountant at chosen workplace. In this method, variable expenses can be taken

into the consideration to choose the product in Mittelstand. Variable cost defines as to the

expenses which get changed with alteration to produce units in manufacturing plant (Soderstrom,

Soderstrom and Stewart, 2017).

It must be developed that after pursuing the calculation of variable cost, per unit remains

constant. However, when unit increases variable cost and expenses also changed over the time.

Marginal costing determines technique that used by the accountant to identify impact of the

variable expenses on the overall production in Mittelstand. With the help of present approach,

break-even is the best approach which helps in identifying number of units which must sold to

cover the cost of production. On the basis of present results, it is the method in which specific

number of unit collected at one place (Mokhtar, Jusoh and Zulkifli, 2016). Marginal costing

method also used for developing valuation of inventory on cost incurred for creating same value

as well. Therefore, it can be stated that there is wide importance of variable cost method.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. (b) Supportive calculation and demonstrate profit in each method

In the present report, profit could be ascertained with using several methods such as

absorption and marginal costing method. In this way, it has been observed which has different

amount of profit that generate in both methods. It can be observed that absorption costing is the

best method in quarter 1 to enhance profits which increasing but in the second quarter it creates

negative results that reflect on the firm to earn more profits and revenue (Soderstrom,

Soderstrom and Stewart, 2017). Mittelstand using two types of approaches such as absorption

and marginal costing method. With the help of several ways, inventory valuation can be done

which is more useful for business operations.

In addition to this, it can be stated that there is wide difference in fixed and variable

expenditure. With evaluating the both approaches, it can be stated that there are several reasons

due to which differences comes in profits which computed with using absorption and marginal

costing method (Bebbington, Unerman and O'Dwyer, 2014). In case of marginal costing method,

inventory declined and cost also reduce which lead to enhance profits. Further, it has been noted

that expenditure incurred on the inventory also variable in nature. In the case of absorption

costing method, inventory also enhance to get more profits in the organisation. It is the reason

which approach to get more profit also changed (Mokhtar, Jusoh and Zulkifli, 2016).

SECTION 2

PART A

(a) Compare different management accounting methods

Budgetary control-refers to a system of controlling various costs by preparing various budget ,

coordinating with different departments and establishing responsibilities, comparing actual

performance with budgeted in order to achieve objective of profitability for an organisation.

Budgetary control refers to the way manger utilize budget to monitor and control various

activities within enterprises. Budgetary control system assist manager in framing various

performance related goals (Bebbington, Unerman and O'Dwyer, 2014). For instance manger can

use this technique for comparing actual performance with standard performance.

Budget:Budget refers to the statement that provides estimation about various income and

expenditure for a set period.

9

In the present report, profit could be ascertained with using several methods such as

absorption and marginal costing method. In this way, it has been observed which has different

amount of profit that generate in both methods. It can be observed that absorption costing is the

best method in quarter 1 to enhance profits which increasing but in the second quarter it creates

negative results that reflect on the firm to earn more profits and revenue (Soderstrom,

Soderstrom and Stewart, 2017). Mittelstand using two types of approaches such as absorption

and marginal costing method. With the help of several ways, inventory valuation can be done

which is more useful for business operations.

In addition to this, it can be stated that there is wide difference in fixed and variable

expenditure. With evaluating the both approaches, it can be stated that there are several reasons

due to which differences comes in profits which computed with using absorption and marginal

costing method (Bebbington, Unerman and O'Dwyer, 2014). In case of marginal costing method,

inventory declined and cost also reduce which lead to enhance profits. Further, it has been noted

that expenditure incurred on the inventory also variable in nature. In the case of absorption

costing method, inventory also enhance to get more profits in the organisation. It is the reason

which approach to get more profit also changed (Mokhtar, Jusoh and Zulkifli, 2016).

SECTION 2

PART A

(a) Compare different management accounting methods

Budgetary control-refers to a system of controlling various costs by preparing various budget ,

coordinating with different departments and establishing responsibilities, comparing actual

performance with budgeted in order to achieve objective of profitability for an organisation.

Budgetary control refers to the way manger utilize budget to monitor and control various

activities within enterprises. Budgetary control system assist manager in framing various

performance related goals (Bebbington, Unerman and O'Dwyer, 2014). For instance manger can

use this technique for comparing actual performance with standard performance.

Budget:Budget refers to the statement that provides estimation about various income and

expenditure for a set period.

9

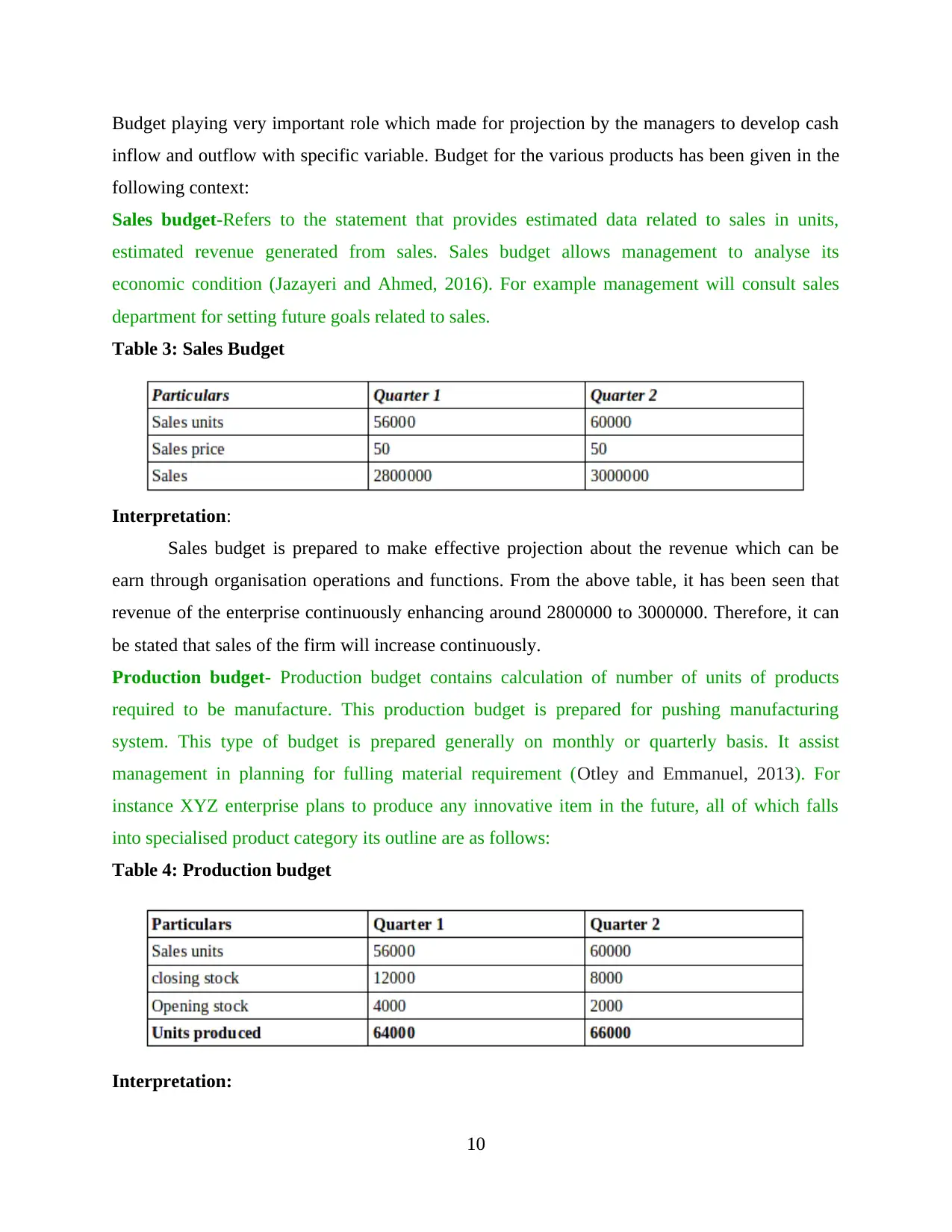

Budget playing very important role which made for projection by the managers to develop cash

inflow and outflow with specific variable. Budget for the various products has been given in the

following context:

Sales budget-Refers to the statement that provides estimated data related to sales in units,

estimated revenue generated from sales. Sales budget allows management to analyse its

economic condition (Jazayeri and Ahmed, 2016). For example management will consult sales

department for setting future goals related to sales.

Table 3: Sales Budget

Interpretation:

Sales budget is prepared to make effective projection about the revenue which can be

earn through organisation operations and functions. From the above table, it has been seen that

revenue of the enterprise continuously enhancing around 2800000 to 3000000. Therefore, it can

be stated that sales of the firm will increase continuously.

Production budget- Production budget contains calculation of number of units of products

required to be manufacture. This production budget is prepared for pushing manufacturing

system. This type of budget is prepared generally on monthly or quarterly basis. It assist

management in planning for fulling material requirement (Otley and Emmanuel, 2013). For

instance XYZ enterprise plans to produce any innovative item in the future, all of which falls

into specialised product category its outline are as follows:

Table 4: Production budget

Interpretation:

10

inflow and outflow with specific variable. Budget for the various products has been given in the

following context:

Sales budget-Refers to the statement that provides estimated data related to sales in units,

estimated revenue generated from sales. Sales budget allows management to analyse its

economic condition (Jazayeri and Ahmed, 2016). For example management will consult sales

department for setting future goals related to sales.

Table 3: Sales Budget

Interpretation:

Sales budget is prepared to make effective projection about the revenue which can be

earn through organisation operations and functions. From the above table, it has been seen that

revenue of the enterprise continuously enhancing around 2800000 to 3000000. Therefore, it can

be stated that sales of the firm will increase continuously.

Production budget- Production budget contains calculation of number of units of products

required to be manufacture. This production budget is prepared for pushing manufacturing

system. This type of budget is prepared generally on monthly or quarterly basis. It assist

management in planning for fulling material requirement (Otley and Emmanuel, 2013). For

instance XYZ enterprise plans to produce any innovative item in the future, all of which falls

into specialised product category its outline are as follows:

Table 4: Production budget

Interpretation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.