Management Accounting: Planning Tools and Financial Shortfalls

VerifiedAdded on 2020/01/23

|12

|2629

|219

Report

AI Summary

This report delves into the multifaceted world of management accounting, examining the crucial role it plays in organizational decision-making. It explores various planning methods like budgetary control, variance analysis, and fixed budgets, highlighting their merits and limitations in managing and controlling financial aspects. The report analyzes different budgeting tools, including cash, sales, production, and raw material budgets, showcasing their application in forecasting financial data. It evaluates how companies adapt management accounting systems to resolve financial shortfalls, tracing the historical evolution of these systems and identifying key financial issues. Furthermore, the report examines diverse management accounting approaches, such as financial governance, budgetary control, key performance indicators, and benchmarking, emphasizing their supportive role in mitigating financial problems. The conclusion underscores the significance of planning tools and management accounting systems in achieving financial objectives and addressing financial challenges.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P4 Explaining merits and limitations of various kinds of the planning methods considered by

management to control over the budgetary............................................................................1

M3 Analysing planning tools along with its application........................................................3

P5 Evaluating how companies adapting systems of management accounting for resolving

financial shortfalls..................................................................................................................6

M4 Analysis that how financial issues can be resolve within organisation by using

management accounting (MA) systems.................................................................................7

D3 Analysing that how planning tools supportive to eliminate financial issues....................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

P4 Explaining merits and limitations of various kinds of the planning methods considered by

management to control over the budgetary............................................................................1

M3 Analysing planning tools along with its application........................................................3

P5 Evaluating how companies adapting systems of management accounting for resolving

financial shortfalls..................................................................................................................6

M4 Analysis that how financial issues can be resolve within organisation by using

management accounting (MA) systems.................................................................................7

D3 Analysing that how planning tools supportive to eliminate financial issues....................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting plays a vital role in the decision-making process by the firm's

manager so, they can effectively able to operate function in most desired way. It is totally

different from the financial accounting as they always look forward for the future due to which

they can able to control functions. The present study describes about the different kinds of the

planning methods which used for control over the budgetary. Apart from this, historical

development of management accounting along with the financial issues are explained in the

present project.

P4 Explaining merits and limitations of various kinds of the planning methods considered by

management to control over the budgetary

Method which refers that in which ways management of the enterprise use budget for

monitoring and controlling over the expenses in a financial year is known as budgetary control.

In this, different budgets are prepared by the management and use at the workplace on the

monthly or quarterly basis (Chenhall and Moers, 2015). Further, benefits of the budgeting as

well as budgetary control are such as follows:

It is the supportive for management in order to meet with goals and objectives of the firm

which are related to the financial aspects.

In order to make proper coordination among different organisational functions or

departments the budgeting is highly effective tool.

For resolving communication issues and problems among different department of the

firm like HR, marketing, finance, production, research and development etc. this is

helpful method. Therefore, better employee relations within workplace can be

established.

Along with this, to allocate resources related to the financials within every function

budget is the supportive tool (Cooper, Ezzamel and Qu, 2017).

There are wide range of planning tools available which are such as variance analysis,

fixed budgets etc. Further, these are explained below:

Variance analysis: It is the tool that compare the actual and estimated results. If actual

outcome is differed from the estimated results then Pearson can get to know about the loop fall

1

Management accounting plays a vital role in the decision-making process by the firm's

manager so, they can effectively able to operate function in most desired way. It is totally

different from the financial accounting as they always look forward for the future due to which

they can able to control functions. The present study describes about the different kinds of the

planning methods which used for control over the budgetary. Apart from this, historical

development of management accounting along with the financial issues are explained in the

present project.

P4 Explaining merits and limitations of various kinds of the planning methods considered by

management to control over the budgetary

Method which refers that in which ways management of the enterprise use budget for

monitoring and controlling over the expenses in a financial year is known as budgetary control.

In this, different budgets are prepared by the management and use at the workplace on the

monthly or quarterly basis (Chenhall and Moers, 2015). Further, benefits of the budgeting as

well as budgetary control are such as follows:

It is the supportive for management in order to meet with goals and objectives of the firm

which are related to the financial aspects.

In order to make proper coordination among different organisational functions or

departments the budgeting is highly effective tool.

For resolving communication issues and problems among different department of the

firm like HR, marketing, finance, production, research and development etc. this is

helpful method. Therefore, better employee relations within workplace can be

established.

Along with this, to allocate resources related to the financials within every function

budget is the supportive tool (Cooper, Ezzamel and Qu, 2017).

There are wide range of planning tools available which are such as variance analysis,

fixed budgets etc. Further, these are explained below:

Variance analysis: It is the tool that compare the actual and estimated results. If actual

outcome is differed from the estimated results then Pearson can get to know about the loop fall

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and can take immediate action to resolve it. By this way issues related to high cost, ineffective

control etc can be resolved soon.

Advantages:

It is helpful for assessing business performance at the end of year.

It acts as a mechanism of controlling costs and enhancing sales.

It facilitates to the management in terms of giving and assigning responsibilities to the

functions and members of organisation (Figge and Hahn, 2013).

Disadvantages:

It is on the basis of financial results and gives information about performance after

completion of month or quarter.

It not helps to analyse every financial factor in detail. Further, it is based on budgeted data which are assumed rather realistic due to which

effectual decisions cannot be taken sometimes.

Fixed budget: Fixed budget is a budget which is not flexible or does not change with the

increase and decrease in sales. It is also known as a static budget. This is an easy way to manage

the expenses and operation when sales volume and total revenue will be set amount during a

period. To find the favourable and unfavourable variances between actual and budgeted

performance is only way so that management get collect the performance of segment. This is the

reason to use static budget (Fullerton, Kennedy and Widener, 2013).

The fixed budget have some advantages. Static budget are easy to prepare and allow

management to focus on operations. Fixed budget are also useful for companies with reliable,

annual trends. For example, if the demand of consumer is same for the past 10 years than

company set volume amount based on prior periods and still maintain accuracy.

Disadvantages:

It is easy to implement and follow, as static budgets do not need to update whole

accounting periods they are intended to cover.

2

control etc can be resolved soon.

Advantages:

It is helpful for assessing business performance at the end of year.

It acts as a mechanism of controlling costs and enhancing sales.

It facilitates to the management in terms of giving and assigning responsibilities to the

functions and members of organisation (Figge and Hahn, 2013).

Disadvantages:

It is on the basis of financial results and gives information about performance after

completion of month or quarter.

It not helps to analyse every financial factor in detail. Further, it is based on budgeted data which are assumed rather realistic due to which

effectual decisions cannot be taken sometimes.

Fixed budget: Fixed budget is a budget which is not flexible or does not change with the

increase and decrease in sales. It is also known as a static budget. This is an easy way to manage

the expenses and operation when sales volume and total revenue will be set amount during a

period. To find the favourable and unfavourable variances between actual and budgeted

performance is only way so that management get collect the performance of segment. This is the

reason to use static budget (Fullerton, Kennedy and Widener, 2013).

The fixed budget have some advantages. Static budget are easy to prepare and allow

management to focus on operations. Fixed budget are also useful for companies with reliable,

annual trends. For example, if the demand of consumer is same for the past 10 years than

company set volume amount based on prior periods and still maintain accuracy.

Disadvantages:

It is easy to implement and follow, as static budgets do not need to update whole

accounting periods they are intended to cover.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A static budget can offer strong insight into a company's cost and profit when variance

analysis is performed.

It allows to company to see the expenditure and revenues so that it can alter the strategy

going forward.

Static budget don't have build in wiggle room, they help company to control cost and

help to take smart decision (Wagenhofer, 2016).

Advantages:

In this budget lack of flexibility is available.

If company establish budget on certain level of sales volume and the volume increase

can't allocate additional resource to keep it.

This give negative impact on company's revenue stream.

Static budget are based on previous data so that newly formed company have to face the

problems to implementing and establishing plans.

M3 Analysing planning tools along with its application

In order to forecast different types of the budget statements prepared which are related to

the various financial data. Further, such budgets along with example given as below:

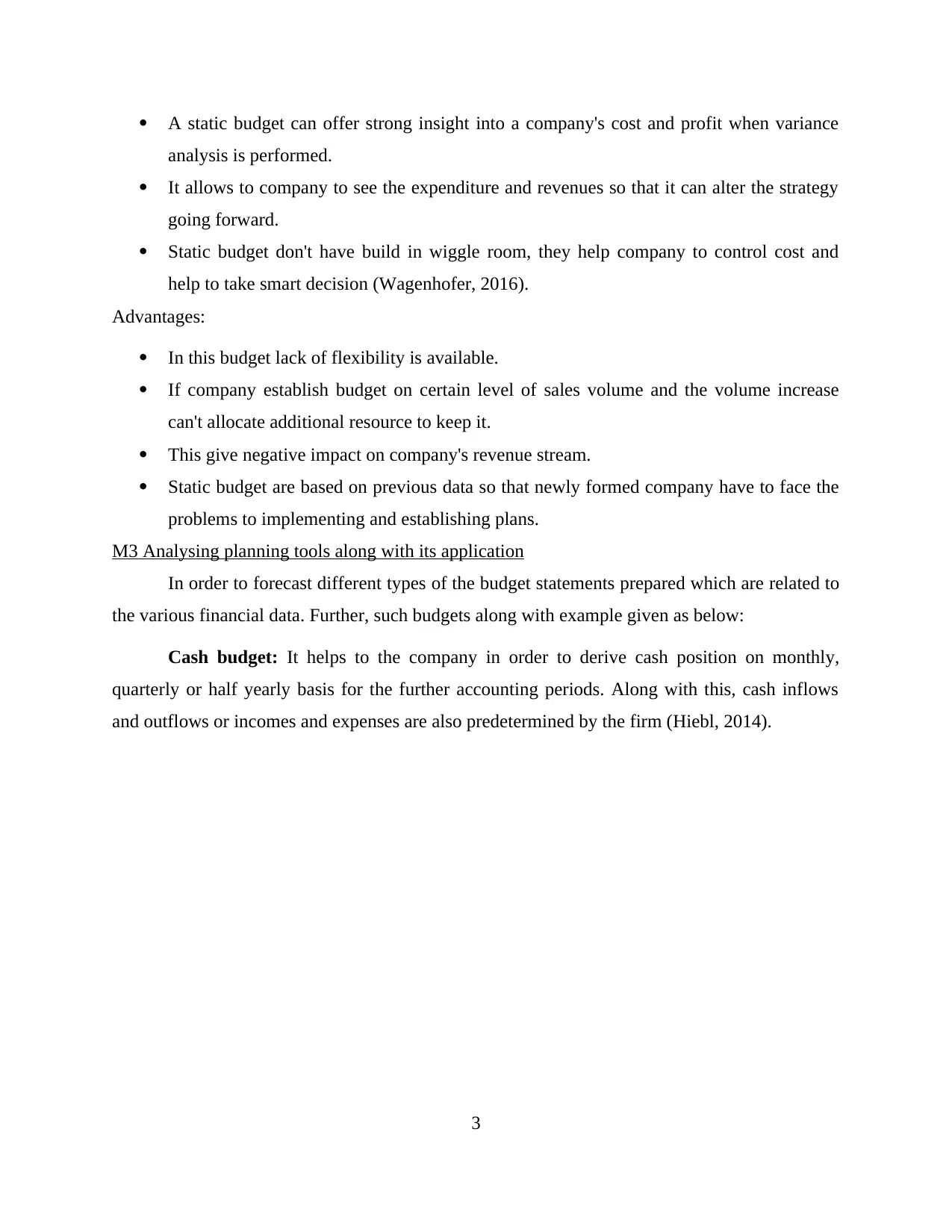

Cash budget: It helps to the company in order to derive cash position on monthly,

quarterly or half yearly basis for the further accounting periods. Along with this, cash inflows

and outflows or incomes and expenses are also predetermined by the firm (Hiebl, 2014).

3

analysis is performed.

It allows to company to see the expenditure and revenues so that it can alter the strategy

going forward.

Static budget don't have build in wiggle room, they help company to control cost and

help to take smart decision (Wagenhofer, 2016).

Advantages:

In this budget lack of flexibility is available.

If company establish budget on certain level of sales volume and the volume increase

can't allocate additional resource to keep it.

This give negative impact on company's revenue stream.

Static budget are based on previous data so that newly formed company have to face the

problems to implementing and establishing plans.

M3 Analysing planning tools along with its application

In order to forecast different types of the budget statements prepared which are related to

the various financial data. Further, such budgets along with example given as below:

Cash budget: It helps to the company in order to derive cash position on monthly,

quarterly or half yearly basis for the further accounting periods. Along with this, cash inflows

and outflows or incomes and expenses are also predetermined by the firm (Hiebl, 2014).

3

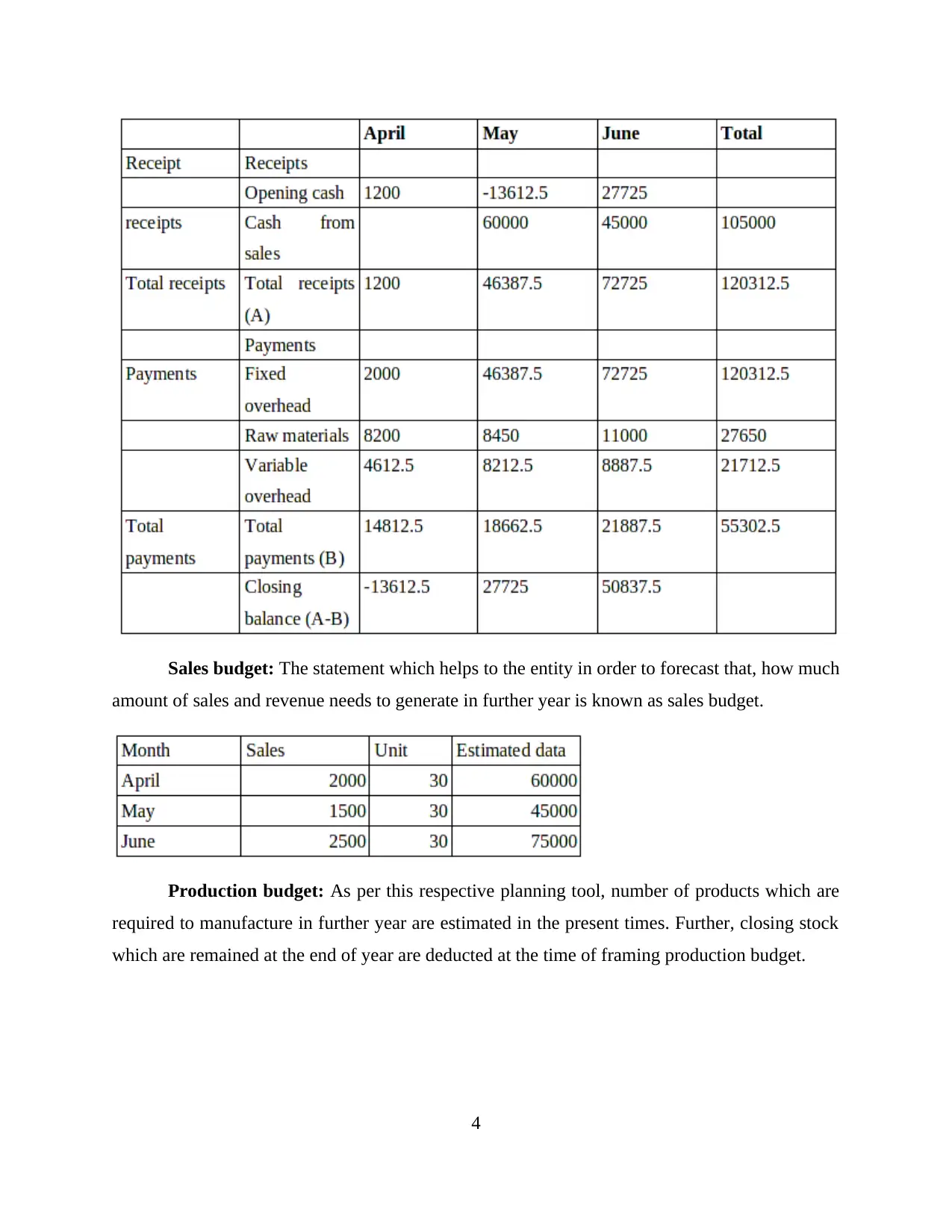

Sales budget: The statement which helps to the entity in order to forecast that, how much

amount of sales and revenue needs to generate in further year is known as sales budget.

Production budget: As per this respective planning tool, number of products which are

required to manufacture in further year are estimated in the present times. Further, closing stock

which are remained at the end of year are deducted at the time of framing production budget.

4

amount of sales and revenue needs to generate in further year is known as sales budget.

Production budget: As per this respective planning tool, number of products which are

required to manufacture in further year are estimated in the present times. Further, closing stock

which are remained at the end of year are deducted at the time of framing production budget.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

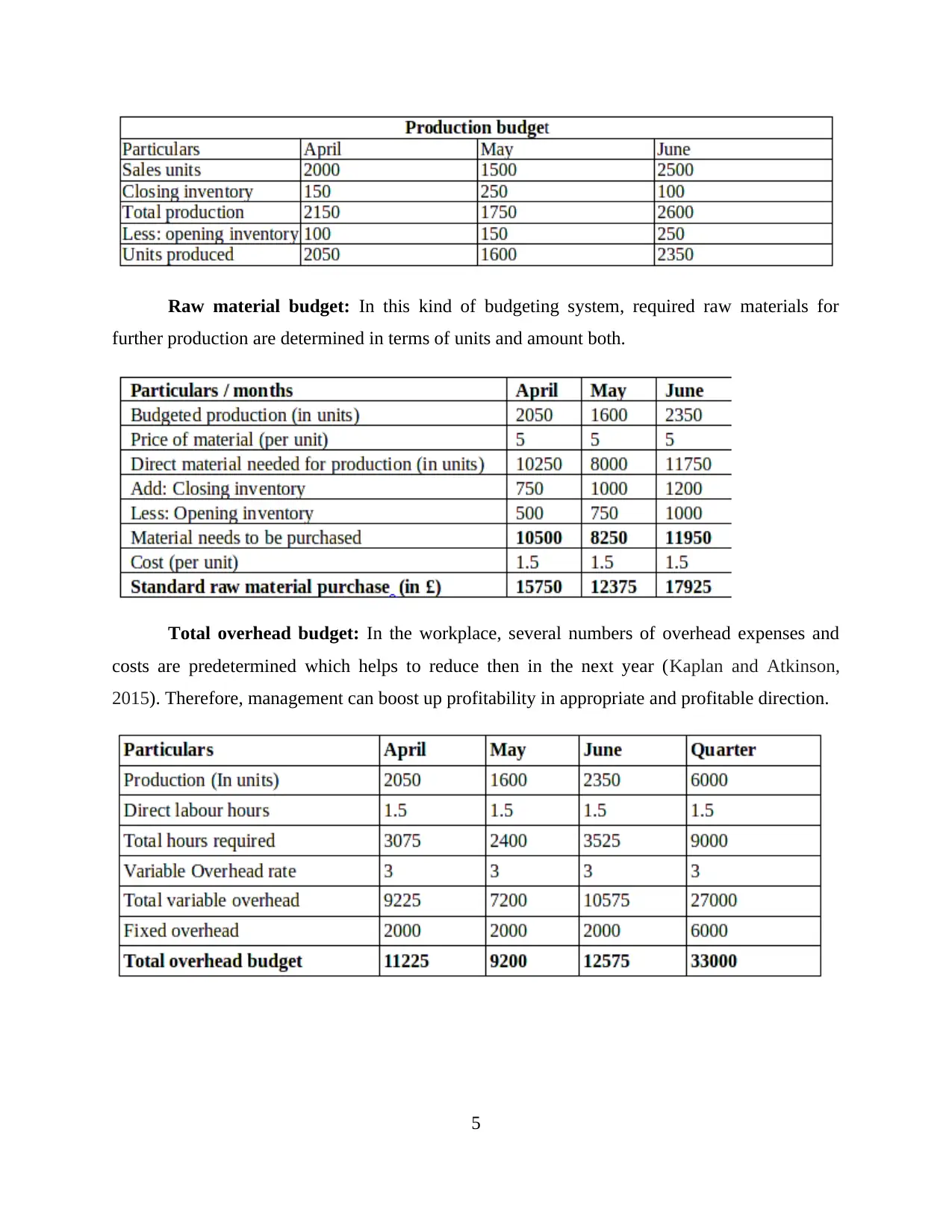

Raw material budget: In this kind of budgeting system, required raw materials for

further production are determined in terms of units and amount both.

Total overhead budget: In the workplace, several numbers of overhead expenses and

costs are predetermined which helps to reduce then in the next year (Kaplan and Atkinson,

2015). Therefore, management can boost up profitability in appropriate and profitable direction.

5

further production are determined in terms of units and amount both.

Total overhead budget: In the workplace, several numbers of overhead expenses and

costs are predetermined which helps to reduce then in the next year (Kaplan and Atkinson,

2015). Therefore, management can boost up profitability in appropriate and profitable direction.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P5 Evaluating how companies adapting systems of management accounting for resolving

financial shortfalls

In the management accounting aspect different kinds of systems and approaches framed

which are helpful for the businesses in order to combat financial problems. Further, such systems

developed step by step within some years. Therefore, its historical development along with the

financial issues described as below:

Phase 1:

Under the phase 1, level of competition is very low and all the required data related to

costs and budget are easily produced. This kind of situation is there until financial year 1950

where information of the management accounting not having higher impact on the decision

making process. Due to this, issues regarding to the financial shortfalls and declining

profitability etc. are very low (Luft, 2016).

Phase 2:

The second phase is between financial period 1950 to 1960 because of not having better

control in the firm over the management systems. Due to lack of problems regarding to the

proper and adequate management within working environment, the systems framed. Because of

these issues regarding to cost increasing and profit condition declining etc. come at the company.

Moreover, at this phase, proper systems of management controlling developed and then issues of

cost enhancement solved up to the certain level.

Phase 3:

Third phase of management accounting is developed during the year 1970 and run up to

the early 1980. In this period because of coming modified and highly innovative technologies

level of competition increase within workplace (Messner and et.al., 2016). Due to this, the

business entities need to pay higher amount of the changed technologies which create cost

related issues. Moreover, during this particular phase, financial obstacles regarding to the cost

increasing comes at the consideration. Furthermore, for resolving this problem cost accounting

system of management accounting is taken into account at the majority level.

Phase 4:

6

financial shortfalls

In the management accounting aspect different kinds of systems and approaches framed

which are helpful for the businesses in order to combat financial problems. Further, such systems

developed step by step within some years. Therefore, its historical development along with the

financial issues described as below:

Phase 1:

Under the phase 1, level of competition is very low and all the required data related to

costs and budget are easily produced. This kind of situation is there until financial year 1950

where information of the management accounting not having higher impact on the decision

making process. Due to this, issues regarding to the financial shortfalls and declining

profitability etc. are very low (Luft, 2016).

Phase 2:

The second phase is between financial period 1950 to 1960 because of not having better

control in the firm over the management systems. Due to lack of problems regarding to the

proper and adequate management within working environment, the systems framed. Because of

these issues regarding to cost increasing and profit condition declining etc. come at the company.

Moreover, at this phase, proper systems of management controlling developed and then issues of

cost enhancement solved up to the certain level.

Phase 3:

Third phase of management accounting is developed during the year 1970 and run up to

the early 1980. In this period because of coming modified and highly innovative technologies

level of competition increase within workplace (Messner and et.al., 2016). Due to this, the

business entities need to pay higher amount of the changed technologies which create cost

related issues. Moreover, during this particular phase, financial obstacles regarding to the cost

increasing comes at the consideration. Furthermore, for resolving this problem cost accounting

system of management accounting is taken into account at the majority level.

Phase 4:

6

At the last or fourth phase which is during 1990 to 2000, manufacturing techniques and

equipments come up with highly innovation. Due to this reason, competition increases and

comes at the cut throat level within every industry. Along with this, to gain competition

advantages and benefits at the working environment, wide range of the effective resources used

by the management. Therefore, higher the usage of resources in improper ways lead to increase

total cost of production. Further, overall profitability position at the end of an accounting period

will decline which indicates that company not performing well in the industry (Otley and

Emmanuel, 2013). In addition to this, at this phase, preferences, attitudes, requirements and

wants of the customers are also changed by which costing aspect increase and create issue of

profit reducing.

M4 Analysis that how financial issues can be resolve within organisation by using management

accounting (MA) systems

In the management accounting, wide range of systems and approaches included which

are supportive for reducing and eliminating financial problems in proper direction. Further, such

systems of MA are described as below: Financial governance: It is one part of the corporate governance in which its members

analyse that company is using all the accounting standards and principles in proper

direction or not. Along with this, auditing procedure is also conducted by financial

governance through which malpractices as well as frauds can be easily identified under

the final accounts (Financial governance, 2017). Henceforth, the problems and issues

regarding to financial aspects can be resolved easily up to the better extent. Budgetary control: Under this, budgets are prepared for different data and information

like cash, revenue, overhead expenses, raw materials etc. At the end of year, actual

figures and data generated by the company are compared with the budgeted and then

problems identified. Once issue defined then management can easily resolve problems of

costing, profitability etc. Key performance indicators: As per this management accounting system, different KPIs

are used and on the basis of that financial obstacles eliminated from the workplace.

Further, KPIs are like cost, net profit, quality, business performance, liquidity position

etc. by which problems can be resolved properly (Tucker and Lowe, 2014).

7

equipments come up with highly innovation. Due to this reason, competition increases and

comes at the cut throat level within every industry. Along with this, to gain competition

advantages and benefits at the working environment, wide range of the effective resources used

by the management. Therefore, higher the usage of resources in improper ways lead to increase

total cost of production. Further, overall profitability position at the end of an accounting period

will decline which indicates that company not performing well in the industry (Otley and

Emmanuel, 2013). In addition to this, at this phase, preferences, attitudes, requirements and

wants of the customers are also changed by which costing aspect increase and create issue of

profit reducing.

M4 Analysis that how financial issues can be resolve within organisation by using management

accounting (MA) systems

In the management accounting, wide range of systems and approaches included which

are supportive for reducing and eliminating financial problems in proper direction. Further, such

systems of MA are described as below: Financial governance: It is one part of the corporate governance in which its members

analyse that company is using all the accounting standards and principles in proper

direction or not. Along with this, auditing procedure is also conducted by financial

governance through which malpractices as well as frauds can be easily identified under

the final accounts (Financial governance, 2017). Henceforth, the problems and issues

regarding to financial aspects can be resolved easily up to the better extent. Budgetary control: Under this, budgets are prepared for different data and information

like cash, revenue, overhead expenses, raw materials etc. At the end of year, actual

figures and data generated by the company are compared with the budgeted and then

problems identified. Once issue defined then management can easily resolve problems of

costing, profitability etc. Key performance indicators: As per this management accounting system, different KPIs

are used and on the basis of that financial obstacles eliminated from the workplace.

Further, KPIs are like cost, net profit, quality, business performance, liquidity position

etc. by which problems can be resolved properly (Tucker and Lowe, 2014).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benchmarking: According to this approach of MA, specific standard and benchmark

settled by the firm internally or used at the industry level. When the firm meets or

achieves targeted benchmark then it can be said that is performs well in the industry.

D3 Analysing that how planning tools supportive to eliminate financial issues

Planning tools which are used and explained in the present study are like variance

analysis and fixed budget. By considering such techniques, the company can easily able to

reduce and resolve costing, profitability etc. financial issues. Under the variance analysis,

budgeted and actual figures are measured and if firm unable to meet with the estimated values

then it can be said that, management not performs well (Shields, 2015). Therefore, issues can be

eliminated in appropriate direction. Apart from this, fixed budget shows all the financial data

which are necessary to meet at the end of further accounting period. If all the data are not

achieved then can be said that financial problems is there.

CONCLUSION

It can be concluded from the report of management accounting that, variance analysis and

fixed budget both are highly supportive planning tool. With the help of such both methods the

management able to control on the budgets and meet with the financial objectives. Further, at the

different stages of the MA, financial issues arise which can be resolved with the help of financial

governance, budgetary control, key performance indicators and benchmarking in proper

direction.

8

settled by the firm internally or used at the industry level. When the firm meets or

achieves targeted benchmark then it can be said that is performs well in the industry.

D3 Analysing that how planning tools supportive to eliminate financial issues

Planning tools which are used and explained in the present study are like variance

analysis and fixed budget. By considering such techniques, the company can easily able to

reduce and resolve costing, profitability etc. financial issues. Under the variance analysis,

budgeted and actual figures are measured and if firm unable to meet with the estimated values

then it can be said that, management not performs well (Shields, 2015). Therefore, issues can be

eliminated in appropriate direction. Apart from this, fixed budget shows all the financial data

which are necessary to meet at the end of further accounting period. If all the data are not

achieved then can be said that financial problems is there.

CONCLUSION

It can be concluded from the report of management accounting that, variance analysis and

fixed budget both are highly supportive planning tool. With the help of such both methods the

management able to control on the budgets and meet with the financial objectives. Further, at the

different stages of the MA, financial issues arise which can be resolved with the help of financial

governance, budgetary control, key performance indicators and benchmarking in proper

direction.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp. 1-13.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.

Figge, F. and Hahn, T., 2013. Value drivers of corporate eco-efficiency: Management accounting

information for the efficient use of environmental resources. Management Accounting

Research, 24(4). pp. 387-400.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp. 50-71.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp. 223-240.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Luft, J., 2016. Management accounting in the laboratory and in social context: Four contrasts,

1975–2014. Accounting, Organizations and Society. 49(C). pp. 9-20.

Messner, M. and et.al., 2016. Struggles for legitimacy and identity: the development of

Germanic management accounting research. Research Gate. pp. 1-38.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research, 27(1). pp. 123-132.

Tucker, B. and D. Lowe, A., 2014. Practitioners are from Mars; academics are from Venus? An

investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal, 27(3). pp. 394-425.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management accounting.

Management Accounting Research. 31. pp. 112-117.

Online

9

Books and Journals

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp. 1-13.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.

Figge, F. and Hahn, T., 2013. Value drivers of corporate eco-efficiency: Management accounting

information for the efficient use of environmental resources. Management Accounting

Research, 24(4). pp. 387-400.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp. 50-71.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp. 223-240.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Luft, J., 2016. Management accounting in the laboratory and in social context: Four contrasts,

1975–2014. Accounting, Organizations and Society. 49(C). pp. 9-20.

Messner, M. and et.al., 2016. Struggles for legitimacy and identity: the development of

Germanic management accounting research. Research Gate. pp. 1-38.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research, 27(1). pp. 123-132.

Tucker, B. and D. Lowe, A., 2014. Practitioners are from Mars; academics are from Venus? An

investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal, 27(3). pp. 394-425.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management accounting.

Management Accounting Research. 31. pp. 112-117.

Online

9

Financial governance, 2017. [online]. Available through:

<http://www.mango.org.uk/guide/financialgovernance> [Accessed on 3rd August 2017]

10

<http://www.mango.org.uk/guide/financialgovernance> [Accessed on 3rd August 2017]

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.