Management Accounting Report: Analysis of Cost and Planning

VerifiedAdded on 2021/02/19

|24

|5930

|86

Report

AI Summary

This report provides an in-depth analysis of management accounting principles and practices, focusing on Burlington Associates Limited and its client, Murrill Construction Limited. The report explores the role of management accounting, its evolution, and its distinction from financial accounting. It delves into various management accounting systems, including inventory management, cost accounting, price optimization, and job costing, highlighting their benefits. The report also examines the characteristics and types of management accounting reports, such as performance reports, budget reports, and cost management reports. Furthermore, it covers cost calculation methods for income statement preparation, including fixed, variable, and semi-variable costs, along with cost analysis techniques. The report also discusses planning tools used for budgetary control and compares organizational approaches to financial problem-solving using management accounting systems. The report provides a comprehensive overview of management accounting concepts and their practical applications in the business environment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Management accounting........................................................................................................2

P2. Management accounting reporting........................................................................................5

TASK 2............................................................................................................................................7

P3. Calculation of costs for the preparation of income statement. .............................................7

TASK 3..........................................................................................................................................14

P4. Planning tools used for budgetary control...........................................................................14

TASK 4..........................................................................................................................................19

P5. Comparison of organisations to solve the financial problem by using management

accounting system......................................................................................................................19

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Management accounting........................................................................................................2

P2. Management accounting reporting........................................................................................5

TASK 2............................................................................................................................................7

P3. Calculation of costs for the preparation of income statement. .............................................7

TASK 3..........................................................................................................................................14

P4. Planning tools used for budgetary control...........................................................................14

TASK 4..........................................................................................................................................19

P5. Comparison of organisations to solve the financial problem by using management

accounting system......................................................................................................................19

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

1

INTRODUCTION

Management accounting is a concept which involves preparation of management reports

along with accounts in order to provide financial information to managers for the purpose of

making strategic decisions for the organisation (Basu, 2012). It helps in identification, collection,

reporting, measurement, analysing and communicating the same information in such manner that

benefits in pursuing towards goals of company. To understand the concept of management

accounting, Burlington Associates Limited is selected which is a medium sized organisation that

provides financial consultancy services to numerous clients. One of its clients is Murrill

Construction Limited which performs its operations in construction industry. This report covers

management accounting systems and their essential requirement. It further discusses about

methods used for management accounting reporting along with usage of costing techniques to

prepare income statements. It further includes various planning tools and the ways adopted by

management of two companies to resolve financial problems that helps in leading towards

sustainable success.

TASK 1

P1. Management accounting.

Accounting is a practice as well as applied aspects of knowledge which includes

recording as per the well-defined principles and rules of the operations related with the sourcing

and usage of resources to accomplish the business strategy.

Management accounting is a process in which accounting reports are prepared as well

as provided to top level management on accurate time period. Managers of Murrill Construction

Limited uses management accounting to facilitate financial planning, making decisions and

keeping records in effective manner (Bellassen and Stephan, 2015).

Management accounting origin, role along with principles

Management accounting was first emerged during early industry revolution in 19 century.

It was arose after financial management which has traced its origins towards stewardship role at

the time of European trading ventures. Other than this, books are balanced which is also part of it

and used from long ago such as 300 years. From that time, management accounting was emerged

as a recognizable field.

2

Management accounting is a concept which involves preparation of management reports

along with accounts in order to provide financial information to managers for the purpose of

making strategic decisions for the organisation (Basu, 2012). It helps in identification, collection,

reporting, measurement, analysing and communicating the same information in such manner that

benefits in pursuing towards goals of company. To understand the concept of management

accounting, Burlington Associates Limited is selected which is a medium sized organisation that

provides financial consultancy services to numerous clients. One of its clients is Murrill

Construction Limited which performs its operations in construction industry. This report covers

management accounting systems and their essential requirement. It further discusses about

methods used for management accounting reporting along with usage of costing techniques to

prepare income statements. It further includes various planning tools and the ways adopted by

management of two companies to resolve financial problems that helps in leading towards

sustainable success.

TASK 1

P1. Management accounting.

Accounting is a practice as well as applied aspects of knowledge which includes

recording as per the well-defined principles and rules of the operations related with the sourcing

and usage of resources to accomplish the business strategy.

Management accounting is a process in which accounting reports are prepared as well

as provided to top level management on accurate time period. Managers of Murrill Construction

Limited uses management accounting to facilitate financial planning, making decisions and

keeping records in effective manner (Bellassen and Stephan, 2015).

Management accounting origin, role along with principles

Management accounting was first emerged during early industry revolution in 19 century.

It was arose after financial management which has traced its origins towards stewardship role at

the time of European trading ventures. Other than this, books are balanced which is also part of it

and used from long ago such as 300 years. From that time, management accounting was emerged

as a recognizable field.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The role of management accounting is different at workplace based on its requirements as

it is a internal part that performs functions related to financial security, handling taxes,

developing accounting systems, maintaining capital structure, fund flow analysis, decision

making on investment appraisal, financing of projects and hence forth.

Principles of management accounting includes the following:

Influence which says communication must be in such manner that provides insight which

are persuaded.

Relevance that is providing information in adequate manner.

Value shows impact on belief that are analysed.

Trust that is stewardship builds belongings.

Comparison between management accounting with financial accounting

Basis Management Accounting Financial Accounting

Purpose This type of accounting is prepared

with the purpose of internal usage.

Such accounting is used for external

reporting as well as management

purposes.

Regulation There are no prescribed rules as well

as legislations for management

accounting (Englund and Gerdin,

2018).

There are prescribed rules based on

accounting concepts along with

standards.

Users The main user is organisational

management.

The main users of financial

accounting are shareholders,

regulators as well as investors.

Management accounting system: It is a forward looking method that includes practices

which are used by businesses to maintain operations as well as providing information for the

purpose of decision making. This accounting system helps various departments of selected

company to plan, organise, coordinate, communicate, direct, improvements and regulation of

several business activities. Some of the accounting systems are as follows:

Inventory management system: This system is related with tracking present status of

products or services. It benefits in supervision of items along with non capitalized assets in

3

it is a internal part that performs functions related to financial security, handling taxes,

developing accounting systems, maintaining capital structure, fund flow analysis, decision

making on investment appraisal, financing of projects and hence forth.

Principles of management accounting includes the following:

Influence which says communication must be in such manner that provides insight which

are persuaded.

Relevance that is providing information in adequate manner.

Value shows impact on belief that are analysed.

Trust that is stewardship builds belongings.

Comparison between management accounting with financial accounting

Basis Management Accounting Financial Accounting

Purpose This type of accounting is prepared

with the purpose of internal usage.

Such accounting is used for external

reporting as well as management

purposes.

Regulation There are no prescribed rules as well

as legislations for management

accounting (Englund and Gerdin,

2018).

There are prescribed rules based on

accounting concepts along with

standards.

Users The main user is organisational

management.

The main users of financial

accounting are shareholders,

regulators as well as investors.

Management accounting system: It is a forward looking method that includes practices

which are used by businesses to maintain operations as well as providing information for the

purpose of decision making. This accounting system helps various departments of selected

company to plan, organise, coordinate, communicate, direct, improvements and regulation of

several business activities. Some of the accounting systems are as follows:

Inventory management system: This system is related with tracking present status of

products or services. It benefits in supervision of items along with non capitalized assets in

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effective manner that results in preventing shortages of material at workplace. This system can

benefit Murril Construction Limited by properly tracking and keeping record of incoming as well

as outgoing materials along with finished products. Using this system, managers can get

information related with current inventory level that results in minimising circumstances related

to over stock or under stock of materials which adds values to keep track of record which adds

value to organisation by keeping detailed record and using them at the time required for analysis.

The essential requirement of inventory management system is to track and maintain records in

systematic manner based on existing or new stock that enters or leaves warehouses or

construction sites at some point of sale.

Cost accounting system: It is another type of accounting system that helps in analysing

product costs such as fixed or variable costs. Its main functionality is to ascertain value of

inventory, controlling costs as well as profitability analysis (Fayol, 2016). Managers of Murril

Construction Limited uses this system to estimate cost of products or services in accurate manner

that that results in profitable operations. It adds value to company by estimating cost of products

or services in order to predicting profits or losses in accurate format. The essential requirement

of such system is to fix standards, determining costs as well as classification of costs such as

factory cost, direct cost, prime cost and so on.

Price optimisation system: A mathematical program which calculates demand

variations at different pricing levels is price optimising system. It performs functions related to

combining data with relevant information based on inventory and cost level to provide

recommendations to change prices for the purpose of improving profits. Such system adds value

to business by understanding perception of clients towards prices of products or services which

are rendered by organisational members and formulating prices accordingly. Price optimisation

system is used by managers of Murril Construction Limited to determine prices of constructional

projects as well as discovering pricing structures as per customer willingness related with

making payment decisions. The essential requirement of price optimising system is to determine

prices of various constructional projects that helps in maximising profits.

Job costing system- Job costing system can be defined as calculating total cost of

particular products and services. Murrill construction limited adopts this system to accumulate

information based on direct material, overhead costs as well as direct labour and it can be

tailored as per the requirements of customers. Functionality of job costing system is to determine

4

benefit Murril Construction Limited by properly tracking and keeping record of incoming as well

as outgoing materials along with finished products. Using this system, managers can get

information related with current inventory level that results in minimising circumstances related

to over stock or under stock of materials which adds values to keep track of record which adds

value to organisation by keeping detailed record and using them at the time required for analysis.

The essential requirement of inventory management system is to track and maintain records in

systematic manner based on existing or new stock that enters or leaves warehouses or

construction sites at some point of sale.

Cost accounting system: It is another type of accounting system that helps in analysing

product costs such as fixed or variable costs. Its main functionality is to ascertain value of

inventory, controlling costs as well as profitability analysis (Fayol, 2016). Managers of Murril

Construction Limited uses this system to estimate cost of products or services in accurate manner

that that results in profitable operations. It adds value to company by estimating cost of products

or services in order to predicting profits or losses in accurate format. The essential requirement

of such system is to fix standards, determining costs as well as classification of costs such as

factory cost, direct cost, prime cost and so on.

Price optimisation system: A mathematical program which calculates demand

variations at different pricing levels is price optimising system. It performs functions related to

combining data with relevant information based on inventory and cost level to provide

recommendations to change prices for the purpose of improving profits. Such system adds value

to business by understanding perception of clients towards prices of products or services which

are rendered by organisational members and formulating prices accordingly. Price optimisation

system is used by managers of Murril Construction Limited to determine prices of constructional

projects as well as discovering pricing structures as per customer willingness related with

making payment decisions. The essential requirement of price optimising system is to determine

prices of various constructional projects that helps in maximising profits.

Job costing system- Job costing system can be defined as calculating total cost of

particular products and services. Murrill construction limited adopts this system to accumulate

information based on direct material, overhead costs as well as direct labour and it can be

tailored as per the requirements of customers. Functionality of job costing system is to determine

4

material cost, factory overhead and labour overhead related with particular job or project. This

system adds value to enterprise by setting standard targets as well as tracking all revenues

pertaining to different jobs in discrete batches. The essential requirement of job costing system is

to ensure that product or job price covers all actual costs and at the same time provide profits.

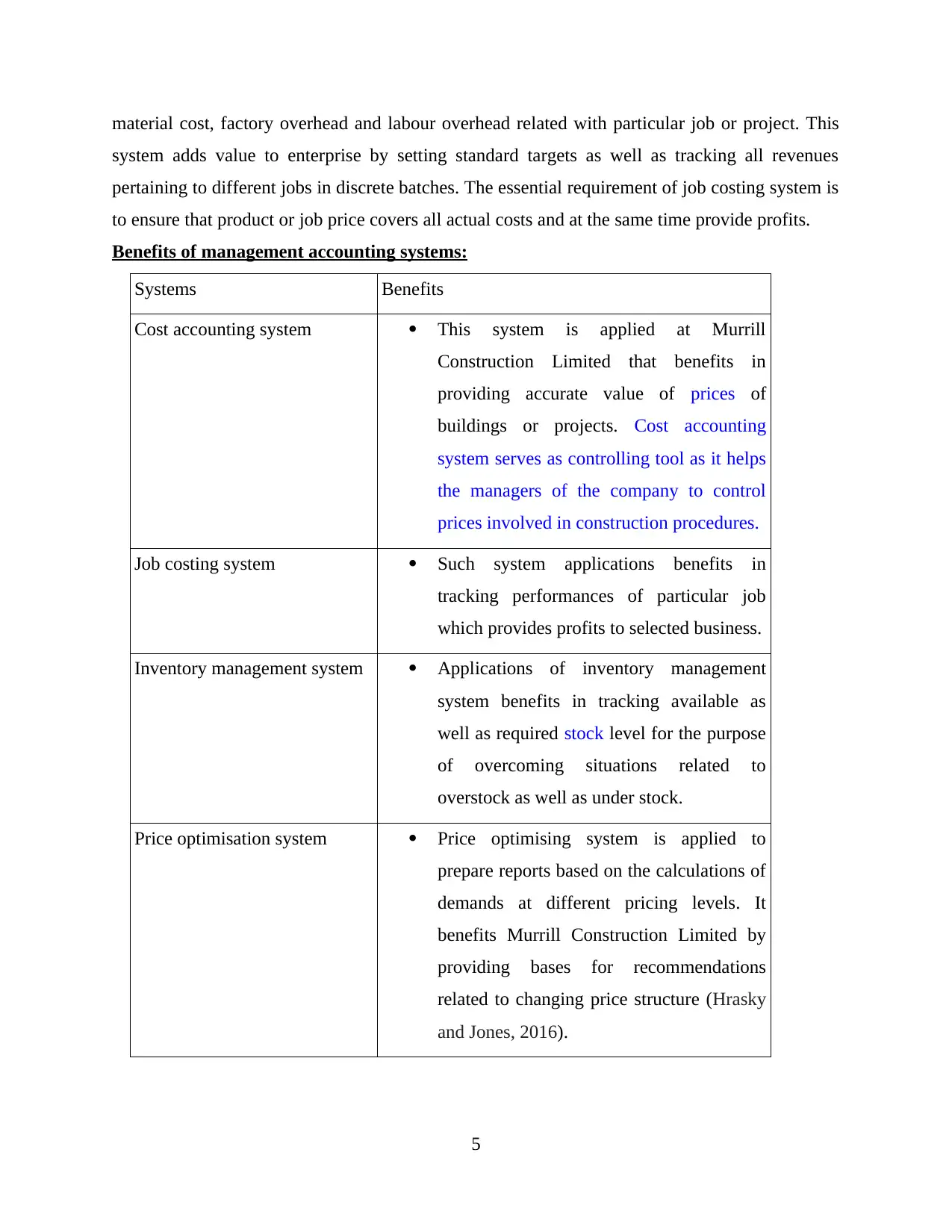

Benefits of management accounting systems:

Systems Benefits

Cost accounting system This system is applied at Murrill

Construction Limited that benefits in

providing accurate value of prices of

buildings or projects. Cost accounting

system serves as controlling tool as it helps

the managers of the company to control

prices involved in construction procedures.

Job costing system Such system applications benefits in

tracking performances of particular job

which provides profits to selected business.

Inventory management system Applications of inventory management

system benefits in tracking available as

well as required stock level for the purpose

of overcoming situations related to

overstock as well as under stock.

Price optimisation system Price optimising system is applied to

prepare reports based on the calculations of

demands at different pricing levels. It

benefits Murrill Construction Limited by

providing bases for recommendations

related to changing price structure (Hrasky

and Jones, 2016).

5

system adds value to enterprise by setting standard targets as well as tracking all revenues

pertaining to different jobs in discrete batches. The essential requirement of job costing system is

to ensure that product or job price covers all actual costs and at the same time provide profits.

Benefits of management accounting systems:

Systems Benefits

Cost accounting system This system is applied at Murrill

Construction Limited that benefits in

providing accurate value of prices of

buildings or projects. Cost accounting

system serves as controlling tool as it helps

the managers of the company to control

prices involved in construction procedures.

Job costing system Such system applications benefits in

tracking performances of particular job

which provides profits to selected business.

Inventory management system Applications of inventory management

system benefits in tracking available as

well as required stock level for the purpose

of overcoming situations related to

overstock as well as under stock.

Price optimisation system Price optimising system is applied to

prepare reports based on the calculations of

demands at different pricing levels. It

benefits Murrill Construction Limited by

providing bases for recommendations

related to changing price structure (Hrasky

and Jones, 2016).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2. Management accounting reporting.

Characteristics: Management accounting system posses certain characteristics that are

relevant with various aspects. Some of the characteristics are as follows:

Reliable: Trustworthiness or reliability of accounting systems for the preparation of

financial statement.

Accuracy: It ensures that stated values on financial statements are accurate as well as

reflects supporting factual data.

Up to date: Financial statements must be updated with all transactions as on specified

time period.

Management accounting reports must be comprehensive and understandable as:

Accounting reports should be understandable as by analysing these reports managers of

Murrill Construction Limited prevents obfuscating as well as misleading usage of

financial statements at time of making decisions.

These reports must be comprehensive as they provides detailed information or summary

of sources of expenses as well as incomes that helps in understanding profitability of

business.

Management accounting reports: Managers prepares different types of accounting

reports and at the same time these reports have significant role in providing information to top

level management (Hyndman, 2016). These reports are used for the purpose of planning,

decision making as well as measuring performances. By evaluating such reports important

strategies along with decisions are formulated for the betterment of organisation. Some of the

management accounting reports are as follows:

Performance reports: In reference to management accounting, these are used for

evaluating performances (goals accomplishment under an effective and efficient use of the

resources available for that purpose) of employees as well as organisation as whole. It is used at

Murrill construction Limited to analyse performances of different departmental members.

Budget reports: Using this report, managers of Murrill construction Limited makes

estimation for expenses and incomes for specific period of time. They compare actual financial

performance with budgeted estimations and frame effective strategies in order to control

deviations. Thus, budget reports help in controlling financial transactions as to attain objectives.

6

Characteristics: Management accounting system posses certain characteristics that are

relevant with various aspects. Some of the characteristics are as follows:

Reliable: Trustworthiness or reliability of accounting systems for the preparation of

financial statement.

Accuracy: It ensures that stated values on financial statements are accurate as well as

reflects supporting factual data.

Up to date: Financial statements must be updated with all transactions as on specified

time period.

Management accounting reports must be comprehensive and understandable as:

Accounting reports should be understandable as by analysing these reports managers of

Murrill Construction Limited prevents obfuscating as well as misleading usage of

financial statements at time of making decisions.

These reports must be comprehensive as they provides detailed information or summary

of sources of expenses as well as incomes that helps in understanding profitability of

business.

Management accounting reports: Managers prepares different types of accounting

reports and at the same time these reports have significant role in providing information to top

level management (Hyndman, 2016). These reports are used for the purpose of planning,

decision making as well as measuring performances. By evaluating such reports important

strategies along with decisions are formulated for the betterment of organisation. Some of the

management accounting reports are as follows:

Performance reports: In reference to management accounting, these are used for

evaluating performances (goals accomplishment under an effective and efficient use of the

resources available for that purpose) of employees as well as organisation as whole. It is used at

Murrill construction Limited to analyse performances of different departmental members.

Budget reports: Using this report, managers of Murrill construction Limited makes

estimation for expenses and incomes for specific period of time. They compare actual financial

performance with budgeted estimations and frame effective strategies in order to control

deviations. Thus, budget reports help in controlling financial transactions as to attain objectives.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Account receivable reports: This report is used to make list of unpaid customer invoice

along with credit memos which are unused by date ranges. It categorises account receivables

according to time outstanding for invoice. Using this report, Murrill construction Limited

managers identify defaulters along with financial health of potential clients. It is prepared in

systematic manner which provides detailed information related to transactions such as date, time,

particulars, amount and so on which reduces complexities to calculate credit values which brings

transparency in collection of credit from various creditors.

Cost management accounting reports: This report helps in computing cost of products

by taking into consideration other costs such as raw material costs, overhead costs, labour costs

and so on that adds costs to products. Financial manager of Murrill Construction Limited uses

this report to provide information related with cost price along with selling price of construction

projects or buildings in order to estimate margin of profits. Inventory wastages, hourly labour

costs and over costs are involved in such report.

Integration of management accounting system and accounting reports: For the

preparation of management accounting reports managers uses accounting systems. These

systems provide necessary information on accurate time period at the time of preparing reports

which are further used by top managers of Murrill construction Limited to make decisions to

achieve results.

TASK 2

P3. Calculation of costs for the preparation of income statement.

Cost: The total amount that is paid by the customer in order to buy the product. For the

purpose of attracting customers, managers of Murrill Construction Limited sets appropriate costs

pertaining with different buildings or projects (Ionescu, 2016).

Fixed Cost: A type of value that does not changes with changes in particular activity is

termed as fixed cost. It remains fixed during accounting year.

Variable Cost: A worth which varies when changes are seen in different level of activity

are known as variable cost. This type of cost is related with direct material cost.

Semi variable Cost: A cost that has features of fixed cost as well as variable cost.

Cost analysis: The breaking down into constituents of cost summary along with

understanding as studying each factors is defined as cost analysis. It is used to make comparisons

7

along with credit memos which are unused by date ranges. It categorises account receivables

according to time outstanding for invoice. Using this report, Murrill construction Limited

managers identify defaulters along with financial health of potential clients. It is prepared in

systematic manner which provides detailed information related to transactions such as date, time,

particulars, amount and so on which reduces complexities to calculate credit values which brings

transparency in collection of credit from various creditors.

Cost management accounting reports: This report helps in computing cost of products

by taking into consideration other costs such as raw material costs, overhead costs, labour costs

and so on that adds costs to products. Financial manager of Murrill Construction Limited uses

this report to provide information related with cost price along with selling price of construction

projects or buildings in order to estimate margin of profits. Inventory wastages, hourly labour

costs and over costs are involved in such report.

Integration of management accounting system and accounting reports: For the

preparation of management accounting reports managers uses accounting systems. These

systems provide necessary information on accurate time period at the time of preparing reports

which are further used by top managers of Murrill construction Limited to make decisions to

achieve results.

TASK 2

P3. Calculation of costs for the preparation of income statement.

Cost: The total amount that is paid by the customer in order to buy the product. For the

purpose of attracting customers, managers of Murrill Construction Limited sets appropriate costs

pertaining with different buildings or projects (Ionescu, 2016).

Fixed Cost: A type of value that does not changes with changes in particular activity is

termed as fixed cost. It remains fixed during accounting year.

Variable Cost: A worth which varies when changes are seen in different level of activity

are known as variable cost. This type of cost is related with direct material cost.

Semi variable Cost: A cost that has features of fixed cost as well as variable cost.

Cost analysis: The breaking down into constituents of cost summary along with

understanding as studying each factors is defined as cost analysis. It is used to make comparisons

7

of standard costs with actual costs during a specified time period and disclosing the same for

further improvements.

Cost volume profit: It a type of cost analysis in which changes in costs as well as

volume are determined that affects operating income of any business.

Flexible budgeting: It is analysed and adjusted as per changes in activity at the time of

completion of projects.

Absorption costing: It is a costing technique that helps in evaluation of costs during an

accounting period. Herein, to sell single product in competitive market place, Galway Plc

calculates cost of product by using such costing technique (Ionescu, 2016).

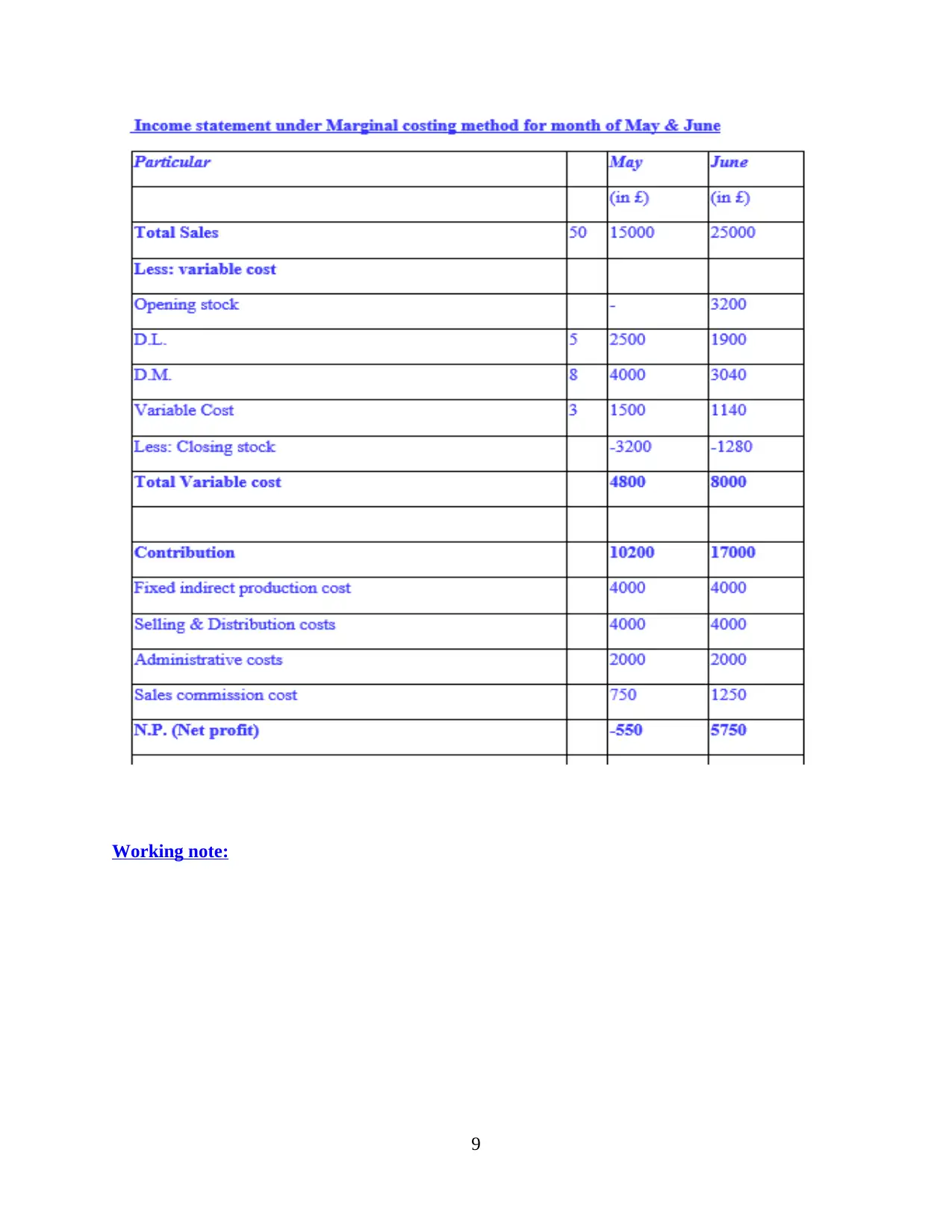

Marginal costing: It is a costing method that emphasis towards classification of all

expenses in terms of variable as well as fixed costs (Jones, 2014). On other hand all fixed cost

are charged as per period costs. Calculations based on marginal costing technique are as follows:

Income statement under Marginal costing method for month of May & June

8

further improvements.

Cost volume profit: It a type of cost analysis in which changes in costs as well as

volume are determined that affects operating income of any business.

Flexible budgeting: It is analysed and adjusted as per changes in activity at the time of

completion of projects.

Absorption costing: It is a costing technique that helps in evaluation of costs during an

accounting period. Herein, to sell single product in competitive market place, Galway Plc

calculates cost of product by using such costing technique (Ionescu, 2016).

Marginal costing: It is a costing method that emphasis towards classification of all

expenses in terms of variable as well as fixed costs (Jones, 2014). On other hand all fixed cost

are charged as per period costs. Calculations based on marginal costing technique are as follows:

Income statement under Marginal costing method for month of May & June

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working note:

9

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

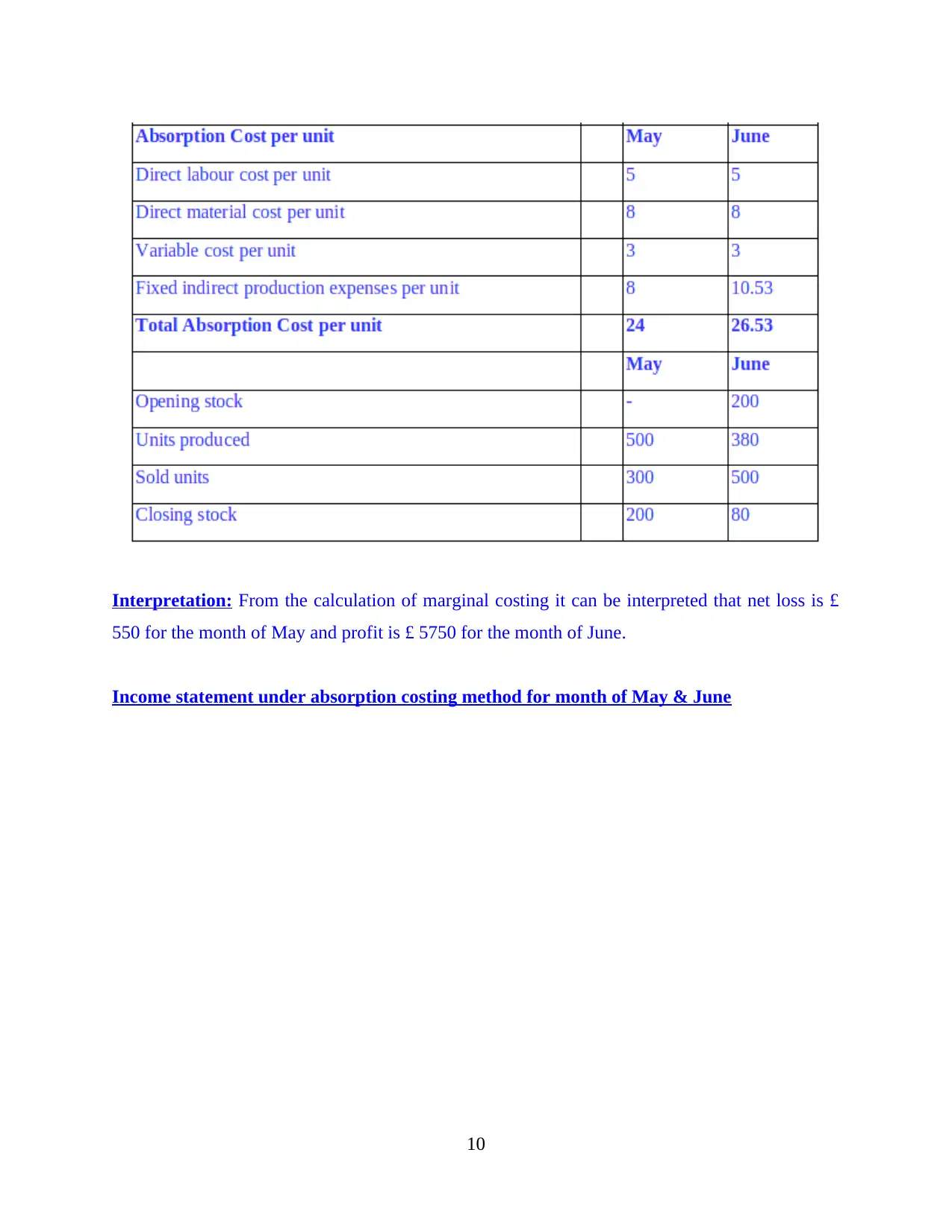

Interpretation: From the calculation of marginal costing it can be interpreted that net loss is £

550 for the month of May and profit is £ 5750 for the month of June.

Income statement under absorption costing method for month of May & June

10

550 for the month of May and profit is £ 5750 for the month of June.

Income statement under absorption costing method for month of May & June

10

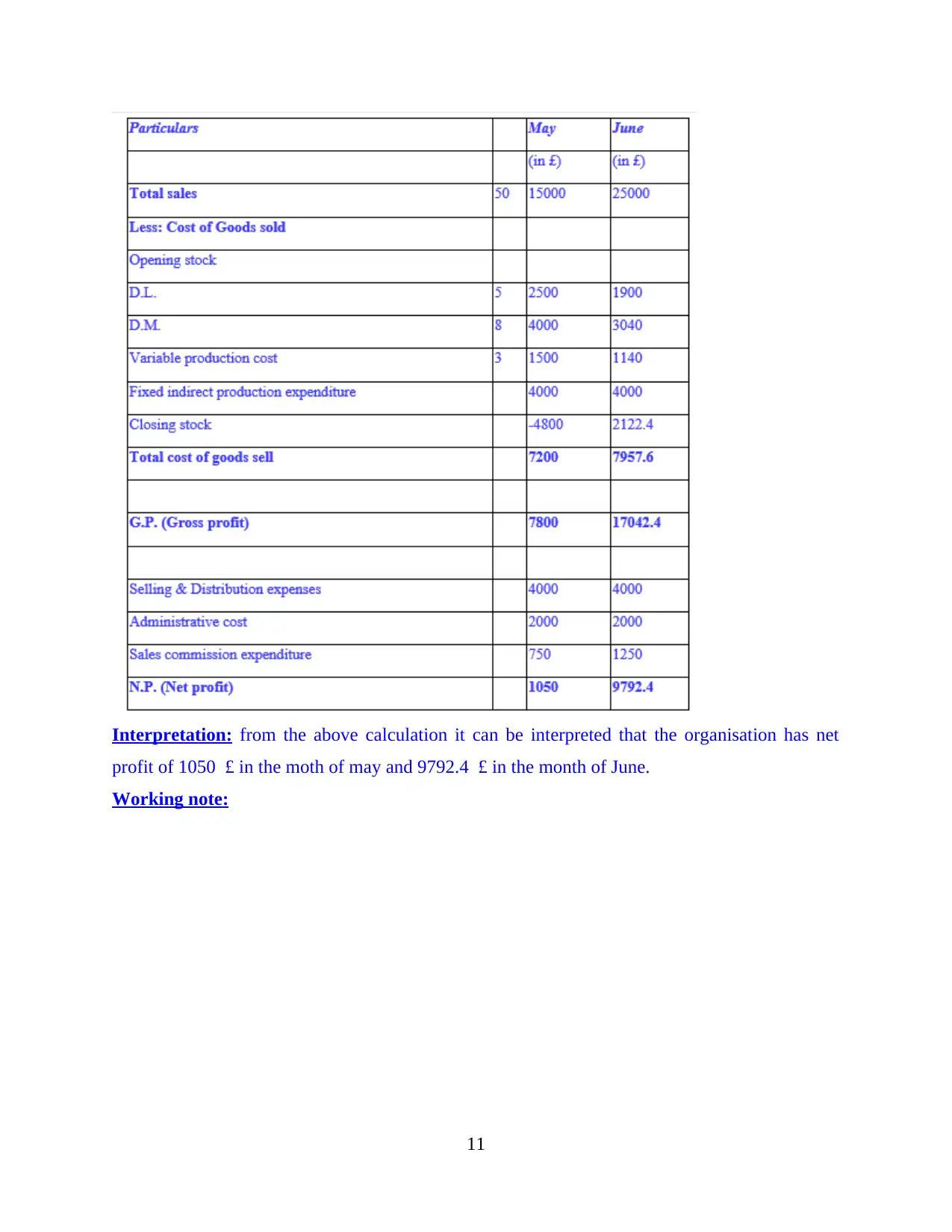

Interpretation: from the above calculation it can be interpreted that the organisation has net

profit of 1050 £ in the moth of may and 9792.4 £ in the month of June.

Working note:

11

profit of 1050 £ in the moth of may and 9792.4 £ in the month of June.

Working note:

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.