Management Accounting Report: Airdri Case Study and Analysis

VerifiedAdded on 2020/06/04

|19

|5287

|112

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to a UK-based business, Airdri. It begins with an introduction to management accounting, its importance, and various types, including cost accounting, inventory management, and job costing systems. The report then explores different management accounting reports, such as budget reports, accounts receivable aging reports, and job cost reports, explaining how these reports aid in decision-making. A significant portion of the report focuses on applying management accounting techniques to Airdri, demonstrating how it can reduce expenses, improve cash flow, and enhance financial returns. Furthermore, the report includes detailed calculations using marginal and absorption costing techniques to prepare income statements, highlighting the differences between these methods. It also discusses various planning tools for budgetary control and their advantages and disadvantages, along with their role in forecasting and problem-solving. The report concludes by evaluating how a management accounting system helps in responding to financial problems and contributing to the sustainable success of an organization. The report provides valuable insights into the practical application of management accounting in a real-world business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of its types............................................1

P2 Types of management accounting report...............................................................................3

M1 Application of management accounting on Airdri along with its benefits...........................5

D1 Integration of management accounting system.....................................................................6

TASK 2............................................................................................................................................6

P.3 Calculations for various costing techniques for Airdri.........................................................6

M2 essential requirement of management accounting technique in financial reporting............9

D2. Providing necessary information to general manager..........................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of planning tools used for budgetary control.....................10

M3 Planning tools for forecasting of budgets...........................................................................13

D2. Evaluating how planning tools can help in resolving problems.........................................13

TASK 4..........................................................................................................................................13

P5. Explaining how management accounting system helps in responding to problems...........13

M4. Analysing response of financial problems in the sustainable success of organisation......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of its types............................................1

P2 Types of management accounting report...............................................................................3

M1 Application of management accounting on Airdri along with its benefits...........................5

D1 Integration of management accounting system.....................................................................6

TASK 2............................................................................................................................................6

P.3 Calculations for various costing techniques for Airdri.........................................................6

M2 essential requirement of management accounting technique in financial reporting............9

D2. Providing necessary information to general manager..........................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of planning tools used for budgetary control.....................10

M3 Planning tools for forecasting of budgets...........................................................................13

D2. Evaluating how planning tools can help in resolving problems.........................................13

TASK 4..........................................................................................................................................13

P5. Explaining how management accounting system helps in responding to problems...........13

M4. Analysing response of financial problems in the sustainable success of organisation......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting also known as managerial accounting provides aid to the

decision making of management by analysing costs and operations of business and preparing

internal financial records, reports and accounts. This system facilitates financial accounting and

financial statement preparation. The main purpose of management accounting is to provide

relevant data to the internal users like management which will enable them in taking future

economic decisions regarding sales, revenue, cost, expenditure, expansion of business, etc. In the

present report various tools and techniques of management accounting has been used along with

the use of those tools and techniques. For the better understanding of this research report,

discussion is based on a small business organisation i.e. Airdri that is based on UK. Various

information is provided to the general manger of Airdri regarding management accounting, its

types, reports under management accounting etc. Further for organisation, income statement has

been prepared with two of the management accounting techniques that is marginal costing and

absorption costing along with explaining difference among two. Different budgets that are used

in management accounting are also provided below.

TASK 1

An Organisation to get success and to get favourable growth in world of competition

need to analyse its internal strength. Therefore, management accounting is a technique that

enables managers and small business owners to take economic future decisions along with

identifying favourable solutions to the business problems (AbRahman and et.al., 2016). It also

helps in improving the efficiency of business operations by using some tools like budgets, costs,

revenue, etc.

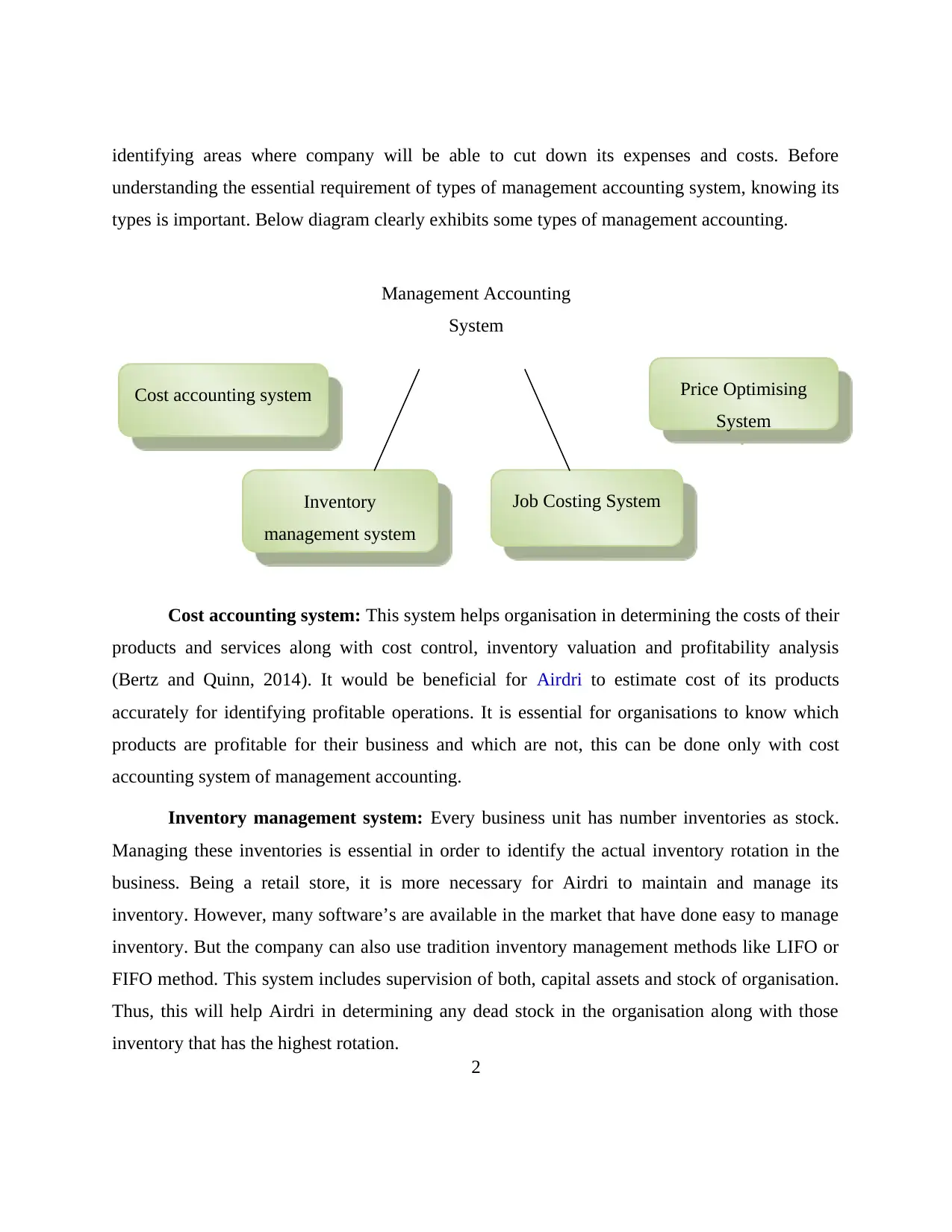

P1 Management accounting and essential requirement of its types

There are different types of management accounting system that can help Airdri in taking

informed decisions by providing the management accurate and timely information such as cost

cutting, increasing time of production, preparation of budgets etc. This system will also be

fruitful for Airdri for adequate allocation of funds in activities like material purchase along with

1

Management accounting also known as managerial accounting provides aid to the

decision making of management by analysing costs and operations of business and preparing

internal financial records, reports and accounts. This system facilitates financial accounting and

financial statement preparation. The main purpose of management accounting is to provide

relevant data to the internal users like management which will enable them in taking future

economic decisions regarding sales, revenue, cost, expenditure, expansion of business, etc. In the

present report various tools and techniques of management accounting has been used along with

the use of those tools and techniques. For the better understanding of this research report,

discussion is based on a small business organisation i.e. Airdri that is based on UK. Various

information is provided to the general manger of Airdri regarding management accounting, its

types, reports under management accounting etc. Further for organisation, income statement has

been prepared with two of the management accounting techniques that is marginal costing and

absorption costing along with explaining difference among two. Different budgets that are used

in management accounting are also provided below.

TASK 1

An Organisation to get success and to get favourable growth in world of competition

need to analyse its internal strength. Therefore, management accounting is a technique that

enables managers and small business owners to take economic future decisions along with

identifying favourable solutions to the business problems (AbRahman and et.al., 2016). It also

helps in improving the efficiency of business operations by using some tools like budgets, costs,

revenue, etc.

P1 Management accounting and essential requirement of its types

There are different types of management accounting system that can help Airdri in taking

informed decisions by providing the management accurate and timely information such as cost

cutting, increasing time of production, preparation of budgets etc. This system will also be

fruitful for Airdri for adequate allocation of funds in activities like material purchase along with

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identifying areas where company will be able to cut down its expenses and costs. Before

understanding the essential requirement of types of management accounting system, knowing its

types is important. Below diagram clearly exhibits some types of management accounting.

Management Accounting

System

Cost accounting system: This system helps organisation in determining the costs of their

products and services along with cost control, inventory valuation and profitability analysis

(Bertz and Quinn, 2014). It would be beneficial for Airdri to estimate cost of its products

accurately for identifying profitable operations. It is essential for organisations to know which

products are profitable for their business and which are not, this can be done only with cost

accounting system of management accounting.

Inventory management system: Every business unit has number inventories as stock.

Managing these inventories is essential in order to identify the actual inventory rotation in the

business. Being a retail store, it is more necessary for Airdri to maintain and manage its

inventory. However, many software’s are available in the market that have done easy to manage

inventory. But the company can also use tradition inventory management methods like LIFO or

FIFO method. This system includes supervision of both, capital assets and stock of organisation.

Thus, this will help Airdri in determining any dead stock in the organisation along with those

inventory that has the highest rotation.

2

Cost accounting system

Inventory

management system

Job Costing System

Price Optimising

System

understanding the essential requirement of types of management accounting system, knowing its

types is important. Below diagram clearly exhibits some types of management accounting.

Management Accounting

System

Cost accounting system: This system helps organisation in determining the costs of their

products and services along with cost control, inventory valuation and profitability analysis

(Bertz and Quinn, 2014). It would be beneficial for Airdri to estimate cost of its products

accurately for identifying profitable operations. It is essential for organisations to know which

products are profitable for their business and which are not, this can be done only with cost

accounting system of management accounting.

Inventory management system: Every business unit has number inventories as stock.

Managing these inventories is essential in order to identify the actual inventory rotation in the

business. Being a retail store, it is more necessary for Airdri to maintain and manage its

inventory. However, many software’s are available in the market that have done easy to manage

inventory. But the company can also use tradition inventory management methods like LIFO or

FIFO method. This system includes supervision of both, capital assets and stock of organisation.

Thus, this will help Airdri in determining any dead stock in the organisation along with those

inventory that has the highest rotation.

2

Cost accounting system

Inventory

management system

Job Costing System

Price Optimising

System

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job Costing system: This method of management accounting system helps in assigning

manufacturing cost to different products of the company. This method id applied when there is a

significant difference among products (Bryer, 2013). However, in case of identical products,

process costing system is used. With the use of this system, management of Airdri would be able

to accumulate cost of labour and overheads to different jobs which ultimately will help in

identifying areas where cost can be reduced.

Price Optimising system: This system of management accounting by using

mathematical analysis determines the response of customers at different price levels of its

products and services. This system will also help Airdri in identifying the best price of its

products that would help in meeting its business objectives like profit maximisation. This system

works using data like inventories, historic prices, operating costs and sales volume.

All the above explained system of management accounting will ultimately benefit Airdri

in making future economic decisions and achieving its business goals and objectives along with

increasing the performance of business.

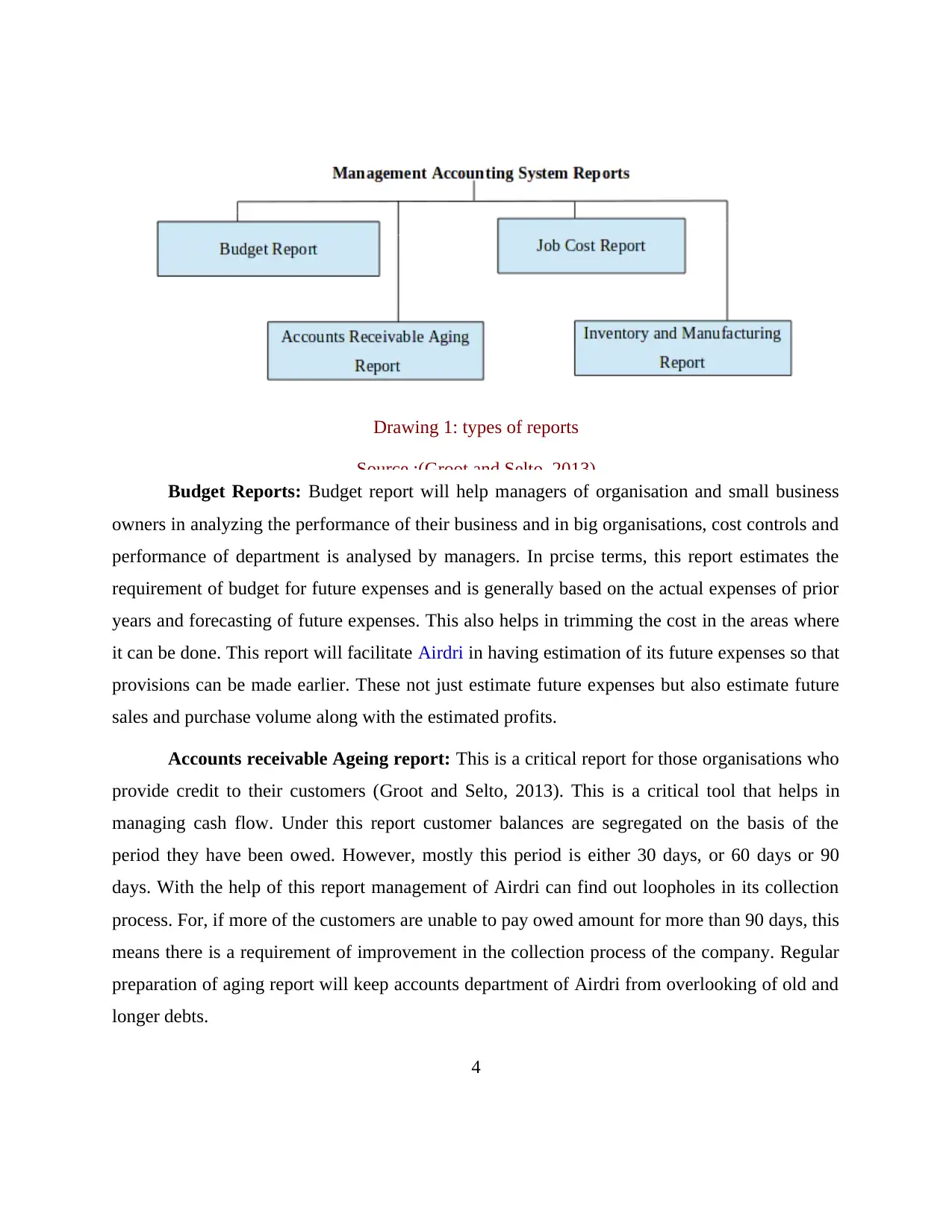

P2 Types of management accounting report

Management accounting is all about providing information to management that to

facilitate decision making. Therefore, to provide information that is necessary for decision

making management accounting reports is used. Different reports provide different information

to its users. Thus, it would be feasible for management Airdri to make favourable decisions using

these reports. The main reason behind the preparation of these reports is identification of

loopholes in the business operations (Chan, 2015). However, no fixed time period is there for the

preparation of these report, these are made as per the needs and requirements of managerial

information. Below diagram exhibits few of such reports.

3

manufacturing cost to different products of the company. This method id applied when there is a

significant difference among products (Bryer, 2013). However, in case of identical products,

process costing system is used. With the use of this system, management of Airdri would be able

to accumulate cost of labour and overheads to different jobs which ultimately will help in

identifying areas where cost can be reduced.

Price Optimising system: This system of management accounting by using

mathematical analysis determines the response of customers at different price levels of its

products and services. This system will also help Airdri in identifying the best price of its

products that would help in meeting its business objectives like profit maximisation. This system

works using data like inventories, historic prices, operating costs and sales volume.

All the above explained system of management accounting will ultimately benefit Airdri

in making future economic decisions and achieving its business goals and objectives along with

increasing the performance of business.

P2 Types of management accounting report

Management accounting is all about providing information to management that to

facilitate decision making. Therefore, to provide information that is necessary for decision

making management accounting reports is used. Different reports provide different information

to its users. Thus, it would be feasible for management Airdri to make favourable decisions using

these reports. The main reason behind the preparation of these reports is identification of

loopholes in the business operations (Chan, 2015). However, no fixed time period is there for the

preparation of these report, these are made as per the needs and requirements of managerial

information. Below diagram exhibits few of such reports.

3

Drawing 1: types of reports

Source :(Groot and Selto, 2013)

Budget Reports: Budget report will help managers of organisation and small business

owners in analyzing the performance of their business and in big organisations, cost controls and

performance of department is analysed by managers. In prcise terms, this report estimates the

requirement of budget for future expenses and is generally based on the actual expenses of prior

years and forecasting of future expenses. This also helps in trimming the cost in the areas where

it can be done. This report will facilitate Airdri in having estimation of its future expenses so that

provisions can be made earlier. These not just estimate future expenses but also estimate future

sales and purchase volume along with the estimated profits.

Accounts receivable Ageing report: This is a critical report for those organisations who

provide credit to their customers (Groot and Selto, 2013). This is a critical tool that helps in

managing cash flow. Under this report customer balances are segregated on the basis of the

period they have been owed. However, mostly this period is either 30 days, or 60 days or 90

days. With the help of this report management of Airdri can find out loopholes in its collection

process. For, if more of the customers are unable to pay owed amount for more than 90 days, this

means there is a requirement of improvement in the collection process of the company. Regular

preparation of aging report will keep accounts department of Airdri from overlooking of old and

longer debts.

4

Source :(Groot and Selto, 2013)

Budget Reports: Budget report will help managers of organisation and small business

owners in analyzing the performance of their business and in big organisations, cost controls and

performance of department is analysed by managers. In prcise terms, this report estimates the

requirement of budget for future expenses and is generally based on the actual expenses of prior

years and forecasting of future expenses. This also helps in trimming the cost in the areas where

it can be done. This report will facilitate Airdri in having estimation of its future expenses so that

provisions can be made earlier. These not just estimate future expenses but also estimate future

sales and purchase volume along with the estimated profits.

Accounts receivable Ageing report: This is a critical report for those organisations who

provide credit to their customers (Groot and Selto, 2013). This is a critical tool that helps in

managing cash flow. Under this report customer balances are segregated on the basis of the

period they have been owed. However, mostly this period is either 30 days, or 60 days or 90

days. With the help of this report management of Airdri can find out loopholes in its collection

process. For, if more of the customers are unable to pay owed amount for more than 90 days, this

means there is a requirement of improvement in the collection process of the company. Regular

preparation of aging report will keep accounts department of Airdri from overlooking of old and

longer debts.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job Cost Report: This report helps in showing expenses of a particular job or project.

These expenses of particular project are then matched with the estimated revenue in order to

evaluate the profitability of different projects. This enables company in knowing which projects

are profitable and which are not. Through this report Airdri can identify its high earning areas

and can make decisions accordingly to focus more efforts on profitable areas rather than wasting

resources on non profitable areas (Joshi and Li, 2016). With the help of job costing report,

expenses can be analysed during the progress of project so that areas of wastage can be corrected

before the cots escalate.

Inventory and manufacturing report: This report is generally requires on Airdri where

manufacturing takes place or those where there is physical inventory. By using this report those

organisations can make their manufacturing process more efficient. Main components of this

report are amount of wastage inventory, labour cost per hour or overheads cost per unit. By

analysing and comparing all the assembly lines within a business unit areas for improvement can

be determined along with best performing departments.

M1 Application of management accounting on Airdri along with its benefits

Management accounting has a wide scope, this can be applied within Airdri in the form

of tax accounting, financial accounting, internal auditing, activity management, inventory

management, cost accounting, price optimising system, etc. All these systems will provide

benefits to Airdri in following ways:

Reduction in Expenses: With the help of management accounting system, Airdri will be

enable in reducing its cost and other operational expenses. Cost of economic resources and other

operations can be reviewed.

Improved cash flow: Budgets under management accounting system are important part

of any business (Khodzytska and Ivchenko, 2014). With the use of budgets, Airdri can have a

financial road map for its future business expenses.

Business decisions: Management accounting system by providing information facilitates

managers in taking decisions for future like business expansion, etc. management accounting

will provide Airdri quantitative information that will enable in better decision making.

5

These expenses of particular project are then matched with the estimated revenue in order to

evaluate the profitability of different projects. This enables company in knowing which projects

are profitable and which are not. Through this report Airdri can identify its high earning areas

and can make decisions accordingly to focus more efforts on profitable areas rather than wasting

resources on non profitable areas (Joshi and Li, 2016). With the help of job costing report,

expenses can be analysed during the progress of project so that areas of wastage can be corrected

before the cots escalate.

Inventory and manufacturing report: This report is generally requires on Airdri where

manufacturing takes place or those where there is physical inventory. By using this report those

organisations can make their manufacturing process more efficient. Main components of this

report are amount of wastage inventory, labour cost per hour or overheads cost per unit. By

analysing and comparing all the assembly lines within a business unit areas for improvement can

be determined along with best performing departments.

M1 Application of management accounting on Airdri along with its benefits

Management accounting has a wide scope, this can be applied within Airdri in the form

of tax accounting, financial accounting, internal auditing, activity management, inventory

management, cost accounting, price optimising system, etc. All these systems will provide

benefits to Airdri in following ways:

Reduction in Expenses: With the help of management accounting system, Airdri will be

enable in reducing its cost and other operational expenses. Cost of economic resources and other

operations can be reviewed.

Improved cash flow: Budgets under management accounting system are important part

of any business (Khodzytska and Ivchenko, 2014). With the use of budgets, Airdri can have a

financial road map for its future business expenses.

Business decisions: Management accounting system by providing information facilitates

managers in taking decisions for future like business expansion, etc. management accounting

will provide Airdri quantitative information that will enable in better decision making.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increase financial returns: With all above benefits, the performance of business and its

financial returns also increases.

D1 Integration of management accounting system

Managerial accounting provides quantitative as well as qualitative information to the

management of organisation for better decision making process (Klemstine and Maher, 2014).

Hence, management accounting information can be integrated in Airdri by the use of its owners,

managers and employees, by planning and controlling of business activities, cash management

and continuous improvement and decision making process. With the constant measurement and

improvement in the various processes of business, techniques of management accounting will be

beneficial and can be integrated within the organisation.

TASK 2

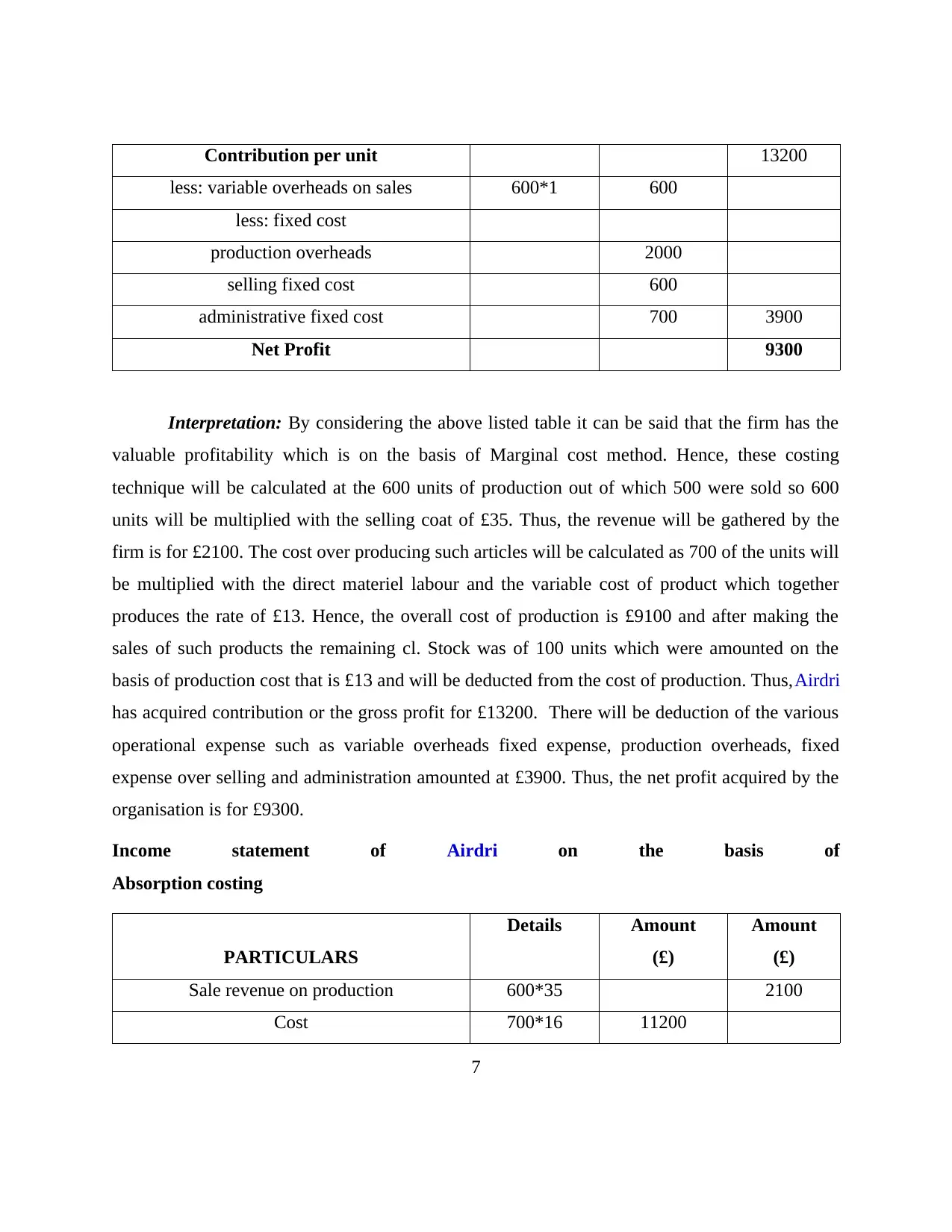

P.3 Calculations for various costing techniques for Airdri

For the purpose of calculation and preparation of income statement, professionals of

Airdri can use two techniques i.e. absorption costing technique and marginal costing techniques.

Both the methods differ from each other because marginal costing technique takes into account

only variable expenses while absorption costing technique takes into account all the expenses

including fixed and variable. Hence, it will be beneficial in analysing the profitability and

revenue earnings of the firm. Thus, in the tables listed below will describe marginal and

absorption costing methods which will reflect lights on the profit gathering of Airdri such as:

Income statement of Airdri on the basis of

Marginal costing

PARTICULARS

Details Amount

(£)

Amount

(£)

Sale revenue on production 600*35 2100

Cost 700*13 9100

Less: closing stock 100*13 1300

variable cost 7800

6

financial returns also increases.

D1 Integration of management accounting system

Managerial accounting provides quantitative as well as qualitative information to the

management of organisation for better decision making process (Klemstine and Maher, 2014).

Hence, management accounting information can be integrated in Airdri by the use of its owners,

managers and employees, by planning and controlling of business activities, cash management

and continuous improvement and decision making process. With the constant measurement and

improvement in the various processes of business, techniques of management accounting will be

beneficial and can be integrated within the organisation.

TASK 2

P.3 Calculations for various costing techniques for Airdri

For the purpose of calculation and preparation of income statement, professionals of

Airdri can use two techniques i.e. absorption costing technique and marginal costing techniques.

Both the methods differ from each other because marginal costing technique takes into account

only variable expenses while absorption costing technique takes into account all the expenses

including fixed and variable. Hence, it will be beneficial in analysing the profitability and

revenue earnings of the firm. Thus, in the tables listed below will describe marginal and

absorption costing methods which will reflect lights on the profit gathering of Airdri such as:

Income statement of Airdri on the basis of

Marginal costing

PARTICULARS

Details Amount

(£)

Amount

(£)

Sale revenue on production 600*35 2100

Cost 700*13 9100

Less: closing stock 100*13 1300

variable cost 7800

6

Contribution per unit 13200

less: variable overheads on sales 600*1 600

less: fixed cost

production overheads 2000

selling fixed cost 600

administrative fixed cost 700 3900

Net Profit 9300

Interpretation: By considering the above listed table it can be said that the firm has the

valuable profitability which is on the basis of Marginal cost method. Hence, these costing

technique will be calculated at the 600 units of production out of which 500 were sold so 600

units will be multiplied with the selling coat of £35. Thus, the revenue will be gathered by the

firm is for £2100. The cost over producing such articles will be calculated as 700 of the units will

be multiplied with the direct materiel labour and the variable cost of product which together

produces the rate of £13. Hence, the overall cost of production is £9100 and after making the

sales of such products the remaining cl. Stock was of 100 units which were amounted on the

basis of production cost that is £13 and will be deducted from the cost of production. Thus,Airdri

has acquired contribution or the gross profit for £13200. There will be deduction of the various

operational expense such as variable overheads fixed expense, production overheads, fixed

expense over selling and administration amounted at £3900. Thus, the net profit acquired by the

organisation is for £9300.

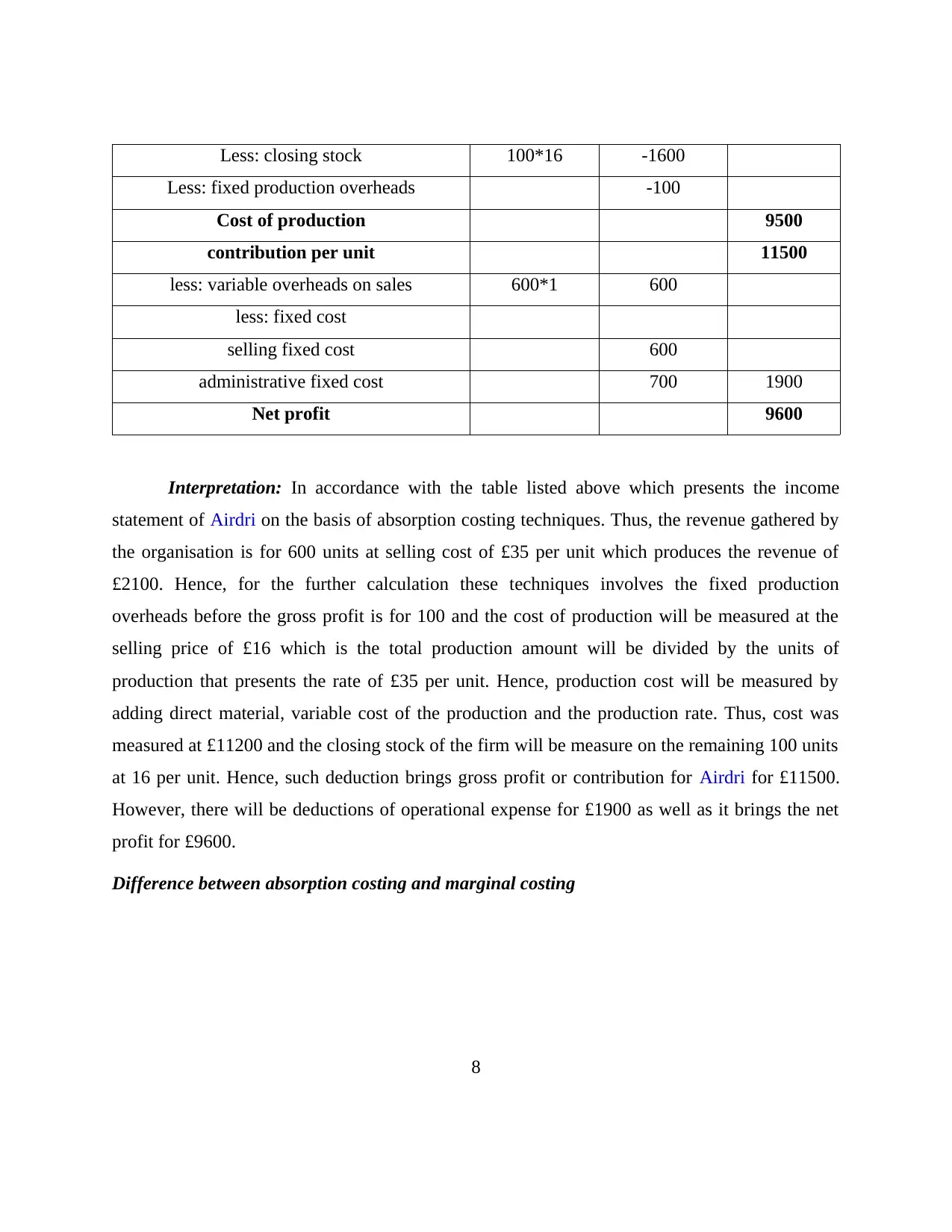

Income statement of Airdri on the basis of

Absorption costing

PARTICULARS

Details Amount

(£)

Amount

(£)

Sale revenue on production 600*35 2100

Cost 700*16 11200

7

less: variable overheads on sales 600*1 600

less: fixed cost

production overheads 2000

selling fixed cost 600

administrative fixed cost 700 3900

Net Profit 9300

Interpretation: By considering the above listed table it can be said that the firm has the

valuable profitability which is on the basis of Marginal cost method. Hence, these costing

technique will be calculated at the 600 units of production out of which 500 were sold so 600

units will be multiplied with the selling coat of £35. Thus, the revenue will be gathered by the

firm is for £2100. The cost over producing such articles will be calculated as 700 of the units will

be multiplied with the direct materiel labour and the variable cost of product which together

produces the rate of £13. Hence, the overall cost of production is £9100 and after making the

sales of such products the remaining cl. Stock was of 100 units which were amounted on the

basis of production cost that is £13 and will be deducted from the cost of production. Thus,Airdri

has acquired contribution or the gross profit for £13200. There will be deduction of the various

operational expense such as variable overheads fixed expense, production overheads, fixed

expense over selling and administration amounted at £3900. Thus, the net profit acquired by the

organisation is for £9300.

Income statement of Airdri on the basis of

Absorption costing

PARTICULARS

Details Amount

(£)

Amount

(£)

Sale revenue on production 600*35 2100

Cost 700*16 11200

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: closing stock 100*16 -1600

Less: fixed production overheads -100

Cost of production 9500

contribution per unit 11500

less: variable overheads on sales 600*1 600

less: fixed cost

selling fixed cost 600

administrative fixed cost 700 1900

Net profit 9600

Interpretation: In accordance with the table listed above which presents the income

statement of Airdri on the basis of absorption costing techniques. Thus, the revenue gathered by

the organisation is for 600 units at selling cost of £35 per unit which produces the revenue of

£2100. Hence, for the further calculation these techniques involves the fixed production

overheads before the gross profit is for 100 and the cost of production will be measured at the

selling price of £16 which is the total production amount will be divided by the units of

production that presents the rate of £35 per unit. Hence, production cost will be measured by

adding direct material, variable cost of the production and the production rate. Thus, cost was

measured at £11200 and the closing stock of the firm will be measure on the remaining 100 units

at 16 per unit. Hence, such deduction brings gross profit or contribution for Airdri for £11500.

However, there will be deductions of operational expense for £1900 as well as it brings the net

profit for £9600.

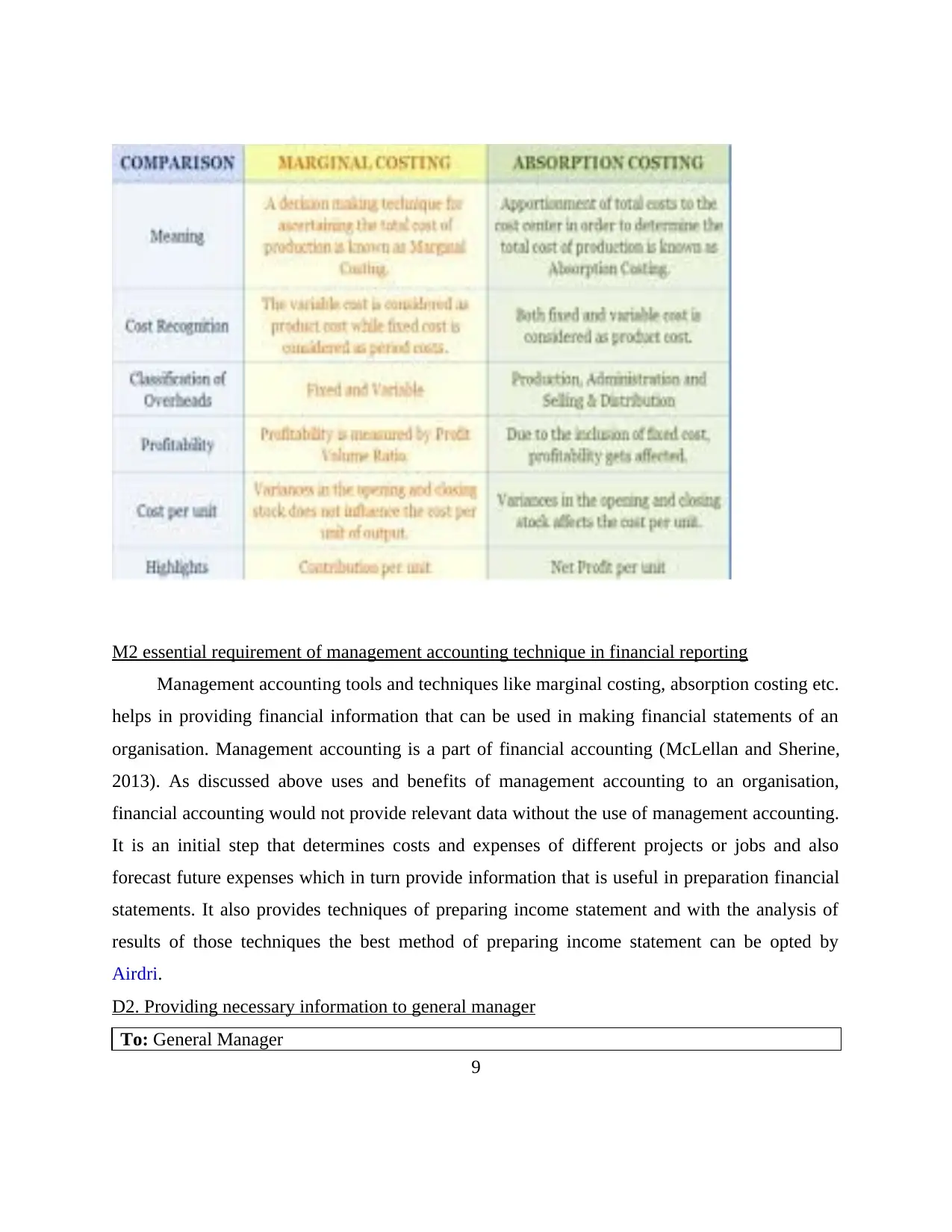

Difference between absorption costing and marginal costing

8

Less: fixed production overheads -100

Cost of production 9500

contribution per unit 11500

less: variable overheads on sales 600*1 600

less: fixed cost

selling fixed cost 600

administrative fixed cost 700 1900

Net profit 9600

Interpretation: In accordance with the table listed above which presents the income

statement of Airdri on the basis of absorption costing techniques. Thus, the revenue gathered by

the organisation is for 600 units at selling cost of £35 per unit which produces the revenue of

£2100. Hence, for the further calculation these techniques involves the fixed production

overheads before the gross profit is for 100 and the cost of production will be measured at the

selling price of £16 which is the total production amount will be divided by the units of

production that presents the rate of £35 per unit. Hence, production cost will be measured by

adding direct material, variable cost of the production and the production rate. Thus, cost was

measured at £11200 and the closing stock of the firm will be measure on the remaining 100 units

at 16 per unit. Hence, such deduction brings gross profit or contribution for Airdri for £11500.

However, there will be deductions of operational expense for £1900 as well as it brings the net

profit for £9600.

Difference between absorption costing and marginal costing

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 essential requirement of management accounting technique in financial reporting

Management accounting tools and techniques like marginal costing, absorption costing etc.

helps in providing financial information that can be used in making financial statements of an

organisation. Management accounting is a part of financial accounting (McLellan and Sherine,

2013). As discussed above uses and benefits of management accounting to an organisation,

financial accounting would not provide relevant data without the use of management accounting.

It is an initial step that determines costs and expenses of different projects or jobs and also

forecast future expenses which in turn provide information that is useful in preparation financial

statements. It also provides techniques of preparing income statement and with the analysis of

results of those techniques the best method of preparing income statement can be opted by

Airdri.

D2. Providing necessary information to general manager

To: General Manager

9

Management accounting tools and techniques like marginal costing, absorption costing etc.

helps in providing financial information that can be used in making financial statements of an

organisation. Management accounting is a part of financial accounting (McLellan and Sherine,

2013). As discussed above uses and benefits of management accounting to an organisation,

financial accounting would not provide relevant data without the use of management accounting.

It is an initial step that determines costs and expenses of different projects or jobs and also

forecast future expenses which in turn provide information that is useful in preparation financial

statements. It also provides techniques of preparing income statement and with the analysis of

results of those techniques the best method of preparing income statement can be opted by

Airdri.

D2. Providing necessary information to general manager

To: General Manager

9

(Airdri store)

From: Management accountant

(Airdri store)

Subject: Information regarding revenues from different techniques

Dear sir,

It is to provide you information that has been assessed by preparing income statement

with marginal costing system and absorption costing system. Preparation of income statement

has been completed. However, there is not much difference between the results of net profit of

both the techniques. But, income statement using absorption costing shows net profit with

£300 more than the income statement prepared by using marginal costing. Therefore, it would

be beneficial for Airdri to use absorption coasting technique because with this better

performance of the company can be shown to its stakeholders.

Thanks and Regards

TASK 3

P4 Advantages and disadvantages of planning tools used for budgetary control

With the use of planning and budgetary control tools will help Airdri in determining

required and adequate information about the firm (UK HR SUPPORT ASSISTANT, 2017). These

techniques include various budgets which will help organisation in strengthening its internal

operations which will enable the company in meeting its future obstacles and problems in the

areas like, production, sales, cash flow, etc. every organisation have different benefits along with

various loopholes which are mostly undermined, these planning and budgetary control tools not

only helps in determining these loopholes but also provides solution to them (Nørrekli, 2014).

Below are some budgeting tools along with their benefits and disadvantages.

Sales Budget: Preparation of sales budget will help Airdri in determining the expected

number of sales in near future along with the expected per unit price of products. By estimating

future sales and per unit price company can make decisions accordingly. For example if it has

10

From: Management accountant

(Airdri store)

Subject: Information regarding revenues from different techniques

Dear sir,

It is to provide you information that has been assessed by preparing income statement

with marginal costing system and absorption costing system. Preparation of income statement

has been completed. However, there is not much difference between the results of net profit of

both the techniques. But, income statement using absorption costing shows net profit with

£300 more than the income statement prepared by using marginal costing. Therefore, it would

be beneficial for Airdri to use absorption coasting technique because with this better

performance of the company can be shown to its stakeholders.

Thanks and Regards

TASK 3

P4 Advantages and disadvantages of planning tools used for budgetary control

With the use of planning and budgetary control tools will help Airdri in determining

required and adequate information about the firm (UK HR SUPPORT ASSISTANT, 2017). These

techniques include various budgets which will help organisation in strengthening its internal

operations which will enable the company in meeting its future obstacles and problems in the

areas like, production, sales, cash flow, etc. every organisation have different benefits along with

various loopholes which are mostly undermined, these planning and budgetary control tools not

only helps in determining these loopholes but also provides solution to them (Nørrekli, 2014).

Below are some budgeting tools along with their benefits and disadvantages.

Sales Budget: Preparation of sales budget will help Airdri in determining the expected

number of sales in near future along with the expected per unit price of products. By estimating

future sales and per unit price company can make decisions accordingly. For example if it has

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.