Management Accounting: A. Reyrolle & Company Financial Analysis Report

VerifiedAdded on 2021/02/19

|23

|6319

|22

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within A. Reyrolle & Company, a British engineering firm. It explores the role and importance of management accounting (MA) in resolving financial issues, enhancing production, and improving employee performance. The report delves into various MA techniques, including cost reports, budgets, and job costing, used to present financial data, manage costs, and optimize pricing. It examines the benefits and limitations of different accounting tools, such as inventory management, job costing, and price optimization systems, and highlights their application in addressing financial challenges like sales variations and profit declines. The report also discusses costing methods like marginal and absorption costing, and elaborates on the integration of management accounting systems and their reports. This analysis aims to provide a clear understanding of how MA supports effective decision-making and financial management within the company, contributing to its strategic goals and overall success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is the procedure of recording, analysing, sorting, managing

activity of company via different accounting tools and take the efficient decisions to promote the

production of company and employees performance. It helps company to solve various problem

by evaluating the financial data. A. Reyrolle & company is a British engineering company which

is the one of the largest employers company on Tyneside. The aim of the company is to produce

the scientific instrument.

The study represents the role of MA in the company and the requirement of accounting to

resolve financial problem. It helps to explain the various technique used by the organization to

report the financial data like cost report, budget, job costing etc. which helps to present income

and expenditure of company by adopting the abnormal and marginal cost. Report explains the

various benefits and limitations of accounting system tools for controlling the budget. It also

highlights the MA system role to suggest solution for various problem related to the finance such

as variation in sales, revenue, decreasing profit etc.

LO 1

P1 MA and the need of MA system

Management accounting : MA is the procedure of using monetary information to

making the decisions for the company for effective and efficient management (Maas,

Schaltegger, and Crutzen, 2016). It supports managers decision to make policy, strategies, plans

to run the business organization. It is used by the internal users such as employee's, owner and

managers.

Requirement of MA systems

The focus of MA system is to give the information to the external and internal user such

as customer, employees, managers, owner, creditors, shareholders etc. MA system requires

taking the financial statement and evaluate the data via various reports like inventory

management report, job costing report, cost report etc. MA system support the decision of the

organisation take the effective and efficient measures by using the various accounting system.

(Cooper, Ezzamel, and Qu, 2017).

Inventory management system: This system lays focus on using software for managing

inventory level, order the inventory, billing the raw material etc. It is required by the A. Reyrolle

3

Management accounting is the procedure of recording, analysing, sorting, managing

activity of company via different accounting tools and take the efficient decisions to promote the

production of company and employees performance. It helps company to solve various problem

by evaluating the financial data. A. Reyrolle & company is a British engineering company which

is the one of the largest employers company on Tyneside. The aim of the company is to produce

the scientific instrument.

The study represents the role of MA in the company and the requirement of accounting to

resolve financial problem. It helps to explain the various technique used by the organization to

report the financial data like cost report, budget, job costing etc. which helps to present income

and expenditure of company by adopting the abnormal and marginal cost. Report explains the

various benefits and limitations of accounting system tools for controlling the budget. It also

highlights the MA system role to suggest solution for various problem related to the finance such

as variation in sales, revenue, decreasing profit etc.

LO 1

P1 MA and the need of MA system

Management accounting : MA is the procedure of using monetary information to

making the decisions for the company for effective and efficient management (Maas,

Schaltegger, and Crutzen, 2016). It supports managers decision to make policy, strategies, plans

to run the business organization. It is used by the internal users such as employee's, owner and

managers.

Requirement of MA systems

The focus of MA system is to give the information to the external and internal user such

as customer, employees, managers, owner, creditors, shareholders etc. MA system requires

taking the financial statement and evaluate the data via various reports like inventory

management report, job costing report, cost report etc. MA system support the decision of the

organisation take the effective and efficient measures by using the various accounting system.

(Cooper, Ezzamel, and Qu, 2017).

Inventory management system: This system lays focus on using software for managing

inventory level, order the inventory, billing the raw material etc. It is required by the A. Reyrolle

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

& company to manage their organization scientific tool and order the quantity when it demanded

in the market (Chenhall, and Moers, 2015). Management of inventory level in organisation help

to reduce the maintenance cost of the inventory in their warehouses. It also supports the

organization to take the effective measures regarding the order level and order the quantity which

they require.

Job costing system : In job costing report the work of task is divided indifferent job and

each job is evaluate on the basis of its importance to the organization. It is used to track the

financial effectiveness and efficiency in the organization. A. Reyrolle & company use the job

costing reporting method to focus on the activity which is highly required by the company. It

helps to monitor and control the different jobs or activities which generate higher profit rather

than to wasting time on less required activities.

Price optimisation system : It is an effective reporting method used by the company to

estimate the price of goods. It helps them to meet their goal and objective by increasing their

profit and revenue of the company. A. Reyrolle & company require the price optimization

system to measure the price of each activity to accomplish the project of providing scientific tool

to the customer (Thomas, 2016).

Cost accounting system : It is used by the firm to record and track production activity by

using the perpetual inventory system. It is required by the company to analyse the profitability,

efficiency and valuation of inventory level in the organization. The estimation of cost of the

product also help to prepare the budget of organisation or firm which measures the activity of the

firm by balancing its performance to the previous month performance. It includes the various

costing method such as job order costing, process costing, traditional costing, activity based

costing etc. (Collis and Hussey, 2017). The use of process costing is to estimate the

manufacturing expenses of process separately, so they can evaluate the cost required by each

process and control the process separately. It also helps the company to manage the tome and

cost by focusing on the individual process rather than to whole process.

P2. Different methods defined under the MA reporting.

This term is defines as a process related with preparation of internal statement by

considering all the monetary as well as arithmetical info aiding in the process of decision making

of company's management. It helps company in providing better understanding of current

business operations and assist in making day to day decision for the improvement of commercial

4

in the market (Chenhall, and Moers, 2015). Management of inventory level in organisation help

to reduce the maintenance cost of the inventory in their warehouses. It also supports the

organization to take the effective measures regarding the order level and order the quantity which

they require.

Job costing system : In job costing report the work of task is divided indifferent job and

each job is evaluate on the basis of its importance to the organization. It is used to track the

financial effectiveness and efficiency in the organization. A. Reyrolle & company use the job

costing reporting method to focus on the activity which is highly required by the company. It

helps to monitor and control the different jobs or activities which generate higher profit rather

than to wasting time on less required activities.

Price optimisation system : It is an effective reporting method used by the company to

estimate the price of goods. It helps them to meet their goal and objective by increasing their

profit and revenue of the company. A. Reyrolle & company require the price optimization

system to measure the price of each activity to accomplish the project of providing scientific tool

to the customer (Thomas, 2016).

Cost accounting system : It is used by the firm to record and track production activity by

using the perpetual inventory system. It is required by the company to analyse the profitability,

efficiency and valuation of inventory level in the organization. The estimation of cost of the

product also help to prepare the budget of organisation or firm which measures the activity of the

firm by balancing its performance to the previous month performance. It includes the various

costing method such as job order costing, process costing, traditional costing, activity based

costing etc. (Collis and Hussey, 2017). The use of process costing is to estimate the

manufacturing expenses of process separately, so they can evaluate the cost required by each

process and control the process separately. It also helps the company to manage the tome and

cost by focusing on the individual process rather than to whole process.

P2. Different methods defined under the MA reporting.

This term is defines as a process related with preparation of internal statement by

considering all the monetary as well as arithmetical info aiding in the process of decision making

of company's management. It helps company in providing better understanding of current

business operations and assist in making day to day decision for the improvement of commercial

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

areas and objects. There are several methods of preparing managerial report that can be used by

A. Reyrolle & Company:

1. Performance Report – The presentation is measured as one of the greatest significant

for every commercial organization which helps in conducting functions related to

monitoring, controlling and reviewing performance level of its operations, processes. It

further assists in monitoring performance of employees and team as a whole as involved

in carrying on a particular business activity. Furthermore, such report provides a base to

A. Reyrolle & Company in strategic decisions for future growth and success of both.

Such delivers a bottomless vision around the employed processes, concepts and

techniques relevant for smooth business activities (Maas, Schaltegger and Crutzen,

2016). By keeping track, it helps in determining whether company is performing

effectively as per the strategies and plans made on the way to the achievement of

commercial areas and if any changes required.

2. Cost Managerial Accounting Report – It determines cost amount incurred for carrying

on production function of the company. At the time of computing cost amount it takes

into account all the expenses related to raw material, overhead, labour and others issues.

It helps the management of A. Reyrolle & Company in making proper realization of the

cost price as well as of selling prices being charged for their products and services for

estimating amount of profit or loss going to happen in the near upcoming after such

business transaction.

3. Budget Report – It elaborates budgetary targets as made by company for making proper

and effective distribution of available occupational as well as monetary capitals. By

framing financial plans it helps A. Reyrolle & Company in projecting future business

expenses and revenue amount. It helps company in making comparison if actual

outcomes with the estimation made for determining variances if any. Further it provides

details about amount of money required to be spent on carrying on any future business

operations. Thus, A. Reyrolle & Company by formulating budgetary plans and strategies

can make more profit and improves its performance. It provides better understanding to

management in making effective use of limited resources. By the assistance of financial

plan report, assessment can be made of own performance level by evaluating whether

5

A. Reyrolle & Company:

1. Performance Report – The presentation is measured as one of the greatest significant

for every commercial organization which helps in conducting functions related to

monitoring, controlling and reviewing performance level of its operations, processes. It

further assists in monitoring performance of employees and team as a whole as involved

in carrying on a particular business activity. Furthermore, such report provides a base to

A. Reyrolle & Company in strategic decisions for future growth and success of both.

Such delivers a bottomless vision around the employed processes, concepts and

techniques relevant for smooth business activities (Maas, Schaltegger and Crutzen,

2016). By keeping track, it helps in determining whether company is performing

effectively as per the strategies and plans made on the way to the achievement of

commercial areas and if any changes required.

2. Cost Managerial Accounting Report – It determines cost amount incurred for carrying

on production function of the company. At the time of computing cost amount it takes

into account all the expenses related to raw material, overhead, labour and others issues.

It helps the management of A. Reyrolle & Company in making proper realization of the

cost price as well as of selling prices being charged for their products and services for

estimating amount of profit or loss going to happen in the near upcoming after such

business transaction.

3. Budget Report – It elaborates budgetary targets as made by company for making proper

and effective distribution of available occupational as well as monetary capitals. By

framing financial plans it helps A. Reyrolle & Company in projecting future business

expenses and revenue amount. It helps company in making comparison if actual

outcomes with the estimation made for determining variances if any. Further it provides

details about amount of money required to be spent on carrying on any future business

operations. Thus, A. Reyrolle & Company by formulating budgetary plans and strategies

can make more profit and improves its performance. It provides better understanding to

management in making effective use of limited resources. By the assistance of financial

plan report, assessment can be made of own performance level by evaluating whether

5

budget made is required to have any changes thereby determining unproductive business

areas incurring charge incidentals.

4. Account Receivable Aging Report – Such report is best for commercial organizations

that deeply rely on spreading praise amenities and services. It helps in determining the

amount which is due or going to be received in an average time period in lieu of credit

sales made to its customers. It is helpful to company especially in conducting its business

operations by gaining of raw material etc. on the credit basis. It further provides details

regarding list of defaulters which are making default in respect of the non-payment of

money (Novas, Alves and Sousa, 2017). A. Reyrolle & Company can evaluate all the

issues which is coming in the money collection process of the company. For overcoming

this default risk, it is required for company to formulate and implement strict policies and

plans in context of business operation carried on credit basis.

This system provides assistance in form of functions such as managing, controlling and

evaluation of all the business operations thereby suggesting any modification required for

making improvement therein. A. Reyrolle & Company by using this system can get benefits in

ways such as:

Management Accounting

System

Benefits

Cost Accounting System AA Reyrolle & Company by designing

financial plan can make contrast of real with

predictable one. Also, it helps in assessing the

most cost incurring part of business department

which is unproductive and unnecessary.

It helps in determining the cost associated with

operational activities, its efficiencies.

Inventory Management System It provides support to company in identifying and

minimizing all the cost related expenses which are

associated with the business operations (King and

Clarkson, 2015).

It helps in making proper valuation and

6

areas incurring charge incidentals.

4. Account Receivable Aging Report – Such report is best for commercial organizations

that deeply rely on spreading praise amenities and services. It helps in determining the

amount which is due or going to be received in an average time period in lieu of credit

sales made to its customers. It is helpful to company especially in conducting its business

operations by gaining of raw material etc. on the credit basis. It further provides details

regarding list of defaulters which are making default in respect of the non-payment of

money (Novas, Alves and Sousa, 2017). A. Reyrolle & Company can evaluate all the

issues which is coming in the money collection process of the company. For overcoming

this default risk, it is required for company to formulate and implement strict policies and

plans in context of business operation carried on credit basis.

This system provides assistance in form of functions such as managing, controlling and

evaluation of all the business operations thereby suggesting any modification required for

making improvement therein. A. Reyrolle & Company by using this system can get benefits in

ways such as:

Management Accounting

System

Benefits

Cost Accounting System AA Reyrolle & Company by designing

financial plan can make contrast of real with

predictable one. Also, it helps in assessing the

most cost incurring part of business department

which is unproductive and unnecessary.

It helps in determining the cost associated with

operational activities, its efficiencies.

Inventory Management System It provides support to company in identifying and

minimizing all the cost related expenses which are

associated with the business operations (King and

Clarkson, 2015).

It helps in making proper valuation and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management of inventory level which can bring

improvement in performance among its customer

and market and increase profitability.

By this scheme the stock out condition can be

avoided and management can have proper

inventory level.

Job Costing System It helps in assessing cost which has been assigned

per job or business activity for making effective

decision related to business process.

This scheme of management accounting helps in

observing, following level of performance of all the

individual employees as well as of the team for

making changes related to cost control, improving

business efficiency and productivity.

Elaborating integration of management accounting system and report

Management accounting system & report is used by company to evaluate performance by

taking different measures and using the various report to improve the effectiveness and

efficiency of the company. A. Reyrolle & company use the MA system to make the report for

gathering information regarding the company. The gathered information is evaluated by the

internal user such as managers, employees and owner to provide the efficient information to the

external users such as customer, creditors, client, government and stakeholders. MA report helps

to record all transaction regarding its sales, revenue, profit and expenses for the different purpose

such as to control the cost, managing the activities, deliver the products on time and improve the

performance according to the requirement and demand of the customer.

LO 2

P3 Use of different costing technique to prepare the income statements

MA techniques and tools : Organization use the MA tools and techniques to calculate

the cost of the company task. It supports them to control the cost of the production and ascertain

the area where the changes are required. There are different kinds of tools which help them to

7

improvement in performance among its customer

and market and increase profitability.

By this scheme the stock out condition can be

avoided and management can have proper

inventory level.

Job Costing System It helps in assessing cost which has been assigned

per job or business activity for making effective

decision related to business process.

This scheme of management accounting helps in

observing, following level of performance of all the

individual employees as well as of the team for

making changes related to cost control, improving

business efficiency and productivity.

Elaborating integration of management accounting system and report

Management accounting system & report is used by company to evaluate performance by

taking different measures and using the various report to improve the effectiveness and

efficiency of the company. A. Reyrolle & company use the MA system to make the report for

gathering information regarding the company. The gathered information is evaluated by the

internal user such as managers, employees and owner to provide the efficient information to the

external users such as customer, creditors, client, government and stakeholders. MA report helps

to record all transaction regarding its sales, revenue, profit and expenses for the different purpose

such as to control the cost, managing the activities, deliver the products on time and improve the

performance according to the requirement and demand of the customer.

LO 2

P3 Use of different costing technique to prepare the income statements

MA techniques and tools : Organization use the MA tools and techniques to calculate

the cost of the company task. It supports them to control the cost of the production and ascertain

the area where the changes are required. There are different kinds of tools which help them to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

present the income and expenditure of the company in proper format and as=certain the net loss

and profit in particular year (Scoccia and et.al., 2018).

Marginal costing : It is the method of calculating the cost by changing in per unit of

output. It is used by the company to determine the optimum use of resources and quantity of the

products manufactured by the company. It also helps to manage the product price when the

customer demanded the minimum price of the product with the higher quality.

Absorption costing system : In this method only fluctuating cost is assign to the

inventory of the organization. It includes the various cost like material expenses, employment

cost, fixed and variable overhead related to manufacturing activity etc. it is required for different

kinds of reporting such as income tax and external financial report (What is absorption costing?,

2019). The major variation in these to costing method is fixed cost. Marginal cost exclude the

fixed cost in its calculation but absorption cost method use the fixed cost in the calculation of

cost per unit and preparation of income statement.

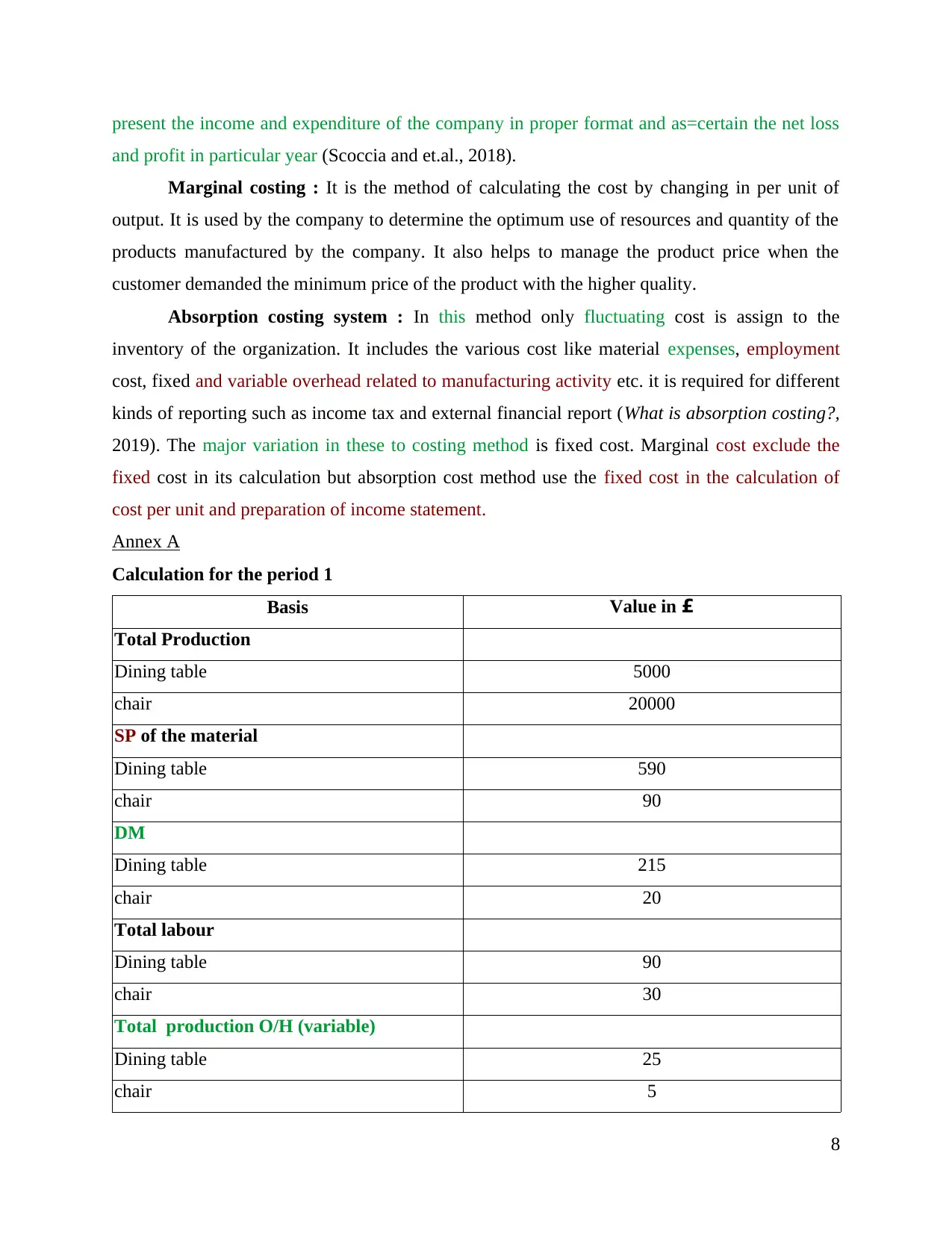

Annex A

Calculation for the period 1

Basis Value in £

Total Production

Dining table 5000

chair 20000

SP of the material

Dining table 590

chair 90

DM

Dining table 215

chair 20

Total labour

Dining table 90

chair 30

Total production O/H (variable)

Dining table 25

chair 5

8

and profit in particular year (Scoccia and et.al., 2018).

Marginal costing : It is the method of calculating the cost by changing in per unit of

output. It is used by the company to determine the optimum use of resources and quantity of the

products manufactured by the company. It also helps to manage the product price when the

customer demanded the minimum price of the product with the higher quality.

Absorption costing system : In this method only fluctuating cost is assign to the

inventory of the organization. It includes the various cost like material expenses, employment

cost, fixed and variable overhead related to manufacturing activity etc. it is required for different

kinds of reporting such as income tax and external financial report (What is absorption costing?,

2019). The major variation in these to costing method is fixed cost. Marginal cost exclude the

fixed cost in its calculation but absorption cost method use the fixed cost in the calculation of

cost per unit and preparation of income statement.

Annex A

Calculation for the period 1

Basis Value in £

Total Production

Dining table 5000

chair 20000

SP of the material

Dining table 590

chair 90

DM

Dining table 215

chair 20

Total labour

Dining table 90

chair 30

Total production O/H (variable)

Dining table 25

chair 5

8

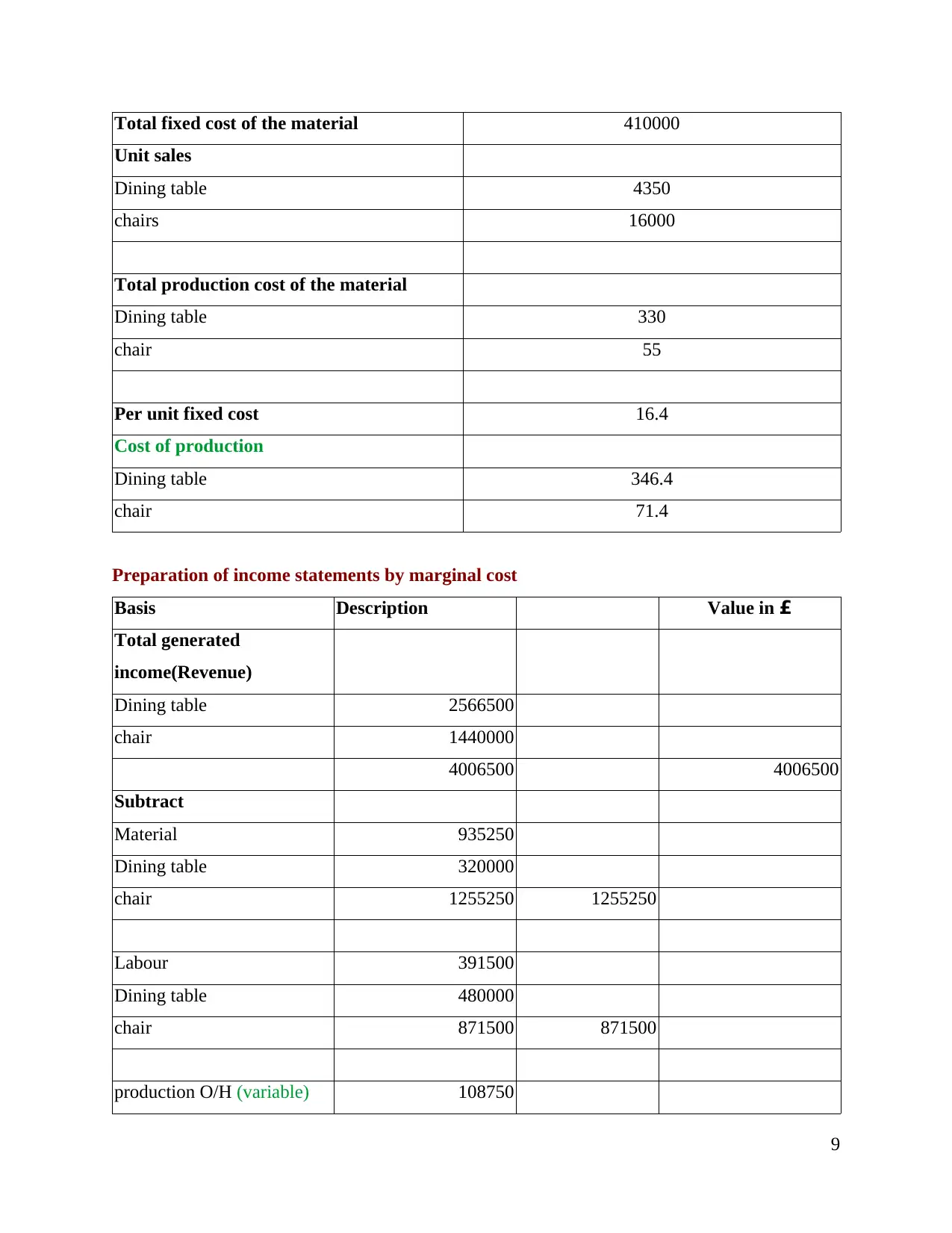

Total fixed cost of the material 410000

Unit sales

Dining table 4350

chairs 16000

Total production cost of the material

Dining table 330

chair 55

Per unit fixed cost 16.4

Cost of production

Dining table 346.4

chair 71.4

Preparation of income statements by marginal cost

Basis Description Value in £

Total generated

income(Revenue)

Dining table 2566500

chair 1440000

4006500 4006500

Subtract

Material 935250

Dining table 320000

chair 1255250 1255250

Labour 391500

Dining table 480000

chair 871500 871500

production O/H (variable) 108750

9

Unit sales

Dining table 4350

chairs 16000

Total production cost of the material

Dining table 330

chair 55

Per unit fixed cost 16.4

Cost of production

Dining table 346.4

chair 71.4

Preparation of income statements by marginal cost

Basis Description Value in £

Total generated

income(Revenue)

Dining table 2566500

chair 1440000

4006500 4006500

Subtract

Material 935250

Dining table 320000

chair 1255250 1255250

Labour 391500

Dining table 480000

chair 871500 871500

production O/H (variable) 108750

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

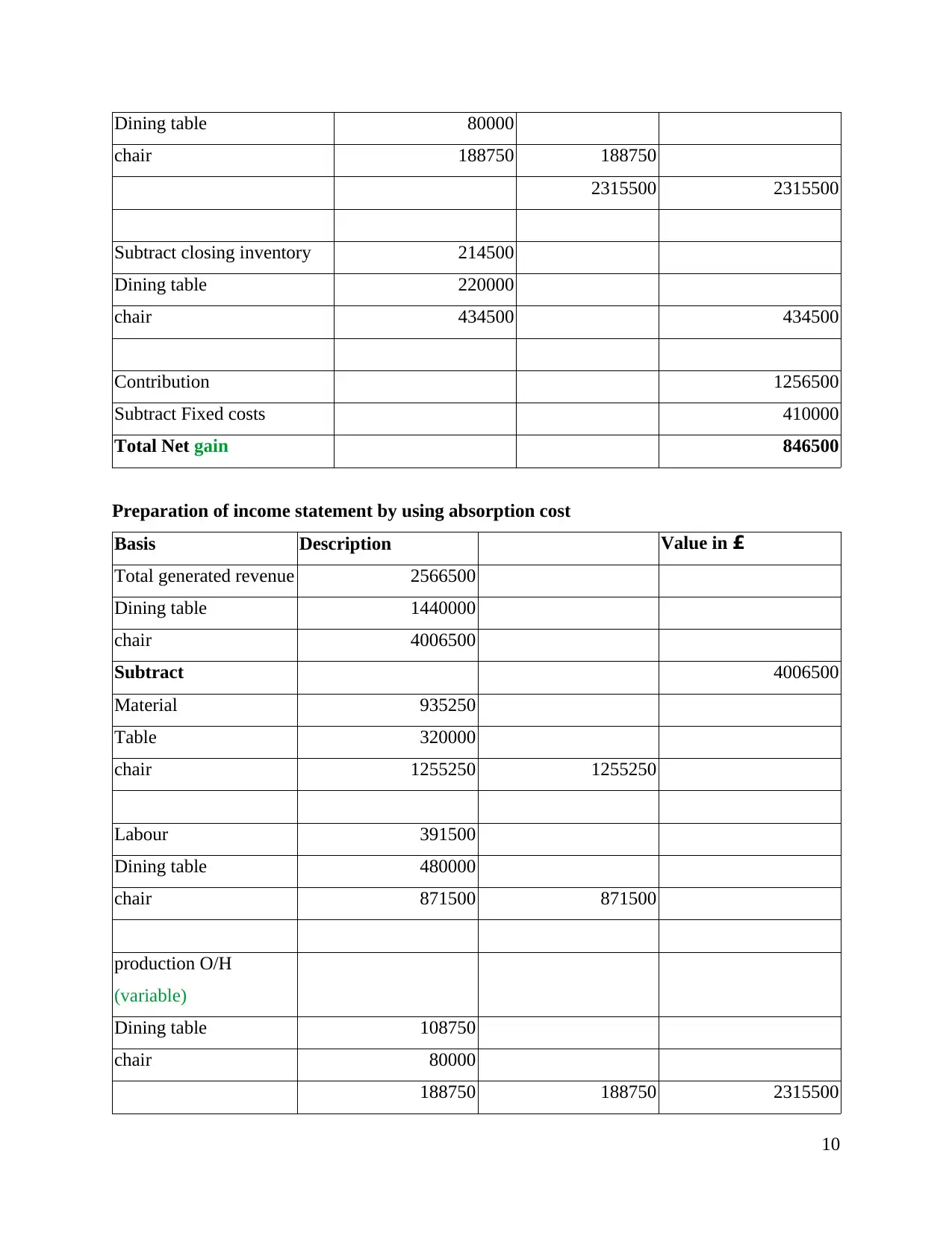

Dining table 80000

chair 188750 188750

2315500 2315500

Subtract closing inventory 214500

Dining table 220000

chair 434500 434500

Contribution 1256500

Subtract Fixed costs 410000

Total Net gain 846500

Preparation of income statement by using absorption cost

Basis Description Value in £

Total generated revenue 2566500

Dining table 1440000

chair 4006500

Subtract 4006500

Material 935250

Table 320000

chair 1255250 1255250

Labour 391500

Dining table 480000

chair 871500 871500

production O/H

(variable)

Dining table 108750

chair 80000

188750 188750 2315500

10

chair 188750 188750

2315500 2315500

Subtract closing inventory 214500

Dining table 220000

chair 434500 434500

Contribution 1256500

Subtract Fixed costs 410000

Total Net gain 846500

Preparation of income statement by using absorption cost

Basis Description Value in £

Total generated revenue 2566500

Dining table 1440000

chair 4006500

Subtract 4006500

Material 935250

Table 320000

chair 1255250 1255250

Labour 391500

Dining table 480000

chair 871500 871500

production O/H

(variable)

Dining table 108750

chair 80000

188750 188750 2315500

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

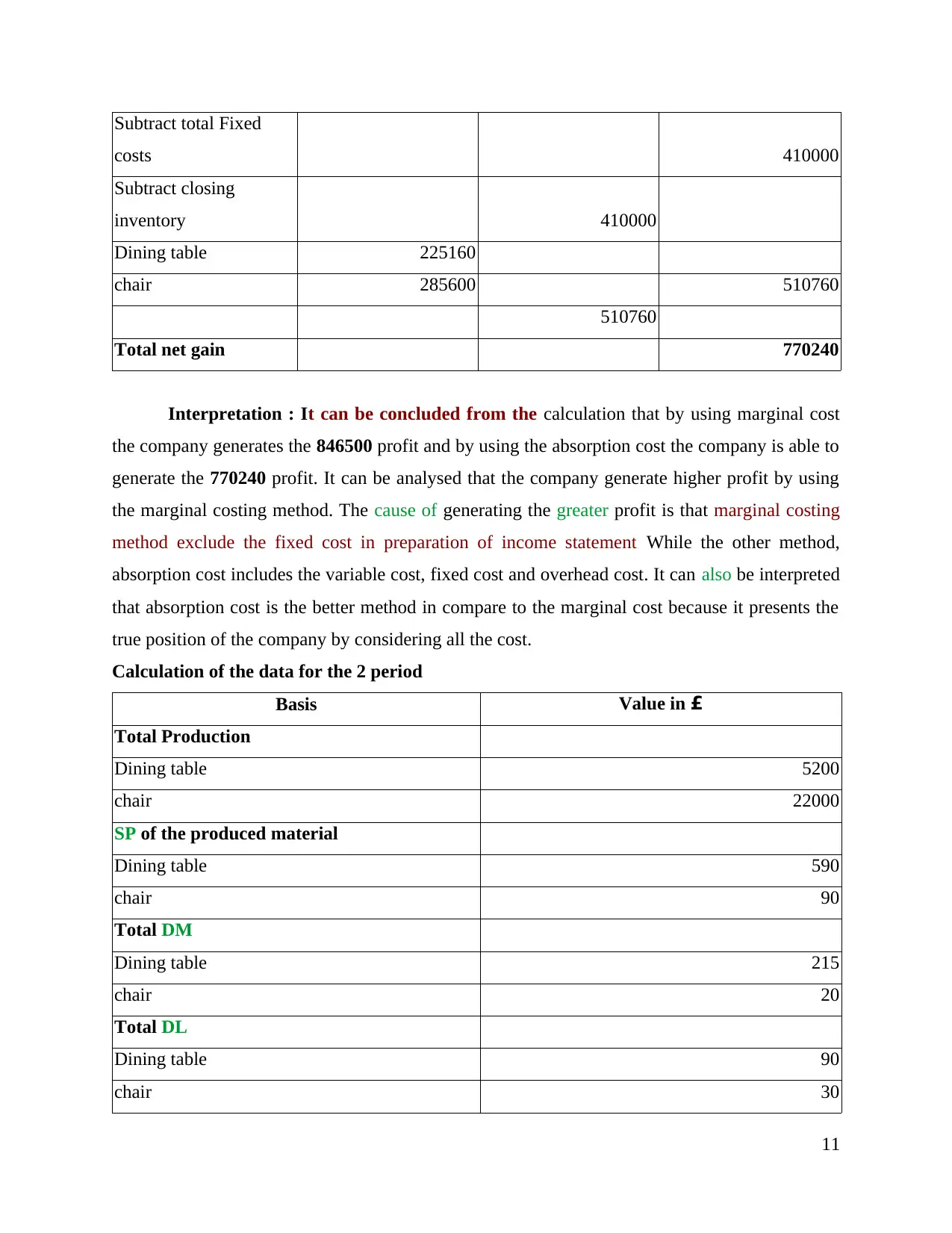

Subtract total Fixed

costs 410000

Subtract closing

inventory 410000

Dining table 225160

chair 285600 510760

510760

Total net gain 770240

Interpretation : It can be concluded from the calculation that by using marginal cost

the company generates the 846500 profit and by using the absorption cost the company is able to

generate the 770240 profit. It can be analysed that the company generate higher profit by using

the marginal costing method. The cause of generating the greater profit is that marginal costing

method exclude the fixed cost in preparation of income statement While the other method,

absorption cost includes the variable cost, fixed cost and overhead cost. It can also be interpreted

that absorption cost is the better method in compare to the marginal cost because it presents the

true position of the company by considering all the cost.

Calculation of the data for the 2 period

Basis Value in £

Total Production

Dining table 5200

chair 22000

SP of the produced material

Dining table 590

chair 90

Total DM

Dining table 215

chair 20

Total DL

Dining table 90

chair 30

11

costs 410000

Subtract closing

inventory 410000

Dining table 225160

chair 285600 510760

510760

Total net gain 770240

Interpretation : It can be concluded from the calculation that by using marginal cost

the company generates the 846500 profit and by using the absorption cost the company is able to

generate the 770240 profit. It can be analysed that the company generate higher profit by using

the marginal costing method. The cause of generating the greater profit is that marginal costing

method exclude the fixed cost in preparation of income statement While the other method,

absorption cost includes the variable cost, fixed cost and overhead cost. It can also be interpreted

that absorption cost is the better method in compare to the marginal cost because it presents the

true position of the company by considering all the cost.

Calculation of the data for the 2 period

Basis Value in £

Total Production

Dining table 5200

chair 22000

SP of the produced material

Dining table 590

chair 90

Total DM

Dining table 215

chair 20

Total DL

Dining table 90

chair 30

11

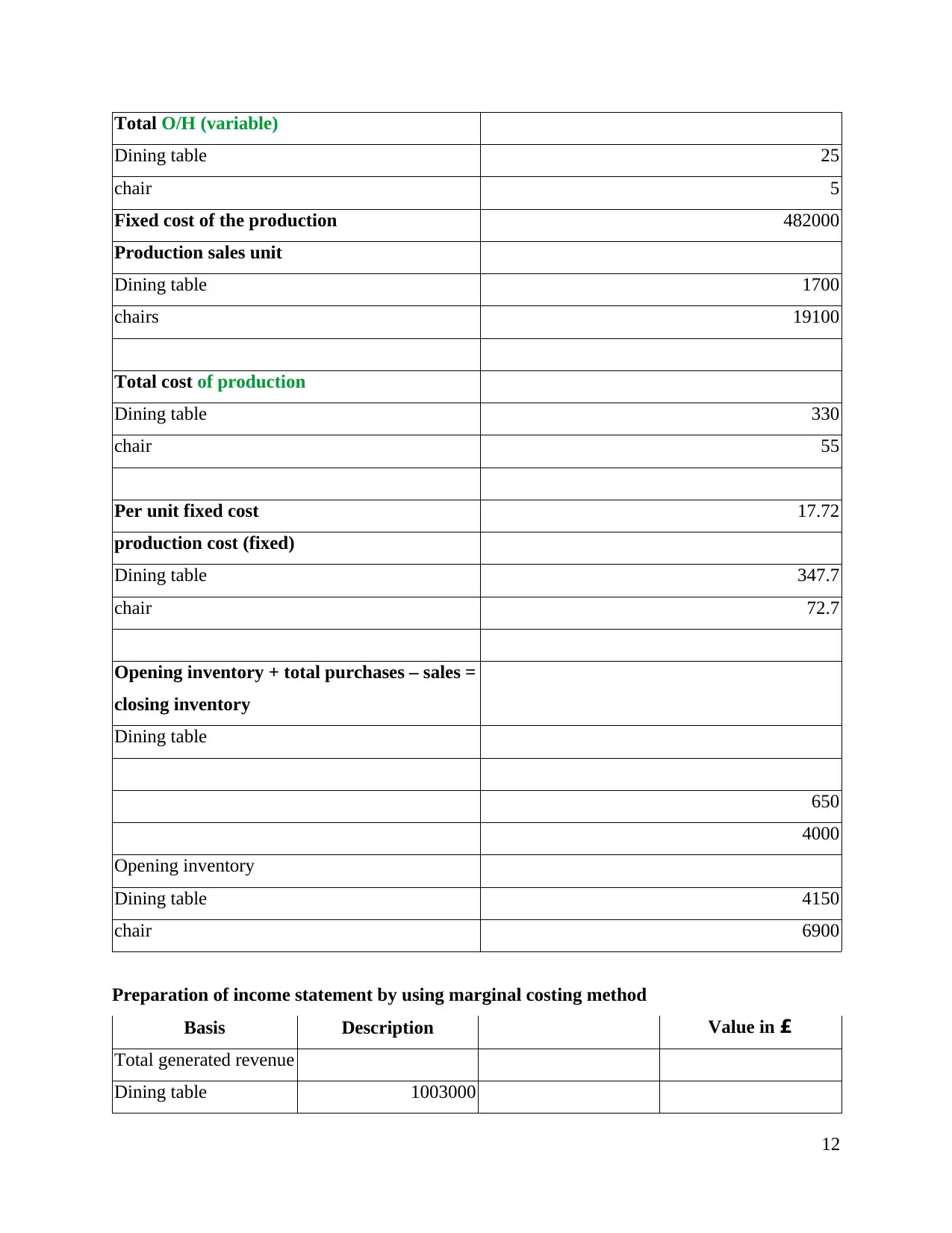

Total O/H (variable)

Dining table 25

chair 5

Fixed cost of the production 482000

Production sales unit

Dining table 1700

chairs 19100

Total cost of production

Dining table 330

chair 55

Per unit fixed cost 17.72

production cost (fixed)

Dining table 347.7

chair 72.7

Opening inventory + total purchases – sales =

closing inventory

Dining table

650

4000

Opening inventory

Dining table 4150

chair 6900

Preparation of income statement by using marginal costing method

Basis Description Value in £

Total generated revenue

Dining table 1003000

12

Dining table 25

chair 5

Fixed cost of the production 482000

Production sales unit

Dining table 1700

chairs 19100

Total cost of production

Dining table 330

chair 55

Per unit fixed cost 17.72

production cost (fixed)

Dining table 347.7

chair 72.7

Opening inventory + total purchases – sales =

closing inventory

Dining table

650

4000

Opening inventory

Dining table 4150

chair 6900

Preparation of income statement by using marginal costing method

Basis Description Value in £

Total generated revenue

Dining table 1003000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.