Management Accounting Report: Aon Consulting and Grange Materials

VerifiedAdded on 2021/02/21

|20

|4974

|163

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its importance for effective business decision-making within the context of Aon Consulting and Grange Construction Materials. It defines management accounting and explores various systems like inventory management, cost accounting, price optimization, and job costing. The report details the integration of these systems, emphasizing their role in enhancing operational efficiency. It then delves into management accounting reporting, covering the presentation of financial information, report types (performance, budget, and accounts receivable), and cost assessment techniques such as cost-volume-profit analysis, flexible budgeting, and marginal and absorption costing. Additionally, the report discusses cost allocation and the application of normal, standard, and activity-based costing methods. The analysis includes advantages and disadvantages of planning tools and a comparison of business entities using management accounting systems to address financial challenges. Finally, it also highlights the differences between management accounting and financial accounting.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management Accounting and different systems of management accounting:............................3

Importance of Integration of management accounting system within an organisation:..............4

Management accounting reporting:.............................................................................................5

TASK 2............................................................................................................................................7

Assessment of costs though most considerable techniques for the purpose of income

statement:.....................................................................................................................................7

TASK 3..........................................................................................................................................12

Advantages and disadvantages of different types of planning tools used for budgetary control:

....................................................................................................................................................12

TASK 4..........................................................................................................................................15

Comparison of business entities applying management accounting systems for responding

different financial problems:.....................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management Accounting and different systems of management accounting:............................3

Importance of Integration of management accounting system within an organisation:..............4

Management accounting reporting:.............................................................................................5

TASK 2............................................................................................................................................7

Assessment of costs though most considerable techniques for the purpose of income

statement:.....................................................................................................................................7

TASK 3..........................................................................................................................................12

Advantages and disadvantages of different types of planning tools used for budgetary control:

....................................................................................................................................................12

TASK 4..........................................................................................................................................15

Comparison of business entities applying management accounting systems for responding

different financial problems:.....................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management's decision and steps decides the future path of a business organisation, for

effective decision-making management accounting is essential. It is a process through which

vital information’s are generated and obtained by managerial personnel’s for taking business and

trade decisions (Ayadi, 2017). For improve understanding of aspects of management accounting

Aon consulting group is selected which provides services of consultancy to its clients related to

hospitality, retail etc. The report's objective is to provide a systematic definition of management

accounting and prerequisite of management accounting systems, approaches of management

accounting reporting, applications of planning tools along with benefits and disadvantages in

context of client company Grange Construction Materials, UK's medium size construction

material manufacture. Company is manufacturer and suppliers of construction material. This

report also contains computation of costs with the help of techniques of costs analysis and

comparative analysis of organisation using management accounting systems for responding

problems.

TASK 1

Management Accounting and different systems of management accounting:

In business framework, management accounting is defined as combination of more than

one functions and activities which assist in developing a structure that gives detailed and

essential financial information for business decision-making. It is provide information that deals

with the source and the use of the funds needed for running any business, and other qualitative

details that are relevant for the same objective. There are one or more management accounting

systems that provide an evenness in organisation's different tasks to achieve organisation's aim

effectively. For this purpose, different management accounting systems like job costing, cost

accounting, price minimisation or optimisation system, inventory management system etc. are

discussed below:

Inventory management system: Inventory in a business enterprise directly affects its

gross and net profit as it act as a most considerable factors in computation of net income. Grange

Construction Materials being a manufacture a recycler of construction material, always tries to

maintain inventories costs to control and increase their profit margin. Company has different

processes for recycling and manufacturing of products thus it is required for company to track

Management's decision and steps decides the future path of a business organisation, for

effective decision-making management accounting is essential. It is a process through which

vital information’s are generated and obtained by managerial personnel’s for taking business and

trade decisions (Ayadi, 2017). For improve understanding of aspects of management accounting

Aon consulting group is selected which provides services of consultancy to its clients related to

hospitality, retail etc. The report's objective is to provide a systematic definition of management

accounting and prerequisite of management accounting systems, approaches of management

accounting reporting, applications of planning tools along with benefits and disadvantages in

context of client company Grange Construction Materials, UK's medium size construction

material manufacture. Company is manufacturer and suppliers of construction material. This

report also contains computation of costs with the help of techniques of costs analysis and

comparative analysis of organisation using management accounting systems for responding

problems.

TASK 1

Management Accounting and different systems of management accounting:

In business framework, management accounting is defined as combination of more than

one functions and activities which assist in developing a structure that gives detailed and

essential financial information for business decision-making. It is provide information that deals

with the source and the use of the funds needed for running any business, and other qualitative

details that are relevant for the same objective. There are one or more management accounting

systems that provide an evenness in organisation's different tasks to achieve organisation's aim

effectively. For this purpose, different management accounting systems like job costing, cost

accounting, price minimisation or optimisation system, inventory management system etc. are

discussed below:

Inventory management system: Inventory in a business enterprise directly affects its

gross and net profit as it act as a most considerable factors in computation of net income. Grange

Construction Materials being a manufacture a recycler of construction material, always tries to

maintain inventories costs to control and increase their profit margin. Company has different

processes for recycling and manufacturing of products thus it is required for company to track

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and ensure availability of raw material and other aggregates to provide continuity in

manufacturing processes (Stead and Stead, 2014).

Cost accounting system: Different expenditures are determining factors in assessment of

profit. Specially manufacturing concern such as Grange Construction Materials always tries to

reduce its expense per unit to achieve profitability situation. System of cost accounting mainly

used by entities to do a detailed cost analysis to ensure profitability by projecting expenses

related to different activities.

Price-optimisation System: System of price-optimisation develop and create a base of

maintaining product or services price which provide feasibility in accomplishing the strategy of

business entity. It includes functions related to analysis of relationship of demand and price of

services and products with an objective to set a price at certain level to achieve highest demand

(Warren, Reeve and Duchac, 2013). Grange Construction Materials adopts price-optimisation

system for minimising price of construction materials lower than its competitors to gain

competitive benefits.

Job costing system: Accounting and management of products and services which are

fully different by nature or in other factors, is difficult task but adoption of system of job costing

can provide smoothness in recording and managing task related to such products. In case of

manufacturing companies like Grange Construction Materials having different variety of

products this system is helpful. In respective company, accountants and managers classifies

products and units which are entirely different from all other product as specific tasks and jobs,

and then assign cost to such particular jobs.

Importance of Integration of management accounting system within an organisation:

A systematic integration of above described systems is required to achieve smoothness in

organisation's operations. These different systems boost the performance of company by

providing important information’s. For instance, cost accounting systems and inventory

management system help management in conducting different process within organisation like

inventory management, preparation of cost sheet, assessment of process cost etc. Such

integration can provide value addition in terms of operating efficiency and effectiveness.

Origin, role and principles of management accounting:

No universal theory about origin of management accounting although origin year of

word “Management Accounting” is 1960s. Management accounting is also deemed as cost

manufacturing processes (Stead and Stead, 2014).

Cost accounting system: Different expenditures are determining factors in assessment of

profit. Specially manufacturing concern such as Grange Construction Materials always tries to

reduce its expense per unit to achieve profitability situation. System of cost accounting mainly

used by entities to do a detailed cost analysis to ensure profitability by projecting expenses

related to different activities.

Price-optimisation System: System of price-optimisation develop and create a base of

maintaining product or services price which provide feasibility in accomplishing the strategy of

business entity. It includes functions related to analysis of relationship of demand and price of

services and products with an objective to set a price at certain level to achieve highest demand

(Warren, Reeve and Duchac, 2013). Grange Construction Materials adopts price-optimisation

system for minimising price of construction materials lower than its competitors to gain

competitive benefits.

Job costing system: Accounting and management of products and services which are

fully different by nature or in other factors, is difficult task but adoption of system of job costing

can provide smoothness in recording and managing task related to such products. In case of

manufacturing companies like Grange Construction Materials having different variety of

products this system is helpful. In respective company, accountants and managers classifies

products and units which are entirely different from all other product as specific tasks and jobs,

and then assign cost to such particular jobs.

Importance of Integration of management accounting system within an organisation:

A systematic integration of above described systems is required to achieve smoothness in

organisation's operations. These different systems boost the performance of company by

providing important information’s. For instance, cost accounting systems and inventory

management system help management in conducting different process within organisation like

inventory management, preparation of cost sheet, assessment of process cost etc. Such

integration can provide value addition in terms of operating efficiency and effectiveness.

Origin, role and principles of management accounting:

No universal theory about origin of management accounting although origin year of

word “Management Accounting” is 1960s. Management accounting is also deemed as cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

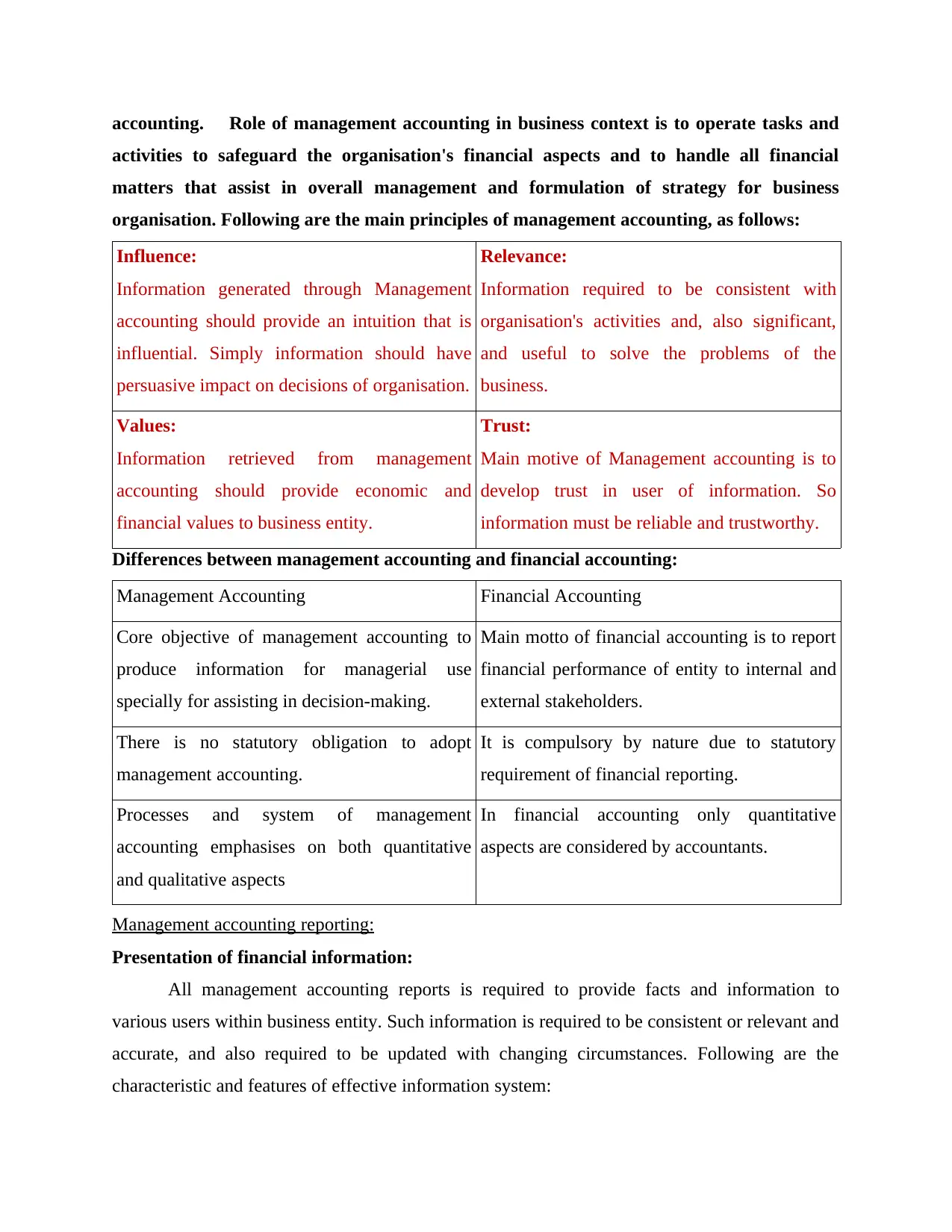

accounting. Role of management accounting in business context is to operate tasks and

activities to safeguard the organisation's financial aspects and to handle all financial

matters that assist in overall management and formulation of strategy for business

organisation. Following are the main principles of management accounting, as follows:

Influence:

Information generated through Management

accounting should provide an intuition that is

influential. Simply information should have

persuasive impact on decisions of organisation.

Relevance:

Information required to be consistent with

organisation's activities and, also significant,

and useful to solve the problems of the

business.

Values:

Information retrieved from management

accounting should provide economic and

financial values to business entity.

Trust:

Main motive of Management accounting is to

develop trust in user of information. So

information must be reliable and trustworthy.

Differences between management accounting and financial accounting:

Management Accounting Financial Accounting

Core objective of management accounting to

produce information for managerial use

specially for assisting in decision-making.

Main motto of financial accounting is to report

financial performance of entity to internal and

external stakeholders.

There is no statutory obligation to adopt

management accounting.

It is compulsory by nature due to statutory

requirement of financial reporting.

Processes and system of management

accounting emphasises on both quantitative

and qualitative aspects

In financial accounting only quantitative

aspects are considered by accountants.

Management accounting reporting:

Presentation of financial information:

All management accounting reports is required to provide facts and information to

various users within business entity. Such information is required to be consistent or relevant and

accurate, and also required to be updated with changing circumstances. Following are the

characteristic and features of effective information system:

activities to safeguard the organisation's financial aspects and to handle all financial

matters that assist in overall management and formulation of strategy for business

organisation. Following are the main principles of management accounting, as follows:

Influence:

Information generated through Management

accounting should provide an intuition that is

influential. Simply information should have

persuasive impact on decisions of organisation.

Relevance:

Information required to be consistent with

organisation's activities and, also significant,

and useful to solve the problems of the

business.

Values:

Information retrieved from management

accounting should provide economic and

financial values to business entity.

Trust:

Main motive of Management accounting is to

develop trust in user of information. So

information must be reliable and trustworthy.

Differences between management accounting and financial accounting:

Management Accounting Financial Accounting

Core objective of management accounting to

produce information for managerial use

specially for assisting in decision-making.

Main motto of financial accounting is to report

financial performance of entity to internal and

external stakeholders.

There is no statutory obligation to adopt

management accounting.

It is compulsory by nature due to statutory

requirement of financial reporting.

Processes and system of management

accounting emphasises on both quantitative

and qualitative aspects

In financial accounting only quantitative

aspects are considered by accountants.

Management accounting reporting:

Presentation of financial information:

All management accounting reports is required to provide facts and information to

various users within business entity. Such information is required to be consistent or relevant and

accurate, and also required to be updated with changing circumstances. Following are the

characteristic and features of effective information system:

It should provide reliable and trustworthy information to different users.

A good information system generates complete and useful information within reasonable

time period.

It emphasises on relevance of information for users.

Manner of presentation of information:

Presentation of information obtained through various systems of management accounting

should be understandable to all users, because such information also includes typical financial

data which is hard for managerial personnel’s to understand. So in order to provide an accurate

interpretation of information, it is necessary that information must be understandable. Also such

information must be in comparative form and comprehend to provide ease in decision-making

process.

Management accounting reports:

Reporting is set of activities which are dedicated to circulation of relevant information’s

form small managers to higher scale managers which are finally applied by them in decision-

making processes. Management accounting systems provides informations that is required to

report to top scale managers. Accountants, production heads, process heads and other employees

within Grange Construction Materials prepare reports like inventory report, budget report,

performance report, account receivable report etc. Following points provide explanation about

different report of management accounting:

Performance Report: An organisation's performance is directly linked with performance

of employees and workers, so assessment of performance of employees is significant to achieve

targeted performance (Wager, Lee and Glaser, 2017). Grange Construction Materials analyse the

performance and provide rewards or incentives to different department's employees to encourage

or promote them, utilise their full efficiency towards organisation's objectives. These reports also

act as a basis for formulation of policies with regards to employees to control and manage their

tasks.

Budget Report: These reports having importance for organisation as it provides

assistance in obtaining short and long term objectives. A simple budget report provides actual

and budgeted figures along with any differences whether unfavourable or favourable. In Grange

Construction Materials, manufacturing and production heads prepares budgets reports to assess

the overall efficiency of company with respect to different operations and functions.

A good information system generates complete and useful information within reasonable

time period.

It emphasises on relevance of information for users.

Manner of presentation of information:

Presentation of information obtained through various systems of management accounting

should be understandable to all users, because such information also includes typical financial

data which is hard for managerial personnel’s to understand. So in order to provide an accurate

interpretation of information, it is necessary that information must be understandable. Also such

information must be in comparative form and comprehend to provide ease in decision-making

process.

Management accounting reports:

Reporting is set of activities which are dedicated to circulation of relevant information’s

form small managers to higher scale managers which are finally applied by them in decision-

making processes. Management accounting systems provides informations that is required to

report to top scale managers. Accountants, production heads, process heads and other employees

within Grange Construction Materials prepare reports like inventory report, budget report,

performance report, account receivable report etc. Following points provide explanation about

different report of management accounting:

Performance Report: An organisation's performance is directly linked with performance

of employees and workers, so assessment of performance of employees is significant to achieve

targeted performance (Wager, Lee and Glaser, 2017). Grange Construction Materials analyse the

performance and provide rewards or incentives to different department's employees to encourage

or promote them, utilise their full efficiency towards organisation's objectives. These reports also

act as a basis for formulation of policies with regards to employees to control and manage their

tasks.

Budget Report: These reports having importance for organisation as it provides

assistance in obtaining short and long term objectives. A simple budget report provides actual

and budgeted figures along with any differences whether unfavourable or favourable. In Grange

Construction Materials, manufacturing and production heads prepares budgets reports to assess

the overall efficiency of company with respect to different operations and functions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivable report: These report provides details about ageing cycle of debtors,

collection from debtors, invoices, debit notes etc. This report explains about organisation's

efficiency to collect cash from debtors. In Grange Construction materials managers prepare this

report to evaluate whether company's debtors are able to pay short term debts and identification

of debtors who may be insolvent in near future.

TASK 2

Assessment of costs though most considerable techniques for the purpose of income statement:

Costs: It implies to monetary amount or consideration which is paid by business entities

to acquire something, produce something or to operate business activities and functions. Costs

are significant for determining organisation's profitability. Cost analysis is vital task in

organisational structure as it provides help in asses the actual performance of company. In

context of manufacturing concerns cost analysis includes critical analysis of costs and output

relationship. In cost analysis all types of cost and their effect on each produced unit is analysed

by accountants. In Grange Construction materials different costs like fixed, variable and semi

variables are analysed by cost accounts to assess the viability of processes of manufacturing.

Cost-volume profit: In Grange Construction materials, this analysis is applied by

managers , includes analysis and evaluation of relationship between production volume and costs

to determine effect on organisation's net profit.

Flexible Budgeting: It is also known as variable budget, In Grange Construction

materials it is also used by company as it provides flexibility in assess the performance and net

income at different level and units of production. It considers variations in net income at

different output level.

Cost Variances: This method is used by Grange Construction materials to recognise the

weak and dull areas of operation within company by evaluating the effect of differences and

variance in different operational areas.

Marginal Costing: Under marginal costing, marginal cost is used by management to

compute contribution and net income. Marginal costs include all direct and variable expenses

like direct expenses, direct material, variable overheads etc. In this approach only fixed expenses

are separately shown in income statements as period cost whether they are related to production

or not.

collection from debtors, invoices, debit notes etc. This report explains about organisation's

efficiency to collect cash from debtors. In Grange Construction materials managers prepare this

report to evaluate whether company's debtors are able to pay short term debts and identification

of debtors who may be insolvent in near future.

TASK 2

Assessment of costs though most considerable techniques for the purpose of income statement:

Costs: It implies to monetary amount or consideration which is paid by business entities

to acquire something, produce something or to operate business activities and functions. Costs

are significant for determining organisation's profitability. Cost analysis is vital task in

organisational structure as it provides help in asses the actual performance of company. In

context of manufacturing concerns cost analysis includes critical analysis of costs and output

relationship. In cost analysis all types of cost and their effect on each produced unit is analysed

by accountants. In Grange Construction materials different costs like fixed, variable and semi

variables are analysed by cost accounts to assess the viability of processes of manufacturing.

Cost-volume profit: In Grange Construction materials, this analysis is applied by

managers , includes analysis and evaluation of relationship between production volume and costs

to determine effect on organisation's net profit.

Flexible Budgeting: It is also known as variable budget, In Grange Construction

materials it is also used by company as it provides flexibility in assess the performance and net

income at different level and units of production. It considers variations in net income at

different output level.

Cost Variances: This method is used by Grange Construction materials to recognise the

weak and dull areas of operation within company by evaluating the effect of differences and

variance in different operational areas.

Marginal Costing: Under marginal costing, marginal cost is used by management to

compute contribution and net income. Marginal costs include all direct and variable expenses

like direct expenses, direct material, variable overheads etc. In this approach only fixed expenses

are separately shown in income statements as period cost whether they are related to production

or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption Costing: In this costing method, all production and manufacturing expenses

and cost (including fixed) are considered as absorption cost. This approach does not classifies

expenses in variable and fixed. These method provides more accurate results about cost per unit

(Capelo, Lopes and Mata, 2015).

Cost allocation: It refers to collection of activities related to gathering, recognising and

allocating expenses and costs to each unit of production. In this context following are different

kind of costs incurred by Grange Construction materials, as follows:

Fixed Costs: These are period cost which remain same with change in production or

output units.

Variable Costs: These are costs that are highly influenced by change in production or

output units.

Semi - Variable costs: These costs are fixed to an extent and also consist of variable

nature. These costs are combination of fixed and variable costs.

Assigning these above costs while considering their effects on each unit provide an

accurate results about organisation's performance.

Normal Costing: It is a simple and traditional approach of costing which is used by

Grange Construction materials to calculate per unit cost of production and setting price. In this

method simply actual material, labour and other overheads costs are considered while setting

price and cost per unit.

Standard Costing: In this method, Grange Construction materials set standard figures

and values than actual performance of company is evaluated by making a systematic comparison

and to fix cost of product based on comparison.

Activity-Based Costing: Under this method accountants of Grange Construction

materials recognise key activities than assign different cost to recognised activities for better

accountability and setting price of products.

Inventory Costs: It includes all expenses which are directly associated with storage,

handling management, organising and procurement of stocks and inventories. In Grange

Construction materials major inventory costs are carrying and handling costs, warehouse costs,

logistic costs etc.

Benefits of reducing inventory costs to an organisation: An increase and decrease in

inventory costs leads to reduction and enhancement in amount of gross and net profit. In Grange

and cost (including fixed) are considered as absorption cost. This approach does not classifies

expenses in variable and fixed. These method provides more accurate results about cost per unit

(Capelo, Lopes and Mata, 2015).

Cost allocation: It refers to collection of activities related to gathering, recognising and

allocating expenses and costs to each unit of production. In this context following are different

kind of costs incurred by Grange Construction materials, as follows:

Fixed Costs: These are period cost which remain same with change in production or

output units.

Variable Costs: These are costs that are highly influenced by change in production or

output units.

Semi - Variable costs: These costs are fixed to an extent and also consist of variable

nature. These costs are combination of fixed and variable costs.

Assigning these above costs while considering their effects on each unit provide an

accurate results about organisation's performance.

Normal Costing: It is a simple and traditional approach of costing which is used by

Grange Construction materials to calculate per unit cost of production and setting price. In this

method simply actual material, labour and other overheads costs are considered while setting

price and cost per unit.

Standard Costing: In this method, Grange Construction materials set standard figures

and values than actual performance of company is evaluated by making a systematic comparison

and to fix cost of product based on comparison.

Activity-Based Costing: Under this method accountants of Grange Construction

materials recognise key activities than assign different cost to recognised activities for better

accountability and setting price of products.

Inventory Costs: It includes all expenses which are directly associated with storage,

handling management, organising and procurement of stocks and inventories. In Grange

Construction materials major inventory costs are carrying and handling costs, warehouse costs,

logistic costs etc.

Benefits of reducing inventory costs to an organisation: An increase and decrease in

inventory costs leads to reduction and enhancement in amount of gross and net profit. In Grange

Construction materials inventory and process heads tries to minimise their cost of inventories to

maximise their net income and profit margin. It is advantageous for company to reduce inventory

cost to increase profitability.

Valuation methods: There are two significant methods which assist in management of

inventory effectively: LIFO and FIFO. Under LIFO method approach of inventory management

inventories are arranged on the assumption that latest purchased inventories is sold at first place.

This is widely accepted approach of inventory recording. Where as in FIFO approach inventories

are arranged on the theory that inventories bought at first place in sequence is sold on priority.

Cost Variance: It simply implies to difference and variations between standard/budgeted

figures and actual amount of costs. Cost variances are used by Grange Construction materials to

recognise the operational weaknesses and areas of threats to enhance its operational

effectiveness.

Overheads Costs: It refers to all kind of day to day expenses excluding manufacturing

and production expenses which are required to produce product in Grange Construction

materials. These expenses may be classified as fixed, variable and semi variable.

Following is income statements of Galway Plc prepared by applying both marginal and

absorption costing methods separately, as follows:

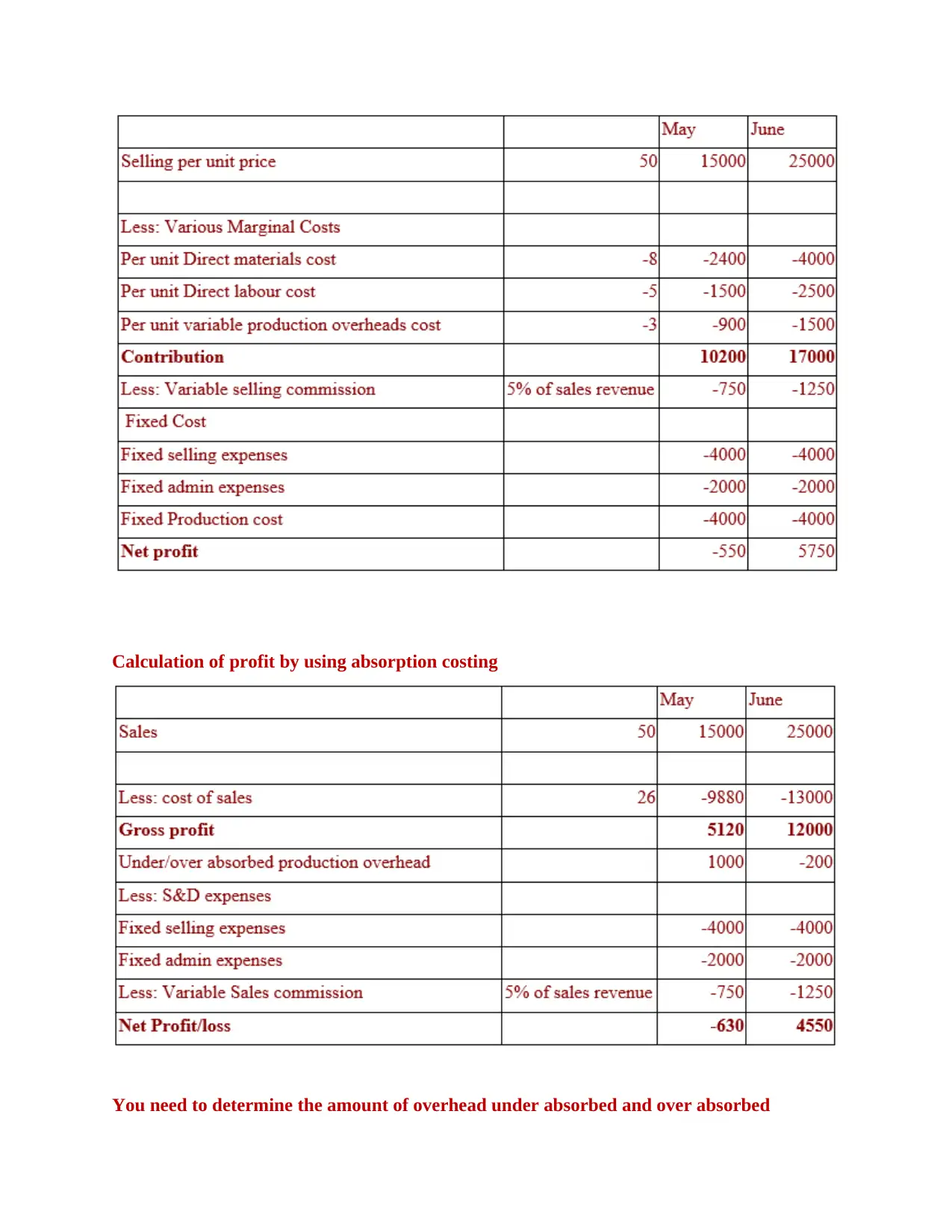

Calculation of profit using marginal costing

maximise their net income and profit margin. It is advantageous for company to reduce inventory

cost to increase profitability.

Valuation methods: There are two significant methods which assist in management of

inventory effectively: LIFO and FIFO. Under LIFO method approach of inventory management

inventories are arranged on the assumption that latest purchased inventories is sold at first place.

This is widely accepted approach of inventory recording. Where as in FIFO approach inventories

are arranged on the theory that inventories bought at first place in sequence is sold on priority.

Cost Variance: It simply implies to difference and variations between standard/budgeted

figures and actual amount of costs. Cost variances are used by Grange Construction materials to

recognise the operational weaknesses and areas of threats to enhance its operational

effectiveness.

Overheads Costs: It refers to all kind of day to day expenses excluding manufacturing

and production expenses which are required to produce product in Grange Construction

materials. These expenses may be classified as fixed, variable and semi variable.

Following is income statements of Galway Plc prepared by applying both marginal and

absorption costing methods separately, as follows:

Calculation of profit using marginal costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of profit by using absorption costing

You need to determine the amount of overhead under absorbed and over absorbed

You need to determine the amount of overhead under absorbed and over absorbed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

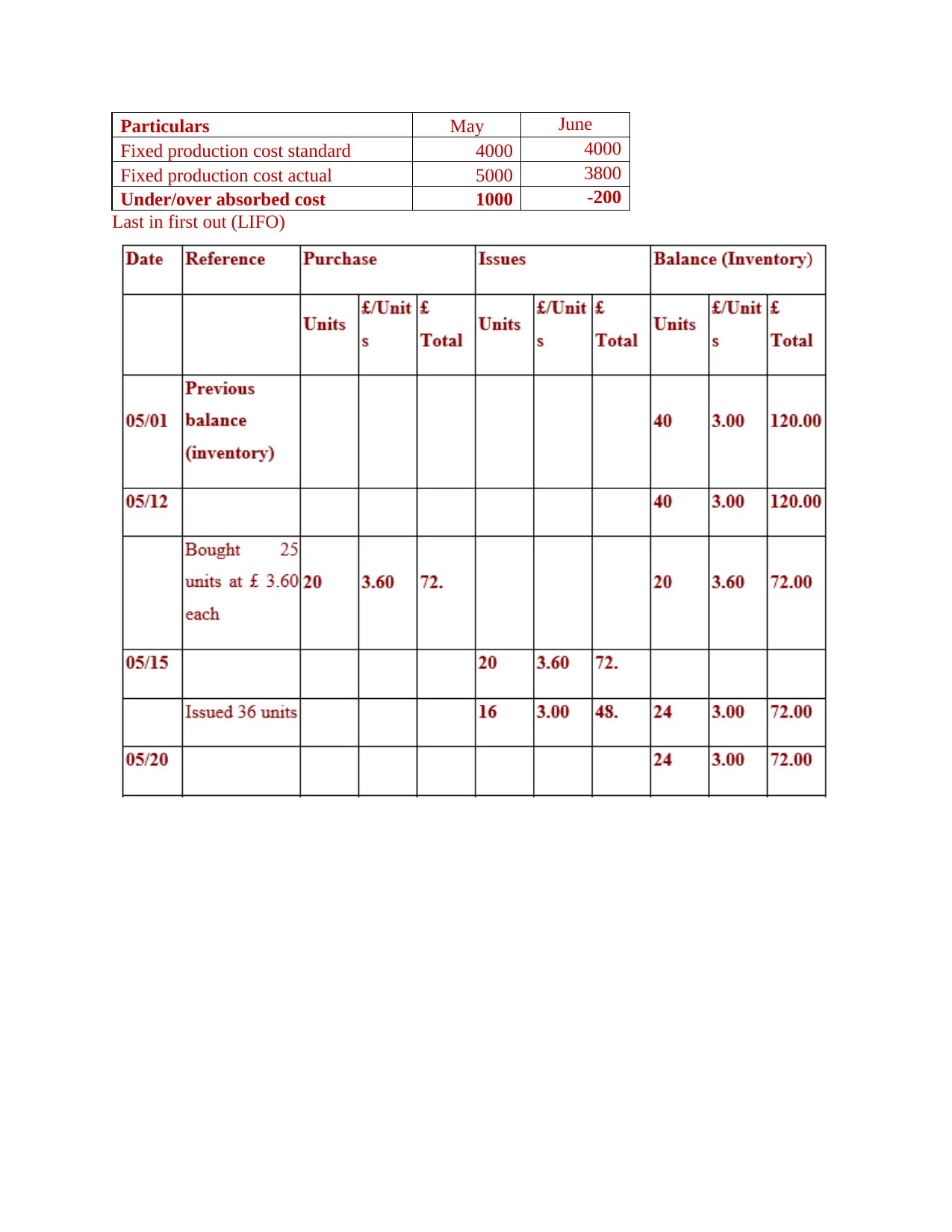

Particulars May June

Fixed production cost standard 4000 4000

Fixed production cost actual 5000 3800

Under/over absorbed cost 1000 -200

Last in first out (LIFO)

Fixed production cost standard 4000 4000

Fixed production cost actual 5000 3800

Under/over absorbed cost 1000 -200

Last in first out (LIFO)

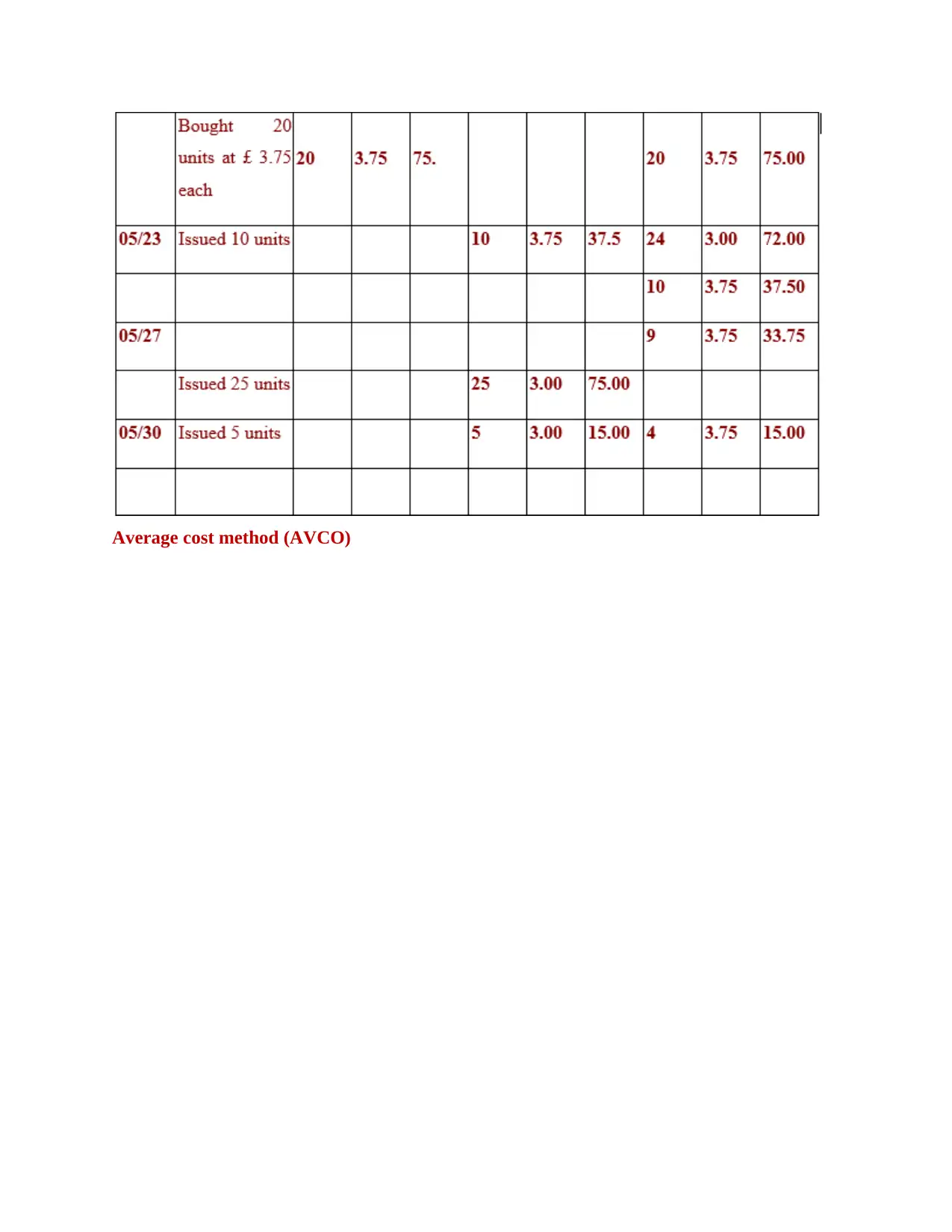

Average cost method (AVCO)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.