Comprehensive Management Accounting Report: Unit 5, Analysis

VerifiedAdded on 2020/11/23

|23

|7136

|258

Report

AI Summary

This report delves into the intricacies of management accounting, focusing on its essential requirements and various reporting methods. It explores cost analysis techniques, including marginal and absorption costing, to prepare income statements. The report evaluates the advantages and disadvantages of different planning tools used for budgetary control and assesses how organizations, such as The Berkeley Partnership, are adopting management accounting systems to address financial challenges and achieve sustainable success. It examines the integration of management accounting systems and reporting within organizational processes, highlighting the benefits of inventory management, job costing, and price optimization systems. The analysis includes a comparison of financial and management accounting, and the report concludes by evaluating how planning tools contribute to solving financial problems and driving organizational success.

UNIT 5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................5

P1. Explanation on management accounting and its essential requirement for different types

of management accounting system.........................................................................................5

P2. Explaining different methods of management accounting reporting...............................7

M1. Evaluating benefits of management accounting systems and its application within an

organisational context.............................................................................................................8

D1. Critically evaluating how management accounting system and management accounting

reporting is integrated within organisational process.............................................................9

LO 2...............................................................................................................................................10

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

..............................................................................................................................................10

Statement using Marginal and absorption costs...................................................................10

M2. Applying a range of management accounting techniques and producing appropriate

financial................................................................................................................................13

reporting documents.............................................................................................................13

D2. Producing financial reports that accurately apply and interpret data for a range of business

..............................................................................................................................................13

activities................................................................................................................................13

LO 3...............................................................................................................................................14

P4. Advantages & disadvantages of different types of planning tools used for budgetary

control...................................................................................................................................14

M3. Different planning tools and their implications for preparing and forecasting budgets.18

D3. Evaluating how planning tool for accounting respond to solve financial problems to lead

..............................................................................................................................................18

organisational sustainable success........................................................................................18

LO 4...............................................................................................................................................19

P5. Comparing how organisations are adopting management accounting systems for

responding financial problems.............................................................................................19

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................5

P1. Explanation on management accounting and its essential requirement for different types

of management accounting system.........................................................................................5

P2. Explaining different methods of management accounting reporting...............................7

M1. Evaluating benefits of management accounting systems and its application within an

organisational context.............................................................................................................8

D1. Critically evaluating how management accounting system and management accounting

reporting is integrated within organisational process.............................................................9

LO 2...............................................................................................................................................10

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

..............................................................................................................................................10

Statement using Marginal and absorption costs...................................................................10

M2. Applying a range of management accounting techniques and producing appropriate

financial................................................................................................................................13

reporting documents.............................................................................................................13

D2. Producing financial reports that accurately apply and interpret data for a range of business

..............................................................................................................................................13

activities................................................................................................................................13

LO 3...............................................................................................................................................14

P4. Advantages & disadvantages of different types of planning tools used for budgetary

control...................................................................................................................................14

M3. Different planning tools and their implications for preparing and forecasting budgets.18

D3. Evaluating how planning tool for accounting respond to solve financial problems to lead

..............................................................................................................................................18

organisational sustainable success........................................................................................18

LO 4...............................................................................................................................................19

P5. Comparing how organisations are adopting management accounting systems for

responding financial problems.............................................................................................19

M4. Analysing how management accounting helps in responding to financial problems

leading organisation to sustainable success..........................................................................21

REFERENCES..............................................................................................................................24

leading organisation to sustainable success..........................................................................21

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process which used by managers in order to find the

provision which relates to accounting information so that effective decision will get develop for

better organisational operations. This is an accounting process which also include non-financial

information which helps in identifying the key performance indicators for various parts of

businesses. For this report selected medium size financial consultancy organisation is The

Berkeley Partnership which deals in providing the best commercial services. In this report,

explanation will be provided on managerial accounting and its essential requirement with

different methods of management accounting reporting. Further, calculation will be provided by

using appropriate cost analysis technique. Moreover, advantages and disadvantages of different

types of planning tools which used in budgetary control will also be discussed in this report with

the ways by which entity will use management accounting in for solving financial problems.

LO 1

P1. Explanation on management accounting and its essential requirement for different types of

management accounting system

Management accounting is the process of analysing costs which relates to businesses and

operations in order to prepare internal financial report, records and account so that managers of

the organisation will able to develop decision for achieving business objectives and goals. In

other words it is the process of analysing data which relates to financial and costing so that it can

be translated into useful information (Kaplan and Atkinson, 2015). Generally this is the process

which look into the events and transaction which happens in and around the business. These are

the type of accounting records which are often used for internal purpose and are confidential too.

Calculation of such accounting will only be based on the managerial need only. Therefore, it can

be said that management accounting considered as profession which plays role in decision

making process of the management, devise proper planning and performance management

system and will also provide expertise financial reporting and control in order to develop

effective organisation strategy. It is the process which provides effective way for communicating

the plans of management which is through upward, downward and outward process. However,

Management accounting is the process which used by managers in order to find the

provision which relates to accounting information so that effective decision will get develop for

better organisational operations. This is an accounting process which also include non-financial

information which helps in identifying the key performance indicators for various parts of

businesses. For this report selected medium size financial consultancy organisation is The

Berkeley Partnership which deals in providing the best commercial services. In this report,

explanation will be provided on managerial accounting and its essential requirement with

different methods of management accounting reporting. Further, calculation will be provided by

using appropriate cost analysis technique. Moreover, advantages and disadvantages of different

types of planning tools which used in budgetary control will also be discussed in this report with

the ways by which entity will use management accounting in for solving financial problems.

LO 1

P1. Explanation on management accounting and its essential requirement for different types of

management accounting system

Management accounting is the process of analysing costs which relates to businesses and

operations in order to prepare internal financial report, records and account so that managers of

the organisation will able to develop decision for achieving business objectives and goals. In

other words it is the process of analysing data which relates to financial and costing so that it can

be translated into useful information (Kaplan and Atkinson, 2015). Generally this is the process

which look into the events and transaction which happens in and around the business. These are

the type of accounting records which are often used for internal purpose and are confidential too.

Calculation of such accounting will only be based on the managerial need only. Therefore, it can

be said that management accounting considered as profession which plays role in decision

making process of the management, devise proper planning and performance management

system and will also provide expertise financial reporting and control in order to develop

effective organisation strategy. It is the process which provides effective way for communicating

the plans of management which is through upward, downward and outward process. However,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

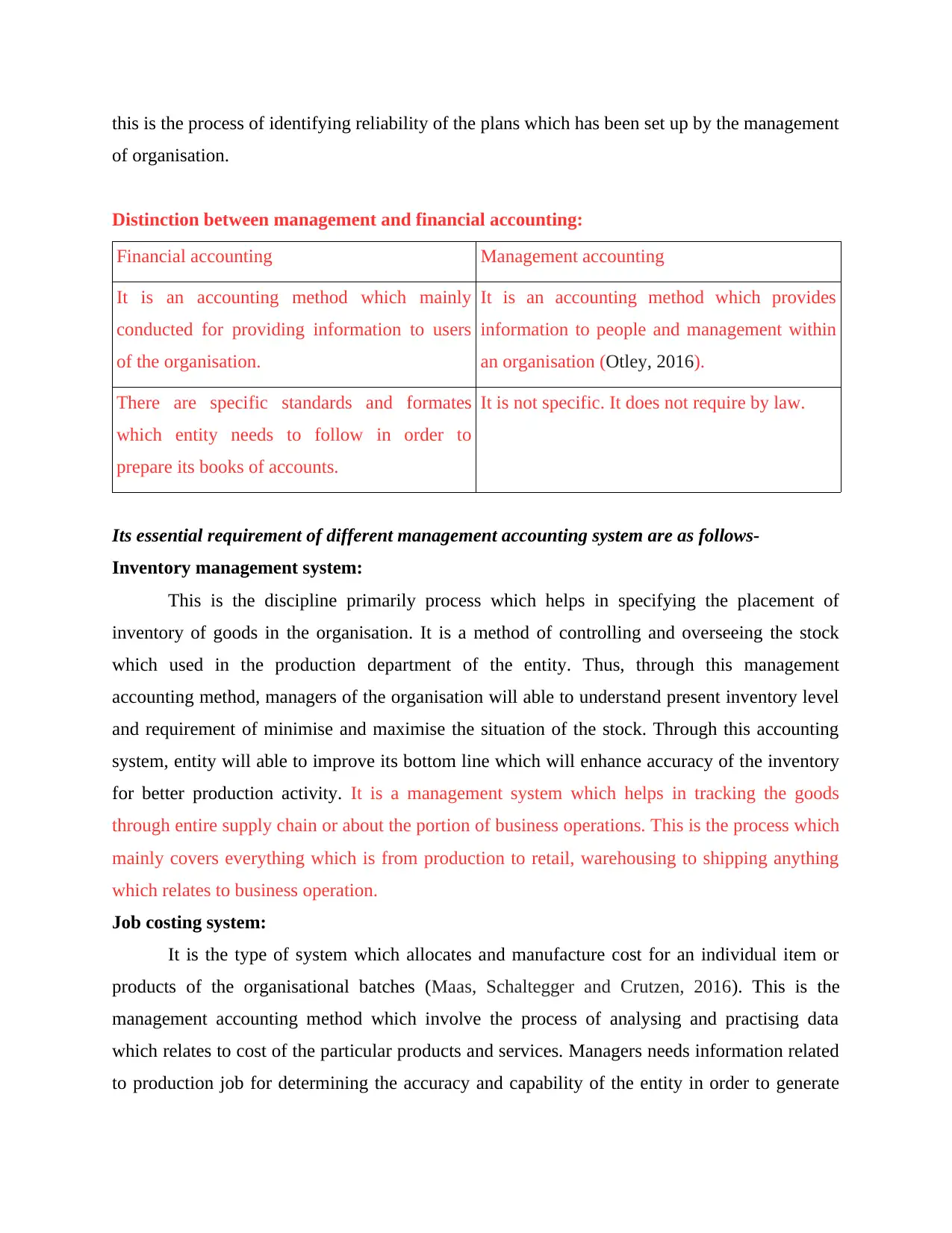

this is the process of identifying reliability of the plans which has been set up by the management

of organisation.

Distinction between management and financial accounting:

Financial accounting Management accounting

It is an accounting method which mainly

conducted for providing information to users

of the organisation.

It is an accounting method which provides

information to people and management within

an organisation (Otley, 2016).

There are specific standards and formates

which entity needs to follow in order to

prepare its books of accounts.

It is not specific. It does not require by law.

Its essential requirement of different management accounting system are as follows-

Inventory management system:

This is the discipline primarily process which helps in specifying the placement of

inventory of goods in the organisation. It is a method of controlling and overseeing the stock

which used in the production department of the entity. Thus, through this management

accounting method, managers of the organisation will able to understand present inventory level

and requirement of minimise and maximise the situation of the stock. Through this accounting

system, entity will able to improve its bottom line which will enhance accuracy of the inventory

for better production activity. It is a management system which helps in tracking the goods

through entire supply chain or about the portion of business operations. This is the process which

mainly covers everything which is from production to retail, warehousing to shipping anything

which relates to business operation.

Job costing system:

It is the type of system which allocates and manufacture cost for an individual item or

products of the organisational batches (Maas, Schaltegger and Crutzen, 2016). This is the

management accounting method which involve the process of analysing and practising data

which relates to cost of the particular products and services. Managers needs information related

to production job for determining the accuracy and capability of the entity in order to generate

of organisation.

Distinction between management and financial accounting:

Financial accounting Management accounting

It is an accounting method which mainly

conducted for providing information to users

of the organisation.

It is an accounting method which provides

information to people and management within

an organisation (Otley, 2016).

There are specific standards and formates

which entity needs to follow in order to

prepare its books of accounts.

It is not specific. It does not require by law.

Its essential requirement of different management accounting system are as follows-

Inventory management system:

This is the discipline primarily process which helps in specifying the placement of

inventory of goods in the organisation. It is a method of controlling and overseeing the stock

which used in the production department of the entity. Thus, through this management

accounting method, managers of the organisation will able to understand present inventory level

and requirement of minimise and maximise the situation of the stock. Through this accounting

system, entity will able to improve its bottom line which will enhance accuracy of the inventory

for better production activity. It is a management system which helps in tracking the goods

through entire supply chain or about the portion of business operations. This is the process which

mainly covers everything which is from production to retail, warehousing to shipping anything

which relates to business operation.

Job costing system:

It is the type of system which allocates and manufacture cost for an individual item or

products of the organisational batches (Maas, Schaltegger and Crutzen, 2016). This is the

management accounting method which involve the process of analysing and practising data

which relates to cost of the particular products and services. Managers needs information related

to production job for determining the accuracy and capability of the entity in order to generate

efficient income. This is the accounting system which used by organisation in order accumulate

information which associate with the cost about specific production or regarding the service job.

Mainly such information gets used by organisation in order to provide information to customer to

whom entity is under the agreement of cost.

Price optimization systems:

This is the process which involve mathematical analysis in determining the reaction of

consumers regarding the prices of goods and services which offered to consumers through

different types of channels. It also helps in determining the price which will be best of the entity

for earning its growth and maximise the operating profit.

This is the process by which management analyse internal areas which needs to improve

for earning better profitability. With its analysis managers of organisation creates budget so that

proper control will get develop on expenses of the entity. By analysing break-even-point,

managers will able to maintain profitability of the businesses (Cooper, Ezzamel and Qu, 2017).

This process used by organisation in order to analyse the willingness of customer in order to pay

for goods and services. It is the type of mathematical program which mainly helps in calculating

the demand which varies at different level of price.

Thus, these are the essential requirement of management accounting by which managers

of the Berkeley Partnership will able to develop effective strategies which will help in achieving

organisational objectives and to in meeting future goals with appropriate and sound business

operations. Through this costing techniques entity and users of organisation gets the information

which is relevant, reliable and also accurate by which they may able to develop economic

decision regarding investment in the capital of company.

P2. Explaining different methods of management accounting reporting

Management accounting generally focuses on generating internal information. This is an

accounting method which applied in the process of controlling, planning and in decision-making.

This mainly depend on the financial statements which generally consist of balance sheet, income

statements and cash flow statement. However, management accounting also applies in other

forms of accounting reports which are as follows-

Cost reports-

In this report of accounting management accounting helps in calculating costs which of

the items which relates to manufacturing (Accounting reports, 2018). This process generally

information which associate with the cost about specific production or regarding the service job.

Mainly such information gets used by organisation in order to provide information to customer to

whom entity is under the agreement of cost.

Price optimization systems:

This is the process which involve mathematical analysis in determining the reaction of

consumers regarding the prices of goods and services which offered to consumers through

different types of channels. It also helps in determining the price which will be best of the entity

for earning its growth and maximise the operating profit.

This is the process by which management analyse internal areas which needs to improve

for earning better profitability. With its analysis managers of organisation creates budget so that

proper control will get develop on expenses of the entity. By analysing break-even-point,

managers will able to maintain profitability of the businesses (Cooper, Ezzamel and Qu, 2017).

This process used by organisation in order to analyse the willingness of customer in order to pay

for goods and services. It is the type of mathematical program which mainly helps in calculating

the demand which varies at different level of price.

Thus, these are the essential requirement of management accounting by which managers

of the Berkeley Partnership will able to develop effective strategies which will help in achieving

organisational objectives and to in meeting future goals with appropriate and sound business

operations. Through this costing techniques entity and users of organisation gets the information

which is relevant, reliable and also accurate by which they may able to develop economic

decision regarding investment in the capital of company.

P2. Explaining different methods of management accounting reporting

Management accounting generally focuses on generating internal information. This is an

accounting method which applied in the process of controlling, planning and in decision-making.

This mainly depend on the financial statements which generally consist of balance sheet, income

statements and cash flow statement. However, management accounting also applies in other

forms of accounting reports which are as follows-

Cost reports-

In this report of accounting management accounting helps in calculating costs which of

the items which relates to manufacturing (Accounting reports, 2018). This process generally

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

done by analysing raw product overhead, costs, labour and any other costs which take into

consideration in business operations. Sum of all these cost further divided into amount which has

been charged on goods purchased. Through this way all the data will get summarised into cost

report. Through this report of management accounting, management of organisation will able to

view the value of product cost in comparison to its selling price so that proper measures will get

developed on control of expenses and also on profit margin.

Budgets-

This is the term which is considered as one of the key element while preparing

management accounting statements. In this process of accounting, budget will get established by

comparing it with previous year and to adjust it with future forecasts. In this statement

management will list down all the expenses and sources of revenue (Quattrone, 2016). Further,

with this report entity will conduct its business operation in order to analyse money has been

incurred during the process of production and money which has been saved.

Performance reports-

This is the another method of management accounting reporting in which management

apply in order to compare actual revenue with the expenditure which is also to the set budgeted

amount. The difference amount which computed with comparison will further evaluate in next

process of creating budget. This is a management accounting report through which managers of

the entity will able to create efficient planning for increasing products demand in future with the

increase in cost.

Account receivable aging report-

This is the another type of management accounting report which mainly concerned with

managing account receivable for the types of entities who engaged in extending credit of the

consumers. This is the process where proper segregation has been with customer balance of

invoices in order to find out the problem which has been associate with entity's collection

process (Chenhall and Moers, 2015). This helps management of entity by reducing bad debt and

by maintaining its liquidity.

consideration in business operations. Sum of all these cost further divided into amount which has

been charged on goods purchased. Through this way all the data will get summarised into cost

report. Through this report of management accounting, management of organisation will able to

view the value of product cost in comparison to its selling price so that proper measures will get

developed on control of expenses and also on profit margin.

Budgets-

This is the term which is considered as one of the key element while preparing

management accounting statements. In this process of accounting, budget will get established by

comparing it with previous year and to adjust it with future forecasts. In this statement

management will list down all the expenses and sources of revenue (Quattrone, 2016). Further,

with this report entity will conduct its business operation in order to analyse money has been

incurred during the process of production and money which has been saved.

Performance reports-

This is the another method of management accounting reporting in which management

apply in order to compare actual revenue with the expenditure which is also to the set budgeted

amount. The difference amount which computed with comparison will further evaluate in next

process of creating budget. This is a management accounting report through which managers of

the entity will able to create efficient planning for increasing products demand in future with the

increase in cost.

Account receivable aging report-

This is the another type of management accounting report which mainly concerned with

managing account receivable for the types of entities who engaged in extending credit of the

consumers. This is the process where proper segregation has been with customer balance of

invoices in order to find out the problem which has been associate with entity's collection

process (Chenhall and Moers, 2015). This helps management of entity by reducing bad debt and

by maintaining its liquidity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

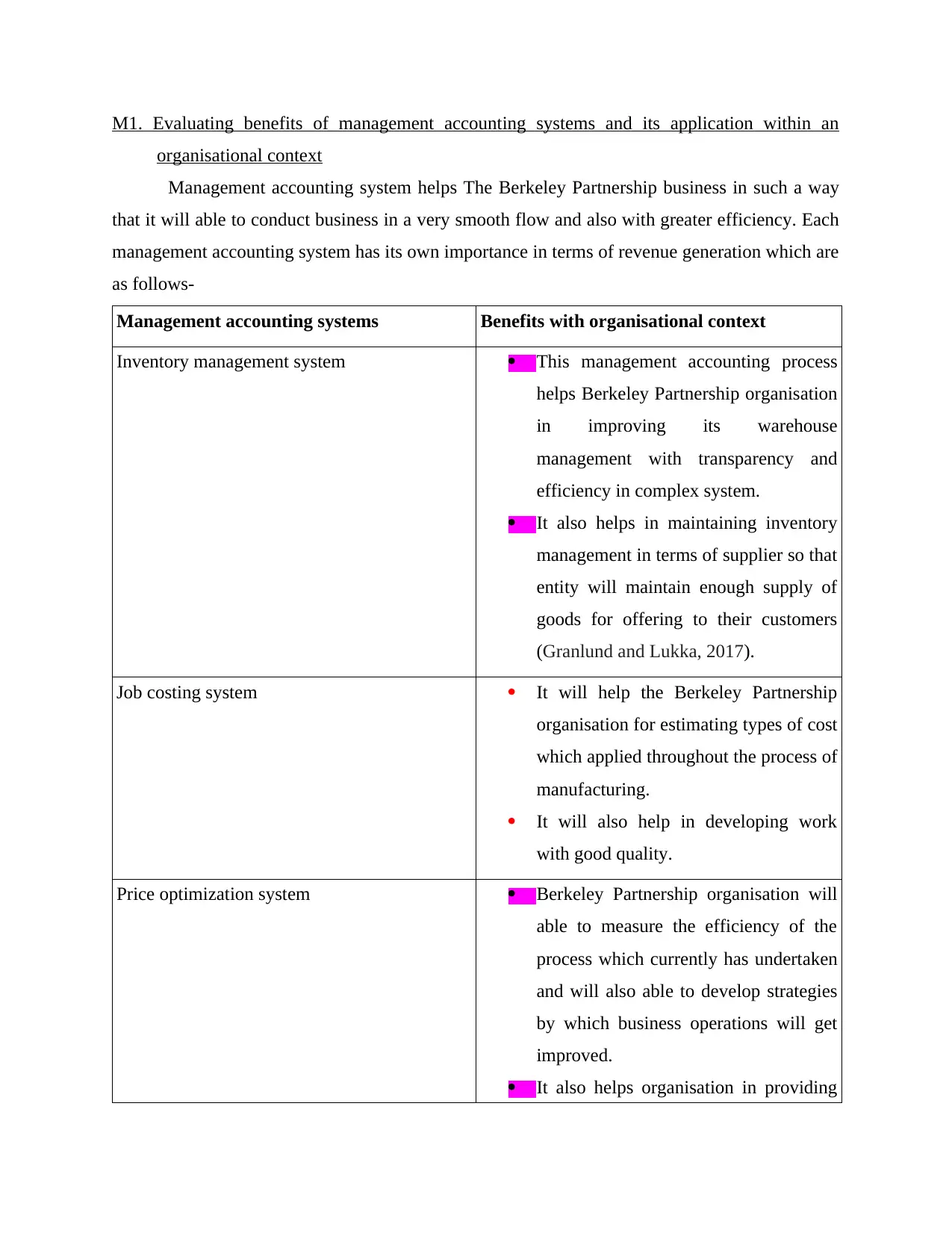

M1. Evaluating benefits of management accounting systems and its application within an

organisational context

Management accounting system helps The Berkeley Partnership business in such a way

that it will able to conduct business in a very smooth flow and also with greater efficiency. Each

management accounting system has its own importance in terms of revenue generation which are

as follows-

Management accounting systems Benefits with organisational context

Inventory management system This management accounting process

helps Berkeley Partnership organisation

in improving its warehouse

management with transparency and

efficiency in complex system.

It also helps in maintaining inventory

management in terms of supplier so that

entity will maintain enough supply of

goods for offering to their customers

(Granlund and Lukka, 2017).

Job costing system It will help the Berkeley Partnership

organisation for estimating types of cost

which applied throughout the process of

manufacturing.

It will also help in developing work

with good quality.

Price optimization system Berkeley Partnership organisation will

able to measure the efficiency of the

process which currently has undertaken

and will also able to develop strategies

by which business operations will get

improved.

It also helps organisation in providing

organisational context

Management accounting system helps The Berkeley Partnership business in such a way

that it will able to conduct business in a very smooth flow and also with greater efficiency. Each

management accounting system has its own importance in terms of revenue generation which are

as follows-

Management accounting systems Benefits with organisational context

Inventory management system This management accounting process

helps Berkeley Partnership organisation

in improving its warehouse

management with transparency and

efficiency in complex system.

It also helps in maintaining inventory

management in terms of supplier so that

entity will maintain enough supply of

goods for offering to their customers

(Granlund and Lukka, 2017).

Job costing system It will help the Berkeley Partnership

organisation for estimating types of cost

which applied throughout the process of

manufacturing.

It will also help in developing work

with good quality.

Price optimization system Berkeley Partnership organisation will

able to measure the efficiency of the

process which currently has undertaken

and will also able to develop strategies

by which business operations will get

improved.

It also helps organisation in providing

necessary information which required

in the process of planning.

D1. Critically evaluating how management accounting system and management accounting

reporting is integrated within organisational process.

Budget report:

With the help of this management accounting report the Berkeley Partnership

organisation will able to concentrate on its production process. It also helps in establishing a

proper path in order to target consumers and to earn income for the entity.

Cost report:

This integration of management accounting will help in calculating cost of items which

are manufactured in the entity so that capability of organisation for generating business profit

will get analysed. Management generally evolute this process through labour costs, overhead and

other cost of consideration. This is the process which helps in analysing the cost value of product

with the selling price.

Performance report:

This integration of management accounting will help managers to develop plan for the

future productions by which cost of production process will get reduced and entity will able to

achieve higher profitability (Dekker, 2016). This report will also help manager in analysing the

performance of the organisation in business market.

Account receivable aging report:

This integration in management accounting will help Berkeley Partnership organisation

in making efforts in order to develop timely collection of the account receivable and to create

proper collection policy by which flexibility and accuracy will get developed in business

operations (Malina, 2018).

LO 2

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

Statement using Marginal and absorption costs.

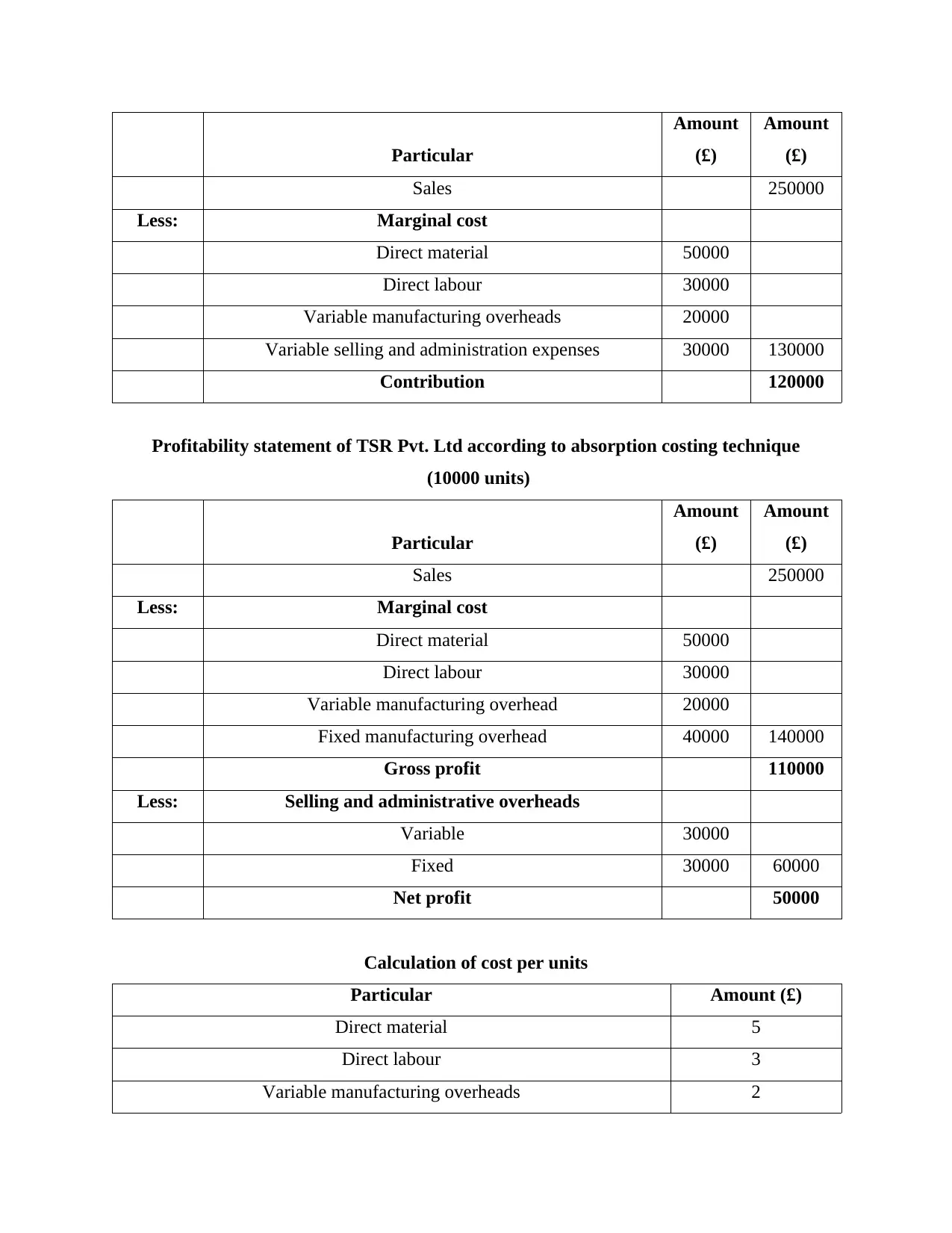

Income statement of TSR Pvt. Ltd as per marginal costing technique (10000 units)

in the process of planning.

D1. Critically evaluating how management accounting system and management accounting

reporting is integrated within organisational process.

Budget report:

With the help of this management accounting report the Berkeley Partnership

organisation will able to concentrate on its production process. It also helps in establishing a

proper path in order to target consumers and to earn income for the entity.

Cost report:

This integration of management accounting will help in calculating cost of items which

are manufactured in the entity so that capability of organisation for generating business profit

will get analysed. Management generally evolute this process through labour costs, overhead and

other cost of consideration. This is the process which helps in analysing the cost value of product

with the selling price.

Performance report:

This integration of management accounting will help managers to develop plan for the

future productions by which cost of production process will get reduced and entity will able to

achieve higher profitability (Dekker, 2016). This report will also help manager in analysing the

performance of the organisation in business market.

Account receivable aging report:

This integration in management accounting will help Berkeley Partnership organisation

in making efforts in order to develop timely collection of the account receivable and to create

proper collection policy by which flexibility and accuracy will get developed in business

operations (Malina, 2018).

LO 2

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

Statement using Marginal and absorption costs.

Income statement of TSR Pvt. Ltd as per marginal costing technique (10000 units)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overheads 20000

Variable selling and administration expenses 30000 130000

Contribution 120000

Profitability statement of TSR Pvt. Ltd according to absorption costing technique

(10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Fixed manufacturing overhead 40000 140000

Gross profit 110000

Less: Selling and administrative overheads

Variable 30000

Fixed 30000 60000

Net profit 50000

Calculation of cost per units

Particular Amount (£)

Direct material 5

Direct labour 3

Variable manufacturing overheads 2

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overheads 20000

Variable selling and administration expenses 30000 130000

Contribution 120000

Profitability statement of TSR Pvt. Ltd according to absorption costing technique

(10000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Fixed manufacturing overhead 40000 140000

Gross profit 110000

Less: Selling and administrative overheads

Variable 30000

Fixed 30000 60000

Net profit 50000

Calculation of cost per units

Particular Amount (£)

Direct material 5

Direct labour 3

Variable manufacturing overheads 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

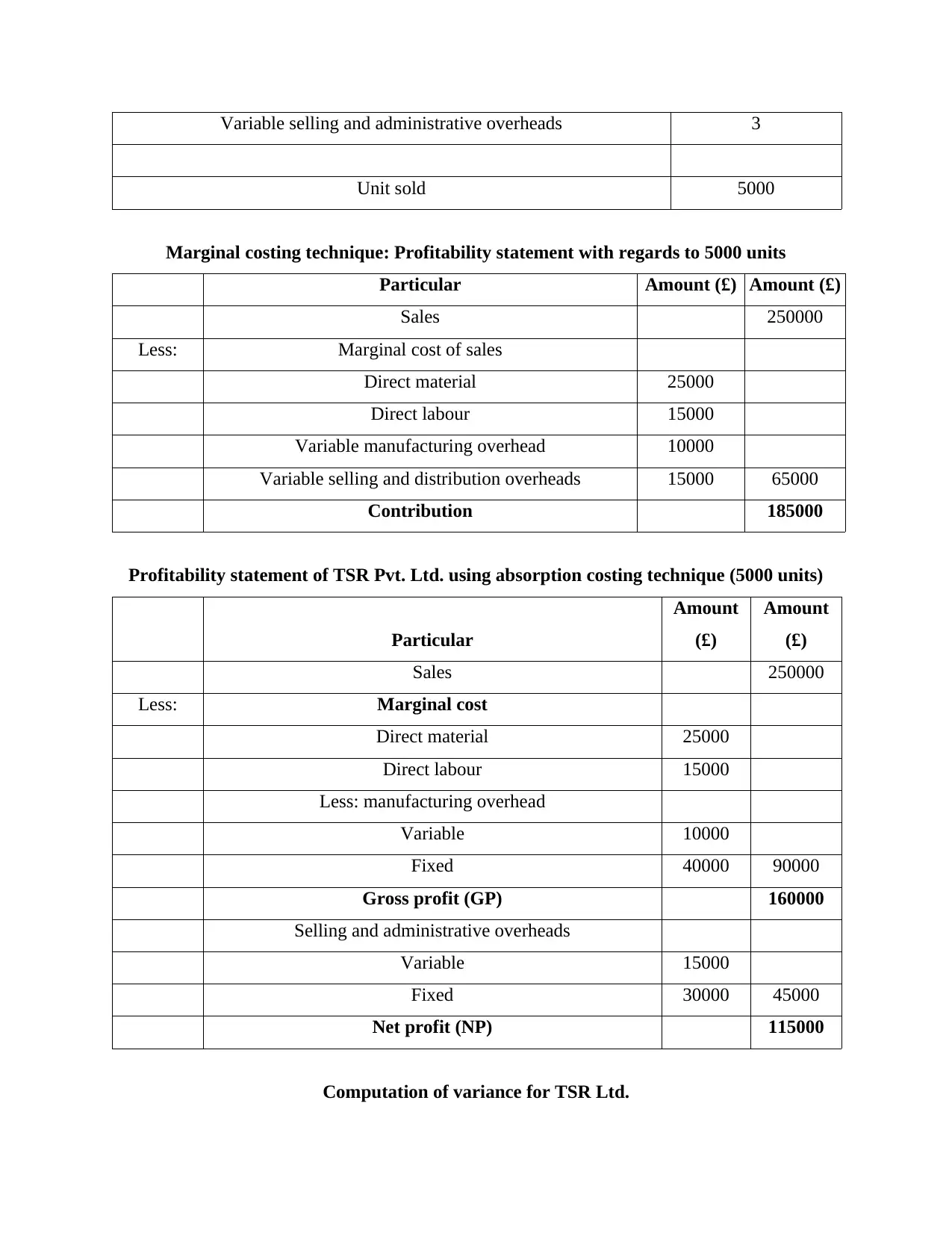

Variable selling and administrative overheads 3

Unit sold 5000

Marginal costing technique: Profitability statement with regards to 5000 units

Particular Amount (£) Amount (£)

Sales 250000

Less: Marginal cost of sales

Direct material 25000

Direct labour 15000

Variable manufacturing overhead 10000

Variable selling and distribution overheads 15000 65000

Contribution 185000

Profitability statement of TSR Pvt. Ltd. using absorption costing technique (5000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 25000

Direct labour 15000

Less: manufacturing overhead

Variable 10000

Fixed 40000 90000

Gross profit (GP) 160000

Selling and administrative overheads

Variable 15000

Fixed 30000 45000

Net profit (NP) 115000

Computation of variance for TSR Ltd.

Unit sold 5000

Marginal costing technique: Profitability statement with regards to 5000 units

Particular Amount (£) Amount (£)

Sales 250000

Less: Marginal cost of sales

Direct material 25000

Direct labour 15000

Variable manufacturing overhead 10000

Variable selling and distribution overheads 15000 65000

Contribution 185000

Profitability statement of TSR Pvt. Ltd. using absorption costing technique (5000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost

Direct material 25000

Direct labour 15000

Less: manufacturing overhead

Variable 10000

Fixed 40000 90000

Gross profit (GP) 160000

Selling and administrative overheads

Variable 15000

Fixed 30000 45000

Net profit (NP) 115000

Computation of variance for TSR Ltd.

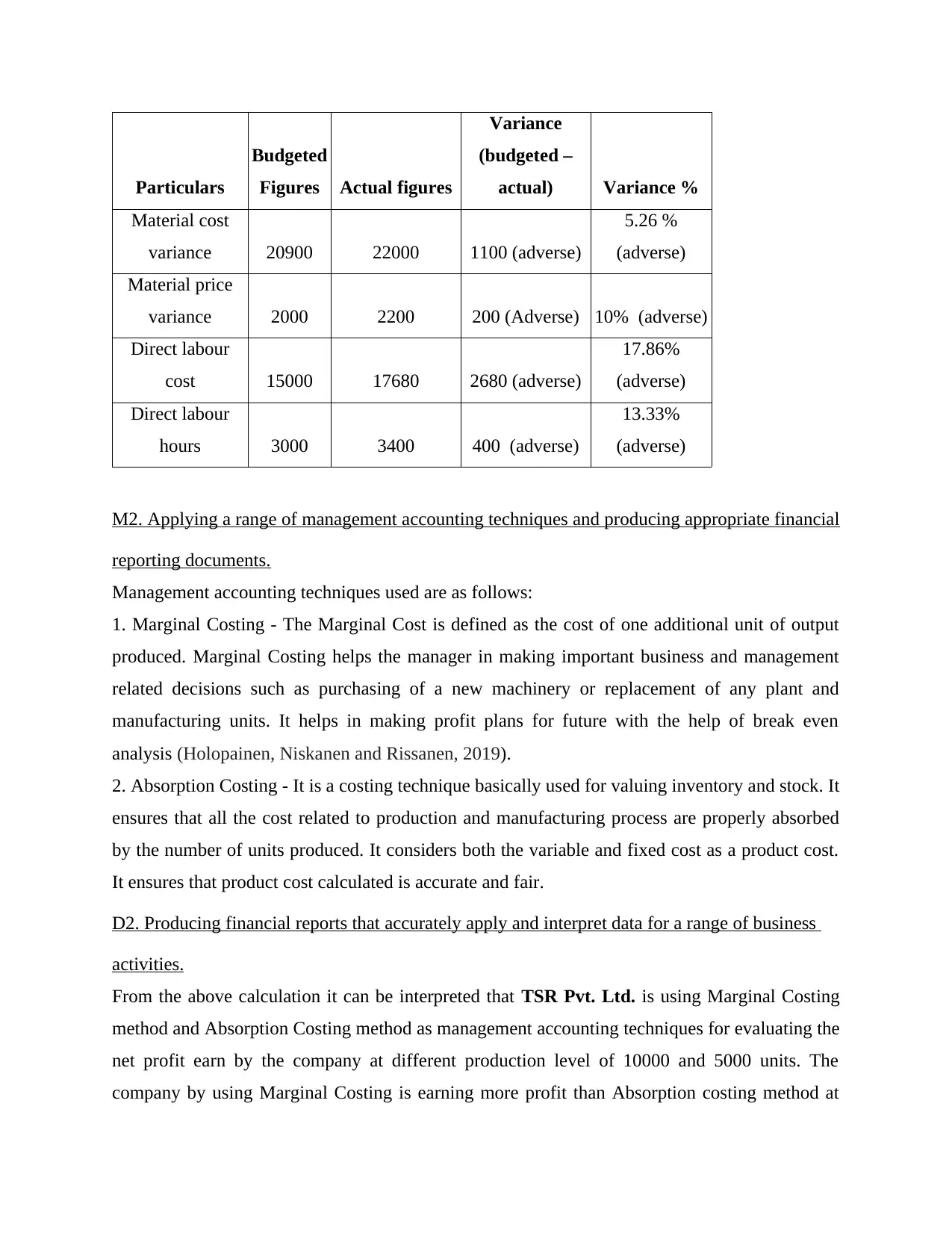

Particulars

Budgeted

Figures Actual figures

Variance

(budgeted –

actual) Variance %

Material cost

variance 20900 22000 1100 (adverse)

5.26 %

(adverse)

Material price

variance 2000 2200 200 (Adverse) 10% (adverse)

Direct labour

cost 15000 17680 2680 (adverse)

17.86%

(adverse)

Direct labour

hours 3000 3400 400 (adverse)

13.33%

(adverse)

M2. Applying a range of management accounting techniques and producing appropriate financial

reporting documents.

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is defined as the cost of one additional unit of output

produced. Marginal Costing helps the manager in making important business and management

related decisions such as purchasing of a new machinery or replacement of any plant and

manufacturing units. It helps in making profit plans for future with the help of break even

analysis (Holopainen, Niskanen and Rissanen, 2019).

2. Absorption Costing - It is a costing technique basically used for valuing inventory and stock. It

ensures that all the cost related to production and manufacturing process are properly absorbed

by the number of units produced. It considers both the variable and fixed cost as a product cost.

It ensures that product cost calculated is accurate and fair.

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities.

From the above calculation it can be interpreted that TSR Pvt. Ltd. is using Marginal Costing

method and Absorption Costing method as management accounting techniques for evaluating the

net profit earn by the company at different production level of 10000 and 5000 units. The

company by using Marginal Costing is earning more profit than Absorption costing method at

Budgeted

Figures Actual figures

Variance

(budgeted –

actual) Variance %

Material cost

variance 20900 22000 1100 (adverse)

5.26 %

(adverse)

Material price

variance 2000 2200 200 (Adverse) 10% (adverse)

Direct labour

cost 15000 17680 2680 (adverse)

17.86%

(adverse)

Direct labour

hours 3000 3400 400 (adverse)

13.33%

(adverse)

M2. Applying a range of management accounting techniques and producing appropriate financial

reporting documents.

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is defined as the cost of one additional unit of output

produced. Marginal Costing helps the manager in making important business and management

related decisions such as purchasing of a new machinery or replacement of any plant and

manufacturing units. It helps in making profit plans for future with the help of break even

analysis (Holopainen, Niskanen and Rissanen, 2019).

2. Absorption Costing - It is a costing technique basically used for valuing inventory and stock. It

ensures that all the cost related to production and manufacturing process are properly absorbed

by the number of units produced. It considers both the variable and fixed cost as a product cost.

It ensures that product cost calculated is accurate and fair.

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities.

From the above calculation it can be interpreted that TSR Pvt. Ltd. is using Marginal Costing

method and Absorption Costing method as management accounting techniques for evaluating the

net profit earn by the company at different production level of 10000 and 5000 units. The

company by using Marginal Costing is earning more profit than Absorption costing method at

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.