Management Accounting Report: Techniques and Financial Solutions

VerifiedAdded on 2020/11/23

|17

|5646

|124

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within a company manufacturing hand dryers (Airdi). It begins by defining management accounting and detailing its various types, including job costing, price optimization, inventory management, and cost accounting systems. The report then explores different management accounting reporting methods like budget reports, inventory reports, and job costing reports. It also discusses the benefits of these systems, such as improved customer behavior analysis, cost reduction, and inventory management. The report further delves into cost calculations for preparing income statements, differentiating between fixed and variable costs, and explaining marginal and absorption costing. Additionally, the report examines planning tools for budgetary control, comparing their advantages and disadvantages, and analyzing how organizations adapt management accounting systems to resolve financial problems. The conclusion summarizes the key findings and emphasizes the importance of management accounting in making informed business decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

M1 Benefits of management accounting system........................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process.........................................................................................................................................4

TASK 2.......................................................................................................................................5

P3 Cost calculations to prepare an income statement.................................................................5

M2 A range of management accounting techniques...................................................................8

D2 Analysis and Interpretation of data.......................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

Budgetary control........................................................................................................................8

M3 Analysis on use of different planning tool for preparing and forecasting budgets.............10

TASK 4..........................................................................................................................................10

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.....................................................................................................................10

M4 Analysis on how management accounting lead to sustainable success..............................12

D3 Evaluation of how planning tools respond to solve financial problems.............................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

M1 Benefits of management accounting system........................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process.........................................................................................................................................4

TASK 2.......................................................................................................................................5

P3 Cost calculations to prepare an income statement.................................................................5

M2 A range of management accounting techniques...................................................................8

D2 Analysis and Interpretation of data.......................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

Budgetary control........................................................................................................................8

M3 Analysis on use of different planning tool for preparing and forecasting budgets.............10

TASK 4..........................................................................................................................................10

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.....................................................................................................................10

M4 Analysis on how management accounting lead to sustainable success..............................12

D3 Evaluation of how planning tools respond to solve financial problems.............................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management Accounting is determine as a presentation of accounting information so as

to formulate different kinds of policies which can further be adopted by management of an

company in order to perform day-to-day activities (Lavia López and Hiebl, 2014). Thus, in

simple words, management accounting assist management in doing entire functions that includes

planning, organising, staffing, directing and controlling. Airdi is a company which is taken in

this assignment and firm deals in manufacturing Hand Dryer thus, this report will discuss about

different methods of management accounting for performing business operations in a better

manner.

Present report will focus on understanding of management accounting system, along with

application of range if management accounting technique is included in this assignment. In

addition to this, explanation of use of planning tools for management accounting is mentioned in

this report. Other than this, comparison of ways are included in this assignment which different

organisation can use for responding to financial issues and problems (Hiebl, 2014).

TASK 1

P1 Management accounting and its different types

Management accounting is consider as a process in which accounting information that are

obtained from financial accounting and cost accounting are interpreted, analysed, identified and

presented. Thus, it can be said that management accounting assist managers of a company in

formulating policies and making decision for day-to-day activities. Therefore, in an organisation

management accounting plays a crucial role in determining as well as forecasting cash flow. For

operating its business in a better manner it is important that Airdi has proper management

accounting department who can help managers in preparing effective reports of budget.

Company is manufacturing Hand Dryer, and is well recognised around the globe.

There are different types of management accounting system which Airdi can incorporate

for operating its business in an effective manner, therefore, crucial management accounting

system are explained below for better understanding (Chiarini and Vagnoni, 2015).

Job Costing System: This is a system that after monitoring the expenses helps an an

individual and management in assigning manufacturing cost for a specific products. Job Costing

system can be used by Airdi and is applicable when company's products are identical and can

1

Management Accounting is determine as a presentation of accounting information so as

to formulate different kinds of policies which can further be adopted by management of an

company in order to perform day-to-day activities (Lavia López and Hiebl, 2014). Thus, in

simple words, management accounting assist management in doing entire functions that includes

planning, organising, staffing, directing and controlling. Airdi is a company which is taken in

this assignment and firm deals in manufacturing Hand Dryer thus, this report will discuss about

different methods of management accounting for performing business operations in a better

manner.

Present report will focus on understanding of management accounting system, along with

application of range if management accounting technique is included in this assignment. In

addition to this, explanation of use of planning tools for management accounting is mentioned in

this report. Other than this, comparison of ways are included in this assignment which different

organisation can use for responding to financial issues and problems (Hiebl, 2014).

TASK 1

P1 Management accounting and its different types

Management accounting is consider as a process in which accounting information that are

obtained from financial accounting and cost accounting are interpreted, analysed, identified and

presented. Thus, it can be said that management accounting assist managers of a company in

formulating policies and making decision for day-to-day activities. Therefore, in an organisation

management accounting plays a crucial role in determining as well as forecasting cash flow. For

operating its business in a better manner it is important that Airdi has proper management

accounting department who can help managers in preparing effective reports of budget.

Company is manufacturing Hand Dryer, and is well recognised around the globe.

There are different types of management accounting system which Airdi can incorporate

for operating its business in an effective manner, therefore, crucial management accounting

system are explained below for better understanding (Chiarini and Vagnoni, 2015).

Job Costing System: This is a system that after monitoring the expenses helps an an

individual and management in assigning manufacturing cost for a specific products. Job Costing

system can be used by Airdi and is applicable when company's products are identical and can

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

keep a record of order expenses. Therefore, job costing system is used by companies when they

have products that are different from one another. A significant variations in products

manufactured can be seen such as direct material can be directly linked with direct labour. Main

requirement of this, is to evaluate the actual cost and revenues of a product and commodity.

Price Optimising System: This is basically used for controlling the prices of resources,

thus, price optimising system can be incorporated by company so as to decide price of multiple

goods at the same time (Senftlechner and Hiebl, 2015). Therefore, for a firm it assist them in

determining the effects of demands after fluctuation in different price level. Moreover, Airdi

company will use this method in order to determine the price as per customer's segments so that

company can know their responses as per different price levels. Main purpose of this is to deliver

best quality products to its customers according to the needs and wants under limited period of

time.

Inventory management System: This basically guides company with when to order a

product and in what proportion. Inventory management system helps firm in minimising the total

cost of inventories so that organisation can generate high level of return. Therefore, with the help

of this method Airdi Ltd., can manufacture their products and keep them as a stock so that it can

be used whenever it is required. This can be further applied by using three different method

which is important for managing the inventory system are LIFO (Last In, First Out), FIFO (First

In, First Out) and ABC. In relation with Airdi Ltd., they are using ABC form for selling their

product. In this category products that comes under the category of A are need for attention

because it has a great impact in terms of finance. Likewise, B and C denotes moderate and low-

value commodities respectively (Bovens, Goodin and Schillemans, 2014).

Cost Accounting System: It is determine as a framework which is used by companies in

order to estimate cost of their products in order to get profitability. Therefore, it is crucial for

Airdi to know what kind of goods are profitable and which one are not. In addition to this, Cost

accounting system helps company in knowing and estimating closing value of material

inventory, work in progress and inventory of finished commodities so that financial statement

can be prepared. This includes two main cost accounting system i.e. job order costing: It is cost

accounting system that compile different manufacturing cost separately as per the job assigned.

Process costing: This is determine as a cost accounting system that accumulates cost of

2

have products that are different from one another. A significant variations in products

manufactured can be seen such as direct material can be directly linked with direct labour. Main

requirement of this, is to evaluate the actual cost and revenues of a product and commodity.

Price Optimising System: This is basically used for controlling the prices of resources,

thus, price optimising system can be incorporated by company so as to decide price of multiple

goods at the same time (Senftlechner and Hiebl, 2015). Therefore, for a firm it assist them in

determining the effects of demands after fluctuation in different price level. Moreover, Airdi

company will use this method in order to determine the price as per customer's segments so that

company can know their responses as per different price levels. Main purpose of this is to deliver

best quality products to its customers according to the needs and wants under limited period of

time.

Inventory management System: This basically guides company with when to order a

product and in what proportion. Inventory management system helps firm in minimising the total

cost of inventories so that organisation can generate high level of return. Therefore, with the help

of this method Airdi Ltd., can manufacture their products and keep them as a stock so that it can

be used whenever it is required. This can be further applied by using three different method

which is important for managing the inventory system are LIFO (Last In, First Out), FIFO (First

In, First Out) and ABC. In relation with Airdi Ltd., they are using ABC form for selling their

product. In this category products that comes under the category of A are need for attention

because it has a great impact in terms of finance. Likewise, B and C denotes moderate and low-

value commodities respectively (Bovens, Goodin and Schillemans, 2014).

Cost Accounting System: It is determine as a framework which is used by companies in

order to estimate cost of their products in order to get profitability. Therefore, it is crucial for

Airdi to know what kind of goods are profitable and which one are not. In addition to this, Cost

accounting system helps company in knowing and estimating closing value of material

inventory, work in progress and inventory of finished commodities so that financial statement

can be prepared. This includes two main cost accounting system i.e. job order costing: It is cost

accounting system that compile different manufacturing cost separately as per the job assigned.

Process costing: This is determine as a cost accounting system that accumulates cost of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manufacturing according to the separate process. The main purpose of cost accounting system is

to estimate cost and revenue for the company (Shields, 2015).

P2 Methods for management accounting Reporting

Management accounting reporting helps management to determine the actual

performance of the organization. These reports are prepared weekly, monthly, quarterly or

yearly. It involves collection of data that gives material information about operations of

organization. Management reports helps the managers to forecast important business decisions.

Airdri Ltd. is a hand dryer manufacturing company. Airdri needs management accounting report

for better decision making because it will help the company to determine existing and future

operations and will provide accurate financial information. Different management accounting

reporting methods are as following:

Budget Reports: Budgeting reports are prepared to analyze related estimated cost. It is

prepared on the basis of expenditure of previous years. It will help Airdri to evaluates the

performance of different departments and help them to control costs. It will also help in

analyzing the actual performance with budgeted performance (Schaltegger, and Burritt,

2017). These reports helps in providing incentives to employees and motivates them to

achieve desired objectives. Therefore, with the help of this report, managers of Airdi Ltd.,

will be able to compare their business performance in one financial year.

Inventory and manufacturing reports: These types of reports are prepared by

manufacturing companies to make inventory and manufacturing process efficient. It

includes labor cost, per unit overhead cost and other cost which are included in

manufacturing process. This report will help Aridri in comparing different assembly lines

of business which provides area of improvement so that performance of the departments

and employees can be improved and it will enhance efficiency and effectiveness.

Job costing reports: This kind of reports helps in determine the cost, expense and

profitability of particular projects. This report will help Aridri to identify the profitable

and non profitable business activities so that they can increase their efforts by focusing on

profit making activities. It will help them in reducing wastage of cost so as to make the

project more successful (Klemstine and Maher, 2014).

3

to estimate cost and revenue for the company (Shields, 2015).

P2 Methods for management accounting Reporting

Management accounting reporting helps management to determine the actual

performance of the organization. These reports are prepared weekly, monthly, quarterly or

yearly. It involves collection of data that gives material information about operations of

organization. Management reports helps the managers to forecast important business decisions.

Airdri Ltd. is a hand dryer manufacturing company. Airdri needs management accounting report

for better decision making because it will help the company to determine existing and future

operations and will provide accurate financial information. Different management accounting

reporting methods are as following:

Budget Reports: Budgeting reports are prepared to analyze related estimated cost. It is

prepared on the basis of expenditure of previous years. It will help Airdri to evaluates the

performance of different departments and help them to control costs. It will also help in

analyzing the actual performance with budgeted performance (Schaltegger, and Burritt,

2017). These reports helps in providing incentives to employees and motivates them to

achieve desired objectives. Therefore, with the help of this report, managers of Airdi Ltd.,

will be able to compare their business performance in one financial year.

Inventory and manufacturing reports: These types of reports are prepared by

manufacturing companies to make inventory and manufacturing process efficient. It

includes labor cost, per unit overhead cost and other cost which are included in

manufacturing process. This report will help Aridri in comparing different assembly lines

of business which provides area of improvement so that performance of the departments

and employees can be improved and it will enhance efficiency and effectiveness.

Job costing reports: This kind of reports helps in determine the cost, expense and

profitability of particular projects. This report will help Aridri to identify the profitable

and non profitable business activities so that they can increase their efforts by focusing on

profit making activities. It will help them in reducing wastage of cost so as to make the

project more successful (Klemstine and Maher, 2014).

3

M1 Benefits of management accounting system

Job Costing System and its benefits:

By incorporating this system, Airdi Ltd., can evaluate changes in behaviour of customers

as per different-different price strategy. Other than this, it assist firm in evaluating the quality of

work which is being done.

Price Optimisation System and its benefits:

With the help of this method Airdi Ltd., can determine the attitude and behaviour of

consumers based on different prices. As a result, through this method company can maximise its

profits (Bennett and James, 2017).

Cost Accounting System and its benefits:

This system measures the efficiency of process which is being incorporated by company

for making improvements. Cost accounting system is applicable for reducing cost of a

commodity.

Inventory Management System and its benefits:

Through this system Airdi Ltd., can improve their accuracy level and effectiveness as

well. It is being used by most of the companies because of its cost and time saving tendency.

With the help of this, stock of inventory can be maintained which can be used for future purpose.

D1 Critical evaluation on management accounting report integrated within organisational process

Types of reporting Integrated within organisational process

Budgeting Report Airdi, with the help of both integrated organisational

process and budgeting reports can make path for

companies activities so that targeted goals and objectives

can be achieved in an effective manner.

Job Cost Report Main purpose of Airdi Ltd., should be of achieving cost

objectives so that price strategies can be decided by

minimising overall cost of a product.

Inventory and manufacturing

report

This report will provide benefit to Airdi Ltd., to track and

monitor procedure of inventory.

4

Job Costing System and its benefits:

By incorporating this system, Airdi Ltd., can evaluate changes in behaviour of customers

as per different-different price strategy. Other than this, it assist firm in evaluating the quality of

work which is being done.

Price Optimisation System and its benefits:

With the help of this method Airdi Ltd., can determine the attitude and behaviour of

consumers based on different prices. As a result, through this method company can maximise its

profits (Bennett and James, 2017).

Cost Accounting System and its benefits:

This system measures the efficiency of process which is being incorporated by company

for making improvements. Cost accounting system is applicable for reducing cost of a

commodity.

Inventory Management System and its benefits:

Through this system Airdi Ltd., can improve their accuracy level and effectiveness as

well. It is being used by most of the companies because of its cost and time saving tendency.

With the help of this, stock of inventory can be maintained which can be used for future purpose.

D1 Critical evaluation on management accounting report integrated within organisational process

Types of reporting Integrated within organisational process

Budgeting Report Airdi, with the help of both integrated organisational

process and budgeting reports can make path for

companies activities so that targeted goals and objectives

can be achieved in an effective manner.

Job Cost Report Main purpose of Airdi Ltd., should be of achieving cost

objectives so that price strategies can be decided by

minimising overall cost of a product.

Inventory and manufacturing

report

This report will provide benefit to Airdi Ltd., to track and

monitor procedure of inventory.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3 Cost calculations to prepare an income statement

Cost indicates the value of money which are being put or used for manufacturing product

so that the same can be deliver to its customers (Cleary, 2015). This includes material required,

resources, time and utilities etc., Furthermore, cosy are of two types:

Fixed Cost: These are constant and doesn't change even after increase or decrease in

number of products or services which are being produced or sold. Fixed cost comes under

operating expenses which cannot be avoided by a firm. This is moreover used in break even

analysis so that level of pricing can be determined. For example: property taxes which has to be

Variable Cost: These are the cost which vary with the proportion of production output.

Variable cost can increase or decrease and it depends upon the goods produced. Therefore, it can

be said that this depends upon the products which are manufactured per unit. In order to calculate

variable cost one can use this formula that is given below:

Total variable cost = Quantity of output X Variable cost per unit of output.

Marginal Costing: This determine as a rate at which a change in total cost can be seen

because of the increase in production by one unit. Marginal cosy is important for an organisation

as it helps a company in taking effective decision for their business operations (Endenich, 2014).

Net income = (sales revenue – marginal cost of goods sold) = (contribution – fixed cost)

Absorption Costing: It is a cost accounting method for valuing inventory. It includes all

the costs of manufacturing a product like fixed and variable costs. This costing method gives a

more comprehensive and accurate view on how much it really costs to produce your inventory.

The components of absorption costing are: Direct material, direct labour, variable manufacturing

overhead and fixed manufacturing overhead. It is possible to use absorption costing to allocate

overhead costs for inventory valuation purpose. Absorption costing is a time-consuming and

expensive costing system.

Net Incomes = (Sales revenue – Cost of goods sold) = (Gross profit – Selling and Administrative

expenses)

Working Notes:

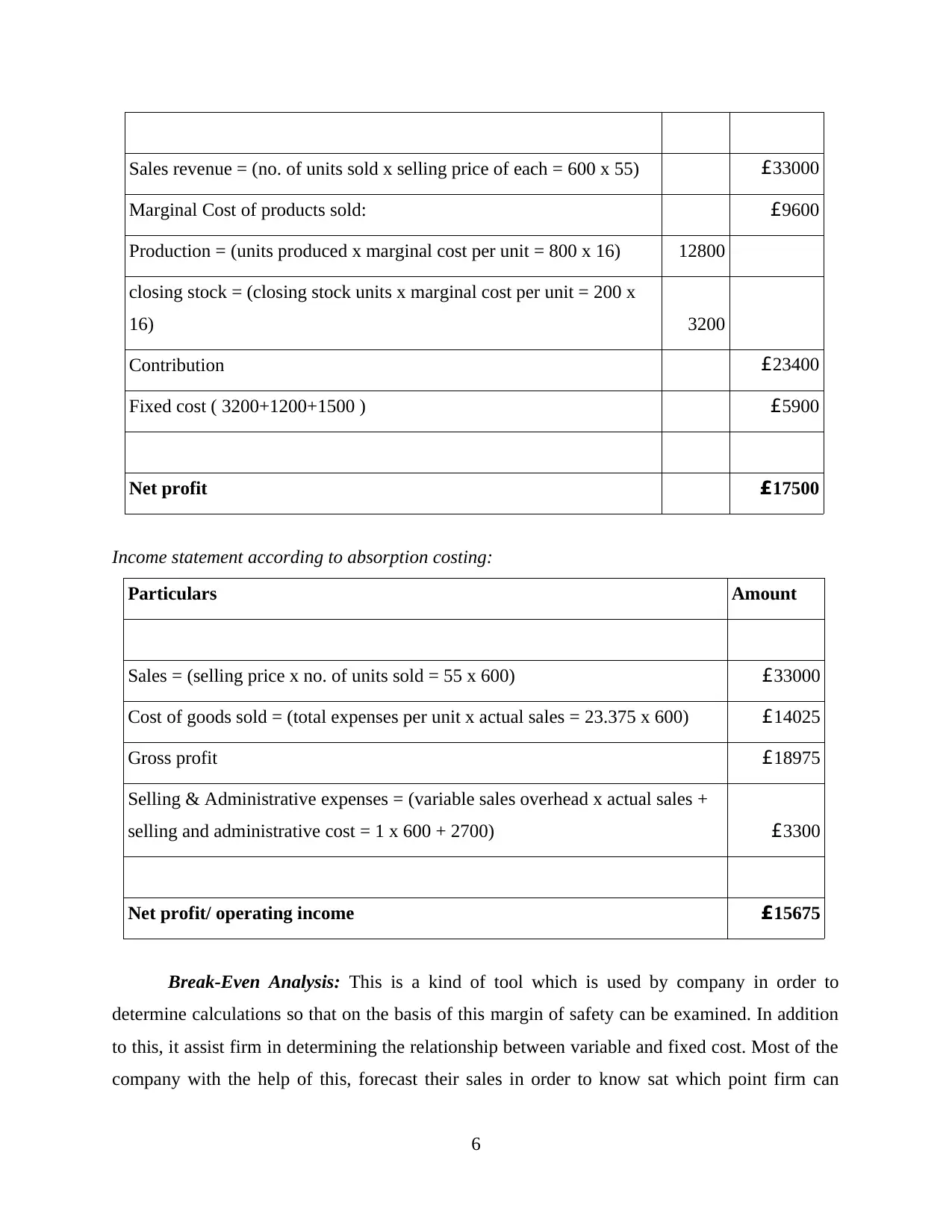

Income statement on the basis of marginal costing:

Particulars Amount

5

P3 Cost calculations to prepare an income statement

Cost indicates the value of money which are being put or used for manufacturing product

so that the same can be deliver to its customers (Cleary, 2015). This includes material required,

resources, time and utilities etc., Furthermore, cosy are of two types:

Fixed Cost: These are constant and doesn't change even after increase or decrease in

number of products or services which are being produced or sold. Fixed cost comes under

operating expenses which cannot be avoided by a firm. This is moreover used in break even

analysis so that level of pricing can be determined. For example: property taxes which has to be

Variable Cost: These are the cost which vary with the proportion of production output.

Variable cost can increase or decrease and it depends upon the goods produced. Therefore, it can

be said that this depends upon the products which are manufactured per unit. In order to calculate

variable cost one can use this formula that is given below:

Total variable cost = Quantity of output X Variable cost per unit of output.

Marginal Costing: This determine as a rate at which a change in total cost can be seen

because of the increase in production by one unit. Marginal cosy is important for an organisation

as it helps a company in taking effective decision for their business operations (Endenich, 2014).

Net income = (sales revenue – marginal cost of goods sold) = (contribution – fixed cost)

Absorption Costing: It is a cost accounting method for valuing inventory. It includes all

the costs of manufacturing a product like fixed and variable costs. This costing method gives a

more comprehensive and accurate view on how much it really costs to produce your inventory.

The components of absorption costing are: Direct material, direct labour, variable manufacturing

overhead and fixed manufacturing overhead. It is possible to use absorption costing to allocate

overhead costs for inventory valuation purpose. Absorption costing is a time-consuming and

expensive costing system.

Net Incomes = (Sales revenue – Cost of goods sold) = (Gross profit – Selling and Administrative

expenses)

Working Notes:

Income statement on the basis of marginal costing:

Particulars Amount

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales revenue = (no. of units sold x selling price of each = 600 x 55) £33000

Marginal Cost of products sold: £9600

Production = (units produced x marginal cost per unit = 800 x 16) 12800

closing stock = (closing stock units x marginal cost per unit = 200 x

16) 3200

Contribution £23400

Fixed cost ( 3200+1200+1500 ) £5900

Net profit £17500

Income statement according to absorption costing:

Particulars Amount

Sales = (selling price x no. of units sold = 55 x 600) £33000

Cost of goods sold = (total expenses per unit x actual sales = 23.375 x 600) £14025

Gross profit £18975

Selling & Administrative expenses = (variable sales overhead x actual sales +

selling and administrative cost = 1 x 600 + 2700) £3300

Net profit/ operating income £15675

Break-Even Analysis: This is a kind of tool which is used by company in order to

determine calculations so that on the basis of this margin of safety can be examined. In addition

to this, it assist firm in determining the relationship between variable and fixed cost. Most of the

company with the help of this, forecast their sales in order to know sat which point firm can

6

Marginal Cost of products sold: £9600

Production = (units produced x marginal cost per unit = 800 x 16) 12800

closing stock = (closing stock units x marginal cost per unit = 200 x

16) 3200

Contribution £23400

Fixed cost ( 3200+1200+1500 ) £5900

Net profit £17500

Income statement according to absorption costing:

Particulars Amount

Sales = (selling price x no. of units sold = 55 x 600) £33000

Cost of goods sold = (total expenses per unit x actual sales = 23.375 x 600) £14025

Gross profit £18975

Selling & Administrative expenses = (variable sales overhead x actual sales +

selling and administrative cost = 1 x 600 + 2700) £3300

Net profit/ operating income £15675

Break-Even Analysis: This is a kind of tool which is used by company in order to

determine calculations so that on the basis of this margin of safety can be examined. In addition

to this, it assist firm in determining the relationship between variable and fixed cost. Most of the

company with the help of this, forecast their sales in order to know sat which point firm can

6

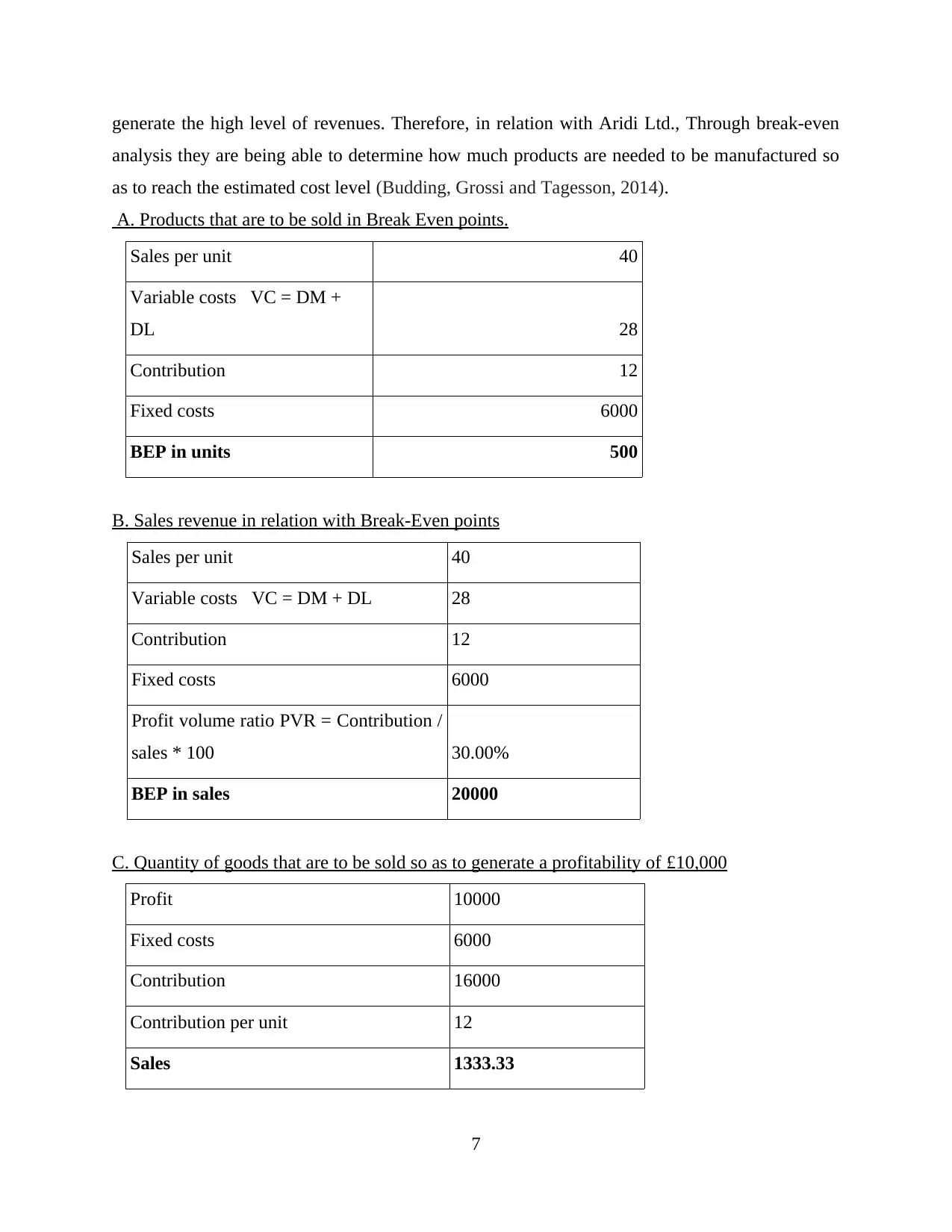

generate the high level of revenues. Therefore, in relation with Aridi Ltd., Through break-even

analysis they are being able to determine how much products are needed to be manufactured so

as to reach the estimated cost level (Budding, Grossi and Tagesson, 2014).

A. Products that are to be sold in Break Even points.

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Sales revenue in relation with Break-Even points

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

C. Quantity of goods that are to be sold so as to generate a profitability of £10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

7

analysis they are being able to determine how much products are needed to be manufactured so

as to reach the estimated cost level (Budding, Grossi and Tagesson, 2014).

A. Products that are to be sold in Break Even points.

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Sales revenue in relation with Break-Even points

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

C. Quantity of goods that are to be sold so as to generate a profitability of £10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

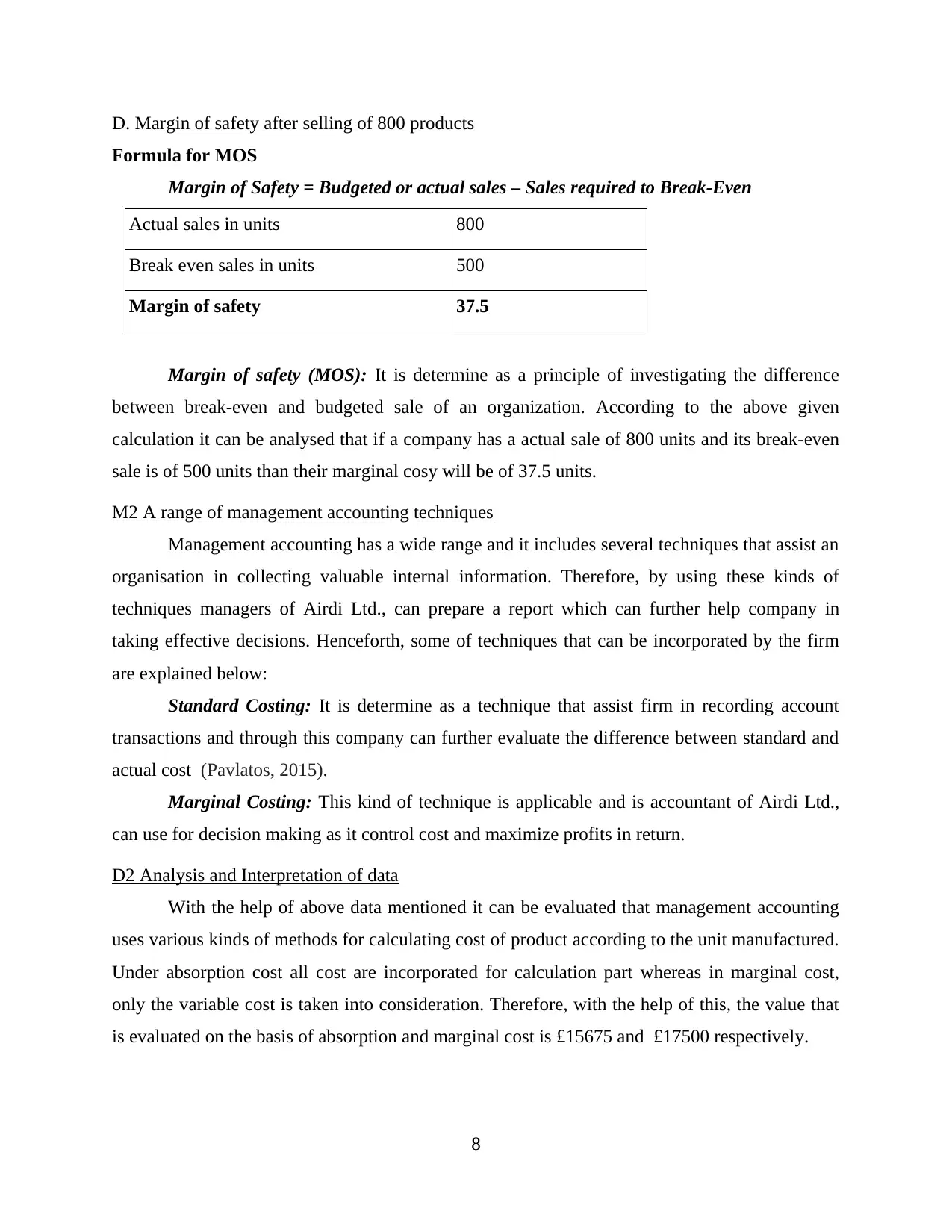

D. Margin of safety after selling of 800 products

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety (MOS): It is determine as a principle of investigating the difference

between break-even and budgeted sale of an organization. According to the above given

calculation it can be analysed that if a company has a actual sale of 800 units and its break-even

sale is of 500 units than their marginal cosy will be of 37.5 units.

M2 A range of management accounting techniques

Management accounting has a wide range and it includes several techniques that assist an

organisation in collecting valuable internal information. Therefore, by using these kinds of

techniques managers of Airdi Ltd., can prepare a report which can further help company in

taking effective decisions. Henceforth, some of techniques that can be incorporated by the firm

are explained below:

Standard Costing: It is determine as a technique that assist firm in recording account

transactions and through this company can further evaluate the difference between standard and

actual cost (Pavlatos, 2015).

Marginal Costing: This kind of technique is applicable and is accountant of Airdi Ltd.,

can use for decision making as it control cost and maximize profits in return.

D2 Analysis and Interpretation of data

With the help of above data mentioned it can be evaluated that management accounting

uses various kinds of methods for calculating cost of product according to the unit manufactured.

Under absorption cost all cost are incorporated for calculation part whereas in marginal cost,

only the variable cost is taken into consideration. Therefore, with the help of this, the value that

is evaluated on the basis of absorption and marginal cost is £15675 and £17500 respectively.

8

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety (MOS): It is determine as a principle of investigating the difference

between break-even and budgeted sale of an organization. According to the above given

calculation it can be analysed that if a company has a actual sale of 800 units and its break-even

sale is of 500 units than their marginal cosy will be of 37.5 units.

M2 A range of management accounting techniques

Management accounting has a wide range and it includes several techniques that assist an

organisation in collecting valuable internal information. Therefore, by using these kinds of

techniques managers of Airdi Ltd., can prepare a report which can further help company in

taking effective decisions. Henceforth, some of techniques that can be incorporated by the firm

are explained below:

Standard Costing: It is determine as a technique that assist firm in recording account

transactions and through this company can further evaluate the difference between standard and

actual cost (Pavlatos, 2015).

Marginal Costing: This kind of technique is applicable and is accountant of Airdi Ltd.,

can use for decision making as it control cost and maximize profits in return.

D2 Analysis and Interpretation of data

With the help of above data mentioned it can be evaluated that management accounting

uses various kinds of methods for calculating cost of product according to the unit manufactured.

Under absorption cost all cost are incorporated for calculation part whereas in marginal cost,

only the variable cost is taken into consideration. Therefore, with the help of this, the value that

is evaluated on the basis of absorption and marginal cost is £15675 and £17500 respectively.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control

Budgetary control refers to planning that helps management in allotment of duties and

authorities, to assist in estimating the plans and policies for future, set standards for result,

provide aid to analyze the standard and actual performance with which management can analyze

performance of operations (Banker and et. al., 2014). It helps in minimizing the wastage in

unprofitable areas of operations and focus their time and skills in profitable areas. Every

organization need to prepare budget to allocate resources to mid-level and lower-level for better

functioning of operations and to achieve objectives and goals.

As any other organization Aridri ltd. also needs budgetary control for smooth

functioning of its operations. Managers needs to control finance activities in less productive

areas because this company deals at small scale. Therefore, every single pound in business is

precious. Moreover, budgetary control also helps in reducing risks which may arise due to

natural disaster(earthquake, flood etc.), fluctuations in economic conditions(changes in demand

and supply, exchange rates, interest rate, inflation, return on investment etc.), innovation and

introduction of new technology and terrorists attack. These kind of risks can affect organization

unfavourably. Thus, for reducing these risks, some control planning tools are given below:-

Planning Tools Usage Advantage Disadvantage

Forecasting planning

tool

Planning is viewed as

a roadmap for an

organization to

achieve its goals and

objectives. Forecasting

means prediction for

future activities.

Therefore, forecasting

tools are used to

anticipate future

uncertainties related to

Aridri Ltd. can use

forecasting tool to

build out strategies to

reduce risk and

achieving competitive

advantages.

As no one can predict

future with certainty,

any kind of change can

be harmful for the

organization because

then it will not be

according to the

forecasting (Mohamad

and et. al., 2015).

9

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control

Budgetary control refers to planning that helps management in allotment of duties and

authorities, to assist in estimating the plans and policies for future, set standards for result,

provide aid to analyze the standard and actual performance with which management can analyze

performance of operations (Banker and et. al., 2014). It helps in minimizing the wastage in

unprofitable areas of operations and focus their time and skills in profitable areas. Every

organization need to prepare budget to allocate resources to mid-level and lower-level for better

functioning of operations and to achieve objectives and goals.

As any other organization Aridri ltd. also needs budgetary control for smooth

functioning of its operations. Managers needs to control finance activities in less productive

areas because this company deals at small scale. Therefore, every single pound in business is

precious. Moreover, budgetary control also helps in reducing risks which may arise due to

natural disaster(earthquake, flood etc.), fluctuations in economic conditions(changes in demand

and supply, exchange rates, interest rate, inflation, return on investment etc.), innovation and

introduction of new technology and terrorists attack. These kind of risks can affect organization

unfavourably. Thus, for reducing these risks, some control planning tools are given below:-

Planning Tools Usage Advantage Disadvantage

Forecasting planning

tool

Planning is viewed as

a roadmap for an

organization to

achieve its goals and

objectives. Forecasting

means prediction for

future activities.

Therefore, forecasting

tools are used to

anticipate future

uncertainties related to

Aridri Ltd. can use

forecasting tool to

build out strategies to

reduce risk and

achieving competitive

advantages.

As no one can predict

future with certainty,

any kind of change can

be harmful for the

organization because

then it will not be

according to the

forecasting (Mohamad

and et. al., 2015).

9

the business. In

context with Aridri,

forecasting tools can

be used for analysing

the risk and

opportunities that may

occur in future.

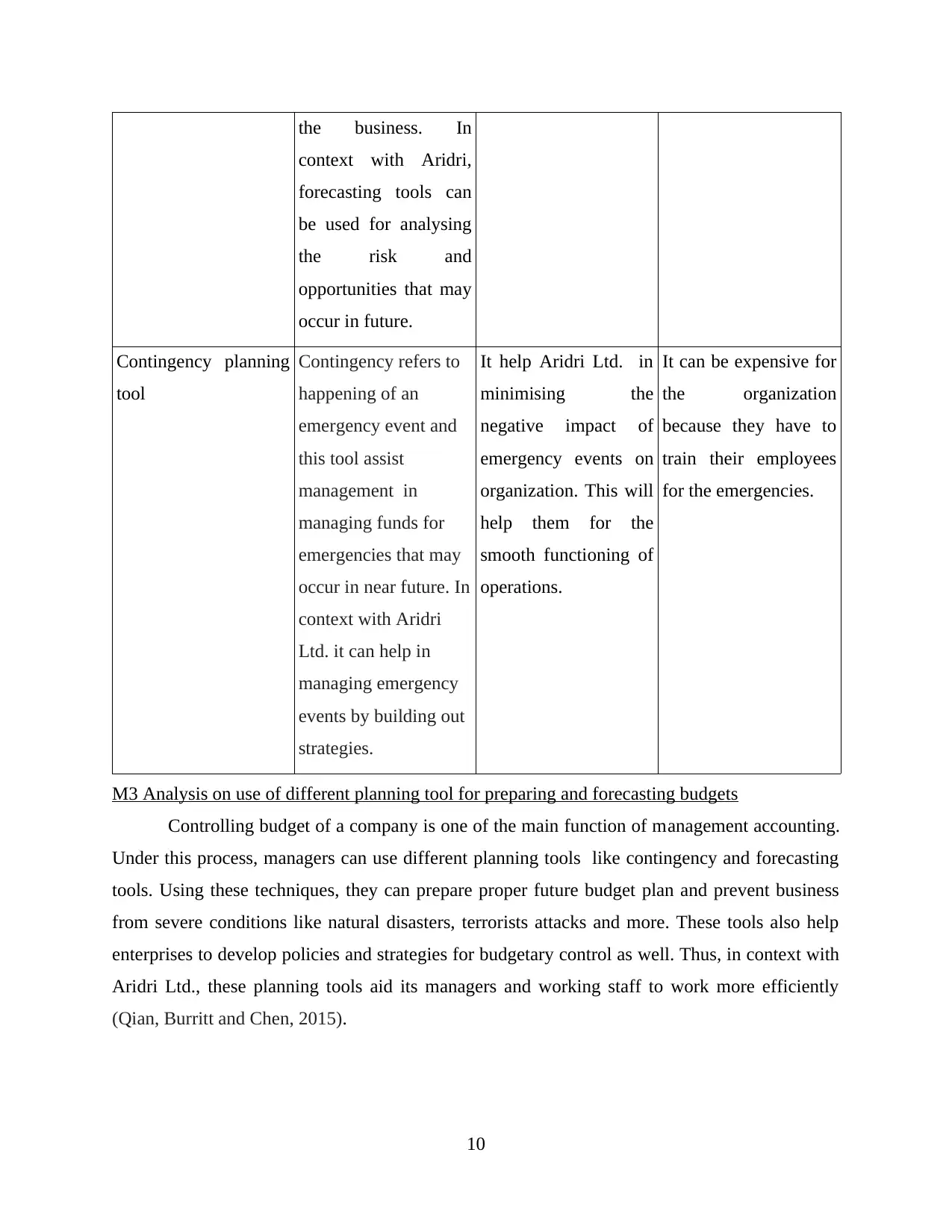

Contingency planning

tool

Contingency refers to

happening of an

emergency event and

this tool assist

management in

managing funds for

emergencies that may

occur in near future. In

context with Aridri

Ltd. it can help in

managing emergency

events by building out

strategies.

It help Aridri Ltd. in

minimising the

negative impact of

emergency events on

organization. This will

help them for the

smooth functioning of

operations.

It can be expensive for

the organization

because they have to

train their employees

for the emergencies.

M3 Analysis on use of different planning tool for preparing and forecasting budgets

Controlling budget of a company is one of the main function of management accounting.

Under this process, managers can use different planning tools like contingency and forecasting

tools. Using these techniques, they can prepare proper future budget plan and prevent business

from severe conditions like natural disasters, terrorists attacks and more. These tools also help

enterprises to develop policies and strategies for budgetary control as well. Thus, in context with

Aridri Ltd., these planning tools aid its managers and working staff to work more efficiently

(Qian, Burritt and Chen, 2015).

10

context with Aridri,

forecasting tools can

be used for analysing

the risk and

opportunities that may

occur in future.

Contingency planning

tool

Contingency refers to

happening of an

emergency event and

this tool assist

management in

managing funds for

emergencies that may

occur in near future. In

context with Aridri

Ltd. it can help in

managing emergency

events by building out

strategies.

It help Aridri Ltd. in

minimising the

negative impact of

emergency events on

organization. This will

help them for the

smooth functioning of

operations.

It can be expensive for

the organization

because they have to

train their employees

for the emergencies.

M3 Analysis on use of different planning tool for preparing and forecasting budgets

Controlling budget of a company is one of the main function of management accounting.

Under this process, managers can use different planning tools like contingency and forecasting

tools. Using these techniques, they can prepare proper future budget plan and prevent business

from severe conditions like natural disasters, terrorists attacks and more. These tools also help

enterprises to develop policies and strategies for budgetary control as well. Thus, in context with

Aridri Ltd., these planning tools aid its managers and working staff to work more efficiently

(Qian, Burritt and Chen, 2015).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.