Management Accounting Report: Pavestone Concrete Products Analysis

VerifiedAdded on 2020/12/10

|18

|5792

|349

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on its application within the context of Pavestone, a concrete product manufacturer. It defines management accounting and explores different types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. The report also examines various management accounting methods such as performance reporting and account receivable reports. Furthermore, it details the benefits of management accounting systems and their integration with organizational processes. The report then analyzes cost calculation techniques, including absorption costing, and discusses the advantages and disadvantages of different planning tools, such as budgetary control. Finally, it addresses how organizations adapt management accounting systems to respond to financial problems, providing a comprehensive overview of the subject.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Define management accounting and different types of management accounting systems ...3

P2 Different methods used for management accounting............................................................5

M1 Benefits of management accounting systems and their application ....................................6

D1 Management accounting systems and management accounting reporting is integrated.......7

TASK 2 ...........................................................................................................................................7

P3 Calculate costs by using appropriate techniques of cost analysis..........................................7

M2 Management accounting techniques and financial reporting documents.............................9

D2 Financial reports that accurately apply and interpret data...................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools....................................10

M3 Use of different planning tools and application for preparing and forecasting budgets.....12

D3 Tools for accounting respond appropriately to solving financial problems........................12

TASK 4..........................................................................................................................................12

P5 Organisations are adapting management accounting systems to respond to financial

problems ...................................................................................................................................12

M4 Responding to financial problems, management accounting.............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Define management accounting and different types of management accounting systems ...3

P2 Different methods used for management accounting............................................................5

M1 Benefits of management accounting systems and their application ....................................6

D1 Management accounting systems and management accounting reporting is integrated.......7

TASK 2 ...........................................................................................................................................7

P3 Calculate costs by using appropriate techniques of cost analysis..........................................7

M2 Management accounting techniques and financial reporting documents.............................9

D2 Financial reports that accurately apply and interpret data...................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools....................................10

M3 Use of different planning tools and application for preparing and forecasting budgets.....12

D3 Tools for accounting respond appropriately to solving financial problems........................12

TASK 4..........................................................................................................................................12

P5 Organisations are adapting management accounting systems to respond to financial

problems ...................................................................................................................................12

M4 Responding to financial problems, management accounting.............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a process of evaluating business and operational costs in order

to formulate internal financial report, accounts and records. This information aid managers in

decision making process for accomplishing firm's goals and objectives. Management accounting

encompasses with formulating and providing timely financial and statistical information to

management as they accomplish day to day operations. Furthermore, Management accounting

reports are also usually confidential and acquired for iinternal decision making process only

(Abugalia, 2011). The present assignment is based upon Pavestone which manufactures and

distribute concrete products for commercial, contractor, residential and retail consumer markets.

The firm also offers stone and brick paving products,, i.e. patio stones, concrete pavers, free

standing wall system etc. Apart from this, the present assignment is going to be described types

and methods of management accounting system. Various techniques of cost accounting which

helps to prepare an income statement will also discuss. Furthermore, readers will also come to

know about advantages and disadvantages of planning tools of budgetary control. There will be

discuss the role of management accounting system to respond towards financial problems.

TASK 1

P1 Define management accounting and different types of management accounting systems

Definition – Management accounting is a branch of accounting which provides critical or

necessary information to top management in a systematic way. It will assists to perform their all

operations and functional areas, i.e. planning, organising, directing as well as taking business

decisions in proper way.

In present corporative world, management accounting has become an essential part for

management. Its a process of developing managerial reports and statements in order to obtain

accurate financial information which is required to complete daily business operations as well as

take short term decisions (Basel, 2012). Management accounting supports to set performance

standards of company with actual outcomes; it also creates monthly and weekly reports for

internal people of an organisation, i.e. employees and managers. It determines, evaluate, assess,

interpret and communicate information which enable Pavestone to pursue its strategic goals and

objectives. Although, management accounting is differ from financial accounting, while

financial accounting render information to people inside and outside of the organisation whereas

Management accounting is a process of evaluating business and operational costs in order

to formulate internal financial report, accounts and records. This information aid managers in

decision making process for accomplishing firm's goals and objectives. Management accounting

encompasses with formulating and providing timely financial and statistical information to

management as they accomplish day to day operations. Furthermore, Management accounting

reports are also usually confidential and acquired for iinternal decision making process only

(Abugalia, 2011). The present assignment is based upon Pavestone which manufactures and

distribute concrete products for commercial, contractor, residential and retail consumer markets.

The firm also offers stone and brick paving products,, i.e. patio stones, concrete pavers, free

standing wall system etc. Apart from this, the present assignment is going to be described types

and methods of management accounting system. Various techniques of cost accounting which

helps to prepare an income statement will also discuss. Furthermore, readers will also come to

know about advantages and disadvantages of planning tools of budgetary control. There will be

discuss the role of management accounting system to respond towards financial problems.

TASK 1

P1 Define management accounting and different types of management accounting systems

Definition – Management accounting is a branch of accounting which provides critical or

necessary information to top management in a systematic way. It will assists to perform their all

operations and functional areas, i.e. planning, organising, directing as well as taking business

decisions in proper way.

In present corporative world, management accounting has become an essential part for

management. Its a process of developing managerial reports and statements in order to obtain

accurate financial information which is required to complete daily business operations as well as

take short term decisions (Basel, 2012). Management accounting supports to set performance

standards of company with actual outcomes; it also creates monthly and weekly reports for

internal people of an organisation, i.e. employees and managers. It determines, evaluate, assess,

interpret and communicate information which enable Pavestone to pursue its strategic goals and

objectives. Although, management accounting is differ from financial accounting, while

financial accounting render information to people inside and outside of the organisation whereas

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management accounting aimed is to assist managers inside the organisation as they can take

make or buy decisions.

Furthermore, management accounting also helps in forecasting or predictions regarding

investments, diversification into market segments and make or buy decisions. This implies to

make forecast about future trends within business. It is essential for management to make

predictions toward cash flows and recognise its impact upon company's operation's in future.

Management accounting comprises with formulation of budgets and trend charts so that

managers can decide how to allocate resources

Information provided through management accounting is changes in stock, raw material,

financial data and then analysis the entire information in order to make imperative

business decisions (Management Accounting, 2015).

Management accounting system are effective and flexible in nature for obtaining accurate

data and information. It will be beneficial for Pavestone to accomplish all operations and

working activities in fast and accurate manner.

This accounting practice is also beneficial for staff members of the company as they

continuously get aware with financial position of the company at market-place. This

helps them to work for obtaining firm's goals and objectives.

Types of accounting system

Cost accounting system- This accounting system is beneficial for companies to evaluate

estimated product costs with the assistance of using profitability analysis, valuation and cost

control approach. Along with this, cost accounting system is acquired by manufactures thus to

keep track of production activities by using a perpetual inventory system. It helps to determine

flow of inventory in business organisation in different stages of production. In context of

Pavestone, cost accounting system aids to estimate the cost of their products for conducting

profitability analysis, inventory valuation and cost control. There are different types of cost

accounting methods, such as – job order costing, process costing, activity based costing system

etc.

Inventory management system – This management accounting system helps to keep

track of goods by evaluating entire supply chain in which a business operates. It covers all

aspects from manufacturing to retail, movements of stock one place to another and warehousing

to shipping. It allows to make better decisions and investments. Two main tools of inventory

make or buy decisions.

Furthermore, management accounting also helps in forecasting or predictions regarding

investments, diversification into market segments and make or buy decisions. This implies to

make forecast about future trends within business. It is essential for management to make

predictions toward cash flows and recognise its impact upon company's operation's in future.

Management accounting comprises with formulation of budgets and trend charts so that

managers can decide how to allocate resources

Information provided through management accounting is changes in stock, raw material,

financial data and then analysis the entire information in order to make imperative

business decisions (Management Accounting, 2015).

Management accounting system are effective and flexible in nature for obtaining accurate

data and information. It will be beneficial for Pavestone to accomplish all operations and

working activities in fast and accurate manner.

This accounting practice is also beneficial for staff members of the company as they

continuously get aware with financial position of the company at market-place. This

helps them to work for obtaining firm's goals and objectives.

Types of accounting system

Cost accounting system- This accounting system is beneficial for companies to evaluate

estimated product costs with the assistance of using profitability analysis, valuation and cost

control approach. Along with this, cost accounting system is acquired by manufactures thus to

keep track of production activities by using a perpetual inventory system. It helps to determine

flow of inventory in business organisation in different stages of production. In context of

Pavestone, cost accounting system aids to estimate the cost of their products for conducting

profitability analysis, inventory valuation and cost control. There are different types of cost

accounting methods, such as – job order costing, process costing, activity based costing system

etc.

Inventory management system – This management accounting system helps to keep

track of goods by evaluating entire supply chain in which a business operates. It covers all

aspects from manufacturing to retail, movements of stock one place to another and warehousing

to shipping. It allows to make better decisions and investments. Two main tools of inventory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management system are – Just in time approach and EOQ (economic order quantity.

Furthermore, inventory management system is a combination of technology and processes which

oversee in monitoring and maintenance of stock of the company.

Job costing approach – The system is tend towards accumulating information about

costs linked with production or service job. This kind of information is needed to submit in cost

reimbursement contract. In addition to this, job costing system is an excellent tool which tracks

specific costs required to perform a job and examine them whether or not these costs can be

reduced later (Christopher, 2016). The approach provides information regarding following

accounting activities – materials, labour and overhead.

Price optimisation system- It is an activity in which companies determine how to

maximise prices of products to which consumers are willing to pay. While optimising prices, it

is essential to find out a perfect balance between profit and value cause values of products and

services are changing at fast pace. Price optimisation system has acquired by Pavestone in order

to select an effective price of its products which also covers entire production cost and provide

huge financial benefits to company.

P2 Different methods used for management accounting

In context of small business organisations, management accounting system allows

companies to recognise their existing financial position and take corporative decisions

accordingly. Management accounting deals with the future and is futuristic in approach, while it

focuses on forecasting and decision-making. It is prime obligation of top management to disclose

financial records among employees as they work to obtain firm's goals and objectives.

Management accounting also prepare and deliver information to managers of Pavestone as they

can take short term or daily basis business decisions. In addition to this, management accountants

are placed to render information which enable to meet changing needs of managerial functions

(Ding, Dekker and Groot, 2013). This succession supports company to review the accounting

information which facilitate planning process.

There are several types of management accounting systems which allows management of

Pavestone to track necessary information about company. Following is defined various methods

of management accounting which are stated as under -

Performance reporting system : It is one of the important method of management

accounting which linked with project communication management. Performance reporting

Furthermore, inventory management system is a combination of technology and processes which

oversee in monitoring and maintenance of stock of the company.

Job costing approach – The system is tend towards accumulating information about

costs linked with production or service job. This kind of information is needed to submit in cost

reimbursement contract. In addition to this, job costing system is an excellent tool which tracks

specific costs required to perform a job and examine them whether or not these costs can be

reduced later (Christopher, 2016). The approach provides information regarding following

accounting activities – materials, labour and overhead.

Price optimisation system- It is an activity in which companies determine how to

maximise prices of products to which consumers are willing to pay. While optimising prices, it

is essential to find out a perfect balance between profit and value cause values of products and

services are changing at fast pace. Price optimisation system has acquired by Pavestone in order

to select an effective price of its products which also covers entire production cost and provide

huge financial benefits to company.

P2 Different methods used for management accounting

In context of small business organisations, management accounting system allows

companies to recognise their existing financial position and take corporative decisions

accordingly. Management accounting deals with the future and is futuristic in approach, while it

focuses on forecasting and decision-making. It is prime obligation of top management to disclose

financial records among employees as they work to obtain firm's goals and objectives.

Management accounting also prepare and deliver information to managers of Pavestone as they

can take short term or daily basis business decisions. In addition to this, management accountants

are placed to render information which enable to meet changing needs of managerial functions

(Ding, Dekker and Groot, 2013). This succession supports company to review the accounting

information which facilitate planning process.

There are several types of management accounting systems which allows management of

Pavestone to track necessary information about company. Following is defined various methods

of management accounting which are stated as under -

Performance reporting system : It is one of the important method of management

accounting which linked with project communication management. Performance reporting

system entails with collecting and disseminating schemes, data, demonstration of future growth,

optimal utilisation of available resources and prepare an ongoing project plan. An annual

performance report will help Pavestone to identify performance of each employee. It aids top

management to evaluate whether or not staff members are working in right direction for a given

project. It is used to compilation of working activities thus to obtain strategic objectives in a

given time period.

Inventory management report: - It is based upon measuring entire supervision of non-

capitalised inventory and products. Inventory management report is made to control upon stocks

which are undertaken by companies. The report is prepared in the end of financial year and

disclose opening and closing account balance of the company. In other words, it often provides a

brief description about inventory account or supply of products in a same time period which

makes easier to understand for managers to take future business decisions (Edwards, 2013).

Furthermore, different tools or techniques are taken into account for valuing stock, such as –

EOQ, Inventory turnover ratio and ABC costing. In Pavestore, inventory management report will

ensure availability of materials in sufficient amount whensoever it is needed, thus to produce in

an effective and efficient manner.

Account receivable report: The report has made upon periodic basis and classified

overall accounting report of the company as per the range of outstanding invoices. Account

receivable reports aids to determine overall financial position of Pavestone thus to make

effective investment decisions. It can be done through primary tools which allows to collect

unpaid invoices from debtors. Accounting receivable report is used by top management in order

to identify efficiency of credits and collection functions. It can be used as a tool for estimating

potential bad debts, which are then used to revise the allowance for doubtful accounts.

M1 Benefits of management accounting systems and their application

Management accounting system Benefits

Cost accounting system It helps in give the economic

development as well as financial

stability.

It eliminate losses, inefficiencies and

wastes.

optimal utilisation of available resources and prepare an ongoing project plan. An annual

performance report will help Pavestone to identify performance of each employee. It aids top

management to evaluate whether or not staff members are working in right direction for a given

project. It is used to compilation of working activities thus to obtain strategic objectives in a

given time period.

Inventory management report: - It is based upon measuring entire supervision of non-

capitalised inventory and products. Inventory management report is made to control upon stocks

which are undertaken by companies. The report is prepared in the end of financial year and

disclose opening and closing account balance of the company. In other words, it often provides a

brief description about inventory account or supply of products in a same time period which

makes easier to understand for managers to take future business decisions (Edwards, 2013).

Furthermore, different tools or techniques are taken into account for valuing stock, such as –

EOQ, Inventory turnover ratio and ABC costing. In Pavestore, inventory management report will

ensure availability of materials in sufficient amount whensoever it is needed, thus to produce in

an effective and efficient manner.

Account receivable report: The report has made upon periodic basis and classified

overall accounting report of the company as per the range of outstanding invoices. Account

receivable reports aids to determine overall financial position of Pavestone thus to make

effective investment decisions. It can be done through primary tools which allows to collect

unpaid invoices from debtors. Accounting receivable report is used by top management in order

to identify efficiency of credits and collection functions. It can be used as a tool for estimating

potential bad debts, which are then used to revise the allowance for doubtful accounts.

M1 Benefits of management accounting systems and their application

Management accounting system Benefits

Cost accounting system It helps in give the economic

development as well as financial

stability.

It eliminate losses, inefficiencies and

wastes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system It aids in determine cost of production.

There is no under or over overheads

recovery (Stergiou, Ashraf and Uddin,

2013).

D1 Management accounting systems and management accounting reporting is integrated

Pavestone company uses the different kinds of management accounting system and also

its reporting for the better planning as well as control to enhance the profit level. This

organisation use its necessary resources in a manner that it they can deal with any kind of

unpredictable events which can develop the negative affect on performance level of business.

Pavestone business firm use this system to control the cost and focus on the target the new

consumers.

Type of reporting Integration with organisational process

Job costing This will help in identification of overall cost

associated with products and services provided

by organisation. This will aid in reduction of

expenses.

Inventory management system This will aid organisation to effectively

manage their stocks for their optimum

utilisation and to attainment of optimum results

TASK 2

P3 Calculate costs by using appropriate techniques of cost analysis

Costs refer with value of amount which is being paid by an individual for getting

something. While production, managers are required a wide range of raw materials and other

inputs from several suppliers in order to produce new and innovative products. Costs is one of

the key factor to perform all business functions or operations in systematic manner. In Pavestone,

cost includes all necessary amount in order to get an asset in place and ready for use. For

example, the cost of an item in inventory also includes the item's freight-in cost. Along with this,

in accounting terms costs consists with monetary value of expenditures for equipments, inputs,

There is no under or over overheads

recovery (Stergiou, Ashraf and Uddin,

2013).

D1 Management accounting systems and management accounting reporting is integrated

Pavestone company uses the different kinds of management accounting system and also

its reporting for the better planning as well as control to enhance the profit level. This

organisation use its necessary resources in a manner that it they can deal with any kind of

unpredictable events which can develop the negative affect on performance level of business.

Pavestone business firm use this system to control the cost and focus on the target the new

consumers.

Type of reporting Integration with organisational process

Job costing This will help in identification of overall cost

associated with products and services provided

by organisation. This will aid in reduction of

expenses.

Inventory management system This will aid organisation to effectively

manage their stocks for their optimum

utilisation and to attainment of optimum results

TASK 2

P3 Calculate costs by using appropriate techniques of cost analysis

Costs refer with value of amount which is being paid by an individual for getting

something. While production, managers are required a wide range of raw materials and other

inputs from several suppliers in order to produce new and innovative products. Costs is one of

the key factor to perform all business functions or operations in systematic manner. In Pavestone,

cost includes all necessary amount in order to get an asset in place and ready for use. For

example, the cost of an item in inventory also includes the item's freight-in cost. Along with this,

in accounting terms costs consists with monetary value of expenditures for equipments, inputs,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

labour, products, supplies etc. Costs is an amount which recorded as an expense in financial

statements (Henri, Boiral and Roy, 2016).

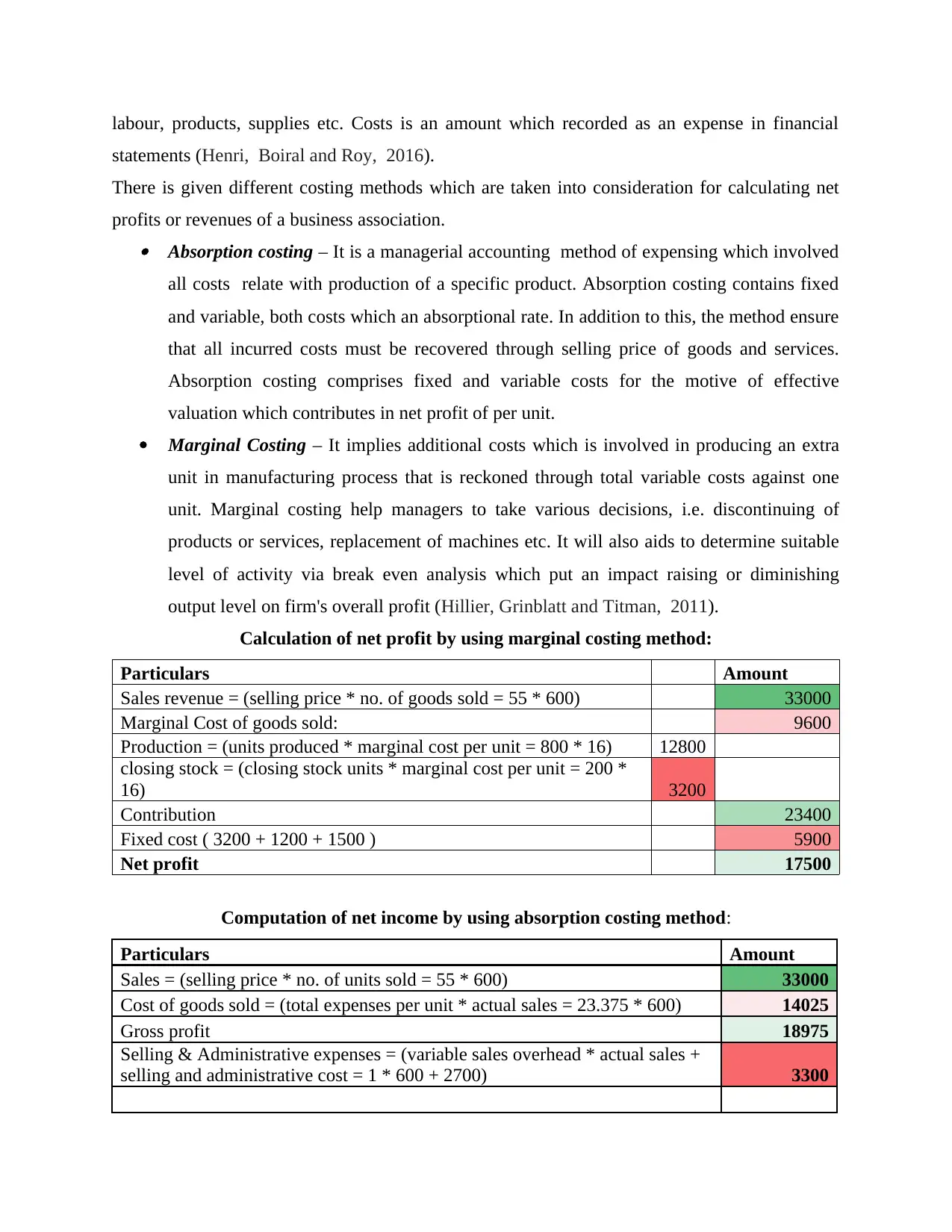

There is given different costing methods which are taken into consideration for calculating net

profits or revenues of a business association. Absorption costing – It is a managerial accounting method of expensing which involved

all costs relate with production of a specific product. Absorption costing contains fixed

and variable, both costs which an absorptional rate. In addition to this, the method ensure

that all incurred costs must be recovered through selling price of goods and services.

Absorption costing comprises fixed and variable costs for the motive of effective

valuation which contributes in net profit of per unit.

Marginal Costing – It implies additional costs which is involved in producing an extra

unit in manufacturing process that is reckoned through total variable costs against one

unit. Marginal costing help managers to take various decisions, i.e. discontinuing of

products or services, replacement of machines etc. It will also aids to determine suitable

level of activity via break even analysis which put an impact raising or diminishing

output level on firm's overall profit (Hillier, Grinblatt and Titman, 2011).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

statements (Henri, Boiral and Roy, 2016).

There is given different costing methods which are taken into consideration for calculating net

profits or revenues of a business association. Absorption costing – It is a managerial accounting method of expensing which involved

all costs relate with production of a specific product. Absorption costing contains fixed

and variable, both costs which an absorptional rate. In addition to this, the method ensure

that all incurred costs must be recovered through selling price of goods and services.

Absorption costing comprises fixed and variable costs for the motive of effective

valuation which contributes in net profit of per unit.

Marginal Costing – It implies additional costs which is involved in producing an extra

unit in manufacturing process that is reckoned through total variable costs against one

unit. Marginal costing help managers to take various decisions, i.e. discontinuing of

products or services, replacement of machines etc. It will also aids to determine suitable

level of activity via break even analysis which put an impact raising or diminishing

output level on firm's overall profit (Hillier, Grinblatt and Titman, 2011).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

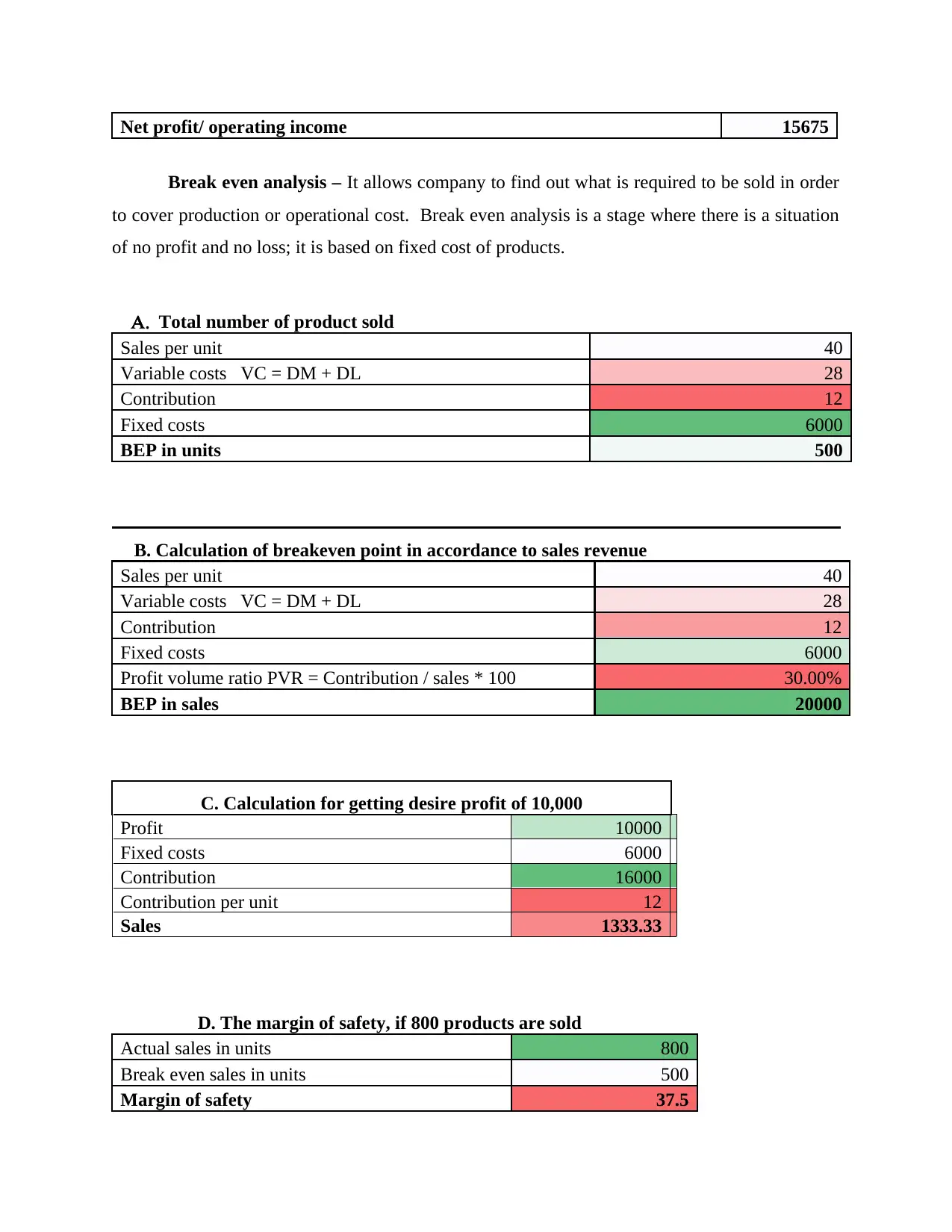

Net profit/ operating income 15675

Break even analysis – It allows company to find out what is required to be sold in order

to cover production or operational cost. Break even analysis is a stage where there is a situation

of no profit and no loss; it is based on fixed cost of products.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Break even analysis – It allows company to find out what is required to be sold in order

to cover production or operational cost. Break even analysis is a stage where there is a situation

of no profit and no loss; it is based on fixed cost of products.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Margin of Safety – It represents difference between actual sales and BEP sale. Margin of

safety implies to reduction of sales which occurs before getting break even point. It also define

differentiation between market and internal value of products. Here, Margin of safety is 37.5.

M2 Management accounting techniques and financial reporting documents

Different kinds of accounting techniques are mention below which are used through

Pavestone organisation:

Marginal costing- It refers to decrease and increase in total manufacturing cost rune for

make the additional unit of products (Schäffer, 2013). Under this, output costs consists labour,

variable overheads and direct material.

Standard costing- These are used as the target costs and developed from analysis of

historical data.

Historical costing- It refers to original asset cost that is recorded in accounting

transaction of an organisation.

D2 Financial reports that accurately apply and interpret data

On the basis of calculation, it has been clear that method of marginal costing will more

effective as comparison to the absorption costing. At the time of calculate net profit through

marginal costing, result was £17500 and result of absorption costing method was £15675.

Difference among both method profit is £9600 because of modifications in the variable cost

(Talha, Raja and Seetharaman, 2017).

TASK 3

P4 Advantages and disadvantages of different types of planning tools

Budgetary control refers to system of the management control under which actual income

as well as spending are compare with the planned spending and income. Under this, manager use

the budgets to control and also monitor the operations and costs in mention accounting period. It

is a procedure for management to decide the performance along with financial goals related

budgets, compare actual budgets and also adjust performance (Mat, Smith and Djajadikerta,

2016). Budgetary control is helpful in control the cost that consists develop of budgets,

establishing responsibilities, coordinating departments, compare the actual performance with

budgeted and also act on outcomes to attain the more profit level. The main aim of budgetary

safety implies to reduction of sales which occurs before getting break even point. It also define

differentiation between market and internal value of products. Here, Margin of safety is 37.5.

M2 Management accounting techniques and financial reporting documents

Different kinds of accounting techniques are mention below which are used through

Pavestone organisation:

Marginal costing- It refers to decrease and increase in total manufacturing cost rune for

make the additional unit of products (Schäffer, 2013). Under this, output costs consists labour,

variable overheads and direct material.

Standard costing- These are used as the target costs and developed from analysis of

historical data.

Historical costing- It refers to original asset cost that is recorded in accounting

transaction of an organisation.

D2 Financial reports that accurately apply and interpret data

On the basis of calculation, it has been clear that method of marginal costing will more

effective as comparison to the absorption costing. At the time of calculate net profit through

marginal costing, result was £17500 and result of absorption costing method was £15675.

Difference among both method profit is £9600 because of modifications in the variable cost

(Talha, Raja and Seetharaman, 2017).

TASK 3

P4 Advantages and disadvantages of different types of planning tools

Budgetary control refers to system of the management control under which actual income

as well as spending are compare with the planned spending and income. Under this, manager use

the budgets to control and also monitor the operations and costs in mention accounting period. It

is a procedure for management to decide the performance along with financial goals related

budgets, compare actual budgets and also adjust performance (Mat, Smith and Djajadikerta,

2016). Budgetary control is helpful in control the cost that consists develop of budgets,

establishing responsibilities, coordinating departments, compare the actual performance with

budgeted and also act on outcomes to attain the more profit level. The main aim of budgetary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

control is to eliminate the wastage and enhance the profitability. It assures planning for the future

through setting up different budgets, expected and needed performance of company that are to be

anticipated. In addition to this, it is continuous procedure that helps in coordination and also

planning. It gives method to control the budget in an effective and better manner. It is planned to

help management for allocation of authority and responsibilities to help in preparing plans and

estimation for future context. In Pavestone company, budgetary control needs expenditure of

money, effort and time. So, it is not easy to make the different types of budgets in company due

to complexities arise in forecasting the budgeting. There are various kinds of planning tools

which are used in budgetary control mention below:

Contingency tool- It is use through Pavestone company to prepare any kind of possible

events which can occur in future. It is executed through company in order to identify the future

risk that have some possibility to be occur (Salehi, Rostami and Mogadam, 2013). This planning

tools helps in deal with any kind of issues which arise in the future. In addition to this,

contingency tool is used to know about outcomes of plans which are implemented through

company on sudden basis.

Advantages Disadvantages

IT helps in distributing the liabilities

between staff members for their each

work.

It aids management of Pavestone

organisation to prepared for any kind of

uncertainty.

This planning tool is rigid in nature and

it works slow if there is need to make

changes in trends..

It is costly planning tool and each

organisations are not able to use and

apply this tool.

Forecasting tools- Forecasting begin with the certain assumptions depends on

experience, judgement and knowledge of management. It helps in forecast the data and

information related to budget. This planning tool facilitated management of Pavestone company

in its attempts to deal with risk of future based on the primary data from previous experience and

also current trends analysis (Schäffer, 2013). In context to this, forecasting planning tools used to

identify the demand of consumers about goods and services in future context of company.

Advantages Disadvantages

through setting up different budgets, expected and needed performance of company that are to be

anticipated. In addition to this, it is continuous procedure that helps in coordination and also

planning. It gives method to control the budget in an effective and better manner. It is planned to

help management for allocation of authority and responsibilities to help in preparing plans and

estimation for future context. In Pavestone company, budgetary control needs expenditure of

money, effort and time. So, it is not easy to make the different types of budgets in company due

to complexities arise in forecasting the budgeting. There are various kinds of planning tools

which are used in budgetary control mention below:

Contingency tool- It is use through Pavestone company to prepare any kind of possible

events which can occur in future. It is executed through company in order to identify the future

risk that have some possibility to be occur (Salehi, Rostami and Mogadam, 2013). This planning

tools helps in deal with any kind of issues which arise in the future. In addition to this,

contingency tool is used to know about outcomes of plans which are implemented through

company on sudden basis.

Advantages Disadvantages

IT helps in distributing the liabilities

between staff members for their each

work.

It aids management of Pavestone

organisation to prepared for any kind of

uncertainty.

This planning tool is rigid in nature and

it works slow if there is need to make

changes in trends..

It is costly planning tool and each

organisations are not able to use and

apply this tool.

Forecasting tools- Forecasting begin with the certain assumptions depends on

experience, judgement and knowledge of management. It helps in forecast the data and

information related to budget. This planning tool facilitated management of Pavestone company

in its attempts to deal with risk of future based on the primary data from previous experience and

also current trends analysis (Schäffer, 2013). In context to this, forecasting planning tools used to

identify the demand of consumers about goods and services in future context of company.

Advantages Disadvantages

It gives reliable as well as accurate data

or information to managers which aids

them in the process of decision making.

Forecasting tool of planning assures

increase use of necessary resources

through identify the weak business

area.

It is not necessary that it will provide

the accurate results.

It is complicated or complex planning

tool.

Scenario tools- This planning tool is used to evaluate the possible future issue and

consequences through including the better possible outcomes (Sharma, Lawrence and Lowe,

2013). It is mainly executed through company to estimate the modifications in position of an

organisation at the market place. Under this, manager of Pavestone firm use this planning tool in

the process of decision making to identify better way to increase profit level for business.

Advantages Disadvantages

Scenario tool of planning is used

through the financial planners of

company in order to deal with the

future crisis.

Scenario tool is used to create the

external information and data of

company that aid in decision making.

There are different complexities are

faced by company at the time of

executing the scenario planning tool at

workplace.

In context to implement this tool, there

is more time and cost required. But

Pavaestone is small size company so it

has minimum cost for hire staff

members for specific analysis.

M3 Use of different planning tools and application for preparing and forecasting budgets

Planning tools are used through Pavestone company to identify the different factors such

as demand or needs of consumers and also prepare for the future financial crisis. The different

planning tools helps in the budgetary control and also provide the reliable data on the basis of

previous data as well as future trends.

or information to managers which aids

them in the process of decision making.

Forecasting tool of planning assures

increase use of necessary resources

through identify the weak business

area.

It is not necessary that it will provide

the accurate results.

It is complicated or complex planning

tool.

Scenario tools- This planning tool is used to evaluate the possible future issue and

consequences through including the better possible outcomes (Sharma, Lawrence and Lowe,

2013). It is mainly executed through company to estimate the modifications in position of an

organisation at the market place. Under this, manager of Pavestone firm use this planning tool in

the process of decision making to identify better way to increase profit level for business.

Advantages Disadvantages

Scenario tool of planning is used

through the financial planners of

company in order to deal with the

future crisis.

Scenario tool is used to create the

external information and data of

company that aid in decision making.

There are different complexities are

faced by company at the time of

executing the scenario planning tool at

workplace.

In context to implement this tool, there

is more time and cost required. But

Pavaestone is small size company so it

has minimum cost for hire staff

members for specific analysis.

M3 Use of different planning tools and application for preparing and forecasting budgets

Planning tools are used through Pavestone company to identify the different factors such

as demand or needs of consumers and also prepare for the future financial crisis. The different

planning tools helps in the budgetary control and also provide the reliable data on the basis of

previous data as well as future trends.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.