Analysis of Management Accounting Systems and Costing Methods Report

VerifiedAdded on 2020/02/12

|18

|6164

|54

Report

AI Summary

This report delves into the realm of management accounting, offering a comprehensive analysis tailored for Agmet Metals. It begins with an introduction to management accounting, emphasizing its role in financial data analysis and its significance in guiding business decisions. The report then explores various management accounting systems, including cost accounting and inventory management, highlighting their requirements and benefits. Furthermore, it examines different reporting methods such as cash flow analysis, fund flow analysis, financial planning, ratio analysis, and operating budget reports, providing insights into their applications within an organization. The report also covers topics like bills receivable reports and performance reports, essential for evaluating departmental performance. Throughout, the report underscores the importance of these tools in enhancing decision-making, cost reduction, and overall business strategy, making it a valuable resource for understanding and implementing effective management accounting practices.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explanation of management accounting and requirements of different types of

management accounting systems...........................................................................................3

P2 Explanation of different methods used for management accounting reporting................5

TASK.2 ...........................................................................................................................................7

P.3 Computation of net profit using absorption costing and marginal costing techniques....7

TASK.3..........................................................................................................................................11

P.4 Similarities and dissimilarities of different types of planning tools used for budgetary

control:..................................................................................................................................11

TASK.4..........................................................................................................................................13

P.5 Management accounting systems to respond to financial problems:.............................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explanation of management accounting and requirements of different types of

management accounting systems...........................................................................................3

P2 Explanation of different methods used for management accounting reporting................5

TASK.2 ...........................................................................................................................................7

P.3 Computation of net profit using absorption costing and marginal costing techniques....7

TASK.3..........................................................................................................................................11

P.4 Similarities and dissimilarities of different types of planning tools used for budgetary

control:..................................................................................................................................11

TASK.4..........................................................................................................................................13

P.5 Management accounting systems to respond to financial problems:.............................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a method which used in the financial data and also to give an

advise for the user company to develop their business activities (Lukka and Modell, 2010). This

is an accounting systems which can help to the company to make a better business activities as

per this accounting system. Organisation have to use this accounting method which can help to

them to collect and analyse the data related to the financial and operational activities of the

business. Management accounting reports are based on the management related data and it is

having focus to improve their managerial decisions which can help to the company to reduce

their internal cost. It has a potential top provide an appropriate data which can be used by the

organisation management to make a better decision and planning. Management accounting is

having an important role in the organisation which can help to the company to make a better

planning and staffing of the employees by which they can make a better position in the targetted

market. This present report is based on the Agmet working in the manufacturing in chemical

manufacturing industry (Luft and Shields, 2010). The below mentioned report is having different

types of management accounting system, different methods to use it the organisation and

advantage and disadvantages of the management accounting system.

TASK 1

P1 Explanation of management accounting and requirements of different types of management

accounting systems

Management accounting is a method which used in the financial data and also to give an

advise for the user company to develop their business activities (Lukka and Modell, 2010). This

is an accounting systems which can help to the company to make a better business activities as

per this accounting system. Organisation have to use this accounting method which can help to

them to collect and analyse the data related to the financial and operational activities of the

business. Management accounting reports are based on the management related data and it is

having focus to improve their managerial decisions which can help to the company to reduce

their internal cost. It has a potential top provide an appropriate data which can be used by the

organisation management to make a better decision and planning. Management accounting is

having an important role in the organisation which can help to the company to make a better

planning and staffing of the employees by which they can make a better position in the targetted

market. This present report is based on the Agmet working in the manufacturing in chemical

manufacturing industry (Luft and Shields, 2010). The below mentioned report is having different

types of management accounting system, different methods to use it the organisation and

advantage and disadvantages of the management accounting system.

TASK 1

P1 Explanation of management accounting and requirements of different types of management

accounting systems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To,

General Manager,

Agmet Metals,

Subject: A report to general manager for management accounting systems and suggesting to

adopt suitable costing techniques for the company. This report will provide details upon

different costing methods and please select a best one for the organisation according to you.

As Agmet is working in the manufacturing industry it is having a huge need of

management accounting systems which can help to the company to deal better with the

situations. Management accounting is a combination of the accounting, finance and

management data to enhance the potentials of the organisation to make a better decisions for the

work force. Simply it is a concept which works on the financial and non financial data which

can help to the company to make a better position in the targeted market. Managers which are

working in the organisation has to use management accounting system by which they can

increase their decision making abilities which are related to the employees and staffing. It help

to the company to make a better strategy and as well as to implement and formulate these

strategies in to the management (Lee, 2011). Basically management accounting systems works

on the work force by which company can make a better work adjustments as per the targets of

the company. As the Agmet is using the management accounting system bin their internal

management which help to them to make a better staffing of the employees to increase the

production and as well as productivity of the people working in the organisation. But it has a

huge need of the data related to the production, performance and finance to make adjustment

according to the target of the company in the management (Kaplan and Atkinson, 2015).

Centralise data can help to the management to make best solutions on the problems which they

are facing in the internal organisation. Management accounting is having different accounting

system which can help to the company to make better strategies:

Cost accounting system: It is an accounting system which works on the cost of the raw

materials, production process and inventory which they can have in the company. It can help to

the company to make a record of the particular factors which are having a significant

investment of the financial sources and as well as it help to the company to make a proper

pricing of the products which they are selling in the market (Jansen, 2011). As the Agmet is

working in the chemical manufacturing so they have to use this system in the company to make

General Manager,

Agmet Metals,

Subject: A report to general manager for management accounting systems and suggesting to

adopt suitable costing techniques for the company. This report will provide details upon

different costing methods and please select a best one for the organisation according to you.

As Agmet is working in the manufacturing industry it is having a huge need of

management accounting systems which can help to the company to deal better with the

situations. Management accounting is a combination of the accounting, finance and

management data to enhance the potentials of the organisation to make a better decisions for the

work force. Simply it is a concept which works on the financial and non financial data which

can help to the company to make a better position in the targeted market. Managers which are

working in the organisation has to use management accounting system by which they can

increase their decision making abilities which are related to the employees and staffing. It help

to the company to make a better strategy and as well as to implement and formulate these

strategies in to the management (Lee, 2011). Basically management accounting systems works

on the work force by which company can make a better work adjustments as per the targets of

the company. As the Agmet is using the management accounting system bin their internal

management which help to them to make a better staffing of the employees to increase the

production and as well as productivity of the people working in the organisation. But it has a

huge need of the data related to the production, performance and finance to make adjustment

according to the target of the company in the management (Kaplan and Atkinson, 2015).

Centralise data can help to the management to make best solutions on the problems which they

are facing in the internal organisation. Management accounting is having different accounting

system which can help to the company to make better strategies:

Cost accounting system: It is an accounting system which works on the cost of the raw

materials, production process and inventory which they can have in the company. It can help to

the company to make a record of the particular factors which are having a significant

investment of the financial sources and as well as it help to the company to make a proper

pricing of the products which they are selling in the market (Jansen, 2011). As the Agmet is

working in the chemical manufacturing so they have to use this system in the company to make

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a proper analysis of the different stages of the process to reduce the cost of the products and

increase their profitability in the production. This accounting system is having requirement of

the data related to the cost of each of the production level and as well as variable overheads

which has to counted in the pricing of the products.

Inventory management: It is an essential management system which is normally used by the

manufacturing and retailer companies to manage their stock level and inventory. It is

controllable by the computer software which help to the company to make a proper

management of the products which they are having in the stock(Talha, Raja and Seetharaman,

2010). It can support to the Agment to make a management in the stock, which stock has to be

sale in to the market and as well as to manage the stock level in the inventory to reduce the

contingencies and risk of the lack of stock for future needs (Hiebl, 2014). This accounting

system is having need of the details of the stock which can help to the company to make

adjustments in the production as per the market demands and accomplish to supply in the

market.

These accounting system can help to the company to price optimization which can help

to the company to make more profits and as well as they can reduce their prices which can

make a positive impact on their sales of the products in to the targeted market.

P2 Explanation of different methods used for management accounting reporting

Management accounting report is a detailed data sheet which explains the sources of

informations which can help to the company to run business in smoother manner. It is a business

document which shows that company is working in profits and loss. Agmet has to use

management accounting reports by which they can make a better decisions about unused units

which are creating a financial pressure on the organisation. Agmet can make it's management

accounting reports on quarterly basis which can help to them to show their status and also

explain participation of different departments in the success of business. Company can make

these kind of reports in the middle level of management because they are having a direct report

from their subordinates managers by their computerized reporting system.

Each and every organisation gas made management accounting reports which help to

them to evaluate their own performance in the targeted market and as well as it supports to them

to make adjustments in to their business activities. These reports are made by the organisation on

increase their profitability in the production. This accounting system is having requirement of

the data related to the cost of each of the production level and as well as variable overheads

which has to counted in the pricing of the products.

Inventory management: It is an essential management system which is normally used by the

manufacturing and retailer companies to manage their stock level and inventory. It is

controllable by the computer software which help to the company to make a proper

management of the products which they are having in the stock(Talha, Raja and Seetharaman,

2010). It can support to the Agment to make a management in the stock, which stock has to be

sale in to the market and as well as to manage the stock level in the inventory to reduce the

contingencies and risk of the lack of stock for future needs (Hiebl, 2014). This accounting

system is having need of the details of the stock which can help to the company to make

adjustments in the production as per the market demands and accomplish to supply in the

market.

These accounting system can help to the company to price optimization which can help

to the company to make more profits and as well as they can reduce their prices which can

make a positive impact on their sales of the products in to the targeted market.

P2 Explanation of different methods used for management accounting reporting

Management accounting report is a detailed data sheet which explains the sources of

informations which can help to the company to run business in smoother manner. It is a business

document which shows that company is working in profits and loss. Agmet has to use

management accounting reports by which they can make a better decisions about unused units

which are creating a financial pressure on the organisation. Agmet can make it's management

accounting reports on quarterly basis which can help to them to show their status and also

explain participation of different departments in the success of business. Company can make

these kind of reports in the middle level of management because they are having a direct report

from their subordinates managers by their computerized reporting system.

Each and every organisation gas made management accounting reports which help to

them to evaluate their own performance in the targeted market and as well as it supports to them

to make adjustments in to their business activities. These reports are made by the organisation on

the basis of the different time durations like; daily, weekly, monthly, quarterly and yearly to

make an analysis of the management, accounting and financial data of the company. Different

types of management accounting reports are here which can be used by the Agmet:

Cash Flow analysis: This is a statement in which cash transactions covered, it is divided in to

three sections which are operating activity, investing activity, financial activity. In these section

of the cash flow statement Agmet has to analyse the cash inflow and cash outflow from the

business (Håkansson, Kraus and Lind, 2010). As the company is working in the chemical

manufacturing and selling so product sale has to be covered in to the operating activities and

return on the investment has to be covered in to the investing and cash inflow and outflow from

the financial sources covered in to the last one.

Fund flow analysis: It is used by the management of the Agmet by which they can make better

working in the organisation by analysing the use of funds which are available for them. It help to

the company to make an analysis of the sources where they can arise financial funds and as well

as it can help to the company to make an appropriate analysis of the points in which they are

investing their financial funds. It can help to the company to make a profitability level in to the

organisation by making a proper analysis of these sources and consumption of the finance.

Financial planning: It is an essential tool for the managers of the Agmet to make proper

planning of the investment and as well as arise finance for the future project. So the Agmet has

to use methods which are given under the management accounting system(Shah, Malik and

Malik, 2011). It can help to the company to select an appropriate source of finance for their

future projects which can help to the company to make a profitability in the investments and as

well as it can help to the company to determine the best source (Herbert and Seal, 2012).

Managers and owners of the Agmet have to use this method which can help to them to select a

source which has a potential to give them proper financial support till to attain their objectives.

So they have to make a proper analysis of the available options of the financial sources and it can

help to the company to make a favourable decision on it.

Ratio analysis: It is based on the mathematical formulas which can help to the company to make

a proper analysis of the profits as per their investments and expenses (Fullerton, Kennedy and

Widener, 2014). Standard ratios has to be used by the company to make a review on the

production cost and pricing.

make an analysis of the management, accounting and financial data of the company. Different

types of management accounting reports are here which can be used by the Agmet:

Cash Flow analysis: This is a statement in which cash transactions covered, it is divided in to

three sections which are operating activity, investing activity, financial activity. In these section

of the cash flow statement Agmet has to analyse the cash inflow and cash outflow from the

business (Håkansson, Kraus and Lind, 2010). As the company is working in the chemical

manufacturing and selling so product sale has to be covered in to the operating activities and

return on the investment has to be covered in to the investing and cash inflow and outflow from

the financial sources covered in to the last one.

Fund flow analysis: It is used by the management of the Agmet by which they can make better

working in the organisation by analysing the use of funds which are available for them. It help to

the company to make an analysis of the sources where they can arise financial funds and as well

as it can help to the company to make an appropriate analysis of the points in which they are

investing their financial funds. It can help to the company to make a profitability level in to the

organisation by making a proper analysis of these sources and consumption of the finance.

Financial planning: It is an essential tool for the managers of the Agmet to make proper

planning of the investment and as well as arise finance for the future project. So the Agmet has

to use methods which are given under the management accounting system(Shah, Malik and

Malik, 2011). It can help to the company to select an appropriate source of finance for their

future projects which can help to the company to make a profitability in the investments and as

well as it can help to the company to determine the best source (Herbert and Seal, 2012).

Managers and owners of the Agmet have to use this method which can help to them to select a

source which has a potential to give them proper financial support till to attain their objectives.

So they have to make a proper analysis of the available options of the financial sources and it can

help to the company to make a favourable decision on it.

Ratio analysis: It is based on the mathematical formulas which can help to the company to make

a proper analysis of the profits as per their investments and expenses (Fullerton, Kennedy and

Widener, 2014). Standard ratios has to be used by the company to make a review on the

production cost and pricing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating Budget Report: Each and every organisation has made a budget which includes all of

the factors on which a company work in a year (Dillard and Roslender, 2011). So Agmet has to

use the budget report by which they can minimise the cost and expenses and as well as they can

manage profitability in the organisation. Agmet has to make annual operating budget on annual

basis which can help to the company to estimate their operating cost for the year and determine

the selling price of their products. An operating budget report can help to the company to make a

better change in the company by which they can be in the profitable conditions. This can help to

the company to analyse those sources which are not working according to expectations and

consuming over cost on the basis of estimated cost.

Bills receivable reports - It is that document in which information related to the amount which

is due to customers but not received is included. This is an important document as in order to

assist the collection department it is necessary that data is properly recorded.

Performance report – It is another text in which results of different department are included

which helps on doing the evaluation of each. Through this it becomes easy to understand that

which section of the department needs to be improved and given more care. Mainly performance

report is created to analyse the performance of a project or employees of organisation, in the

context of Agmet, it will be effective to use this to measure the performance of employees which

is essential. It can help to the company to maintain a standardized productivity of workers. The

performance reports having some essential elements in it which are investment, standardize

output from an employee and actual performance of employee. Management of Agmet can draft

these reports on monthly basis to evaluate the productivity of each employees which can help to

the company to be in profitable situations.

Inventory management report – It includes the information related to the present stock level of

the company which is of great importance. By this report both the situation of excess or deficit in

inventory can be avoided. As company is dealing in the chemical manufacturing industry so it is

having a huge need of the inventory management because it can help to the purchase team to buy

enough raw material to convert it in chemical. It is essential that production of chemical has to be

appropriate according to market demands which can help to the company to be in the profitable

situation. By using inventory management company will able to maintain an enough stock which

can help to them invest in profitable manner.

the factors on which a company work in a year (Dillard and Roslender, 2011). So Agmet has to

use the budget report by which they can minimise the cost and expenses and as well as they can

manage profitability in the organisation. Agmet has to make annual operating budget on annual

basis which can help to the company to estimate their operating cost for the year and determine

the selling price of their products. An operating budget report can help to the company to make a

better change in the company by which they can be in the profitable conditions. This can help to

the company to analyse those sources which are not working according to expectations and

consuming over cost on the basis of estimated cost.

Bills receivable reports - It is that document in which information related to the amount which

is due to customers but not received is included. This is an important document as in order to

assist the collection department it is necessary that data is properly recorded.

Performance report – It is another text in which results of different department are included

which helps on doing the evaluation of each. Through this it becomes easy to understand that

which section of the department needs to be improved and given more care. Mainly performance

report is created to analyse the performance of a project or employees of organisation, in the

context of Agmet, it will be effective to use this to measure the performance of employees which

is essential. It can help to the company to maintain a standardized productivity of workers. The

performance reports having some essential elements in it which are investment, standardize

output from an employee and actual performance of employee. Management of Agmet can draft

these reports on monthly basis to evaluate the productivity of each employees which can help to

the company to be in profitable situations.

Inventory management report – It includes the information related to the present stock level of

the company which is of great importance. By this report both the situation of excess or deficit in

inventory can be avoided. As company is dealing in the chemical manufacturing industry so it is

having a huge need of the inventory management because it can help to the purchase team to buy

enough raw material to convert it in chemical. It is essential that production of chemical has to be

appropriate according to market demands which can help to the company to be in the profitable

situation. By using inventory management company will able to maintain an enough stock which

can help to them invest in profitable manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These all of the methods has to be used by the Agmet to manage their financial resources

to attain their objectives with maximum profitability.

TASK.2

P.3 Computation of net profit using absorption costing and marginal costing techniques

Net profits can be figured out through different procedures in the management

accounting. Income according to the absorption costing and marginal costing is appeared as

underneath:

• Absorption Costing: This costing methodology is a system of management accounting by

which different costs which are connected with various sorts of production procedures are

absorbed on an item(Setthasakko, 2010). Absorption costing is required to assess the stock

of an association. Budgetary forecasting is the principle component of management

accounting(Sánchez-Rodríguez and Spraakman, 2012).

.

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

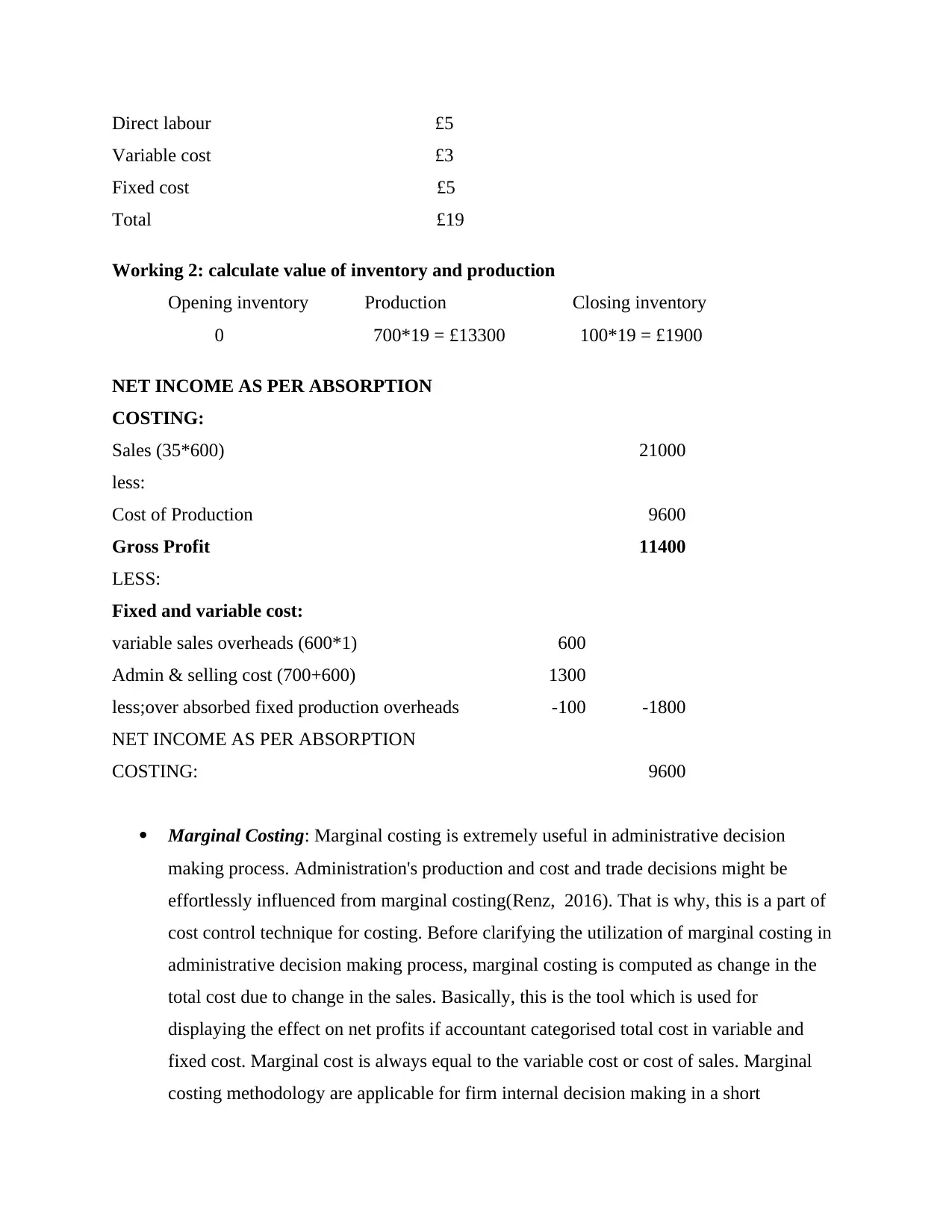

Working 1: Calculate full production cost

Direct material £6

to attain their objectives with maximum profitability.

TASK.2

P.3 Computation of net profit using absorption costing and marginal costing techniques

Net profits can be figured out through different procedures in the management

accounting. Income according to the absorption costing and marginal costing is appeared as

underneath:

• Absorption Costing: This costing methodology is a system of management accounting by

which different costs which are connected with various sorts of production procedures are

absorbed on an item(Setthasakko, 2010). Absorption costing is required to assess the stock

of an association. Budgetary forecasting is the principle component of management

accounting(Sánchez-Rodríguez and Spraakman, 2012).

.

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

Marginal Costing: Marginal costing is extremely useful in administrative decision

making process. Administration's production and cost and trade decisions might be

effortlessly influenced from marginal costing(Renz, 2016). That is why, this is a part of

cost control technique for costing. Before clarifying the utilization of marginal costing in

administrative decision making process, marginal costing is computed as change in the

total cost due to change in the sales. Basically, this is the tool which is used for

displaying the effect on net profits if accountant categorised total cost in variable and

fixed cost. Marginal cost is always equal to the variable cost or cost of sales. Marginal

costing methodology are applicable for firm internal decision making in a short

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

Marginal Costing: Marginal costing is extremely useful in administrative decision

making process. Administration's production and cost and trade decisions might be

effortlessly influenced from marginal costing(Renz, 2016). That is why, this is a part of

cost control technique for costing. Before clarifying the utilization of marginal costing in

administrative decision making process, marginal costing is computed as change in the

total cost due to change in the sales. Basically, this is the tool which is used for

displaying the effect on net profits if accountant categorised total cost in variable and

fixed cost. Marginal cost is always equal to the variable cost or cost of sales. Marginal

costing methodology are applicable for firm internal decision making in a short

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

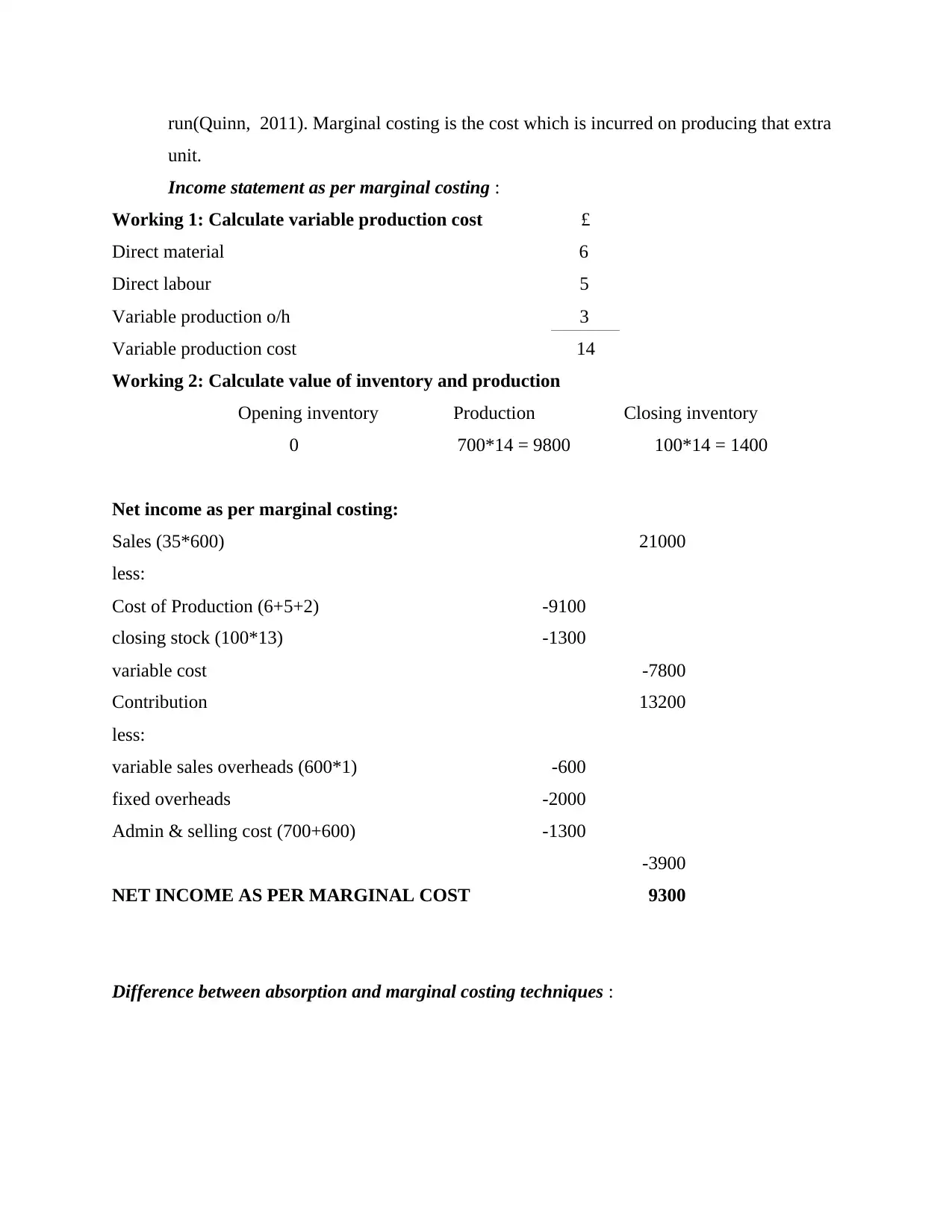

run(Quinn, 2011). Marginal costing is the cost which is incurred on producing that extra

unit.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production o/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net income as per marginal costing:

Sales (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

Difference between absorption and marginal costing techniques :

unit.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production o/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net income as per marginal costing:

Sales (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

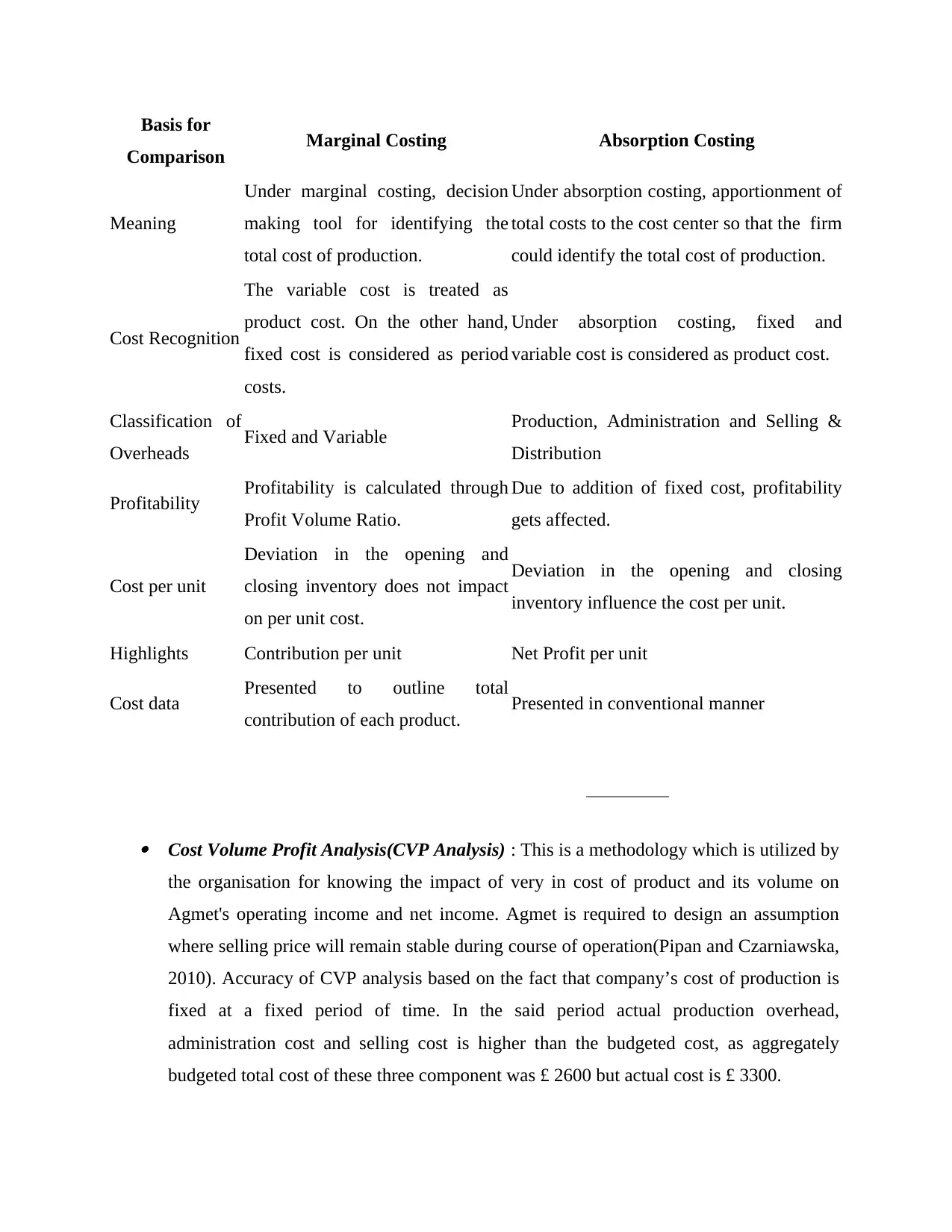

Difference between absorption and marginal costing techniques :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basis for

Comparison Marginal Costing Absorption Costing

Meaning

Under marginal costing, decision

making tool for identifying the

total cost of production.

Under absorption costing, apportionment of

total costs to the cost center so that the firm

could identify the total cost of production.

Cost Recognition

The variable cost is treated as

product cost. On the other hand,

fixed cost is considered as period

costs.

Under absorption costing, fixed and

variable cost is considered as product cost.

Classification of

Overheads Fixed and Variable Production, Administration and Selling &

Distribution

Profitability Profitability is calculated through

Profit Volume Ratio.

Due to addition of fixed cost, profitability

gets affected.

Cost per unit

Deviation in the opening and

closing inventory does not impact

on per unit cost.

Deviation in the opening and closing

inventory influence the cost per unit.

Highlights Contribution per unit Net Profit per unit

Cost data Presented to outline total

contribution of each product. Presented in conventional manner

Cost Volume Profit Analysis(CVP Analysis) : This is a methodology which is utilized by

the organisation for knowing the impact of very in cost of product and its volume on

Agmet's operating income and net income. Agmet is required to design an assumption

where selling price will remain stable during course of operation(Pipan and Czarniawska,

2010). Accuracy of CVP analysis based on the fact that company’s cost of production is

fixed at a fixed period of time. In the said period actual production overhead,

administration cost and selling cost is higher than the budgeted cost, as aggregately

budgeted total cost of these three component was £ 2600 but actual cost is £ 3300.

Comparison Marginal Costing Absorption Costing

Meaning

Under marginal costing, decision

making tool for identifying the

total cost of production.

Under absorption costing, apportionment of

total costs to the cost center so that the firm

could identify the total cost of production.

Cost Recognition

The variable cost is treated as

product cost. On the other hand,

fixed cost is considered as period

costs.

Under absorption costing, fixed and

variable cost is considered as product cost.

Classification of

Overheads Fixed and Variable Production, Administration and Selling &

Distribution

Profitability Profitability is calculated through

Profit Volume Ratio.

Due to addition of fixed cost, profitability

gets affected.

Cost per unit

Deviation in the opening and

closing inventory does not impact

on per unit cost.

Deviation in the opening and closing

inventory influence the cost per unit.

Highlights Contribution per unit Net Profit per unit

Cost data Presented to outline total

contribution of each product. Presented in conventional manner

Cost Volume Profit Analysis(CVP Analysis) : This is a methodology which is utilized by

the organisation for knowing the impact of very in cost of product and its volume on

Agmet's operating income and net income. Agmet is required to design an assumption

where selling price will remain stable during course of operation(Pipan and Czarniawska,

2010). Accuracy of CVP analysis based on the fact that company’s cost of production is

fixed at a fixed period of time. In the said period actual production overhead,

administration cost and selling cost is higher than the budgeted cost, as aggregately

budgeted total cost of these three component was £ 2600 but actual cost is £ 3300.

Absorption Costing : As per the above mentioned income statement which is made as

per absorption costing. Total cost per unit of Agmet was £ 19 which includes £ 6 for

direct material, £ 5 for direct labour, £ 3 is for variable cost and £ 5 of fixed cost

apportioned on specific basis. Under absorption costing, Agmet search out under and

over absorbed production overhead in order to attain better cost management (Nandan,

2010).

TASK.3

P.4 Similarities and dissimilarities of different types of planning tools used for budgetary

control:

Budgetary control is utilized as a device of administration control and determines a few

advantages. As the company is committed in manufacturing, it is essential for it to make a

budgetary control on the activities conducted in to the manufacturing. Higher management of the

Agmet has to develop different types of budget e.g. master budget, operating budget,

departmental budget, purchase budget etc. These can help to managers of the company to

maintain to cost of their operations according to the budget. It can also help to the company to

analyse the factors where company has put more investment of resources according to estimated

budget. So Agmet has to develop these different types of budget which can help to them to be in

the Win position in their industry by creating profits. There are few budgetary tools which are

mentioned hereunder:

Cash budget: Under cash budget, entire expenses or revenues related to cash considered. With

the help of cash budget, company is able to allocate its earnings in a most effective manner and

also able to plan effectively.

Advantages –

Estimation of future needs: It can help to the company to make an estimate of the future

needs of cash. This will help to the company to gather informations of those expenses

which are related to the future of the organisation, so it can help to the company to

manage their liquidity to bear these expenses.

Control cash flow: It can help to the company to manage their cash inflow and outflow

to deal with the stakeholders. Agmet is having debtors and creditors, each one is having

per absorption costing. Total cost per unit of Agmet was £ 19 which includes £ 6 for

direct material, £ 5 for direct labour, £ 3 is for variable cost and £ 5 of fixed cost

apportioned on specific basis. Under absorption costing, Agmet search out under and

over absorbed production overhead in order to attain better cost management (Nandan,

2010).

TASK.3

P.4 Similarities and dissimilarities of different types of planning tools used for budgetary

control:

Budgetary control is utilized as a device of administration control and determines a few

advantages. As the company is committed in manufacturing, it is essential for it to make a

budgetary control on the activities conducted in to the manufacturing. Higher management of the

Agmet has to develop different types of budget e.g. master budget, operating budget,

departmental budget, purchase budget etc. These can help to managers of the company to

maintain to cost of their operations according to the budget. It can also help to the company to

analyse the factors where company has put more investment of resources according to estimated

budget. So Agmet has to develop these different types of budget which can help to them to be in

the Win position in their industry by creating profits. There are few budgetary tools which are

mentioned hereunder:

Cash budget: Under cash budget, entire expenses or revenues related to cash considered. With

the help of cash budget, company is able to allocate its earnings in a most effective manner and

also able to plan effectively.

Advantages –

Estimation of future needs: It can help to the company to make an estimate of the future

needs of cash. This will help to the company to gather informations of those expenses

which are related to the future of the organisation, so it can help to the company to

manage their liquidity to bear these expenses.

Control cash flow: It can help to the company to manage their cash inflow and outflow

to deal with the stakeholders. Agmet is having debtors and creditors, each one is having

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.