Management Accounting Report: Zylla Company Cost Analysis and Planning

VerifiedAdded on 2020/07/23

|14

|4147

|31

Report

AI Summary

This report provides a detailed analysis of management accounting principles and techniques, focusing on their application within the context of Zylla, a multinational organization. It begins by defining management accounting and outlining the requirements of different types, including traditional, lean, throughput, and transfer pricing methods. The report then explores various management accounting reporting methods, such as budget reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports, highlighting their importance in monitoring company performance. A significant portion of the report is dedicated to cost analysis techniques, specifically marginal and absorption costing, with illustrative income statements provided for both methods. The report concludes by examining the advantages and disadvantages of different planning tools used in budgetary control, offering recommendations for Zylla's accounting system to optimize its financial decision-making and operational efficiency. The report emphasizes the integration of different accounting approaches for optimal outcomes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

P1 Meaning of management accounting and requirements of different types of management

accounting...................................................................................................................................1

P2. Methods of management accounting reporting.....................................................................2

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costing.........................................................................................................................................3

P4 Advantages and disadvantages of different types of planning tools used in budgetary

control.........................................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

P1 Meaning of management accounting and requirements of different types of management

accounting...................................................................................................................................1

P2. Methods of management accounting reporting.....................................................................2

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costing.........................................................................................................................................3

P4 Advantages and disadvantages of different types of planning tools used in budgetary

control.........................................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Zylla is a large multinational organisation, it has undergone a multiple changes over a

period of time. These modifications results in expansion of a business into new markets and

locations. It also results in restructuring and acquisitions.

In this report, recommendation for changes have been explained through explaining about

management accounting systems, techniques and planning tools have been explained. Also

financial problems in applying tools and techniques has been described by using management

accounting concepts.

The purpose of this report is to conduct a research on developments in management

accounting and also to recommend changes in accounting system of Zylla company.

TASK

P1 Meaning of management accounting and requirements of different types of management

accounting

Management accounting are all set of provisions related to accounting information which

is to be followed by managers to decide issues within organisations (Ward, K., 2012). Overall it

is the provision of financial and non-financial decision making informations which is useful for

managers. The main users of management accounting are Investors, creditors and operational

managers. Each users have different motives to use accounting informations.

Some of the essential requirements of different types of management accounting are as

follows:

Traditional Accounting: This accounting system records overall costs through job order

and process costing methods (DRURY, C.M., 2013). Job order costing is used for giant

projects where its easy to record all costs related to individual projects on the other hand

process costing method is suitable for those projects which is producing homogeneous

goods. It is essentially required for Zylla to follow traditional management accounting

system because by following these methods company can determine how it allocates its

costs which is related to Cost of goods sold like raw materials, direct labour and

manufacturing overhead expenses.

Lean Accounting: This type of management accounting, uses revolutionary techniques

by focusing on strategies to reduce costs. Accounting managers in this system provides

1

Zylla is a large multinational organisation, it has undergone a multiple changes over a

period of time. These modifications results in expansion of a business into new markets and

locations. It also results in restructuring and acquisitions.

In this report, recommendation for changes have been explained through explaining about

management accounting systems, techniques and planning tools have been explained. Also

financial problems in applying tools and techniques has been described by using management

accounting concepts.

The purpose of this report is to conduct a research on developments in management

accounting and also to recommend changes in accounting system of Zylla company.

TASK

P1 Meaning of management accounting and requirements of different types of management

accounting

Management accounting are all set of provisions related to accounting information which

is to be followed by managers to decide issues within organisations (Ward, K., 2012). Overall it

is the provision of financial and non-financial decision making informations which is useful for

managers. The main users of management accounting are Investors, creditors and operational

managers. Each users have different motives to use accounting informations.

Some of the essential requirements of different types of management accounting are as

follows:

Traditional Accounting: This accounting system records overall costs through job order

and process costing methods (DRURY, C.M., 2013). Job order costing is used for giant

projects where its easy to record all costs related to individual projects on the other hand

process costing method is suitable for those projects which is producing homogeneous

goods. It is essentially required for Zylla to follow traditional management accounting

system because by following these methods company can determine how it allocates its

costs which is related to Cost of goods sold like raw materials, direct labour and

manufacturing overhead expenses.

Lean Accounting: This type of management accounting, uses revolutionary techniques

by focusing on strategies to reduce costs. Accounting managers in this system provides

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

immediate financial informations at the time of decisions making. Hence, it is essentially

required for management accounting of Zylla because this method helps in cost reduction

by focusing on elimination of waste to decrease expenses to a business.

Throughput accounting: This type of management accounting doesn't follow costing

process as like in traditional management accounting systems. In this system accountants

focus on identifying the pitfalls within operational production system (Bodie, Z., 2013).

Defects may be insufficient levels of raw materials, labour and equipments within a

company. These type is essentially required by Zylla management accounting because

eliminating these pitfalls will help Zylla in increasing its production volume with

reducing cost of production at each individual level of unit produced.

Transfer Pricing method: In this management accounting type, companies will cost

goods with moving through different departments. This types of management accounting

is essentially required by Zylla because it reflects actual cost of a product by adding small

portion to a products cost every time when it is moving from one department to another.

This method recommends to add common costs which is variable and opportunity

expenses to a product as if in the absence of this costs, Zylla can undervalue its products

and can face run out of cash.

Hence, after analysing all the above essential requirements of different types of

management accounting it is recommended that, company should use best combination of all the

above approaches to get optimum result from it. Zylla can't independently use only one method

or approach, it has to use all approaches of management accounting.

P2. Methods of management accounting reporting

Management accounting reports helps business in monitoring company's performance

(Baldvinsdottir, Mitchell and Nørreklit, 2010). It is made at the end of every accounting period

or it can be present at the time of requirement of it like managers may request for quarterly,

monthly, weekly or even daily reports. There are several methods for management accounting

reporting which is explained below:

Budget Report: Through this method of management accounting reporting company can

know its company's performance through analysing budget reports. This report helps in

controlling excess costs bear by company on some departments. Budget reports compares

department's performance with its costs. In this method estimated budget for that

2

required for management accounting of Zylla because this method helps in cost reduction

by focusing on elimination of waste to decrease expenses to a business.

Throughput accounting: This type of management accounting doesn't follow costing

process as like in traditional management accounting systems. In this system accountants

focus on identifying the pitfalls within operational production system (Bodie, Z., 2013).

Defects may be insufficient levels of raw materials, labour and equipments within a

company. These type is essentially required by Zylla management accounting because

eliminating these pitfalls will help Zylla in increasing its production volume with

reducing cost of production at each individual level of unit produced.

Transfer Pricing method: In this management accounting type, companies will cost

goods with moving through different departments. This types of management accounting

is essentially required by Zylla because it reflects actual cost of a product by adding small

portion to a products cost every time when it is moving from one department to another.

This method recommends to add common costs which is variable and opportunity

expenses to a product as if in the absence of this costs, Zylla can undervalue its products

and can face run out of cash.

Hence, after analysing all the above essential requirements of different types of

management accounting it is recommended that, company should use best combination of all the

above approaches to get optimum result from it. Zylla can't independently use only one method

or approach, it has to use all approaches of management accounting.

P2. Methods of management accounting reporting

Management accounting reports helps business in monitoring company's performance

(Baldvinsdottir, Mitchell and Nørreklit, 2010). It is made at the end of every accounting period

or it can be present at the time of requirement of it like managers may request for quarterly,

monthly, weekly or even daily reports. There are several methods for management accounting

reporting which is explained below:

Budget Report: Through this method of management accounting reporting company can

know its company's performance through analysing budget reports. This report helps in

controlling excess costs bear by company on some departments. Budget reports compares

department's performance with its costs. In this method estimated budget for that

2

particular period is made, this estimation is based on trends of its actual expenses.

Owners and managers can also use budget reports to allocate incentives among their

employees. Budget reports needs strong analytical and analyses skills to make useful

management accounting reports. Overall it is the most fundamental report in managerial

accounting. It helps business in control costs across enterprises.

Accounts receivable Aging Report: This reporting method of management accounting

is very important for any business that sales their products on credit. Usually credits are

given into different categories like 30, 60 and 90 days (Lukka and Modell 2010). This

method is a critical tool for managing cash flow for companies while giving credit to

their clients. Zylla can use the aging report to find issues in company's collection process.

For instance, Zylla should strict its credit policies, if large number of customers are

unable to pay their balances on time.

Job costs Reports: This method of management accounting provides a reports which

shows expenses for a specific project. These costs is matched with an estimate revenue to

analyse profitability of the job. This method classifies the higher earning areas of a

business which helps company to focus on allocating its funds among these areas instead

wasting its money and cost in using funds in less earning areas. Job Cost Report is also

used to analyse expenses of work-in-progress projects to control waste before completing

it.

Inventory and manufacturing reports: This method of management accounting is

useful for those companies who produces physical products like manufacturing

industries. Inventory and manufacturing report helps in collecting data's on inventory

costs, labour and other overheads of production process. Manufacturing companies can

use managerial accounting reports to make their operational process more efficient.

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costing

Marginal costing of an item is its variable cost. Whereas the marginal cost of production

includes direct material cost, direct labour cost, direct expenses and variable overhead cost of

production (Ferreira, Moulang and Hendro 2010). Hence marginal costing is the management

accounting system in which total variable costs are charged to cost units and fixed cost is written

off to find contribution.

3

Owners and managers can also use budget reports to allocate incentives among their

employees. Budget reports needs strong analytical and analyses skills to make useful

management accounting reports. Overall it is the most fundamental report in managerial

accounting. It helps business in control costs across enterprises.

Accounts receivable Aging Report: This reporting method of management accounting

is very important for any business that sales their products on credit. Usually credits are

given into different categories like 30, 60 and 90 days (Lukka and Modell 2010). This

method is a critical tool for managing cash flow for companies while giving credit to

their clients. Zylla can use the aging report to find issues in company's collection process.

For instance, Zylla should strict its credit policies, if large number of customers are

unable to pay their balances on time.

Job costs Reports: This method of management accounting provides a reports which

shows expenses for a specific project. These costs is matched with an estimate revenue to

analyse profitability of the job. This method classifies the higher earning areas of a

business which helps company to focus on allocating its funds among these areas instead

wasting its money and cost in using funds in less earning areas. Job Cost Report is also

used to analyse expenses of work-in-progress projects to control waste before completing

it.

Inventory and manufacturing reports: This method of management accounting is

useful for those companies who produces physical products like manufacturing

industries. Inventory and manufacturing report helps in collecting data's on inventory

costs, labour and other overheads of production process. Manufacturing companies can

use managerial accounting reports to make their operational process more efficient.

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costing

Marginal costing of an item is its variable cost. Whereas the marginal cost of production

includes direct material cost, direct labour cost, direct expenses and variable overhead cost of

production (Ferreira, Moulang and Hendro 2010). Hence marginal costing is the management

accounting system in which total variable costs are charged to cost units and fixed cost is written

off to find contribution.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable costs are those expenses which changes with per unit of production (Cinquini

and Tenucci 2010). Marginal costing is used in decision making process because it allows Zylla

to focus on the changes in variable cost on the basis of this company can make price decisions.

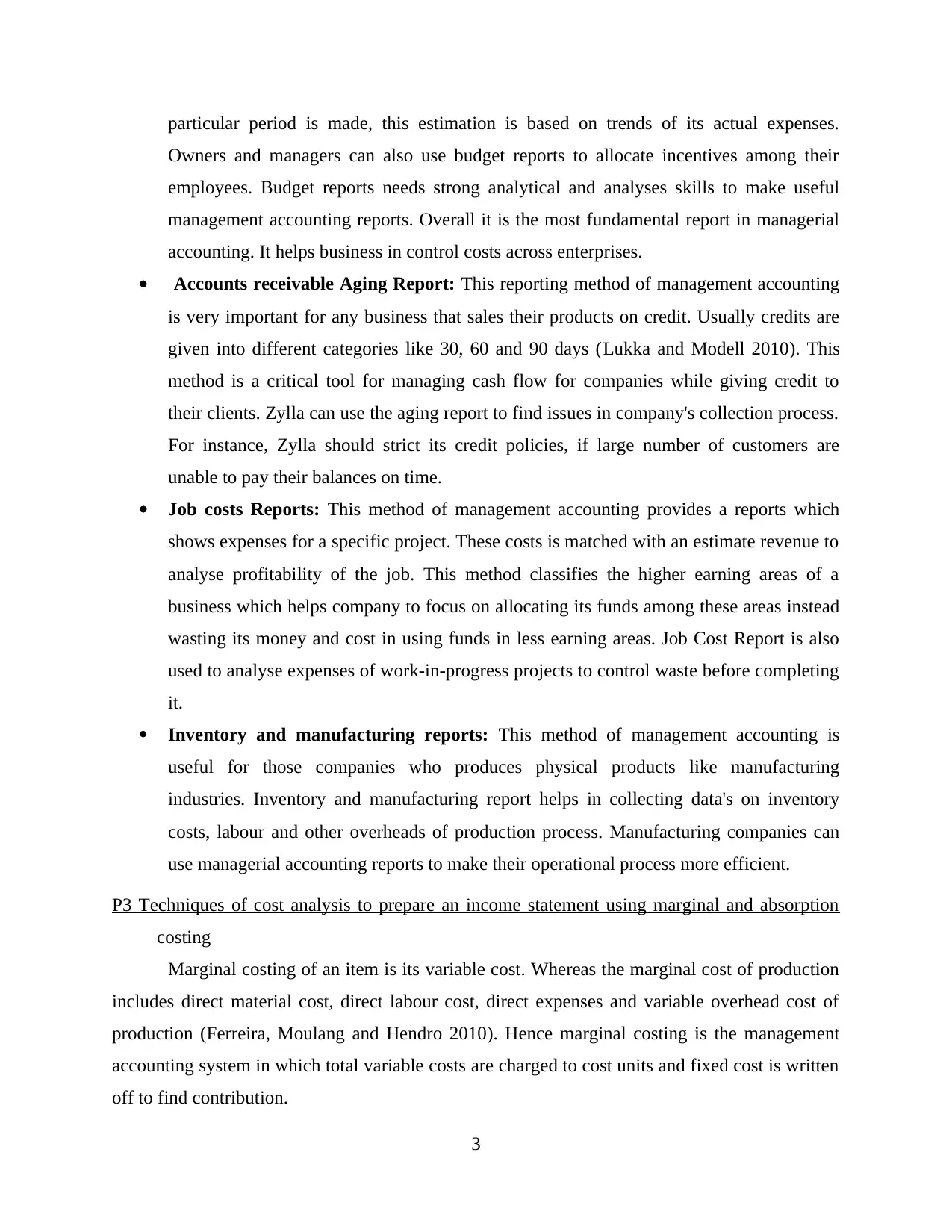

Below is the illustration in which income statement of Zylla is prepared on the basis of

Marginal costing:

Marginal Costing Income statement of Zylla

Amount $ '000 Amount $ '000

Sales 100

Less: Cost of Sales

Opening Inventory 40

Variable cost of Production 50

Less: Closing Inventory -10

-80

20

Less:Other variable Costs -5

Contribution 15

Less: Fixed Costs -5

EBIT (Operating profit) 10

(Imagery figure)

Hence, in the above marginal income statement, opening and closing inventory are

valued at marginal variable cost under marginal costing concept. Fixed costs is deducted from

contribution to determine the EBIT or earning before interest and taxes for the period.

Therefore, marginal concept considers the expense per unit produced. Thus to reduce

expense, that unit is to avoid to produce.

Absorption Costing: It is the method of building up a full cost of a product by adding

direct costs and a proportion of overhead costs of a production (Cohen and Zarowin 2010). This

costs are analysed on the basis of overhead absorption rates.

Absorption costs is determined on the basis of per unit production of a good. Some of the

various overhead expenses are:

4

and Tenucci 2010). Marginal costing is used in decision making process because it allows Zylla

to focus on the changes in variable cost on the basis of this company can make price decisions.

Below is the illustration in which income statement of Zylla is prepared on the basis of

Marginal costing:

Marginal Costing Income statement of Zylla

Amount $ '000 Amount $ '000

Sales 100

Less: Cost of Sales

Opening Inventory 40

Variable cost of Production 50

Less: Closing Inventory -10

-80

20

Less:Other variable Costs -5

Contribution 15

Less: Fixed Costs -5

EBIT (Operating profit) 10

(Imagery figure)

Hence, in the above marginal income statement, opening and closing inventory are

valued at marginal variable cost under marginal costing concept. Fixed costs is deducted from

contribution to determine the EBIT or earning before interest and taxes for the period.

Therefore, marginal concept considers the expense per unit produced. Thus to reduce

expense, that unit is to avoid to produce.

Absorption Costing: It is the method of building up a full cost of a product by adding

direct costs and a proportion of overhead costs of a production (Cohen and Zarowin 2010). This

costs are analysed on the basis of overhead absorption rates.

Absorption costs is determined on the basis of per unit production of a good. Some of the

various overhead expenses are:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct expense and Indirect expenses: Direct expenses are directly linked with

production process. It is identified with a particular cost per unit. For example royalties

paid to a designer and paying wages and electric charges of factory is considered as

Direct expenses. Overall it is the part of prime cost of a product.

Indirect costing cannot be identified directly because it includes administration

and selling activities of a product. It includes rents, salaries and advertisement cost to a company.

For example the cost of renting of a shirt factory is considered as an indirect cost if others clothes

such as trousers, suits and blazers are also made in the same factory. Overhead expenses can be

called as indirect expenses.

Production overhead absorption: It is the total indirect production costs or fixed

production overhead costs.

Fixed production overhead costs = indirect materials + Indirect labour + indirect expenses

These costs are fixed in nature, as per unit production doesn't affect this expenses until

unless business is expanded. Some of the examples of this costs are heating, lighting and renting

costs of a factory.

Hence, absorption costing method accepts only those costs which can be fully absorbed

in production process. The aim of absorption costing is to recover overheads so that it can

reflects total time and effort consumed in making a product and services. Absorption costing can

be calculated by following below steps:

Allocation and appointment of overheads: In this stage absorption costing, allocation

and apportionment of overheads is done. Allocation involves charging overhead expenses

directly to production and service department. Apportioned of overheads have to be done

between different departments on the basis of expenses on it.

Reappointment of service cost centre overheads: Service cost centres or departments

are not directly make the products, therefore their fixed overhead charges should be

allocated between production departments on the cost basis. Some of the examples of

cost centres are as follows: Stores, Canteen, Maintenance department and payroll

department. These costs should be included in production overheads because without

these centres production departments can't work. Therefore it will be considered as

indirect cost of production centres and thus it should be absorbed,

5

production process. It is identified with a particular cost per unit. For example royalties

paid to a designer and paying wages and electric charges of factory is considered as

Direct expenses. Overall it is the part of prime cost of a product.

Indirect costing cannot be identified directly because it includes administration

and selling activities of a product. It includes rents, salaries and advertisement cost to a company.

For example the cost of renting of a shirt factory is considered as an indirect cost if others clothes

such as trousers, suits and blazers are also made in the same factory. Overhead expenses can be

called as indirect expenses.

Production overhead absorption: It is the total indirect production costs or fixed

production overhead costs.

Fixed production overhead costs = indirect materials + Indirect labour + indirect expenses

These costs are fixed in nature, as per unit production doesn't affect this expenses until

unless business is expanded. Some of the examples of this costs are heating, lighting and renting

costs of a factory.

Hence, absorption costing method accepts only those costs which can be fully absorbed

in production process. The aim of absorption costing is to recover overheads so that it can

reflects total time and effort consumed in making a product and services. Absorption costing can

be calculated by following below steps:

Allocation and appointment of overheads: In this stage absorption costing, allocation

and apportionment of overheads is done. Allocation involves charging overhead expenses

directly to production and service department. Apportioned of overheads have to be done

between different departments on the basis of expenses on it.

Reappointment of service cost centre overheads: Service cost centres or departments

are not directly make the products, therefore their fixed overhead charges should be

allocated between production departments on the cost basis. Some of the examples of

cost centres are as follows: Stores, Canteen, Maintenance department and payroll

department. These costs should be included in production overheads because without

these centres production departments can't work. Therefore it will be considered as

indirect cost of production centres and thus it should be absorbed,

5

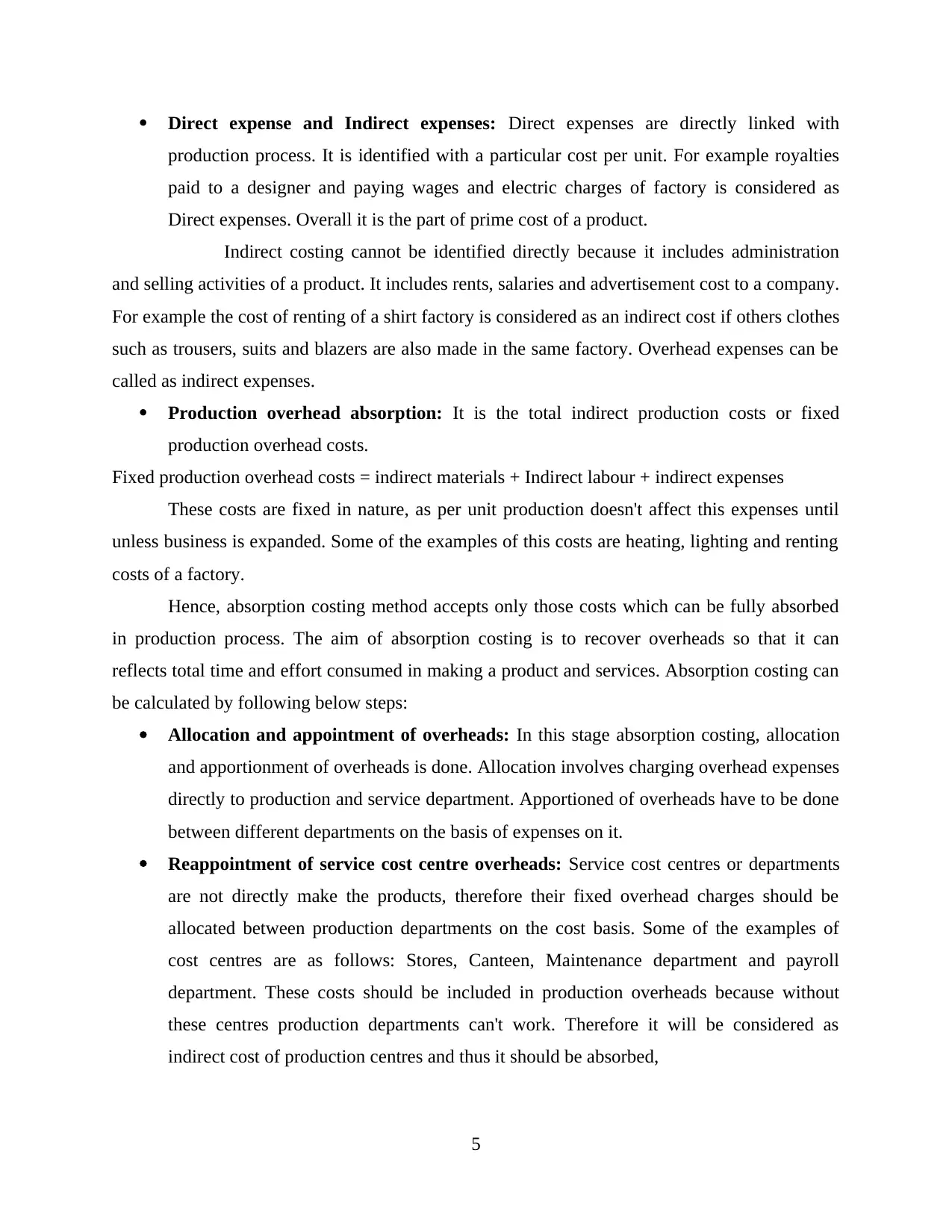

Absorption of overheads: Overhead absorption is a method in which overheads

expenses are included in the total cost of a product. It is defined as charging per unit cost

of production by calculating on the basis of total no. of units to be produced. Overhead

absorption rate can be identified by dividing total overheads from number of units of

absorption products available. Sometimes number of units is estimated on the basis of

demand or previous trends. It can be understand with the help of this given illustration:

Suppose annual demand for its Zylla product is 10000 units. Its sales is $100000 and

variable overhead is $60000. Hence, its selling price per unit will be $100000/10000 =

$10 per unit and variable overhead per unit will be = $60000/10000 = $6 per unit.

Calculation of Income statement on the basis of absorption cost is given below:

Absorption costing income statement

Amount $

'000

Amount $

'000

Sales 100

Less: Cost of Sales

Opening inventory 40

Variable cost of production 50

Fixed overhead absorbed 5

Less: Closing Inventory -10

-85

Under absorption cost -5

Gross profit 10

Less: Non-production costs -1

Net Profit 9

(Imaginary figures)

Hence, the basic difference between marginal costing and absorption method is, in

absorption costing gross profit is identified but not in Marginal costing. Under absorption costs

represents that Zylla's estimated budget of overhead variable cost is less than actual variable

overheads.

6

expenses are included in the total cost of a product. It is defined as charging per unit cost

of production by calculating on the basis of total no. of units to be produced. Overhead

absorption rate can be identified by dividing total overheads from number of units of

absorption products available. Sometimes number of units is estimated on the basis of

demand or previous trends. It can be understand with the help of this given illustration:

Suppose annual demand for its Zylla product is 10000 units. Its sales is $100000 and

variable overhead is $60000. Hence, its selling price per unit will be $100000/10000 =

$10 per unit and variable overhead per unit will be = $60000/10000 = $6 per unit.

Calculation of Income statement on the basis of absorption cost is given below:

Absorption costing income statement

Amount $

'000

Amount $

'000

Sales 100

Less: Cost of Sales

Opening inventory 40

Variable cost of production 50

Fixed overhead absorbed 5

Less: Closing Inventory -10

-85

Under absorption cost -5

Gross profit 10

Less: Non-production costs -1

Net Profit 9

(Imaginary figures)

Hence, the basic difference between marginal costing and absorption method is, in

absorption costing gross profit is identified but not in Marginal costing. Under absorption costs

represents that Zylla's estimated budget of overhead variable cost is less than actual variable

overheads.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P4 Advantages and disadvantages of different types of planning tools used in budgetary control

Budgetary control is a system of management control where actual income and

expenditure are compared with planned income and expenditure (Burritt, Schaltegger and

Zvezdov 2011). It tells about variations between planned and actual. Less variations shows

efficiency of a plan.

Different planning tools of Budgetary control are:

Financial Budgets: In this budget, how much cash will come in and how to allocate

these cash is estimated. The sources of estimations are sales revenue, sales of assets,

stock and loans of previous years. In financial budget, three different types of budgets are

made like cash budget, Capital expenditure budget and Balance sheet budget.

Operating Budgets: This budget is estimation done on allocation of funds on operational

activities of a company. In this type of budget it has three types: Sales budget, Expense

budget and Project budget.

Non-Monetary Budgets: These types of budgets are expresses in non-financial sales or

revenues and expenses like profit.

Fixed and variable budgets: These budgets are the estimation about fixed and variable

expenses of a company based on past trends. Some of the sources of these budgets are:

Fixed costs, variable costs and semi-variable costs of a company.

Advantages of different types of planning tools used in budgetary control:

This tools facilitate effective tools to business: Different tools of budgetary control

helps Zylla in functioning of business in effective way. As financial budgets helps a

company in knowing in advance about how much cash will come in and where to allocate

these funds.

This tools facilitate co-ordination and communication: This tools helps various

department in getting information about all the activities they have to execute in advance.

For example Zylla's Marketing department will know in advance about how much fund is

allocated to them and they can co-ordinate and communicate these to their employees

accordingly.

It facilitate record keeping: It motivates company to keep past records because all past

entries are basis for budgetary planning.

7

Budgetary control is a system of management control where actual income and

expenditure are compared with planned income and expenditure (Burritt, Schaltegger and

Zvezdov 2011). It tells about variations between planned and actual. Less variations shows

efficiency of a plan.

Different planning tools of Budgetary control are:

Financial Budgets: In this budget, how much cash will come in and how to allocate

these cash is estimated. The sources of estimations are sales revenue, sales of assets,

stock and loans of previous years. In financial budget, three different types of budgets are

made like cash budget, Capital expenditure budget and Balance sheet budget.

Operating Budgets: This budget is estimation done on allocation of funds on operational

activities of a company. In this type of budget it has three types: Sales budget, Expense

budget and Project budget.

Non-Monetary Budgets: These types of budgets are expresses in non-financial sales or

revenues and expenses like profit.

Fixed and variable budgets: These budgets are the estimation about fixed and variable

expenses of a company based on past trends. Some of the sources of these budgets are:

Fixed costs, variable costs and semi-variable costs of a company.

Advantages of different types of planning tools used in budgetary control:

This tools facilitate effective tools to business: Different tools of budgetary control

helps Zylla in functioning of business in effective way. As financial budgets helps a

company in knowing in advance about how much cash will come in and where to allocate

these funds.

This tools facilitate co-ordination and communication: This tools helps various

department in getting information about all the activities they have to execute in advance.

For example Zylla's Marketing department will know in advance about how much fund is

allocated to them and they can co-ordinate and communicate these to their employees

accordingly.

It facilitate record keeping: It motivates company to keep past records because all past

entries are basis for budgetary planning.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These tools are natural complement to planning: Making budget is substitute of

planning, because both planning and budgets works on estimation. Through planning,

Zylla can know its strength and weaknesses.

Disadvantages of different types of planning tools used in budgetary control:

This tools are rigid: Tools of budgetary control are rigid in nature because management

can't change anything after budget is made.

It is time consuming: It is not a short process, it requires analytical assessment of whole

data's available. Expert team is required in making budget. It takes years to make a

budget.

It limits innovation: Budget is only made on the behalf of past data's. Hence, innovation

and modification is totally ignored by tools of budgetary control.

Future is uncertain: Tools of budgetary control makes future estimation, and future is

not certain. Like no one can estimated about floods, impact of political changes and wars.

It is dependent on the support of top management: Without the support and

supervision of top management, budgetary control process will not work. So, it is limited

to action of top management only.

P5. Use of management accounting system during financial problem.

Management accounting system is normally the accounting information which managers

use to address any problem and make such effective decisions. They have the duty to look and

inspect the files and after that they analyse the matters or the accounts (Ferreira and Merchant

1992). After going through all these they forward it to the company. Through this, Zylla can

improve their performance of their management thus reaching to new goals which they have

desired for. The managerial team at Zylla does not have to do with any external authority like

bank or something else. This system is a beneficial system in which managers gets a help in

preparing the budget and other planning functions. Recording of the data related to budget is

done in past and then these will be analysed through comparing the data which shows revenues

and expenses which will be acquired by the organisation. The manager take care that the pending

bill of the company are paid as management account assist them in arranging the data in proper

sequence and structure. Using these system makes them flexible and in any time they can extract

the information whenever they require it but with the modification or variations in the internal

and external factors of the company can make things different. There are lots of companies

8

planning, because both planning and budgets works on estimation. Through planning,

Zylla can know its strength and weaknesses.

Disadvantages of different types of planning tools used in budgetary control:

This tools are rigid: Tools of budgetary control are rigid in nature because management

can't change anything after budget is made.

It is time consuming: It is not a short process, it requires analytical assessment of whole

data's available. Expert team is required in making budget. It takes years to make a

budget.

It limits innovation: Budget is only made on the behalf of past data's. Hence, innovation

and modification is totally ignored by tools of budgetary control.

Future is uncertain: Tools of budgetary control makes future estimation, and future is

not certain. Like no one can estimated about floods, impact of political changes and wars.

It is dependent on the support of top management: Without the support and

supervision of top management, budgetary control process will not work. So, it is limited

to action of top management only.

P5. Use of management accounting system during financial problem.

Management accounting system is normally the accounting information which managers

use to address any problem and make such effective decisions. They have the duty to look and

inspect the files and after that they analyse the matters or the accounts (Ferreira and Merchant

1992). After going through all these they forward it to the company. Through this, Zylla can

improve their performance of their management thus reaching to new goals which they have

desired for. The managerial team at Zylla does not have to do with any external authority like

bank or something else. This system is a beneficial system in which managers gets a help in

preparing the budget and other planning functions. Recording of the data related to budget is

done in past and then these will be analysed through comparing the data which shows revenues

and expenses which will be acquired by the organisation. The manager take care that the pending

bill of the company are paid as management account assist them in arranging the data in proper

sequence and structure. Using these system makes them flexible and in any time they can extract

the information whenever they require it but with the modification or variations in the internal

and external factors of the company can make things different. There are lots of companies

8

which has faced financial problem but due to ineffective processes adopted by them they have

failed to recover from it this shutting it down. There were very few of them who have survived

because of the policies, strategies and business structure they have adapted. Some of them are

failing in adopting management accounting system and each of them have different ways to deal

with it thus there is variation in the use of tools and techniques.

Key performance indicator (KPI) are the elements which are utilised for measuring and

analysing the performance of the company through qualitative, quantitative, input, output and

etc. are some kind of indicators which can be considered while evaluating their performance.

Following are some of the accounting system which can be considered in different situation:-

Key performance indicators (KPI):- This is the procedure which can be used by almost

all the companies and through it identification of all the factors which briefs the

performance is done in the procedure. Through analysing the performance Zylla can get

an idea about the areas where they are lagging behind and the areas very there is scope of

improvement. Either there will be evaluation of any particular activity or the success

which they have gained. The customer to whom which they are giving or delivering their

services it is necessary that they should ask them about their opinion and reviews

regarding their experience and this they can get through introducing feedback system. For

this Zylla should give a paper where some questions are mentioned in it thus asking their

opinion.

Benchmarking:- This is the procedure through which the performance of the

organisation will be analysed and measured through taking the comparison with their

competitors. There are various factors on which they analyse and some of them are

quality, time and cost with their opponents who are trading in the same segment.

Budgetary Targets/Control:- Zylla company's management can easily control the flow of

money in different activities. They are aware of the fact that to carry out any business activities

they need money and without it they will not able to undergo different tasks. It becomes

important for them to look at the flow of financial resources. It is their duty to ensure that they

frame a document highlighting the activities require certain money.

CONCLUSION

From the above report it can be analysed that management accounting can help the

organisation in gaining competitive advantage. The financial statement can show variations in

9

failed to recover from it this shutting it down. There were very few of them who have survived

because of the policies, strategies and business structure they have adapted. Some of them are

failing in adopting management accounting system and each of them have different ways to deal

with it thus there is variation in the use of tools and techniques.

Key performance indicator (KPI) are the elements which are utilised for measuring and

analysing the performance of the company through qualitative, quantitative, input, output and

etc. are some kind of indicators which can be considered while evaluating their performance.

Following are some of the accounting system which can be considered in different situation:-

Key performance indicators (KPI):- This is the procedure which can be used by almost

all the companies and through it identification of all the factors which briefs the

performance is done in the procedure. Through analysing the performance Zylla can get

an idea about the areas where they are lagging behind and the areas very there is scope of

improvement. Either there will be evaluation of any particular activity or the success

which they have gained. The customer to whom which they are giving or delivering their

services it is necessary that they should ask them about their opinion and reviews

regarding their experience and this they can get through introducing feedback system. For

this Zylla should give a paper where some questions are mentioned in it thus asking their

opinion.

Benchmarking:- This is the procedure through which the performance of the

organisation will be analysed and measured through taking the comparison with their

competitors. There are various factors on which they analyse and some of them are

quality, time and cost with their opponents who are trading in the same segment.

Budgetary Targets/Control:- Zylla company's management can easily control the flow of

money in different activities. They are aware of the fact that to carry out any business activities

they need money and without it they will not able to undergo different tasks. It becomes

important for them to look at the flow of financial resources. It is their duty to ensure that they

frame a document highlighting the activities require certain money.

CONCLUSION

From the above report it can be analysed that management accounting can help the

organisation in gaining competitive advantage. The financial statement can show variations in

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.