Management Accounting Report: Costing Techniques and Planning Tools

VerifiedAdded on 2021/01/01

|20

|4967

|346

Report

AI Summary

This report delves into the core concepts of management accounting, providing a detailed analysis of costing techniques and planning tools. The report begins by calculating costs using both marginal and absorption costing methods, preparing income statements for three consecutive years. It highlights the differences in net profit calculations under these two methods, explaining the reasons for variances. Furthermore, the report explores various planning tools used in management accounting, particularly focusing on budgetary tools and their implications in preparing and forecasting budgets. The report also investigates how management accounting aids organizations in addressing financial challenges, leading to sustainable success. The analysis includes income statements, cost calculations, and explanations of key concepts, offering a comprehensive overview of management accounting principles.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Calculating costs by applying different costing techniques for preparing income statements1

TASK 2............................................................................................................................................7

a) Explaining the use of planning tools used in management accounting..............................7

Analyzing use of planning tools and implications in preparing and forecasting budgets ....8

c) Evaluating how organizations are adapting management accounting for responding

financial problems..................................................................................................................8

d) Analyzing how management accounting leads organizations to sustainable success........8

e) Evaluating how planning tools helps in solving financial issues.......................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Calculating costs by applying different costing techniques for preparing income statements1

TASK 2............................................................................................................................................7

a) Explaining the use of planning tools used in management accounting..............................7

Analyzing use of planning tools and implications in preparing and forecasting budgets ....8

c) Evaluating how organizations are adapting management accounting for responding

financial problems..................................................................................................................8

d) Analyzing how management accounting leads organizations to sustainable success........8

e) Evaluating how planning tools helps in solving financial issues.......................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is the technique or process of representing the financial

information in the most discrete way that could help the management in taking rational decisions

for the company (Kaplan and Atkinson, 2015). The present report is going to discuss the

difference between marginal and absorption costing, reasons for variances in net profit

calculations under these methods. Further the report will cover planning tools of budgetary tools

and how management accounting helps organisations in responding to their financial problems.

TASK 1

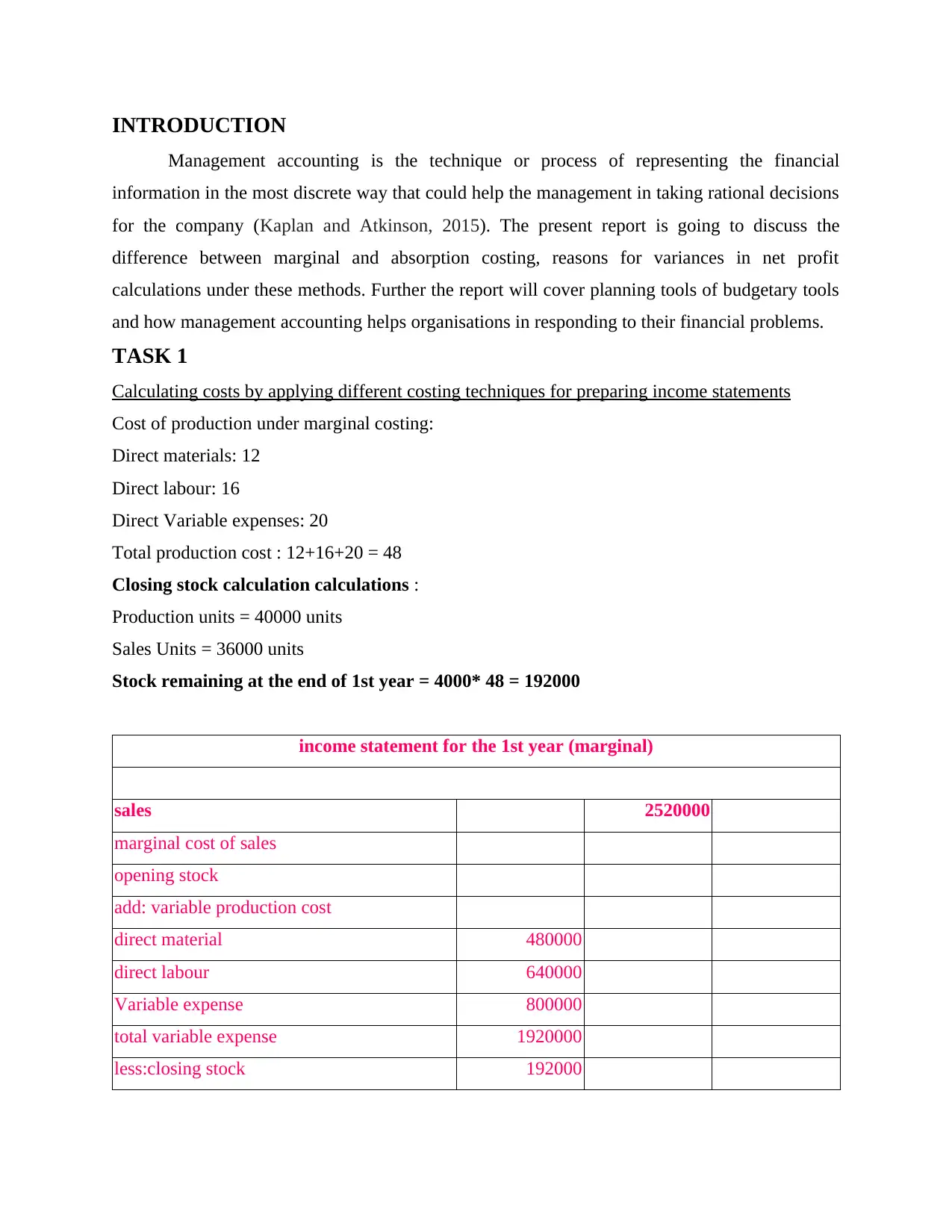

Calculating costs by applying different costing techniques for preparing income statements

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 40000 units

Sales Units = 36000 units

Stock remaining at the end of 1st year = 4000* 48 = 192000

income statement for the 1st year (marginal)

sales 2520000

marginal cost of sales

opening stock

add: variable production cost

direct material 480000

direct labour 640000

Variable expense 800000

total variable expense 1920000

less:closing stock 192000

Management accounting is the technique or process of representing the financial

information in the most discrete way that could help the management in taking rational decisions

for the company (Kaplan and Atkinson, 2015). The present report is going to discuss the

difference between marginal and absorption costing, reasons for variances in net profit

calculations under these methods. Further the report will cover planning tools of budgetary tools

and how management accounting helps organisations in responding to their financial problems.

TASK 1

Calculating costs by applying different costing techniques for preparing income statements

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 40000 units

Sales Units = 36000 units

Stock remaining at the end of 1st year = 4000* 48 = 192000

income statement for the 1st year (marginal)

sales 2520000

marginal cost of sales

opening stock

add: variable production cost

direct material 480000

direct labour 640000

Variable expense 800000

total variable expense 1920000

less:closing stock 192000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

marginal cost of sales 1728000

fixed cost of production 64000

gross profit 728000

selling&distribution overheads 10000

admin costs 15000

EBIT 703000

less: interest 1000

Profit before tax 702000

Tax @19% 133380

PAT 568620

(£)

Income statement under Absorption costing :

Cost of production under absorption costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

Total production cost : 12+16+20+0.25+1.975 = 50.225

Closing stock calculation calculations :

Production units = 40000 units

Sales Units = 36000 units

Stock remaining at the end of 1st year = 4000* 50.225 = 200900

(£)

income statement for the 1st year (absorption)

sales 2520000

marginal cost of sales

fixed cost of production 64000

gross profit 728000

selling&distribution overheads 10000

admin costs 15000

EBIT 703000

less: interest 1000

Profit before tax 702000

Tax @19% 133380

PAT 568620

(£)

Income statement under Absorption costing :

Cost of production under absorption costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

Total production cost : 12+16+20+0.25+1.975 = 50.225

Closing stock calculation calculations :

Production units = 40000 units

Sales Units = 36000 units

Stock remaining at the end of 1st year = 4000* 50.225 = 200900

(£)

income statement for the 1st year (absorption)

sales 2520000

marginal cost of sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

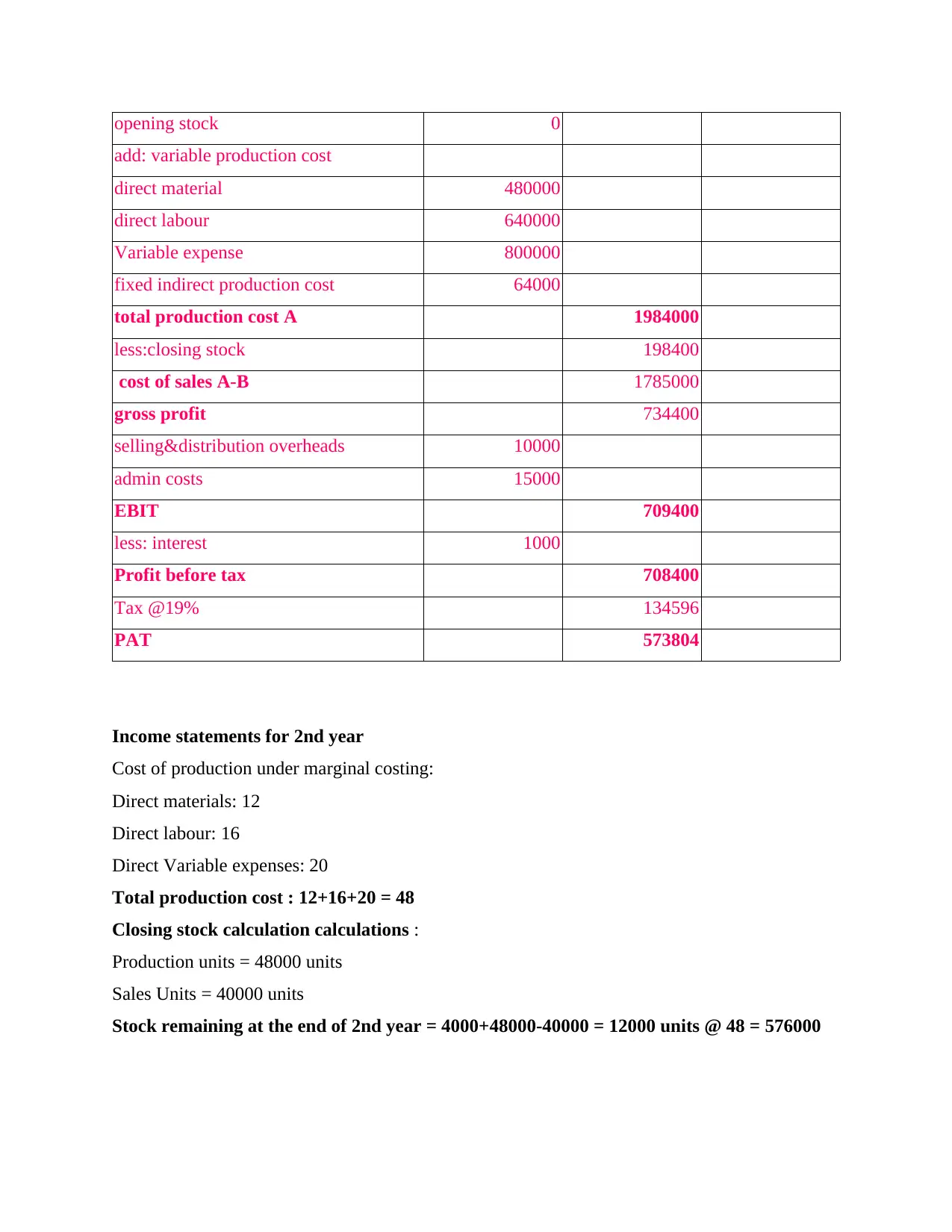

opening stock 0

add: variable production cost

direct material 480000

direct labour 640000

Variable expense 800000

fixed indirect production cost 64000

total production cost A 1984000

less:closing stock 198400

cost of sales A-B 1785000

gross profit 734400

selling&distribution overheads 10000

admin costs 15000

EBIT 709400

less: interest 1000

Profit before tax 708400

Tax @19% 134596

PAT 573804

Income statements for 2nd year

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 2nd year = 4000+48000-40000 = 12000 units @ 48 = 576000

add: variable production cost

direct material 480000

direct labour 640000

Variable expense 800000

fixed indirect production cost 64000

total production cost A 1984000

less:closing stock 198400

cost of sales A-B 1785000

gross profit 734400

selling&distribution overheads 10000

admin costs 15000

EBIT 709400

less: interest 1000

Profit before tax 708400

Tax @19% 134596

PAT 573804

Income statements for 2nd year

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 2nd year = 4000+48000-40000 = 12000 units @ 48 = 576000

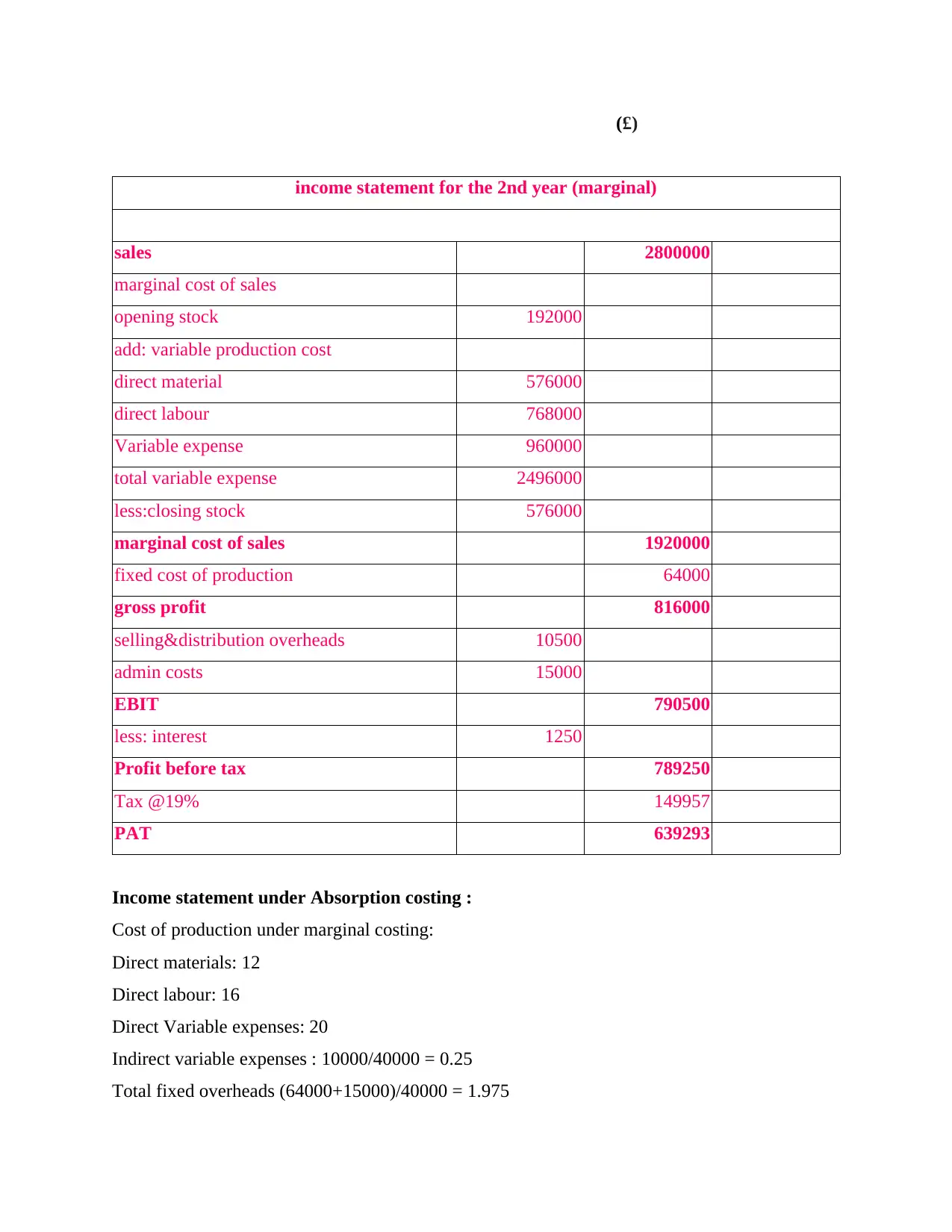

(£)

income statement for the 2nd year (marginal)

sales 2800000

marginal cost of sales

opening stock 192000

add: variable production cost

direct material 576000

direct labour 768000

Variable expense 960000

total variable expense 2496000

less:closing stock 576000

marginal cost of sales 1920000

fixed cost of production 64000

gross profit 816000

selling&distribution overheads 10500

admin costs 15000

EBIT 790500

less: interest 1250

Profit before tax 789250

Tax @19% 149957

PAT 639293

Income statement under Absorption costing :

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

income statement for the 2nd year (marginal)

sales 2800000

marginal cost of sales

opening stock 192000

add: variable production cost

direct material 576000

direct labour 768000

Variable expense 960000

total variable expense 2496000

less:closing stock 576000

marginal cost of sales 1920000

fixed cost of production 64000

gross profit 816000

selling&distribution overheads 10500

admin costs 15000

EBIT 790500

less: interest 1250

Profit before tax 789250

Tax @19% 149957

PAT 639293

Income statement under Absorption costing :

Cost of production under marginal costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

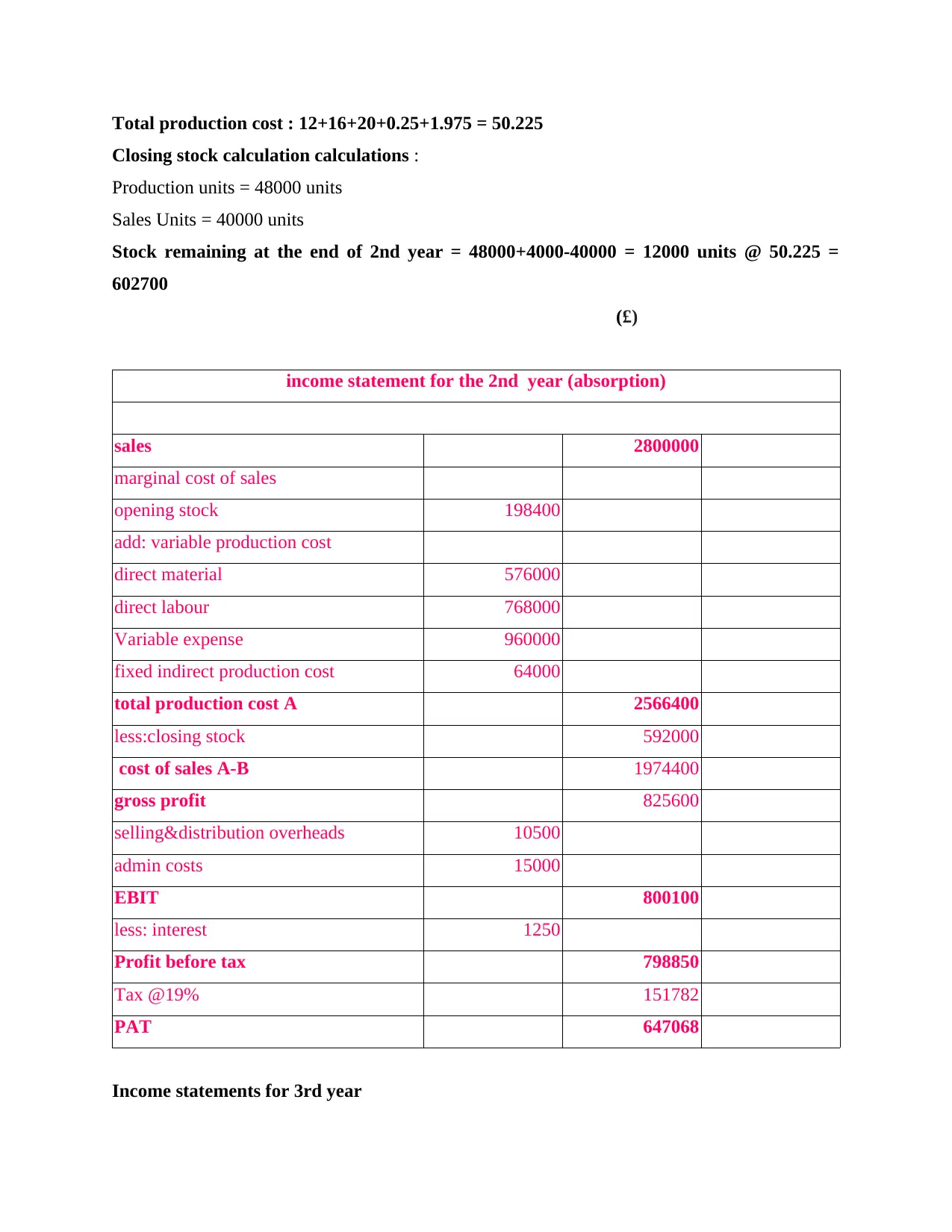

Total production cost : 12+16+20+0.25+1.975 = 50.225

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 2nd year = 48000+4000-40000 = 12000 units @ 50.225 =

602700

(£)

income statement for the 2nd year (absorption)

sales 2800000

marginal cost of sales

opening stock 198400

add: variable production cost

direct material 576000

direct labour 768000

Variable expense 960000

fixed indirect production cost 64000

total production cost A 2566400

less:closing stock 592000

cost of sales A-B 1974400

gross profit 825600

selling&distribution overheads 10500

admin costs 15000

EBIT 800100

less: interest 1250

Profit before tax 798850

Tax @19% 151782

PAT 647068

Income statements for 3rd year

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 2nd year = 48000+4000-40000 = 12000 units @ 50.225 =

602700

(£)

income statement for the 2nd year (absorption)

sales 2800000

marginal cost of sales

opening stock 198400

add: variable production cost

direct material 576000

direct labour 768000

Variable expense 960000

fixed indirect production cost 64000

total production cost A 2566400

less:closing stock 592000

cost of sales A-B 1974400

gross profit 825600

selling&distribution overheads 10500

admin costs 15000

EBIT 800100

less: interest 1250

Profit before tax 798850

Tax @19% 151782

PAT 647068

Income statements for 3rd year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

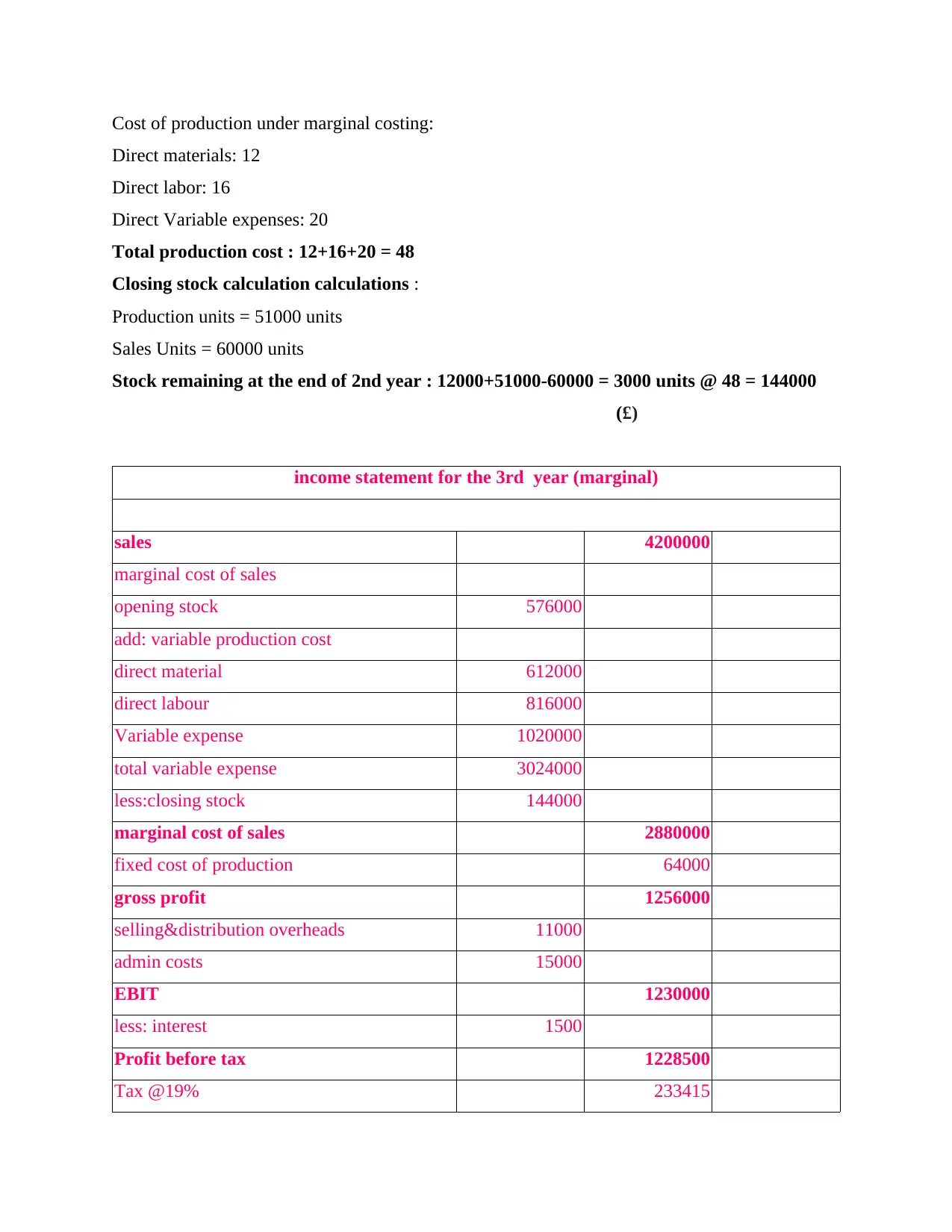

Cost of production under marginal costing:

Direct materials: 12

Direct labor: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 51000 units

Sales Units = 60000 units

Stock remaining at the end of 2nd year : 12000+51000-60000 = 3000 units @ 48 = 144000

(£)

income statement for the 3rd year (marginal)

sales 4200000

marginal cost of sales

opening stock 576000

add: variable production cost

direct material 612000

direct labour 816000

Variable expense 1020000

total variable expense 3024000

less:closing stock 144000

marginal cost of sales 2880000

fixed cost of production 64000

gross profit 1256000

selling&distribution overheads 11000

admin costs 15000

EBIT 1230000

less: interest 1500

Profit before tax 1228500

Tax @19% 233415

Direct materials: 12

Direct labor: 16

Direct Variable expenses: 20

Total production cost : 12+16+20 = 48

Closing stock calculation calculations :

Production units = 51000 units

Sales Units = 60000 units

Stock remaining at the end of 2nd year : 12000+51000-60000 = 3000 units @ 48 = 144000

(£)

income statement for the 3rd year (marginal)

sales 4200000

marginal cost of sales

opening stock 576000

add: variable production cost

direct material 612000

direct labour 816000

Variable expense 1020000

total variable expense 3024000

less:closing stock 144000

marginal cost of sales 2880000

fixed cost of production 64000

gross profit 1256000

selling&distribution overheads 11000

admin costs 15000

EBIT 1230000

less: interest 1500

Profit before tax 1228500

Tax @19% 233415

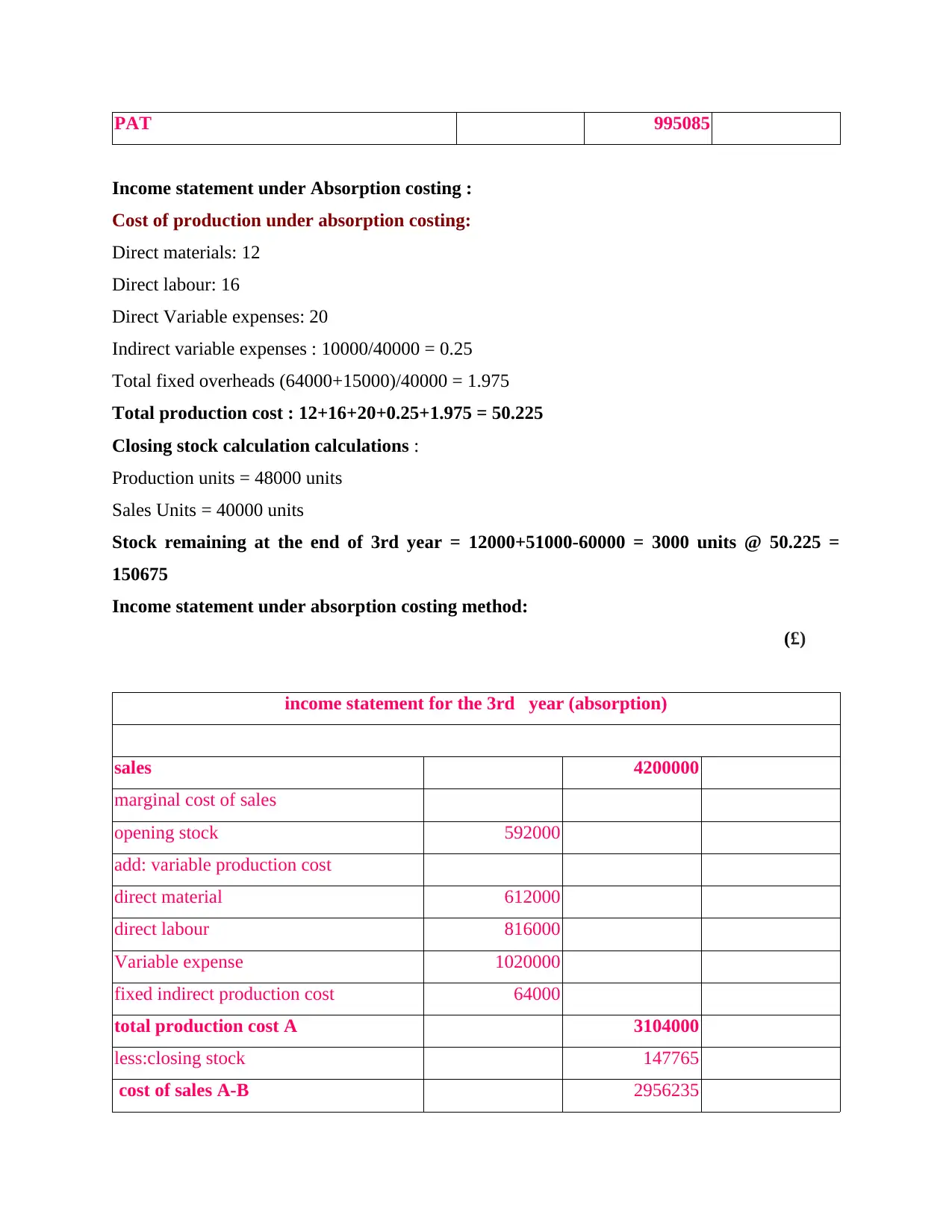

PAT 995085

Income statement under Absorption costing :

Cost of production under absorption costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

Total production cost : 12+16+20+0.25+1.975 = 50.225

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 3rd year = 12000+51000-60000 = 3000 units @ 50.225 =

150675

Income statement under absorption costing method:

(£)

income statement for the 3rd year (absorption)

sales 4200000

marginal cost of sales

opening stock 592000

add: variable production cost

direct material 612000

direct labour 816000

Variable expense 1020000

fixed indirect production cost 64000

total production cost A 3104000

less:closing stock 147765

cost of sales A-B 2956235

Income statement under Absorption costing :

Cost of production under absorption costing:

Direct materials: 12

Direct labour: 16

Direct Variable expenses: 20

Indirect variable expenses : 10000/40000 = 0.25

Total fixed overheads (64000+15000)/40000 = 1.975

Total production cost : 12+16+20+0.25+1.975 = 50.225

Closing stock calculation calculations :

Production units = 48000 units

Sales Units = 40000 units

Stock remaining at the end of 3rd year = 12000+51000-60000 = 3000 units @ 50.225 =

150675

Income statement under absorption costing method:

(£)

income statement for the 3rd year (absorption)

sales 4200000

marginal cost of sales

opening stock 592000

add: variable production cost

direct material 612000

direct labour 816000

Variable expense 1020000

fixed indirect production cost 64000

total production cost A 3104000

less:closing stock 147765

cost of sales A-B 2956235

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

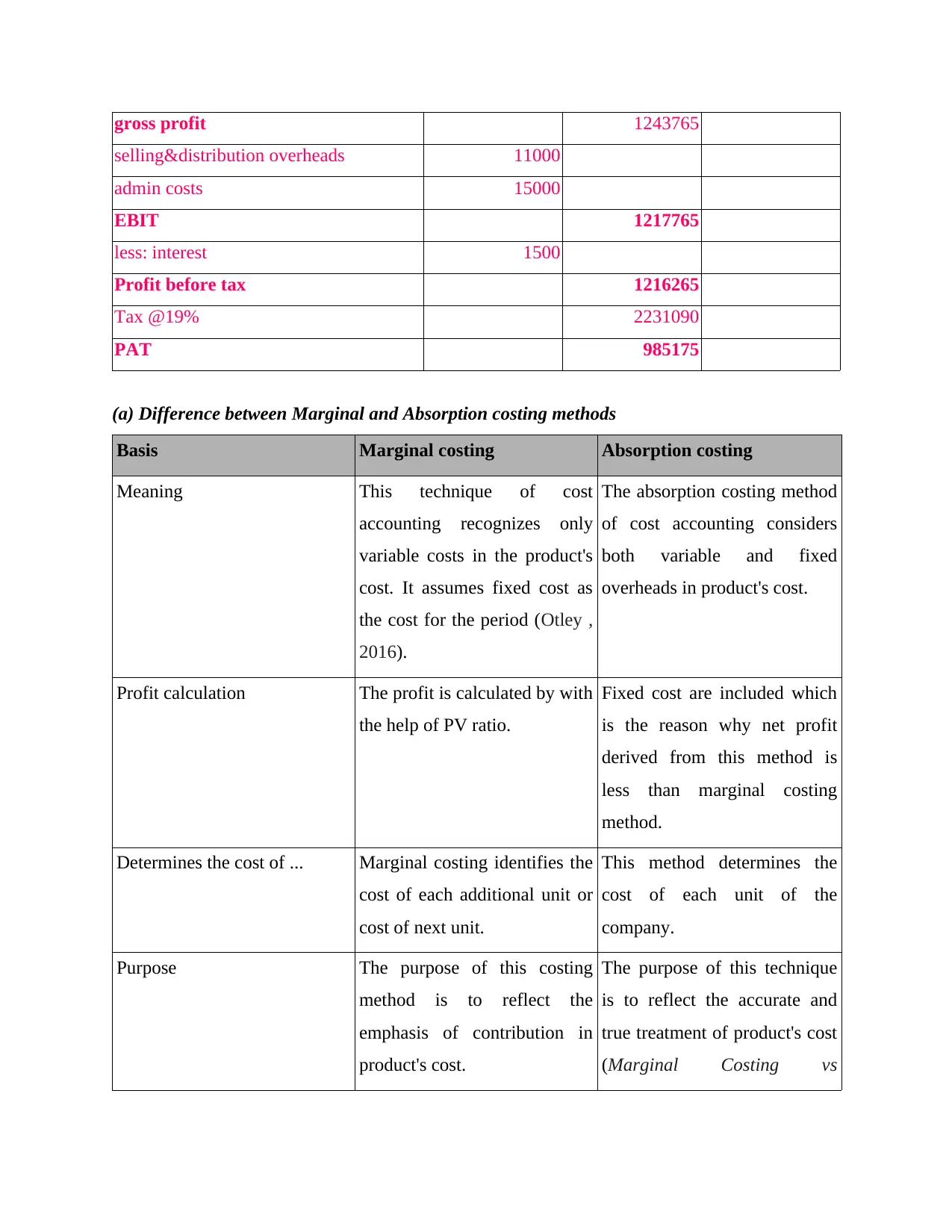

gross profit 1243765

selling&distribution overheads 11000

admin costs 15000

EBIT 1217765

less: interest 1500

Profit before tax 1216265

Tax @19% 2231090

PAT 985175

(a) Difference between Marginal and Absorption costing methods

Basis Marginal costing Absorption costing

Meaning This technique of cost

accounting recognizes only

variable costs in the product's

cost. It assumes fixed cost as

the cost for the period (Otley ,

2016).

The absorption costing method

of cost accounting considers

both variable and fixed

overheads in product's cost.

Profit calculation The profit is calculated by with

the help of PV ratio.

Fixed cost are included which

is the reason why net profit

derived from this method is

less than marginal costing

method.

Determines the cost of ... Marginal costing identifies the

cost of each additional unit or

cost of next unit.

This method determines the

cost of each unit of the

company.

Purpose The purpose of this costing

method is to reflect the

emphasis of contribution in

product's cost.

The purpose of this technique

is to reflect the accurate and

true treatment of product's cost

(Marginal Costing vs

selling&distribution overheads 11000

admin costs 15000

EBIT 1217765

less: interest 1500

Profit before tax 1216265

Tax @19% 2231090

PAT 985175

(a) Difference between Marginal and Absorption costing methods

Basis Marginal costing Absorption costing

Meaning This technique of cost

accounting recognizes only

variable costs in the product's

cost. It assumes fixed cost as

the cost for the period (Otley ,

2016).

The absorption costing method

of cost accounting considers

both variable and fixed

overheads in product's cost.

Profit calculation The profit is calculated by with

the help of PV ratio.

Fixed cost are included which

is the reason why net profit

derived from this method is

less than marginal costing

method.

Determines the cost of ... Marginal costing identifies the

cost of each additional unit or

cost of next unit.

This method determines the

cost of each unit of the

company.

Purpose The purpose of this costing

method is to reflect the

emphasis of contribution in

product's cost.

The purpose of this technique

is to reflect the accurate and

true treatment of product's cost

(Marginal Costing vs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption Costing, 2018).

(b) Use of marginal costing in business

Marginal costing is a method of costing accounting that the deals with the identification

of cost of a product and analysation of cost information for assisting management in its decision-

making process.

The chair manufacturing company uses this technique in the following areas that are

discussed below:

Cost control : As the method focuses on variable costs, it provides the management a

tool for controlling these variable expenses in the company that are contributing directly to the

product's cost. Bifurcation of cost into fixed and variable helps the mangers of manufacturing

business in keeping control over the cost of production, making the operations efficient (Wouters

and et.al., 2018.).

Determination of cost of product : The cost accountant in the manufacturing

organisation applies this method for recording and finding out the cost of its chairs. Clear

distinction between the fixed and variable cost makes the cost determination clear for the

manager.

Decision making : The marginal costing is used by the business organisation for forming

rationale and optimum decisions. The method analyses the cost information that assists the

management in taking their day to day decisions. The areas where this method solves problems

are; profit planning, make or buy decisions, product mix and product's pricing (Maas,

Schaltegger and Crutzen, 2016).

(c) Reasons for variance in profits under different costing methods

From the above calculations, the difference between net profits under marginal and

absorption method is clearly visible. In the 1st year, net profit under marginal method is (£)

722000 whereas the net profit under absorption method (£) 711900. The difference was due to

the treatment of fixed overheads under the absorption method. Marginal costing only considered

variable expenses in product cost which became the basis for valuing the closing stock. The

absorption costing method considered fixed and variable both the expenses in its products cost,

which then became the basis for valuing its opening and closing stock. It is always for this reason

(b) Use of marginal costing in business

Marginal costing is a method of costing accounting that the deals with the identification

of cost of a product and analysation of cost information for assisting management in its decision-

making process.

The chair manufacturing company uses this technique in the following areas that are

discussed below:

Cost control : As the method focuses on variable costs, it provides the management a

tool for controlling these variable expenses in the company that are contributing directly to the

product's cost. Bifurcation of cost into fixed and variable helps the mangers of manufacturing

business in keeping control over the cost of production, making the operations efficient (Wouters

and et.al., 2018.).

Determination of cost of product : The cost accountant in the manufacturing

organisation applies this method for recording and finding out the cost of its chairs. Clear

distinction between the fixed and variable cost makes the cost determination clear for the

manager.

Decision making : The marginal costing is used by the business organisation for forming

rationale and optimum decisions. The method analyses the cost information that assists the

management in taking their day to day decisions. The areas where this method solves problems

are; profit planning, make or buy decisions, product mix and product's pricing (Maas,

Schaltegger and Crutzen, 2016).

(c) Reasons for variance in profits under different costing methods

From the above calculations, the difference between net profits under marginal and

absorption method is clearly visible. In the 1st year, net profit under marginal method is (£)

722000 whereas the net profit under absorption method (£) 711900. The difference was due to

the treatment of fixed overheads under the absorption method. Marginal costing only considered

variable expenses in product cost which became the basis for valuing the closing stock. The

absorption costing method considered fixed and variable both the expenses in its products cost,

which then became the basis for valuing its opening and closing stock. It is always for this reason

that absorption costing shows less net profit than marginal costing method. Likewise, in the

subsequent years, absorption costing is showing lesser net profit marginal costing because of the

treatment of fixed expenses (Messner, 2016).

TASK 2

Report on Management Accounting

By a management accountant

a) Explaining the use of planning tools used in management accounting

Budgeting is the process of formulating plans of incurring expenses for conducting

business activities for the future. It is expressed in numerical terms. The organisation prepares

budgets on the basis of divisions, departments or for the overall company. These plans or budgets

are usually prepared for the shorter period like one year, six months etc. Budgets are the most

effective way of controlling the costs and operations of the business organisation. The

advantage of preparing budget is that it acts as guideline for spending the funds appropriately.

Limitation of the budget is that it is prepared on the basis of historical data that does not help in

forecasting expenses accurately.

There are different planning tools of budgetary control that are explained below:

Fixed budgets : These are those budgets that does not change due to change in other

variables of a budget such as sales volume, income etc., but remains constant. The costs and

expenses under this budget is estimated on the basis of the data gathered and analysed before the

starting of budget period in the company (Chenhall and Moers, 2015).

Advantages :

The fixed budgets are easier to formulate and implemented because it does not call for

continuous updates of facts and figures during budget period.

It helps the organisation in prioritising its expenses.

Disadvantages :

The biggest limitation of fixed budget is that it does not provide room for flexibility. It

does not make any amendments in its estimated figure.

These are prepared on the basis of historical data which is not so relevant for the decision

making. Companies that faces high fluctuation in their sales volume and income cannot

subsequent years, absorption costing is showing lesser net profit marginal costing because of the

treatment of fixed expenses (Messner, 2016).

TASK 2

Report on Management Accounting

By a management accountant

a) Explaining the use of planning tools used in management accounting

Budgeting is the process of formulating plans of incurring expenses for conducting

business activities for the future. It is expressed in numerical terms. The organisation prepares

budgets on the basis of divisions, departments or for the overall company. These plans or budgets

are usually prepared for the shorter period like one year, six months etc. Budgets are the most

effective way of controlling the costs and operations of the business organisation. The

advantage of preparing budget is that it acts as guideline for spending the funds appropriately.

Limitation of the budget is that it is prepared on the basis of historical data that does not help in

forecasting expenses accurately.

There are different planning tools of budgetary control that are explained below:

Fixed budgets : These are those budgets that does not change due to change in other

variables of a budget such as sales volume, income etc., but remains constant. The costs and

expenses under this budget is estimated on the basis of the data gathered and analysed before the

starting of budget period in the company (Chenhall and Moers, 2015).

Advantages :

The fixed budgets are easier to formulate and implemented because it does not call for

continuous updates of facts and figures during budget period.

It helps the organisation in prioritising its expenses.

Disadvantages :

The biggest limitation of fixed budget is that it does not provide room for flexibility. It

does not make any amendments in its estimated figure.

These are prepared on the basis of historical data which is not so relevant for the decision

making. Companies that faces high fluctuation in their sales volume and income cannot

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.