Management Accounting Report: Grange Aggregates Company Analysis

VerifiedAdded on 2021/02/21

|18

|6205

|571

Report

AI Summary

This report provides a detailed overview of management accounting, focusing on its functions, systems, and applications within a business context. It begins by defining management accounting and differentiating it from financial accounting, emphasizing its role in internal decision-making. The report then explores various management accounting systems, including price optimization, cost accounting, inventory management, and job costing systems, illustrating their practical application with examples from Grange Aggregates Company. It further discusses the presentation of financial information, different types of management accounting reports (performance, budget, and inventory management), and the crucial role of management accounting in strategic planning and resource management. The report also covers cost analysis techniques, including direct vs. indirect costs, fixed vs. variable costs, and absorption costing, to analyze cost behavior and improve profitability.

UNIT 5:

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and different types of management accounting systems:...................3

TASK 2............................................................................................................................................7

Computation of cost applying appropriate techniques:...............................................................7

TASK 3..........................................................................................................................................10

Application of various budgets in respect of control and planning:.........................................10

Pricing strategy..............................................................................................................................12

TASK 4..........................................................................................................................................12

Identification of various Financial problem and techniques for responding financial problems:

...................................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and different types of management accounting systems:...................3

TASK 2............................................................................................................................................7

Computation of cost applying appropriate techniques:...............................................................7

TASK 3..........................................................................................................................................10

Application of various budgets in respect of control and planning:.........................................10

Pricing strategy..............................................................................................................................12

TASK 4..........................................................................................................................................12

Identification of various Financial problem and techniques for responding financial problems:

...................................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

In business term management accounting contains functions and tasks directly or

indirectly connected with collecting and transferring financial information within entity to

provide assistance in decision making processes. It is adopted by business entities to manage

their functions in structured way to attain predetermined targets or objectives. It provides

smoothness in process of implementation of strategies and formulation of plans (Astuty, 2019).

In establishing of internal control and check systems at different level within an entity,

management accounting plays a significant role. In this context, this report provides a detailed

explanation about different elements of management accounting system, reporting methods of

management accounting, advantages of different systems of management accounting and

application of planning tools in context of Grange Aggregates Company. It is UK based

company and engaged in manufacturing of construction material like cement, concrete and other

construction aggregates. Report also includes a comparison of two organisations which are

adapting systems of management accounting in order to responding financial problems.

TASK 1

1 Management accounting and different types of management accounting systems:

In a business entity there are various function and activities which generates numerous

kind information of information, some of them may be irrelevant for management. Management

accounting system provides relevant information which assist management in process of taking

decisions for achieving business objectives. It includes function such as systematic classification

of information, entering information, measuring whether information is valuable for business

organisation and at last communicate them for conducting process of taking decision effectively.

There are various systems of management accounting that covers different aspects of an

enterprise's business. Following is discussion about different management accounting systems,

as follows:

Price optimisation system- Every organisation put their efforts to make expansion in

market but due to high competition and large number of competitors they are forced to put down

price of product. In this system clients or customers’ response is used to analyse the relationship

of demand and price of product (Barnard and Mostert, 2015). Under price optimisation system a

particular price is identified by business organisation at which demand is of product is high and

In business term management accounting contains functions and tasks directly or

indirectly connected with collecting and transferring financial information within entity to

provide assistance in decision making processes. It is adopted by business entities to manage

their functions in structured way to attain predetermined targets or objectives. It provides

smoothness in process of implementation of strategies and formulation of plans (Astuty, 2019).

In establishing of internal control and check systems at different level within an entity,

management accounting plays a significant role. In this context, this report provides a detailed

explanation about different elements of management accounting system, reporting methods of

management accounting, advantages of different systems of management accounting and

application of planning tools in context of Grange Aggregates Company. It is UK based

company and engaged in manufacturing of construction material like cement, concrete and other

construction aggregates. Report also includes a comparison of two organisations which are

adapting systems of management accounting in order to responding financial problems.

TASK 1

1 Management accounting and different types of management accounting systems:

In a business entity there are various function and activities which generates numerous

kind information of information, some of them may be irrelevant for management. Management

accounting system provides relevant information which assist management in process of taking

decisions for achieving business objectives. It includes function such as systematic classification

of information, entering information, measuring whether information is valuable for business

organisation and at last communicate them for conducting process of taking decision effectively.

There are various systems of management accounting that covers different aspects of an

enterprise's business. Following is discussion about different management accounting systems,

as follows:

Price optimisation system- Every organisation put their efforts to make expansion in

market but due to high competition and large number of competitors they are forced to put down

price of product. In this system clients or customers’ response is used to analyse the relationship

of demand and price of product (Barnard and Mostert, 2015). Under price optimisation system a

particular price is identified by business organisation at which demand is of product is high and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also company is gaining competitive advantages. In Grange Aggregates Company this system

helps to fix a price of its construction material equal to or below the competitive brand to take

competitive benefits. It also helps to increase the demand of product by setting a specific price of

its various construction materials.

Cost Accounting System: This is cost focused management accounting system because

this system combines activities related to recording, summarising, classifying, controlling and

monitoring of costs and expenses within a business enterprise. In manufacturing concern like

Grange Aggregates Company apply this system help in controlling costs and reducing them to

increase operating profits of company (Bedford and Speklé, 2018). For instance, in production of

construction material like cement, concentrate and other aggregates, it is hard for company to

analyse reason of increase in cost among large number of production processes so management

with help of this system identifies the main cause of excessive costs.

Inventory management system: in organisation like Grange Aggregates Company,

there are large variety of products are produced by company and there are numerous kind of

inventories such as finished goods, unprocessed goods, finished inventories etc. Inventory

management system help in organising different inventories by combining activities like

classification of inventories, inventory recording and monitoring inventories to manage

inventories in efficient way (Bolt-Lee and Monte Swain, 2016). In Grange, it is applied by

manufacturing and process heads to control the movement of stock and optimise inventory costs

like handling or storage to increase per unit profit, it also assists in ensuring availability of

inventories in warehouse for manufacturing process. Following are two most common methods

of inventory valuation used by company, as follows:

LIFO – In this method inventories are managed with assumption that last or recently

purchased inventories are sold first.

FIFO – In this method inventories are managed with assumption that inventory

purchased in first would be sold first.

AVOC – Under this method inventories are valued at average of cost of inventories

purchased at different price and date.

Job costing system – In organisations that have products which are totally unrelated, this

system of costing is adopted. This system purely focused on classification of products as a task

and assign different cost to such job. In Grange Aggregates Company, this system is used to

helps to fix a price of its construction material equal to or below the competitive brand to take

competitive benefits. It also helps to increase the demand of product by setting a specific price of

its various construction materials.

Cost Accounting System: This is cost focused management accounting system because

this system combines activities related to recording, summarising, classifying, controlling and

monitoring of costs and expenses within a business enterprise. In manufacturing concern like

Grange Aggregates Company apply this system help in controlling costs and reducing them to

increase operating profits of company (Bedford and Speklé, 2018). For instance, in production of

construction material like cement, concentrate and other aggregates, it is hard for company to

analyse reason of increase in cost among large number of production processes so management

with help of this system identifies the main cause of excessive costs.

Inventory management system: in organisation like Grange Aggregates Company,

there are large variety of products are produced by company and there are numerous kind of

inventories such as finished goods, unprocessed goods, finished inventories etc. Inventory

management system help in organising different inventories by combining activities like

classification of inventories, inventory recording and monitoring inventories to manage

inventories in efficient way (Bolt-Lee and Monte Swain, 2016). In Grange, it is applied by

manufacturing and process heads to control the movement of stock and optimise inventory costs

like handling or storage to increase per unit profit, it also assists in ensuring availability of

inventories in warehouse for manufacturing process. Following are two most common methods

of inventory valuation used by company, as follows:

LIFO – In this method inventories are managed with assumption that last or recently

purchased inventories are sold first.

FIFO – In this method inventories are managed with assumption that inventory

purchased in first would be sold first.

AVOC – Under this method inventories are valued at average of cost of inventories

purchased at different price and date.

Job costing system – In organisations that have products which are totally unrelated, this

system of costing is adopted. This system purely focused on classification of products as a task

and assign different cost to such job. In Grange Aggregates Company, this system is used to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

classify some of their construction materials in jobs to attain effective accountability. This

system is used to analyse the reason of excess cost making jobs and minimise costs to achieve

efficiency in job processes.

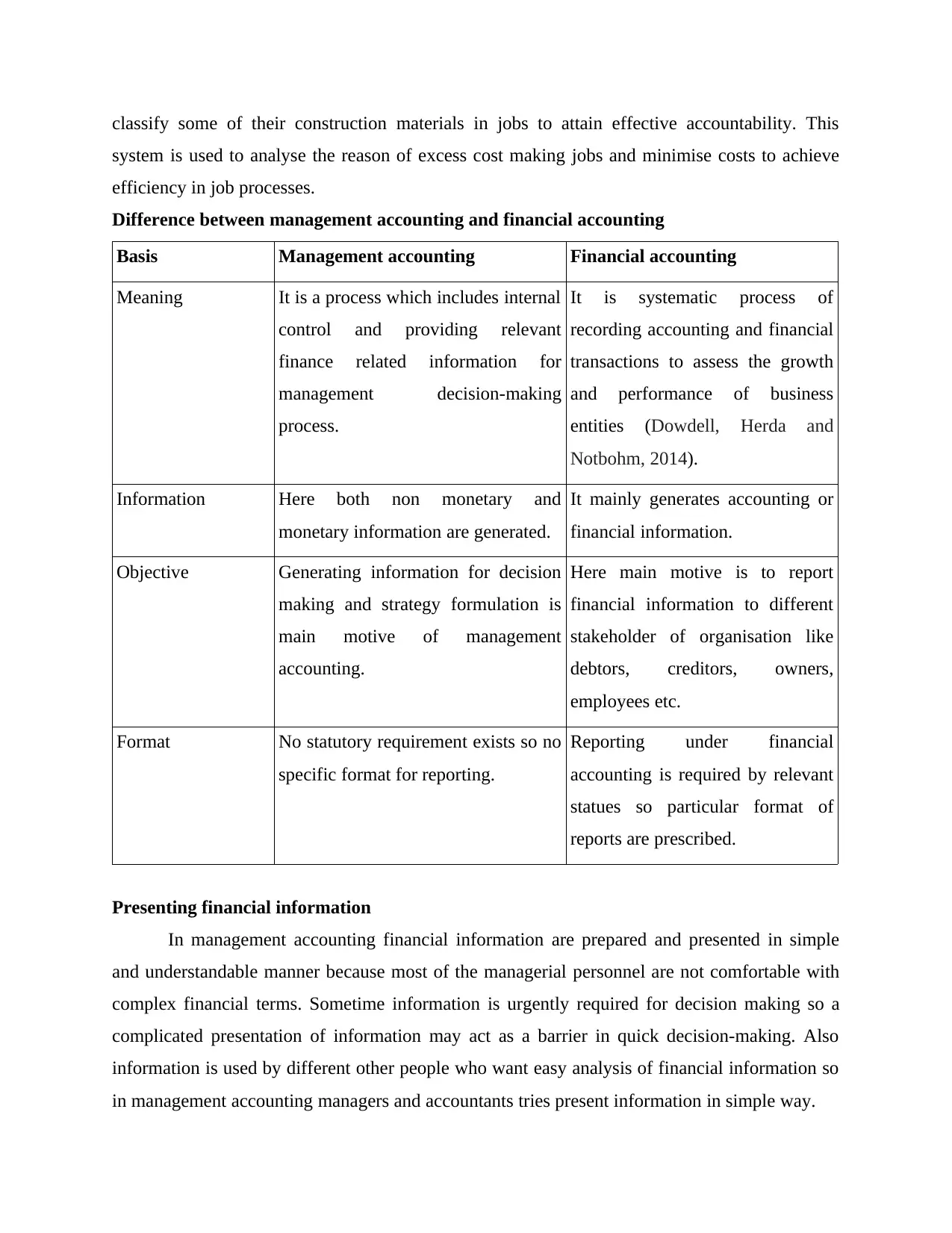

Difference between management accounting and financial accounting

Basis Management accounting Financial accounting

Meaning It is a process which includes internal

control and providing relevant

finance related information for

management decision-making

process.

It is systematic process of

recording accounting and financial

transactions to assess the growth

and performance of business

entities (Dowdell, Herda and

Notbohm, 2014).

Information Here both non monetary and

monetary information are generated.

It mainly generates accounting or

financial information.

Objective Generating information for decision

making and strategy formulation is

main motive of management

accounting.

Here main motive is to report

financial information to different

stakeholder of organisation like

debtors, creditors, owners,

employees etc.

Format No statutory requirement exists so no

specific format for reporting.

Reporting under financial

accounting is required by relevant

statues so particular format of

reports are prescribed.

Presenting financial information

In management accounting financial information are prepared and presented in simple

and understandable manner because most of the managerial personnel are not comfortable with

complex financial terms. Sometime information is urgently required for decision making so a

complicated presentation of information may act as a barrier in quick decision-making. Also

information is used by different other people who want easy analysis of financial information so

in management accounting managers and accountants tries present information in simple way.

system is used to analyse the reason of excess cost making jobs and minimise costs to achieve

efficiency in job processes.

Difference between management accounting and financial accounting

Basis Management accounting Financial accounting

Meaning It is a process which includes internal

control and providing relevant

finance related information for

management decision-making

process.

It is systematic process of

recording accounting and financial

transactions to assess the growth

and performance of business

entities (Dowdell, Herda and

Notbohm, 2014).

Information Here both non monetary and

monetary information are generated.

It mainly generates accounting or

financial information.

Objective Generating information for decision

making and strategy formulation is

main motive of management

accounting.

Here main motive is to report

financial information to different

stakeholder of organisation like

debtors, creditors, owners,

employees etc.

Format No statutory requirement exists so no

specific format for reporting.

Reporting under financial

accounting is required by relevant

statues so particular format of

reports are prescribed.

Presenting financial information

In management accounting financial information are prepared and presented in simple

and understandable manner because most of the managerial personnel are not comfortable with

complex financial terms. Sometime information is urgently required for decision making so a

complicated presentation of information may act as a barrier in quick decision-making. Also

information is used by different other people who want easy analysis of financial information so

in management accounting managers and accountants tries present information in simple way.

Different types of managerial accounting reports

Reports are used by managers to communicate the performance of company over a

particular period. In this context management accounting also provides reporting of outcomes of

its different systems. In management accounting reporting, reports are generated through

management accounting systems are reported by lower level managers and process heads to top

level management. Following are reports under management accounting reporting, as discussed:

Performance Report: This report is mainly concerned with evaluation of performance,

skills, efficiencies and abilities of employees over a period. Main objectives of this report is to

keep tracking of performance of workers and employees and assess how effectively they are

engaged in achievement of entity's targets/goals (Gunarathne, 2015). In Grange Aggregates

Company, this report helps to ensure proper utilisation of human resources. It also helps to

control the employees cost in company and, to recognise and promote skill and efficient

employees. It provides a base for promotion and rewards of employees and workers.

Budget Report: Budget reports are important statements which provides a detailed

projection of each and every income and expense of an organisation in order to budgeted or

standard targets. Different kind of budgets such as sales budget, cash budget, inventory budget,

purchase budget etc. help in analysis of all aspects of business organisation. In Grange

Aggregates Company, budgets reports are used to analyse the operating effectiveness of different

activities and functions over a specific period to achieve targets. Budget provide a comparative

evaluation of projected performance and actual performance of company in terms of different

financial areas like sales, inventories, purchase, cash etc.

Inventory Management Report: Inventory report is significant report which provide a

detailed description of various inventories and manage them in effective manner to control

inventory costs. This report is generally prepared on weekly or monthly basis. Grange

Aggregates Company use this report to ensure the adequateness of raw items required for

manufacturing of cement, concentrate and other materials of construction. These report also

provide assistance in minimising storage and handling expenses of stock in company to reduce

overall cost of production (Taschner, 2015).

Role of management accounting: Major role of management accounting is performing set of

different functions to provide assurance about safeguard of fiscal resources, forecasting and other

important matters. It provide assistance in effective forecasting, decision making and, analysis of

Reports are used by managers to communicate the performance of company over a

particular period. In this context management accounting also provides reporting of outcomes of

its different systems. In management accounting reporting, reports are generated through

management accounting systems are reported by lower level managers and process heads to top

level management. Following are reports under management accounting reporting, as discussed:

Performance Report: This report is mainly concerned with evaluation of performance,

skills, efficiencies and abilities of employees over a period. Main objectives of this report is to

keep tracking of performance of workers and employees and assess how effectively they are

engaged in achievement of entity's targets/goals (Gunarathne, 2015). In Grange Aggregates

Company, this report helps to ensure proper utilisation of human resources. It also helps to

control the employees cost in company and, to recognise and promote skill and efficient

employees. It provides a base for promotion and rewards of employees and workers.

Budget Report: Budget reports are important statements which provides a detailed

projection of each and every income and expense of an organisation in order to budgeted or

standard targets. Different kind of budgets such as sales budget, cash budget, inventory budget,

purchase budget etc. help in analysis of all aspects of business organisation. In Grange

Aggregates Company, budgets reports are used to analyse the operating effectiveness of different

activities and functions over a specific period to achieve targets. Budget provide a comparative

evaluation of projected performance and actual performance of company in terms of different

financial areas like sales, inventories, purchase, cash etc.

Inventory Management Report: Inventory report is significant report which provide a

detailed description of various inventories and manage them in effective manner to control

inventory costs. This report is generally prepared on weekly or monthly basis. Grange

Aggregates Company use this report to ensure the adequateness of raw items required for

manufacturing of cement, concentrate and other materials of construction. These report also

provide assistance in minimising storage and handling expenses of stock in company to reduce

overall cost of production (Taschner, 2015).

Role of management accounting: Major role of management accounting is performing set of

different functions to provide assurance about safeguard of fiscal resources, forecasting and other

important matters. It provide assistance in effective forecasting, decision making and, analysis of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

any variance in performance, cash flows, current and proposed rate of return to attain

organisation's targets. It also play role in strategic planning and circulating crucial information

among different level of management.

TASK 2

1 Computation of cost applying appropriate techniques:

Cost and cost analysis: Cost and expenses are most significant aspect of a business

organisation. In manufacturing company like Grange Aggregates Company, costs and expenses

have considerable effect on price of product and net profit of company. Minimisation of cost is

important for company to increase their profit margin and to make expansion in market, for this

systematic analysis of various costs is required. In cost analysis cost column profit, flexible

budget, cost variances etc. are used by accountant to increase effectiveness of analysis. Under

analysis of cost all the factors are critically evaluated by managers to optimise cost and allocate

areas which lead to increase in costs and expenses. Following are major kind of costs, as follows:

Direct and indirect costs: Direct costs are expenses which are directly concerned with

manufacturing of product or services. Whereas indirect costs are cost that are not directly

attributable to product cost (Harris and Cassidy, 2014).

Fixed and variable costs: Fixed costs are expenses which does not varies with change in

volume of production whereas variable costs are cost which fluctuates as the numbers of

units produced increases or decreases.

Production and non production expenses: Cost associated with manufacturing of product

is classified as production expenses and other all expenses are considered as non

production expenses.

Absorption costing: It is a kind of costing method in which expenses are classified in fixed and

variables, separately disclosed while calculating net income of business organisation.

Marginal Costing: Under this method of costing, all fixed costs are considered as period

expenses. It is just opposite approach so here only variable expenses are regarded as cost of

goods sold.

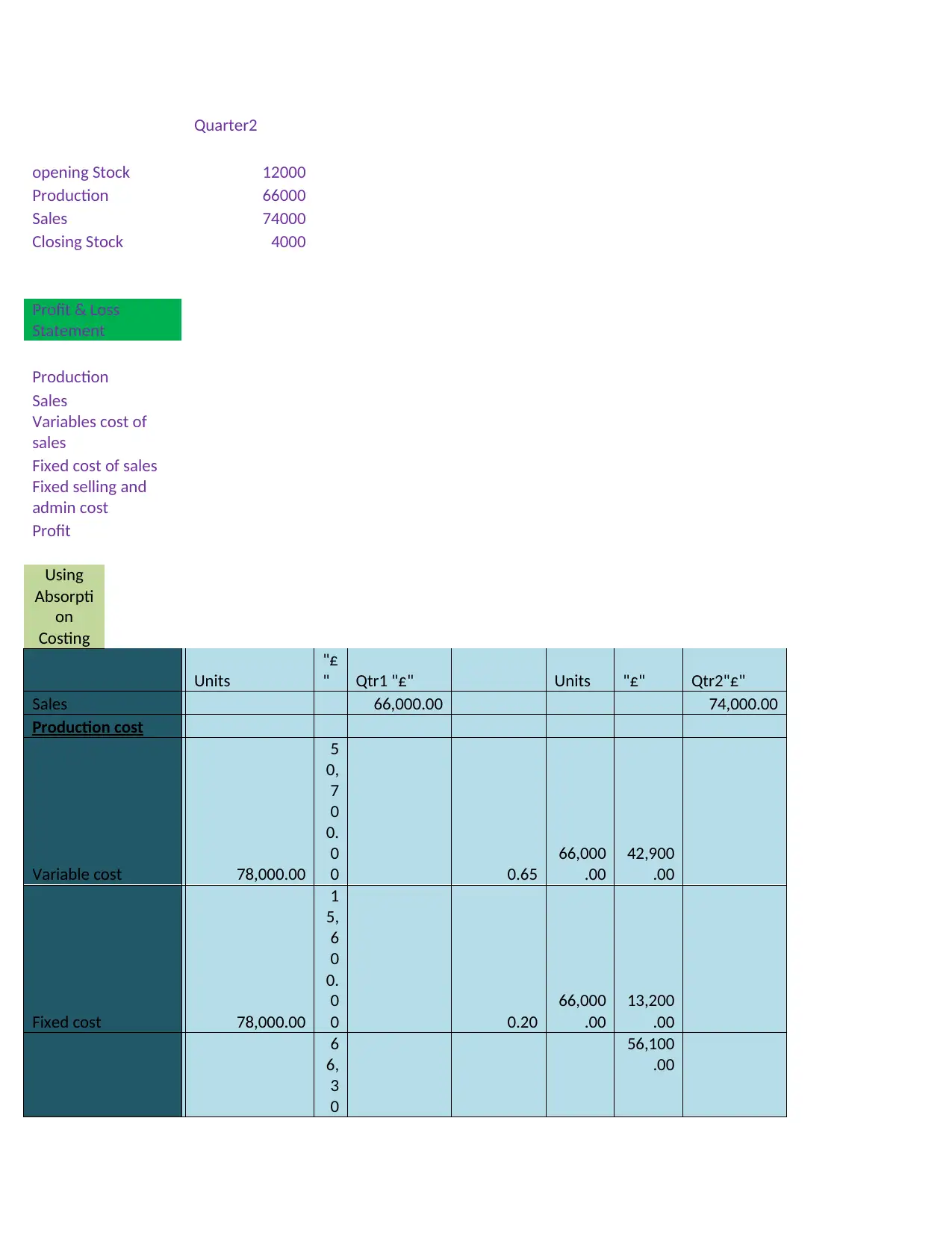

Actual production,

sales and stock in

units for quarters 1

and 2 are:

organisation's targets. It also play role in strategic planning and circulating crucial information

among different level of management.

TASK 2

1 Computation of cost applying appropriate techniques:

Cost and cost analysis: Cost and expenses are most significant aspect of a business

organisation. In manufacturing company like Grange Aggregates Company, costs and expenses

have considerable effect on price of product and net profit of company. Minimisation of cost is

important for company to increase their profit margin and to make expansion in market, for this

systematic analysis of various costs is required. In cost analysis cost column profit, flexible

budget, cost variances etc. are used by accountant to increase effectiveness of analysis. Under

analysis of cost all the factors are critically evaluated by managers to optimise cost and allocate

areas which lead to increase in costs and expenses. Following are major kind of costs, as follows:

Direct and indirect costs: Direct costs are expenses which are directly concerned with

manufacturing of product or services. Whereas indirect costs are cost that are not directly

attributable to product cost (Harris and Cassidy, 2014).

Fixed and variable costs: Fixed costs are expenses which does not varies with change in

volume of production whereas variable costs are cost which fluctuates as the numbers of

units produced increases or decreases.

Production and non production expenses: Cost associated with manufacturing of product

is classified as production expenses and other all expenses are considered as non

production expenses.

Absorption costing: It is a kind of costing method in which expenses are classified in fixed and

variables, separately disclosed while calculating net income of business organisation.

Marginal Costing: Under this method of costing, all fixed costs are considered as period

expenses. It is just opposite approach so here only variable expenses are regarded as cost of

goods sold.

Actual production,

sales and stock in

units for quarters 1

and 2 are:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quarter2

opening Stock 12000

Production 66000

Sales 74000

Closing Stock 4000

Profit & Loss

Statement

Production

Sales

Variables cost of

sales

Fixed cost of sales

Fixed selling and

admin cost

Profit

Using

Absorpti

on

Costing

Units

"£

" Qtr1 "£" Units "£" Qtr2"£"

Sales 66,000.00 74,000.00

Production cost

Variable cost 78,000.00

5

0,

7

0

0.

0

0 0.65

66,000

.00

42,900

.00

Fixed cost 78,000.00

1

5,

6

0

0.

0

0 0.20

66,000

.00

13,200

.00

6

6,

3

0

56,100

.00

opening Stock 12000

Production 66000

Sales 74000

Closing Stock 4000

Profit & Loss

Statement

Production

Sales

Variables cost of

sales

Fixed cost of sales

Fixed selling and

admin cost

Profit

Using

Absorpti

on

Costing

Units

"£

" Qtr1 "£" Units "£" Qtr2"£"

Sales 66,000.00 74,000.00

Production cost

Variable cost 78,000.00

5

0,

7

0

0.

0

0 0.65

66,000

.00

42,900

.00

Fixed cost 78,000.00

1

5,

6

0

0.

0

0 0.20

66,000

.00

13,200

.00

6

6,

3

0

56,100

.00

0.

0

0

Add: Opening Stock 0.00

0.

0

0 0.85

12,000

.00

10,200

.00

Total stock available

for sale

6

6,

3

0

0.

0

0

66,300

.00

Less Closing stock 12,000.00

1

0,

2

0

0.

0

0 0.85

4,000.

00

3,400.

00

56,100.00 62,900.00

Gross profit 9,900.00 11,100.00

Less: under

absorption or Fixed

Overhead 0.20 400.00 0.20 2,800.00

Selling & Admin

Costs 5,200.00

Selling &

Admin

Costs 5,200.00

Net Profit 4,300.00 3,100.00

Profit &

Loss

Stateme

nt Using

Marginal

Costing

Units

"£

" Qtr1 "£" Units "£" Qtr2"£"

Sales 66,000.00 74,000.00

Production cost

Variable cost 78,000.00 5

0,

7

0.65 66,000

.00

42,900

.00

0

0

Add: Opening Stock 0.00

0.

0

0 0.85

12,000

.00

10,200

.00

Total stock available

for sale

6

6,

3

0

0.

0

0

66,300

.00

Less Closing stock 12,000.00

1

0,

2

0

0.

0

0 0.85

4,000.

00

3,400.

00

56,100.00 62,900.00

Gross profit 9,900.00 11,100.00

Less: under

absorption or Fixed

Overhead 0.20 400.00 0.20 2,800.00

Selling & Admin

Costs 5,200.00

Selling &

Admin

Costs 5,200.00

Net Profit 4,300.00 3,100.00

Profit &

Loss

Stateme

nt Using

Marginal

Costing

Units

"£

" Qtr1 "£" Units "£" Qtr2"£"

Sales 66,000.00 74,000.00

Production cost

Variable cost 78,000.00 5

0,

7

0.65 66,000

.00

42,900

.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0

0.

0

0

5

0,

7

0

0.

0

0

42,900

.00

Add: Opening Stock 0.00

0.

0

0 0.65

12,000

.00

7,800.

00

Total stock available

for sale

5

0,

7

0

0.

0

0

50,700

.00

Less Closing stock 12,000.00

7,

8

0

0.

0

0 0.65

4,000.

00

2,600.

00

42,900.00 48,100.00

Gross profit 23,100.00 25,900.00

Fixed Overhead 16,000.00 16,000.00

Selling & Admin

Costs 5,200.00 5,200.00

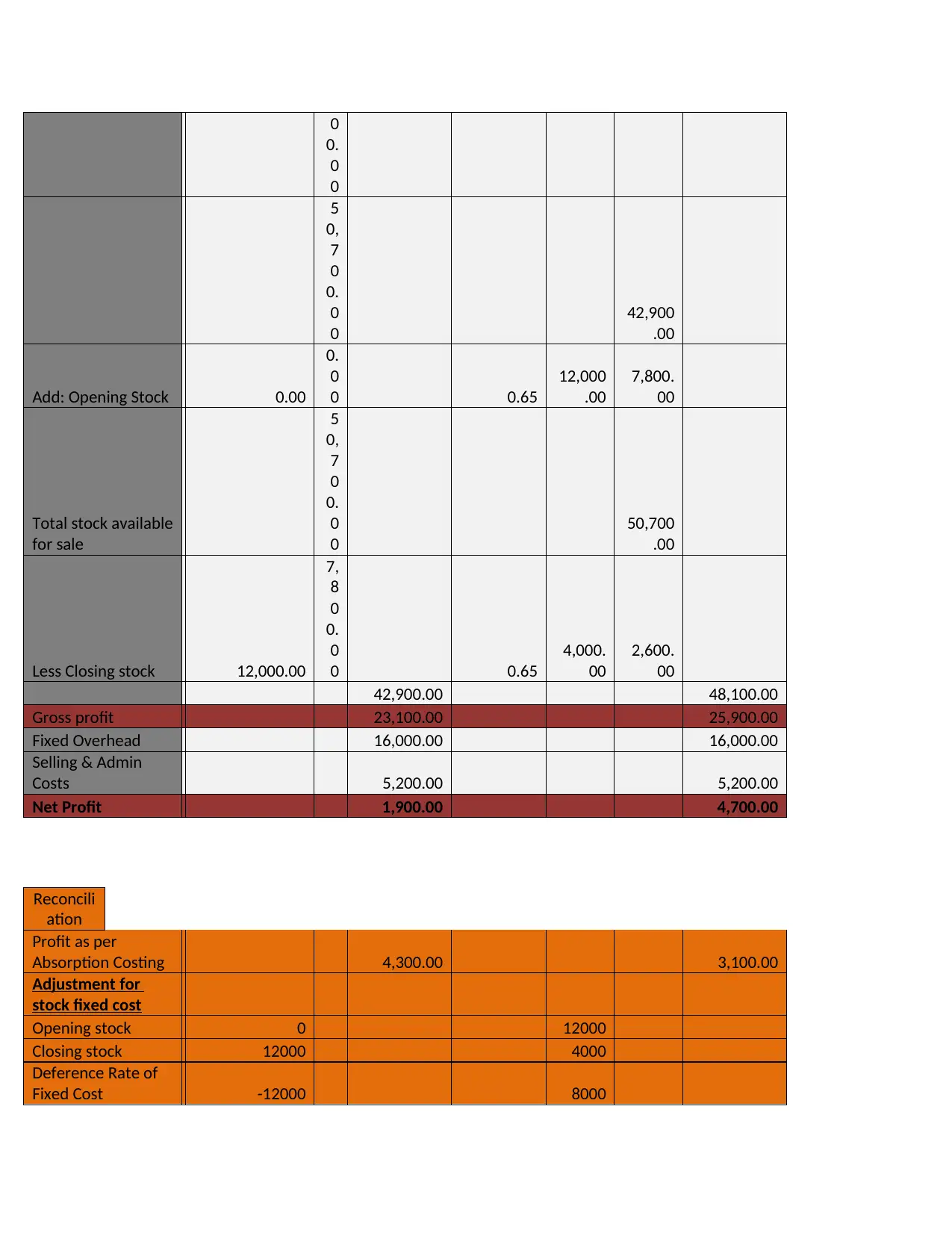

Net Profit 1,900.00 4,700.00

Reconcili

ation

Profit as per

Absorption Costing 4,300.00 3,100.00

Adjustment for

stock fixed cost

Opening stock 0 12000

Closing stock 12000 4000

Deference Rate of

Fixed Cost -12000 8000

0.

0

0

5

0,

7

0

0.

0

0

42,900

.00

Add: Opening Stock 0.00

0.

0

0 0.65

12,000

.00

7,800.

00

Total stock available

for sale

5

0,

7

0

0.

0

0

50,700

.00

Less Closing stock 12,000.00

7,

8

0

0.

0

0 0.65

4,000.

00

2,600.

00

42,900.00 48,100.00

Gross profit 23,100.00 25,900.00

Fixed Overhead 16,000.00 16,000.00

Selling & Admin

Costs 5,200.00 5,200.00

Net Profit 1,900.00 4,700.00

Reconcili

ation

Profit as per

Absorption Costing 4,300.00 3,100.00

Adjustment for

stock fixed cost

Opening stock 0 12000

Closing stock 12000 4000

Deference Rate of

Fixed Cost -12000 8000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.20 -2400 0.20 1600

1,900.00 4,700.00

Interpretation

As in above presented net income is calculated from both absorption and marginal

costing. Results from both exhibits different results. Net profit from absorption method as

computed is 4300 and 3100 in quarter 1st and 2nd respectively. Whereas net income from

marginal costing is 1900 and 4700 in Q1 and Q2 respectively. Reconciled difference in both

results shows that difference is mainly due to varaition in treatment of fixed costs.

Cause for analysing variations in profit

As per above presented income statement it is found that there is a variation in results of

income statement prepared using absorption and marginal methods. Difference arises due to

different treatment of fixed costs in both methods. In marginal method all fixed costs or expenses

are treated as period cost (Lau and Scully, 2015). On other hand in absorption method production

related fixed costs are not treated as period cost.

TASK 3

1 Application of various budgets in respect of control and planning:

Budget preparation: A budget is comparative statement which also includes future

estimated income and expenses, and assist in analysis about to what extent company is efficient

to achieve projected income and expenses. Preparation of budget is essential for business

organisation to identify weak elements in organisational structure. Budget also provide raw data

for development of new strategies and implementation of plans for future actions to attain

targets. In Nero Limited, managers set standards for achievement of objectives and prepare

budgets on the basis of these standards. Following are key budgets prepared by company, as

follows:

Operational Budget: Operational budget is a pre-planned structure or report which

reflects an estimate of overheads related to functions and transactions which are required in order

to run any organization in a specific time period. It includes all variable cost, fixed costs, non-

cash transactions, non-operating expenses, revenue etc. (Leoni and Florio, 2015). Nero Ltd is

1,900.00 4,700.00

Interpretation

As in above presented net income is calculated from both absorption and marginal

costing. Results from both exhibits different results. Net profit from absorption method as

computed is 4300 and 3100 in quarter 1st and 2nd respectively. Whereas net income from

marginal costing is 1900 and 4700 in Q1 and Q2 respectively. Reconciled difference in both

results shows that difference is mainly due to varaition in treatment of fixed costs.

Cause for analysing variations in profit

As per above presented income statement it is found that there is a variation in results of

income statement prepared using absorption and marginal methods. Difference arises due to

different treatment of fixed costs in both methods. In marginal method all fixed costs or expenses

are treated as period cost (Lau and Scully, 2015). On other hand in absorption method production

related fixed costs are not treated as period cost.

TASK 3

1 Application of various budgets in respect of control and planning:

Budget preparation: A budget is comparative statement which also includes future

estimated income and expenses, and assist in analysis about to what extent company is efficient

to achieve projected income and expenses. Preparation of budget is essential for business

organisation to identify weak elements in organisational structure. Budget also provide raw data

for development of new strategies and implementation of plans for future actions to attain

targets. In Nero Limited, managers set standards for achievement of objectives and prepare

budgets on the basis of these standards. Following are key budgets prepared by company, as

follows:

Operational Budget: Operational budget is a pre-planned structure or report which

reflects an estimate of overheads related to functions and transactions which are required in order

to run any organization in a specific time period. It includes all variable cost, fixed costs, non-

cash transactions, non-operating expenses, revenue etc. (Leoni and Florio, 2015). Nero Ltd is

involved in manufacturing of cement and concrete material and has to prepare operational budget

so that it can measure the efficiency needed to complete the projects, maintain a proper record of

operations in order to make appropriate future decisions and planning and calculate and control

the variances.

Advantages: It is a short term budget so in Nero Ltd, it facilitates management of routine

operations and activities in company.

Disadvantage: Preparation of an operational budget is complex and time taking task and

some time it provides ambiguous results.

Master Budget: Master budget is an expected summary of all the subsidiary budgets

which are prepared for the different departments and different projects within a specific time (Li,

Tseng and Chen, 2016). It includes major information about sales budget, purchase budget, cash

budget, capital budget, production and manufacturing budget etc. Nero Ltd prepares the master

budget because it helps in taking the financial decisions and provides a brief about all

departments in one go. It helps the management of the company to fairly allocate the financial

resources available in organization among various departments. Further this budget assists the

management to measure performance of the selected company.

Advantages: A master budget provides a complete and true picture of company's

performance in quickly manner.

Disadvantage: As financial statements of company also provides a complete analysis of

organisation's performance so preparation of master budget is not so much useful for

reporting purpose.

Zero Based Budget: Zero based budgeting is a new approach of budgeting emerging

now a day in organizations. This budget includes an estimation of costs which calculates

expenses on the basis of its need in upcoming period without considering the previous budget

valuations. It re-evaluates and justify the expenses to be incurred (Qiang and et.al, 2014). Nero

Ltd. management has started to prepare zero based budgets for efficient and accurate calculation

of costs. This method helps the management to eliminate unproductive and inefficient activities

and expenses. Management of the selected firm also includes the employees in order to prepare

this budget which improves better communication and co-ordination in the firm.

Advantage: it provides more future oriented results for decision-making purpose as it

does not emphasise on previous results of company.

so that it can measure the efficiency needed to complete the projects, maintain a proper record of

operations in order to make appropriate future decisions and planning and calculate and control

the variances.

Advantages: It is a short term budget so in Nero Ltd, it facilitates management of routine

operations and activities in company.

Disadvantage: Preparation of an operational budget is complex and time taking task and

some time it provides ambiguous results.

Master Budget: Master budget is an expected summary of all the subsidiary budgets

which are prepared for the different departments and different projects within a specific time (Li,

Tseng and Chen, 2016). It includes major information about sales budget, purchase budget, cash

budget, capital budget, production and manufacturing budget etc. Nero Ltd prepares the master

budget because it helps in taking the financial decisions and provides a brief about all

departments in one go. It helps the management of the company to fairly allocate the financial

resources available in organization among various departments. Further this budget assists the

management to measure performance of the selected company.

Advantages: A master budget provides a complete and true picture of company's

performance in quickly manner.

Disadvantage: As financial statements of company also provides a complete analysis of

organisation's performance so preparation of master budget is not so much useful for

reporting purpose.

Zero Based Budget: Zero based budgeting is a new approach of budgeting emerging

now a day in organizations. This budget includes an estimation of costs which calculates

expenses on the basis of its need in upcoming period without considering the previous budget

valuations. It re-evaluates and justify the expenses to be incurred (Qiang and et.al, 2014). Nero

Ltd. management has started to prepare zero based budgets for efficient and accurate calculation

of costs. This method helps the management to eliminate unproductive and inefficient activities

and expenses. Management of the selected firm also includes the employees in order to prepare

this budget which improves better communication and co-ordination in the firm.

Advantage: it provides more future oriented results for decision-making purpose as it

does not emphasise on previous results of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.