Management Accounting Report: Financial Performance Analysis - Unit 5

VerifiedAdded on 2021/02/20

|27

|5404

|46

Report

AI Summary

This report, prepared by a trainee management accountant, delves into the core concepts of management accounting, exploring its definition, essential requirements, and various systems. It examines the differences between management and financial accounting, outlining different types of management accounting systems such as job costing, inventory management, price optimization, and cost accounting systems, and their benefits. The report then details different management accounting reports, including budget reports, accounts receivable aging reports, job cost reports, and performance reports. Furthermore, it presents a practical analysis of Digittera Ltd, calculating net profit or loss using both marginal and absorption costing methods. The report also discusses the advantages and disadvantages of various planning tools used for budgetary control and compares ways in which the organization is using management accounting systems to deal with financial problems, concluding with a comprehensive overview of the financial landscape and recommendations for improvement.

Unit 5

Management Accounting

Learners Declaration: I certify that the work

submitted for this unit is my own and the

research sources are fully acknowledged.

Learners Signature: Date:

Management Accounting

Learners Declaration: I certify that the work

submitted for this unit is my own and the

research sources are fully acknowledged.

Learners Signature: Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table Of Content

INTRODUCTION...........................................................................................................................3

Scenario 1.........................................................................................................................................3

Explaining meaning of management accounting and essential requirement of different MA

systems in the business...........................................................................................................3

P 2 Different methods used for management accounting reports...........................................6

LO 2.................................................................................................................................................7

P 3 Calculation of Net profit or loss under Marginal Costing and Absorption Costing for

Digittera Ltd...........................................................................................................................7

LO 3...............................................................................................................................................14

P4 Explaining advantages and disadvantages of different types of planning tools which can be

used for budgetary control....................................................................................................14

LO 4...............................................................................................................................................16

P5 Comparing ways in which organization is using management accounting system for

dealing with financial problems...........................................................................................16

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

Scenario 1.........................................................................................................................................3

Explaining meaning of management accounting and essential requirement of different MA

systems in the business...........................................................................................................3

P 2 Different methods used for management accounting reports...........................................6

LO 2.................................................................................................................................................7

P 3 Calculation of Net profit or loss under Marginal Costing and Absorption Costing for

Digittera Ltd...........................................................................................................................7

LO 3...............................................................................................................................................14

P4 Explaining advantages and disadvantages of different types of planning tools which can be

used for budgetary control....................................................................................................14

LO 4...............................................................................................................................................16

P5 Comparing ways in which organization is using management accounting system for

dealing with financial problems...........................................................................................16

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a financial term that defines a set of process starting from

analysis of the each financial transaction of the company and ends with development of effective

strategies for the business in order to help the firm in achieving its set goals and objective

(Kaplan and Atkinson, 2015) . In simple terms, the MA can be defined as a process of analysing

and summarising all the financial transactions of the company, evaluation of company's planned

or estimated performance. In addition, the process also includes comparing of actual and planned

performance of the company in order to analysing the efficiency of the business and developing

plans and strategies of the business accordingly so that managers can help the company in

achieving its set goals and objectives. Digittera group is financial consultancy firm based on UK.

It provides financial consultancy services to various businesses relating to manufacturing, retail

industry etc. The present assignment contains a report developed by a trainee management

accountant of the company that explains MA system, MA reporting and their essential

requirement within the business organisation. Furthermore, the study shows use of several

budgetary control tools in order to formulate plans for the company. In addition, the report

contains a practical part that shows preparation of income statements through marginal and

absorption technique of the management accounting. At the end of report, the assignment

includes several MA system that can be adopted by the business in order to improve the

efficiency of company in facing several financial problems.

Scenario 1

Explaining meaning of management accounting and essential requirement of different MA

systems in the business

Management Accounting

Management accounting is a financial term that defines a set of process starting from

analysis of the each financial transaction of the company and ends with development of effective

strategies for the business in order to help the firm in achieving its set goals and objective

(Kaplan and Atkinson, 2015) . In simple terms, the MA can be defined as a process of analysing

and summarising all the financial transactions of the company, evaluation of company's planned

or estimated performance. In addition, the process also includes comparing of actual and planned

performance of the company in order to analysing the efficiency of the business and developing

plans and strategies of the business accordingly so that managers can help the company in

achieving its set goals and objectives. Digittera group is financial consultancy firm based on UK.

It provides financial consultancy services to various businesses relating to manufacturing, retail

industry etc. The present assignment contains a report developed by a trainee management

accountant of the company that explains MA system, MA reporting and their essential

requirement within the business organisation. Furthermore, the study shows use of several

budgetary control tools in order to formulate plans for the company. In addition, the report

contains a practical part that shows preparation of income statements through marginal and

absorption technique of the management accounting. At the end of report, the assignment

includes several MA system that can be adopted by the business in order to improve the

efficiency of company in facing several financial problems.

Scenario 1

Explaining meaning of management accounting and essential requirement of different MA

systems in the business

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

"Management accounting is a procedure performed by professional managerial

accountant in order to analyse and summarise different financial performance of the company in

order to collect data relating to financial transactions of the company and summarising and

presenting each information in such a way so that it could help the managers in having a overall

review of overall financial performance of the company (Management Accounting – Meaning,

Advantages & Functions. 2017)."

Origin of management accounting

The system of management accounting was developed by various mass merchants when

the amount of business activities handled by them started increasing day by day. They

formulated their own systems for managing their several business activities in order to manage

each business activity in an effective manner.

Management accounting system

Management accounting system is a part of overall management system of a business

organisation that concerns with performing a range of managerial function for the purpose of

reviewing each financial transaction including various monetary and non monitory activities of

the firm. Further, the system also includes a process of developing more effective strategies,

plans and procedures of the firm in order to improve the efficiency of business in performing

financial activities and enhancing financial position of the company as well.

Difference between management accounting and financial accounting

Both management accounting and financial accounting are different from each other.

Some major difference between these two concepts are as under:

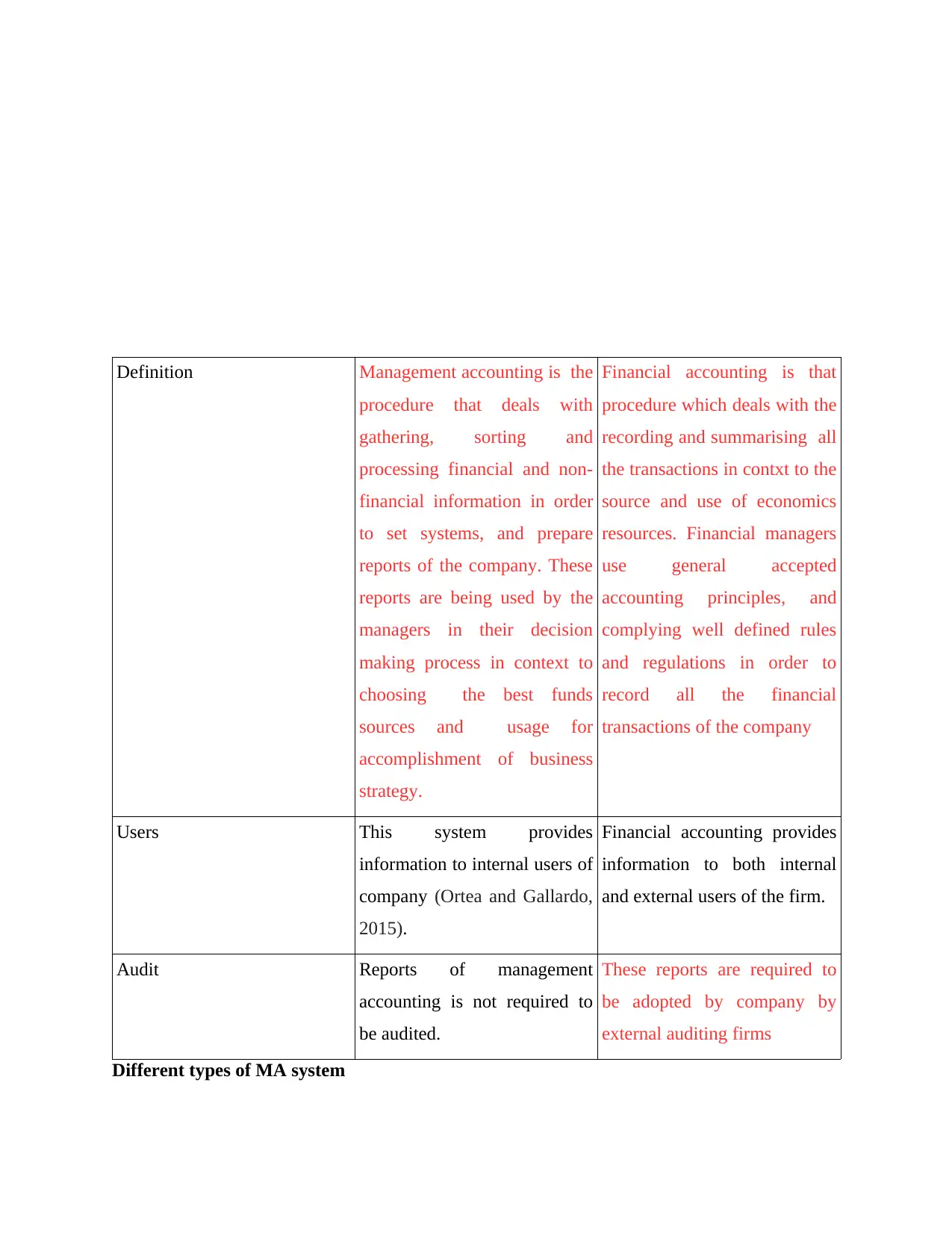

Basis Management Accounting Financial Accounting

accountant in order to analyse and summarise different financial performance of the company in

order to collect data relating to financial transactions of the company and summarising and

presenting each information in such a way so that it could help the managers in having a overall

review of overall financial performance of the company (Management Accounting – Meaning,

Advantages & Functions. 2017)."

Origin of management accounting

The system of management accounting was developed by various mass merchants when

the amount of business activities handled by them started increasing day by day. They

formulated their own systems for managing their several business activities in order to manage

each business activity in an effective manner.

Management accounting system

Management accounting system is a part of overall management system of a business

organisation that concerns with performing a range of managerial function for the purpose of

reviewing each financial transaction including various monetary and non monitory activities of

the firm. Further, the system also includes a process of developing more effective strategies,

plans and procedures of the firm in order to improve the efficiency of business in performing

financial activities and enhancing financial position of the company as well.

Difference between management accounting and financial accounting

Both management accounting and financial accounting are different from each other.

Some major difference between these two concepts are as under:

Basis Management Accounting Financial Accounting

Definition Management accounting is the

procedure that deals with

gathering, sorting and

processing financial and non-

financial information in order

to set systems, and prepare

reports of the company. These

reports are being used by the

managers in their decision

making process in context to

choosing the best funds

sources and usage for

accomplishment of business

strategy.

Financial accounting is that

procedure which deals with the

recording and summarising all

the transactions in contxt to the

source and use of economics

resources. Financial managers

use general accepted

accounting principles, and

complying well defined rules

and regulations in order to

record all the financial

transactions of the company

Users This system provides

information to internal users of

company (Ortea and Gallardo,

2015).

Financial accounting provides

information to both internal

and external users of the firm.

Audit Reports of management

accounting is not required to

be audited.

These reports are required to

be adopted by company by

external auditing firms

Different types of MA system

procedure that deals with

gathering, sorting and

processing financial and non-

financial information in order

to set systems, and prepare

reports of the company. These

reports are being used by the

managers in their decision

making process in context to

choosing the best funds

sources and usage for

accomplishment of business

strategy.

Financial accounting is that

procedure which deals with the

recording and summarising all

the transactions in contxt to the

source and use of economics

resources. Financial managers

use general accepted

accounting principles, and

complying well defined rules

and regulations in order to

record all the financial

transactions of the company

Users This system provides

information to internal users of

company (Ortea and Gallardo,

2015).

Financial accounting provides

information to both internal

and external users of the firm.

Audit Reports of management

accounting is not required to

be audited.

These reports are required to

be adopted by company by

external auditing firms

Different types of MA system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are various types of MA systems that can be adopted by managers while

performing their business activities in order to improve their quality of managing all the financial

activities of the company and improving its financial position in the competitive market as well.

Effectiveness of these systems can be analysed as under:

Job costing system : This system of MA system provides process through which

managers can develop their plans regarding helping the company in generating

appropriate amount of profit from the sales. The Job costing system is adopted by

managers of those companies that provides customised product or services to their

customers that costs differently for each product or services. For developing a good job

costing system, an organization must create a system in a way that helps it in identifying

each job from material stage till its delivery.

Benefits:

▪ This system helps in determining cost incurred in production of each unit.

▪ It is required to set the most appropriate price of each product.

▪ It is essential to be adopted to analyse the profit earned in trading of each product.

Inventory management system: Inventory management refers to monitoring each

movement of stock of firm and development of controlling measures in this regard so as

to eliminate wastage. Inventory management system provides several methods such as

LIFO, FIFO etc. for maintaining record of movement effectively. In addition, it also

provides methods like EOQ method through which managers of Digittera group can

determine actual need of stock and avoid its wastage as well. An inventory management

system of an enterprise is said to be good when it provides for reorder notifications which

will enables a manager in finding out that when the product's stock level declines below

the certain level.

performing their business activities in order to improve their quality of managing all the financial

activities of the company and improving its financial position in the competitive market as well.

Effectiveness of these systems can be analysed as under:

Job costing system : This system of MA system provides process through which

managers can develop their plans regarding helping the company in generating

appropriate amount of profit from the sales. The Job costing system is adopted by

managers of those companies that provides customised product or services to their

customers that costs differently for each product or services. For developing a good job

costing system, an organization must create a system in a way that helps it in identifying

each job from material stage till its delivery.

Benefits:

▪ This system helps in determining cost incurred in production of each unit.

▪ It is required to set the most appropriate price of each product.

▪ It is essential to be adopted to analyse the profit earned in trading of each product.

Inventory management system: Inventory management refers to monitoring each

movement of stock of firm and development of controlling measures in this regard so as

to eliminate wastage. Inventory management system provides several methods such as

LIFO, FIFO etc. for maintaining record of movement effectively. In addition, it also

provides methods like EOQ method through which managers of Digittera group can

determine actual need of stock and avoid its wastage as well. An inventory management

system of an enterprise is said to be good when it provides for reorder notifications which

will enables a manager in finding out that when the product's stock level declines below

the certain level.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits:

▪ To prevent company from wastage of stock

▪ To analyse minimum requirement of stock in each area of business.

▪ To maintain accurate records regarding volume of stock used by each department.

▪ To eliminate chances of insufficiency of the inventory within firm.

Price optimisation system: This system of MA helps in setting up the most appropriate

price of the product or services traded by the firm (Smith, 2017). This system enable

managers in analysing the maximum price that can be charged against the product or

services and minimum price below which the company would suffer loss from trading.

With the help of this evaluation, managers of Digittera group becomes able to set the

most economical value of product. Adoption of this system is resulted as good because it

facilitates automation, provides for real time adjustments in the price and also contains

flexible filters.

Benefits:

▪ To attract customers towards the company through economical price of product.

▪ To maintain profitability in the business.

Cost accounting system: Cost accounting is a part of MA system that provides gudelines

and procedures through which managers can improve the efficiency of company while

performing several business activities. This system is required to be adopted by Digittera

group for avoiding wastage of resources of the firm. This system is said to be ideal as it

provides suitability, comparability and flexibility within the activities of the business.

Benefits

▪ It helps in improving profitability of the business.

▪ To prevent company from wastage of stock

▪ To analyse minimum requirement of stock in each area of business.

▪ To maintain accurate records regarding volume of stock used by each department.

▪ To eliminate chances of insufficiency of the inventory within firm.

Price optimisation system: This system of MA helps in setting up the most appropriate

price of the product or services traded by the firm (Smith, 2017). This system enable

managers in analysing the maximum price that can be charged against the product or

services and minimum price below which the company would suffer loss from trading.

With the help of this evaluation, managers of Digittera group becomes able to set the

most economical value of product. Adoption of this system is resulted as good because it

facilitates automation, provides for real time adjustments in the price and also contains

flexible filters.

Benefits:

▪ To attract customers towards the company through economical price of product.

▪ To maintain profitability in the business.

Cost accounting system: Cost accounting is a part of MA system that provides gudelines

and procedures through which managers can improve the efficiency of company while

performing several business activities. This system is required to be adopted by Digittera

group for avoiding wastage of resources of the firm. This system is said to be ideal as it

provides suitability, comparability and flexibility within the activities of the business.

Benefits

▪ It helps in improving profitability of the business.

▪ With the help of budgetary control method of cost accounting system, the

managers can easily predict requirement of resources within the company in its

near future.

▪ It helps managers in developing more effective controlling measures for cost

controlling procedure.

Characteristics of good information system:

Relevant- An information attained from application of the management accounting

systems is said to be good as it provides for relevant and useful information to the firm.

Complete- MAS facilitates the information that comprises if all the facts which helps the

managers in taking effective and suitable decisions.

Timely- Using MA systems, managers could be able to deliver adequate information at

right time to the right person so that better controlling of activities can be attained.

P 2 Different methods used for management accounting reports

Management Accounting reports are prepared by the managers of the company in order to

know the happenings in the business. The reports help the management in taking certain

decisions related to the profit maximization of Digiterra ltd. The reports are based on the

previous year’s happenings in the company. Various types of reports prepared in the Digiterra

Ltd are

Budget reports

Budget reports are those reports which are prepared to set the targets for the company

which are to be achieved by the management in order to reduce the cost of the company and

increase the profits of Digiterra Ltd (Kaplan, 2015). The budget reports are compared with the

actual performance of the company and if any deviations are found then the relevant actions are

taken in order to reduce the cost of the company.

managers can easily predict requirement of resources within the company in its

near future.

▪ It helps managers in developing more effective controlling measures for cost

controlling procedure.

Characteristics of good information system:

Relevant- An information attained from application of the management accounting

systems is said to be good as it provides for relevant and useful information to the firm.

Complete- MAS facilitates the information that comprises if all the facts which helps the

managers in taking effective and suitable decisions.

Timely- Using MA systems, managers could be able to deliver adequate information at

right time to the right person so that better controlling of activities can be attained.

P 2 Different methods used for management accounting reports

Management Accounting reports are prepared by the managers of the company in order to

know the happenings in the business. The reports help the management in taking certain

decisions related to the profit maximization of Digiterra ltd. The reports are based on the

previous year’s happenings in the company. Various types of reports prepared in the Digiterra

Ltd are

Budget reports

Budget reports are those reports which are prepared to set the targets for the company

which are to be achieved by the management in order to reduce the cost of the company and

increase the profits of Digiterra Ltd (Kaplan, 2015). The budget reports are compared with the

actual performance of the company and if any deviations are found then the relevant actions are

taken in order to reduce the cost of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Receivable aging reports

Accounting receivable reports shows that in how much time Digiterra Ltd convert its

debtors into the cash for the company. This report helps the company in improving its policy of

converting the debtors into the cash. It also helps the managers in knowing that where the

company is lacking in taking payments from its debtors (Ortea and Gallardo, 2015)..

Job Cost Reports

Job cost Reports are needs to know where the extra cost has been allocated and in which

department company needs more cost to earn more profits for the company. These reports also

help the Digiterra Ltd in knowing the total cost incurred by the company in production of the

goods.

Performance Reports

Performance Reports help the company in knowing the performance of every department

in the company (Avdjiev, and et.al., 2015). It also presents the report of every department where

the extra cost is allocated and which department there is need of more cost in order to earn more

profits for Digiterra Ltd.

LO 2

P 3 Calculation of Net profit or loss under Marginal Costing and Absorption Costing for

Digittera Ltd.

Meaning of cost and different type of costs and cost analysis

Cost can be defined as the total expenses occurred in the production of goods produced

by the company. It is also said as the total expenses absorbed by the company in production of

the goods. Cost is consists of direct expenses and indirect expenses Digiterra Ltd. Direct

Accounting receivable reports shows that in how much time Digiterra Ltd convert its

debtors into the cash for the company. This report helps the company in improving its policy of

converting the debtors into the cash. It also helps the managers in knowing that where the

company is lacking in taking payments from its debtors (Ortea and Gallardo, 2015)..

Job Cost Reports

Job cost Reports are needs to know where the extra cost has been allocated and in which

department company needs more cost to earn more profits for the company. These reports also

help the Digiterra Ltd in knowing the total cost incurred by the company in production of the

goods.

Performance Reports

Performance Reports help the company in knowing the performance of every department

in the company (Avdjiev, and et.al., 2015). It also presents the report of every department where

the extra cost is allocated and which department there is need of more cost in order to earn more

profits for Digiterra Ltd.

LO 2

P 3 Calculation of Net profit or loss under Marginal Costing and Absorption Costing for

Digittera Ltd.

Meaning of cost and different type of costs and cost analysis

Cost can be defined as the total expenses occurred in the production of goods produced

by the company. It is also said as the total expenses absorbed by the company in production of

the goods. Cost is consists of direct expenses and indirect expenses Digiterra Ltd. Direct

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses are those expenses which are directly related in the production of the goods. Indirect

expenses are those expenses which occurred in the selling of the goods. Cost analysis is the

measure of cost and output relationship of Digiterra Ltd (Namazi, 2016). It can be defined as the

cost incurred is directly related to output of the company.

Cost- Volume Profit can be defined as how Digiterra Ltd measures the change in the cost

and output of the company which affect the net income of the company. Flexible Budgeting is

the budget prepared on the basis of the level of activity of the company. Company’s level of

activity then the expenses of the company also increases. Cost variances means the difference

occurred in the cost of the company when compared actual cost with the budgeted cost of the

company.

On the basis of level of activity cost can be divided in two parts i.e. fixed costs and

Variable costs. Fixed costs are the cost which does not change with the change in the level of the

activity whereas variable costs are the costs which changes with the level of activity in the

company. Cost Allocation can be defined as allocating the different costs to the different

departments according to the needs of costs in the department (Mertzanis, 2016).

Normal costing is the actual performance of the company which is actual cost occurred in

the production of the company. Standard Costing is the set budgets prepared by the company in

order to estimate the cost of Digiterra Ltd. Activity- Based costing is the costing in which costing

is done on the basis of activity in each department in the company. The main role of the costing

is to allocate the costs in every department in Digiterra Ltd.

Marginal Costing and Absorption Costing

Absorption costing and marginal costing are the two techniques of calculating an income

statement for Digiterra Ltd. Under absorption method company takes all the fixed and variable

expenses of the company for valuation of closing inventory. It takes into all the cost which are

expenses are those expenses which occurred in the selling of the goods. Cost analysis is the

measure of cost and output relationship of Digiterra Ltd (Namazi, 2016). It can be defined as the

cost incurred is directly related to output of the company.

Cost- Volume Profit can be defined as how Digiterra Ltd measures the change in the cost

and output of the company which affect the net income of the company. Flexible Budgeting is

the budget prepared on the basis of the level of activity of the company. Company’s level of

activity then the expenses of the company also increases. Cost variances means the difference

occurred in the cost of the company when compared actual cost with the budgeted cost of the

company.

On the basis of level of activity cost can be divided in two parts i.e. fixed costs and

Variable costs. Fixed costs are the cost which does not change with the change in the level of the

activity whereas variable costs are the costs which changes with the level of activity in the

company. Cost Allocation can be defined as allocating the different costs to the different

departments according to the needs of costs in the department (Mertzanis, 2016).

Normal costing is the actual performance of the company which is actual cost occurred in

the production of the company. Standard Costing is the set budgets prepared by the company in

order to estimate the cost of Digiterra Ltd. Activity- Based costing is the costing in which costing

is done on the basis of activity in each department in the company. The main role of the costing

is to allocate the costs in every department in Digiterra Ltd.

Marginal Costing and Absorption Costing

Absorption costing and marginal costing are the two techniques of calculating an income

statement for Digiterra Ltd. Under absorption method company takes all the fixed and variable

expenses of the company for valuation of closing inventory. It takes into all the cost which are

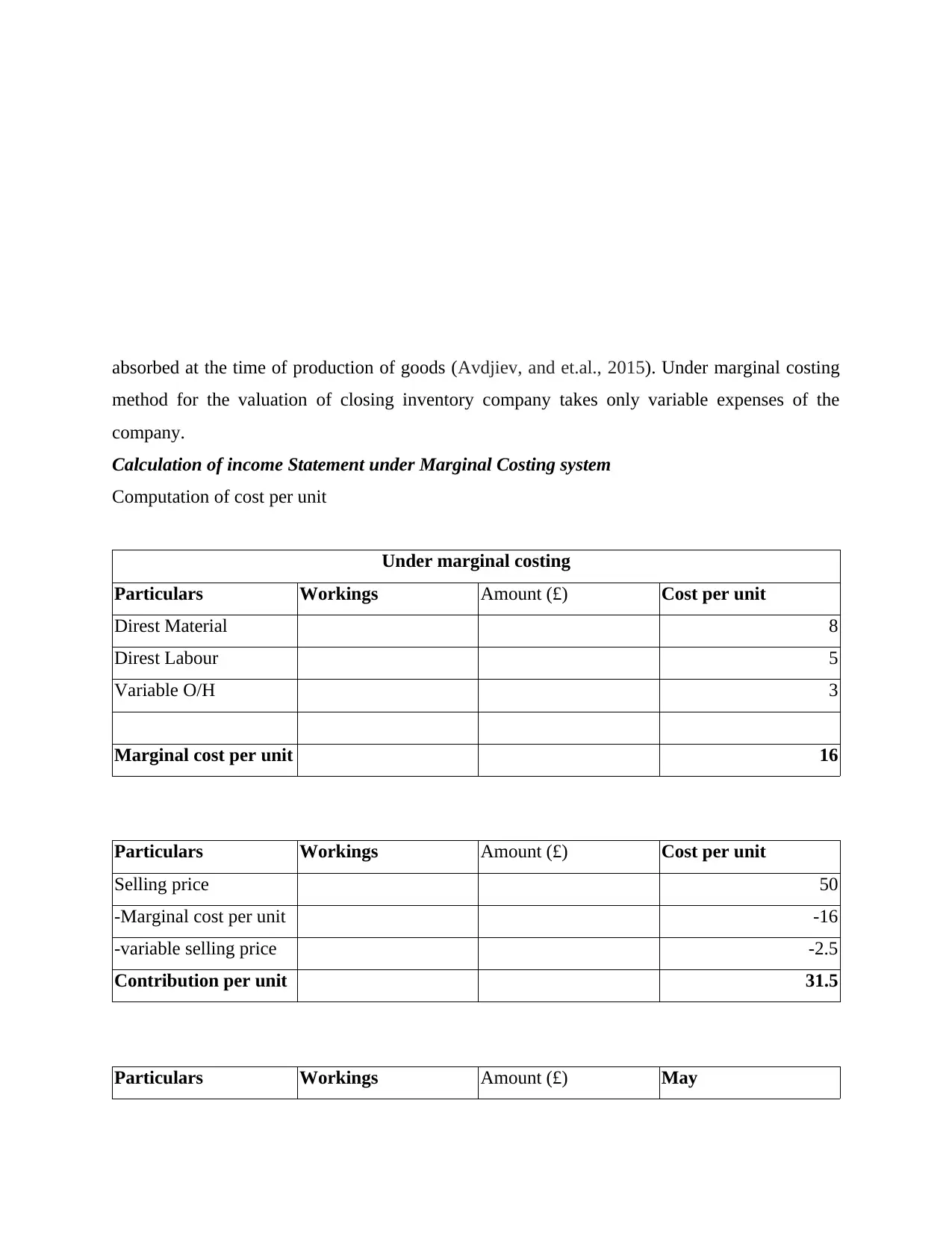

absorbed at the time of production of goods (Avdjiev, and et.al., 2015). Under marginal costing

method for the valuation of closing inventory company takes only variable expenses of the

company.

Calculation of income Statement under Marginal Costing system

Computation of cost per unit

Under marginal costing

Particulars Workings Amount (£) Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Particulars Workings Amount (£) Cost per unit

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.5

Contribution per unit 31.5

Particulars Workings Amount (£) May

method for the valuation of closing inventory company takes only variable expenses of the

company.

Calculation of income Statement under Marginal Costing system

Computation of cost per unit

Under marginal costing

Particulars Workings Amount (£) Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Particulars Workings Amount (£) Cost per unit

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.5

Contribution per unit 31.5

Particulars Workings Amount (£) May

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.