Management Accounting & Control Assessment Report - LK Ltd & Kadlex

VerifiedAdded on 2021/02/21

|18

|5618

|29

Report

AI Summary

This report provides a comprehensive analysis of management accounting and control assessments, focusing on two key scenarios involving LK Ltd and Kadlex Consultancy. The first scenario delves into LK Ltd's production planning, profit and loss statements, and the evaluation of cost reduction techniques such as Economic Order Quantity, Margin of Safety, and Just-in-Time systems. It also explores the use of a Balanced Scorecard for cost control. The second scenario shifts to Kadlex Consultancy, evaluating investment decisions and the benefits and limitations of investment appraisal measures. It culminates in the preparation of a Balanced Scorecard to address short-term financial performance concerns. The report incorporates various accounting methods and tools to assess cost control, production efficiency, and financial performance, offering valuable insights into optimizing business operations and maximizing profitability. The document also discusses ad hoc analysis for cost reduction and the implementation of ABC analysis and safety stocks to optimize inventory management and cost control.

Management Accounting &

Control Assessment

Control Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

Scenario 1.............................................................................................................................................3

(a) Calculation of production plan and profit and loss statement for LK Ltd.................................3

(b) Evaluation of adopting Economic Order Quantity, Margin- of- safety and Just- in- Time in

cost reduction by LK Ltd.................................................................................................................4

(c) Using Balanced Scorecard evaluating the areas where cost can be controlled..........................5

Scenario 2.............................................................................................................................................7

(a) Evaluation of best Investment Decision to be selected for Kadlex Consultancy from available

alternatives.......................................................................................................................................7

(b) Evaluating the benefits and limitations of measures used in selection of Investment

Appraisals by kadlex Consultancy Ltd..........................................................................................10

(c) Preparation of Balanced Scorecard for short- term Financial Performance by Kadlex

Consultancy for reduction of short- term orientation....................................................................12

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................14

INTRODUCTION................................................................................................................................3

Scenario 1.............................................................................................................................................3

(a) Calculation of production plan and profit and loss statement for LK Ltd.................................3

(b) Evaluation of adopting Economic Order Quantity, Margin- of- safety and Just- in- Time in

cost reduction by LK Ltd.................................................................................................................4

(c) Using Balanced Scorecard evaluating the areas where cost can be controlled..........................5

Scenario 2.............................................................................................................................................7

(a) Evaluation of best Investment Decision to be selected for Kadlex Consultancy from available

alternatives.......................................................................................................................................7

(b) Evaluating the benefits and limitations of measures used in selection of Investment

Appraisals by kadlex Consultancy Ltd..........................................................................................10

(c) Preparation of Balanced Scorecard for short- term Financial Performance by Kadlex

Consultancy for reduction of short- term orientation....................................................................12

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................14

INTRODUCTION

Management Accounting can be defined as the accounting used for identifying, analysing,

measuring, interpretation and recording to preparation of Financial Statements. Accounting

considers all the monetary transactions to be recorder in the books of account. It also deals with

other accounting methods such as Cost accounting, financial accounting etc. Control Assessment

helps in controlling of various extra costs allocated in different departments of company.

Management Accounting helps in preparation of books of accounts (Management Accounting and

Control Assessment, 2019). This books of accounts help in analysing the various loopholes in

company and where company can control extra cost allocation. Im this manner, management

accounting helps in controlling and assessing cost in LK Ltd. Lazy King Ltd is a company who

wants to maximize its profits by preparing proper production plan for the company. Company wants

to prepare such production plan which helps company in achieving their targets and maximizing

company's profits. The report covers profit or loss statement and production plan for four goods

which are produced by company in order to maximize profits of company. Company wants to also

know Economic order quantity, Margin of safety and Just- in- time system in order to know

minimum requirement of raw material for completing maximum demands of company. LK Ltd also

uses Balanced Score Card in order to make decisions on how to control extra cost in company. LK

Ltd sells its company to Kadlex Consultancy in order to earn higher profits. Kadlex Consultancy

uses divisional method for running its business.

Scenario 1

(a) Calculation of production plan and profit and loss statement for LK Ltd

Production Plan can be defined as the process which starts from purchasing raw material to

converting them into finished goods (Becher, and et.al., 2018). This process helps in knowing the

cost of production and manufacturing cost. It helps in preparing the optimum level of different types

of products portfolio so as to earn higher profits as compared to the past performance.

Calculation of weekly Profit/ Loss that will yield maximum profit for LK Ltd

Revenue 33133

Less:- COGS -22923

Gross Profit 10210

Less:- Fixed Costs -6390

Net Profit 3820

Management Accounting can be defined as the accounting used for identifying, analysing,

measuring, interpretation and recording to preparation of Financial Statements. Accounting

considers all the monetary transactions to be recorder in the books of account. It also deals with

other accounting methods such as Cost accounting, financial accounting etc. Control Assessment

helps in controlling of various extra costs allocated in different departments of company.

Management Accounting helps in preparation of books of accounts (Management Accounting and

Control Assessment, 2019). This books of accounts help in analysing the various loopholes in

company and where company can control extra cost allocation. Im this manner, management

accounting helps in controlling and assessing cost in LK Ltd. Lazy King Ltd is a company who

wants to maximize its profits by preparing proper production plan for the company. Company wants

to prepare such production plan which helps company in achieving their targets and maximizing

company's profits. The report covers profit or loss statement and production plan for four goods

which are produced by company in order to maximize profits of company. Company wants to also

know Economic order quantity, Margin of safety and Just- in- time system in order to know

minimum requirement of raw material for completing maximum demands of company. LK Ltd also

uses Balanced Score Card in order to make decisions on how to control extra cost in company. LK

Ltd sells its company to Kadlex Consultancy in order to earn higher profits. Kadlex Consultancy

uses divisional method for running its business.

Scenario 1

(a) Calculation of production plan and profit and loss statement for LK Ltd

Production Plan can be defined as the process which starts from purchasing raw material to

converting them into finished goods (Becher, and et.al., 2018). This process helps in knowing the

cost of production and manufacturing cost. It helps in preparing the optimum level of different types

of products portfolio so as to earn higher profits as compared to the past performance.

Calculation of weekly Profit/ Loss that will yield maximum profit for LK Ltd

Revenue 33133

Less:- COGS -22923

Gross Profit 10210

Less:- Fixed Costs -6390

Net Profit 3820

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of Production plan which will maximize company's profit

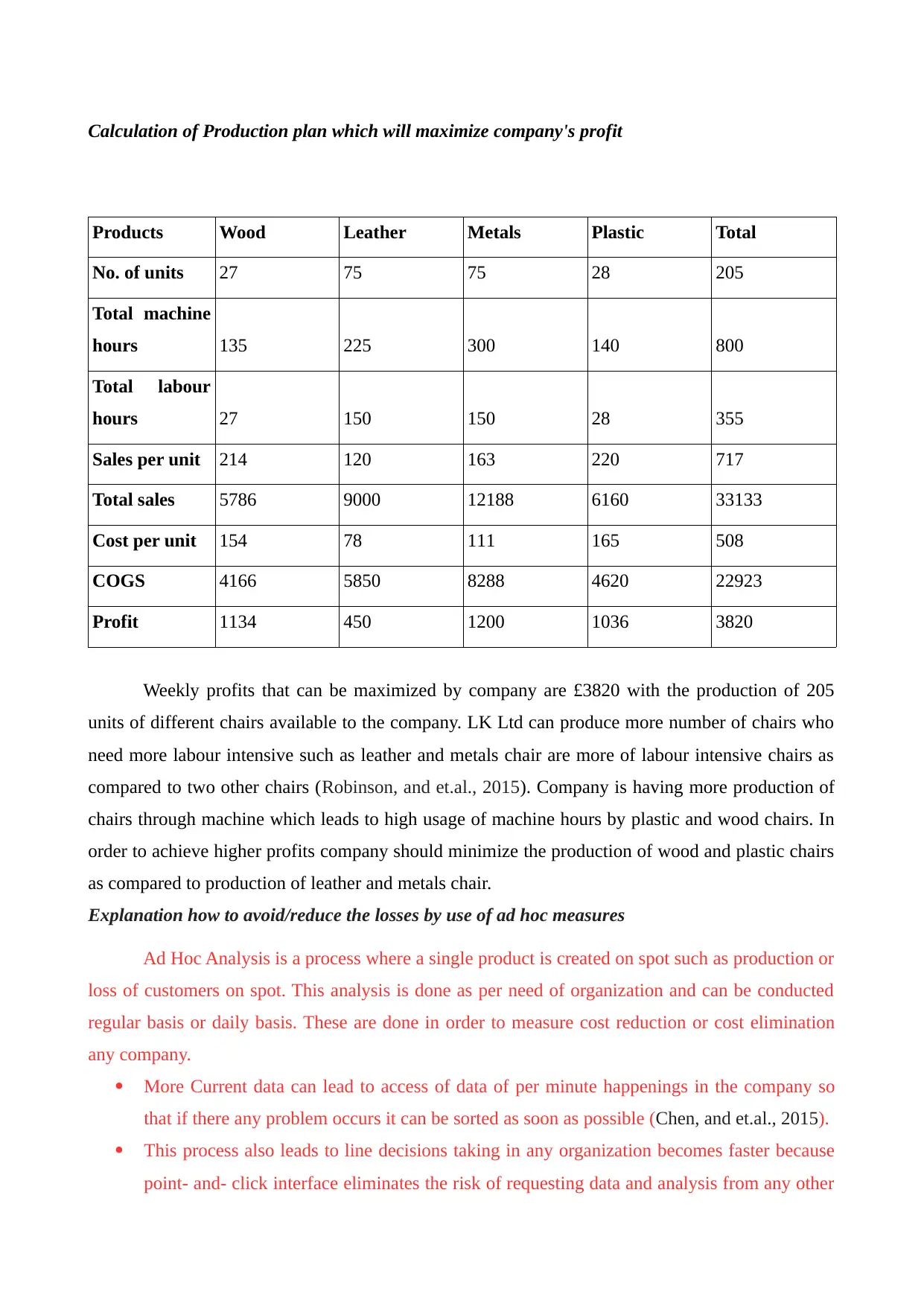

Products Wood Leather Metals Plastic Total

No. of units 27 75 75 28 205

Total machine

hours 135 225 300 140 800

Total labour

hours 27 150 150 28 355

Sales per unit 214 120 163 220 717

Total sales 5786 9000 12188 6160 33133

Cost per unit 154 78 111 165 508

COGS 4166 5850 8288 4620 22923

Profit 1134 450 1200 1036 3820

Weekly profits that can be maximized by company are £3820 with the production of 205

units of different chairs available to the company. LK Ltd can produce more number of chairs who

need more labour intensive such as leather and metals chair are more of labour intensive chairs as

compared to two other chairs (Robinson, and et.al., 2015). Company is having more production of

chairs through machine which leads to high usage of machine hours by plastic and wood chairs. In

order to achieve higher profits company should minimize the production of wood and plastic chairs

as compared to production of leather and metals chair.

Explanation how to avoid/reduce the losses by use of ad hoc measures

Ad Hoc Analysis is a process where a single product is created on spot such as production or

loss of customers on spot. This analysis is done as per need of organization and can be conducted

regular basis or daily basis. These are done in order to measure cost reduction or cost elimination

any company.

More Current data can lead to access of data of per minute happenings in the company so

that if there any problem occurs it can be sorted as soon as possible (Chen, and et.al., 2015).

This process also leads to line decisions taking in any organization becomes faster because

point- and- click interface eliminates the risk of requesting data and analysis from any other

Products Wood Leather Metals Plastic Total

No. of units 27 75 75 28 205

Total machine

hours 135 225 300 140 800

Total labour

hours 27 150 150 28 355

Sales per unit 214 120 163 220 717

Total sales 5786 9000 12188 6160 33133

Cost per unit 154 78 111 165 508

COGS 4166 5850 8288 4620 22923

Profit 1134 450 1200 1036 3820

Weekly profits that can be maximized by company are £3820 with the production of 205

units of different chairs available to the company. LK Ltd can produce more number of chairs who

need more labour intensive such as leather and metals chair are more of labour intensive chairs as

compared to two other chairs (Robinson, and et.al., 2015). Company is having more production of

chairs through machine which leads to high usage of machine hours by plastic and wood chairs. In

order to achieve higher profits company should minimize the production of wood and plastic chairs

as compared to production of leather and metals chair.

Explanation how to avoid/reduce the losses by use of ad hoc measures

Ad Hoc Analysis is a process where a single product is created on spot such as production or

loss of customers on spot. This analysis is done as per need of organization and can be conducted

regular basis or daily basis. These are done in order to measure cost reduction or cost elimination

any company.

More Current data can lead to access of data of per minute happenings in the company so

that if there any problem occurs it can be sorted as soon as possible (Chen, and et.al., 2015).

This process also leads to line decisions taking in any organization becomes faster because

point- and- click interface eliminates the risk of requesting data and analysis from any other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

group in within that company. This capacity helps in quicker response times when business

decisions are to be taken.

Ad Hoc also help IT users to run their own queries in organization than it leads IT team to

fewer create reports and can easily focus on other tasks (Balaji, 2019).

(b) Evaluation of adopting Economic Order Quantity, Margin- of- safety and Just- in- Time in cost

reduction by LK Ltd

Economic Order Quantity can be defined as in how many time company has to order goods

from its suppliers keeping in context of cost of production, demand rate by the competitors and

other suitable variables (Bian, and et.al., 2017). This method helps the company in controlling the

cost of company by evaluating that how much quantity should be purchased by company so that

their will be no problem of order in future. The main aim of this method is to minimize its cost of

production by taking delivery on time. EOQ can be calculated by using following formula:-

Q= (2 DS/ H )^1/2

where; Q= EOQ Units

D= Demand in units

S= Order Cost

H= Cost of holding inventory

Margin of safety refers to a principle where an investor generally purchases inventory when

the purchasing price of inventory is less than intrinsic value. Margin of safety is the difference

between intrinsic value of inventory and purchasing price of inventory (Gosse, 2017). It is generally

purchased in order to gain more benefits for LK Ltd. This is the difference between actual price and

break even sales of company in order to gain profits. It also refers to as the difference between

forecasted sales or current sales and break even sales is divided by current sales or forecasted sales

in order to know high percentage yield. If the forecasted sales are lower than break even sales than

margin of safety is negative which shows poor performance of company.

Margin of safety= Actual Sales- Break Even Point

Margin of safety (in % )= Margin of Safety/Actual Sales *100

Just- in- time is the system where raw material suppliers directly aligns with those of

production schedules. Companies uses this system in order to increase the efficiency and decreasing

the waste by receiving goods only when are in need of production (Kamei, and et.al., 2016). This

system helps in forecasting future demands accurately. Just- in- Time helps the company in

knowing the minimum raw material to be available with company so as to achieve maximum

decisions are to be taken.

Ad Hoc also help IT users to run their own queries in organization than it leads IT team to

fewer create reports and can easily focus on other tasks (Balaji, 2019).

(b) Evaluation of adopting Economic Order Quantity, Margin- of- safety and Just- in- Time in cost

reduction by LK Ltd

Economic Order Quantity can be defined as in how many time company has to order goods

from its suppliers keeping in context of cost of production, demand rate by the competitors and

other suitable variables (Bian, and et.al., 2017). This method helps the company in controlling the

cost of company by evaluating that how much quantity should be purchased by company so that

their will be no problem of order in future. The main aim of this method is to minimize its cost of

production by taking delivery on time. EOQ can be calculated by using following formula:-

Q= (2 DS/ H )^1/2

where; Q= EOQ Units

D= Demand in units

S= Order Cost

H= Cost of holding inventory

Margin of safety refers to a principle where an investor generally purchases inventory when

the purchasing price of inventory is less than intrinsic value. Margin of safety is the difference

between intrinsic value of inventory and purchasing price of inventory (Gosse, 2017). It is generally

purchased in order to gain more benefits for LK Ltd. This is the difference between actual price and

break even sales of company in order to gain profits. It also refers to as the difference between

forecasted sales or current sales and break even sales is divided by current sales or forecasted sales

in order to know high percentage yield. If the forecasted sales are lower than break even sales than

margin of safety is negative which shows poor performance of company.

Margin of safety= Actual Sales- Break Even Point

Margin of safety (in % )= Margin of Safety/Actual Sales *100

Just- in- time is the system where raw material suppliers directly aligns with those of

production schedules. Companies uses this system in order to increase the efficiency and decreasing

the waste by receiving goods only when are in need of production (Kamei, and et.al., 2016). This

system helps in forecasting future demands accurately. Just- in- Time helps the company in

knowing the minimum raw material to be available with company so as to achieve maximum

market demand by LK Ltd. It helps company in increasing high- quality products, no beak down

machines and reliable suppliers.

ABC is the method which can be also in cost reduction in any organization. In this “A items”

refers to very tight and there is accurate recording of inventory, “B items” are with very less tightly

controlled and good records are maintained of inventory and “C items” are very less tighten in

company and with very minimum records are kept of these items. ABC analysis is the method in

which overall inventory cost has been defined and requires different inventory controls in any

organization (Kumar, 2015). “A items” are very important to be kept in any organization. It is also

estimated that 'A items' covers 20% of inventory charges for 70% of annual consumption, 'B items'

covers 30% of total inventory charges 25% of annual consumption and 'C items' covers 50% of

inventory charges 5% of annual consumption.

Safety stocks can be defined as an additional quantity required in order to minimise risks in

an organization. This inventory helps at the time when there is huge sale occurring in company

because of which huge production occurs which needs raw material in company (Albrecht, 2017). If

any manufacturer properly maintains safety stocks in any company than it can avoid risk of

production. In this way safety stocks can help company in production of extra products at time of

extra sales.

All these factors will be helping LK Ltd in cost reduction because these factors help

company in knowing what quantity are to be purchased, in what time period inventory is to be

purchased. The other factors which are also present in cost reduction of company by knowing the

actual sales of company and break even sales of company. If company comes to know about the

minimum order quantity to complete the maximum demand of LK Ltd will be helping company in

cost elimination. Just- in- Time also help decrease in break down of machines which helps the

company in decreasing their cost. Margin safety helps in increasing profits of company by

purchasing raw material at the difference between forecasted sales and actual sale of company. In

this manner, all these above mentioned factors help LK Ltd in cost reduction or cost elimination of

company.

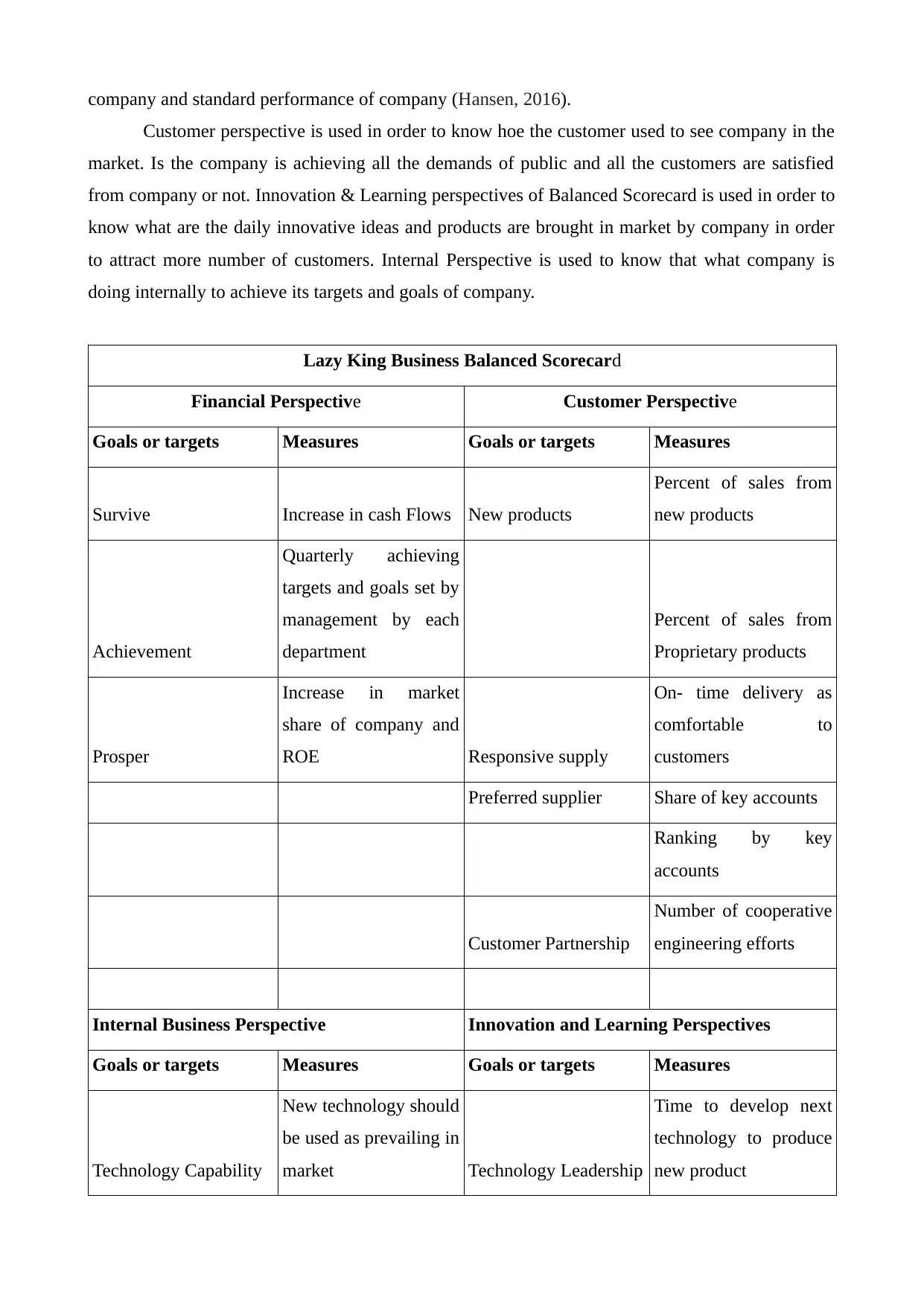

(c) Using Balanced Scorecard evaluating the areas where cost can be controlled

Balance Scorecard is prepared on the basis of four perspectives i.e. Financial Perspective,

International Business Perspectives, Customer Perspectives and Innovation & Learning Perspective.

Balance Scorecard is prepared to know the standard set for organization and these are to be

achieved by management in all perspectives. These are prepared on the past performance of

company for current year's performance. Financial Perspectives are used to know that company is

achieving its standard targets or not. This helps in comparison between actual performance of

machines and reliable suppliers.

ABC is the method which can be also in cost reduction in any organization. In this “A items”

refers to very tight and there is accurate recording of inventory, “B items” are with very less tightly

controlled and good records are maintained of inventory and “C items” are very less tighten in

company and with very minimum records are kept of these items. ABC analysis is the method in

which overall inventory cost has been defined and requires different inventory controls in any

organization (Kumar, 2015). “A items” are very important to be kept in any organization. It is also

estimated that 'A items' covers 20% of inventory charges for 70% of annual consumption, 'B items'

covers 30% of total inventory charges 25% of annual consumption and 'C items' covers 50% of

inventory charges 5% of annual consumption.

Safety stocks can be defined as an additional quantity required in order to minimise risks in

an organization. This inventory helps at the time when there is huge sale occurring in company

because of which huge production occurs which needs raw material in company (Albrecht, 2017). If

any manufacturer properly maintains safety stocks in any company than it can avoid risk of

production. In this way safety stocks can help company in production of extra products at time of

extra sales.

All these factors will be helping LK Ltd in cost reduction because these factors help

company in knowing what quantity are to be purchased, in what time period inventory is to be

purchased. The other factors which are also present in cost reduction of company by knowing the

actual sales of company and break even sales of company. If company comes to know about the

minimum order quantity to complete the maximum demand of LK Ltd will be helping company in

cost elimination. Just- in- Time also help decrease in break down of machines which helps the

company in decreasing their cost. Margin safety helps in increasing profits of company by

purchasing raw material at the difference between forecasted sales and actual sale of company. In

this manner, all these above mentioned factors help LK Ltd in cost reduction or cost elimination of

company.

(c) Using Balanced Scorecard evaluating the areas where cost can be controlled

Balance Scorecard is prepared on the basis of four perspectives i.e. Financial Perspective,

International Business Perspectives, Customer Perspectives and Innovation & Learning Perspective.

Balance Scorecard is prepared to know the standard set for organization and these are to be

achieved by management in all perspectives. These are prepared on the past performance of

company for current year's performance. Financial Perspectives are used to know that company is

achieving its standard targets or not. This helps in comparison between actual performance of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company and standard performance of company (Hansen, 2016).

Customer perspective is used in order to know hoe the customer used to see company in the

market. Is the company is achieving all the demands of public and all the customers are satisfied

from company or not. Innovation & Learning perspectives of Balanced Scorecard is used in order to

know what are the daily innovative ideas and products are brought in market by company in order

to attract more number of customers. Internal Perspective is used to know that what company is

doing internally to achieve its targets and goals of company.

Lazy King Business Balanced Scorecard

Financial Perspective Customer Perspective

Goals or targets Measures Goals or targets Measures

Survive Increase in cash Flows New products

Percent of sales from

new products

Achievement

Quarterly achieving

targets and goals set by

management by each

department

Percent of sales from

Proprietary products

Prosper

Increase in market

share of company and

ROE Responsive supply

On- time delivery as

comfortable to

customers

Preferred supplier Share of key accounts

Ranking by key

accounts

Customer Partnership

Number of cooperative

engineering efforts

Internal Business Perspective Innovation and Learning Perspectives

Goals or targets Measures Goals or targets Measures

Technology Capability

New technology should

be used as prevailing in

market Technology Leadership

Time to develop next

technology to produce

new product

Customer perspective is used in order to know hoe the customer used to see company in the

market. Is the company is achieving all the demands of public and all the customers are satisfied

from company or not. Innovation & Learning perspectives of Balanced Scorecard is used in order to

know what are the daily innovative ideas and products are brought in market by company in order

to attract more number of customers. Internal Perspective is used to know that what company is

doing internally to achieve its targets and goals of company.

Lazy King Business Balanced Scorecard

Financial Perspective Customer Perspective

Goals or targets Measures Goals or targets Measures

Survive Increase in cash Flows New products

Percent of sales from

new products

Achievement

Quarterly achieving

targets and goals set by

management by each

department

Percent of sales from

Proprietary products

Prosper

Increase in market

share of company and

ROE Responsive supply

On- time delivery as

comfortable to

customers

Preferred supplier Share of key accounts

Ranking by key

accounts

Customer Partnership

Number of cooperative

engineering efforts

Internal Business Perspective Innovation and Learning Perspectives

Goals or targets Measures Goals or targets Measures

Technology Capability

New technology should

be used as prevailing in

market Technology Leadership

Time to develop next

technology to produce

new product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manufacturing

Excellence

Time taken to convert

from raw material into

finished goods

Manufacturing

Learning

Process time to

maturity

Design Productivity

Wood and leather

efficiency Product Focus

90% sale of products

which are been

produced by company

New product

introduction in market

Actual production

versus Standard

production Time to market

Exact time to introduce

new product in market

Balanced Scorecard help in knowing actual performance of company are been achieved by

company or not. In LK Ltd., company is trying to achieve its goals and standards which are been set

by management of company. LK Ltd is planning for production plan which is used to achieve

optimum profit or loss of company by preparing a portfolio of different products which are giving

company higher profits as compared to those products who are giving less profits.

Leather and metals chair are giving higher profits to LK Ltd as compared to weed and

plastic so production plan is also prepared by taking 75 units of leather and metals chair. By

preparation of Balance Scorecard company will be knowing about that how much company has

achieved and what are not attained by LK Ltd.

Special Pricing Strategies which is best to be used by company

There are different types pricing strategies that can be used by any organization in order to

price their products which is helpful in company to earn higher profits on available inventory.

Several Pricing strategies are as follows :-

Cost- Plus Pricing-

In this strategy of pricing there is a small percentage which is added in cost to know total

price of product which is charged by company from its customers (Liozu, and et.al., 2015). In Table

1 profit is negative which shows that company should go for this cost plus pricing strategy because

it leads to negative profits. Company is adding 10% of profit in cost but it will be increasing with

the increase in percentage of profit. Thus, it is not best method for this company.

Competitive Pricing-

Competitive pricing strategy is the strategy where organization sets up price of product on

the basis of competitors existing in the market. In this case, there are no competitors given who can

be benchmarked for this organization as an competition and price can be set on that basis. Thus, it

is better to go with the existing strategy of pricing the product in company (Liu, 2019).

Profit – Margin based strategy-

Excellence

Time taken to convert

from raw material into

finished goods

Manufacturing

Learning

Process time to

maturity

Design Productivity

Wood and leather

efficiency Product Focus

90% sale of products

which are been

produced by company

New product

introduction in market

Actual production

versus Standard

production Time to market

Exact time to introduce

new product in market

Balanced Scorecard help in knowing actual performance of company are been achieved by

company or not. In LK Ltd., company is trying to achieve its goals and standards which are been set

by management of company. LK Ltd is planning for production plan which is used to achieve

optimum profit or loss of company by preparing a portfolio of different products which are giving

company higher profits as compared to those products who are giving less profits.

Leather and metals chair are giving higher profits to LK Ltd as compared to weed and

plastic so production plan is also prepared by taking 75 units of leather and metals chair. By

preparation of Balance Scorecard company will be knowing about that how much company has

achieved and what are not attained by LK Ltd.

Special Pricing Strategies which is best to be used by company

There are different types pricing strategies that can be used by any organization in order to

price their products which is helpful in company to earn higher profits on available inventory.

Several Pricing strategies are as follows :-

Cost- Plus Pricing-

In this strategy of pricing there is a small percentage which is added in cost to know total

price of product which is charged by company from its customers (Liozu, and et.al., 2015). In Table

1 profit is negative which shows that company should go for this cost plus pricing strategy because

it leads to negative profits. Company is adding 10% of profit in cost but it will be increasing with

the increase in percentage of profit. Thus, it is not best method for this company.

Competitive Pricing-

Competitive pricing strategy is the strategy where organization sets up price of product on

the basis of competitors existing in the market. In this case, there are no competitors given who can

be benchmarked for this organization as an competition and price can be set on that basis. Thus, it

is better to go with the existing strategy of pricing the product in company (Liu, 2019).

Profit – Margin based strategy-

In this strategy price is set by keeping some profit margin on sale after deciding sales per

unit. This strategy of pricing is best strategy which any organization can use and also it is easy to

calculate and implement in company. In table 2 profit shown are positive and company should go

for adopting this strategy of pricing the products in its business.

Scenario 2

(a) Evaluation of best Investment Decision to be selected for Kadlex Consultancy from available

alternatives

As per the calculation presented in appendix criteria of selecting best option for Kadlex

consultancy using various investment appraisals, wood Division is the best option for investment. It

is because wood division in Table 2 of Appendix pay back period is of 3 years and in Table 3 of

Appendix IRR is also highest with 15.59% as compared to other two divisions. Table 1 of Appendix

Net Present Value of Wood division is positive as compared to the other division of Kadlex Ltd

which are obtaining negative profits. Kadlex Ltd should go for investing in Wood division because

this division is giving higher profits as compared to other divisions.

(b) Evaluating the benefits and limitations of measures used in selection of Investment Appraisals

by kadlex Consultancy Ltd.

Measures used by Kadlex Ltd in order to select best investment in company are Net Present

value, Internal Rate Of return and Pay Back Period. These are the best measures which can help

company in knowing that in which project company should invest in order to obtain maximum

profits for company. These various measure of investment appraisals are as follows-

Net Present Value- Net Present Value can be defined as bringing all the cash flows of company at

present value in order to know what are the present value of future cash flows (Jansen, 2016). It also

considers various aspects such as salvage value, depreciation etc. in order to know the net cash

inflows and cash outflows of company. Net present value can be calculated by deducting initial

investment from discounted cash inflows of company. Discounted cash Inflows are calculated by

dividing cash inflows from cost of capital.

Advantages Disadvantages

This method takes time of value in

account by dividing all the cash inflows

from weighted cost of capital;

This method helps in increasing the

firm's value;

It is difficult to calculate because it is

hard to understand;

It needs professionals to understand

situation of company;

It is very lengthy process to be

unit. This strategy of pricing is best strategy which any organization can use and also it is easy to

calculate and implement in company. In table 2 profit shown are positive and company should go

for adopting this strategy of pricing the products in its business.

Scenario 2

(a) Evaluation of best Investment Decision to be selected for Kadlex Consultancy from available

alternatives

As per the calculation presented in appendix criteria of selecting best option for Kadlex

consultancy using various investment appraisals, wood Division is the best option for investment. It

is because wood division in Table 2 of Appendix pay back period is of 3 years and in Table 3 of

Appendix IRR is also highest with 15.59% as compared to other two divisions. Table 1 of Appendix

Net Present Value of Wood division is positive as compared to the other division of Kadlex Ltd

which are obtaining negative profits. Kadlex Ltd should go for investing in Wood division because

this division is giving higher profits as compared to other divisions.

(b) Evaluating the benefits and limitations of measures used in selection of Investment Appraisals

by kadlex Consultancy Ltd.

Measures used by Kadlex Ltd in order to select best investment in company are Net Present

value, Internal Rate Of return and Pay Back Period. These are the best measures which can help

company in knowing that in which project company should invest in order to obtain maximum

profits for company. These various measure of investment appraisals are as follows-

Net Present Value- Net Present Value can be defined as bringing all the cash flows of company at

present value in order to know what are the present value of future cash flows (Jansen, 2016). It also

considers various aspects such as salvage value, depreciation etc. in order to know the net cash

inflows and cash outflows of company. Net present value can be calculated by deducting initial

investment from discounted cash inflows of company. Discounted cash Inflows are calculated by

dividing cash inflows from cost of capital.

Advantages Disadvantages

This method takes time of value in

account by dividing all the cash inflows

from weighted cost of capital;

This method helps in increasing the

firm's value;

It is difficult to calculate because it is

hard to understand;

It needs professionals to understand

situation of company;

It is very lengthy process to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability and risk associated with

those profits are given highest priority;

Both cash flows after and before are

taken into account over the span of life.

implemented in company;

It is very difficult to calculate appropriate

discount rate for company.

Pay Back Period- Pay Back Period is defined as that period in which all the investment in an

project are covered by cash inflows. It does not takes into account time of value in order to calculate

this method (Orioli, 2017). It is calculated by knowing that in how much time all cash inflows

covers the initial investment of company. It is very method and can be implemented in any

organization to know which project can give fast pay back of initial investment.

Advantages Disadvantages

It is very easy to calculate and

implement in any organization;

It does not need any professional to

understand this method to implement in

an organization;

This method shows that in how much

time company will be getting back its all

investment in a project.

This does not take into time of value

which is a huge lacking in this method;

This method does not take cash inflows

after depreciation and taxes paid;

It is not applicable in big organization

because there are various expenses such

as inflation rates, interest rates etc.

Internal Rate of Return- Internal Rate of Return can be defined as that rate which company can

earn from initial investment and future cash flows. It is defined as the rate at which company wants

to earn otherwise company will be facing losses (Sim, 2017). The project is accepted if Internal

Rate of Return is higher than cost of capital of company. It is calculated by taking all the cash

inflows and initial investment into account and finding out the rate at which company is earning

cash inflows for company.

Advantages Disadvantages

It is very easy method to calculate and

also does not need any professional to

calculate this method;

The method is not very expensive and

It does not take into net cash inflows

which takes into account depreciation

and salvage value of project;

It is useful for big firms who wants to

those profits are given highest priority;

Both cash flows after and before are

taken into account over the span of life.

implemented in company;

It is very difficult to calculate appropriate

discount rate for company.

Pay Back Period- Pay Back Period is defined as that period in which all the investment in an

project are covered by cash inflows. It does not takes into account time of value in order to calculate

this method (Orioli, 2017). It is calculated by knowing that in how much time all cash inflows

covers the initial investment of company. It is very method and can be implemented in any

organization to know which project can give fast pay back of initial investment.

Advantages Disadvantages

It is very easy to calculate and

implement in any organization;

It does not need any professional to

understand this method to implement in

an organization;

This method shows that in how much

time company will be getting back its all

investment in a project.

This does not take into time of value

which is a huge lacking in this method;

This method does not take cash inflows

after depreciation and taxes paid;

It is not applicable in big organization

because there are various expenses such

as inflation rates, interest rates etc.

Internal Rate of Return- Internal Rate of Return can be defined as that rate which company can

earn from initial investment and future cash flows. It is defined as the rate at which company wants

to earn otherwise company will be facing losses (Sim, 2017). The project is accepted if Internal

Rate of Return is higher than cost of capital of company. It is calculated by taking all the cash

inflows and initial investment into account and finding out the rate at which company is earning

cash inflows for company.

Advantages Disadvantages

It is very easy method to calculate and

also does not need any professional to

calculate this method;

The method is not very expensive and

It does not take into net cash inflows

which takes into account depreciation

and salvage value of project;

It is useful for big firms who wants to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be used by small firms;

Method helps in knowing the net rate of

return of company by future cash inflows

and initial investment.

know net return rate of company;

It does not takes into various expenses

such as interest rates, inflation rates etc.

(c) Preparation of Balanced Scorecard for short- term Financial Performance by Kadlex

Consultancy for reduction of short- term orientation

Balanced Scorecard can help Kadlex Plc in knowing the short term financial performance.

For example, from financial perspective company wants minimum working capital which is set

under balanced scorecard. If company keeps that minimum working capital than Kadlex will never

be facing any liquidity crunch because there will be proper balance of working capital in company

(Akkermans, 2018).

It will also help company in paying off all its current liabilities by current assets at the time

of facing any liquidity crunch in the company. It will also not stop in the process of production if

there is minimum working capital in the company and will continue company's daily requirement of

working capital. These are the short term benefits of preparing Balanced Scorecard by Kadlex Plc.

CONCLUSION

From the above report it can be summarized that the cost controlling and reduction can be

done through preparing Balanced Scorecard which help the company in setting up standards.

Balanced Scorecard help both companies in knowing what targets are to be achieved by company

for earning higher profits and achieving organizational goals and growth. This report also represents

production plan used to maximize profits of LK Ltd in order to achieve higher profits for company.

Production plan help LK Ltd in preparing portfolio of different products to maximize company's

profits. Kadlex Ltd has different way of working and uses divisional profits in order to know profits

in each department. Company wants to invest in department which will be giving higher profits.

This is measured by company by using different investment appraisals such as Net present value,

Internal rate of return and Pay back period. These measure help the company in knowing that Wood

Division is giving highest profits to Kadlex consultancy as compared to other divisions. Thus,

Kadlex consultancy Ltd should go for investing in Wood Division in order to higher profits for

company.

Method helps in knowing the net rate of

return of company by future cash inflows

and initial investment.

know net return rate of company;

It does not takes into various expenses

such as interest rates, inflation rates etc.

(c) Preparation of Balanced Scorecard for short- term Financial Performance by Kadlex

Consultancy for reduction of short- term orientation

Balanced Scorecard can help Kadlex Plc in knowing the short term financial performance.

For example, from financial perspective company wants minimum working capital which is set

under balanced scorecard. If company keeps that minimum working capital than Kadlex will never

be facing any liquidity crunch because there will be proper balance of working capital in company

(Akkermans, 2018).

It will also help company in paying off all its current liabilities by current assets at the time

of facing any liquidity crunch in the company. It will also not stop in the process of production if

there is minimum working capital in the company and will continue company's daily requirement of

working capital. These are the short term benefits of preparing Balanced Scorecard by Kadlex Plc.

CONCLUSION

From the above report it can be summarized that the cost controlling and reduction can be

done through preparing Balanced Scorecard which help the company in setting up standards.

Balanced Scorecard help both companies in knowing what targets are to be achieved by company

for earning higher profits and achieving organizational goals and growth. This report also represents

production plan used to maximize profits of LK Ltd in order to achieve higher profits for company.

Production plan help LK Ltd in preparing portfolio of different products to maximize company's

profits. Kadlex Ltd has different way of working and uses divisional profits in order to know profits

in each department. Company wants to invest in department which will be giving higher profits.

This is measured by company by using different investment appraisals such as Net present value,

Internal rate of return and Pay back period. These measure help the company in knowing that Wood

Division is giving highest profits to Kadlex consultancy as compared to other divisions. Thus,

Kadlex consultancy Ltd should go for investing in Wood Division in order to higher profits for

company.

REFERENCES

Books and Journals

Akkermans, H. A. and Van Oorschot, K. E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan. London.

Albrecht, M., 2017. Optimization of safety stocks in models with an order service level objective or

constraint. European Journal of Operational Research. 263(3). pp.900-909.

Balaji, N. A., Sukumar, R. and Parvathy, M., 2019. Enhanced dual authentication and key

management scheme for data authentication in vehicular ad hoc network. Computers &

Electrical Engineering. 76. pp.94-110.

Becher, S., and et.al., 2018. A method for manufacturing a product according to a production plan.

U.S. Patent Application 15/553.459.

Bian, Y., and et.al., 2017. An EOQ-based profit maximization model considering financing cost of

working capital requirement.

Chen, M., and et.al., 2015. On the computation offloading at ad hoc cloudlet: architecture and

service modes. IEEE Communications Magazine. 53(6). pp.18-24.

Gosse, J. H. and Sharp, E. J., 2017. September. Explicit Margin of Safety Assessment of Composite

Structure. In International Workshop on Meshfree Methods for Partial Differential

Equations (pp. 43-51). Springer. Cham.

Hansen, E. G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic review

of architectures. Journal of Business Ethics. 133(2). pp.193-221.

Jansen, J. G. J., 2016. Dredge Mining Sequence Optimization: Maximizing the Net Present Value

(NPV).

Kamei, Y., and et.al., 2016. Studying just-in-time defect prediction using cross-project

models. Empirical Software Engineering. 21(5). pp.2072-2106.

Kumar, S. and Chakravarty, A., 2015. ABC–VED analysis of expendable medical stores at a tertiary

care hospital. Medical journal armed forces india. 71(1). pp.24-27.

Liozu, S., and et.al., 2015. Mindful Pricing: Transforming Organizations Through Value Based

Pricing. In Marketing Dynamism & Sustainability: Things Change, Things Stay the

Same… (pp. 412-421). Springer, Cham.

Liu, Z., Gao, R., Zhou, C. and Ma, N., 2019. Two-period pricing and strategy choice for a supply

Books and Journals

Akkermans, H. A. and Van Oorschot, K. E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan. London.

Albrecht, M., 2017. Optimization of safety stocks in models with an order service level objective or

constraint. European Journal of Operational Research. 263(3). pp.900-909.

Balaji, N. A., Sukumar, R. and Parvathy, M., 2019. Enhanced dual authentication and key

management scheme for data authentication in vehicular ad hoc network. Computers &

Electrical Engineering. 76. pp.94-110.

Becher, S., and et.al., 2018. A method for manufacturing a product according to a production plan.

U.S. Patent Application 15/553.459.

Bian, Y., and et.al., 2017. An EOQ-based profit maximization model considering financing cost of

working capital requirement.

Chen, M., and et.al., 2015. On the computation offloading at ad hoc cloudlet: architecture and

service modes. IEEE Communications Magazine. 53(6). pp.18-24.

Gosse, J. H. and Sharp, E. J., 2017. September. Explicit Margin of Safety Assessment of Composite

Structure. In International Workshop on Meshfree Methods for Partial Differential

Equations (pp. 43-51). Springer. Cham.

Hansen, E. G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic review

of architectures. Journal of Business Ethics. 133(2). pp.193-221.

Jansen, J. G. J., 2016. Dredge Mining Sequence Optimization: Maximizing the Net Present Value

(NPV).

Kamei, Y., and et.al., 2016. Studying just-in-time defect prediction using cross-project

models. Empirical Software Engineering. 21(5). pp.2072-2106.

Kumar, S. and Chakravarty, A., 2015. ABC–VED analysis of expendable medical stores at a tertiary

care hospital. Medical journal armed forces india. 71(1). pp.24-27.

Liozu, S., and et.al., 2015. Mindful Pricing: Transforming Organizations Through Value Based

Pricing. In Marketing Dynamism & Sustainability: Things Change, Things Stay the

Same… (pp. 412-421). Springer, Cham.

Liu, Z., Gao, R., Zhou, C. and Ma, N., 2019. Two-period pricing and strategy choice for a supply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.