Management Accounting: Planning Tools, Financial Analysis, and Success

VerifiedAdded on 2020/10/05

|12

|3335

|144

Report

AI Summary

This report provides a detailed analysis of management accounting, focusing on budgetary control and its various planning tools, including fixed, flexible, incremental, zero-based budgets, variance analysis, and cash budgets. It assesses the advantages and disadvantages of each tool. The report then explores the evolution of management accounting, from cost accounting to value-based management, and examines how organizations respond to financial problems using ratio analysis, key performance indicators (KPIs), and benchmarking. The report also evaluates how management accounting systems, particularly cost control systems, are used to solve financial problems. The report concludes with an assessment of how management accounting can contribute to an organization's sustainable success, emphasizing the importance of planning tools in addressing financial challenges and fostering growth.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 2..........................................................................................................................................................3

P4. Advantages and disadvantages of different planning tools used for budgetary control....................3

M3. Assessment of different planning tools and their application for preparing and forecasting budget.

.................................................................................................................................................................5

P5. Assessment of management accounting system in respond to financial problems...........................6

M4. Assessment of how management accounting can lead organization to sustainable success...........9

D3. Assessment of planning tools to solve financial problems which leads to sustainable growth and

success of organization............................................................................................................................9

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

2

INTRODUCTION...........................................................................................................................................3

TASK 2..........................................................................................................................................................3

P4. Advantages and disadvantages of different planning tools used for budgetary control....................3

M3. Assessment of different planning tools and their application for preparing and forecasting budget.

.................................................................................................................................................................5

P5. Assessment of management accounting system in respond to financial problems...........................6

M4. Assessment of how management accounting can lead organization to sustainable success...........9

D3. Assessment of planning tools to solve financial problems which leads to sustainable growth and

success of organization............................................................................................................................9

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

2

INTRODUCTION

Management accounting is the process of identifying, classifying, summarizing, recording,

analysing and monitoring financial information which are used by internal management of the

organization for strategic decision making to attain organizational goals and objectives. This

report will highlight advantages and disadvantages of various planning tools used in budgetary

control. It also includes brief history of evolution of management accounting and assessment of

how organization adapt to various financial problem in reference to ratio analysis, key

performance indicators and benchmarking. It also highlights management accounting system

which are used to solve the financial problems of the organization effectively and efficiently.

TASK 2

P4. Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control is a tool of finance that helps the manager of the company to control cost

of the company which includes budget preparation, department coordination and comparing

actual performances with estimated performances of the company. It helps the company in

controlling cost and maximize the profit of company, it leads to coordination among various

departments of the company and it helps company to achieve economies of scale.

1. Fixed budget: This planning tool of budgetary control is also referred to as static budget.

Fixed budget do not vary with the change in the operation of business. Costs are fixed so

that expenses do not vary with the change in the revenue (Chenhall and Moers, 2015).

Advantages of Fixed budget

Fixed budget helps in measuring profits and performance of the business

according to the planned budget.

This type of budget helps in keeping the cost down of business and gives clear

distinct ideas to prioritize important activities which are essential for the growth

and expansion of business (Van der Stede, 2015).

This budget is easy to use and easier to estimate the amount of tax for the

particular period.

Disadvantages of Fixed budget

Fixed budget cannot be amended at any time during the financial year, even when

there is a change in the operation of business activity.

3

Management accounting is the process of identifying, classifying, summarizing, recording,

analysing and monitoring financial information which are used by internal management of the

organization for strategic decision making to attain organizational goals and objectives. This

report will highlight advantages and disadvantages of various planning tools used in budgetary

control. It also includes brief history of evolution of management accounting and assessment of

how organization adapt to various financial problem in reference to ratio analysis, key

performance indicators and benchmarking. It also highlights management accounting system

which are used to solve the financial problems of the organization effectively and efficiently.

TASK 2

P4. Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control is a tool of finance that helps the manager of the company to control cost

of the company which includes budget preparation, department coordination and comparing

actual performances with estimated performances of the company. It helps the company in

controlling cost and maximize the profit of company, it leads to coordination among various

departments of the company and it helps company to achieve economies of scale.

1. Fixed budget: This planning tool of budgetary control is also referred to as static budget.

Fixed budget do not vary with the change in the operation of business. Costs are fixed so

that expenses do not vary with the change in the revenue (Chenhall and Moers, 2015).

Advantages of Fixed budget

Fixed budget helps in measuring profits and performance of the business

according to the planned budget.

This type of budget helps in keeping the cost down of business and gives clear

distinct ideas to prioritize important activities which are essential for the growth

and expansion of business (Van der Stede, 2015).

This budget is easy to use and easier to estimate the amount of tax for the

particular period.

Disadvantages of Fixed budget

Fixed budget cannot be amended at any time during the financial year, even when

there is a change in the operation of business activity.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed budget is do not account for unpredictable events and activities and is

highly inflexible to the change in operations of business.

This planning tool of budgetary control is not an effective measure to track and

control expenses.

2. Flexible budget: It is a budget that adjusts with change in the volume and activity.

Flexible budget gets altered amid the year for original sales, changes in cost of

production and any other change in business working conditions.

Advantages of Flexible budget

Variable cost in flexible budgets are characterized as percentages of sales. For example,

if sales somehow increment significantly, flexible budgets would change in accordance

with spending on marketing to gain more profit of unexpected increase in income.

A flexible budget can detect change in the overall revenue, and the team can take

remedial actions to fix the issue.

Disadvantages of Flexible budget

It can be tedious to think of exactly how variant those variable costs might be. Time is

mostly at premium during the budgetary season.

A lot of rules lead to people breaking them as it becomes difficult for them to abide with

them.

3. Incremental budget: This type of budget is prepared by analysing and evaluating

previous year’s budgeted plan by adding some incremental value to the budget which

helps in achieving desired goals and objective effectively and efficiently.

Advantages of Incremental budget

This planning tool of budget is simple to use and well structured to consistently

operate in a stable manner for attaining long term goal of the company.

Incremental budget is flexible and ensure there is no large deviation in the budget

as it changes gradually year after year (Advantages and Disadvantages of

Incremental Budgeting, 2019).

Disadvantages of Incremental budget

This method leads to lack of innovation and stays same with minimum changes in

budget plan.

4

highly inflexible to the change in operations of business.

This planning tool of budgetary control is not an effective measure to track and

control expenses.

2. Flexible budget: It is a budget that adjusts with change in the volume and activity.

Flexible budget gets altered amid the year for original sales, changes in cost of

production and any other change in business working conditions.

Advantages of Flexible budget

Variable cost in flexible budgets are characterized as percentages of sales. For example,

if sales somehow increment significantly, flexible budgets would change in accordance

with spending on marketing to gain more profit of unexpected increase in income.

A flexible budget can detect change in the overall revenue, and the team can take

remedial actions to fix the issue.

Disadvantages of Flexible budget

It can be tedious to think of exactly how variant those variable costs might be. Time is

mostly at premium during the budgetary season.

A lot of rules lead to people breaking them as it becomes difficult for them to abide with

them.

3. Incremental budget: This type of budget is prepared by analysing and evaluating

previous year’s budgeted plan by adding some incremental value to the budget which

helps in achieving desired goals and objective effectively and efficiently.

Advantages of Incremental budget

This planning tool of budget is simple to use and well structured to consistently

operate in a stable manner for attaining long term goal of the company.

Incremental budget is flexible and ensure there is no large deviation in the budget

as it changes gradually year after year (Advantages and Disadvantages of

Incremental Budgeting, 2019).

Disadvantages of Incremental budget

This method leads to lack of innovation and stays same with minimum changes in

budget plan.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This planning tool encourages higher spending to maintain same amount for the

upcoming budget plan.

4. Zero based budget: It is setting up of a financial plan from the start with a zero-base.

Advantages of Zero-based budget

Proficient allotment of resources, it does not focus on the past numbers whereas they look

over to the actual number.

Removes all ineffective and unnecessary activities which results in cost effective ways

and recognizing new opportunities.

Disadvantages of Zero-based budget

Unyielding and time-consuming work for a company.

Lack of expertise amongst the employees on the topic

5. Variance analysis: Variance Analysis is the quantitative examination of the deviation

between the actual number and the planned budgeted number. For instance, if you plan a

budget for sales to be $20000 but the actual sales in $18000 then the variance analysis

provides a difference of $2000.

Advantages of Variance analysis

Combative Lead: Variance analysis assists a company to be proactive in attaining their

business goals and helps in discovering and alleviate any probable risk.

Recognizing the changes: Sometimes comparing budget with the genuine outcomes may

divert our attention to re-evaluate the target customers (Miller, 2018).

Disadvantages of Variance analysis

Delayed Process: Management teams needs the feedback as soon as possible but

accounting team assembles variances at the end of the month only.

Improper Analysis: If planning is not performed taking into account the detailed analysis

of each and every factor then the budgeting process may not astray from the actual

numbers.

6. Cash Budget: Expected flow of cash inflows and outflows which analyses revenues and

expenses of the company.

Advantages of cash budget

Decision making - It helps the company to know future cash position of the company to

make future decisions.

5

upcoming budget plan.

4. Zero based budget: It is setting up of a financial plan from the start with a zero-base.

Advantages of Zero-based budget

Proficient allotment of resources, it does not focus on the past numbers whereas they look

over to the actual number.

Removes all ineffective and unnecessary activities which results in cost effective ways

and recognizing new opportunities.

Disadvantages of Zero-based budget

Unyielding and time-consuming work for a company.

Lack of expertise amongst the employees on the topic

5. Variance analysis: Variance Analysis is the quantitative examination of the deviation

between the actual number and the planned budgeted number. For instance, if you plan a

budget for sales to be $20000 but the actual sales in $18000 then the variance analysis

provides a difference of $2000.

Advantages of Variance analysis

Combative Lead: Variance analysis assists a company to be proactive in attaining their

business goals and helps in discovering and alleviate any probable risk.

Recognizing the changes: Sometimes comparing budget with the genuine outcomes may

divert our attention to re-evaluate the target customers (Miller, 2018).

Disadvantages of Variance analysis

Delayed Process: Management teams needs the feedback as soon as possible but

accounting team assembles variances at the end of the month only.

Improper Analysis: If planning is not performed taking into account the detailed analysis

of each and every factor then the budgeting process may not astray from the actual

numbers.

6. Cash Budget: Expected flow of cash inflows and outflows which analyses revenues and

expenses of the company.

Advantages of cash budget

Decision making - It helps the company to know future cash position of the company to

make future decisions.

5

Reduction in cost - It helps company to know their cash deficit and the areas of

operations where cost needs to be reduced.

Disadvantages of cash budget

Do no considered credit or non-monetary transaction

Advantages of pricing strategies

Profit maximisation - It helps in maximising the profit of the company and increase in

sales of the company if right pricing strategy is chosen.

Increase in market share – The correct price strategy helps in increasing the market

share of the company.

M3. Assessment of different planning tools and their application for preparing and forecasting

budget.

Fixed budget is used to measure and evaluate both short term budget plan and long-term

budget plan. Fixed budget helps in forecasting and preparing budget by keeping the cost and

expenses constant with the change in sales or revenue. Fixed budget helps in forecasting both

short term and long-term budget plan for effective decision making.

Flexible budget is useful when cost is aligned with the change in the operations of business

activity. Flexible budget helps in forecasting the change in the budget plan and resources needed

to accomplish the task.

Incremental budget helps is useful in planning orientation and is useful for management to

focus on long term goals of business on a timely manner. This planning tool of budgetary control

helps in forecasting the need and objective of future and accordingly implement changes in the

preceding year’s budget plan.

Zero based budgeting is flexible which helps in lowering the cost and execution of plan in

the most disciplined manner from the scratch. This budget plan helps in preparation and

forecasting of budge by aligning company’s spending with objectives.

Variance analysis is useful identifying the deviations by comparing actual performance

with the budgeted plan. Variance analysis helps in preparation and forecasting budget as it act as

an in-depth control tool for more accuracy and efficiency. Variance analysis is useful in

managing risk.

6

operations where cost needs to be reduced.

Disadvantages of cash budget

Do no considered credit or non-monetary transaction

Advantages of pricing strategies

Profit maximisation - It helps in maximising the profit of the company and increase in

sales of the company if right pricing strategy is chosen.

Increase in market share – The correct price strategy helps in increasing the market

share of the company.

M3. Assessment of different planning tools and their application for preparing and forecasting

budget.

Fixed budget is used to measure and evaluate both short term budget plan and long-term

budget plan. Fixed budget helps in forecasting and preparing budget by keeping the cost and

expenses constant with the change in sales or revenue. Fixed budget helps in forecasting both

short term and long-term budget plan for effective decision making.

Flexible budget is useful when cost is aligned with the change in the operations of business

activity. Flexible budget helps in forecasting the change in the budget plan and resources needed

to accomplish the task.

Incremental budget helps is useful in planning orientation and is useful for management to

focus on long term goals of business on a timely manner. This planning tool of budgetary control

helps in forecasting the need and objective of future and accordingly implement changes in the

preceding year’s budget plan.

Zero based budgeting is flexible which helps in lowering the cost and execution of plan in

the most disciplined manner from the scratch. This budget plan helps in preparation and

forecasting of budge by aligning company’s spending with objectives.

Variance analysis is useful identifying the deviations by comparing actual performance

with the budgeted plan. Variance analysis helps in preparation and forecasting budget as it act as

an in-depth control tool for more accuracy and efficiency. Variance analysis is useful in

managing risk.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P5. Assessment of management accounting system in respond to financial problems.

Management accounting system helps manager in outlining manager in financial decision

making by helping in analysis of balance sheet, income statements, etc.

EVOLUTION OF MANAGEMENT ACCOUNTING

1st STAGE: COST ACCOUNTING (1920-1950):

This is the first phase of management accounting where matching principles of

accounting concept were developed. This phase of accounting focus on determination of cost and

control of finances (Chenhall and Moers, 2015).

2nd STAGE: MANAGERIAL ACCOUNTING (1951-1980)

Next phase after the period of cost accounting is managerial accounting who aims at

providing information to the management which helps in planning, controlling, monitoring and

implementing the desired plan to achieve organizational goals and objective effectively and

efficiently.

3rd STAGE: CAM-I COST MANAGEMENT (1980’s)

This phase of management accounting shifts its focus on reducing cost and achieving

economies of scale by using various cost control tools. This helps in managing inventory and raw

material by analysing product life cycle.

4th STAGE: VALUE BASED MANAGEMENT (1990’s)

This is the current phase of management by completely shifting its focus on creation on

more value to its customer and helps in higher market share and larger customer base (Historical

Evolution of Management Accounting, 2015). This phase of management accounting aims at

adding value to its customers and higher customer base and market share.

Evaluation of financial problem of the organization in context with the ratio analysis, key

performance indicator and benchmarking.

Ratio analysis: It is a quantitative method of analysing company’s financial performance

by using various financial tools (Williams and Dobelman, 2017). There are various financial

ratio like current ratio, liquidity ratio, performance indicator ratio, inventory turnover ratio,

return on capital employed ratio, return on investment ratio, etc. which helps in determining

various aspects of organization.

Critical evaluation of ratio analysis to solve financial problem:

7

Management accounting system helps manager in outlining manager in financial decision

making by helping in analysis of balance sheet, income statements, etc.

EVOLUTION OF MANAGEMENT ACCOUNTING

1st STAGE: COST ACCOUNTING (1920-1950):

This is the first phase of management accounting where matching principles of

accounting concept were developed. This phase of accounting focus on determination of cost and

control of finances (Chenhall and Moers, 2015).

2nd STAGE: MANAGERIAL ACCOUNTING (1951-1980)

Next phase after the period of cost accounting is managerial accounting who aims at

providing information to the management which helps in planning, controlling, monitoring and

implementing the desired plan to achieve organizational goals and objective effectively and

efficiently.

3rd STAGE: CAM-I COST MANAGEMENT (1980’s)

This phase of management accounting shifts its focus on reducing cost and achieving

economies of scale by using various cost control tools. This helps in managing inventory and raw

material by analysing product life cycle.

4th STAGE: VALUE BASED MANAGEMENT (1990’s)

This is the current phase of management by completely shifting its focus on creation on

more value to its customer and helps in higher market share and larger customer base (Historical

Evolution of Management Accounting, 2015). This phase of management accounting aims at

adding value to its customers and higher customer base and market share.

Evaluation of financial problem of the organization in context with the ratio analysis, key

performance indicator and benchmarking.

Ratio analysis: It is a quantitative method of analysing company’s financial performance

by using various financial tools (Williams and Dobelman, 2017). There are various financial

ratio like current ratio, liquidity ratio, performance indicator ratio, inventory turnover ratio,

return on capital employed ratio, return on investment ratio, etc. which helps in determining

various aspects of organization.

Critical evaluation of ratio analysis to solve financial problem:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This tool helps in analysing financial performance of the organization by using various

financial ratios. Ratio analysis helps in identifying and evaluating the strengths and weakness of

the organization. This helps in strategic decision making of the organization to achieve long term

and short term goals and objective.

Key performance indicators: It is a performance metrics used by company’s and

management of the organization to analyse and evaluate the performance and financial position

of the organization. Key performance indicator is important for measuring the performance and

evaluating whether goals and targets are achieved or not.

Critical evaluation of key performance indicators to solve financial problem:

Key performance indicator is quantifiable and helps in solving financial problem of the

organization by keeping employees motivated to focus on key task which are important for the

sustainable growth and success of organization. KPI also helps in highlighting success or issues

related with business and helps in effective decision making. KPI is well defined and can be

communicated throughout the hierarchy of the organization.

Benchmarking: It is a process of identifying and evaluating the actual position of

business by applying best practices to the operations of the organization effectively and

efficiently to achieve long term goals and objectives (Benchmarking, 2018).

Critical evaluation of benchmarking to solve financial problem:

Benchmarking helps in identifying the financial problem by critically evaluating the

performance externally with its competitors and internally with operations within the

organization. In case of any financial problem or deviation benchmarking helps in improving the

performance by practicing more innovation in the operations. This tool of performance metrics

helps solving financial problem by setting a standardized procedure and identifying areas of

improvement (Maas, Schaltegger and Crutzen, 2016).

Evaluation of how management accounting system are used by organization to solve

financial problems.

Cost control system: It is a type of management accounting system which helps in

minimizing the cost of business and carry out operations in the more economical way to

achieve economies of scale.

Critical evaluation of cost control system to solve financial problems of the organization.

8

financial ratios. Ratio analysis helps in identifying and evaluating the strengths and weakness of

the organization. This helps in strategic decision making of the organization to achieve long term

and short term goals and objective.

Key performance indicators: It is a performance metrics used by company’s and

management of the organization to analyse and evaluate the performance and financial position

of the organization. Key performance indicator is important for measuring the performance and

evaluating whether goals and targets are achieved or not.

Critical evaluation of key performance indicators to solve financial problem:

Key performance indicator is quantifiable and helps in solving financial problem of the

organization by keeping employees motivated to focus on key task which are important for the

sustainable growth and success of organization. KPI also helps in highlighting success or issues

related with business and helps in effective decision making. KPI is well defined and can be

communicated throughout the hierarchy of the organization.

Benchmarking: It is a process of identifying and evaluating the actual position of

business by applying best practices to the operations of the organization effectively and

efficiently to achieve long term goals and objectives (Benchmarking, 2018).

Critical evaluation of benchmarking to solve financial problem:

Benchmarking helps in identifying the financial problem by critically evaluating the

performance externally with its competitors and internally with operations within the

organization. In case of any financial problem or deviation benchmarking helps in improving the

performance by practicing more innovation in the operations. This tool of performance metrics

helps solving financial problem by setting a standardized procedure and identifying areas of

improvement (Maas, Schaltegger and Crutzen, 2016).

Evaluation of how management accounting system are used by organization to solve

financial problems.

Cost control system: It is a type of management accounting system which helps in

minimizing the cost of business and carry out operations in the more economical way to

achieve economies of scale.

Critical evaluation of cost control system to solve financial problems of the organization.

8

Cost control system helps in solving financial problem by simply preventing wastage

within its business operations. This system also helps in analysing variance by comparing actual

results with budgeted plan. It also helps in identifying cost drivers which helps in increasing

operational productivity and profitability.

Example: In case of financial problem like high cost in production, management of the

organization uses cost control system to identify the cause of problem which leads to strategic

decision making, cost reduction and lower level of wastage.

Inventory management system: This management system of the organization helps in

keeping track on the production of the business which leads to ordering, storing and

controlling the inventory for smooth flow and operations of the company.

Critical evaluation of Inventory management system to solve financial problems of the

organization.

Inventory management system helps in solving financial problem by reducing labour

cost, storage cost and dead stock which leads to improved cash flows and effective forecasting

capabilities to enhance transparency and improved supplier relationship (What is an Inventory

Management System? Definition of Inventory Management Systems, Benefits, Best Practices &

More, 2019).

Example: In case of insufficient inventory or raw material in the organization which leads to

lower operational efficiency and productivity. Management of the organization will adopt

inventory management system to keep track of inventory and order raw material on a timely

manner.

Price optimization system: This is a quantitative analysis of data to determine the

behaviour of customers in respond to varied prices of different products and services.

Critical evaluation of Price optimization system to solve financial problems of the

organization.

Price optimization system helps in solving financial problem by determining the prices

which are best suitable for meeting business objective and maximizing profits.

Example: Rivalry competitor in the market offers products at more attractive price which

leads to higher customer switching rate. Organization strategically adapt to price optimization

system to determine how much the customer is willing to pay for the product and how much

value does it add to product.

9

within its business operations. This system also helps in analysing variance by comparing actual

results with budgeted plan. It also helps in identifying cost drivers which helps in increasing

operational productivity and profitability.

Example: In case of financial problem like high cost in production, management of the

organization uses cost control system to identify the cause of problem which leads to strategic

decision making, cost reduction and lower level of wastage.

Inventory management system: This management system of the organization helps in

keeping track on the production of the business which leads to ordering, storing and

controlling the inventory for smooth flow and operations of the company.

Critical evaluation of Inventory management system to solve financial problems of the

organization.

Inventory management system helps in solving financial problem by reducing labour

cost, storage cost and dead stock which leads to improved cash flows and effective forecasting

capabilities to enhance transparency and improved supplier relationship (What is an Inventory

Management System? Definition of Inventory Management Systems, Benefits, Best Practices &

More, 2019).

Example: In case of insufficient inventory or raw material in the organization which leads to

lower operational efficiency and productivity. Management of the organization will adopt

inventory management system to keep track of inventory and order raw material on a timely

manner.

Price optimization system: This is a quantitative analysis of data to determine the

behaviour of customers in respond to varied prices of different products and services.

Critical evaluation of Price optimization system to solve financial problems of the

organization.

Price optimization system helps in solving financial problem by determining the prices

which are best suitable for meeting business objective and maximizing profits.

Example: Rivalry competitor in the market offers products at more attractive price which

leads to higher customer switching rate. Organization strategically adapt to price optimization

system to determine how much the customer is willing to pay for the product and how much

value does it add to product.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

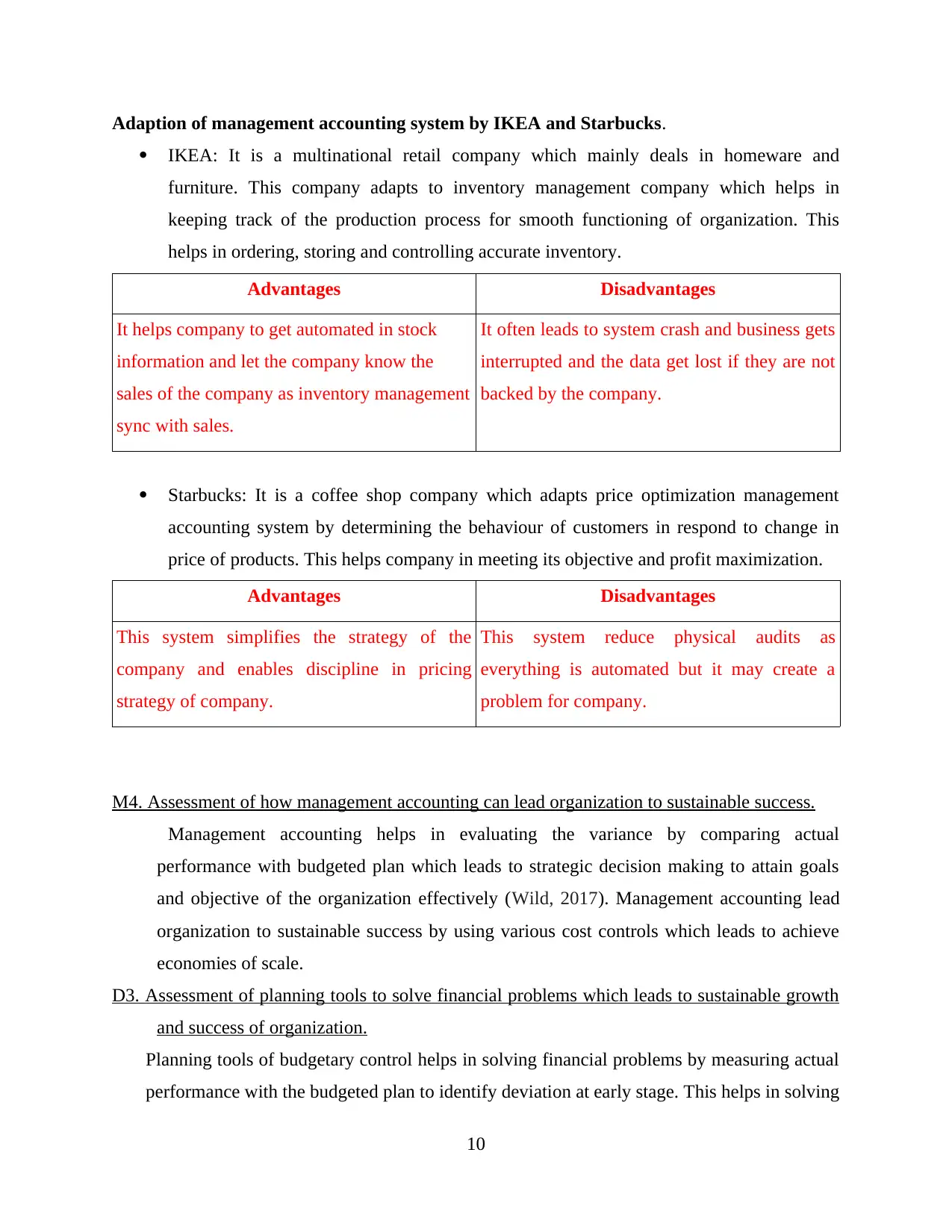

Adaption of management accounting system by IKEA and Starbucks.

IKEA: It is a multinational retail company which mainly deals in homeware and

furniture. This company adapts to inventory management company which helps in

keeping track of the production process for smooth functioning of organization. This

helps in ordering, storing and controlling accurate inventory.

Advantages Disadvantages

It helps company to get automated in stock

information and let the company know the

sales of the company as inventory management

sync with sales.

It often leads to system crash and business gets

interrupted and the data get lost if they are not

backed by the company.

Starbucks: It is a coffee shop company which adapts price optimization management

accounting system by determining the behaviour of customers in respond to change in

price of products. This helps company in meeting its objective and profit maximization.

Advantages Disadvantages

This system simplifies the strategy of the

company and enables discipline in pricing

strategy of company.

This system reduce physical audits as

everything is automated but it may create a

problem for company.

M4. Assessment of how management accounting can lead organization to sustainable success.

Management accounting helps in evaluating the variance by comparing actual

performance with budgeted plan which leads to strategic decision making to attain goals

and objective of the organization effectively (Wild, 2017). Management accounting lead

organization to sustainable success by using various cost controls which leads to achieve

economies of scale.

D3. Assessment of planning tools to solve financial problems which leads to sustainable growth

and success of organization.

Planning tools of budgetary control helps in solving financial problems by measuring actual

performance with the budgeted plan to identify deviation at early stage. This helps in solving

10

IKEA: It is a multinational retail company which mainly deals in homeware and

furniture. This company adapts to inventory management company which helps in

keeping track of the production process for smooth functioning of organization. This

helps in ordering, storing and controlling accurate inventory.

Advantages Disadvantages

It helps company to get automated in stock

information and let the company know the

sales of the company as inventory management

sync with sales.

It often leads to system crash and business gets

interrupted and the data get lost if they are not

backed by the company.

Starbucks: It is a coffee shop company which adapts price optimization management

accounting system by determining the behaviour of customers in respond to change in

price of products. This helps company in meeting its objective and profit maximization.

Advantages Disadvantages

This system simplifies the strategy of the

company and enables discipline in pricing

strategy of company.

This system reduce physical audits as

everything is automated but it may create a

problem for company.

M4. Assessment of how management accounting can lead organization to sustainable success.

Management accounting helps in evaluating the variance by comparing actual

performance with budgeted plan which leads to strategic decision making to attain goals

and objective of the organization effectively (Wild, 2017). Management accounting lead

organization to sustainable success by using various cost controls which leads to achieve

economies of scale.

D3. Assessment of planning tools to solve financial problems which leads to sustainable growth

and success of organization.

Planning tools of budgetary control helps in solving financial problems by measuring actual

performance with the budgeted plan to identify deviation at early stage. This helps in solving

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

problem effectively on a timely manner to attain operational efficiency and productivity.

This helps in efficient utilization of resources to ensure lower spending (de Campos and

Rodrigues, 2016).

CONCLUSION

From the above study it has been summarized that management accounting plays a

critical part in effective decision making by internal management to attain goals of the company

effectively. This study also concludes that there are various planning tools for budgetary control

which helps in finding out deviation on a timely manner and take necessary corrective actions

accordingly.

This study also highlights various management accounting system and performance

metrics to evaluate financial position and operations of the business and critical evaluation of

how they help in solving financial problems of the company.

11

This helps in efficient utilization of resources to ensure lower spending (de Campos and

Rodrigues, 2016).

CONCLUSION

From the above study it has been summarized that management accounting plays a

critical part in effective decision making by internal management to attain goals of the company

effectively. This study also concludes that there are various planning tools for budgetary control

which helps in finding out deviation on a timely manner and take necessary corrective actions

accordingly.

This study also highlights various management accounting system and performance

metrics to evaluate financial position and operations of the business and critical evaluation of

how they help in solving financial problems of the company.

11

REFERENCES

Books and journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

de Campos, C. M. P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global

Encyclopedia of Public Administration, Public Policy, and Governance. pp.1-10.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Miller, G., 2018. Performance based budgeting. Routledge.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Wild, T., 2017. Best practice in inventory management. Routledge.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Online

Advantages and Disadvantages of Incremental Budgeting. 2019. [ONLINE]. Available

through:< https://efinancemanagement.com/budgeting/advantages-and-disadvantages-of-

incremental-budgeting >

Benchmarking. 2018. [ONLINE]. Available through:<

https://www.bain.com/insights/management-tools-benchmarking/>

Historical Evolution of Management Accounting. 2015. [ONLINE]. Available through:<

https://pdfs.semanticscholar.org/9cac/ded8e84907ec54b54d228cd Horngren, C.T.,

Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T., 2002. Management and cost

accounting. Harlow: Financial Times/Prentice Hall.3f863a3546b58.pdf>

What is an Inventory Management System? Definition of Inventory Management Systems,

Benefits, Best Practices & More. 2019. [ONLINE]. Available through:<

https://www.camcode.com/asset-tags/what-is-an-inventory-management-system/>

12

Books and journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

de Campos, C. M. P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global

Encyclopedia of Public Administration, Public Policy, and Governance. pp.1-10.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Miller, G., 2018. Performance based budgeting. Routledge.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Wild, T., 2017. Best practice in inventory management. Routledge.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Online

Advantages and Disadvantages of Incremental Budgeting. 2019. [ONLINE]. Available

through:< https://efinancemanagement.com/budgeting/advantages-and-disadvantages-of-

incremental-budgeting >

Benchmarking. 2018. [ONLINE]. Available through:<

https://www.bain.com/insights/management-tools-benchmarking/>

Historical Evolution of Management Accounting. 2015. [ONLINE]. Available through:<

https://pdfs.semanticscholar.org/9cac/ded8e84907ec54b54d228cd Horngren, C.T.,

Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T., 2002. Management and cost

accounting. Harlow: Financial Times/Prentice Hall.3f863a3546b58.pdf>

What is an Inventory Management System? Definition of Inventory Management Systems,

Benefits, Best Practices & More. 2019. [ONLINE]. Available through:<

https://www.camcode.com/asset-tags/what-is-an-inventory-management-system/>

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.