Management Accounting Report: Costing Methods and Analysis

VerifiedAdded on 2020/10/05

|14

|3853

|251

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its principles and techniques applicable to a business environment. It analyzes the decision-making processes of a manufacturing organization, Swain & Jones, using various accounting techniques such as job costing and inventory management. The report explores the differences between absorption and marginal costing, as well as the advantages and disadvantages of various planning tools used for budgetary control, including zero-based and incremental budgeting. Furthermore, it addresses the adaptability of management accounting systems in responding to financial problems, emphasizing the importance of performance, cost, and budget reports in managerial decision-making. The report also details the key differences between marginal and absorption costing methods. This analysis provides valuable insights into the application of management accounting in real-world business scenarios.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P1 Management Accounting, types and its requirement.............................................................1

P2. Various methods of Management Accounting Report..........................................................3

P3 Calculating cost by using appropriate methods.....................................................................4

P4 Advantages and disadvantages of various planning tools used for budgetary control .........6

P5 Management accounting system for responding financial problems.....................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

P1 Management Accounting, types and its requirement.............................................................1

P2. Various methods of Management Accounting Report..........................................................3

P3 Calculating cost by using appropriate methods.....................................................................4

P4 Advantages and disadvantages of various planning tools used for budgetary control .........6

P5 Management accounting system for responding financial problems.....................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is very necessary for each entity with its various principles and

techniques. The main aim of this report is to highlight fundamentals of management accounting

which can be applicable for business environment and for firms who are operating in certain

environment. It has been applied in all financial data for determining and monitoring the

financial; performance of organization. The present report is about a manufacturing organization

that is Swain & Jones who is operating with 45 employees and there decision making process has

been analysed by using several accounting techniques such as job costing, inventory

management etc. in this report there is brief discussion about income statement according to both

methods, absorption and marginal costing with there key differences. There is explanation about

various planning tools for management accounting with its limitations and merits. In the last part

of this report, adaptability of management accounting systems in context of responding several

financial problems has been addressed.

P1 Management Accounting, types and its requirement

Managerial decisions are undertaken by considering management accounting in very

effective manner (Fullerton, Kennedy and Widener, 2014). All business managers who are

contributing in decision making for short term or even day to day operation are using

management accounting for preparing statistical and financial information. The financial

information is classified, analysed, recorded, identified, delivered and interpreted with

perspective of objectives of an organization that has been termed as Cost Accounting. As they

both sound similar but they have different variations as management accounting assist managers

of organization for decision making and financial accounting gives information for external

parties of entity.

When management accounts reports are prepared, gives very specific, accurate and timely

statistical and financial information which are considered as very important aspect for decision

making of short term and day to day decisions. The management requirements are also

accomplished in these reports.

The information of management accounting is directly used for the purpose of internal

users and it creates a difference from financial accounting systems as it is publicly reported. The

managerial accounting has been applicable which always varies as system is customised for

providing information which is essential for management for decision-making. Management

1

Management accounting is very necessary for each entity with its various principles and

techniques. The main aim of this report is to highlight fundamentals of management accounting

which can be applicable for business environment and for firms who are operating in certain

environment. It has been applied in all financial data for determining and monitoring the

financial; performance of organization. The present report is about a manufacturing organization

that is Swain & Jones who is operating with 45 employees and there decision making process has

been analysed by using several accounting techniques such as job costing, inventory

management etc. in this report there is brief discussion about income statement according to both

methods, absorption and marginal costing with there key differences. There is explanation about

various planning tools for management accounting with its limitations and merits. In the last part

of this report, adaptability of management accounting systems in context of responding several

financial problems has been addressed.

P1 Management Accounting, types and its requirement

Managerial decisions are undertaken by considering management accounting in very

effective manner (Fullerton, Kennedy and Widener, 2014). All business managers who are

contributing in decision making for short term or even day to day operation are using

management accounting for preparing statistical and financial information. The financial

information is classified, analysed, recorded, identified, delivered and interpreted with

perspective of objectives of an organization that has been termed as Cost Accounting. As they

both sound similar but they have different variations as management accounting assist managers

of organization for decision making and financial accounting gives information for external

parties of entity.

When management accounts reports are prepared, gives very specific, accurate and timely

statistical and financial information which are considered as very important aspect for decision

making of short term and day to day decisions. The management requirements are also

accomplished in these reports.

The information of management accounting is directly used for the purpose of internal

users and it creates a difference from financial accounting systems as it is publicly reported. The

managerial accounting has been applicable which always varies as system is customised for

providing information which is essential for management for decision-making. Management

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting has various kinds which are price optimisation, cost accounting system, inventory

management and job costing system. Every kind has their role and functions in management

accounting which is elaborated as follows:

Price Optimisation: It is considered as a basic method for applying different

mathematical analysis of Swain & Jones for identifying customer reaction for different cost of

goods and services via various channels. Generally prices are identified which Swain & Jones

might attain objectives such as rising operating profit. For achieving performance or cost, it can

be discovered by taking alternatives and it will be very effective for constraints, by increasing the

aspects which are desired and vice versa (Messner, 2016).

Cost Accounting System: It is a basic framework which is undertaken by various

corporations for determining product's cost, profitability analysis, and cost control and inventory

valuation. The cost allocation will be according to activity based costing or traditional costing

system. The production cost of different corporation has to be captured is considered as main aim

and along with this input cost has been weighted for every step of production and fixed cost like

capital equipment and depreciation. This system is known as special concept of management

accounting as it provides particular analytical tools like budgetary control, marginal costing,

inventory control and standard costing who are applicable with perspective of management by

replacing their reproducibility in very efficient manner.

Inventory Management: Generally, it has been referred for tracing and recording of

application, ordering and storing component of different production of goods which are sold by

them. The desktop software, barcode printers, barcode scanners and mobile devices are

combined for streamlining inventory system like consumables, goods and stock.

In this system finished goods which ready for sale are also tracked as their main aim is to

signify present level of inventory. In this context they identify stocks for minimising or

maximising for Swain & Jones. Their main role is to constitute purchasing orders, disposing,

relocating, receiving and adjusting the inventory. Sales order, shipping, picking and packaging

has been created by them for production and physical count of inventory is performed here. It

directly reflects in bottom line of company by enhancing accuracy of inventory, workflow of

organization and in same series it is improved.

Job Costing System: The manufacturing cost is allocated here for individual item of

product or some specific batch. Generally it is applicable where goods are processes from one to

2

management and job costing system. Every kind has their role and functions in management

accounting which is elaborated as follows:

Price Optimisation: It is considered as a basic method for applying different

mathematical analysis of Swain & Jones for identifying customer reaction for different cost of

goods and services via various channels. Generally prices are identified which Swain & Jones

might attain objectives such as rising operating profit. For achieving performance or cost, it can

be discovered by taking alternatives and it will be very effective for constraints, by increasing the

aspects which are desired and vice versa (Messner, 2016).

Cost Accounting System: It is a basic framework which is undertaken by various

corporations for determining product's cost, profitability analysis, and cost control and inventory

valuation. The cost allocation will be according to activity based costing or traditional costing

system. The production cost of different corporation has to be captured is considered as main aim

and along with this input cost has been weighted for every step of production and fixed cost like

capital equipment and depreciation. This system is known as special concept of management

accounting as it provides particular analytical tools like budgetary control, marginal costing,

inventory control and standard costing who are applicable with perspective of management by

replacing their reproducibility in very efficient manner.

Inventory Management: Generally, it has been referred for tracing and recording of

application, ordering and storing component of different production of goods which are sold by

them. The desktop software, barcode printers, barcode scanners and mobile devices are

combined for streamlining inventory system like consumables, goods and stock.

In this system finished goods which ready for sale are also tracked as their main aim is to

signify present level of inventory. In this context they identify stocks for minimising or

maximising for Swain & Jones. Their main role is to constitute purchasing orders, disposing,

relocating, receiving and adjusting the inventory. Sales order, shipping, picking and packaging

has been created by them for production and physical count of inventory is performed here. It

directly reflects in bottom line of company by enhancing accuracy of inventory, workflow of

organization and in same series it is improved.

Job Costing System: The manufacturing cost is allocated here for individual item of

product or some specific batch. Generally it is applicable where goods are processes from one to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

another. The information is very essential for submitting price data to individuals who are

involved in contract and even it has been refunded. It is very essential for identifying accuracy

and system of Swain & Jones who is capable for price quoting.

P2. Various methods of Management Accounting Report

Management accounting gives special emphasis on information which is originated

internally via financial accounting. It has been applied very essentially fpr the objective of

controlling, planning and decision making. Managerial accounts are dependent on financial

statements like balance sheet, income statement and statement of cash flow. In this context, these

are not only sourcing for evaluating financial information as it can also be evaluated from

performance report, cost report, budget report and product report (Moshchenko and et. al.,

2018).

Performance Report: This report is formed for the purpose of reviewing performance of

Swain & Jones for every employee or even whole organization report. In many large

organizations that have huge turnover, performance report is generated according to each

department. The strategic decision of future is taken with perspective of these reports. There are

various individuals who are praised because of their commitment and motivation towards

organization and even lay off are because of vice versa situation. Deep insights related to

organization's operations has been given by performance of managerial accounting.

In these reports, accountants usually observe the performance is according to expected

outcome or not and if any variations are there then it should be rectified. In the end of every year,

performance report has been formed but financial information has been quantified for framing

report of performance, it may be quarterly or monthly as well (Quattrone, 2016).

Cost Report: The cost of manufacturing items is calculated in management accounting.

In this report, all raw production overheads, labour, cost and any extra cost is considered for

calculating manufacturing cost and its aggregate is divided into produced goods. All the

information with context of business of Swain & Jones in summarized format in this specific

report. The cost price of particular item while comparing with selling price has provided by

manager. The cost managerial accounting report estimate and monitor the profit margin. All the

expenses are depicting clear picture for optimum utilisation of resources of every department.

Usually they are matched with estimation of revenue so Swain & Jones gives proper evaluation

of profit which will be giving high earning are of business and its special focus will be given on

3

involved in contract and even it has been refunded. It is very essential for identifying accuracy

and system of Swain & Jones who is capable for price quoting.

P2. Various methods of Management Accounting Report

Management accounting gives special emphasis on information which is originated

internally via financial accounting. It has been applied very essentially fpr the objective of

controlling, planning and decision making. Managerial accounts are dependent on financial

statements like balance sheet, income statement and statement of cash flow. In this context, these

are not only sourcing for evaluating financial information as it can also be evaluated from

performance report, cost report, budget report and product report (Moshchenko and et. al.,

2018).

Performance Report: This report is formed for the purpose of reviewing performance of

Swain & Jones for every employee or even whole organization report. In many large

organizations that have huge turnover, performance report is generated according to each

department. The strategic decision of future is taken with perspective of these reports. There are

various individuals who are praised because of their commitment and motivation towards

organization and even lay off are because of vice versa situation. Deep insights related to

organization's operations has been given by performance of managerial accounting.

In these reports, accountants usually observe the performance is according to expected

outcome or not and if any variations are there then it should be rectified. In the end of every year,

performance report has been formed but financial information has been quantified for framing

report of performance, it may be quarterly or monthly as well (Quattrone, 2016).

Cost Report: The cost of manufacturing items is calculated in management accounting.

In this report, all raw production overheads, labour, cost and any extra cost is considered for

calculating manufacturing cost and its aggregate is divided into produced goods. All the

information with context of business of Swain & Jones in summarized format in this specific

report. The cost price of particular item while comparing with selling price has provided by

manager. The cost managerial accounting report estimate and monitor the profit margin. All the

expenses are depicting clear picture for optimum utilisation of resources of every department.

Usually they are matched with estimation of revenue so Swain & Jones gives proper evaluation

of profit which will be giving high earning are of business and its special focus will be given on

3

efforts rather than wasting resources and time who are giving less profit margin. The income

limit has been also planned and managed via cost reports.

Budget Report: The most fundamental report in managerial accounting has been

considered as budget report. It has been drawn by every organization whether it is small or big as

it provides appropriate understanding of schemes which are very popular in context of business.

Generally budgets are prepared by taking base as previous year budget and it has been adjusted

for future forecast on context of circumstances which might arise. The budget of Swain & Jones

provides all sources of expenses and revenue. For attaining goal in budgeted amount, all efforts

are put by Swain & Jones. For staying in budget manager always finds new vendor for

purchasing raw material in less price and they also keep record of sales and expenses which are

increased or decreased. These reports helps in providing employee incentives, cutting cost and

negotiation for raw material. To every industry and business budget report is explanatory (Smith,

2017).

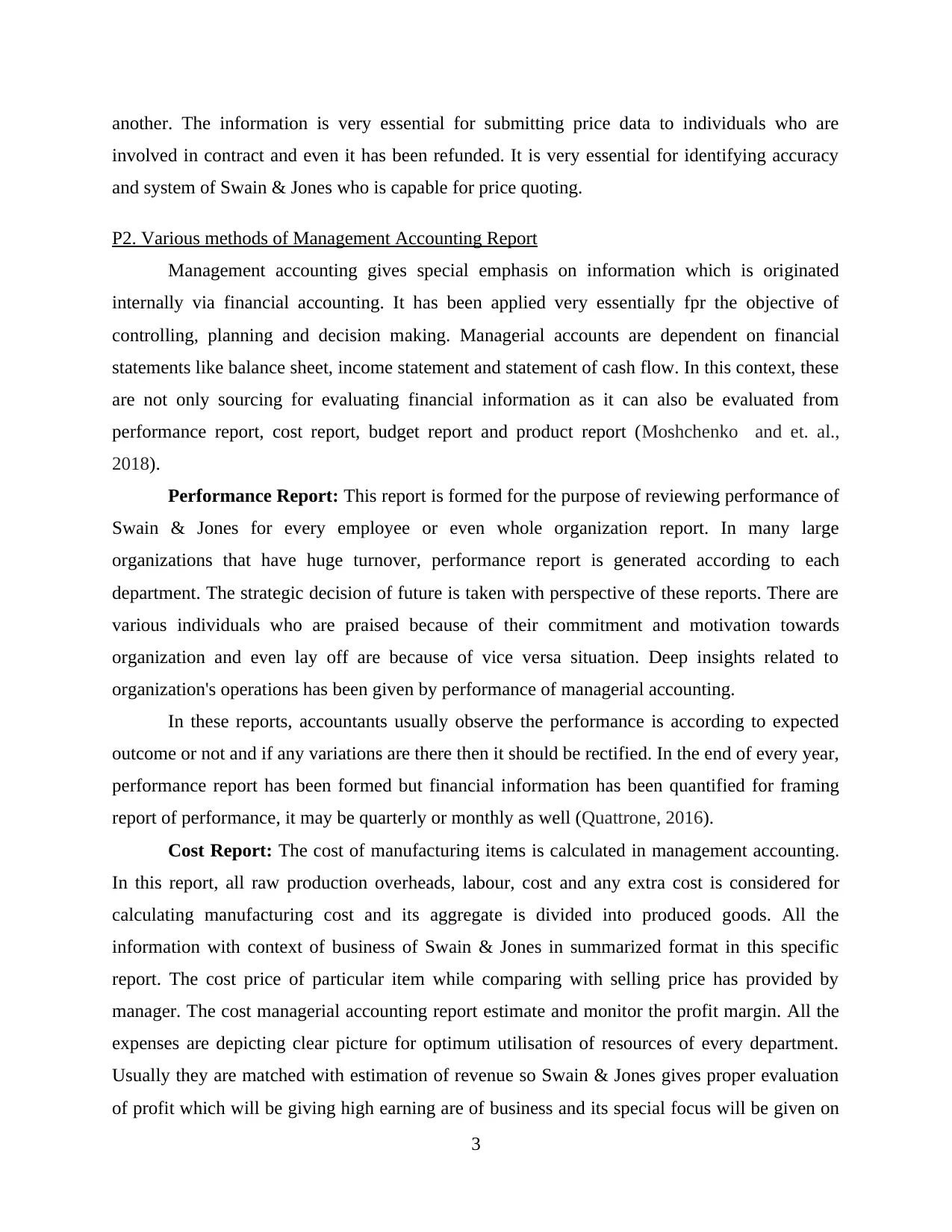

P3 Calculating cost by using appropriate methods

Marginal costing

4

limit has been also planned and managed via cost reports.

Budget Report: The most fundamental report in managerial accounting has been

considered as budget report. It has been drawn by every organization whether it is small or big as

it provides appropriate understanding of schemes which are very popular in context of business.

Generally budgets are prepared by taking base as previous year budget and it has been adjusted

for future forecast on context of circumstances which might arise. The budget of Swain & Jones

provides all sources of expenses and revenue. For attaining goal in budgeted amount, all efforts

are put by Swain & Jones. For staying in budget manager always finds new vendor for

purchasing raw material in less price and they also keep record of sales and expenses which are

increased or decreased. These reports helps in providing employee incentives, cutting cost and

negotiation for raw material. To every industry and business budget report is explanatory (Smith,

2017).

P3 Calculating cost by using appropriate methods

Marginal costing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

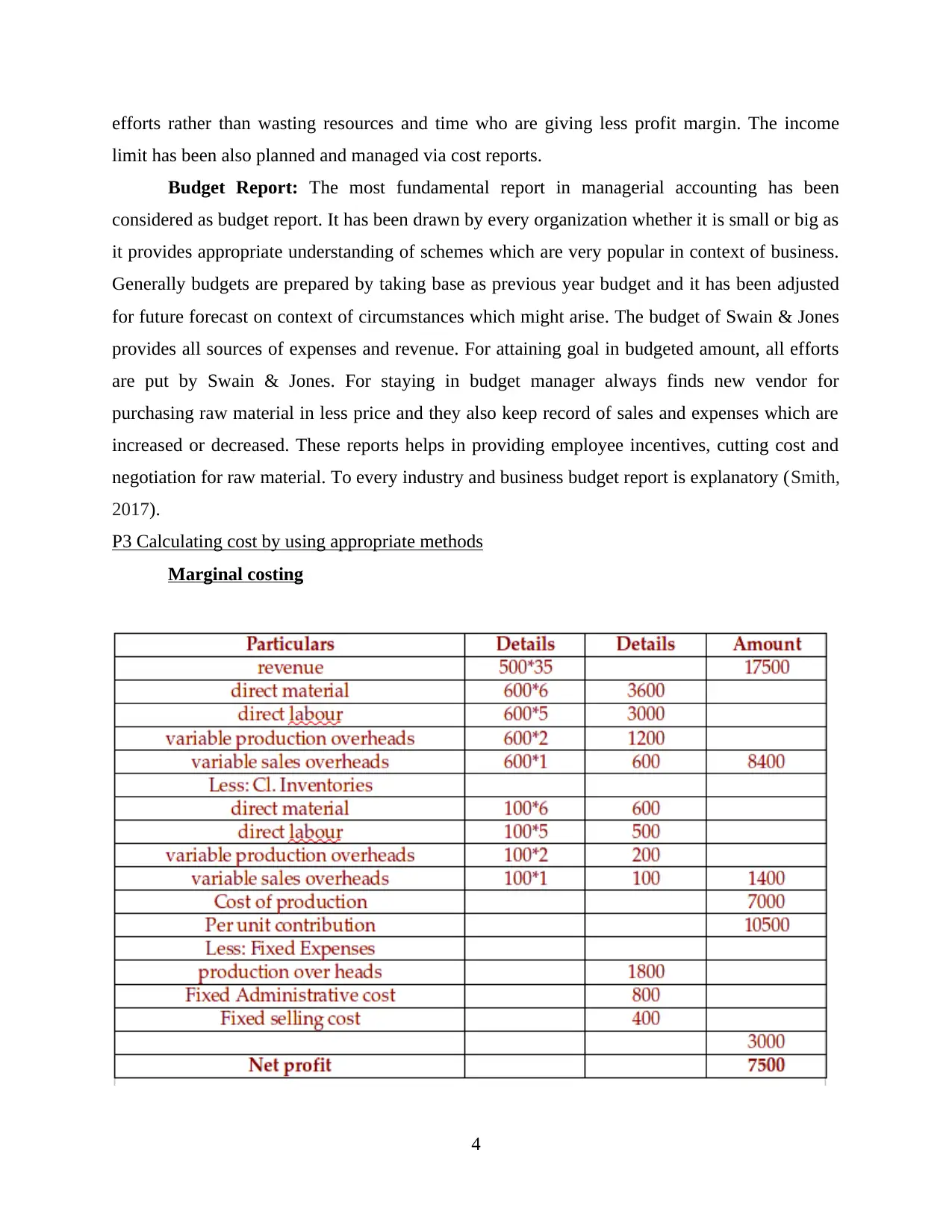

Absorption costing

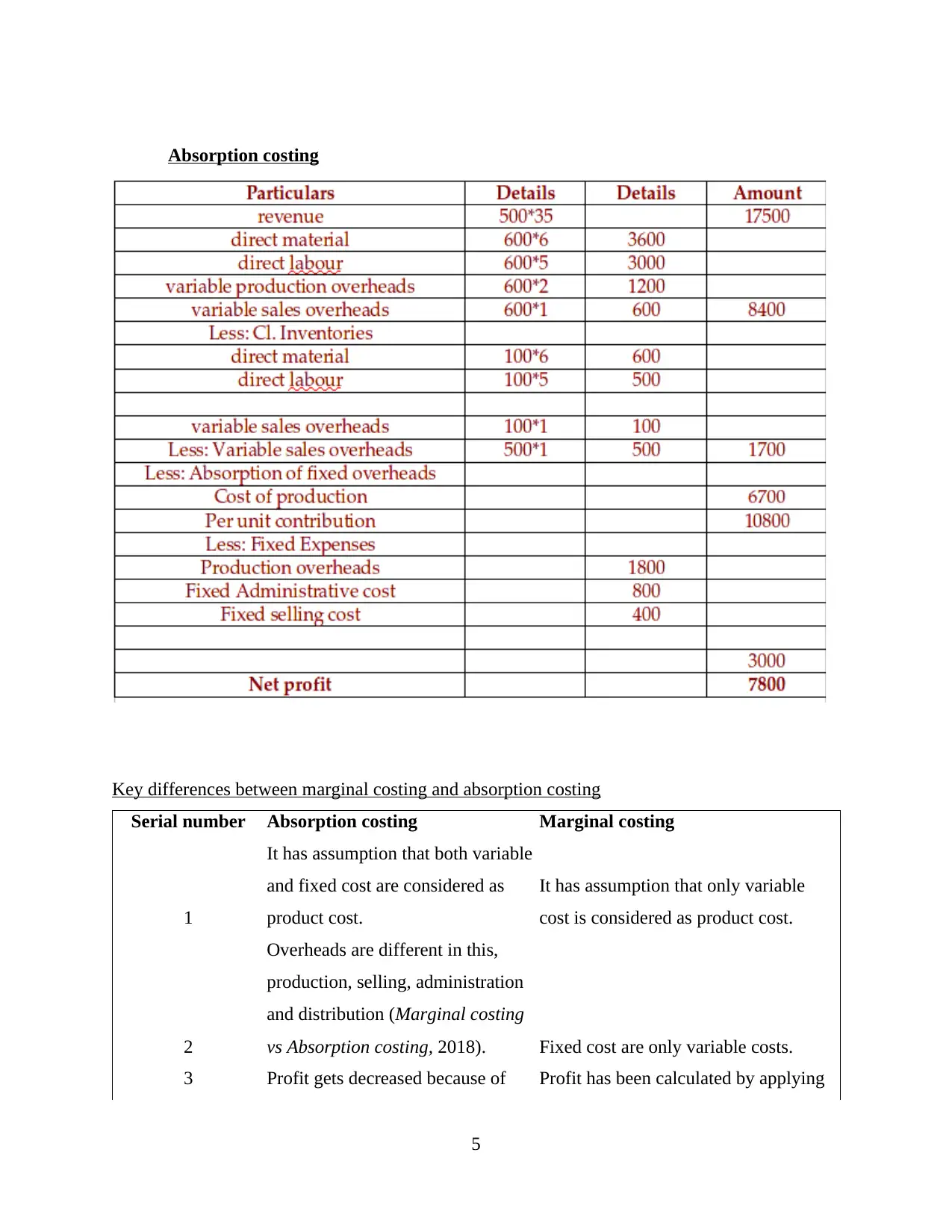

Key differences between marginal costing and absorption costing

Serial number Absorption costing Marginal costing

1

It has assumption that both variable

and fixed cost are considered as

product cost.

It has assumption that only variable

cost is considered as product cost.

2

Overheads are different in this,

production, selling, administration

and distribution (Marginal costing

vs Absorption costing, 2018). Fixed cost are only variable costs.

3 Profit gets decreased because of Profit has been calculated by applying

5

Key differences between marginal costing and absorption costing

Serial number Absorption costing Marginal costing

1

It has assumption that both variable

and fixed cost are considered as

product cost.

It has assumption that only variable

cost is considered as product cost.

2

Overheads are different in this,

production, selling, administration

and distribution (Marginal costing

vs Absorption costing, 2018). Fixed cost are only variable costs.

3 Profit gets decreased because of Profit has been calculated by applying

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considering fixed cost. profit volume ratio.

4 It identifies cost of every unit. It determines cost of next unit.

5

Opening and closing stock impacts

cost per unit.

Opening and closing stock does not

affect cost per unit.

6

Net profit per unit is considered as

most important aspect.

Contribution per unit is considered as

most important aspect.

7

Its main objective is to give

accurate and fair treatment to

product cost.

Its main objective is to give special

emphasis of contribution is product

cost.

8

It is replicated in very conventional

aspect for financial and tax

reporting.

It is replicated by outlining the sum of

contribution.

P4 Advantages and disadvantages of various planning tools used for budgetary control

For budgetary control there are different planning tools which are as follows :

Zero based budgeting

Incremental budgeting

Activity based budgeting

Zero based budgeting : In this planning tool, budget has been prepared by considering

zero as base. There is re-evaluation of every line of statement of cash flow and it has been

justified by every expenditure that has been incurred by each department of entity.

Advantages

The arbitrary alterations with respect to budget of previous year is directly involved in

this method and it will tend to re look all items of cash flow extracting operating cost. It

will be a major contribution for cutting cost and reflecting clear picture of cost which will

be against the performance (Lavia López and Hiebl, 2014).

Historical number are ignored, only actual numbers are evaluated in budgeting technique

and it will help in allocating resources in very efficient manner.

Activities which are unproductive and redundant are substituted and it determines

different opportunities in cost effective manner.

Disadvantages

6

4 It identifies cost of every unit. It determines cost of next unit.

5

Opening and closing stock impacts

cost per unit.

Opening and closing stock does not

affect cost per unit.

6

Net profit per unit is considered as

most important aspect.

Contribution per unit is considered as

most important aspect.

7

Its main objective is to give

accurate and fair treatment to

product cost.

Its main objective is to give special

emphasis of contribution is product

cost.

8

It is replicated in very conventional

aspect for financial and tax

reporting.

It is replicated by outlining the sum of

contribution.

P4 Advantages and disadvantages of various planning tools used for budgetary control

For budgetary control there are different planning tools which are as follows :

Zero based budgeting

Incremental budgeting

Activity based budgeting

Zero based budgeting : In this planning tool, budget has been prepared by considering

zero as base. There is re-evaluation of every line of statement of cash flow and it has been

justified by every expenditure that has been incurred by each department of entity.

Advantages

The arbitrary alterations with respect to budget of previous year is directly involved in

this method and it will tend to re look all items of cash flow extracting operating cost. It

will be a major contribution for cutting cost and reflecting clear picture of cost which will

be against the performance (Lavia López and Hiebl, 2014).

Historical number are ignored, only actual numbers are evaluated in budgeting technique

and it will help in allocating resources in very efficient manner.

Activities which are unproductive and redundant are substituted and it determines

different opportunities in cost effective manner.

Disadvantages

6

There is very huge requirement of man power.

It consumes too much time or it has been elaborated as very time consuming method.

It shows deficiency in expertise.

Incremental budgeting : It is considered as most important part of management

accounting which usually signifies minor change from budget of previous year to new year

budget. The fiscal year has been elaborated as base of next year for budgetary allocation. The

main assumption has been undertaken in this method that all previous year expenses will be

continuing in next year and additional amount will be added as well.

Advantages

Implementation is very easy as it has absence of complexity in different calculations

which are obtained by various departments if there is lack of any problem due to detailed

analysis is not required.

There is not requirement of justification of funding as it has ensured about continuation

of funding for every department.

This method easily determines variations and impact.

This method eliminates rivalry as it is most popular method among various organizations

and it creates value of equality in every department because everyone gets similar

increment over past year (Gooneratne and Hoque, 2016).

Disadvantages

It affects net income as it encourages spending and it will be aggregated in expenses as

this budget will be maintained in coming year.

Its main assumption is that year requirement will be marginally different from past year

but in reality there are various alterations in context of economy or industry as well

which might reflect in budget.

It will be creating lack of creativity, innovation and absence of incentives for cutting cost

to certain managers.

It will be creating budgetary slack, as it is expensive method because of ease availability.

Activity based budgeting : Generally it considers cost of overhead in preparing budgets.

It totally ignores budget of past year for framing budget of current year. In the context of

outcome, allocation of resources are according to activity. It is known as activity oriented budget

not a function oriented budget.

7

It consumes too much time or it has been elaborated as very time consuming method.

It shows deficiency in expertise.

Incremental budgeting : It is considered as most important part of management

accounting which usually signifies minor change from budget of previous year to new year

budget. The fiscal year has been elaborated as base of next year for budgetary allocation. The

main assumption has been undertaken in this method that all previous year expenses will be

continuing in next year and additional amount will be added as well.

Advantages

Implementation is very easy as it has absence of complexity in different calculations

which are obtained by various departments if there is lack of any problem due to detailed

analysis is not required.

There is not requirement of justification of funding as it has ensured about continuation

of funding for every department.

This method easily determines variations and impact.

This method eliminates rivalry as it is most popular method among various organizations

and it creates value of equality in every department because everyone gets similar

increment over past year (Gooneratne and Hoque, 2016).

Disadvantages

It affects net income as it encourages spending and it will be aggregated in expenses as

this budget will be maintained in coming year.

Its main assumption is that year requirement will be marginally different from past year

but in reality there are various alterations in context of economy or industry as well

which might reflect in budget.

It will be creating lack of creativity, innovation and absence of incentives for cutting cost

to certain managers.

It will be creating budgetary slack, as it is expensive method because of ease availability.

Activity based budgeting : Generally it considers cost of overhead in preparing budgets.

It totally ignores budget of past year for framing budget of current year. In the context of

outcome, allocation of resources are according to activity. It is known as activity oriented budget

not a function oriented budget.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages

In this method every cost driver is evaluated along with every step which is considered

and it eliminates all irrelevant activities.

While eliminating irrelevant activities it reduces cost and with its outcome production of

goods and services are performing at its best as compared to competitors.

It will be treating whole business as single unit as it cannot be in department aspect.

Relationship has been improved in this technique in every department and customer as

well.

Disadvantage

All the functional areas must be understood of business, if there will be lack in

understanding of manager then it will directly reflect negative in budget and various

discrepancies.

It is replicated as very complex process as in this method different factor has to be

researched and analysed properly because of accurate estimation of demand according to

different activities (Cools, Stouthuysen and Van den Abbeele, 2017).

It consumes so many resources, all the top officials get best training and proper numeric

analysis. It is also a time consuming method. If there is presence of optimum utilisation

of resources in operational activities then it will be giving best returns.

It gives special consideration to short term goals as it usually ignores goals in context of

long term.

P5 Management accounting system for responding financial problems.

Concepts Swain & Jones Ford

Benchmarking: Usually it

compares the performance

standards by business practices

of organization to other firms

who are of same industry.

It has performed proper

financial analysis and

compared the outcome for

identifying overall efficiency,

productivity and

competitiveness of their own.

They have measured common

value with respect to time and

cost. The strategic

In the case of Ford, they have

measure there common value

by quality in their own auto

mobile industry. For running

there business in very efficient

manner, they have identified

various requirements for

improvements which will be

an end from learnings with

8

In this method every cost driver is evaluated along with every step which is considered

and it eliminates all irrelevant activities.

While eliminating irrelevant activities it reduces cost and with its outcome production of

goods and services are performing at its best as compared to competitors.

It will be treating whole business as single unit as it cannot be in department aspect.

Relationship has been improved in this technique in every department and customer as

well.

Disadvantage

All the functional areas must be understood of business, if there will be lack in

understanding of manager then it will directly reflect negative in budget and various

discrepancies.

It is replicated as very complex process as in this method different factor has to be

researched and analysed properly because of accurate estimation of demand according to

different activities (Cools, Stouthuysen and Van den Abbeele, 2017).

It consumes so many resources, all the top officials get best training and proper numeric

analysis. It is also a time consuming method. If there is presence of optimum utilisation

of resources in operational activities then it will be giving best returns.

It gives special consideration to short term goals as it usually ignores goals in context of

long term.

P5 Management accounting system for responding financial problems.

Concepts Swain & Jones Ford

Benchmarking: Usually it

compares the performance

standards by business practices

of organization to other firms

who are of same industry.

It has performed proper

financial analysis and

compared the outcome for

identifying overall efficiency,

productivity and

competitiveness of their own.

They have measured common

value with respect to time and

cost. The strategic

In the case of Ford, they have

measure there common value

by quality in their own auto

mobile industry. For running

there business in very efficient

manner, they have identified

various requirements for

improvements which will be

an end from learnings with

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management has applied this

method and created high

turnover of there industry.

outcome of benchmarking.

The strategic management has

applied this method and it

created efficiency in increasing

sales and revenue as well.

Key performance indicator :

It elaborates the success of

organisation or progress in

perspective of specific

objective. There are two types

of KPI which are Financial

KPIs and non financial KPI

(Ax and Greve, 2017).

By tracking progress of

attaining strategic objective is

delivered in strategic map. It is

indicated in reporting

scorecard and dashboard and

provides top management and

other stakeholders for focusing

on success of organisation.

Financial KPI is on basis of

balance sheet or profit and loss

statement which is justifying

in this organisation with

alterations of sales growth or

expenses category. In this

organisation both KPIs are

combined and they achieved

great success in context of

long term.

In this organization, non

financial KPIs are indicating

for assessment of activities

which gives significance in

attaining strategic objectives.

In this strategic execution is

improved by aligning activities

of Ford and individual actions

along with strategic objectives.

KPI are framed very well in

this organization so it leads to

medium for management and

board has monitored along

with core activities rather than

simply measure of financial

success of different outcome.

In this combination of both

KPI had improved quality of

service, efficiency and they

achieved long term success in

terms of financial

performance.

Variance analysis : It

elaborates the differences

between planned numbers and

In this context, company has

assessed its favour-ability by

comparing its actual cost and

The organization has

performed variance analysis

and it determined by standard

9

method and created high

turnover of there industry.

outcome of benchmarking.

The strategic management has

applied this method and it

created efficiency in increasing

sales and revenue as well.

Key performance indicator :

It elaborates the success of

organisation or progress in

perspective of specific

objective. There are two types

of KPI which are Financial

KPIs and non financial KPI

(Ax and Greve, 2017).

By tracking progress of

attaining strategic objective is

delivered in strategic map. It is

indicated in reporting

scorecard and dashboard and

provides top management and

other stakeholders for focusing

on success of organisation.

Financial KPI is on basis of

balance sheet or profit and loss

statement which is justifying

in this organisation with

alterations of sales growth or

expenses category. In this

organisation both KPIs are

combined and they achieved

great success in context of

long term.

In this organization, non

financial KPIs are indicating

for assessment of activities

which gives significance in

attaining strategic objectives.

In this strategic execution is

improved by aligning activities

of Ford and individual actions

along with strategic objectives.

KPI are framed very well in

this organization so it leads to

medium for management and

board has monitored along

with core activities rather than

simply measure of financial

success of different outcome.

In this combination of both

KPI had improved quality of

service, efficiency and they

achieved long term success in

terms of financial

performance.

Variance analysis : It

elaborates the differences

between planned numbers and

In this context, company has

assessed its favour-ability by

comparing its actual cost and

The organization has

performed variance analysis

and it determined by standard

9

actual performance (Fisher and

Krumwiede, 2015). The

strategic management work on

deviations and tries to improve

there performance. The sum of

aggregate of different variance

provides overall picture of

performance of organization.

standard cost. The deviations

were giving very negative

aspect so it improved its

quantity and cost of material as

well. They managed there raw

material at right point which

tends to improve there

financial performance of

coming year and it leads to

bring more efficient operation

in business. Along with this,

organization has created more

revenue and sales by variance

analysis (Ekwue, 2014).

and actual cost that there is

issue in labour and variable

overhead and it is directly

reported to management. It

created deep understanding of

reason of fluctuations and

ways for reducing variance. By

cutting cost of these specified

overhead had created

efficiency in management by

its specific justification. The

managers of Ford were able to

justify performance is good or

not in specific duration.

CONCLUSION

From the above report it has been concluded that management accounting is very

important concept in this present era. It has essential role in each and every organization whether

it is of any industry such as hospitality, retail, manufacturing etc. The financial performance of

Swain & Jones has been elaborated in this report which depicts that management accounting

gives information in very reliable and accurate manner. It has been cleared that practically

accounting must be very easy to understand as it has disciples all details of transaction ion

context of finance and organization. The above report has shown importance of profit and loss

statement according to marginal costing and absorption costing, as more net income is justified

by absorption costing method because of various overheads. Further it has been summed up by

different concept of budgeting such as zero based, activity based and incremental based

budgeting with there merits and demerits. It had clearly that, weakness of increment budgeting

has been overcome by zero based budgeting. Last but not least, benchmarking, key performance

indicator and variance analysis are best possible way for tackling problems.

10

Krumwiede, 2015). The

strategic management work on

deviations and tries to improve

there performance. The sum of

aggregate of different variance

provides overall picture of

performance of organization.

standard cost. The deviations

were giving very negative

aspect so it improved its

quantity and cost of material as

well. They managed there raw

material at right point which

tends to improve there

financial performance of

coming year and it leads to

bring more efficient operation

in business. Along with this,

organization has created more

revenue and sales by variance

analysis (Ekwue, 2014).

and actual cost that there is

issue in labour and variable

overhead and it is directly

reported to management. It

created deep understanding of

reason of fluctuations and

ways for reducing variance. By

cutting cost of these specified

overhead had created

efficiency in management by

its specific justification. The

managers of Ford were able to

justify performance is good or

not in specific duration.

CONCLUSION

From the above report it has been concluded that management accounting is very

important concept in this present era. It has essential role in each and every organization whether

it is of any industry such as hospitality, retail, manufacturing etc. The financial performance of

Swain & Jones has been elaborated in this report which depicts that management accounting

gives information in very reliable and accurate manner. It has been cleared that practically

accounting must be very easy to understand as it has disciples all details of transaction ion

context of finance and organization. The above report has shown importance of profit and loss

statement according to marginal costing and absorption costing, as more net income is justified

by absorption costing method because of various overheads. Further it has been summed up by

different concept of budgeting such as zero based, activity based and incremental based

budgeting with there merits and demerits. It had clearly that, weakness of increment budgeting

has been overcome by zero based budgeting. Last but not least, benchmarking, key performance

indicator and variance analysis are best possible way for tackling problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.