Management Accounting System Report: 4Comp PLC Analysis

VerifiedAdded on 2020/07/23

|17

|4974

|214

Report

AI Summary

This report, prepared by a Management Accounting Officer, analyzes the management accounting system at 4Comp PLC. It begins with an introduction to management accounting (MA) and its essential requirements, emphasizing its role in providing crucial financial and non-financial information for effective decision-making. The report then delves into various MA reporting methods, including job cost reporting, operational budget reports, inventory management reports, and performance reports. The core of the report focuses on costing techniques, computing net income using different methods, and evaluating the merits of these techniques within the context of 4Comp PLC. It further explores budgetary control processes, discussing the merits and demerits of planning tools and their effective use in reducing financial issues. Finally, the report addresses the resolution of financial issues through the application of MA principles, offering an evaluation of potential financial challenges and concluding with recommendations for improved financial management at 4Comp PLC. The report highlights the importance of MA in planning, controlling costs, and improving profitability within a business organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

4Comp PLC COMPANY................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its essential requirement....................................................1

P2: Methods used for management accounting reporting......................................................3

M1: Merits of MA and its applications..................................................................................5

D1: Critically evaluate management reporting system..........................................................5

TASK 2............................................................................................................................................5

P3: Computation of net income by using various costing techniques....................................5

M2: Different management accounting methods...................................................................8

D2: Analysis of income statements........................................................................................8

TASK 3............................................................................................................................................9

P4: Merits and demerits of planning tools used for budgetary control process.....................9

M3: Critically evaluation of planning tools..........................................................................10

D3: Effective use of tools to reduce financial issues. ..........................................................11

TASK 4..........................................................................................................................................11

P5: To resolve financial issues with the use of MA.............................................................11

M4: Evaluation of financial issues.......................................................................................13

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

4Comp PLC COMPANY................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its essential requirement....................................................1

P2: Methods used for management accounting reporting......................................................3

M1: Merits of MA and its applications..................................................................................5

D1: Critically evaluate management reporting system..........................................................5

TASK 2............................................................................................................................................5

P3: Computation of net income by using various costing techniques....................................5

M2: Different management accounting methods...................................................................8

D2: Analysis of income statements........................................................................................8

TASK 3............................................................................................................................................9

P4: Merits and demerits of planning tools used for budgetary control process.....................9

M3: Critically evaluation of planning tools..........................................................................10

D3: Effective use of tools to reduce financial issues. ..........................................................11

TASK 4..........................................................................................................................................11

P5: To resolve financial issues with the use of MA.............................................................11

M4: Evaluation of financial issues.......................................................................................13

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

4Comp PLC COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting information are an important aspect of any business organisation

in order to manage their daily financial transactions. A financial manager is held responsible for

managing different organisational activities as well as capital in effectively. In order to do so they

prepare various reports by using accounting systems. “4Com” company uses a variety of

accounting tools and techniques to control and maintain their operations. As, an accounting

officer I have been required to make a report which can provide necessary requirements of using

accounting systems in an organisation.

The project research carries analysis of different costing methods which can help them to

determine positive and negative results. This will help to make valuable decision in order to get

future profitability (Routledge, 2014). This project explains how 4com company is using

budgeting process in accordance to manage their cash-flows and other operating expenses in

order to manager their financial statements. In that context, different methods of budget and its

merits and demerits are discussed under this particular report. The purpose of this project is to

analyse performance evaluation by comparing financial issues with the other company.

TASK 1

P1: Management accounting and its essential requirement

MA is a technique that belong to integration of financial and non-financial statements to

present valuable information to the top management. It is responsible for taking an effective

decision for the betterment of an organisation. MA plays a crucial role in delivering necessary

information to the people of organisation. They nature and scope of accounting is wide because it

consists of different types of accounting data related to the 4com company. It will be lead to

positive decision making if the data provided to the authority is more relevant and accurate. In

1

TO,

GENERAL MANAGER

4Comp PLC COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting information are an important aspect of any business organisation

in order to manage their daily financial transactions. A financial manager is held responsible for

managing different organisational activities as well as capital in effectively. In order to do so they

prepare various reports by using accounting systems. “4Com” company uses a variety of

accounting tools and techniques to control and maintain their operations. As, an accounting

officer I have been required to make a report which can provide necessary requirements of using

accounting systems in an organisation.

The project research carries analysis of different costing methods which can help them to

determine positive and negative results. This will help to make valuable decision in order to get

future profitability (Routledge, 2014). This project explains how 4com company is using

budgeting process in accordance to manage their cash-flows and other operating expenses in

order to manager their financial statements. In that context, different methods of budget and its

merits and demerits are discussed under this particular report. The purpose of this project is to

analyse performance evaluation by comparing financial issues with the other company.

TASK 1

P1: Management accounting and its essential requirement

MA is a technique that belong to integration of financial and non-financial statements to

present valuable information to the top management. It is responsible for taking an effective

decision for the betterment of an organisation. MA plays a crucial role in delivering necessary

information to the people of organisation. They nature and scope of accounting is wide because it

consists of different types of accounting data related to the 4com company. It will be lead to

positive decision making if the data provided to the authority is more relevant and accurate. In

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the other words, all the data that are related to the administration can affect the decision making

if the information is not according to the set standard (Ward, 2012). The management accountant

must consider the belongings of shareholders and also, they are accountable for guiding the

company in right direction.

All are done in order to increase the profit and performance of 4com in coming year. The

main purpose of using accounting system is to make proper utilisation of resources which are

used by the company during the year. It will be more effective to determine the total cost

incurred by company in producing a product and services. The MA will be essential aspects in

planning process as it provides right ways to invest in new venture. However, management

always tries to get more profit from its limited resource by using appropriate techniques. In this

process, they incur heavy funds in achieving their target that will be controlled and managed

with the use of different accounting systems. MA help to control costs and losses which are

incurred during production process in 4com plc (Gates, Jean-Louis Nicolas and Paul Walker,

2012). As an account officer, it is my important role to use right accounting system to manager

company financial transactions. 4Com plc is a small business organisation which is associated

with production of electronic products so they need a perfect system to record their daily

transactions. Some of the accounting system which can be used by 4com company are as

follows:

Inventory management system: It is said am automatically controlled inventory system

that is used in order to manage, locate and control objects and material. The main objective of

this accounting system is to track stock levels, order summary, sales report and delivery timing.

It is mostly related with those company which deal in large-scale production of units, 4com is

one of them.

Cost accounting system: It is simply related with the process of collecting, recording,

analysing and evaluating different alternative course of action. The main role of this system is to

provide managers necessary information that are based on cost efficiency and performance

capabilities. In order to determine the cost of a product there are several costs which are used

such as normal, standard and actual costing.

Price optimisation system: It is considered as numerical analysis by an organisation to

estimate how customers will react to various prices for its goods and services through other

2

if the information is not according to the set standard (Ward, 2012). The management accountant

must consider the belongings of shareholders and also, they are accountable for guiding the

company in right direction.

All are done in order to increase the profit and performance of 4com in coming year. The

main purpose of using accounting system is to make proper utilisation of resources which are

used by the company during the year. It will be more effective to determine the total cost

incurred by company in producing a product and services. The MA will be essential aspects in

planning process as it provides right ways to invest in new venture. However, management

always tries to get more profit from its limited resource by using appropriate techniques. In this

process, they incur heavy funds in achieving their target that will be controlled and managed

with the use of different accounting systems. MA help to control costs and losses which are

incurred during production process in 4com plc (Gates, Jean-Louis Nicolas and Paul Walker,

2012). As an account officer, it is my important role to use right accounting system to manager

company financial transactions. 4Com plc is a small business organisation which is associated

with production of electronic products so they need a perfect system to record their daily

transactions. Some of the accounting system which can be used by 4com company are as

follows:

Inventory management system: It is said am automatically controlled inventory system

that is used in order to manage, locate and control objects and material. The main objective of

this accounting system is to track stock levels, order summary, sales report and delivery timing.

It is mostly related with those company which deal in large-scale production of units, 4com is

one of them.

Cost accounting system: It is simply related with the process of collecting, recording,

analysing and evaluating different alternative course of action. The main role of this system is to

provide managers necessary information that are based on cost efficiency and performance

capabilities. In order to determine the cost of a product there are several costs which are used

such as normal, standard and actual costing.

Price optimisation system: It is considered as numerical analysis by an organisation to

estimate how customers will react to various prices for its goods and services through other

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

modes. The major objective of 4com company is to determine the price that will meet its aims

such as to increase operating profit during the year.

Job costing system: It is related with that process through which identification of

assigning cost that are incurred on a particular job in which an individual as well as company is

associated with. The job costing system is mainly used where the products produced are

relatively different from each other.

Batch costing system: It is very much similar to job costing in which a lot size of

product is taken into consideration. This is an easy way to identify a product with its number. All

product related information such manufacturing date, time and year are mentioned in it.

Essential of MA is a dynamic techniques that is focused on effective business accounting

policies which are used by the company. It consists of preparation of planning, strategies,

necessary measurement and effective control measures for performance management.

P2: Methods used for management accounting reporting

In an organisation, it is important to have an appropriate accounting system which can

help the company to record its financial transactions (Merchant, 2012). It will be more helpful

for future decision making by taking the information from the available record entries. MA is an

essential part of any business organisation that integrate all departments working for the

common motive. They are mostly associated with internal and external environment that are

affecting the business of an organisation. It concerns with information which is based on cultural

issues and other social factors. In short, data that is related to 4com plc and can impact the

accounting decision making are recorded into MA.

Reporting: It refers as those statement and records which are prepares by the account

department by taking help of events, situation and other investment activities which are

necessary for the growth of the business. In other words, the procedures of delivering

information to the management is said to be reporting. It can help to guide other expertise those

are having necessaries skills and ability to formulated good financial report on the basis of

current and past year position. It is all done in order to get an ideas for future investment that are

made by stakeholders. It assists management to prepare a perfect plan which can help the

company to reach its set goals.

Reporting help the company by providing valuable information to other stages of

organisation level. Whether they are lacking behind with necessary resources and support in the

3

such as to increase operating profit during the year.

Job costing system: It is related with that process through which identification of

assigning cost that are incurred on a particular job in which an individual as well as company is

associated with. The job costing system is mainly used where the products produced are

relatively different from each other.

Batch costing system: It is very much similar to job costing in which a lot size of

product is taken into consideration. This is an easy way to identify a product with its number. All

product related information such manufacturing date, time and year are mentioned in it.

Essential of MA is a dynamic techniques that is focused on effective business accounting

policies which are used by the company. It consists of preparation of planning, strategies,

necessary measurement and effective control measures for performance management.

P2: Methods used for management accounting reporting

In an organisation, it is important to have an appropriate accounting system which can

help the company to record its financial transactions (Merchant, 2012). It will be more helpful

for future decision making by taking the information from the available record entries. MA is an

essential part of any business organisation that integrate all departments working for the

common motive. They are mostly associated with internal and external environment that are

affecting the business of an organisation. It concerns with information which is based on cultural

issues and other social factors. In short, data that is related to 4com plc and can impact the

accounting decision making are recorded into MA.

Reporting: It refers as those statement and records which are prepares by the account

department by taking help of events, situation and other investment activities which are

necessary for the growth of the business. In other words, the procedures of delivering

information to the management is said to be reporting. It can help to guide other expertise those

are having necessaries skills and ability to formulated good financial report on the basis of

current and past year position. It is all done in order to get an ideas for future investment that are

made by stakeholders. It assists management to prepare a perfect plan which can help the

company to reach its set goals.

Reporting help the company by providing valuable information to other stages of

organisation level. Whether they are lacking behind with necessary resources and support in the

3

ways of achieving their objectives (Bodie, 2013). There are so many statements which are

helpful to the managers in making analysis of company's position. Company effectiveness can

be determine by using proper skills in analysing performances and stability position. Income

statements and balance sheet are the two important statements of the company through which its

identity and growth are determined. During production process it is used an important tool by

which a manager can analyse total cost incurred on producing one unit of product. There are

various reporting system which can be used by 4com plc in their business organisation to

manager there accounting data. In the ways of determining the major reaction or changes in

financial statements of company. Some of the reporting system which are more helpful for 4com

plc in managing their business operations are:

Job cost reporting: It is related with those costs which is incurred by 4com plc in

production of product in a financial year. These are basically associated with as assumption of

revenue generated during the year (Parker, 2011). On the other hand, each job activities are

incurring how much of the profit to the company are analyse by this reporting system. It will also

evaluate those areas which are earning maximum profit with minimum efforts.

Operational budget report: This particular budget reports generate information

regarding the expenses which are incur by 4com plc during production process. It is considered

as one of the major reporting system which help the managers to get complete details of actual

cost beard by company. It included various sub parts such as sale budget, variable budgets and

many more. It can be prepared during month, half yearly or on annual basis.

Inventory management report: This report generally focuses on stock management and

its control. All those physical stock that are used by 4com as managerial reporting to determine

various level of stock availability (Burritt, Schaltegger and Zvezdov, 2011). It includes various

steps which are required to be followed by managers in order to protect and record stock details

in the books of account. There are various tools such as EOQ and ABC costing that can be used

to analyse the results.

Performance report: Accounting can be more effectively use by finance departments to

judge performance of the company. It would be done by taking data of current and past year.

Different information which are related with the employees, team, company goodwill and other

outside competitors are analysed with the help of this report.

4

helpful to the managers in making analysis of company's position. Company effectiveness can

be determine by using proper skills in analysing performances and stability position. Income

statements and balance sheet are the two important statements of the company through which its

identity and growth are determined. During production process it is used an important tool by

which a manager can analyse total cost incurred on producing one unit of product. There are

various reporting system which can be used by 4com plc in their business organisation to

manager there accounting data. In the ways of determining the major reaction or changes in

financial statements of company. Some of the reporting system which are more helpful for 4com

plc in managing their business operations are:

Job cost reporting: It is related with those costs which is incurred by 4com plc in

production of product in a financial year. These are basically associated with as assumption of

revenue generated during the year (Parker, 2011). On the other hand, each job activities are

incurring how much of the profit to the company are analyse by this reporting system. It will also

evaluate those areas which are earning maximum profit with minimum efforts.

Operational budget report: This particular budget reports generate information

regarding the expenses which are incur by 4com plc during production process. It is considered

as one of the major reporting system which help the managers to get complete details of actual

cost beard by company. It included various sub parts such as sale budget, variable budgets and

many more. It can be prepared during month, half yearly or on annual basis.

Inventory management report: This report generally focuses on stock management and

its control. All those physical stock that are used by 4com as managerial reporting to determine

various level of stock availability (Burritt, Schaltegger and Zvezdov, 2011). It includes various

steps which are required to be followed by managers in order to protect and record stock details

in the books of account. There are various tools such as EOQ and ABC costing that can be used

to analyse the results.

Performance report: Accounting can be more effectively use by finance departments to

judge performance of the company. It would be done by taking data of current and past year.

Different information which are related with the employees, team, company goodwill and other

outside competitors are analysed with the help of this report.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivable report: All the cash related information are recorded under this

report. This specific report is used in order to manage company's cash transaction or relation to

credit amount.

M1: Merits of MA and its applications

In 4com plc the above discussed different accounting system can help them to reach at

their destination. The company can use either of them to manager and control their business

operations. Any organisation whether small or medium-sized are working in order to earn

maximum profit with its limited resources. MA can help the company to increase efficiency so

that future goals can be attain. Other advantages of MA is to increase profitability, performances

and other aspects which are necessary for the growth prospective. With the use of job costing and

inventory costing system they can maintain their position and gain competitive advantages over

other.

D1: Critically evaluate management reporting system

In an organisation, reporting of financial transaction into books of account with proper

correction are essential. Because on that basis necessary decision are relies. The growth and

performance of the company are totally based on this reporting system (Renz, 2016). Some of

them are job costing reporting and performances reporting are considered as two of the important

reporting which can provide more accurate information about the company's performance.

Operating budget reporting is another reporting used by managers to control extra costs which

are done over the production of one extra units. It takes minimum time and cost to manage

regular transactions.

TASK 2

P3: Computation of net income by using various costing techniques

Costing: It is known as, a techniques of accounting which help to provide information

about assembling and recording of all key component of costs incurred to attain a objectives. It is

associated with that cost which is incurred on various activities or a units of work. In simple

words, cost is associated with production of a product and services by 4com plc. It include

various cost such as variable costs, fixed costs and semi- variable cost. It is considered as that

amount which is represented on billing invoice as the cost and recorded in preparation of

5

report. This specific report is used in order to manage company's cash transaction or relation to

credit amount.

M1: Merits of MA and its applications

In 4com plc the above discussed different accounting system can help them to reach at

their destination. The company can use either of them to manager and control their business

operations. Any organisation whether small or medium-sized are working in order to earn

maximum profit with its limited resources. MA can help the company to increase efficiency so

that future goals can be attain. Other advantages of MA is to increase profitability, performances

and other aspects which are necessary for the growth prospective. With the use of job costing and

inventory costing system they can maintain their position and gain competitive advantages over

other.

D1: Critically evaluate management reporting system

In an organisation, reporting of financial transaction into books of account with proper

correction are essential. Because on that basis necessary decision are relies. The growth and

performance of the company are totally based on this reporting system (Renz, 2016). Some of

them are job costing reporting and performances reporting are considered as two of the important

reporting which can provide more accurate information about the company's performance.

Operating budget reporting is another reporting used by managers to control extra costs which

are done over the production of one extra units. It takes minimum time and cost to manage

regular transactions.

TASK 2

P3: Computation of net income by using various costing techniques

Costing: It is known as, a techniques of accounting which help to provide information

about assembling and recording of all key component of costs incurred to attain a objectives. It is

associated with that cost which is incurred on various activities or a units of work. In simple

words, cost is associated with production of a product and services by 4com plc. It include

various cost such as variable costs, fixed costs and semi- variable cost. It is considered as that

amount which is represented on billing invoice as the cost and recorded in preparation of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

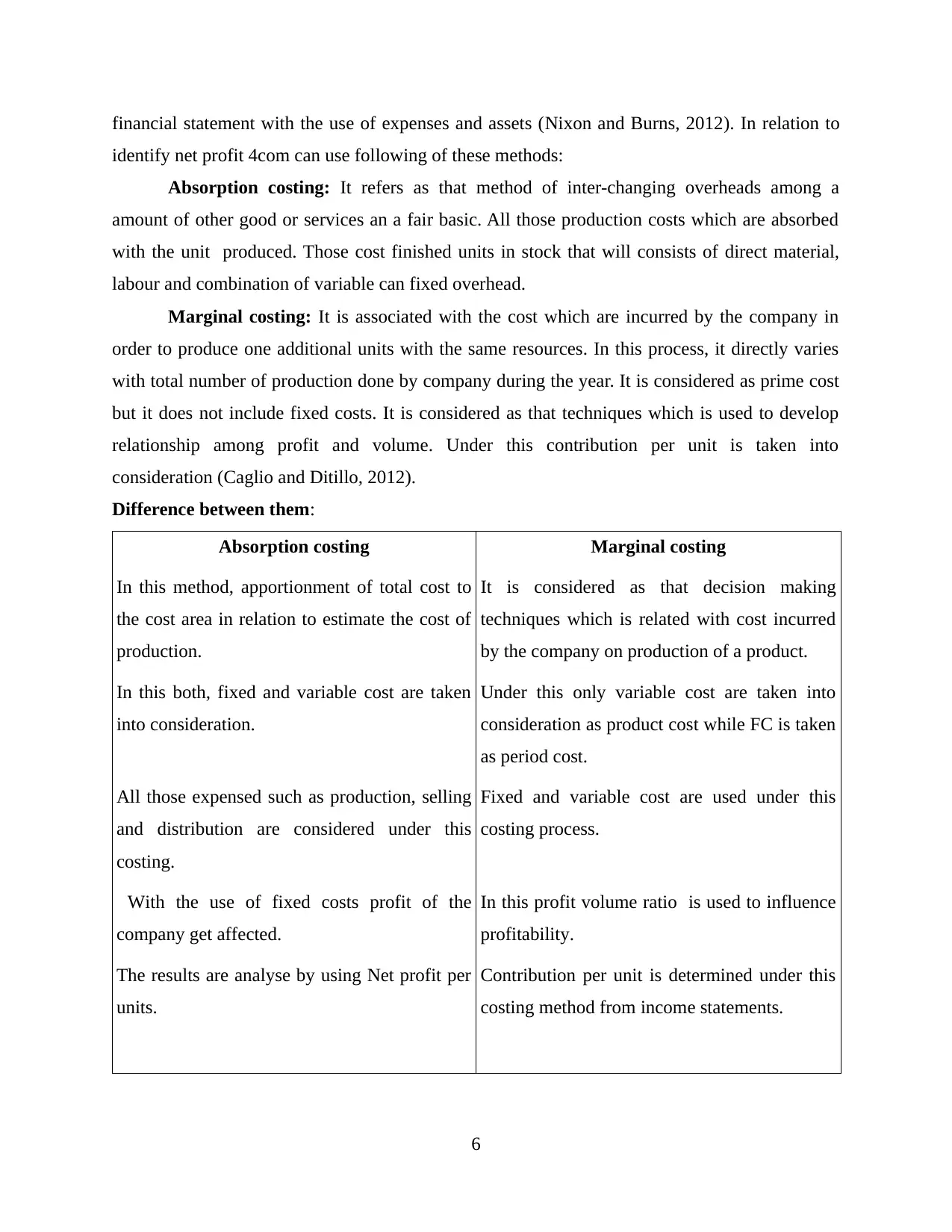

financial statement with the use of expenses and assets (Nixon and Burns, 2012). In relation to

identify net profit 4com can use following of these methods:

Absorption costing: It refers as that method of inter-changing overheads among a

amount of other good or services an a fair basic. All those production costs which are absorbed

with the unit produced. Those cost finished units in stock that will consists of direct material,

labour and combination of variable can fixed overhead.

Marginal costing: It is associated with the cost which are incurred by the company in

order to produce one additional units with the same resources. In this process, it directly varies

with total number of production done by company during the year. It is considered as prime cost

but it does not include fixed costs. It is considered as that techniques which is used to develop

relationship among profit and volume. Under this contribution per unit is taken into

consideration (Caglio and Ditillo, 2012).

Difference between them:

Absorption costing Marginal costing

In this method, apportionment of total cost to

the cost area in relation to estimate the cost of

production.

It is considered as that decision making

techniques which is related with cost incurred

by the company on production of a product.

In this both, fixed and variable cost are taken

into consideration.

Under this only variable cost are taken into

consideration as product cost while FC is taken

as period cost.

All those expensed such as production, selling

and distribution are considered under this

costing.

Fixed and variable cost are used under this

costing process.

With the use of fixed costs profit of the

company get affected.

In this profit volume ratio is used to influence

profitability.

The results are analyse by using Net profit per

units.

Contribution per unit is determined under this

costing method from income statements.

6

identify net profit 4com can use following of these methods:

Absorption costing: It refers as that method of inter-changing overheads among a

amount of other good or services an a fair basic. All those production costs which are absorbed

with the unit produced. Those cost finished units in stock that will consists of direct material,

labour and combination of variable can fixed overhead.

Marginal costing: It is associated with the cost which are incurred by the company in

order to produce one additional units with the same resources. In this process, it directly varies

with total number of production done by company during the year. It is considered as prime cost

but it does not include fixed costs. It is considered as that techniques which is used to develop

relationship among profit and volume. Under this contribution per unit is taken into

consideration (Caglio and Ditillo, 2012).

Difference between them:

Absorption costing Marginal costing

In this method, apportionment of total cost to

the cost area in relation to estimate the cost of

production.

It is considered as that decision making

techniques which is related with cost incurred

by the company on production of a product.

In this both, fixed and variable cost are taken

into consideration.

Under this only variable cost are taken into

consideration as product cost while FC is taken

as period cost.

All those expensed such as production, selling

and distribution are considered under this

costing.

Fixed and variable cost are used under this

costing process.

With the use of fixed costs profit of the

company get affected.

In this profit volume ratio is used to influence

profitability.

The results are analyse by using Net profit per

units.

Contribution per unit is determined under this

costing method from income statements.

6

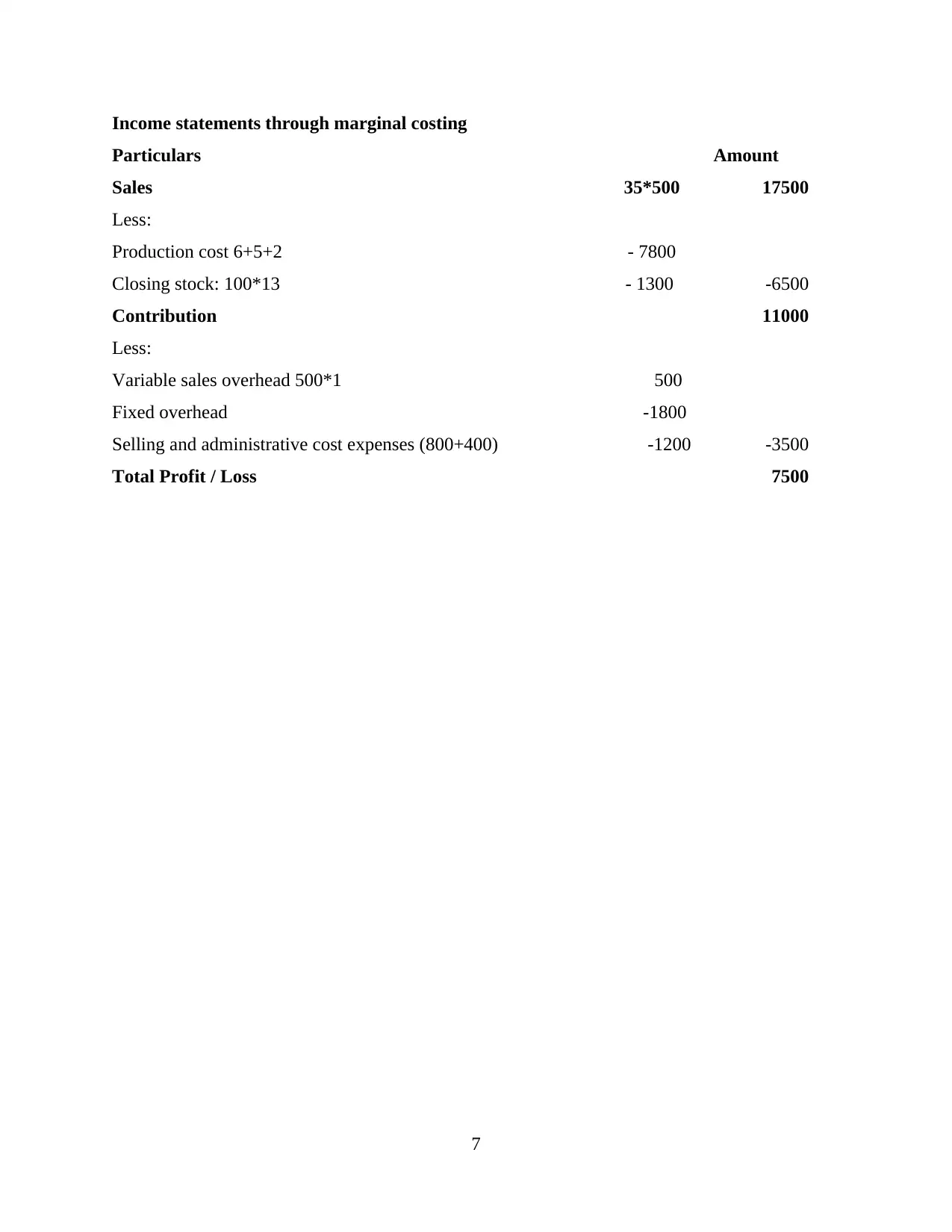

Income statements through marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

7

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

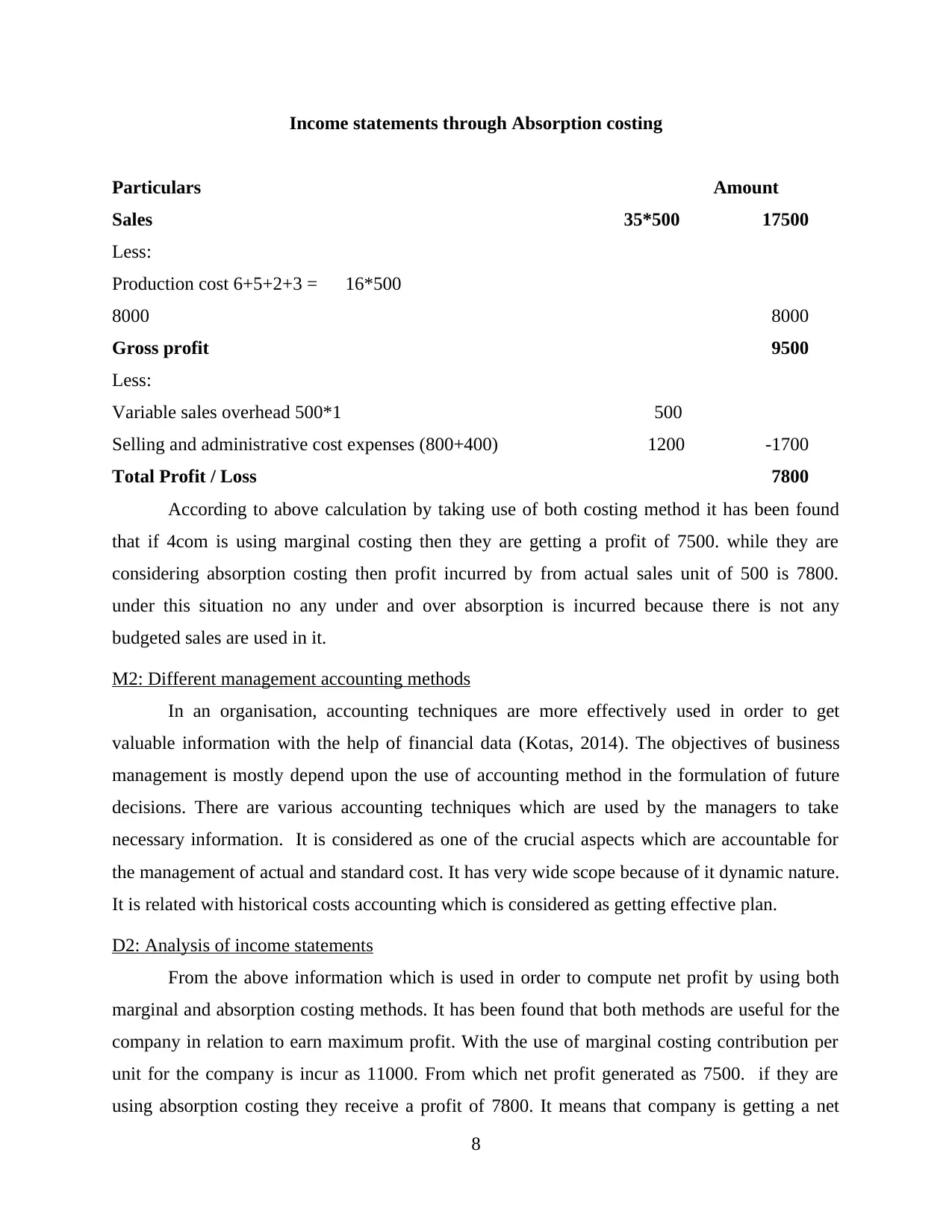

Income statements through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

According to above calculation by taking use of both costing method it has been found

that if 4com is using marginal costing then they are getting a profit of 7500. while they are

considering absorption costing then profit incurred by from actual sales unit of 500 is 7800.

under this situation no any under and over absorption is incurred because there is not any

budgeted sales are used in it.

M2: Different management accounting methods

In an organisation, accounting techniques are more effectively used in order to get

valuable information with the help of financial data (Kotas, 2014). The objectives of business

management is mostly depend upon the use of accounting method in the formulation of future

decisions. There are various accounting techniques which are used by the managers to take

necessary information. It is considered as one of the crucial aspects which are accountable for

the management of actual and standard cost. It has very wide scope because of it dynamic nature.

It is related with historical costs accounting which is considered as getting effective plan.

D2: Analysis of income statements

From the above information which is used in order to compute net profit by using both

marginal and absorption costing methods. It has been found that both methods are useful for the

company in relation to earn maximum profit. With the use of marginal costing contribution per

unit for the company is incur as 11000. From which net profit generated as 7500. if they are

using absorption costing they receive a profit of 7800. It means that company is getting a net

8

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

According to above calculation by taking use of both costing method it has been found

that if 4com is using marginal costing then they are getting a profit of 7500. while they are

considering absorption costing then profit incurred by from actual sales unit of 500 is 7800.

under this situation no any under and over absorption is incurred because there is not any

budgeted sales are used in it.

M2: Different management accounting methods

In an organisation, accounting techniques are more effectively used in order to get

valuable information with the help of financial data (Kotas, 2014). The objectives of business

management is mostly depend upon the use of accounting method in the formulation of future

decisions. There are various accounting techniques which are used by the managers to take

necessary information. It is considered as one of the crucial aspects which are accountable for

the management of actual and standard cost. It has very wide scope because of it dynamic nature.

It is related with historical costs accounting which is considered as getting effective plan.

D2: Analysis of income statements

From the above information which is used in order to compute net profit by using both

marginal and absorption costing methods. It has been found that both methods are useful for the

company in relation to earn maximum profit. With the use of marginal costing contribution per

unit for the company is incur as 11000. From which net profit generated as 7500. if they are

using absorption costing they receive a profit of 7800. It means that company is getting a net

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earning of 300. There is no any over and under absorption situation is under this calculation

because of absences of budgeted values.

TASK 3

P4: Merits and demerits of planning tools used for budgetary control process

Budget: It refers as an estimation of the total revenue and expenditure that are used for a

specific time duration. The main objectives of budget preparation is to determine the future cost

that are going to be invested by the company.

Budgetary control: It is considered as the system which uses budgets as an important

sources of planning and controlling of all those aspects which are associated with production and

selling of product and services. The main objects of 4com plc is to manage and control its daily

operations by using a perfect budget plan (Elsevier, 2015). It is done by using actual and

standard unit through making a positive comparison among them. It is related with

comprehensive control system that help the administration to regulate its business operations.

Process of budgetary control:

Estimation of budget for future: In the initial stage, company need to plan its business

activities by using appropriate ideas from financial department. A perfect strategies can make the

company to earn maximum profit with the minimum cost expenses. It consists of different

factors of costs which is used by company during production process.

Actual costs should be taken into consideration: In the second phase, managers need to

look about the actual cost which are invested by company in its production of products. It

determine the actual performance that are carried and regulated in current year (Callahan, Stetz

and Brooks, 2011). With the use of this manager get two reaction, one which is in favourable

form and the other one is adverse. The positive results are taken and adverse are need to be

analyse for further evaluation.

Examination between actual and standard values: In this procedures, with the

preparation of actual figure the next step in budgetary control process is to determine correct

value by comparing both actual and standard costs. It is will be more productive as the outcomes

are more effective.

Corrective phase: Under this process, all correction and review are taken into account.

The managers are responsible for making evaluating the mistakes and requirement of each

9

because of absences of budgeted values.

TASK 3

P4: Merits and demerits of planning tools used for budgetary control process

Budget: It refers as an estimation of the total revenue and expenditure that are used for a

specific time duration. The main objectives of budget preparation is to determine the future cost

that are going to be invested by the company.

Budgetary control: It is considered as the system which uses budgets as an important

sources of planning and controlling of all those aspects which are associated with production and

selling of product and services. The main objects of 4com plc is to manage and control its daily

operations by using a perfect budget plan (Elsevier, 2015). It is done by using actual and

standard unit through making a positive comparison among them. It is related with

comprehensive control system that help the administration to regulate its business operations.

Process of budgetary control:

Estimation of budget for future: In the initial stage, company need to plan its business

activities by using appropriate ideas from financial department. A perfect strategies can make the

company to earn maximum profit with the minimum cost expenses. It consists of different

factors of costs which is used by company during production process.

Actual costs should be taken into consideration: In the second phase, managers need to

look about the actual cost which are invested by company in its production of products. It

determine the actual performance that are carried and regulated in current year (Callahan, Stetz

and Brooks, 2011). With the use of this manager get two reaction, one which is in favourable

form and the other one is adverse. The positive results are taken and adverse are need to be

analyse for further evaluation.

Examination between actual and standard values: In this procedures, with the

preparation of actual figure the next step in budgetary control process is to determine correct

value by comparing both actual and standard costs. It is will be more productive as the outcomes

are more effective.

Corrective phase: Under this process, all correction and review are taken into account.

The managers are responsible for making evaluating the mistakes and requirement of each

9

departments. They need to analyse whether this budget is going to fulfil all the needs of finance

department as well as the performance of company.

Some of the important budget are:

Operating budgets: It is related with the expenses which are incurred by the company

during the production of product and services (Quinn, 2014). The main objective of this budget

is to analyse the total costs and expenses which are incur by the company on producing one unit

of a product. It is prepared with the use of taking information from all concern departments such

as sales, manufacturing and production etc.

Advantages:

It help the company to analyse the cost on regular, weakly, monthly or yearly basis.

The major benefits of preparing this budget is to determine the total cost required for the

future growth and sustainability.

Disadvantages:

Difficult to analyse if the information is in limited access.

It required much time to reach out to a perfect conclusion.

Static budget: It is said to be an estimation of predicated data used at one level of

activities. It is mainly prepared at the opening of budgeted session and last for only the planned

level of task. It is only suitable for planning process (Static budget, 2015.).

Advantages:

It is prepared under certain terms and condition in which all the information are based on

assumption basis that cannot be changed.

Disadvantages

It has limited source of application and is ineffective as a tool for controlling costs.

Cash-flows budget: It is related with the identification of total cash inflows and outflow

during the year (DRURY, 2013). It includes various activities which are responsible for

generating of cash such investing, financing and operating.

Advantages:

Total estimation of cash-inflows and out-flows are determine through using this budgets.

Disadvantages

It ignore cash-flows after the completion of payback period.

It is not considered in the process of measuring profitability.

10

department as well as the performance of company.

Some of the important budget are:

Operating budgets: It is related with the expenses which are incurred by the company

during the production of product and services (Quinn, 2014). The main objective of this budget

is to analyse the total costs and expenses which are incur by the company on producing one unit

of a product. It is prepared with the use of taking information from all concern departments such

as sales, manufacturing and production etc.

Advantages:

It help the company to analyse the cost on regular, weakly, monthly or yearly basis.

The major benefits of preparing this budget is to determine the total cost required for the

future growth and sustainability.

Disadvantages:

Difficult to analyse if the information is in limited access.

It required much time to reach out to a perfect conclusion.

Static budget: It is said to be an estimation of predicated data used at one level of

activities. It is mainly prepared at the opening of budgeted session and last for only the planned

level of task. It is only suitable for planning process (Static budget, 2015.).

Advantages:

It is prepared under certain terms and condition in which all the information are based on

assumption basis that cannot be changed.

Disadvantages

It has limited source of application and is ineffective as a tool for controlling costs.

Cash-flows budget: It is related with the identification of total cash inflows and outflow

during the year (DRURY, 2013). It includes various activities which are responsible for

generating of cash such investing, financing and operating.

Advantages:

Total estimation of cash-inflows and out-flows are determine through using this budgets.

Disadvantages

It ignore cash-flows after the completion of payback period.

It is not considered in the process of measuring profitability.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.