Management Accounting Report: Costing Systems and Analysis

VerifiedAdded on 2020/10/23

|8

|2192

|156

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on job costing, activity-based costing (ABC), work in progress, and finished goods inventory. The report begins with an introduction to management accounting, explaining its role in decision-making and operational efficiency. It then delves into the job costing system, explaining its suitability for companies like Connectta Ltd., which produce various products. The report includes calculations for work in progress inventory, finished goods, and manufacturing overhead, including examples of over-applied overhead. It also discusses accounting treatments for under-applied and over-applied overhead, and highlights the benefits of the ABC system in overcoming deficiencies of traditional job costing. The conclusion emphasizes the importance of management accounting in internal control and decision-making, and the report references several academic sources to support its findings.

MANAGEMENT

ACCOUTING

PROBLEM

ACCOUTING

PROBLEM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

Calculation of work in progress inventory account.....................................................................2

TASK 3............................................................................................................................................2

Calculation of cost of chair in finished goods.............................................................................2

TASK 4............................................................................................................................................3

Calculation...................................................................................................................................3

TASK 5............................................................................................................................................4

TASK 6............................................................................................................................................5

CONCLUSION................................................................................................................................5

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

Calculation of work in progress inventory account.....................................................................2

TASK 3............................................................................................................................................2

Calculation of cost of chair in finished goods.............................................................................2

TASK 4............................................................................................................................................3

Calculation...................................................................................................................................3

TASK 5............................................................................................................................................4

TASK 6............................................................................................................................................5

CONCLUSION................................................................................................................................5

INTRODUCTION

Management accounting which is also known as the cost accounting or managerial

accounting is considered as a branch of accounting which is basically concerned about the

identification, analysis, interpretation and measurement of accounting information which is used

by managers to formulate new strategies and take effective decisions to improve its operational

efficiency (Kaplan, 2015). The following report contains the detailed analysis of various

problems associated with management accounting. It also contains the reason which an

organisation considers while adopting job costing system, and the accounting treatment for under

applied and over applied manufacturing overhead. It also focuses on the deficiency which can be

overcome by using Activity Based Costing Methods. This report also shows the calculation of

work in progress and finished goods inventory.

TASK 1

Job Costing system: Job costing which is also known as job order costing, it is a

methodology used in accounting which help production managers to track down its cost which it

occurred while producing a unique product. It gives managers a clear view by tracking down its

expenses which are associated to a particular job, it helps business to analyse its individual cost

of a job and find out new ways or new policies which help business to reduce the cost which is

incurred during a particular process.

It is appropriate for a company to use job costing system when a company deals in so

many products, it is important for a company to calculate the cost of each product individually to

find out the maximum cost is incurred by which type of product. As in the above given case of

Connectta Ltd, it produces various product such as Computer caddy, Chair, printer stand and

desk it is important for Connectta to identify the individual cost which is associated with the

manufacturing of its products. In this case managers of Connectta Ltd has to identify the cost

which it is incurring in manufacturing of its chairs, computer caddy, desk and printer stand. It

helps mangers to allocate overheads in the ratio in which its cost is incurred. Company uses this

method to find out the individual efficiency of its production department associated with each

type of product (Hyvönen, 2003). This help managers of production department to take effective

decisions to formulate new strategies in order to improve the efficiency of each product

manufacturing process and reduce its total cost and increase its profit margin resulting in the

1

Management accounting which is also known as the cost accounting or managerial

accounting is considered as a branch of accounting which is basically concerned about the

identification, analysis, interpretation and measurement of accounting information which is used

by managers to formulate new strategies and take effective decisions to improve its operational

efficiency (Kaplan, 2015). The following report contains the detailed analysis of various

problems associated with management accounting. It also contains the reason which an

organisation considers while adopting job costing system, and the accounting treatment for under

applied and over applied manufacturing overhead. It also focuses on the deficiency which can be

overcome by using Activity Based Costing Methods. This report also shows the calculation of

work in progress and finished goods inventory.

TASK 1

Job Costing system: Job costing which is also known as job order costing, it is a

methodology used in accounting which help production managers to track down its cost which it

occurred while producing a unique product. It gives managers a clear view by tracking down its

expenses which are associated to a particular job, it helps business to analyse its individual cost

of a job and find out new ways or new policies which help business to reduce the cost which is

incurred during a particular process.

It is appropriate for a company to use job costing system when a company deals in so

many products, it is important for a company to calculate the cost of each product individually to

find out the maximum cost is incurred by which type of product. As in the above given case of

Connectta Ltd, it produces various product such as Computer caddy, Chair, printer stand and

desk it is important for Connectta to identify the individual cost which is associated with the

manufacturing of its products. In this case managers of Connectta Ltd has to identify the cost

which it is incurring in manufacturing of its chairs, computer caddy, desk and printer stand. It

helps mangers to allocate overheads in the ratio in which its cost is incurred. Company uses this

method to find out the individual efficiency of its production department associated with each

type of product (Hyvönen, 2003). This help managers of production department to take effective

decisions to formulate new strategies in order to improve the efficiency of each product

manufacturing process and reduce its total cost and increase its profit margin resulting in the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enhancements of its financial position and gain competitive advantages over other. It also helps

manager to identify the problems in each job manufacturing process and take effective decisions

to overcome its problems and improve its efficiency in order to reduce its total cost of

production.

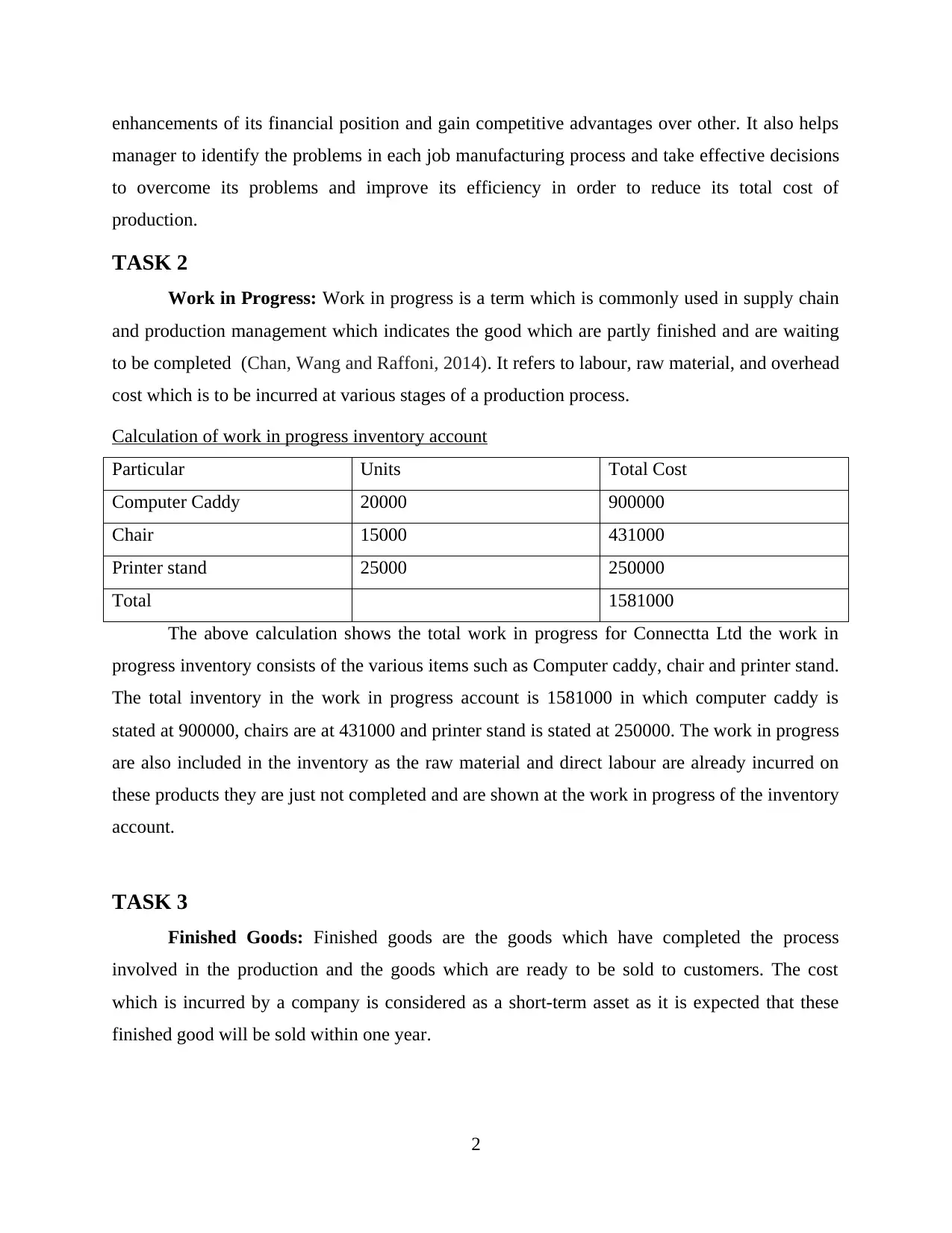

TASK 2

Work in Progress: Work in progress is a term which is commonly used in supply chain

and production management which indicates the good which are partly finished and are waiting

to be completed (Chan, Wang and Raffoni, 2014). It refers to labour, raw material, and overhead

cost which is to be incurred at various stages of a production process.

Calculation of work in progress inventory account

Particular Units Total Cost

Computer Caddy 20000 900000

Chair 15000 431000

Printer stand 25000 250000

Total 1581000

The above calculation shows the total work in progress for Connectta Ltd the work in

progress inventory consists of the various items such as Computer caddy, chair and printer stand.

The total inventory in the work in progress account is 1581000 in which computer caddy is

stated at 900000, chairs are at 431000 and printer stand is stated at 250000. The work in progress

are also included in the inventory as the raw material and direct labour are already incurred on

these products they are just not completed and are shown at the work in progress of the inventory

account.

TASK 3

Finished Goods: Finished goods are the goods which have completed the process

involved in the production and the goods which are ready to be sold to customers. The cost

which is incurred by a company is considered as a short-term asset as it is expected that these

finished good will be sold within one year.

2

manager to identify the problems in each job manufacturing process and take effective decisions

to overcome its problems and improve its efficiency in order to reduce its total cost of

production.

TASK 2

Work in Progress: Work in progress is a term which is commonly used in supply chain

and production management which indicates the good which are partly finished and are waiting

to be completed (Chan, Wang and Raffoni, 2014). It refers to labour, raw material, and overhead

cost which is to be incurred at various stages of a production process.

Calculation of work in progress inventory account

Particular Units Total Cost

Computer Caddy 20000 900000

Chair 15000 431000

Printer stand 25000 250000

Total 1581000

The above calculation shows the total work in progress for Connectta Ltd the work in

progress inventory consists of the various items such as Computer caddy, chair and printer stand.

The total inventory in the work in progress account is 1581000 in which computer caddy is

stated at 900000, chairs are at 431000 and printer stand is stated at 250000. The work in progress

are also included in the inventory as the raw material and direct labour are already incurred on

these products they are just not completed and are shown at the work in progress of the inventory

account.

TASK 3

Finished Goods: Finished goods are the goods which have completed the process

involved in the production and the goods which are ready to be sold to customers. The cost

which is incurred by a company is considered as a short-term asset as it is expected that these

finished good will be sold within one year.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

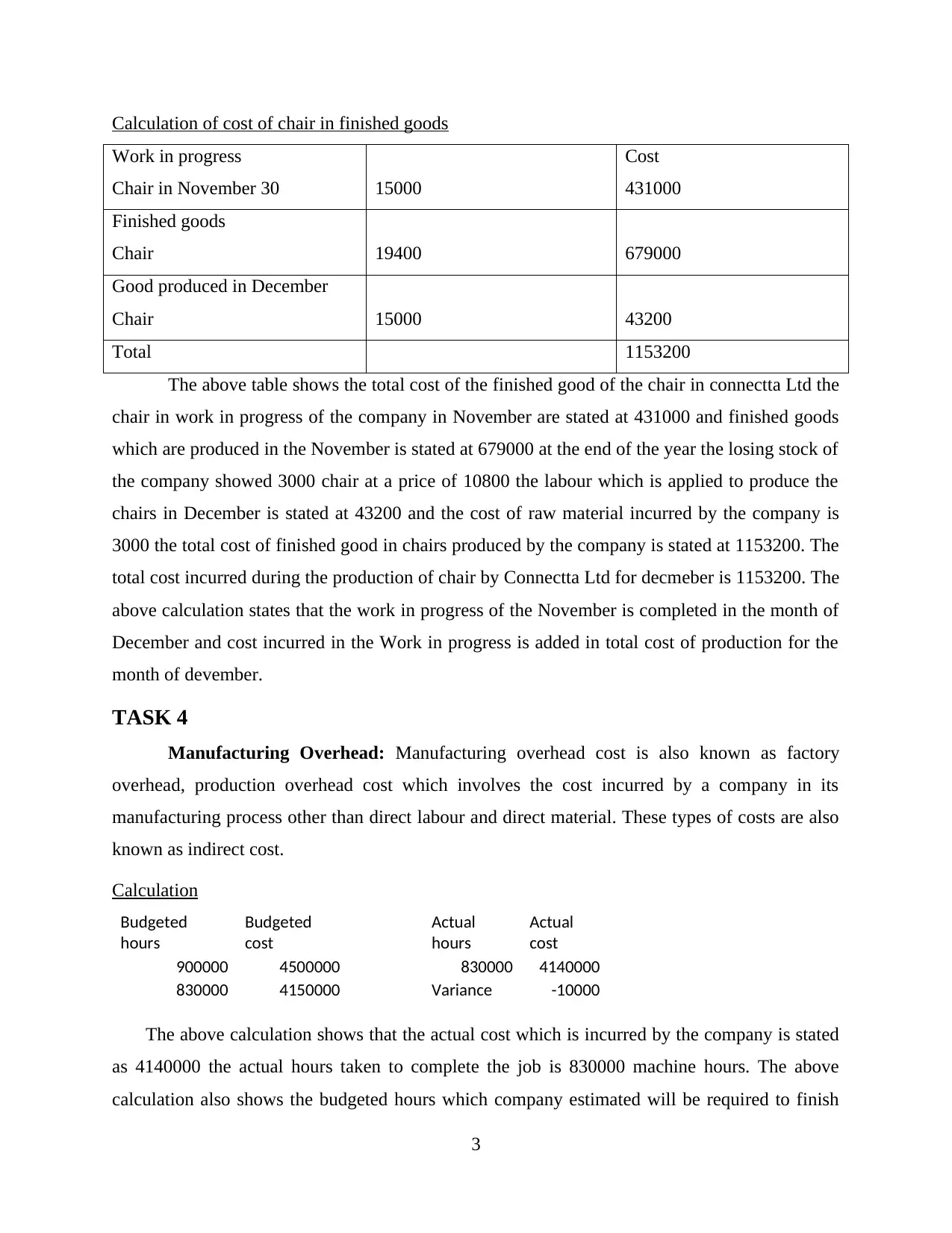

Calculation of cost of chair in finished goods

Work in progress

Chair in November 30 15000

Cost

431000

Finished goods

Chair 19400 679000

Good produced in December

Chair 15000 43200

Total 1153200

The above table shows the total cost of the finished good of the chair in connectta Ltd the

chair in work in progress of the company in November are stated at 431000 and finished goods

which are produced in the November is stated at 679000 at the end of the year the losing stock of

the company showed 3000 chair at a price of 10800 the labour which is applied to produce the

chairs in December is stated at 43200 and the cost of raw material incurred by the company is

3000 the total cost of finished good in chairs produced by the company is stated at 1153200. The

total cost incurred during the production of chair by Connectta Ltd for decmeber is 1153200. The

above calculation states that the work in progress of the November is completed in the month of

December and cost incurred in the Work in progress is added in total cost of production for the

month of devember.

TASK 4

Manufacturing Overhead: Manufacturing overhead cost is also known as factory

overhead, production overhead cost which involves the cost incurred by a company in its

manufacturing process other than direct labour and direct material. These types of costs are also

known as indirect cost.

Calculation

Budgeted

hours

Budgeted

cost

Actual

hours

Actual

cost

900000 4500000 830000 4140000

830000 4150000 Variance -10000

The above calculation shows that the actual cost which is incurred by the company is stated

as 4140000 the actual hours taken to complete the job is 830000 machine hours. The above

calculation also shows the budgeted hours which company estimated will be required to finish

3

Work in progress

Chair in November 30 15000

Cost

431000

Finished goods

Chair 19400 679000

Good produced in December

Chair 15000 43200

Total 1153200

The above table shows the total cost of the finished good of the chair in connectta Ltd the

chair in work in progress of the company in November are stated at 431000 and finished goods

which are produced in the November is stated at 679000 at the end of the year the losing stock of

the company showed 3000 chair at a price of 10800 the labour which is applied to produce the

chairs in December is stated at 43200 and the cost of raw material incurred by the company is

3000 the total cost of finished good in chairs produced by the company is stated at 1153200. The

total cost incurred during the production of chair by Connectta Ltd for decmeber is 1153200. The

above calculation states that the work in progress of the November is completed in the month of

December and cost incurred in the Work in progress is added in total cost of production for the

month of devember.

TASK 4

Manufacturing Overhead: Manufacturing overhead cost is also known as factory

overhead, production overhead cost which involves the cost incurred by a company in its

manufacturing process other than direct labour and direct material. These types of costs are also

known as indirect cost.

Calculation

Budgeted

hours

Budgeted

cost

Actual

hours

Actual

cost

900000 4500000 830000 4140000

830000 4150000 Variance -10000

The above calculation shows that the actual cost which is incurred by the company is stated

as 4140000 the actual hours taken to complete the job is 830000 machine hours. The above

calculation also shows the budgeted hours which company estimated will be required to finish

3

the job is stated at 900000 hours and the cost which will be incurred is estimated at 4500000.

From the above calculation it can be noted that the company has applied additional overhead of

10000 in its budgeted estimates while calculating the total cost of production. In this case

company has over applied its manufacturing overhead. Now this over applied manufacturing

overhead will be added back to the profit and loss account of the company as the income.

Company uses this method to and over estimated its overhead this over estimated overhead is

added back to the profit in order to calculate the actual profit earned by the company. In this case

Connectta Ltd has also over applied its manufacturing overhead in this case the company will

add this variance of 10000 to its profit and loss statements to calculate the actual profit earned by

the company.

TASK 5

The under or over applied overhead is known as a difference between the overhead cost

which was applied to the work in process and the actual overhead cost which was incurred by a

company during its manufacturing process.

Over applied manufacturing overhead = Applied overhead > Actual overhead

Under applied manufacturing overhead = Applied overhead < Actual overhead

Accounting treatment

In order to treat the over applied or under applied overhead cost actual manufacturing

overhead cost which is incurred by company during its production process are recorded on the

debit side of the manufacturing overhead account and the applied manufacturing overhead cost is

shown at the credit side of manufacturing overhead account (Cardoni, 2012). Applied overhead

cost are shown on the credit side as it is applied to work in progress whereas the actual overhead

cost are shown on the debit side as they are actually incurred by a company during its production

process. At the end of a given period if the account shows credit balance, the overhead which is

applied is considered as a over applied overhead. Whereas if the balance of debit side is more

than the credit side it states that the overhead is under applied overhead. At the end of the year

the balance which is shown in the debit side or credit side of the manufacturing overhead account

is allocated by using two methods. One is by allocating it to the various works involved in the

process of production which includes process, cost of goods sold and finished goods. The second

method is by transferring the complete amount shown in the overhead account to the cost of

4

From the above calculation it can be noted that the company has applied additional overhead of

10000 in its budgeted estimates while calculating the total cost of production. In this case

company has over applied its manufacturing overhead. Now this over applied manufacturing

overhead will be added back to the profit and loss account of the company as the income.

Company uses this method to and over estimated its overhead this over estimated overhead is

added back to the profit in order to calculate the actual profit earned by the company. In this case

Connectta Ltd has also over applied its manufacturing overhead in this case the company will

add this variance of 10000 to its profit and loss statements to calculate the actual profit earned by

the company.

TASK 5

The under or over applied overhead is known as a difference between the overhead cost

which was applied to the work in process and the actual overhead cost which was incurred by a

company during its manufacturing process.

Over applied manufacturing overhead = Applied overhead > Actual overhead

Under applied manufacturing overhead = Applied overhead < Actual overhead

Accounting treatment

In order to treat the over applied or under applied overhead cost actual manufacturing

overhead cost which is incurred by company during its production process are recorded on the

debit side of the manufacturing overhead account and the applied manufacturing overhead cost is

shown at the credit side of manufacturing overhead account (Cardoni, 2012). Applied overhead

cost are shown on the credit side as it is applied to work in progress whereas the actual overhead

cost are shown on the debit side as they are actually incurred by a company during its production

process. At the end of a given period if the account shows credit balance, the overhead which is

applied is considered as a over applied overhead. Whereas if the balance of debit side is more

than the credit side it states that the overhead is under applied overhead. At the end of the year

the balance which is shown in the debit side or credit side of the manufacturing overhead account

is allocated by using two methods. One is by allocating it to the various works involved in the

process of production which includes process, cost of goods sold and finished goods. The second

method is by transferring the complete amount shown in the overhead account to the cost of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goods sold account. These are the two accounting treatments which are available with the

managers to allocate its over or under applied overhead cost to the its total cost of production.

TASK 6

Activity based costing system: It is an accounting method which is used by mangers to

identify the cost and assign costs to various overhead activities. It helps managers to recognize

the relationship between various activities such as cost, manufactured product and overhead

activities. With the help of this relationship it becomes easy for the managers to assign its

indirect cost to product less arbitrarily than traditional method.

Activity based costing system could overcome the various deficiencies which are

inherent in the existing job costing system as it is considered to be more accurate as it considers

various important factor which are taken into account before assigning its total cost to a product.

Activity based costing system help managers to identify the individual cost which is associated

to individual activity involved in the production process. In Connectta Ltd they follow the job

costing system in which it allocates the cost of individual job processed in the production process

and sometimes it misses some important activities involved in the production process. Whereas

activity-based system identifies each cost associated with every activity and it highlights the

different activities which are performed in an organisation. It also helps managers to properly

allocate its manufacturing overhead cost to specific activities and in job costing system it directly

allocates its overhead cost to the various jobs involving various products. In activity-based

costing system manufacturing cost is identified for individual activity and identifies the ways

through which it can improve its efficiency of different activities.

CONCLUSION

From the above file it can be concluded that management accounting plays an important role

in the internal control and decision making process. the above file also shows the reason due to

which a company should use job costing system in order to reduce its cost and identify cost

associated with each of the job involved. It also states the calculation of Work in progress

inventory accounts of the company. With the help of this report it can be established that the

company uses various methods through which it can treat the over and under applied

manufacturing overheads. This report also states the areas and problems which are inherent by

using job costing system and can be over come by using Activity cost based system.

5

managers to allocate its over or under applied overhead cost to the its total cost of production.

TASK 6

Activity based costing system: It is an accounting method which is used by mangers to

identify the cost and assign costs to various overhead activities. It helps managers to recognize

the relationship between various activities such as cost, manufactured product and overhead

activities. With the help of this relationship it becomes easy for the managers to assign its

indirect cost to product less arbitrarily than traditional method.

Activity based costing system could overcome the various deficiencies which are

inherent in the existing job costing system as it is considered to be more accurate as it considers

various important factor which are taken into account before assigning its total cost to a product.

Activity based costing system help managers to identify the individual cost which is associated

to individual activity involved in the production process. In Connectta Ltd they follow the job

costing system in which it allocates the cost of individual job processed in the production process

and sometimes it misses some important activities involved in the production process. Whereas

activity-based system identifies each cost associated with every activity and it highlights the

different activities which are performed in an organisation. It also helps managers to properly

allocate its manufacturing overhead cost to specific activities and in job costing system it directly

allocates its overhead cost to the various jobs involving various products. In activity-based

costing system manufacturing cost is identified for individual activity and identifies the ways

through which it can improve its efficiency of different activities.

CONCLUSION

From the above file it can be concluded that management accounting plays an important role

in the internal control and decision making process. the above file also shows the reason due to

which a company should use job costing system in order to reduce its cost and identify cost

associated with each of the job involved. It also states the calculation of Work in progress

inventory accounts of the company. With the help of this report it can be established that the

company uses various methods through which it can treat the over and under applied

manufacturing overheads. This report also states the areas and problems which are inherent by

using job costing system and can be over come by using Activity cost based system.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFRENCES

Books and Journals

Kaplan, R. S., 2015. The evolution of management accounting. In Readings in accounting for

management control (pp. 586-621). Springer, Boston, MA.

Hyvönen, T., 2003. Management accounting and information systems: ERP versus

BoB. European Accounting Review, 12(1), pp.155-173.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review, 46(4), pp.344-360.

Cardoni, A., 2012. Business planning and management accounting in strategic networks:

theoretical development and empirical evidence from enterprises’ network"

agreement". Management Control.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Vosselman, E., 2014. The ‘performativity thesis’ and its critics: Towards a relational ontology of

management accounting. Accounting and Business Research. 44(2). pp.181-203.

6

Books and Journals

Kaplan, R. S., 2015. The evolution of management accounting. In Readings in accounting for

management control (pp. 586-621). Springer, Boston, MA.

Hyvönen, T., 2003. Management accounting and information systems: ERP versus

BoB. European Accounting Review, 12(1), pp.155-173.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review, 46(4), pp.344-360.

Cardoni, A., 2012. Business planning and management accounting in strategic networks:

theoretical development and empirical evidence from enterprises’ network"

agreement". Management Control.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Vosselman, E., 2014. The ‘performativity thesis’ and its critics: Towards a relational ontology of

management accounting. Accounting and Business Research. 44(2). pp.181-203.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.