Management Accounting Report for Tech (UK) Ltd - Budgeting & Costing

VerifiedAdded on 2020/09/17

|12

|3600

|75

Report

AI Summary

This report examines management accounting practices within Tech (UK) Limited, focusing on improving decision-making through financial information. It covers essential aspects of management accounting, including its role in planning, organizing, and controlling operations. The report delves into various costing methods like absorption and marginal costing, alongside different budgeting types, their advantages, and disadvantages. It outlines the budget preparation process and highlights the significance of budgeting for planning and control. Additionally, the report explores the Balanced Scorecard approach as a performance management tool. The content provides a comprehensive overview of management accounting principles and their practical application in a business context.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

a) Discussing about the management accounting and the necessary need to management

accounting system.......................................................................................................................1

P2 Presenting Financial information...........................................................................................3

Task 2...............................................................................................................................................4

P3 Income statement on the basis Absorption costing and marginal costing.............................4

TASK 3............................................................................................................................................5

P4.................................................................................................................................................5

(a) Different types of budget and their advantages and disadvantages.......................................5

(b) Process for preparing budget.................................................................................................7

c The significance of budget as tool for planning and control purposes.....................................7

Task 4...............................................................................................................................................8

P5. Balanced scorecard Approach...............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

a) Discussing about the management accounting and the necessary need to management

accounting system.......................................................................................................................1

P2 Presenting Financial information...........................................................................................3

Task 2...............................................................................................................................................4

P3 Income statement on the basis Absorption costing and marginal costing.............................4

TASK 3............................................................................................................................................5

P4.................................................................................................................................................5

(a) Different types of budget and their advantages and disadvantages.......................................5

(b) Process for preparing budget.................................................................................................7

c The significance of budget as tool for planning and control purposes.....................................7

Task 4...............................................................................................................................................8

P5. Balanced scorecard Approach...............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is the important role in the organisation which will assist in

managing various system for day to day operation in the firm. In other words, this can help to

perform each and every role to consider such as planing, organising, staffing, directing and

controlling. The current report is based on the Tech (UK) Limited who deals in a particular

charger of the mobile handsets and various tech gadget which are used in the stores of retail

sector in the United Kingdom. The issue have been arisen in the organisation regarding lack of

information to improve their decision making. The aim of current report is to understand about

appropriate and essential requirement of the management accounting as well financial source on

types managerial accounting reports and significant for the information to be presented in

manner that should be approachable. Further, various types of budget their advantages and

disadvantages as well preparation of budget procedure to find out the pricing and various costing

system which can be utilised for the company.

Task 1

a) Discussing about the management accounting and the necessary need to management

accounting system.

The management accounting is the area of accounting which will evaluate and gives

pricing information for taking various decision as well assist in planning and controlling by the

internal management. But on the other hand financial accounting have aim is to disclose the end

outcomes of the enterprises and on a specific period it focuses in the financial situation. The

audience of the management accounting is any top management as well lower level employees to

know data or the information will be utilised within firm or

There are certain management accounting information system tools which can be used for taking

decision making by the department manager(Eldenburg 2016). Each and every manager or the

professional who are working in the financial division for that appropriate evaluation of the

financial accounting. It will assist in maintaining various transaction in the data which are given

the exact outcomes. The cost accounting is more effective as well increasing profit in context of

evaluation the cost incurred in all the role of the business entity.

Cost Accounting: This are the techniques which are used by the manager to take

decision in term of financial system of the organisation. The cost accounting will assist

for evaluation as well appropriate requirement of budget for accomplish different

1

Management accounting is the important role in the organisation which will assist in

managing various system for day to day operation in the firm. In other words, this can help to

perform each and every role to consider such as planing, organising, staffing, directing and

controlling. The current report is based on the Tech (UK) Limited who deals in a particular

charger of the mobile handsets and various tech gadget which are used in the stores of retail

sector in the United Kingdom. The issue have been arisen in the organisation regarding lack of

information to improve their decision making. The aim of current report is to understand about

appropriate and essential requirement of the management accounting as well financial source on

types managerial accounting reports and significant for the information to be presented in

manner that should be approachable. Further, various types of budget their advantages and

disadvantages as well preparation of budget procedure to find out the pricing and various costing

system which can be utilised for the company.

Task 1

a) Discussing about the management accounting and the necessary need to management

accounting system.

The management accounting is the area of accounting which will evaluate and gives

pricing information for taking various decision as well assist in planning and controlling by the

internal management. But on the other hand financial accounting have aim is to disclose the end

outcomes of the enterprises and on a specific period it focuses in the financial situation. The

audience of the management accounting is any top management as well lower level employees to

know data or the information will be utilised within firm or

There are certain management accounting information system tools which can be used for taking

decision making by the department manager(Eldenburg 2016). Each and every manager or the

professional who are working in the financial division for that appropriate evaluation of the

financial accounting. It will assist in maintaining various transaction in the data which are given

the exact outcomes. The cost accounting is more effective as well increasing profit in context of

evaluation the cost incurred in all the role of the business entity.

Cost Accounting: This are the techniques which are used by the manager to take

decision in term of financial system of the organisation. The cost accounting will assist

for evaluation as well appropriate requirement of budget for accomplish different

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operation in company. Under cost accounting there are various cost considering such as

job costing, batch costing, variable, fixed, direct and indirect.

Tax accounting: It is a necessary for the enterprises' development as well growth for the

making effective revenue of the organisation as well payment of organisational taxes and

other charges such as conveyance, duties on different services.

Budgetary: This is another techniques which is used by the manager to show an

assumption of finance and cost consist for the various expenditure to achieve long terms

as well short term goals(Christ and Burritt, 2017). For the organisation there are certain

types of budget require to set such as marketing and production.

Auditing: This can be most important techniques which will help to find out the errors

and suggest organisation to improve their finance performance.

Cost accounting system which are important for the managerial accounting to fulfil the different

accounting: Actual: It is a cost accounting system which is recorded on the basis of cost incurred for

goods on various factors including actual cost of material, labour and overhead. Normal: It is utilised for the valuation of production of goods with the actual material

cost, direct labour cost and production overhead cost on the basis already finding out

manufacturing overhead price. Therefore, this will help to derive the cost of goods and

services provide by the organisation. Standard costing: It is a cost accounting system under which all the inventory of

organisation is values at the standard cost and any changes in the standards is incurred as

the PPV or the purchase price variance. Inventory management system:It is another administration bookkeeping framework

which keeps up the stock or stock bookkeeping framework (Fullerton, Kennedy and

Widener, 2014). Assembling organizations need to embrace these frameworks to stable

the item overload to maintain a strategic distance from blackouts. This is the most basic

and critical apparatus to make stock information.

Job costing system:On the opposite side, another administration bookkeeping framework

is Job costing framework. It is the best instrument of bookkeeping. This is the assembling

expense to an individual item or clumps of items which help to recognize the item

character. This framework is utilized for the most part in those assembling firms where

2

job costing, batch costing, variable, fixed, direct and indirect.

Tax accounting: It is a necessary for the enterprises' development as well growth for the

making effective revenue of the organisation as well payment of organisational taxes and

other charges such as conveyance, duties on different services.

Budgetary: This is another techniques which is used by the manager to show an

assumption of finance and cost consist for the various expenditure to achieve long terms

as well short term goals(Christ and Burritt, 2017). For the organisation there are certain

types of budget require to set such as marketing and production.

Auditing: This can be most important techniques which will help to find out the errors

and suggest organisation to improve their finance performance.

Cost accounting system which are important for the managerial accounting to fulfil the different

accounting: Actual: It is a cost accounting system which is recorded on the basis of cost incurred for

goods on various factors including actual cost of material, labour and overhead. Normal: It is utilised for the valuation of production of goods with the actual material

cost, direct labour cost and production overhead cost on the basis already finding out

manufacturing overhead price. Therefore, this will help to derive the cost of goods and

services provide by the organisation. Standard costing: It is a cost accounting system under which all the inventory of

organisation is values at the standard cost and any changes in the standards is incurred as

the PPV or the purchase price variance. Inventory management system:It is another administration bookkeeping framework

which keeps up the stock or stock bookkeeping framework (Fullerton, Kennedy and

Widener, 2014). Assembling organizations need to embrace these frameworks to stable

the item overload to maintain a strategic distance from blackouts. This is the most basic

and critical apparatus to make stock information.

Job costing system:On the opposite side, another administration bookkeeping framework

is Job costing framework. It is the best instrument of bookkeeping. This is the assembling

expense to an individual item or clumps of items which help to recognize the item

character. This framework is utilized for the most part in those assembling firms where

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

items produced are adequately not quite the same as others. It is the report of direct

material and direct work.

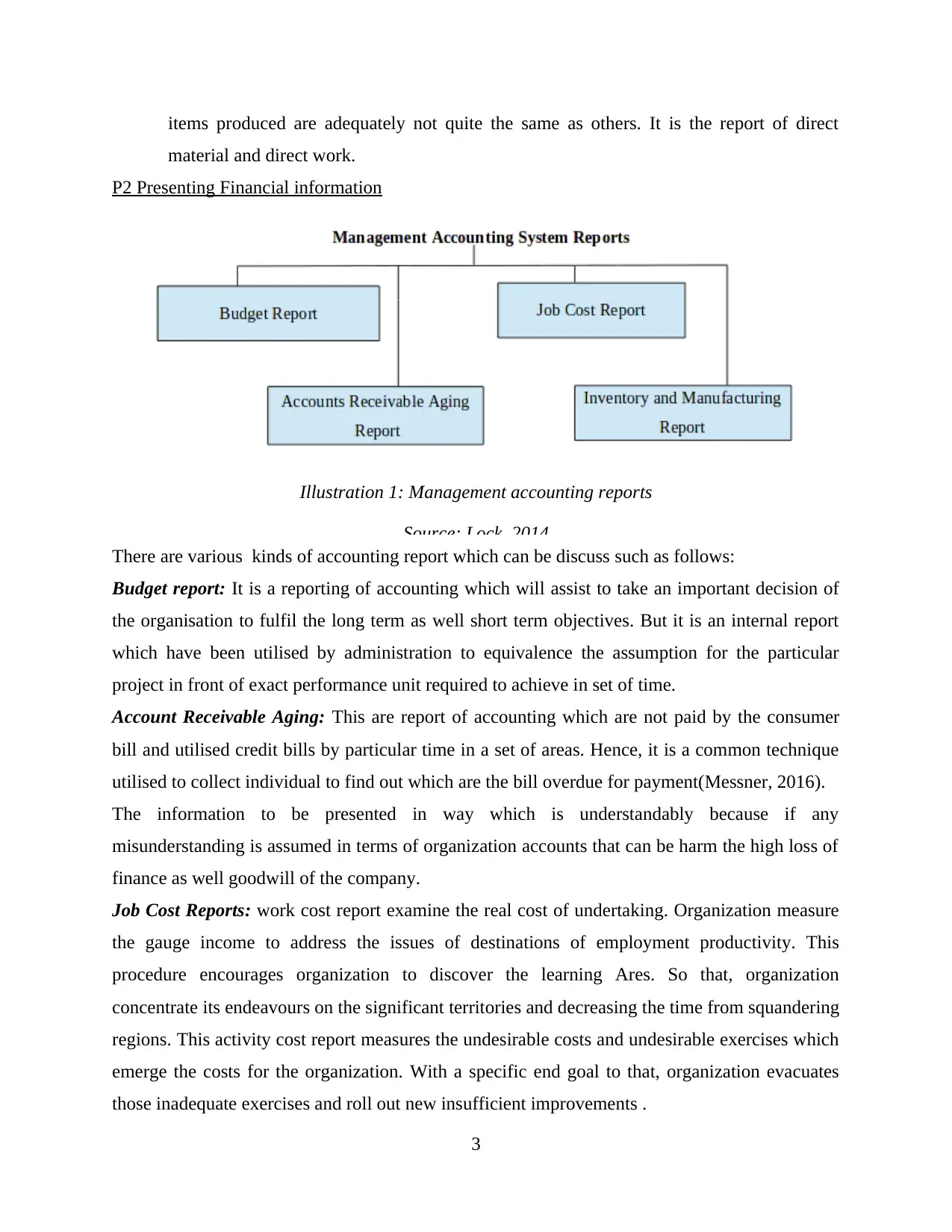

P2 Presenting Financial information

Illustration 1: Management accounting reports

Source: Lock, 2014

There are various kinds of accounting report which can be discuss such as follows:

Budget report: It is a reporting of accounting which will assist to take an important decision of

the organisation to fulfil the long term as well short term objectives. But it is an internal report

which have been utilised by administration to equivalence the assumption for the particular

project in front of exact performance unit required to achieve in set of time.

Account Receivable Aging: This are report of accounting which are not paid by the consumer

bill and utilised credit bills by particular time in a set of areas. Hence, it is a common technique

utilised to collect individual to find out which are the bill overdue for payment(Messner, 2016).

The information to be presented in way which is understandably because if any

misunderstanding is assumed in terms of organization accounts that can be harm the high loss of

finance as well goodwill of the company.

Job Cost Reports: work cost report examine the real cost of undertaking. Organization measure

the gauge income to address the issues of destinations of employment productivity. This

procedure encourages organization to discover the learning Ares. So that, organization

concentrate its endeavours on the significant territories and decreasing the time from squandering

regions. This activity cost report measures the undesirable costs and undesirable exercises which

emerge the costs for the organization. With a specific end goal to that, organization evacuates

those inadequate exercises and roll out new insufficient improvements .

3

material and direct work.

P2 Presenting Financial information

Illustration 1: Management accounting reports

Source: Lock, 2014

There are various kinds of accounting report which can be discuss such as follows:

Budget report: It is a reporting of accounting which will assist to take an important decision of

the organisation to fulfil the long term as well short term objectives. But it is an internal report

which have been utilised by administration to equivalence the assumption for the particular

project in front of exact performance unit required to achieve in set of time.

Account Receivable Aging: This are report of accounting which are not paid by the consumer

bill and utilised credit bills by particular time in a set of areas. Hence, it is a common technique

utilised to collect individual to find out which are the bill overdue for payment(Messner, 2016).

The information to be presented in way which is understandably because if any

misunderstanding is assumed in terms of organization accounts that can be harm the high loss of

finance as well goodwill of the company.

Job Cost Reports: work cost report examine the real cost of undertaking. Organization measure

the gauge income to address the issues of destinations of employment productivity. This

procedure encourages organization to discover the learning Ares. So that, organization

concentrate its endeavours on the significant territories and decreasing the time from squandering

regions. This activity cost report measures the undesirable costs and undesirable exercises which

emerge the costs for the organization. With a specific end goal to that, organization evacuates

those inadequate exercises and roll out new insufficient improvements .

3

Inventory and Manufacturing: This report of stock makes the organization producing forms

more effective. Occupation cost report incorporates squander, hourly work costs, per unit

overhead costs things. In this detailing administrator of the organization thinks about the

distinctive mechanical production systems in the organization to upgrade the change and

rewards to the best performing divisions. This makes condition positive and fiery(Renz and

Herman, 2016).

Based on above detailing strategies, these all are for the improvement of the organization. With

the assistance of all these detailing strategies organization make new money related

arrangements to meet the destinations or objectives of the organization. This makes the

administration bookkeeping framework all the more capable and extended

Task 2

P3 Income statement on the basis Absorption costing and marginal costing.

Absorption costing: It is a managerial accounting cost of techniques of incurring each and every

costs associated with the manufacturing a specific goods and necessary for then GAAP outside

reporting.

Income statement on the basis of Absorption costing:

Particular Unit Per Unit cost Amount

sales 1500 35 $2500

-COGS

Direct Material 2000 8 -16000

Direct Labour 2000 5 -10000

Variable production

overhead

2000 2 -4000

Fixed Production

overhead

2000 5 -10000

Gross Profit 12500

-Admin and Selling

Fixed (100000*1) -10000

4

more effective. Occupation cost report incorporates squander, hourly work costs, per unit

overhead costs things. In this detailing administrator of the organization thinks about the

distinctive mechanical production systems in the organization to upgrade the change and

rewards to the best performing divisions. This makes condition positive and fiery(Renz and

Herman, 2016).

Based on above detailing strategies, these all are for the improvement of the organization. With

the assistance of all these detailing strategies organization make new money related

arrangements to meet the destinations or objectives of the organization. This makes the

administration bookkeeping framework all the more capable and extended

Task 2

P3 Income statement on the basis Absorption costing and marginal costing.

Absorption costing: It is a managerial accounting cost of techniques of incurring each and every

costs associated with the manufacturing a specific goods and necessary for then GAAP outside

reporting.

Income statement on the basis of Absorption costing:

Particular Unit Per Unit cost Amount

sales 1500 35 $2500

-COGS

Direct Material 2000 8 -16000

Direct Labour 2000 5 -10000

Variable production

overhead

2000 2 -4000

Fixed Production

overhead

2000 5 -10000

Gross Profit 12500

-Admin and Selling

Fixed (100000*1) -10000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable 52500*15% -7875

Net Loss -5375

Marginal costing: it is an accounting system in which the variable cost which are incurring to

cost units and fixed costs of the period are set off in full and final settlement on behalf of average

contribution in the organisation.

Income statement on the basis of Marginal costing

Particular Unit Per Unit cost Amount

Sales 1500 35

-COGS

Direct Material 2000 8 -16000

Direct Labor 2000 5 -10000

Variable production

overhead

2000 2 -4000

Gross Profit 22500

-Admin and Selling

Fixed (10000*1) -10000

Variable 52500*15% -7875

Net Profit 4625

TASK 3

P4

(a) Different types of budget and their advantages and disadvantages

Financial plan is compelling methodology help to figure and settle on choices inside the

endeavour. In this viewpoint, business tasks of company can likewise increase different thoughts

which enhance money related position of spending program that is gets ready for arranging

technique. There are different sorts of spending plan can be set up that are clarifies under here:

5

Net Loss -5375

Marginal costing: it is an accounting system in which the variable cost which are incurring to

cost units and fixed costs of the period are set off in full and final settlement on behalf of average

contribution in the organisation.

Income statement on the basis of Marginal costing

Particular Unit Per Unit cost Amount

Sales 1500 35

-COGS

Direct Material 2000 8 -16000

Direct Labor 2000 5 -10000

Variable production

overhead

2000 2 -4000

Gross Profit 22500

-Admin and Selling

Fixed (10000*1) -10000

Variable 52500*15% -7875

Net Profit 4625

TASK 3

P4

(a) Different types of budget and their advantages and disadvantages

Financial plan is compelling methodology help to figure and settle on choices inside the

endeavour. In this viewpoint, business tasks of company can likewise increase different thoughts

which enhance money related position of spending program that is gets ready for arranging

technique. There are different sorts of spending plan can be set up that are clarifies under here:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed budget: It is a spending that does not change or flex when deals or some other

action increments or declines. A settled spending plan is likewise alluded to as a static

spending plan.

Flexible budget: It is a spending that alters or flexes for changes in the volume of action.

The adaptable spending plan is more advanced and valuable than a static spending plan,

which stays at one sum paying little respect to the volume of action.

Zero based budgeting: It is methods of budget plan from the initial level and all the past

data are not considering to make organisation budget. In other words it beginning from

the zero balance and the budget will be allocate on the basis of need for overall operation

in the firm.

Advantages of budget

The significant quality of planning is that it organizes exercises crosswise over divisions.

Budgets give a brilliant record of authoritative exercises.

Advantages of the Zero based Budgeting:

it is an easily modified budget as the finance will be allocated to the enterprises' operation

on the basis firm requirement.

The Budget is prepared on the zero basis for which will help to incurred less costs for the

firm.

Disadvantages of Zero bases budgeting:

it is a huge possibility of making wrong practice of the data or the budget need to the

organisation for short term period.

Incremental Budgeting: This are the techniques which will help to bring the manger and

accounting employees of entity evaluation the price occurred in the past year and prepare an

effective budge which shows a surplus fund to overall finance(Pimentel and Major, 2010). The

main advantages of the increment budget help to determine the price and make the funds for the

various activity. Further, it enables the ongoing enterprises to have a consistency increment in

activity also in searching out.

There are also disadvantages of the budget is the operation and the need of budge in all time,

hence, in several period it will require increasing the budget which are used in operation to

increase the manipulation of the capital.

Disadvantage of budget

6

action increments or declines. A settled spending plan is likewise alluded to as a static

spending plan.

Flexible budget: It is a spending that alters or flexes for changes in the volume of action.

The adaptable spending plan is more advanced and valuable than a static spending plan,

which stays at one sum paying little respect to the volume of action.

Zero based budgeting: It is methods of budget plan from the initial level and all the past

data are not considering to make organisation budget. In other words it beginning from

the zero balance and the budget will be allocate on the basis of need for overall operation

in the firm.

Advantages of budget

The significant quality of planning is that it organizes exercises crosswise over divisions.

Budgets give a brilliant record of authoritative exercises.

Advantages of the Zero based Budgeting:

it is an easily modified budget as the finance will be allocated to the enterprises' operation

on the basis firm requirement.

The Budget is prepared on the zero basis for which will help to incurred less costs for the

firm.

Disadvantages of Zero bases budgeting:

it is a huge possibility of making wrong practice of the data or the budget need to the

organisation for short term period.

Incremental Budgeting: This are the techniques which will help to bring the manger and

accounting employees of entity evaluation the price occurred in the past year and prepare an

effective budge which shows a surplus fund to overall finance(Pimentel and Major, 2010). The

main advantages of the increment budget help to determine the price and make the funds for the

various activity. Further, it enables the ongoing enterprises to have a consistency increment in

activity also in searching out.

There are also disadvantages of the budget is the operation and the need of budge in all time,

hence, in several period it will require increasing the budget which are used in operation to

increase the manipulation of the capital.

Disadvantage of budget

6

The significant issue happens when spending plans are connected mechanically and inflexibly.

Budgets can cause view of shamefulness.

A unbending spending structure decreases activity and development at bring down levels,

making it difficult to get cash for new thoughts.

(b) Process for preparing budget.

To set up the spending program, it is imperative to evaluate adequacy of the business in

deliberate way. It will help to develop tasks and capacities in fruitful way. With the assistance of

actualizing spending program organization can increase different advantages at working

environment. By having an effective development of diverse measures in context to the budget

preparation the overall development can be taken into account. Along with this, it has been

noticed that using diverse standards in terms of sustainability and financial planning need to be

referred by members(Ax, and Greve, 2017). Budgeting process is the way an association

approaches building its financial plan. A decent planning process draws in the individuals who

are in charge of holding fast to the financial plan and actualizing the association's targets in

making the financial plan. Planning choices are driven both by mission needs and monetary

responsibility. In addition to this, it can be said that process of budgeting involves number of

stages which need to be referred by management properly. Classification of stages can be as

follows:

Update budget assumptions

Review bottlenecks

Assess available fund

Creating budget packages

Obtain revenue and department budget.

c The significance of budget as tool for planning and control purposes.

Budget can be defined as quantitative statement for a defined period. It is the best control

process in the company which improves controlling process of working. Budget process controls

the revenue, expenses, assets, liabilities and cash flow. It makes good impression on the

behaviour of working process of the company. They are very useful resource to allocate the

resources in an effective process of working. It makes potential working staff which makes

7

Budgets can cause view of shamefulness.

A unbending spending structure decreases activity and development at bring down levels,

making it difficult to get cash for new thoughts.

(b) Process for preparing budget.

To set up the spending program, it is imperative to evaluate adequacy of the business in

deliberate way. It will help to develop tasks and capacities in fruitful way. With the assistance of

actualizing spending program organization can increase different advantages at working

environment. By having an effective development of diverse measures in context to the budget

preparation the overall development can be taken into account. Along with this, it has been

noticed that using diverse standards in terms of sustainability and financial planning need to be

referred by members(Ax, and Greve, 2017). Budgeting process is the way an association

approaches building its financial plan. A decent planning process draws in the individuals who

are in charge of holding fast to the financial plan and actualizing the association's targets in

making the financial plan. Planning choices are driven both by mission needs and monetary

responsibility. In addition to this, it can be said that process of budgeting involves number of

stages which need to be referred by management properly. Classification of stages can be as

follows:

Update budget assumptions

Review bottlenecks

Assess available fund

Creating budget packages

Obtain revenue and department budget.

c The significance of budget as tool for planning and control purposes.

Budget can be defined as quantitative statement for a defined period. It is the best control

process in the company which improves controlling process of working. Budget process controls

the revenue, expenses, assets, liabilities and cash flow. It makes good impression on the

behaviour of working process of the company. They are very useful resource to allocate the

resources in an effective process of working. It makes potential working staff which makes

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effective process. Budget helps to make the plan in advance manner on the basis of business

money plans and process. Following steps are helps in controlling process.

Planning: budget are the plans which pursued the period to attain certain objectives and task.

Budgetary control planning always take care of needs of planning process. This also helps to

force at all management.

Control: budgetary control the unnecessary activities in the organization which creates

unnecessary practices in the organization. It helps to bring the new ideas and use of productive

resources of management. It helps to control the and make the each department budget separately

which helps to make easier working process for the company.

Coordination: Budgetary involves in the participation of a master budget. Through which Tech

limited can easily work in coordinated manner(Renz and Herman, 2016). Budgetary helps to

make process easier and productive.

Increase in efficiency: Budgetary controls also helps to maintained the efficiency level of the

management. It helps to enhance the company advanced level. It also makes the impact decision

making process of working.

Financial planning: the most important term or plan is that to make financial planning for the

company betterment. It also very much essential process of working. Financial is the productive

process of working which helps to amend the impact decision making approach.

Task 4

P5. Balanced scorecard Approach

This could be regarded to as the most useful approach in order to identify and then

resolve the issue. Balanced scorecard is the performance metric which is been used by the

strategic management so that they could identify what is the problem and then make an effective

way out to solve that one. This is basically dealing with the internal functions of organisation

like that of finance or related to employees of company. So as Tech UK was having the loss of

about £1.5 million and their auditor showed them the path that with the use of this balanced score

card techniques they would be able to solve this problem in near future. The main purpose of this

plan is to enforce good behaviour into organisation by the analysing of four major area of

organisation(Otley, 2016). These areas are like that of business process, customers, learning and

growth of employees and then finance.

8

money plans and process. Following steps are helps in controlling process.

Planning: budget are the plans which pursued the period to attain certain objectives and task.

Budgetary control planning always take care of needs of planning process. This also helps to

force at all management.

Control: budgetary control the unnecessary activities in the organization which creates

unnecessary practices in the organization. It helps to bring the new ideas and use of productive

resources of management. It helps to control the and make the each department budget separately

which helps to make easier working process for the company.

Coordination: Budgetary involves in the participation of a master budget. Through which Tech

limited can easily work in coordinated manner(Renz and Herman, 2016). Budgetary helps to

make process easier and productive.

Increase in efficiency: Budgetary controls also helps to maintained the efficiency level of the

management. It helps to enhance the company advanced level. It also makes the impact decision

making process of working.

Financial planning: the most important term or plan is that to make financial planning for the

company betterment. It also very much essential process of working. Financial is the productive

process of working which helps to amend the impact decision making approach.

Task 4

P5. Balanced scorecard Approach

This could be regarded to as the most useful approach in order to identify and then

resolve the issue. Balanced scorecard is the performance metric which is been used by the

strategic management so that they could identify what is the problem and then make an effective

way out to solve that one. This is basically dealing with the internal functions of organisation

like that of finance or related to employees of company. So as Tech UK was having the loss of

about £1.5 million and their auditor showed them the path that with the use of this balanced score

card techniques they would be able to solve this problem in near future. The main purpose of this

plan is to enforce good behaviour into organisation by the analysing of four major area of

organisation(Otley, 2016). These areas are like that of business process, customers, learning and

growth of employees and then finance.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

But then the management analysed that implementation of this application which company

would be very much costly for the company as they would be needing many people and money

so that t hey could implement this. So team of management made out some more important and

differentiating way out with the use of which they could manage their money and use it

effectively.

Key performance indicators

These methods would b evaluating the success of company with the help of various techniques

like that of focusing on projects and products of company. This would be including that company

is using its best products and projects in order to showcase to others and then earning profits.

This is easy and cost effective so management of Tech UK could be implementing this and then

gaining out from this.

CONCLUSION

From the basis of above conclusion it can be concluded that management accounting is

the most crucial and important part of the organisation. It influences different managerial

practises. Moreover, present study based on accounting process Tech limited, study discussed

about the important method and process through which company can easily adopt effective

management skills. It also discussed about management accounting information as a decision

making tool for department managers, it also explained about inventory management system

which influence system and job costing system. Moreover, it summarized the process of working

of the company which highly influenced about the method through which company can easily

adopt the best possible action in terms of to manage good financial sources and sustain their

quality management. It also covered managerial accounting reports. On the basis of income

statement of the Tech (UK) Limited the firm required to control on their direct expenses and

required to focus on preparing a budget report so that organisation control their various

operational cost which are not necessary for them.

9

would be very much costly for the company as they would be needing many people and money

so that t hey could implement this. So team of management made out some more important and

differentiating way out with the use of which they could manage their money and use it

effectively.

Key performance indicators

These methods would b evaluating the success of company with the help of various techniques

like that of focusing on projects and products of company. This would be including that company

is using its best products and projects in order to showcase to others and then earning profits.

This is easy and cost effective so management of Tech UK could be implementing this and then

gaining out from this.

CONCLUSION

From the basis of above conclusion it can be concluded that management accounting is

the most crucial and important part of the organisation. It influences different managerial

practises. Moreover, present study based on accounting process Tech limited, study discussed

about the important method and process through which company can easily adopt effective

management skills. It also discussed about management accounting information as a decision

making tool for department managers, it also explained about inventory management system

which influence system and job costing system. Moreover, it summarized the process of working

of the company which highly influenced about the method through which company can easily

adopt the best possible action in terms of to manage good financial sources and sustain their

quality management. It also covered managerial accounting reports. On the basis of income

statement of the Tech (UK) Limited the firm required to control on their direct expenses and

required to focus on preparing a budget report so that organisation control their various

operational cost which are not necessary for them.

9

REFERENCES

Books and Journal

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34. pp.59-74.

Black, W. H., 2017. Book review: History of Management Accounting in Japan: Institutional &

Cultural Significance of Accounting.

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for corporate

practice. Journal of Cleaner Production. 152. pp.379-386.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Eldenburg, L. G. and et.al., 2016. Cost management: Measuring, monitoring, and motivating

performance. Wiley Global Education.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management. 32(7-8). pp.414-428.

Lock M.D. 2014, The essential of project management. Ashgate Publishing Ltd.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Pimentel, L. and Major, M. J., 2010. Management accounting change: a case study of Balanced

Scorecard implementation in a Portuguese service company. Contabilidade e Gestão:

Portuguese Journal of Accounting and Management. (8). pp.89-109.

Renz, D. O. and Herman, R. D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

10

Books and Journal

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34. pp.59-74.

Black, W. H., 2017. Book review: History of Management Accounting in Japan: Institutional &

Cultural Significance of Accounting.

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for corporate

practice. Journal of Cleaner Production. 152. pp.379-386.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Eldenburg, L. G. and et.al., 2016. Cost management: Measuring, monitoring, and motivating

performance. Wiley Global Education.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management. 32(7-8). pp.414-428.

Lock M.D. 2014, The essential of project management. Ashgate Publishing Ltd.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Pimentel, L. and Major, M. J., 2010. Management accounting change: a case study of Balanced

Scorecard implementation in a Portuguese service company. Contabilidade e Gestão:

Portuguese Journal of Accounting and Management. (8). pp.89-109.

Renz, D. O. and Herman, R. D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.