Management Accounting Report: Lion Hudson Plc's Financial Analysis

VerifiedAdded on 2021/02/20

|19

|5198

|21

Report

AI Summary

This report provides a detailed analysis of the management accounting system implemented by Lion Hudson Plc, a book publishing company. It explores the role and principles of management accounting, differentiating it from financial accounting. The report delves into various management accounting systems used by the company, including inventory management, cost accounting, job costing, and price optimization systems, highlighting their advantages and disadvantages. It emphasizes the characteristics of a good management accounting system, such as accuracy, reliability, and timeliness. Furthermore, the report examines management accounting reporting, including inventory management reports, accounts receivable aging reports, and performance reports. It also covers different management accounting techniques like cost-volume-profit analysis, flexible budgeting, and cost variances, along with a discussion of absorption and marginal costing. The report includes profit and cost calculations using these techniques, providing a comprehensive overview of Lion Hudson Plc's financial management practices. This report is contributed to Desklib, a platform offering AI-based study tools for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Characteristics of good Management accounting System:..........................................................3

TASK 2............................................................................................................................................4

Profit and cost calculation by different management accounting techniques:.............................6

TASK 3 ...........................................................................................................................................9

Planning tools used for budgetary control:..................................................................................9

TASK 4..........................................................................................................................................13

Management accounting systems used to identify financial problems:.....................................13

CONCLUSION..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Characteristics of good Management accounting System:..........................................................3

TASK 2............................................................................................................................................4

Profit and cost calculation by different management accounting techniques:.............................6

TASK 3 ...........................................................................................................................................9

Planning tools used for budgetary control:..................................................................................9

TASK 4..........................................................................................................................................13

Management accounting systems used to identify financial problems:.....................................13

CONCLUSION..............................................................................................................................15

INTRODUCTION

In today's business environment, management accounting plays a key role in creating

plans and hence it is crucial for management personnels in the organization that they must have

efficient knowledge of creating and using management accounting subject matter. Now a days,

businessmen want to track execution of information that goes beyond just the cost and profit

information provided by traditional financial accounting information thus management

accounting system has been evolved (Management accounting, 2019).

For the better understanding of managerial accounting system, a trainee management

accountant of Cogneesol limited is presenting report on the management accounting system of

Lion Hudson Plc which is a book publisher company deriving its business in Oxford, UK since

2003 by the merger of Lion Publishing and Hudson International.

This report covers detailed information about management accounting system, different

types of reporting that help in dealing with various financial problems. In this report several

costing techniques are used to calculate net profit for the year. In Addition, advantages and

disadvantages of planning tool and benefits of management accounting in are defined in detail.

TASK 1

Management Accounting and its systems:

Management Accounting: Managerial accounting can be defined as the tools and

techniques that prepare and present available data and information in such a professional way

that it may help the management in order to make its planning and decisions in an effective

manner so that efficiency and performance can be attempt at its fullest (Abbasi, Zamani and

Valmohammadi, 2014).

Origin, Role and Principles of Management Accounting: At the beginning of

nineteenth century, big private organizations felt the necessity of a procedure that can

effectively measure and control over internal production centres in order to survive in

economy. Managerial accounting plays a crucial role in managing and operating internal

activities of an organization. This process focus on four main principles which are influence,

relevancy, worth and creditability.

Difference between Financial and Managerial Accounting:

Aspects Financial Accounting Management Accounting

1

In today's business environment, management accounting plays a key role in creating

plans and hence it is crucial for management personnels in the organization that they must have

efficient knowledge of creating and using management accounting subject matter. Now a days,

businessmen want to track execution of information that goes beyond just the cost and profit

information provided by traditional financial accounting information thus management

accounting system has been evolved (Management accounting, 2019).

For the better understanding of managerial accounting system, a trainee management

accountant of Cogneesol limited is presenting report on the management accounting system of

Lion Hudson Plc which is a book publisher company deriving its business in Oxford, UK since

2003 by the merger of Lion Publishing and Hudson International.

This report covers detailed information about management accounting system, different

types of reporting that help in dealing with various financial problems. In this report several

costing techniques are used to calculate net profit for the year. In Addition, advantages and

disadvantages of planning tool and benefits of management accounting in are defined in detail.

TASK 1

Management Accounting and its systems:

Management Accounting: Managerial accounting can be defined as the tools and

techniques that prepare and present available data and information in such a professional way

that it may help the management in order to make its planning and decisions in an effective

manner so that efficiency and performance can be attempt at its fullest (Abbasi, Zamani and

Valmohammadi, 2014).

Origin, Role and Principles of Management Accounting: At the beginning of

nineteenth century, big private organizations felt the necessity of a procedure that can

effectively measure and control over internal production centres in order to survive in

economy. Managerial accounting plays a crucial role in managing and operating internal

activities of an organization. This process focus on four main principles which are influence,

relevancy, worth and creditability.

Difference between Financial and Managerial Accounting:

Aspects Financial Accounting Management Accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

User Financial accounts are prepared to

provide information to external

stakeholders.

Managerial accounts are creates to help

the internal users, specially

management.

Format An specific formate provides by the

governance is followed in preparation

of these statements.

These statements are not mandatory to

be prepared hence haven't any

particular format.

Data This approach only covers funds and

money related data and information.

Monetary as well as non-monetary

material is included in this accounting

process.

Management Accounting System: Management accounting system is a process of

collecting, classifying, recording, summarising and presenting financial and non-financial

meaningful content in order to help the administration in determining, planning and organising

its policies and procedures (Alawattage, Wickramasingh and Uddin, 2017). Each and every

material statement is prepared in Lion Hudson Plc so that the management can estimate

budgets properly and make decisions accordingly. Various has been adopted by respective firm

which are described as under:

Inventory Management System: It is the most essential system for an retailer company

as inventory is the main source of revenue in such firms. This system helps to keep a record of

products, company holds during a particular time period, estimate required raw material,

materials tracking, automated reordering etc. In respective firm, managers use this system to

keep a adequate record from purchase of raw material to warehousing of finished goods. This

helps them to order goods accordingly.

Advantages: It escalate the efficiency in administration and save space, money and time.

Disadvantage: The items cannot be grouped and ordered at a time.

Cost Accounting System: It has been found that in order to effectively producing profit

from business activities, it is required to know the cost allocated with the specific activity. It

includes events founded on accepting, recording, analysing, grouping and summarizing costs

related with valuable goods and services (Barnard and Mostert, 2015). In Lion Hudson Plc,

2

provide information to external

stakeholders.

Managerial accounts are creates to help

the internal users, specially

management.

Format An specific formate provides by the

governance is followed in preparation

of these statements.

These statements are not mandatory to

be prepared hence haven't any

particular format.

Data This approach only covers funds and

money related data and information.

Monetary as well as non-monetary

material is included in this accounting

process.

Management Accounting System: Management accounting system is a process of

collecting, classifying, recording, summarising and presenting financial and non-financial

meaningful content in order to help the administration in determining, planning and organising

its policies and procedures (Alawattage, Wickramasingh and Uddin, 2017). Each and every

material statement is prepared in Lion Hudson Plc so that the management can estimate

budgets properly and make decisions accordingly. Various has been adopted by respective firm

which are described as under:

Inventory Management System: It is the most essential system for an retailer company

as inventory is the main source of revenue in such firms. This system helps to keep a record of

products, company holds during a particular time period, estimate required raw material,

materials tracking, automated reordering etc. In respective firm, managers use this system to

keep a adequate record from purchase of raw material to warehousing of finished goods. This

helps them to order goods accordingly.

Advantages: It escalate the efficiency in administration and save space, money and time.

Disadvantage: The items cannot be grouped and ordered at a time.

Cost Accounting System: It has been found that in order to effectively producing profit

from business activities, it is required to know the cost allocated with the specific activity. It

includes events founded on accepting, recording, analysing, grouping and summarizing costs

related with valuable goods and services (Barnard and Mostert, 2015). In Lion Hudson Plc,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost accounting system is useful to compute the cost included in running various production

operation, cost incurred of manpower and other assorted cost.

Advantages: It ascertain the cost of every product of company and modify price to increase

quality.

Disadvantage: It uses previous data to make future decisions which is irrelevant.

Job Costing Systems: Job costing system is evolve to calculate the cost of particular

task or unit. This system is beneficial to determine the expenditures related with specific job

involved in production activity and other division. Selected organization creates job costing

system to find out the cost of specific inventory which immediately send to the customer with

evaluating in inventory management or cost accounting systems.

Advantages: It gives advantage of being able to keep track of individuals' and teams'

performance.

Disadvantage: A lot of paper work take place in this costing system.

Price Optimisation System: Price optimisation system is a mathematical tool that aids

in analysing the perception and behaviour of customers regarding the prices of various products

in different markets. With the help of this method, a cost module as well as price module is

generated Further a set of optimum price is generated according to the minimum cost with

maximum profit margin combination. Respective firm opt this system to fix the best price in

order to provide optimum customer satisfaction.

Advantages: The managers are capable in improving operational profits while keeping

optimum prices.

Disadvantage: Both good and bad products may be sold at the same time.

Characteristics of good Management accounting System:

Accuracy: The accounting system should include all the substantial content and factors

so that it can help in making effectual decision.

Reliability: The information rendered by the system must be trustworthy and

conformable. Specious or inadequate accounting system can cause weak determination in

planning.

Up-to-date: Managerial accounting system must comply with updates in policies and

informations on time to time so that effective decisions may be taken on time.

3

operation, cost incurred of manpower and other assorted cost.

Advantages: It ascertain the cost of every product of company and modify price to increase

quality.

Disadvantage: It uses previous data to make future decisions which is irrelevant.

Job Costing Systems: Job costing system is evolve to calculate the cost of particular

task or unit. This system is beneficial to determine the expenditures related with specific job

involved in production activity and other division. Selected organization creates job costing

system to find out the cost of specific inventory which immediately send to the customer with

evaluating in inventory management or cost accounting systems.

Advantages: It gives advantage of being able to keep track of individuals' and teams'

performance.

Disadvantage: A lot of paper work take place in this costing system.

Price Optimisation System: Price optimisation system is a mathematical tool that aids

in analysing the perception and behaviour of customers regarding the prices of various products

in different markets. With the help of this method, a cost module as well as price module is

generated Further a set of optimum price is generated according to the minimum cost with

maximum profit margin combination. Respective firm opt this system to fix the best price in

order to provide optimum customer satisfaction.

Advantages: The managers are capable in improving operational profits while keeping

optimum prices.

Disadvantage: Both good and bad products may be sold at the same time.

Characteristics of good Management accounting System:

Accuracy: The accounting system should include all the substantial content and factors

so that it can help in making effectual decision.

Reliability: The information rendered by the system must be trustworthy and

conformable. Specious or inadequate accounting system can cause weak determination in

planning.

Up-to-date: Managerial accounting system must comply with updates in policies and

informations on time to time so that effective decisions may be taken on time.

3

Management accounting is used to help the management in examining and performing

day to day functions in organization and planning & making decisions for upcoming period of

time. It is important for the management accounting system to be effective and understandable

so that these planning and procedures may work impressively (Cassell, Myers and Seidel,

2015).

Management Accounting Reporting: It is expressed as process of reporting where

various types of reports are prepared by managers to get an estimate of costs, incomes and

expenses for an accounting period. With help of this reporting process, management can

evaluate the performance of employees. Lion Hudson Plc keeps an idea about performance of

activities functioning in the firm and take remedial actions in order to eliminate variances with

help of management accounting reporting.

Inventory Management Report: This report is very important for company as it helps

to maintain inventory hold during a year. It covers essential detail from purchase raw material

to finished products ready for sales. In this context of client company managers are required to

maintain a proper record of available raw material, goods that are already in transit and actual

goods in warehouses. Inventory management report provides information about quality and

costs of the products. It also helps in opting correct method for valuation of goods and

products.

Accounts receivable aging report: Receivables are the expected payments due from the

customers or retailers. Accounts receivable ageing report is a list of unpaid customers of

respective firm that provides necessary informations about sum of amount due from the

customers, over due receivables' dates, interest on due amount, contact details of creditors and

other important details regarding payments from the customers of selected organization. They

are required to control liquidity position and strong credit policies of a company (Cattarino and

others, 2016).

Performance report: It is a detailed statement that includes performance based

appraisals to staff so that they may get motivated and work productively. A company can grow

by rewarding over achievers while lading off under performers. With the help of performance

report, selected organization provides bonus as well as training sessions to the people working

at the end of accounting period by evaluating their overall performance.

4

day to day functions in organization and planning & making decisions for upcoming period of

time. It is important for the management accounting system to be effective and understandable

so that these planning and procedures may work impressively (Cassell, Myers and Seidel,

2015).

Management Accounting Reporting: It is expressed as process of reporting where

various types of reports are prepared by managers to get an estimate of costs, incomes and

expenses for an accounting period. With help of this reporting process, management can

evaluate the performance of employees. Lion Hudson Plc keeps an idea about performance of

activities functioning in the firm and take remedial actions in order to eliminate variances with

help of management accounting reporting.

Inventory Management Report: This report is very important for company as it helps

to maintain inventory hold during a year. It covers essential detail from purchase raw material

to finished products ready for sales. In this context of client company managers are required to

maintain a proper record of available raw material, goods that are already in transit and actual

goods in warehouses. Inventory management report provides information about quality and

costs of the products. It also helps in opting correct method for valuation of goods and

products.

Accounts receivable aging report: Receivables are the expected payments due from the

customers or retailers. Accounts receivable ageing report is a list of unpaid customers of

respective firm that provides necessary informations about sum of amount due from the

customers, over due receivables' dates, interest on due amount, contact details of creditors and

other important details regarding payments from the customers of selected organization. They

are required to control liquidity position and strong credit policies of a company (Cattarino and

others, 2016).

Performance report: It is a detailed statement that includes performance based

appraisals to staff so that they may get motivated and work productively. A company can grow

by rewarding over achievers while lading off under performers. With the help of performance

report, selected organization provides bonus as well as training sessions to the people working

at the end of accounting period by evaluating their overall performance.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Management Accounting Techniques:

Cost is a monetary value which a company like Lion Hudson Plc spends in order to

produce something valuable such as inventory. Cost analysis refers to measure of cost which is

incurred in different production process. There are different cost which are incurred. Some of

these are as follows:

Direct costs: These are costs which can be easily identify in production of a particular

product of a manufacturing company. For example, raw material cost, labour cost etc.

Indirect Costs: These are costs which can not be identify in production of a particular

product. For example, electricity expenses, depreciation etc.

Cost volume Profit: CVP analysis is used to decide how changes in costs and volume

affects a company's operating income and net income. In doing this analysis, various analysis

is used by the company like sales per unit and variable price per unit should be constant.

Flexible Budgeting: Flexible budget is used when company is unable to predict its

future level of production. In this case, company prepare budget for future period for more than

one production volumes so that it help the company to adopt appropriate budgeted volume.

Cost variances: It refers to difference between the actual cost figure with estimated

standard cost figures. For example, material cost variances, labour efficiency variances etc.

Absorption costing: It is an technique of management accounting which is used by

companies in allocation of all the cost either relevant or irrelevant (fixed cost). Under

absorption technique, All fixed costs are absorbed by a fixed recovery rate (Chen, Cheng and

Wang, 2015).

Marginal costing: This technique is used by the enterprises in order to find out the

break even point so that required stock of inventory and desired profit can be derived.

Fixed costs: These are costs which are remain same irrespective of its volume of

production. It may either be incurred in past or will be incurred in future but obligation of

which is determined in past. For example, rent expense, supervisory salary etc.

Variable costs: These are costs which are always relevant in all alternative course of

action and it increases in total with increase in volume of production. Though per unit cost is

remain same irrespective of its volume of production. For example, variable overhead, labour

cost etc.

5

Management Accounting Techniques:

Cost is a monetary value which a company like Lion Hudson Plc spends in order to

produce something valuable such as inventory. Cost analysis refers to measure of cost which is

incurred in different production process. There are different cost which are incurred. Some of

these are as follows:

Direct costs: These are costs which can be easily identify in production of a particular

product of a manufacturing company. For example, raw material cost, labour cost etc.

Indirect Costs: These are costs which can not be identify in production of a particular

product. For example, electricity expenses, depreciation etc.

Cost volume Profit: CVP analysis is used to decide how changes in costs and volume

affects a company's operating income and net income. In doing this analysis, various analysis

is used by the company like sales per unit and variable price per unit should be constant.

Flexible Budgeting: Flexible budget is used when company is unable to predict its

future level of production. In this case, company prepare budget for future period for more than

one production volumes so that it help the company to adopt appropriate budgeted volume.

Cost variances: It refers to difference between the actual cost figure with estimated

standard cost figures. For example, material cost variances, labour efficiency variances etc.

Absorption costing: It is an technique of management accounting which is used by

companies in allocation of all the cost either relevant or irrelevant (fixed cost). Under

absorption technique, All fixed costs are absorbed by a fixed recovery rate (Chen, Cheng and

Wang, 2015).

Marginal costing: This technique is used by the enterprises in order to find out the

break even point so that required stock of inventory and desired profit can be derived.

Fixed costs: These are costs which are remain same irrespective of its volume of

production. It may either be incurred in past or will be incurred in future but obligation of

which is determined in past. For example, rent expense, supervisory salary etc.

Variable costs: These are costs which are always relevant in all alternative course of

action and it increases in total with increase in volume of production. Though per unit cost is

remain same irrespective of its volume of production. For example, variable overhead, labour

cost etc.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost allocation: It is a process in which cost is identified and allotted the cost to cost

objects. For example, a product, a sales region etc.

Normal costing: It is a method of costing that is used in cost derivation. It is consist of

actual cost of material, actual cost of direct labour and absorbed overhead based on recovery

rate.

Standard costing: It is another technique of cost accounting in which management

compares the actual cost which standard cost figures to identify the weaknesses in production

process.

Activity based costing: It is another method that helps the Lion Hudson Plc in

identifying the different activities which are responsible for incurring the costs. These fixed

cost are then assigned to its various product line according to activities involves in these

product lines.

Inventory cost: This cost is associated with the inventory of the company such as

purchase cost inventory storage cost etc. If company tries to cut down the inventory cost then it

can help it in reducing its product cost. Inventory valuation methods are LIFO (Last in first

out), FIFO (First in first out) and weighted average method.

Overhead cost: It is a cost which is incurred indirectly in production process i.e. can

not be identified in a specific product.

Profit and cost calculation by different management accounting techniques:

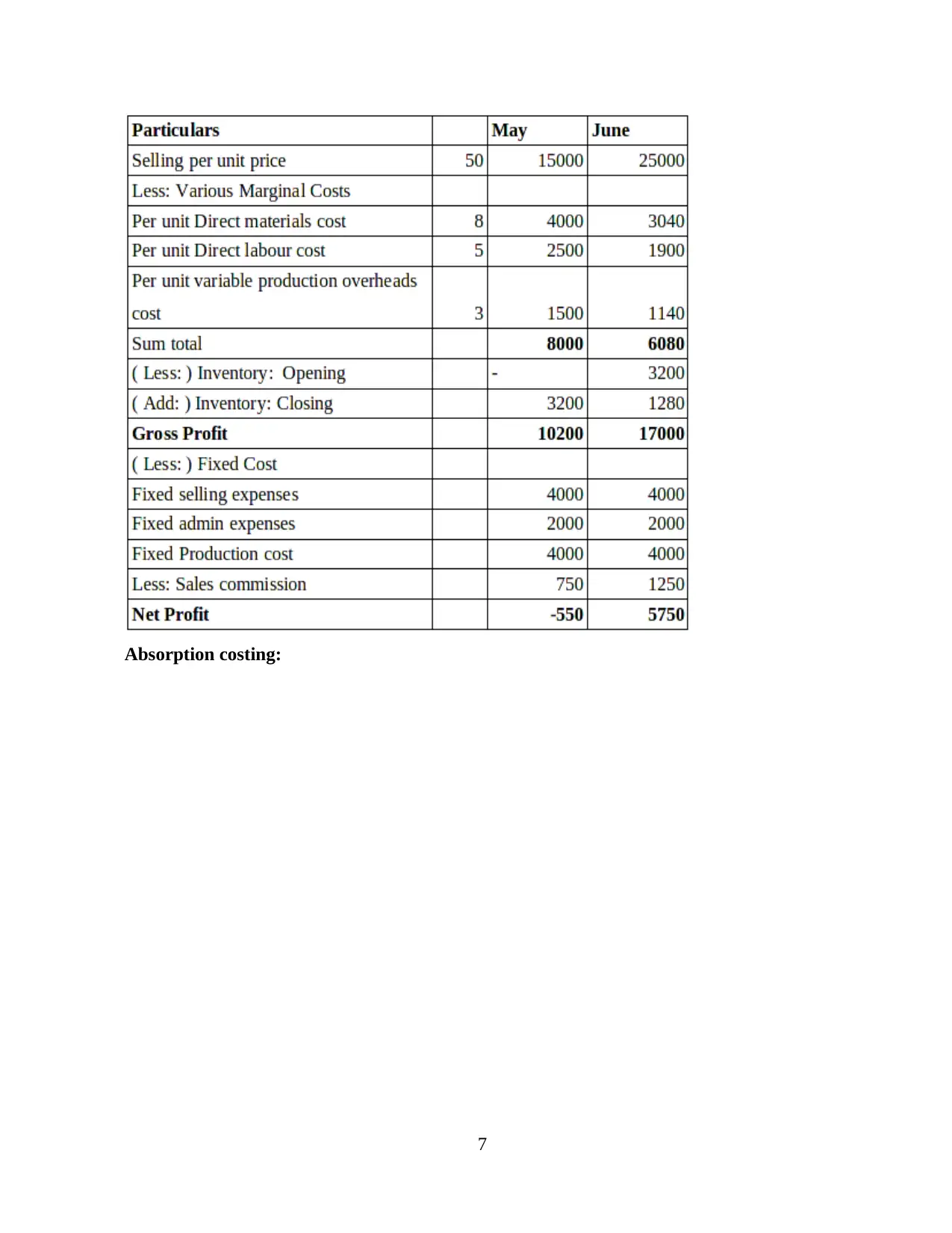

Marginal costing:

6

objects. For example, a product, a sales region etc.

Normal costing: It is a method of costing that is used in cost derivation. It is consist of

actual cost of material, actual cost of direct labour and absorbed overhead based on recovery

rate.

Standard costing: It is another technique of cost accounting in which management

compares the actual cost which standard cost figures to identify the weaknesses in production

process.

Activity based costing: It is another method that helps the Lion Hudson Plc in

identifying the different activities which are responsible for incurring the costs. These fixed

cost are then assigned to its various product line according to activities involves in these

product lines.

Inventory cost: This cost is associated with the inventory of the company such as

purchase cost inventory storage cost etc. If company tries to cut down the inventory cost then it

can help it in reducing its product cost. Inventory valuation methods are LIFO (Last in first

out), FIFO (First in first out) and weighted average method.

Overhead cost: It is a cost which is incurred indirectly in production process i.e. can

not be identified in a specific product.

Profit and cost calculation by different management accounting techniques:

Marginal costing:

6

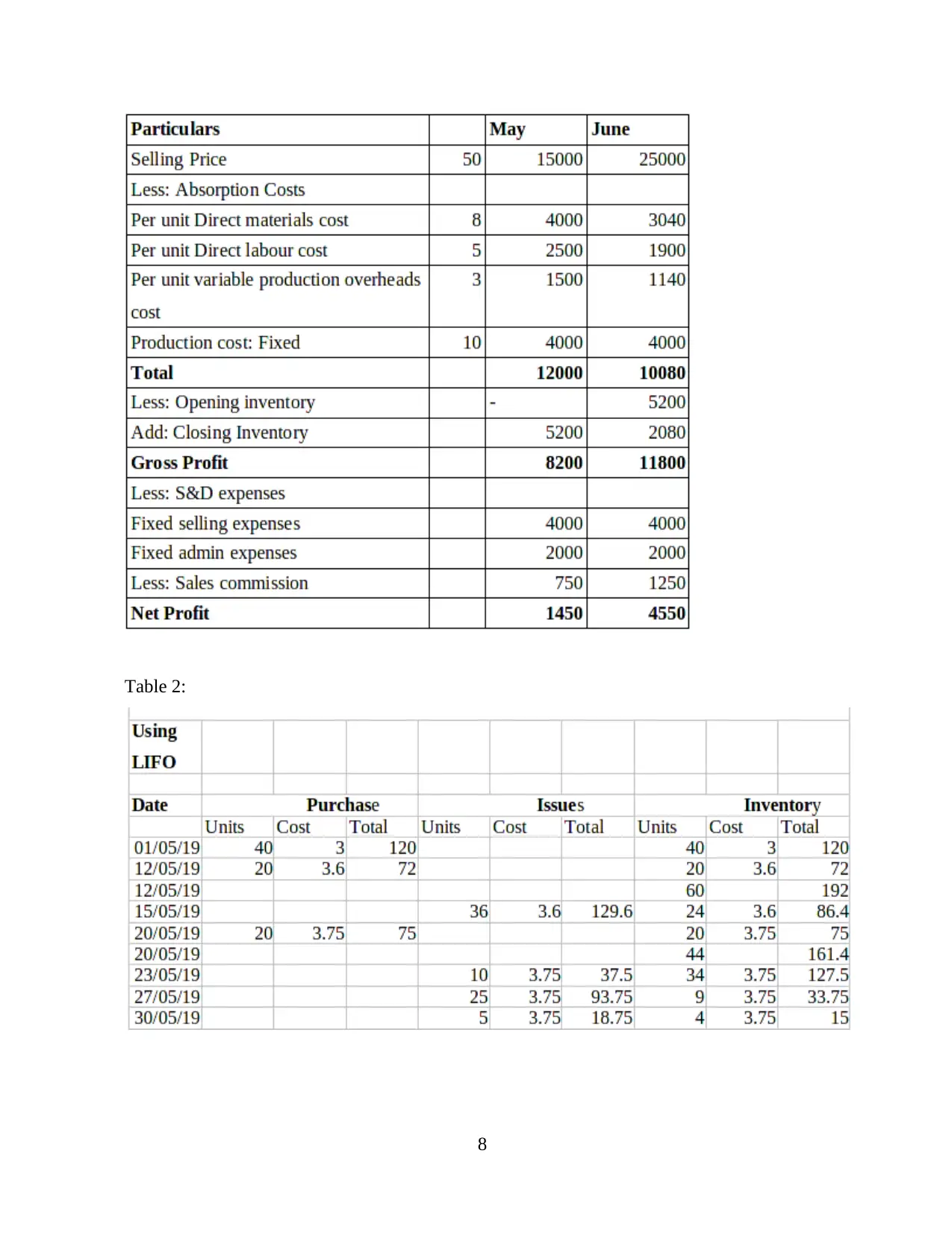

Absorption costing:

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table 2:

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

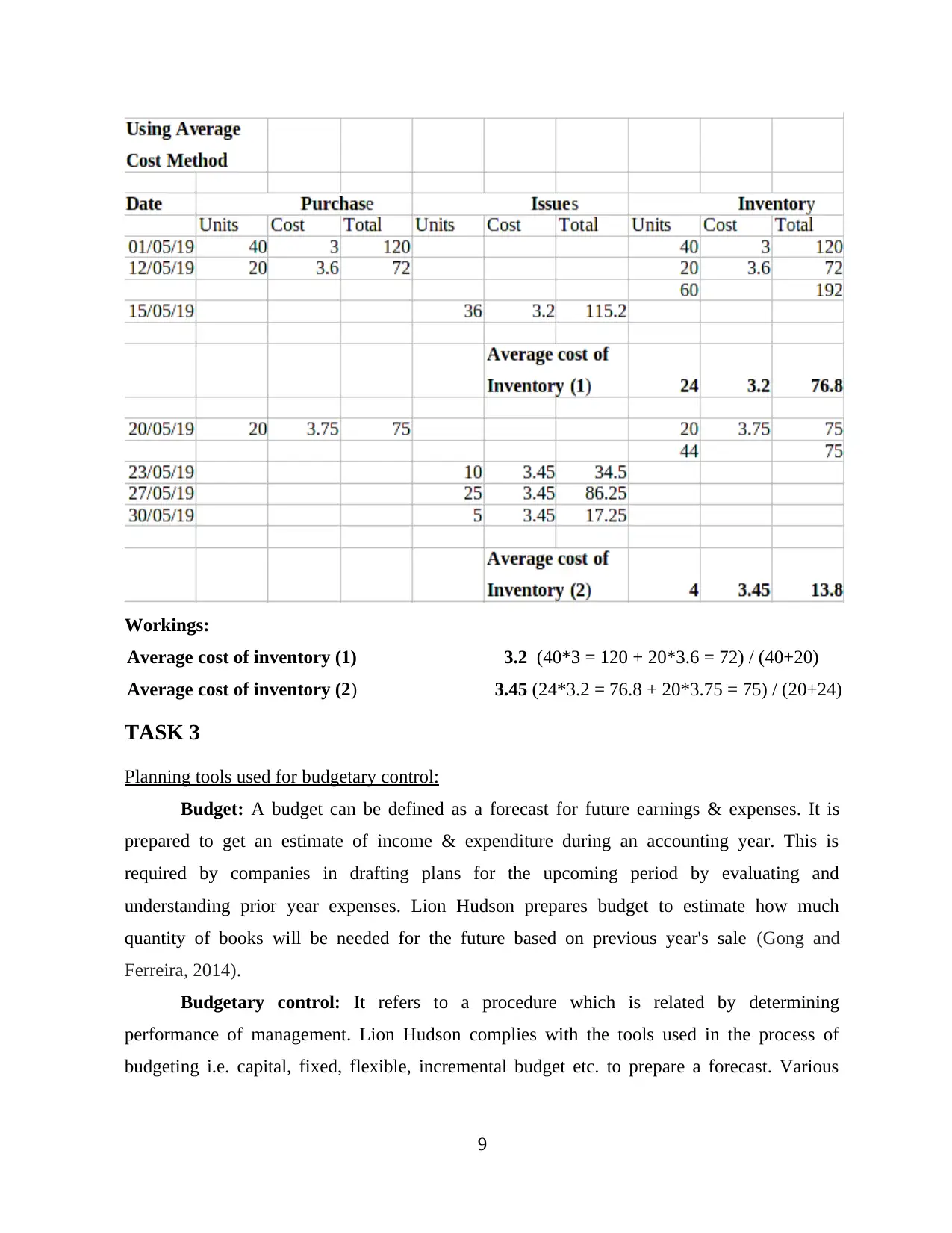

Workings:

Average cost of inventory (1) 3.2 (40*3 = 120 + 20*3.6 = 72) / (40+20)

Average cost of inventory (2) 3.45 (24*3.2 = 76.8 + 20*3.75 = 75) / (20+24)

TASK 3

Planning tools used for budgetary control:

Budget: A budget can be defined as a forecast for future earnings & expenses. It is

prepared to get an estimate of income & expenditure during an accounting year. This is

required by companies in drafting plans for the upcoming period by evaluating and

understanding prior year expenses. Lion Hudson prepares budget to estimate how much

quantity of books will be needed for the future based on previous year's sale (Gong and

Ferreira, 2014).

Budgetary control: It refers to a procedure which is related by determining

performance of management. Lion Hudson complies with the tools used in the process of

budgeting i.e. capital, fixed, flexible, incremental budget etc. to prepare a forecast. Various

9

Average cost of inventory (1) 3.2 (40*3 = 120 + 20*3.6 = 72) / (40+20)

Average cost of inventory (2) 3.45 (24*3.2 = 76.8 + 20*3.75 = 75) / (20+24)

TASK 3

Planning tools used for budgetary control:

Budget: A budget can be defined as a forecast for future earnings & expenses. It is

prepared to get an estimate of income & expenditure during an accounting year. This is

required by companies in drafting plans for the upcoming period by evaluating and

understanding prior year expenses. Lion Hudson prepares budget to estimate how much

quantity of books will be needed for the future based on previous year's sale (Gong and

Ferreira, 2014).

Budgetary control: It refers to a procedure which is related by determining

performance of management. Lion Hudson complies with the tools used in the process of

budgeting i.e. capital, fixed, flexible, incremental budget etc. to prepare a forecast. Various

9

monetary as well as non-monetary targets are assigned to managers in order to achieve success

by following organisational objectives.

The process of budgeting involves certain steps to be followed that include identifying

business objectives, potential strategies, choosing alternative course of action, implementing

long-term plan, measurement of actual results with budgeted figures, preparing a draft and

getting it checked by the higher authorities i.e. board of directors.

Different types of budget: There are different types of budgetary techniques implied

by business enterprises which are mentioned below:

Capital budget: This is a budget which is used to ascertain how much funding is

required by an organisation to perform its long term investments which include purchase of

machinery, research & development projects, new products etc. It consists of capital receipts

and payments that are used in a business on a day-to-day basis (Guffey and Harp, 2016). This

budget is prepared by Lion Hudson with the help of various capital budgeting techniques like

internal rate of return, net present value, payback period etc. which help the company to

analyse position of their earnings.

Advantages:

It helps in decision making of any investment opportunities that may arise in a business

by using NPV, IRR, ARR etc. Lion Hudson calculates its cash flows with the help of

capital budgeting techniques.

Disadvantages:

It leads to uncertain risks and incorrect applicability of resources if any wrong

budgeting technique is used.

Operating Budget: It involves a detailed projection of income and expenditure which

are based on forecasted revenue during a period of time. This is a statement that involves

estimation of all expenses which are used on a daily basis by following operations of a

business. It is a short term budget which excludes the effect of capital payment as they are

long-term costs. Lion Hudson prepared operating budget by keeping a track over its earnings

and expenditure.

Advantages:

10

by following organisational objectives.

The process of budgeting involves certain steps to be followed that include identifying

business objectives, potential strategies, choosing alternative course of action, implementing

long-term plan, measurement of actual results with budgeted figures, preparing a draft and

getting it checked by the higher authorities i.e. board of directors.

Different types of budget: There are different types of budgetary techniques implied

by business enterprises which are mentioned below:

Capital budget: This is a budget which is used to ascertain how much funding is

required by an organisation to perform its long term investments which include purchase of

machinery, research & development projects, new products etc. It consists of capital receipts

and payments that are used in a business on a day-to-day basis (Guffey and Harp, 2016). This

budget is prepared by Lion Hudson with the help of various capital budgeting techniques like

internal rate of return, net present value, payback period etc. which help the company to

analyse position of their earnings.

Advantages:

It helps in decision making of any investment opportunities that may arise in a business

by using NPV, IRR, ARR etc. Lion Hudson calculates its cash flows with the help of

capital budgeting techniques.

Disadvantages:

It leads to uncertain risks and incorrect applicability of resources if any wrong

budgeting technique is used.

Operating Budget: It involves a detailed projection of income and expenditure which

are based on forecasted revenue during a period of time. This is a statement that involves

estimation of all expenses which are used on a daily basis by following operations of a

business. It is a short term budget which excludes the effect of capital payment as they are

long-term costs. Lion Hudson prepared operating budget by keeping a track over its earnings

and expenditure.

Advantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.