Management Accounting Report: Tuffen Mark Ltd. Analysis and Strategies

VerifiedAdded on 2020/12/09

|13

|3039

|274

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Tuffen Mark Ltd., a small family company involved in the design, manufacture, and sale of air ventilation systems. The report begins with an introduction to management accounting and its various systems, including cost accounting, inventory management, job costing, and price optimizing systems. It then explores different methods used for management accounting reporting, such as budgets, variance analysis, profit and loss statements, and cash flow analysis. The core of the report involves calculating costs using both absorption and marginal costing methods, followed by the preparation of income statements based on budgeted results. Furthermore, it evaluates the advantages and disadvantages of various planning tools employed for budgetary control, including scenario and forecasting tools. Finally, the report addresses the adaptation of the management accounting system to respond to financial problems, providing a holistic view of financial management within the company.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1.Management accounting and different types of management accounting system............3

P2.Different methods used for management accounting reporting........................................4

TASK 2............................................................................................................................................5

P3.Calculation of cost and preparation of income statements................................................5

TASK 3............................................................................................................................................7

P4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................7

TASK 4............................................................................................................................................9

P5.Adaption of management accounting system to respond to financial problems...............9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1.Management accounting and different types of management accounting system............3

P2.Different methods used for management accounting reporting........................................4

TASK 2............................................................................................................................................5

P3.Calculation of cost and preparation of income statements................................................5

TASK 3............................................................................................................................................7

P4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................7

TASK 4............................................................................................................................................9

P5.Adaption of management accounting system to respond to financial problems...............9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the methods to examine the costs of business and operations

to prepare internal financial accounts, reports and records that assist managers in process of

decision making for accomplishing the organisational objectives (Bagautdinova, Kundakchyan

and Malakhov, 2013). For this report the chosen organisation is Tuffen Mark Ltd which is a

small family company. It deals with the sells, designs and manufactures air ventilation system in

UK market. In this report, management accounting and different types of management

accounting system. Various methods used for management accounting reporting are mentioned.

Calculation of cost and preparation of income system using marginal and absorption costing.

Advantages and disadvantages of various types of planning tools. Along with this management

accounting system responds to financial problems are also mentioned in this report.

TASK 1

P1.Management accounting and different types of management accounting system.

Management accounting is a activity of investigation, presentation and interpretation of

accounting data gathered by using cost-accounting and financial accounting so that it help

management in decision making, formulating policies and regular operations of company.

Management accounting system is a confidential internal reports which assist managers to make

decisions. Assistant Management Accountant of Tuffen Mark Ltd. used management accounting

system to prepare management accounts and reports which facilitate actual financial and non-

financial data to managers in making decisions for short-term and long term. Some various types

of management accounting system that is applied by Assistant Management Accountant of

Tuffen Mark Ltd. Are mentioned below:

Cost accounting system:

Cost accounting system is a structure which is utilised by company to compute the

product costs to analyse the profit, valuation of inventory and control of cost (Barnabè and

Busco, 2012). Essential requirement of cost accounting system to Tuffen Mark Ltd. is to used

this system in decisions making related to costs and also to identify manageable ratio or area that

need to be develop so that cost can be controlled.

Inventory management system:

Management accounting is the methods to examine the costs of business and operations

to prepare internal financial accounts, reports and records that assist managers in process of

decision making for accomplishing the organisational objectives (Bagautdinova, Kundakchyan

and Malakhov, 2013). For this report the chosen organisation is Tuffen Mark Ltd which is a

small family company. It deals with the sells, designs and manufactures air ventilation system in

UK market. In this report, management accounting and different types of management

accounting system. Various methods used for management accounting reporting are mentioned.

Calculation of cost and preparation of income system using marginal and absorption costing.

Advantages and disadvantages of various types of planning tools. Along with this management

accounting system responds to financial problems are also mentioned in this report.

TASK 1

P1.Management accounting and different types of management accounting system.

Management accounting is a activity of investigation, presentation and interpretation of

accounting data gathered by using cost-accounting and financial accounting so that it help

management in decision making, formulating policies and regular operations of company.

Management accounting system is a confidential internal reports which assist managers to make

decisions. Assistant Management Accountant of Tuffen Mark Ltd. used management accounting

system to prepare management accounts and reports which facilitate actual financial and non-

financial data to managers in making decisions for short-term and long term. Some various types

of management accounting system that is applied by Assistant Management Accountant of

Tuffen Mark Ltd. Are mentioned below:

Cost accounting system:

Cost accounting system is a structure which is utilised by company to compute the

product costs to analyse the profit, valuation of inventory and control of cost (Barnabè and

Busco, 2012). Essential requirement of cost accounting system to Tuffen Mark Ltd. is to used

this system in decisions making related to costs and also to identify manageable ratio or area that

need to be develop so that cost can be controlled.

Inventory management system:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system is a accumulation of technology and method which

oversees to supervise and maintain the stocked goods either that products are raw materials,

supplies, finished products and assets of company. The essential requirement of inventory

management system in Tuffen Mark Ltd. Is for maintaining records of each products and assets

that help to control company inventory effectively and efficiently. For example: FIFO is First In

First Out, it is a assumptions of cash flow that are utilise to remove cost from stock accounts.

LIFO is Last In First Out, this is applied for cost of inventory where recent items are produced

that to be recorded as sold first. AVCO is calculated by dividing inventory cost of goods sold by

goods numbers at any time.

Job costing system:

Job costing system is a method used to combine data regarding cost related with

particular production and job service (Ji, 2017). The essential requirement of job cost accounting

system to Tuffen Mark Ltd is to assign the cost of inventory of each producing products. Also to

check either manufacturing cost exceeds the materials price and overheads this help them to

facilitate profitability for overall process.

Price optimising system:

Price optimising system is a analysis to ascertain that how consumers will react to various

prices for their services and goods through by using different channels. Price optimising system

is essential for Tuffen Mark Ltd as it is used to ascertain prices that will decide by them to attain

their goals like increasing operating profitability.

All the above systems of management accounting helps Assistant Management

Accountant of Tuffen Mark Ltd. To prepare internal reports that are useful for the growth of

company.

P2.Different methods used for management accounting reporting.

Management accounting reports are used to modify, execute, prepare and measure the

performance. This reports is perpetual returns at the time of accounting periods and bookkeeping

as per the requirements (Bennett and James, 2017). Assistant Management Accountant of Tuffen

Mark Ltd prepare this reports to get information that are required to reduce cost, rewards given

for good performance and find out the products which provides good financial returns for their

businesses. The various methods that are used by Assistant Management Accountant of Tuffen

Mark Ltd. For management accounting reports are explained below:

5

oversees to supervise and maintain the stocked goods either that products are raw materials,

supplies, finished products and assets of company. The essential requirement of inventory

management system in Tuffen Mark Ltd. Is for maintaining records of each products and assets

that help to control company inventory effectively and efficiently. For example: FIFO is First In

First Out, it is a assumptions of cash flow that are utilise to remove cost from stock accounts.

LIFO is Last In First Out, this is applied for cost of inventory where recent items are produced

that to be recorded as sold first. AVCO is calculated by dividing inventory cost of goods sold by

goods numbers at any time.

Job costing system:

Job costing system is a method used to combine data regarding cost related with

particular production and job service (Ji, 2017). The essential requirement of job cost accounting

system to Tuffen Mark Ltd is to assign the cost of inventory of each producing products. Also to

check either manufacturing cost exceeds the materials price and overheads this help them to

facilitate profitability for overall process.

Price optimising system:

Price optimising system is a analysis to ascertain that how consumers will react to various

prices for their services and goods through by using different channels. Price optimising system

is essential for Tuffen Mark Ltd as it is used to ascertain prices that will decide by them to attain

their goals like increasing operating profitability.

All the above systems of management accounting helps Assistant Management

Accountant of Tuffen Mark Ltd. To prepare internal reports that are useful for the growth of

company.

P2.Different methods used for management accounting reporting.

Management accounting reports are used to modify, execute, prepare and measure the

performance. This reports is perpetual returns at the time of accounting periods and bookkeeping

as per the requirements (Bennett and James, 2017). Assistant Management Accountant of Tuffen

Mark Ltd prepare this reports to get information that are required to reduce cost, rewards given

for good performance and find out the products which provides good financial returns for their

businesses. The various methods that are used by Assistant Management Accountant of Tuffen

Mark Ltd. For management accounting reports are explained below:

5

Budgets:

Budget is a formal statement where income and expenditure are estimated according to

objectives and future plan. This is an internal report utilize by management to equivalent the

approximate, budgeted plan with number of actual performance attained at a given periods.

Assistant Management Accountant of Tuffen Mark Ltd. Used this method to determine

performance of their business and also to control cost.

Variance analysis:

Variance analysis is a quantifiable research among planned and actual behaviours. This

method is used by Assistant Management Accountant of Tuffen Mark Ltd. As it assist them to

maintain the expenditures of their projects by monitoring deviations related to actual and

budgeted financial performance.

Profit and loss:

Profit and loss is a financial statements which is used to state the costs, expenditures and

income that are occurred at a specified time periods generally a financial quarter or year.

Assistant Management Accountant of Tuffen Mark Ltd. Used this method of management

accounting reports as it assist them to interpret their net profit which will be useful to make

effective decisions.

Cash flow:

Cash flow refers to the gross amount of cash and cash equivalents that are usually

transferred within and out of company (Flamholtz, 2012). Assistant Management Accountant of

Tuffen Mark Ltd. Applied this method of management accounting reports as it help them to

manage the cash position so that further it can be used for rent, stock, raw materials and so on to

increase production for more profitability.

Management performs its activity on the basis of planes that are developed from past

experiences and future goals. For planning various tools are used by management of Tuffen

Mark Ltd. So that planning can be done effectively. Strategic forecasting in planning helps to

predict future and design all the activities that can be achieved as per future activity. On the basis

of forecasting budgets are prepared by management team. These budgets creates basis for

6

Budget is a formal statement where income and expenditure are estimated according to

objectives and future plan. This is an internal report utilize by management to equivalent the

approximate, budgeted plan with number of actual performance attained at a given periods.

Assistant Management Accountant of Tuffen Mark Ltd. Used this method to determine

performance of their business and also to control cost.

Variance analysis:

Variance analysis is a quantifiable research among planned and actual behaviours. This

method is used by Assistant Management Accountant of Tuffen Mark Ltd. As it assist them to

maintain the expenditures of their projects by monitoring deviations related to actual and

budgeted financial performance.

Profit and loss:

Profit and loss is a financial statements which is used to state the costs, expenditures and

income that are occurred at a specified time periods generally a financial quarter or year.

Assistant Management Accountant of Tuffen Mark Ltd. Used this method of management

accounting reports as it assist them to interpret their net profit which will be useful to make

effective decisions.

Cash flow:

Cash flow refers to the gross amount of cash and cash equivalents that are usually

transferred within and out of company (Flamholtz, 2012). Assistant Management Accountant of

Tuffen Mark Ltd. Applied this method of management accounting reports as it help them to

manage the cash position so that further it can be used for rent, stock, raw materials and so on to

increase production for more profitability.

Management performs its activity on the basis of planes that are developed from past

experiences and future goals. For planning various tools are used by management of Tuffen

Mark Ltd. So that planning can be done effectively. Strategic forecasting in planning helps to

predict future and design all the activities that can be achieved as per future activity. On the basis

of forecasting budgets are prepared by management team. These budgets creates basis for

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making and helps in calculating variations. Effective actions are taken to reduced

variations and reasons for these variations are noted by management team.

TASK 2

P3.Calculation of cost and preparation of income statements

Cost of Tuffen mark Ltd. Are calculated by using various techniques are mentioned

below:

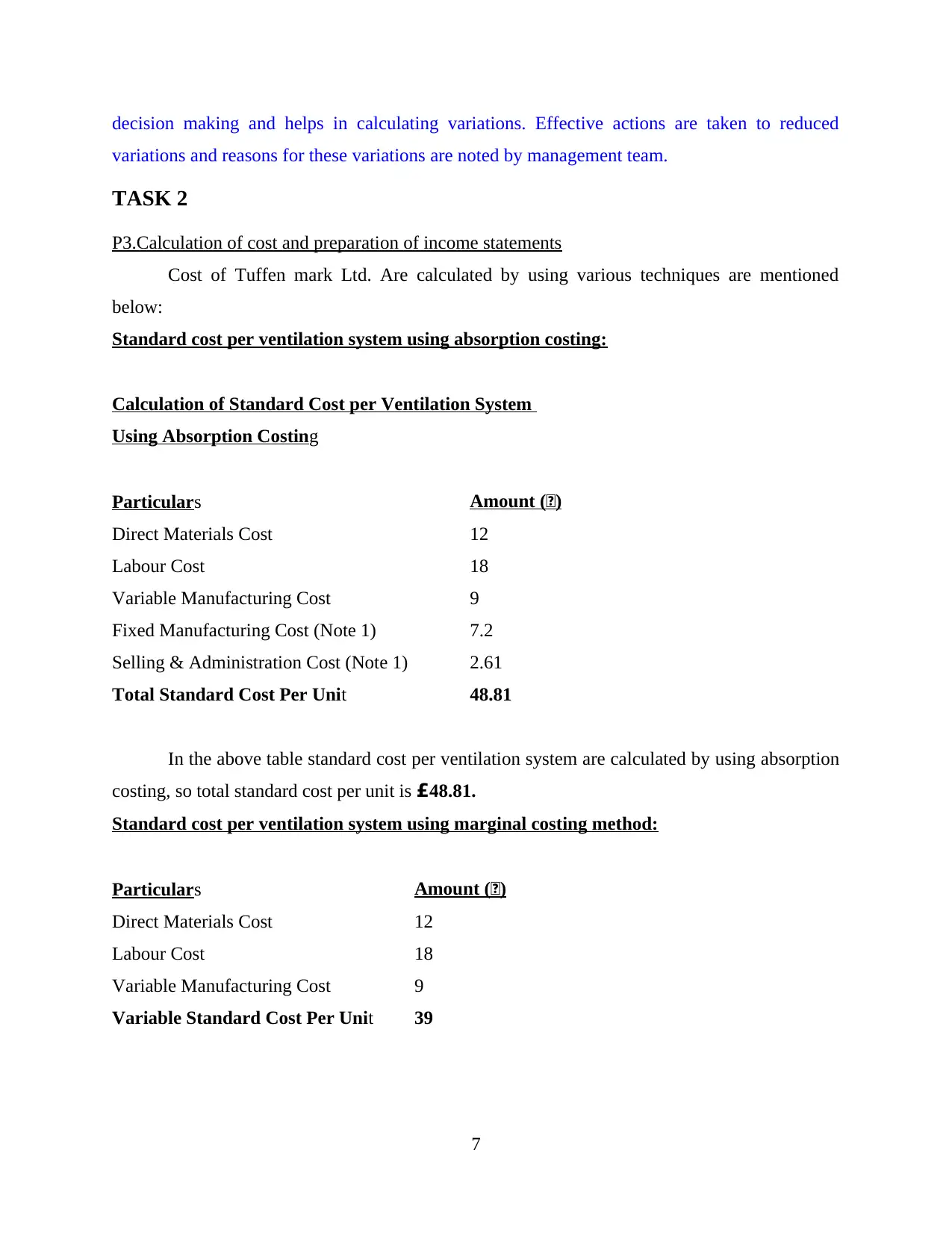

Standard cost per ventilation system using absorption costing:

Calculation of Standard Cost per Ventilation System

Using Absorption Costing

Particulars Amount (£)

Direct Materials Cost 12

Labour Cost 18

Variable Manufacturing Cost 9

Fixed Manufacturing Cost (Note 1) 7.2

Selling & Administration Cost (Note 1) 2.61

Total Standard Cost Per Unit 48.81

In the above table standard cost per ventilation system are calculated by using absorption

costing, so total standard cost per unit is £48.81.

Standard cost per ventilation system using marginal costing method:

Particulars Amount (£)

Direct Materials Cost 12

Labour Cost 18

Variable Manufacturing Cost 9

Variable Standard Cost Per Unit 39

7

variations and reasons for these variations are noted by management team.

TASK 2

P3.Calculation of cost and preparation of income statements

Cost of Tuffen mark Ltd. Are calculated by using various techniques are mentioned

below:

Standard cost per ventilation system using absorption costing:

Calculation of Standard Cost per Ventilation System

Using Absorption Costing

Particulars Amount (£)

Direct Materials Cost 12

Labour Cost 18

Variable Manufacturing Cost 9

Fixed Manufacturing Cost (Note 1) 7.2

Selling & Administration Cost (Note 1) 2.61

Total Standard Cost Per Unit 48.81

In the above table standard cost per ventilation system are calculated by using absorption

costing, so total standard cost per unit is £48.81.

Standard cost per ventilation system using marginal costing method:

Particulars Amount (£)

Direct Materials Cost 12

Labour Cost 18

Variable Manufacturing Cost 9

Variable Standard Cost Per Unit 39

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the above table standard cost are calculated by using marginal costing so, variable

standard cost per unit is £39.

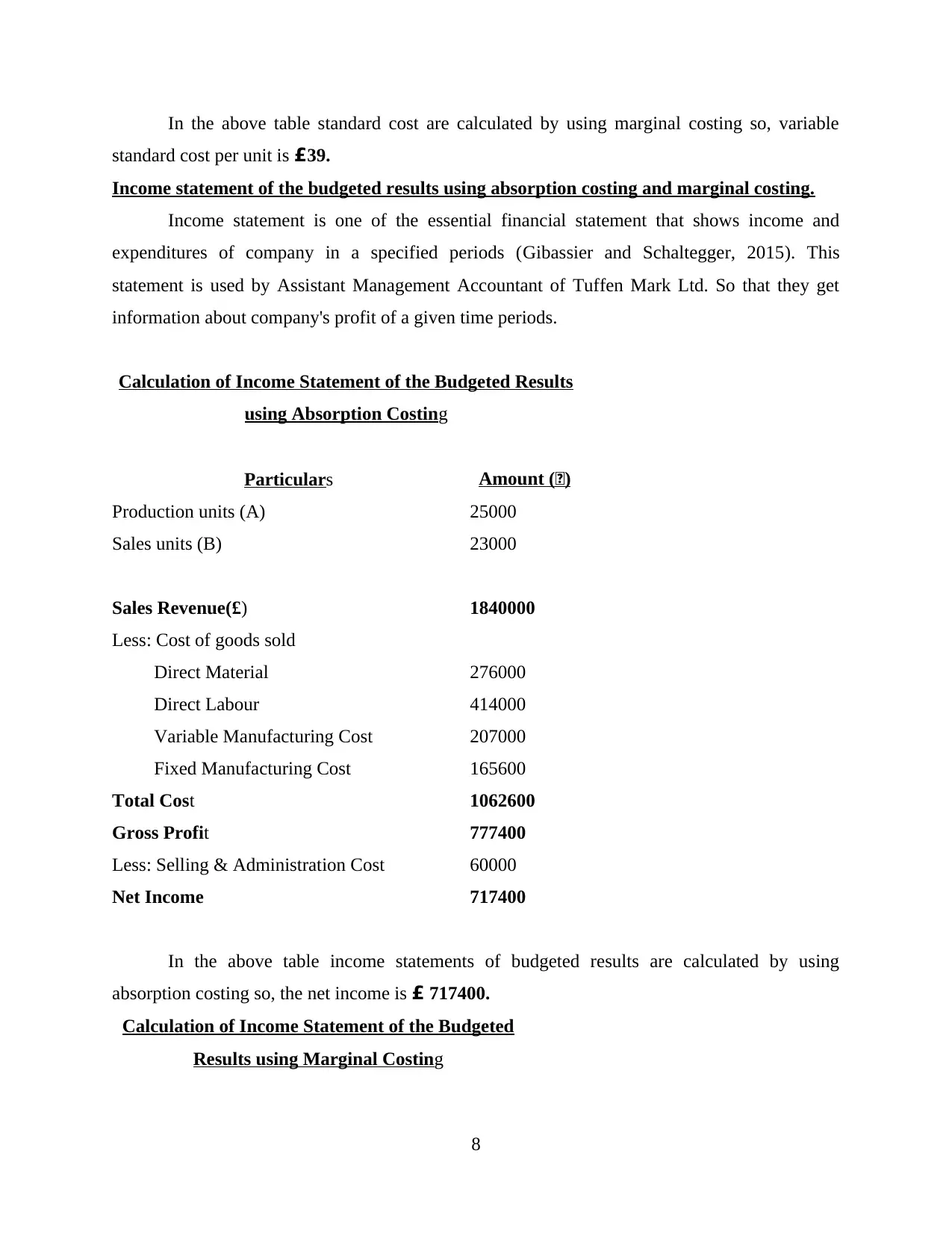

Income statement of the budgeted results using absorption costing and marginal costing.

Income statement is one of the essential financial statement that shows income and

expenditures of company in a specified periods (Gibassier and Schaltegger, 2015). This

statement is used by Assistant Management Accountant of Tuffen Mark Ltd. So that they get

information about company's profit of a given time periods.

Calculation of Income Statement of the Budgeted Results

using Absorption Costing

Particulars Amount (£)

Production units (A) 25000

Sales units (B) 23000

Sales Revenue(£) 1840000

Less: Cost of goods sold

Direct Material 276000

Direct Labour 414000

Variable Manufacturing Cost 207000

Fixed Manufacturing Cost 165600

Total Cost 1062600

Gross Profit 777400

Less: Selling & Administration Cost 60000

Net Income 717400

In the above table income statements of budgeted results are calculated by using

absorption costing so, the net income is £ 717400.

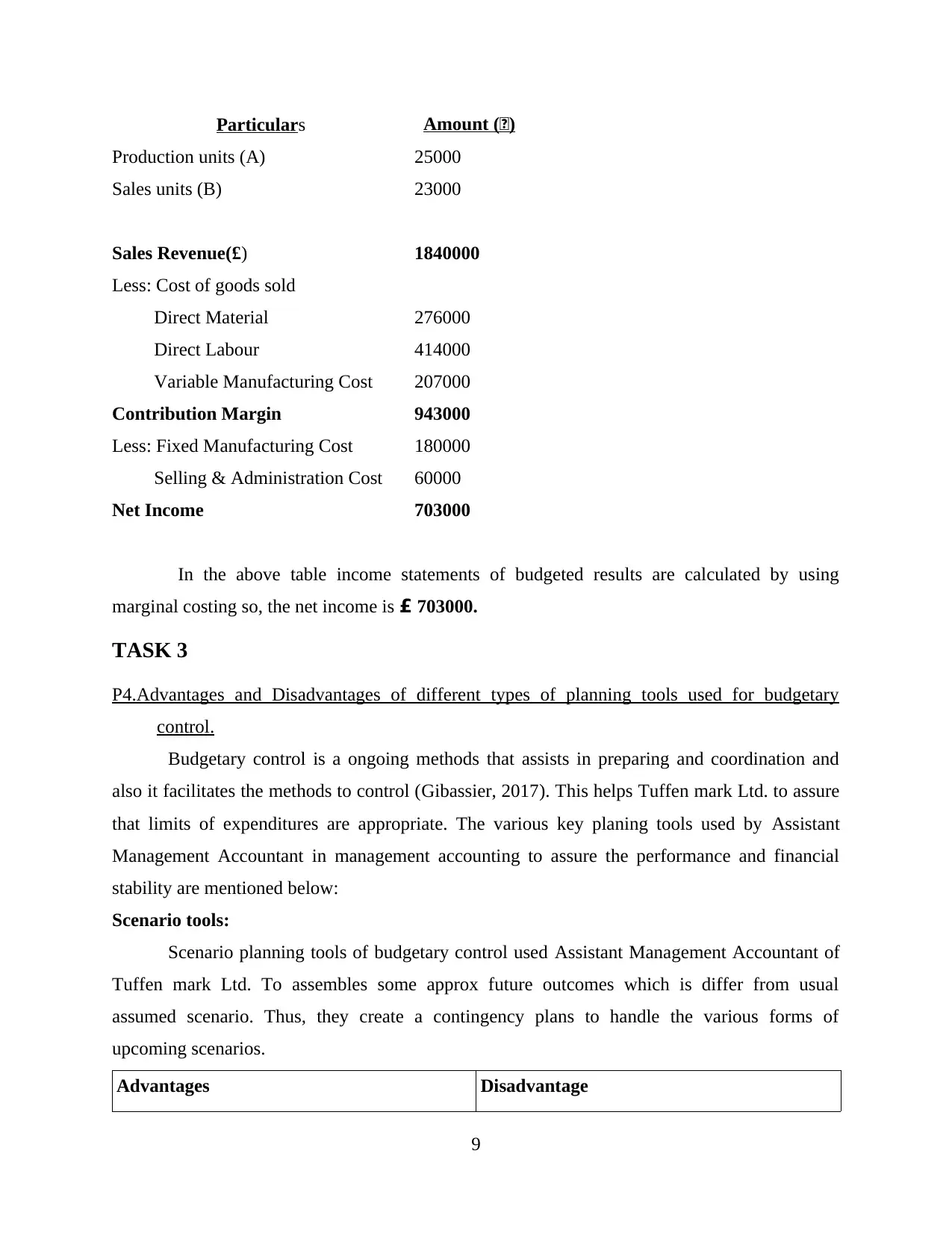

Calculation of Income Statement of the Budgeted

Results using Marginal Costing

8

standard cost per unit is £39.

Income statement of the budgeted results using absorption costing and marginal costing.

Income statement is one of the essential financial statement that shows income and

expenditures of company in a specified periods (Gibassier and Schaltegger, 2015). This

statement is used by Assistant Management Accountant of Tuffen Mark Ltd. So that they get

information about company's profit of a given time periods.

Calculation of Income Statement of the Budgeted Results

using Absorption Costing

Particulars Amount (£)

Production units (A) 25000

Sales units (B) 23000

Sales Revenue(£) 1840000

Less: Cost of goods sold

Direct Material 276000

Direct Labour 414000

Variable Manufacturing Cost 207000

Fixed Manufacturing Cost 165600

Total Cost 1062600

Gross Profit 777400

Less: Selling & Administration Cost 60000

Net Income 717400

In the above table income statements of budgeted results are calculated by using

absorption costing so, the net income is £ 717400.

Calculation of Income Statement of the Budgeted

Results using Marginal Costing

8

Particulars Amount (£)

Production units (A) 25000

Sales units (B) 23000

Sales Revenue(£) 1840000

Less: Cost of goods sold

Direct Material 276000

Direct Labour 414000

Variable Manufacturing Cost 207000

Contribution Margin 943000

Less: Fixed Manufacturing Cost 180000

Selling & Administration Cost 60000

Net Income 703000

In the above table income statements of budgeted results are calculated by using

marginal costing so, the net income is £ 703000.

TASK 3

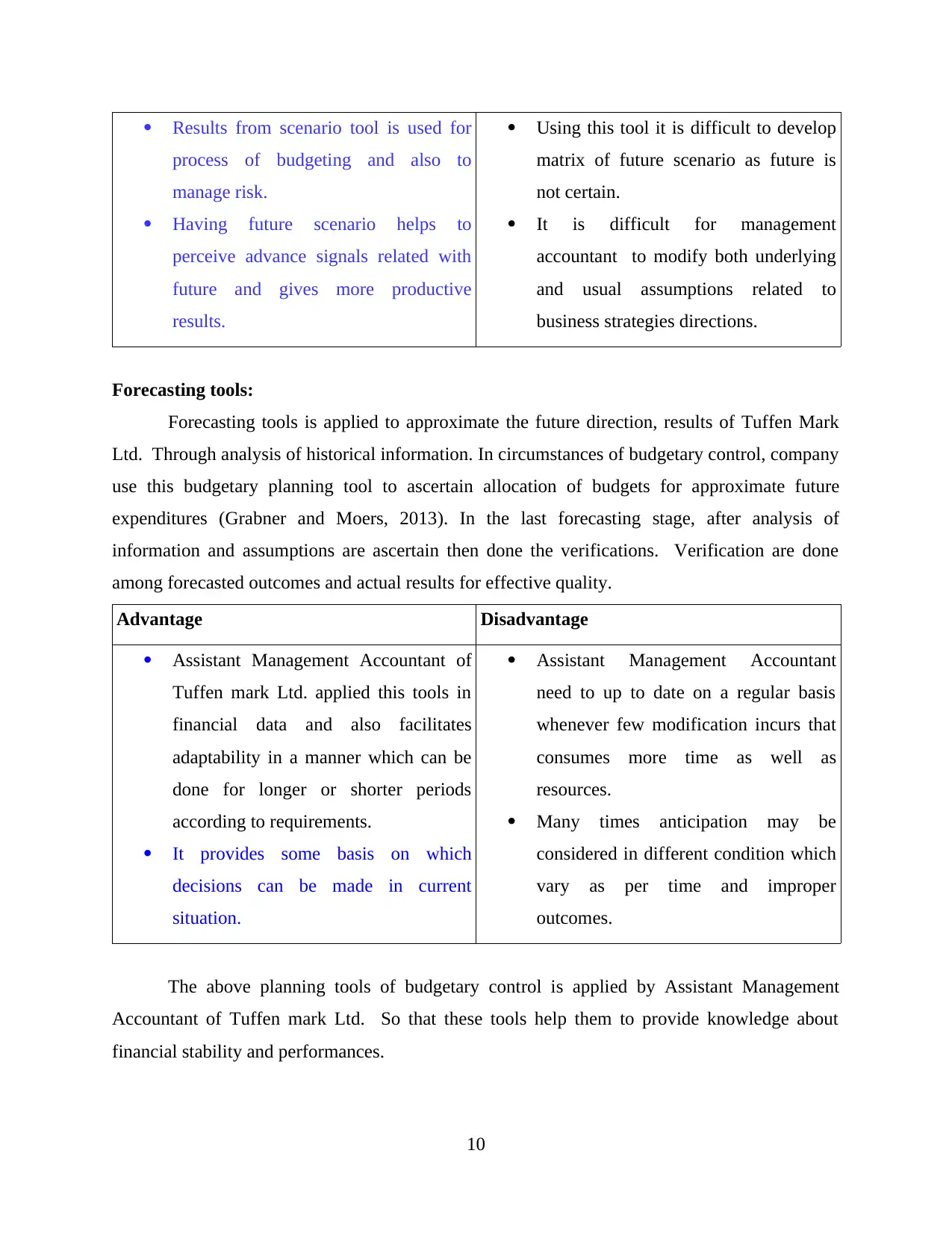

P4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.

Budgetary control is a ongoing methods that assists in preparing and coordination and

also it facilitates the methods to control (Gibassier, 2017). This helps Tuffen mark Ltd. to assure

that limits of expenditures are appropriate. The various key planing tools used by Assistant

Management Accountant in management accounting to assure the performance and financial

stability are mentioned below:

Scenario tools:

Scenario planning tools of budgetary control used Assistant Management Accountant of

Tuffen mark Ltd. To assembles some approx future outcomes which is differ from usual

assumed scenario. Thus, they create a contingency plans to handle the various forms of

upcoming scenarios.

Advantages Disadvantage

9

Production units (A) 25000

Sales units (B) 23000

Sales Revenue(£) 1840000

Less: Cost of goods sold

Direct Material 276000

Direct Labour 414000

Variable Manufacturing Cost 207000

Contribution Margin 943000

Less: Fixed Manufacturing Cost 180000

Selling & Administration Cost 60000

Net Income 703000

In the above table income statements of budgeted results are calculated by using

marginal costing so, the net income is £ 703000.

TASK 3

P4.Advantages and Disadvantages of different types of planning tools used for budgetary

control.

Budgetary control is a ongoing methods that assists in preparing and coordination and

also it facilitates the methods to control (Gibassier, 2017). This helps Tuffen mark Ltd. to assure

that limits of expenditures are appropriate. The various key planing tools used by Assistant

Management Accountant in management accounting to assure the performance and financial

stability are mentioned below:

Scenario tools:

Scenario planning tools of budgetary control used Assistant Management Accountant of

Tuffen mark Ltd. To assembles some approx future outcomes which is differ from usual

assumed scenario. Thus, they create a contingency plans to handle the various forms of

upcoming scenarios.

Advantages Disadvantage

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Results from scenario tool is used for

process of budgeting and also to

manage risk.

Having future scenario helps to

perceive advance signals related with

future and gives more productive

results.

Using this tool it is difficult to develop

matrix of future scenario as future is

not certain.

It is difficult for management

accountant to modify both underlying

and usual assumptions related to

business strategies directions.

Forecasting tools:

Forecasting tools is applied to approximate the future direction, results of Tuffen Mark

Ltd. Through analysis of historical information. In circumstances of budgetary control, company

use this budgetary planning tool to ascertain allocation of budgets for approximate future

expenditures (Grabner and Moers, 2013). In the last forecasting stage, after analysis of

information and assumptions are ascertain then done the verifications. Verification are done

among forecasted outcomes and actual results for effective quality.

Advantage Disadvantage

Assistant Management Accountant of

Tuffen mark Ltd. applied this tools in

financial data and also facilitates

adaptability in a manner which can be

done for longer or shorter periods

according to requirements.

It provides some basis on which

decisions can be made in current

situation.

Assistant Management Accountant

need to up to date on a regular basis

whenever few modification incurs that

consumes more time as well as

resources.

Many times anticipation may be

considered in different condition which

vary as per time and improper

outcomes.

The above planning tools of budgetary control is applied by Assistant Management

Accountant of Tuffen mark Ltd. So that these tools help them to provide knowledge about

financial stability and performances.

10

process of budgeting and also to

manage risk.

Having future scenario helps to

perceive advance signals related with

future and gives more productive

results.

Using this tool it is difficult to develop

matrix of future scenario as future is

not certain.

It is difficult for management

accountant to modify both underlying

and usual assumptions related to

business strategies directions.

Forecasting tools:

Forecasting tools is applied to approximate the future direction, results of Tuffen Mark

Ltd. Through analysis of historical information. In circumstances of budgetary control, company

use this budgetary planning tool to ascertain allocation of budgets for approximate future

expenditures (Grabner and Moers, 2013). In the last forecasting stage, after analysis of

information and assumptions are ascertain then done the verifications. Verification are done

among forecasted outcomes and actual results for effective quality.

Advantage Disadvantage

Assistant Management Accountant of

Tuffen mark Ltd. applied this tools in

financial data and also facilitates

adaptability in a manner which can be

done for longer or shorter periods

according to requirements.

It provides some basis on which

decisions can be made in current

situation.

Assistant Management Accountant

need to up to date on a regular basis

whenever few modification incurs that

consumes more time as well as

resources.

Many times anticipation may be

considered in different condition which

vary as per time and improper

outcomes.

The above planning tools of budgetary control is applied by Assistant Management

Accountant of Tuffen mark Ltd. So that these tools help them to provide knowledge about

financial stability and performances.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5.Adaption of management accounting system to respond to financial problems.

Tuffen Mark Ltd. Faces various problems related to systems of management accounting.

This bear critical conditions to handle resources of finance within business. There are many

kinds of issues related to finances like growth promotion with minimum interest rates and also

improving new and reliable revenue sources. These problems can be solved by applying some

tools are explained below:

Benchmarking:

Benchmarking is a tool that is utilised to equivalent one business with other to identify

the manner to increase competitive advantages (Jakobsen, 2012). The key metrics to used to

operate business of Tuffen Mark Ltd. Are compared with Ever joy enterprises Ltd. Through

benchmarking over performance and underperformance areas are identified. Different models of

business are adapted to raise and speed up modification for effective growth. With the

application of bench marking accountant are able to develop new and reliable revenue sources as

they analysis there past records and formulate strategies and set benchmarking standards for the

same.

KPI:

Key performance indicators are quantity value which ascertains effectualness to

accomplish goals of Tuffen marks Ltd. In method to attain objectives, Tuffen mark Ltd. Apply

this indicators at various levels. At high level, it shows overall performance of company and low

level are related with individual workforce of different sections. The company want to do

promotion of growth with low interest rate so to overcome from this issues they apply KPIs as it

evaluate whole performance of business.

In today's competitive scenario organisations are facing financial issues at large scale. To

resolve issues related to finances management techniques like budgeting and forecasting is

highly recommended. Through forecasting future is estimated to some extend and on the basis of

which budgets are prepared. These tools helps in estimation of finances required in performing

11

P5.Adaption of management accounting system to respond to financial problems.

Tuffen Mark Ltd. Faces various problems related to systems of management accounting.

This bear critical conditions to handle resources of finance within business. There are many

kinds of issues related to finances like growth promotion with minimum interest rates and also

improving new and reliable revenue sources. These problems can be solved by applying some

tools are explained below:

Benchmarking:

Benchmarking is a tool that is utilised to equivalent one business with other to identify

the manner to increase competitive advantages (Jakobsen, 2012). The key metrics to used to

operate business of Tuffen Mark Ltd. Are compared with Ever joy enterprises Ltd. Through

benchmarking over performance and underperformance areas are identified. Different models of

business are adapted to raise and speed up modification for effective growth. With the

application of bench marking accountant are able to develop new and reliable revenue sources as

they analysis there past records and formulate strategies and set benchmarking standards for the

same.

KPI:

Key performance indicators are quantity value which ascertains effectualness to

accomplish goals of Tuffen marks Ltd. In method to attain objectives, Tuffen mark Ltd. Apply

this indicators at various levels. At high level, it shows overall performance of company and low

level are related with individual workforce of different sections. The company want to do

promotion of growth with low interest rate so to overcome from this issues they apply KPIs as it

evaluate whole performance of business.

In today's competitive scenario organisations are facing financial issues at large scale. To

resolve issues related to finances management techniques like budgeting and forecasting is

highly recommended. Through forecasting future is estimated to some extend and on the basis of

which budgets are prepared. These tools helps in estimation of finances required in performing

11

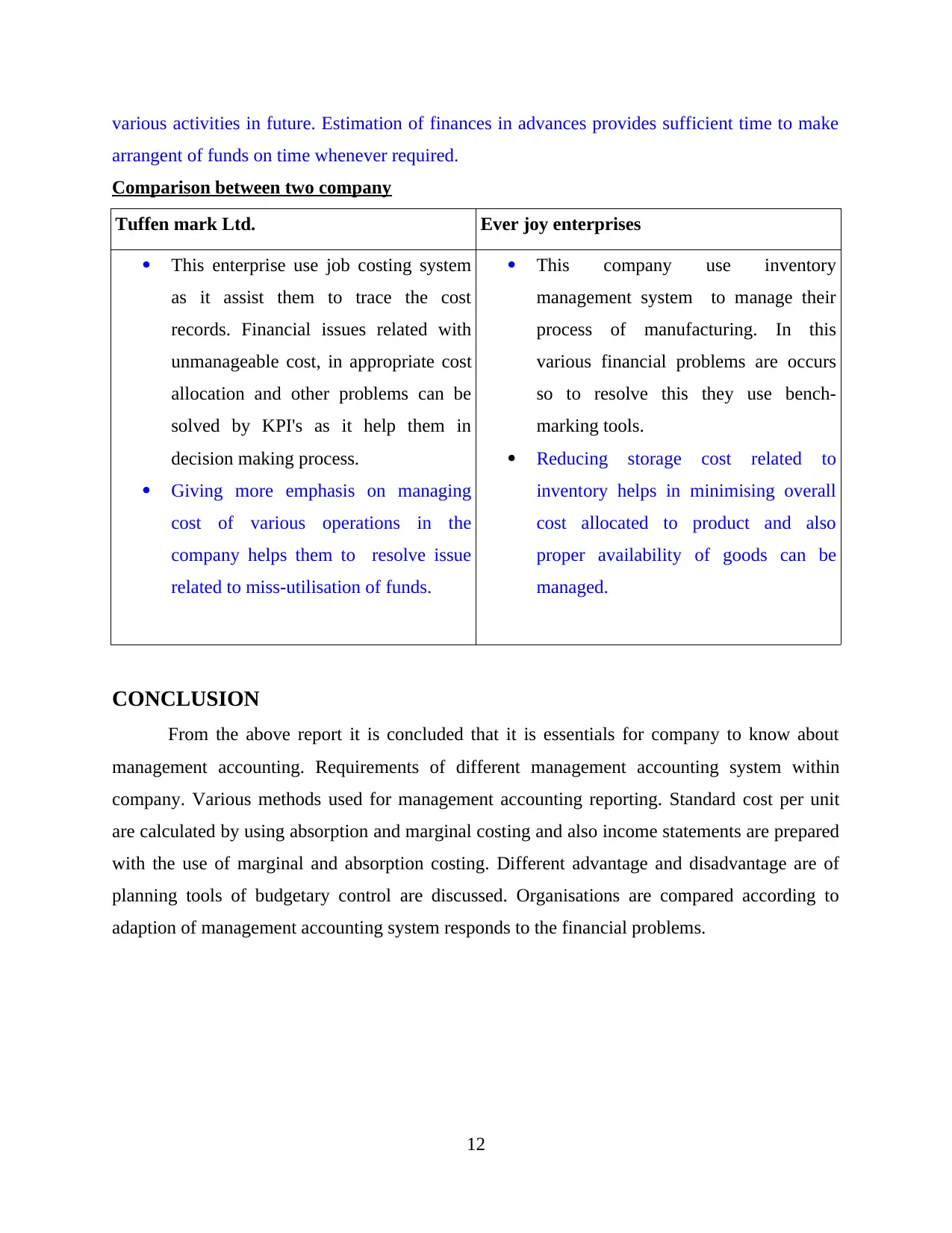

various activities in future. Estimation of finances in advances provides sufficient time to make

arrangent of funds on time whenever required.

Comparison between two company

Tuffen mark Ltd. Ever joy enterprises

This enterprise use job costing system

as it assist them to trace the cost

records. Financial issues related with

unmanageable cost, in appropriate cost

allocation and other problems can be

solved by KPI's as it help them in

decision making process.

Giving more emphasis on managing

cost of various operations in the

company helps them to resolve issue

related to miss-utilisation of funds.

This company use inventory

management system to manage their

process of manufacturing. In this

various financial problems are occurs

so to resolve this they use bench-

marking tools.

Reducing storage cost related to

inventory helps in minimising overall

cost allocated to product and also

proper availability of goods can be

managed.

CONCLUSION

From the above report it is concluded that it is essentials for company to know about

management accounting. Requirements of different management accounting system within

company. Various methods used for management accounting reporting. Standard cost per unit

are calculated by using absorption and marginal costing and also income statements are prepared

with the use of marginal and absorption costing. Different advantage and disadvantage are of

planning tools of budgetary control are discussed. Organisations are compared according to

adaption of management accounting system responds to the financial problems.

12

arrangent of funds on time whenever required.

Comparison between two company

Tuffen mark Ltd. Ever joy enterprises

This enterprise use job costing system

as it assist them to trace the cost

records. Financial issues related with

unmanageable cost, in appropriate cost

allocation and other problems can be

solved by KPI's as it help them in

decision making process.

Giving more emphasis on managing

cost of various operations in the

company helps them to resolve issue

related to miss-utilisation of funds.

This company use inventory

management system to manage their

process of manufacturing. In this

various financial problems are occurs

so to resolve this they use bench-

marking tools.

Reducing storage cost related to

inventory helps in minimising overall

cost allocated to product and also

proper availability of goods can be

managed.

CONCLUSION

From the above report it is concluded that it is essentials for company to know about

management accounting. Requirements of different management accounting system within

company. Various methods used for management accounting reporting. Standard cost per unit

are calculated by using absorption and marginal costing and also income statements are prepared

with the use of marginal and absorption costing. Different advantage and disadvantage are of

planning tools of budgetary control are discussed. Organisations are compared according to

adaption of management accounting system responds to the financial problems.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.