Management Accounting Report: Budgetary Control and Systems

VerifiedAdded on 2020/06/04

|16

|4969

|376

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its crucial role in organizational decision-making and performance enhancement. It begins by defining management accounting and outlining its essential requirements, exploring various methods for reporting financial and non-financial information. The report then focuses on cost analysis techniques, demonstrating how to calculate costs effectively using relevant methods. It also examines the advantages and disadvantages of planning tools used for budgetary control, providing insights into their practical application. Furthermore, the report addresses how organizations adapt accounting systems to respond to business problems, offering a comprehensive overview of the subject matter. Throughout the report, real-world examples, such as the case of Airdri, a hand dryer manufacturer, are used to illustrate key concepts and provide practical context.

MNG ACC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and requirement of management accounting...................3

P2 Explain methods for management accounting reporting.......................................................5

TASK 2 ...........................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis..............................................8

TASK 3............................................................................................................................................9

P4 Advantages and Disadvantages of planning tools used for budgetary control......................9

TASK 4..........................................................................................................................................11

P5 How organisations are adapting accounting systems to respond to problems....................11

CONCLUSION.............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and requirement of management accounting...................3

P2 Explain methods for management accounting reporting.......................................................5

TASK 2 ...........................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis..............................................8

TASK 3............................................................................................................................................9

P4 Advantages and Disadvantages of planning tools used for budgetary control......................9

TASK 4..........................................................................................................................................11

P5 How organisations are adapting accounting systems to respond to problems....................11

CONCLUSION.............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting includes, participating in the decision making process that

revolves around the functions of the management. It the process of preparing and managing

accounting and managerial reports in order to carry out formulations of business fluently. The

only purpose of the management accounting is to contribute in the enhancement of the

organisation. It identifies, measures and then analyze the goals and objectives of the organisation

in order to provide structure to the organisation. This report is based on the requirements and

different types of management accounting system, methods used for reporting management

accounting, calculating cost and preparing income statement and lastly advantages and

disadvantages of planning tools used for budgetary control.

TASK 1

P1 Explain management accounting and requirement of management accounting.

Management accounting is the process of managing accounting and managerial reports in

order to function the business effectively and efficiently. It is the process of integrating the

financial and non-financial statements of the business with the purpose to provide full and

equivalent information tot eh management department. It plays very crucial role in generating

and then implementing the information to the management. It is very broad concept and its

specifications are very formulated, every business big or small requires functions of management

accounting in order to function it effectively and efficiently. It area of region is very wide, it can

formulate in each and every business. Management accounting is not a technique it is practice

which is conducted by the business to evaluate regulations in its function. All the reports of the

management accounting contains familiar data, for providing financial information about the

business to the orgamisation (Chenhall, 2015).

Airdri, was the first manufacturer of hand dryer, situated in Witney. Their total number

of employees working in an firm is 47. As per the reports of 2016, their sales percentage was

9.62 and in 2015 it was 8.9. Their main aim is to provide, new technologies and extended

versions of hand dryers and their current motive is to make them five times more long lasting

(Ayre, 2017).

Every organisation small or medium requires working of management accounting

because it plays a keen role today in evaluating functions of the business. As the general

manager of the Airdri, notices the importance of management accounting in the organisation for

Management accounting includes, participating in the decision making process that

revolves around the functions of the management. It the process of preparing and managing

accounting and managerial reports in order to carry out formulations of business fluently. The

only purpose of the management accounting is to contribute in the enhancement of the

organisation. It identifies, measures and then analyze the goals and objectives of the organisation

in order to provide structure to the organisation. This report is based on the requirements and

different types of management accounting system, methods used for reporting management

accounting, calculating cost and preparing income statement and lastly advantages and

disadvantages of planning tools used for budgetary control.

TASK 1

P1 Explain management accounting and requirement of management accounting.

Management accounting is the process of managing accounting and managerial reports in

order to function the business effectively and efficiently. It is the process of integrating the

financial and non-financial statements of the business with the purpose to provide full and

equivalent information tot eh management department. It plays very crucial role in generating

and then implementing the information to the management. It is very broad concept and its

specifications are very formulated, every business big or small requires functions of management

accounting in order to function it effectively and efficiently. It area of region is very wide, it can

formulate in each and every business. Management accounting is not a technique it is practice

which is conducted by the business to evaluate regulations in its function. All the reports of the

management accounting contains familiar data, for providing financial information about the

business to the orgamisation (Chenhall, 2015).

Airdri, was the first manufacturer of hand dryer, situated in Witney. Their total number

of employees working in an firm is 47. As per the reports of 2016, their sales percentage was

9.62 and in 2015 it was 8.9. Their main aim is to provide, new technologies and extended

versions of hand dryers and their current motive is to make them five times more long lasting

(Ayre, 2017).

Every organisation small or medium requires working of management accounting

because it plays a keen role today in evaluating functions of the business. As the general

manager of the Airdri, notices the importance of management accounting in the organisation for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

implementing structured and detailed information system (Chiarini, 2015). It helps in analyze the

ratio of funds required, and also helps in regulating the ratio of expenses, with the help pf

collected information systematic financial outcomes can be accomplished in the firm for future

practices.

Airdri, is a small firm managing their financial statements is very essential for them in

order to generate accurate and good ratio of profit. Estimation provides accurate set of

information which in turn can be beneficial for the working of the firm. Essential requirements

of different types of management accounting systems are:

Price optimisation: It revolves around the mathematical analysis done by the company to

identify the reactions of the customers on different prices of its products and services evaluate

through various channels. It also combines the prizes with the objectives of the company in order

to maximize the profits of the operating units. It works with operating costs, statements and

historical sales and prices of the products. Industries like retail, banking manufacturing, banking

and hotel sectors etc can practice price optimisation in their business (Fullerton, 2014).

Price optimisation is use to analyse the data and information to study the behaviour of the

core customers upon the variations in the prices of their products. The fist step in price

optimisation is customer segmentation. For handling complex calculations of the business many

business use software for price optimisation.

Cost Accounting: It is the process of controlling the outcomes of the cost by recording,

classifying, summarized, allocation and numerous alternative aspects. Information and the

methods of cost accounting comes along with the financial accounting. It is also used by the

managers and the leaders to take the decisions at initial level. Every type of business whether its

is small, medium or large use functions of cost accounting to evaluate the financial statements of

the firm. Variable cost is dynamic it keep on changing, there are various cost which remains

same under any kind of circumstances.

Cost accounting is important for tracking the various types of activities of the firms like

Airdri. As the cited firm is manufacturer of hand dryer, a single product, so to make each hand

dryer, the firm needed to purchase $60 for raw materials and other components which are

required to develop hand dryer, and they have to pay $40 to 6 workers as a wages. Hence total

variable cost for developing each hand dryer is $300. so manufacturing cost of single hand dryer

ratio of funds required, and also helps in regulating the ratio of expenses, with the help pf

collected information systematic financial outcomes can be accomplished in the firm for future

practices.

Airdri, is a small firm managing their financial statements is very essential for them in

order to generate accurate and good ratio of profit. Estimation provides accurate set of

information which in turn can be beneficial for the working of the firm. Essential requirements

of different types of management accounting systems are:

Price optimisation: It revolves around the mathematical analysis done by the company to

identify the reactions of the customers on different prices of its products and services evaluate

through various channels. It also combines the prizes with the objectives of the company in order

to maximize the profits of the operating units. It works with operating costs, statements and

historical sales and prices of the products. Industries like retail, banking manufacturing, banking

and hotel sectors etc can practice price optimisation in their business (Fullerton, 2014).

Price optimisation is use to analyse the data and information to study the behaviour of the

core customers upon the variations in the prices of their products. The fist step in price

optimisation is customer segmentation. For handling complex calculations of the business many

business use software for price optimisation.

Cost Accounting: It is the process of controlling the outcomes of the cost by recording,

classifying, summarized, allocation and numerous alternative aspects. Information and the

methods of cost accounting comes along with the financial accounting. It is also used by the

managers and the leaders to take the decisions at initial level. Every type of business whether its

is small, medium or large use functions of cost accounting to evaluate the financial statements of

the firm. Variable cost is dynamic it keep on changing, there are various cost which remains

same under any kind of circumstances.

Cost accounting is important for tracking the various types of activities of the firms like

Airdri. As the cited firm is manufacturer of hand dryer, a single product, so to make each hand

dryer, the firm needed to purchase $60 for raw materials and other components which are

required to develop hand dryer, and they have to pay $40 to 6 workers as a wages. Hence total

variable cost for developing each hand dryer is $300. so manufacturing cost of single hand dryer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is $300 so they can't sell it below that and as per the rules and norms any price which is more

than $300 becomes the contribution in the fixed cost of the firm (Lapsley, 2017).

Basically, internal system of reporting in the firm for conducting decision making

process is generally referred as cost accounting.

Job costing: It is the method of recording the total cost involved in manufacturing job.

Tracks and records of each job can be accurately assessed with the help of job costing. Usually a

project manager or accountant keeps the tract of the cost of the each and every job occurring in

the firm. It s used to calculate the total cost involved in the process manufacturing jobs. It is also

useful in storing the relevant data for the business operations.

The job costing is based on the specific customer products and services in order to

regulate the variations in the cost.

Tracks of costs and revenues are evaluated by job costing accounting.

Inventory management: Supervising the assets which are non capitalized and items of

the stocks can be termed as inventory management, it regulates the flow of goods and services

from warehouse to that of point of sale. The inventories and stocks of the company is its most

valuable assess. The large inventories can prove to be risky for the firms like Airdri, it is

important that it get sold in right time to avoid the situation of extreme damage, theft or spoilage.

For the business of any size, whether it is small, medium or large managing inventories is

crucial requirement (Laudon, 2016).

P2 Explain methods for management accounting reporting.

Management accounting and financial accounting are two different concepts. The reports

presented by the cost accounting is often based on the information which are gathered from the

internal stakeholders of the organisation. The main aim of management accounting is to present

the periodic reports for the managers and accountants of the firms like Airdri. It is useful as it

provides information in a very fast manner which than can prove to be very helpful for he

managers and decision making unit of the companies (Maas, 2016). Various approaches of

management accounting reports are:

Segmental or departmental report: It is the report which covered the differentiate

financial information and a distinct strategies of the management. It can be of any type like

geographical, departmental or based on the line of the business. In management accounting

segmental or departmental reports are used to carry out the comparison between the different

than $300 becomes the contribution in the fixed cost of the firm (Lapsley, 2017).

Basically, internal system of reporting in the firm for conducting decision making

process is generally referred as cost accounting.

Job costing: It is the method of recording the total cost involved in manufacturing job.

Tracks and records of each job can be accurately assessed with the help of job costing. Usually a

project manager or accountant keeps the tract of the cost of the each and every job occurring in

the firm. It s used to calculate the total cost involved in the process manufacturing jobs. It is also

useful in storing the relevant data for the business operations.

The job costing is based on the specific customer products and services in order to

regulate the variations in the cost.

Tracks of costs and revenues are evaluated by job costing accounting.

Inventory management: Supervising the assets which are non capitalized and items of

the stocks can be termed as inventory management, it regulates the flow of goods and services

from warehouse to that of point of sale. The inventories and stocks of the company is its most

valuable assess. The large inventories can prove to be risky for the firms like Airdri, it is

important that it get sold in right time to avoid the situation of extreme damage, theft or spoilage.

For the business of any size, whether it is small, medium or large managing inventories is

crucial requirement (Laudon, 2016).

P2 Explain methods for management accounting reporting.

Management accounting and financial accounting are two different concepts. The reports

presented by the cost accounting is often based on the information which are gathered from the

internal stakeholders of the organisation. The main aim of management accounting is to present

the periodic reports for the managers and accountants of the firms like Airdri. It is useful as it

provides information in a very fast manner which than can prove to be very helpful for he

managers and decision making unit of the companies (Maas, 2016). Various approaches of

management accounting reports are:

Segmental or departmental report: It is the report which covered the differentiate

financial information and a distinct strategies of the management. It can be of any type like

geographical, departmental or based on the line of the business. In management accounting

segmental or departmental reports are used to carry out the comparison between the different

working sections of the business. It use to evaluate that way of conducting tasks of which area is

better than the other. It is used for braking the financial data of the business in to various

divisions or sections in order to carry out the specific information which is related to the

functions of the business. Its main aim is to provide accurate and clear picture of the functions of

the business, so that in annual report it can present performance of the company to their share

holders. It deals with the each section of the business like income, expenses etc.

Performance report: It is developed for each and every employee of the company in

order to asses and guide their level of performance. Such reports also helps the management

units to analyse the success of the projects and the products and evaluation of the productivity of

the management accounting approaches. Its main aim is to provide comparison between the

actual and the budgeted amount of the cost which is in the hand of firm for its accountants and

managers. It is used to analyse the evaluation in the activities and in the work of an individual.

As the name say itself performance report is basically based on the performance criteria of the

organisation or its employee. For the firms like Airdri, such reports can prove to be very helpful

in analysing the performance criteria of their employees. As the number of employees in the firm

are less, it is easy for their managers to identify the working criteria of each and every employee

critically (Nitzl, 2018).

Inventory management report: Such reports are generated to analyse the overall

informations about the inventories of the organisation. This will help in keeping the track about

the products which are available within the firm and are ready to use in the warehouses. This

also helps in tracking the damage, theft or spoilage of the products which are being stored in the

warehouses. The inventory report is subdivided into three parts:

Inventory status report: It is used to record the status of the report by analysing its

location, time or period or any other factors that can be calculated.

Inventory analysis report: This present the profit ratio, turnovers, supply and demand for

the inventories.

Inventory integrity report: This section is use to identify the reasonable difference

between the information which is related to the various items and information that

revolves around the accounting.

Inventory management report is use to analyse the storage of goods and products in the

warehouses to keep the track of the availability of items within the firm.

better than the other. It is used for braking the financial data of the business in to various

divisions or sections in order to carry out the specific information which is related to the

functions of the business. Its main aim is to provide accurate and clear picture of the functions of

the business, so that in annual report it can present performance of the company to their share

holders. It deals with the each section of the business like income, expenses etc.

Performance report: It is developed for each and every employee of the company in

order to asses and guide their level of performance. Such reports also helps the management

units to analyse the success of the projects and the products and evaluation of the productivity of

the management accounting approaches. Its main aim is to provide comparison between the

actual and the budgeted amount of the cost which is in the hand of firm for its accountants and

managers. It is used to analyse the evaluation in the activities and in the work of an individual.

As the name say itself performance report is basically based on the performance criteria of the

organisation or its employee. For the firms like Airdri, such reports can prove to be very helpful

in analysing the performance criteria of their employees. As the number of employees in the firm

are less, it is easy for their managers to identify the working criteria of each and every employee

critically (Nitzl, 2018).

Inventory management report: Such reports are generated to analyse the overall

informations about the inventories of the organisation. This will help in keeping the track about

the products which are available within the firm and are ready to use in the warehouses. This

also helps in tracking the damage, theft or spoilage of the products which are being stored in the

warehouses. The inventory report is subdivided into three parts:

Inventory status report: It is used to record the status of the report by analysing its

location, time or period or any other factors that can be calculated.

Inventory analysis report: This present the profit ratio, turnovers, supply and demand for

the inventories.

Inventory integrity report: This section is use to identify the reasonable difference

between the information which is related to the various items and information that

revolves around the accounting.

Inventory management report is use to analyse the storage of goods and products in the

warehouses to keep the track of the availability of items within the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts receivables ageing report: It is used to analyse the invoices of the unpaid customers of

an organisation. This report keeps the track of various factors like:

How much amount is unpaid by the customer

For how long that amount is not received from the customers

From which customer maximum amount of money is receivable

Assigned dates for the invoices of the sale.

With the criteria of ageing periods such reports are broken into various parts, and

required changes can be made in such reports in every 30 days.

Job cost report: This report is used to record the total cost involved in manufacturing

job. Tracks and records of each job can be accurately assessed with the help of job costing.

Usually a project manager or accountant keeps the tract of the cost of the each and every job

occurring in the firm. It s used to calculate the total cost involved in the process manufacturing

jobs. It is also useful in storing the relevant data for the business operations. The job costing is

based on the specific customer products and services in order to regulate the variations in the

cost. Tracks of costs and revenues are evaluated by job costing accounting. This reports shows

the each and every detail of overall cost involved in all the costs which are related to the various

kinds of the jobs presented in the organisation.

Operational budget report: The profits and expenses of the organisation effects its

operational budget for practising business currently and for in the future. When a repost is made

related to the budget of the organisation, all the operational budgets are combined in order to

prepare the income statement for the organisation. This reports shows the each and every detail

about the companies earning and their expenses over a period of time in order to present the

expenses for the expected future.

It is important part of any business, as it associates with all the operations of the business.

Management accounting is the process of managing accounting and managerial reports in order

to function the business effectively and efficiently. It is the process of integrating the financial

and non-financial statements of the business with the purpose to provide full and equivalent

information tot eh management department. It plays very crucial role in generating and then

implementing the information to the management (Otley, 2016).

an organisation. This report keeps the track of various factors like:

How much amount is unpaid by the customer

For how long that amount is not received from the customers

From which customer maximum amount of money is receivable

Assigned dates for the invoices of the sale.

With the criteria of ageing periods such reports are broken into various parts, and

required changes can be made in such reports in every 30 days.

Job cost report: This report is used to record the total cost involved in manufacturing

job. Tracks and records of each job can be accurately assessed with the help of job costing.

Usually a project manager or accountant keeps the tract of the cost of the each and every job

occurring in the firm. It s used to calculate the total cost involved in the process manufacturing

jobs. It is also useful in storing the relevant data for the business operations. The job costing is

based on the specific customer products and services in order to regulate the variations in the

cost. Tracks of costs and revenues are evaluated by job costing accounting. This reports shows

the each and every detail of overall cost involved in all the costs which are related to the various

kinds of the jobs presented in the organisation.

Operational budget report: The profits and expenses of the organisation effects its

operational budget for practising business currently and for in the future. When a repost is made

related to the budget of the organisation, all the operational budgets are combined in order to

prepare the income statement for the organisation. This reports shows the each and every detail

about the companies earning and their expenses over a period of time in order to present the

expenses for the expected future.

It is important part of any business, as it associates with all the operations of the business.

Management accounting is the process of managing accounting and managerial reports in order

to function the business effectively and efficiently. It is the process of integrating the financial

and non-financial statements of the business with the purpose to provide full and equivalent

information tot eh management department. It plays very crucial role in generating and then

implementing the information to the management (Otley, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

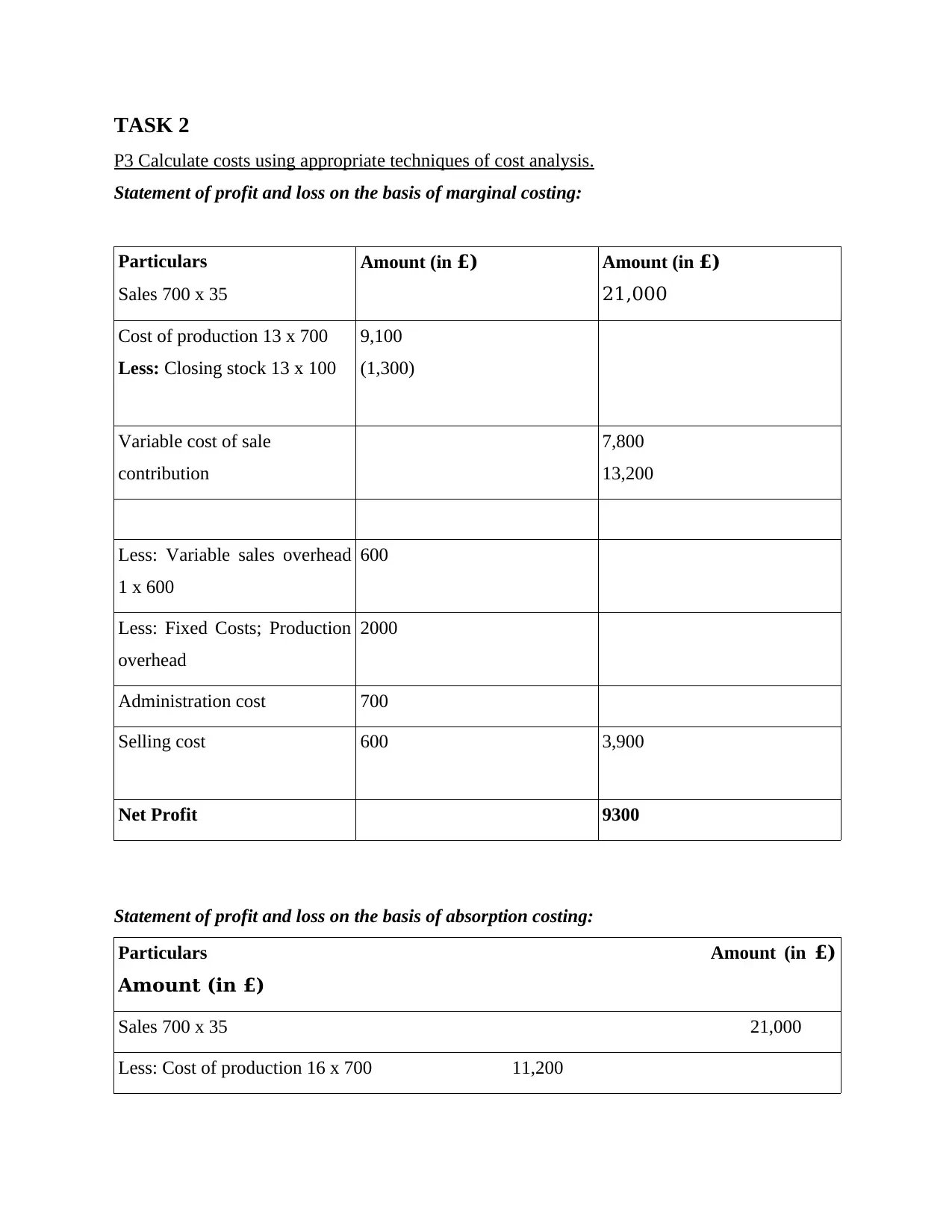

P3 Calculate costs using appropriate techniques of cost analysis.

Statement of profit and loss on the basis of marginal costing:

Particulars

Sales 700 x 35

Amount (in £) Amount (in £)

21,000

Cost of production 13 x 700

Less: Closing stock 13 x 100

9,100

(1,300)

Variable cost of sale

contribution

7,800

13,200

Less: Variable sales overhead

1 x 600

600

Less: Fixed Costs; Production

overhead

2000

Administration cost 700

Selling cost 600 3,900

Net Profit 9300

Statement of profit and loss on the basis of absorption costing:

Particulars Amount (in £)

Amount (in £)

Sales 700 x 35 21,000

Less: Cost of production 16 x 700 11,200

P3 Calculate costs using appropriate techniques of cost analysis.

Statement of profit and loss on the basis of marginal costing:

Particulars

Sales 700 x 35

Amount (in £) Amount (in £)

21,000

Cost of production 13 x 700

Less: Closing stock 13 x 100

9,100

(1,300)

Variable cost of sale

contribution

7,800

13,200

Less: Variable sales overhead

1 x 600

600

Less: Fixed Costs; Production

overhead

2000

Administration cost 700

Selling cost 600 3,900

Net Profit 9300

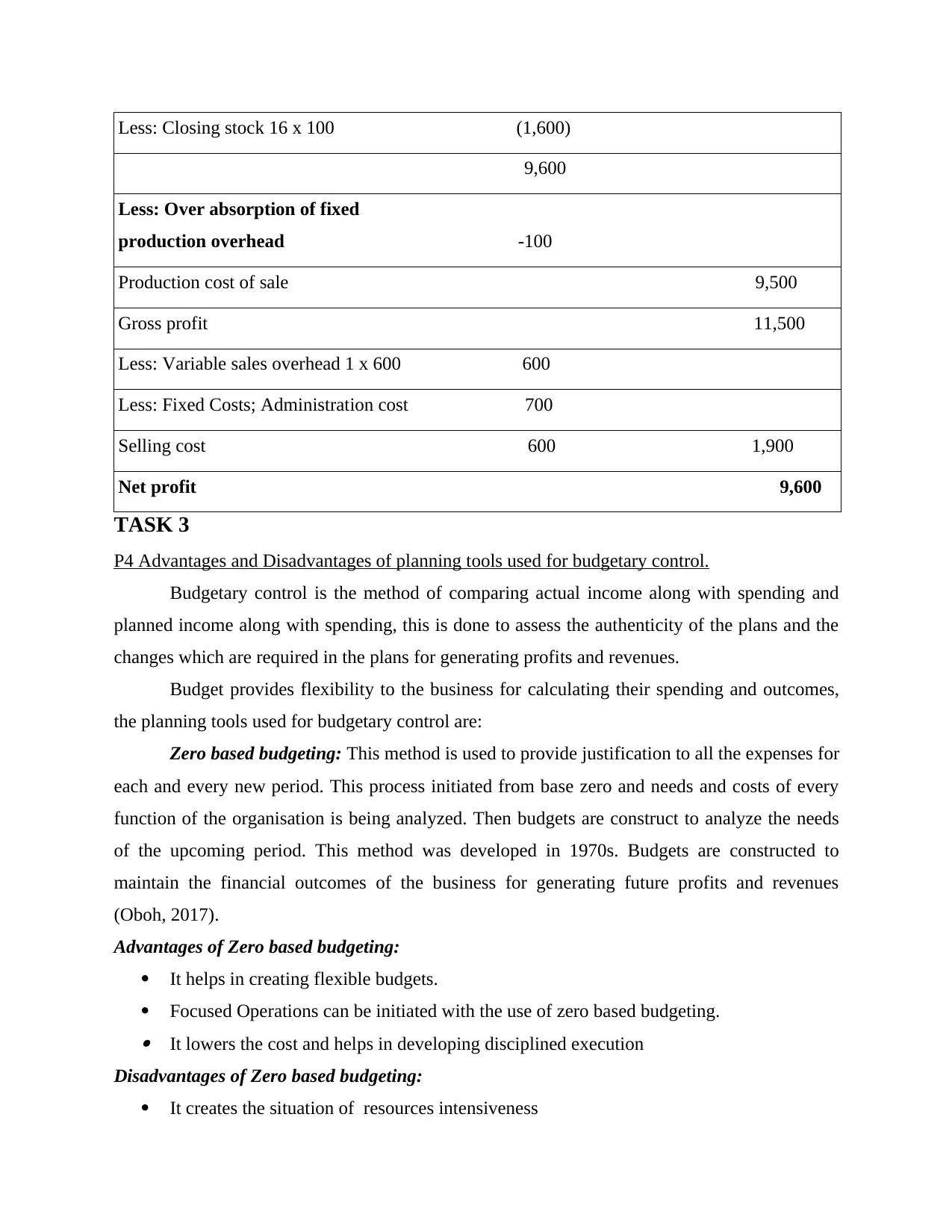

Statement of profit and loss on the basis of absorption costing:

Particulars Amount (in £)

Amount (in £)

Sales 700 x 35 21,000

Less: Cost of production 16 x 700 11,200

Less: Closing stock 16 x 100 (1,600)

…................................................................................. 9,600

Less: Over absorption of fixed

production overhead -100

Production cost of sale 9,500

Gross profit 11,500

Less: Variable sales overhead 1 x 600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Net profit 9,600

TASK 3

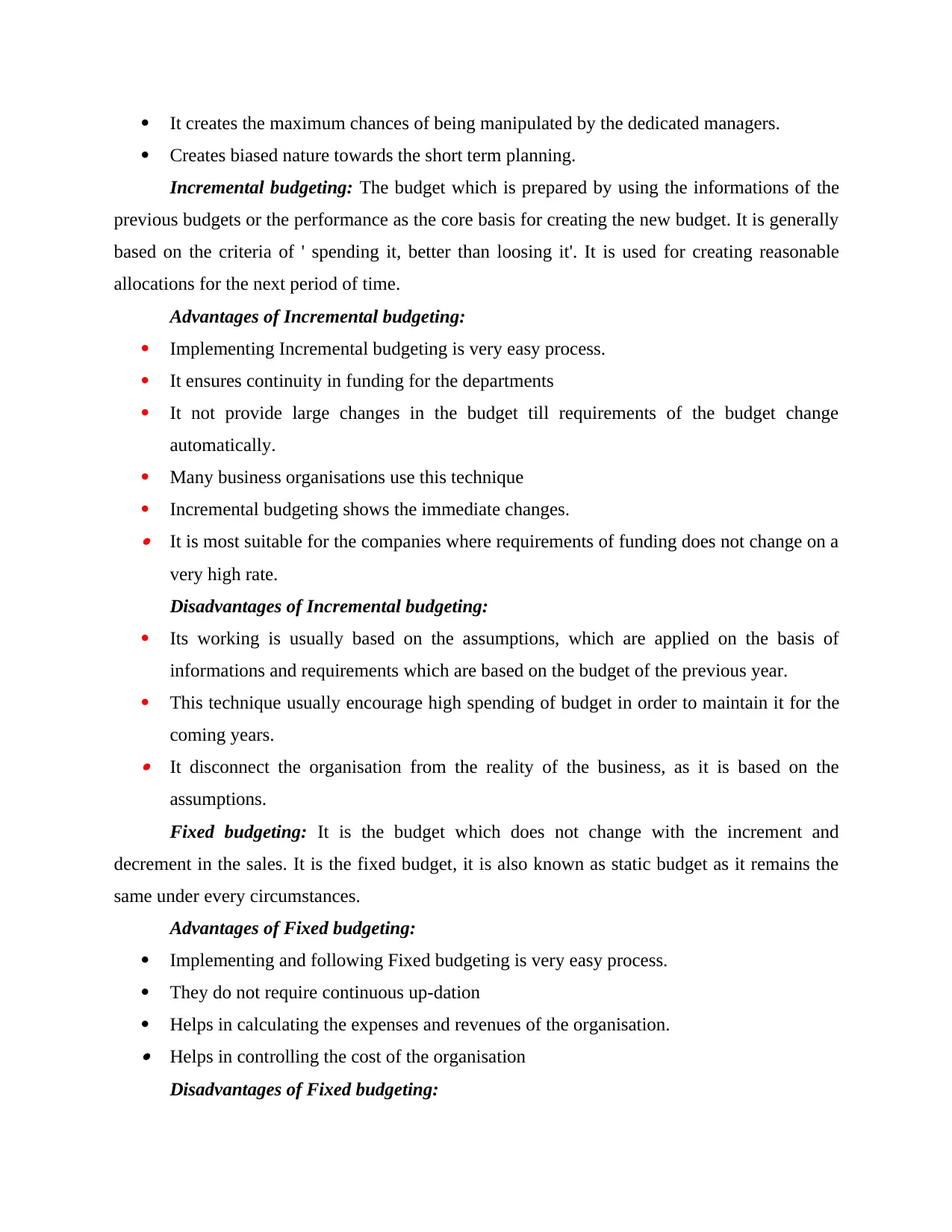

P4 Advantages and Disadvantages of planning tools used for budgetary control.

Budgetary control is the method of comparing actual income along with spending and

planned income along with spending, this is done to assess the authenticity of the plans and the

changes which are required in the plans for generating profits and revenues.

Budget provides flexibility to the business for calculating their spending and outcomes,

the planning tools used for budgetary control are:

Zero based budgeting: This method is used to provide justification to all the expenses for

each and every new period. This process initiated from base zero and needs and costs of every

function of the organisation is being analyzed. Then budgets are construct to analyze the needs

of the upcoming period. This method was developed in 1970s. Budgets are constructed to

maintain the financial outcomes of the business for generating future profits and revenues

(Oboh, 2017).

Advantages of Zero based budgeting:

It helps in creating flexible budgets.

Focused Operations can be initiated with the use of zero based budgeting. It lowers the cost and helps in developing disciplined execution

Disadvantages of Zero based budgeting:

It creates the situation of resources intensiveness

…................................................................................. 9,600

Less: Over absorption of fixed

production overhead -100

Production cost of sale 9,500

Gross profit 11,500

Less: Variable sales overhead 1 x 600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Net profit 9,600

TASK 3

P4 Advantages and Disadvantages of planning tools used for budgetary control.

Budgetary control is the method of comparing actual income along with spending and

planned income along with spending, this is done to assess the authenticity of the plans and the

changes which are required in the plans for generating profits and revenues.

Budget provides flexibility to the business for calculating their spending and outcomes,

the planning tools used for budgetary control are:

Zero based budgeting: This method is used to provide justification to all the expenses for

each and every new period. This process initiated from base zero and needs and costs of every

function of the organisation is being analyzed. Then budgets are construct to analyze the needs

of the upcoming period. This method was developed in 1970s. Budgets are constructed to

maintain the financial outcomes of the business for generating future profits and revenues

(Oboh, 2017).

Advantages of Zero based budgeting:

It helps in creating flexible budgets.

Focused Operations can be initiated with the use of zero based budgeting. It lowers the cost and helps in developing disciplined execution

Disadvantages of Zero based budgeting:

It creates the situation of resources intensiveness

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It creates the maximum chances of being manipulated by the dedicated managers.

Creates biased nature towards the short term planning.

Incremental budgeting: The budget which is prepared by using the informations of the

previous budgets or the performance as the core basis for creating the new budget. It is generally

based on the criteria of ' spending it, better than loosing it'. It is used for creating reasonable

allocations for the next period of time.

Advantages of Incremental budgeting:

Implementing Incremental budgeting is very easy process.

It ensures continuity in funding for the departments

It not provide large changes in the budget till requirements of the budget change

automatically.

Many business organisations use this technique

Incremental budgeting shows the immediate changes. It is most suitable for the companies where requirements of funding does not change on a

very high rate.

Disadvantages of Incremental budgeting:

Its working is usually based on the assumptions, which are applied on the basis of

informations and requirements which are based on the budget of the previous year.

This technique usually encourage high spending of budget in order to maintain it for the

coming years. It disconnect the organisation from the reality of the business, as it is based on the

assumptions.

Fixed budgeting: It is the budget which does not change with the increment and

decrement in the sales. It is the fixed budget, it is also known as static budget as it remains the

same under every circumstances.

Advantages of Fixed budgeting:

Implementing and following Fixed budgeting is very easy process.

They do not require continuous up-dation

Helps in calculating the expenses and revenues of the organisation. Helps in controlling the cost of the organisation

Disadvantages of Fixed budgeting:

Creates biased nature towards the short term planning.

Incremental budgeting: The budget which is prepared by using the informations of the

previous budgets or the performance as the core basis for creating the new budget. It is generally

based on the criteria of ' spending it, better than loosing it'. It is used for creating reasonable

allocations for the next period of time.

Advantages of Incremental budgeting:

Implementing Incremental budgeting is very easy process.

It ensures continuity in funding for the departments

It not provide large changes in the budget till requirements of the budget change

automatically.

Many business organisations use this technique

Incremental budgeting shows the immediate changes. It is most suitable for the companies where requirements of funding does not change on a

very high rate.

Disadvantages of Incremental budgeting:

Its working is usually based on the assumptions, which are applied on the basis of

informations and requirements which are based on the budget of the previous year.

This technique usually encourage high spending of budget in order to maintain it for the

coming years. It disconnect the organisation from the reality of the business, as it is based on the

assumptions.

Fixed budgeting: It is the budget which does not change with the increment and

decrement in the sales. It is the fixed budget, it is also known as static budget as it remains the

same under every circumstances.

Advantages of Fixed budgeting:

Implementing and following Fixed budgeting is very easy process.

They do not require continuous up-dation

Helps in calculating the expenses and revenues of the organisation. Helps in controlling the cost of the organisation

Disadvantages of Fixed budgeting:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

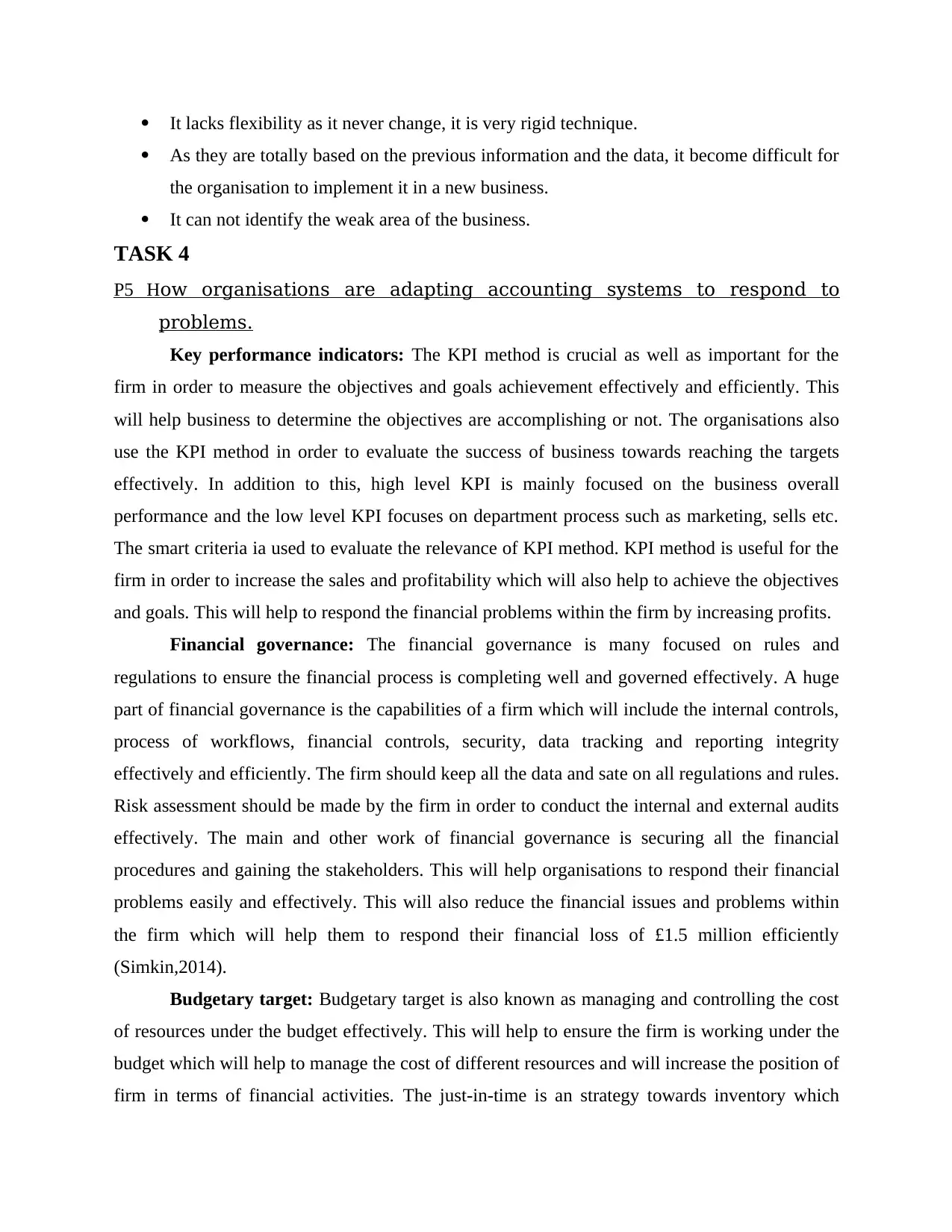

It lacks flexibility as it never change, it is very rigid technique.

As they are totally based on the previous information and the data, it become difficult for

the organisation to implement it in a new business.

It can not identify the weak area of the business.

TASK 4

P5 How organisations are adapting accounting systems to respond to

problems.

Key performance indicators: The KPI method is crucial as well as important for the

firm in order to measure the objectives and goals achievement effectively and efficiently. This

will help business to determine the objectives are accomplishing or not. The organisations also

use the KPI method in order to evaluate the success of business towards reaching the targets

effectively. In addition to this, high level KPI is mainly focused on the business overall

performance and the low level KPI focuses on department process such as marketing, sells etc.

The smart criteria ia used to evaluate the relevance of KPI method. KPI method is useful for the

firm in order to increase the sales and profitability which will also help to achieve the objectives

and goals. This will help to respond the financial problems within the firm by increasing profits.

Financial governance: The financial governance is many focused on rules and

regulations to ensure the financial process is completing well and governed effectively. A huge

part of financial governance is the capabilities of a firm which will include the internal controls,

process of workflows, financial controls, security, data tracking and reporting integrity

effectively and efficiently. The firm should keep all the data and sate on all regulations and rules.

Risk assessment should be made by the firm in order to conduct the internal and external audits

effectively. The main and other work of financial governance is securing all the financial

procedures and gaining the stakeholders. This will help organisations to respond their financial

problems easily and effectively. This will also reduce the financial issues and problems within

the firm which will help them to respond their financial loss of £1.5 million efficiently

(Simkin,2014).

Budgetary target: Budgetary target is also known as managing and controlling the cost

of resources under the budget effectively. This will help to ensure the firm is working under the

budget which will help to manage the cost of different resources and will increase the position of

firm in terms of financial activities. The just-in-time is an strategy towards inventory which

As they are totally based on the previous information and the data, it become difficult for

the organisation to implement it in a new business.

It can not identify the weak area of the business.

TASK 4

P5 How organisations are adapting accounting systems to respond to

problems.

Key performance indicators: The KPI method is crucial as well as important for the

firm in order to measure the objectives and goals achievement effectively and efficiently. This

will help business to determine the objectives are accomplishing or not. The organisations also

use the KPI method in order to evaluate the success of business towards reaching the targets

effectively. In addition to this, high level KPI is mainly focused on the business overall

performance and the low level KPI focuses on department process such as marketing, sells etc.

The smart criteria ia used to evaluate the relevance of KPI method. KPI method is useful for the

firm in order to increase the sales and profitability which will also help to achieve the objectives

and goals. This will help to respond the financial problems within the firm by increasing profits.

Financial governance: The financial governance is many focused on rules and

regulations to ensure the financial process is completing well and governed effectively. A huge

part of financial governance is the capabilities of a firm which will include the internal controls,

process of workflows, financial controls, security, data tracking and reporting integrity

effectively and efficiently. The firm should keep all the data and sate on all regulations and rules.

Risk assessment should be made by the firm in order to conduct the internal and external audits

effectively. The main and other work of financial governance is securing all the financial

procedures and gaining the stakeholders. This will help organisations to respond their financial

problems easily and effectively. This will also reduce the financial issues and problems within

the firm which will help them to respond their financial loss of £1.5 million efficiently

(Simkin,2014).

Budgetary target: Budgetary target is also known as managing and controlling the cost

of resources under the budget effectively. This will help to ensure the firm is working under the

budget which will help to manage the cost of different resources and will increase the position of

firm in terms of financial activities. The just-in-time is an strategy towards inventory which

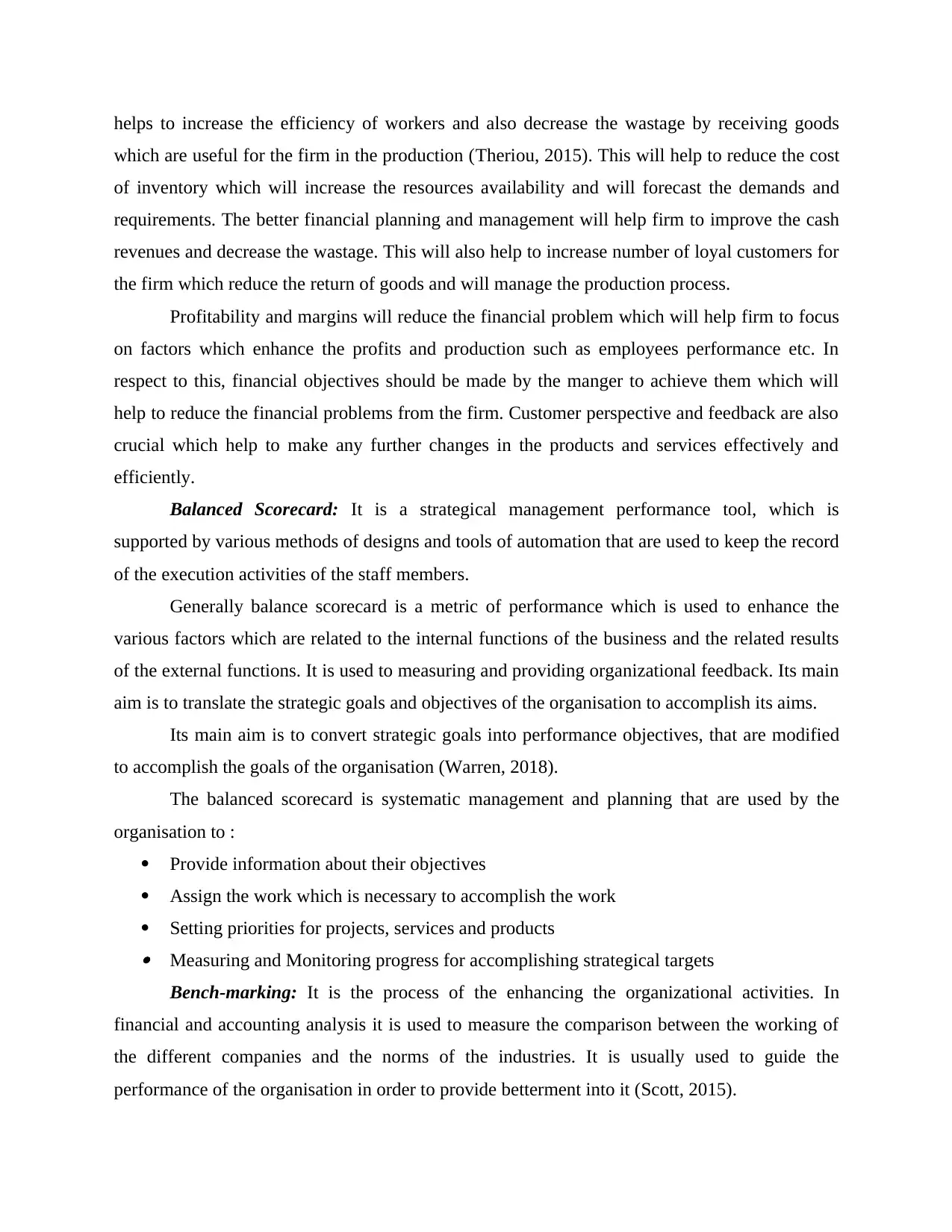

helps to increase the efficiency of workers and also decrease the wastage by receiving goods

which are useful for the firm in the production (Theriou, 2015). This will help to reduce the cost

of inventory which will increase the resources availability and will forecast the demands and

requirements. The better financial planning and management will help firm to improve the cash

revenues and decrease the wastage. This will also help to increase number of loyal customers for

the firm which reduce the return of goods and will manage the production process.

Profitability and margins will reduce the financial problem which will help firm to focus

on factors which enhance the profits and production such as employees performance etc. In

respect to this, financial objectives should be made by the manger to achieve them which will

help to reduce the financial problems from the firm. Customer perspective and feedback are also

crucial which help to make any further changes in the products and services effectively and

efficiently.

Balanced Scorecard: It is a strategical management performance tool, which is

supported by various methods of designs and tools of automation that are used to keep the record

of the execution activities of the staff members.

Generally balance scorecard is a metric of performance which is used to enhance the

various factors which are related to the internal functions of the business and the related results

of the external functions. It is used to measuring and providing organizational feedback. Its main

aim is to translate the strategic goals and objectives of the organisation to accomplish its aims.

Its main aim is to convert strategic goals into performance objectives, that are modified

to accomplish the goals of the organisation (Warren, 2018).

The balanced scorecard is systematic management and planning that are used by the

organisation to :

Provide information about their objectives

Assign the work which is necessary to accomplish the work

Setting priorities for projects, services and products Measuring and Monitoring progress for accomplishing strategical targets

Bench-marking: It is the process of the enhancing the organizational activities. In

financial and accounting analysis it is used to measure the comparison between the working of

the different companies and the norms of the industries. It is usually used to guide the

performance of the organisation in order to provide betterment into it (Scott, 2015).

which are useful for the firm in the production (Theriou, 2015). This will help to reduce the cost

of inventory which will increase the resources availability and will forecast the demands and

requirements. The better financial planning and management will help firm to improve the cash

revenues and decrease the wastage. This will also help to increase number of loyal customers for

the firm which reduce the return of goods and will manage the production process.

Profitability and margins will reduce the financial problem which will help firm to focus

on factors which enhance the profits and production such as employees performance etc. In

respect to this, financial objectives should be made by the manger to achieve them which will

help to reduce the financial problems from the firm. Customer perspective and feedback are also

crucial which help to make any further changes in the products and services effectively and

efficiently.

Balanced Scorecard: It is a strategical management performance tool, which is

supported by various methods of designs and tools of automation that are used to keep the record

of the execution activities of the staff members.

Generally balance scorecard is a metric of performance which is used to enhance the

various factors which are related to the internal functions of the business and the related results

of the external functions. It is used to measuring and providing organizational feedback. Its main

aim is to translate the strategic goals and objectives of the organisation to accomplish its aims.

Its main aim is to convert strategic goals into performance objectives, that are modified

to accomplish the goals of the organisation (Warren, 2018).

The balanced scorecard is systematic management and planning that are used by the

organisation to :

Provide information about their objectives

Assign the work which is necessary to accomplish the work

Setting priorities for projects, services and products Measuring and Monitoring progress for accomplishing strategical targets

Bench-marking: It is the process of the enhancing the organizational activities. In

financial and accounting analysis it is used to measure the comparison between the working of

the different companies and the norms of the industries. It is usually used to guide the

performance of the organisation in order to provide betterment into it (Scott, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.