Management Accounting Report: Principles, Systems, and Techniques

VerifiedAdded on 2021/02/19

|18

|3250

|496

Report

AI Summary

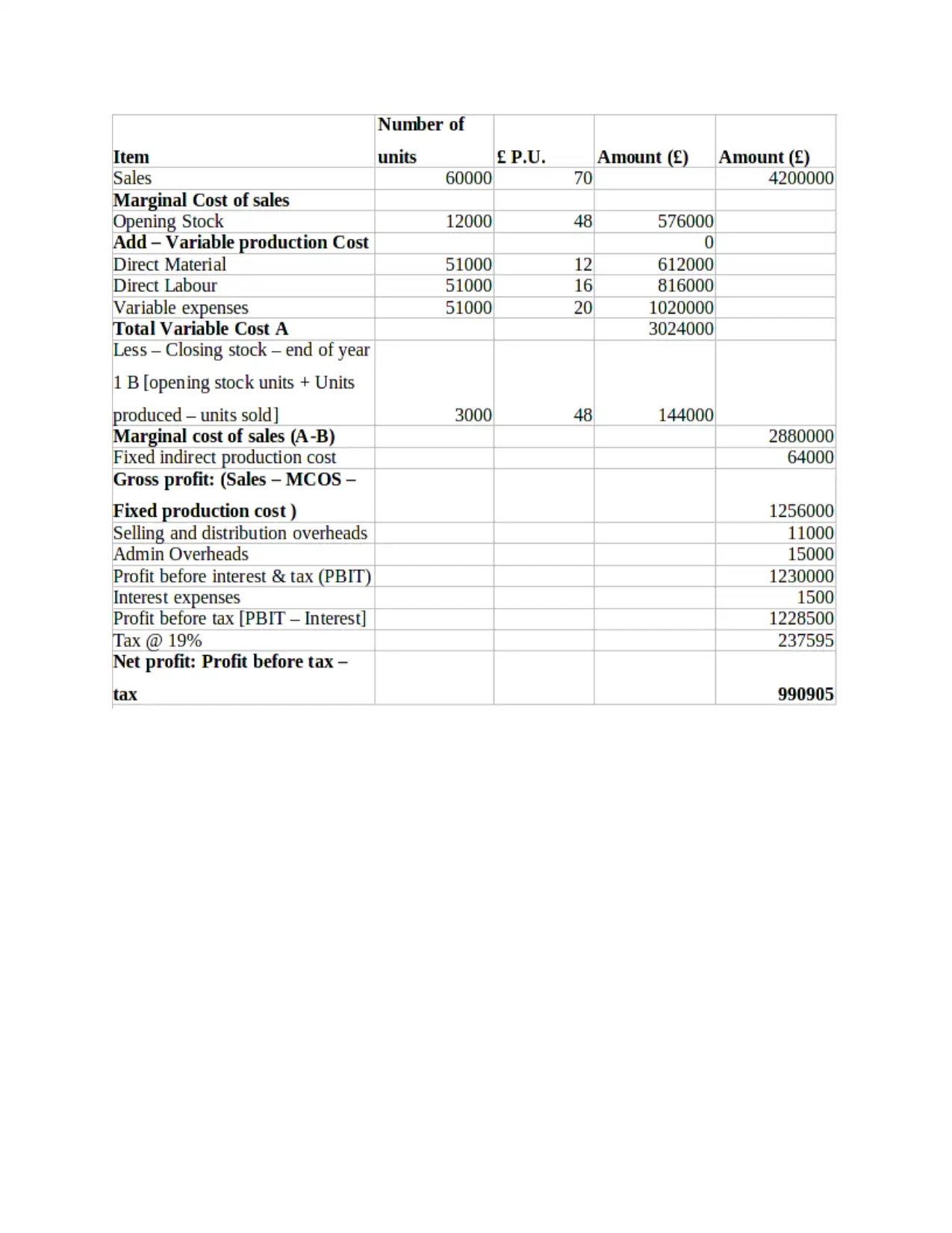

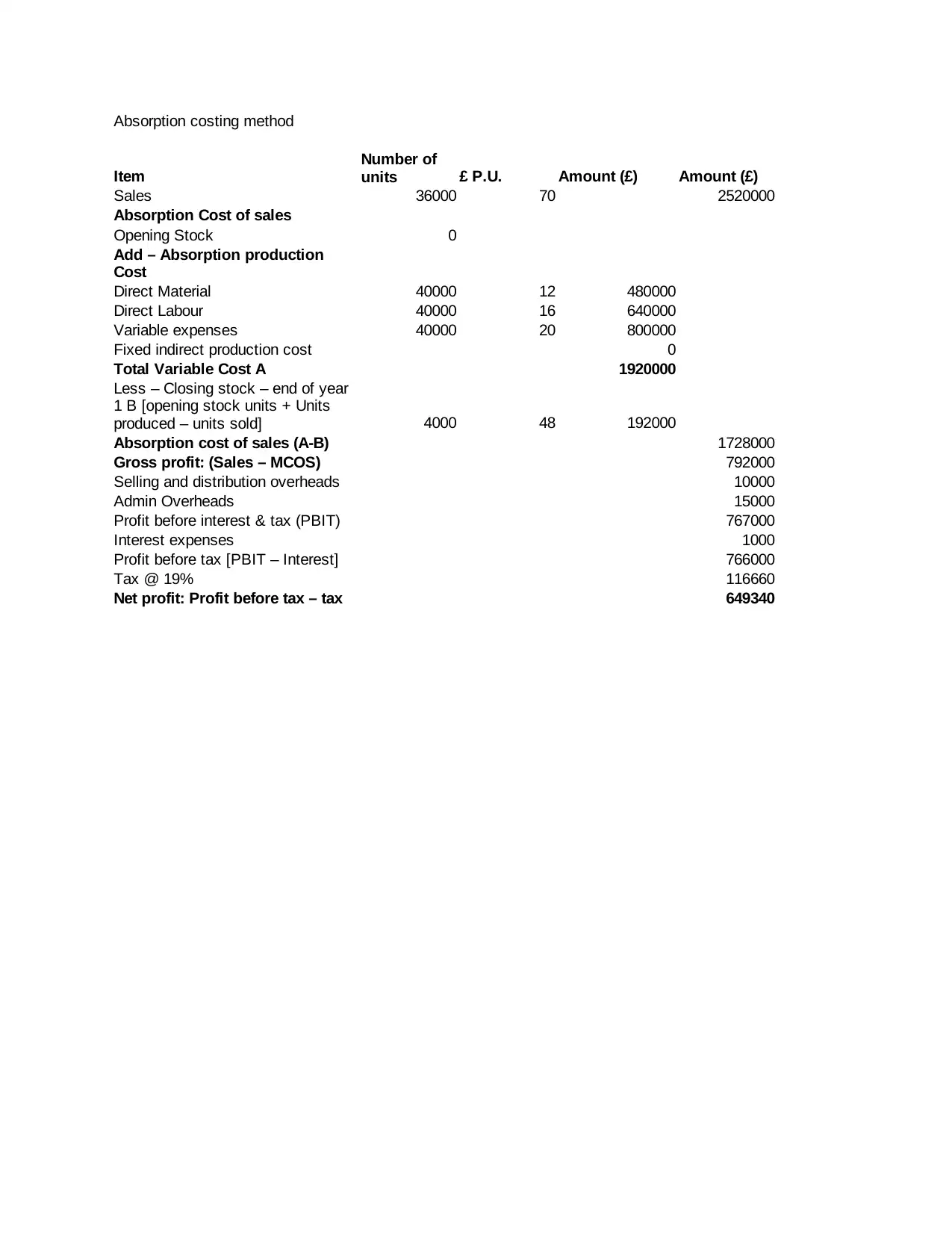

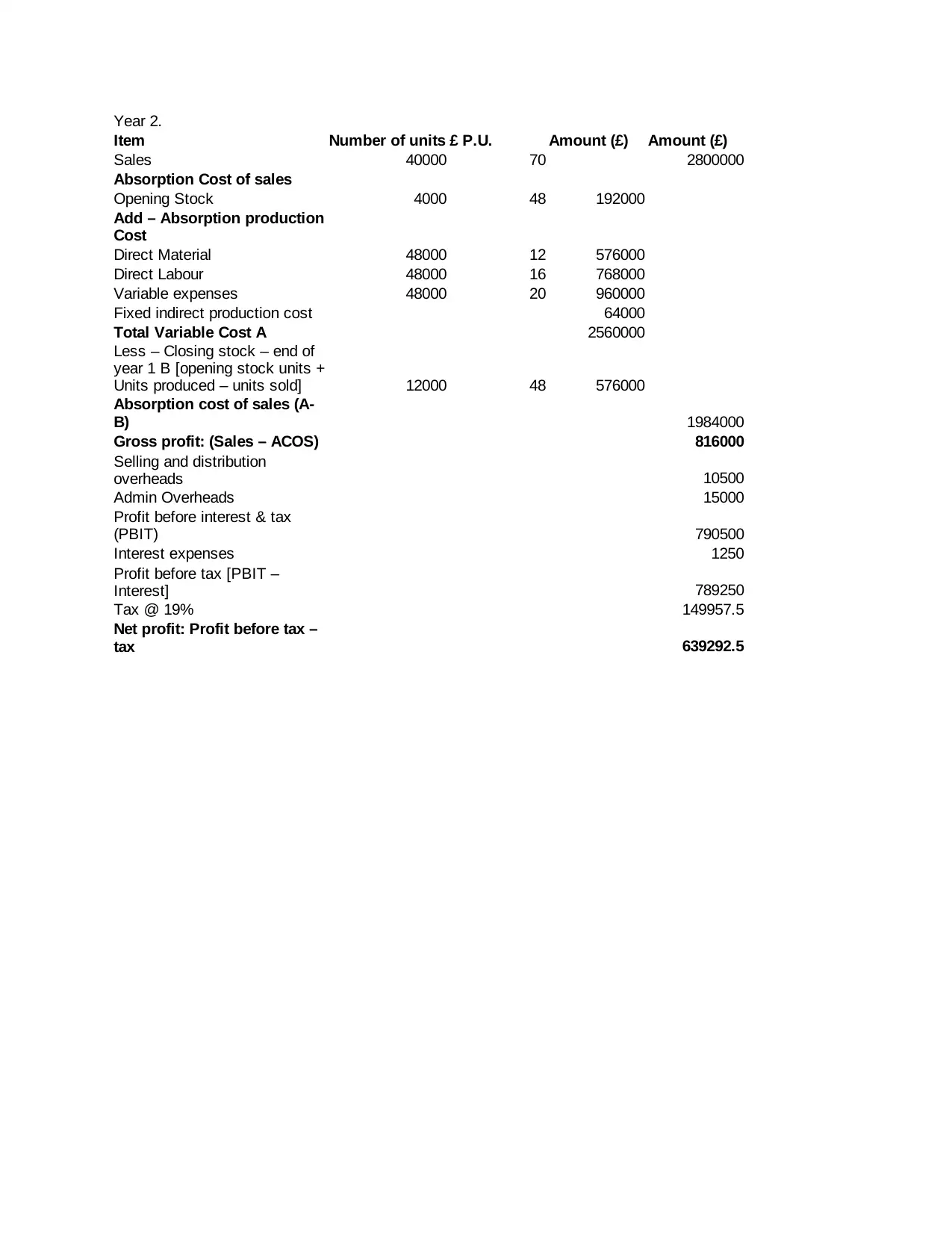

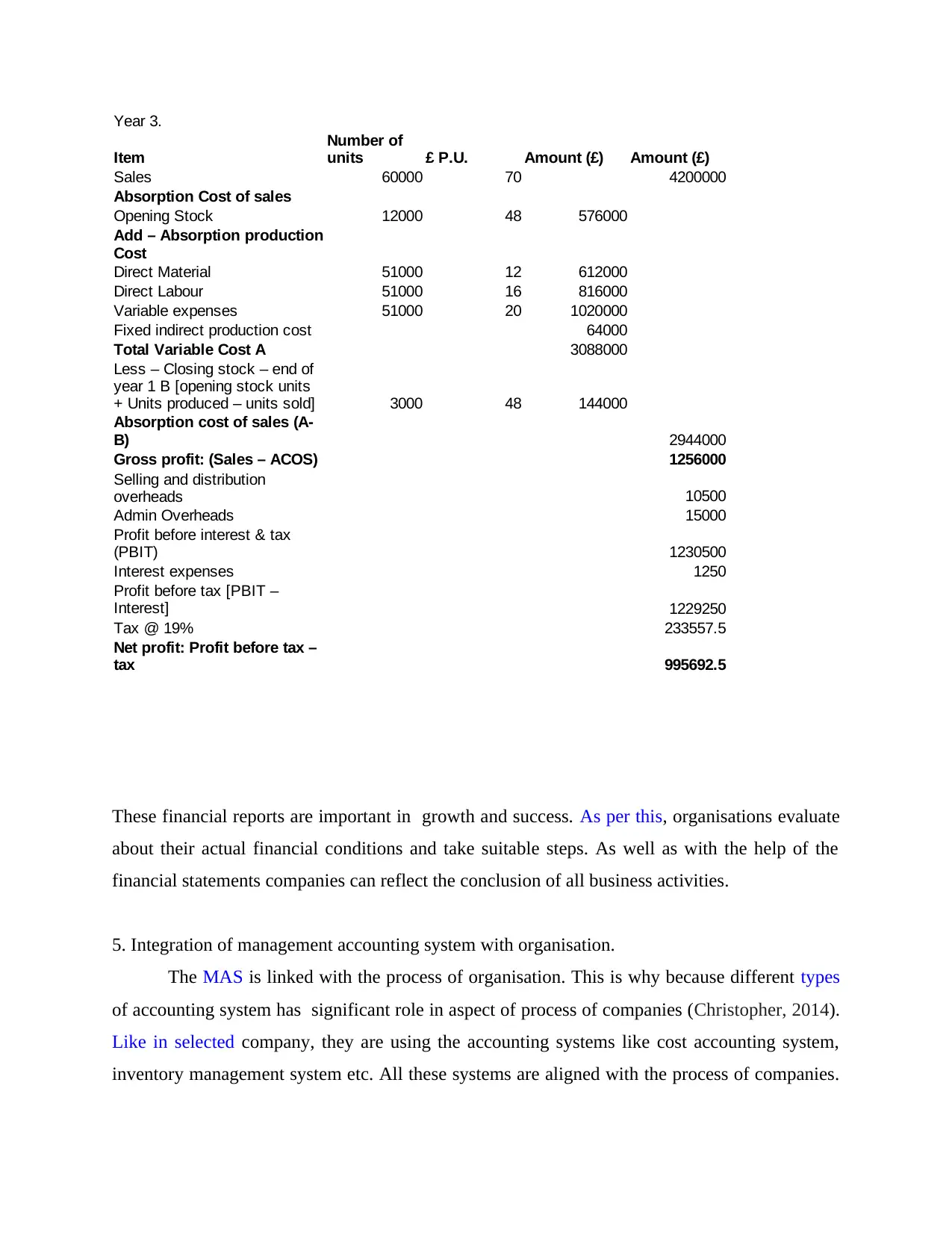

This report delves into the field of management accounting (MA), providing insights into its principles, systems, and techniques. The report analyzes MA's role within TPG Processing, a manufacturing company, and is divided into two parts. Part 1 covers MA principles (influence, relevance, value, trust), its role in decision-making and control, and various MA systems like price optimization, inventory management, and cost accounting. It also explores different reporting methods, including cost accounting and budget reports, and the use of marginal and absorption costing to produce income statements. Part 2 examines planning tools such as budgets (fixed, flexible, incremental, zero-based) and variance analysis, highlighting their benefits and drawbacks. The report concludes that MA is crucial for internal management, offering tools for cost reduction, job costing, inventory management, and price optimization, ultimately aiding in informed decision-making and financial success. The report emphasizes the integration of MAS within an organization's processes, and the importance of planning tools in budget preparation and forecasting.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.