Management Accounting Report: Cost Analysis, Budgeting, and Systems

VerifiedAdded on 2020/11/12

|17

|4418

|127

Report

AI Summary

This report delves into the realm of management accounting, focusing on its vital role in organizational decision-making and financial strategy. It begins by defining management accounting and contrasting it with financial accounting, highlighting the different types of management accounting systems such as cost-accounting, inventory management, job-costing, and price-optimizing systems. The report then explores various management accounting reporting methods, including budgets, performance reports, and aging reports. A significant portion of the report is dedicated to cost analysis techniques, with detailed explanations and examples of absorption costing and marginal costing. Income statements are generated using both methods, demonstrating how costs are allocated and how different costing approaches impact profitability. The report provides detailed financial statements for a company, TSR Pvt. Ltd., under varying production and sales scenarios. The report also discusses the merits and demerits of budgetary control and compares the adaptation of management accounting systems in response to financial problems.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management Accounting and essential requirements of various accounting systems.........1

P2. Different Methods for Management Accounting Reporting.................................................3

TASK 2............................................................................................................................................4

P3. Implementation of suitable Cost Analysis techniques to generate Income Statements........4

TASK 3............................................................................................................................................8

P4. Merits and Demerits of various planning tools used for Budgetary control.........................8

TASK 4..........................................................................................................................................11

P5. Comparing adaptation of Management Accounting Systems in response to financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

APPENDICES...............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management Accounting and essential requirements of various accounting systems.........1

P2. Different Methods for Management Accounting Reporting.................................................3

TASK 2............................................................................................................................................4

P3. Implementation of suitable Cost Analysis techniques to generate Income Statements........4

TASK 3............................................................................................................................................8

P4. Merits and Demerits of various planning tools used for Budgetary control.........................8

TASK 4..........................................................................................................................................11

P5. Comparing adaptation of Management Accounting Systems in response to financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

APPENDICES...............................................................................................................................15

INTRODUCTION

Management or Managerial Accounting refers to the systematic acquisition,

classification, interpretation and presentation of financial information to the management so that

they are able to make informed decisions and formulate policies. This is mainly related to

internal processes that help in proper coordination and control of activities so as to generate

maximum profits for the business. This report essentially discusses the various types of

accounting system employed by the companies, their role in formation of income statements,

budgetary controls and resolution of financial problems. In order to depict these with clarity, a

dynamic organisation, Zylla has been chosen whose management is looking for revamping of its

accounting system so as to make it more relevant to the changes that have occurred in its

operations over the years.

TASK 1

P1. Management Accounting and essential requirements of various accounting systems

Management Accounting:

Management Accounting can be defined as the process of collecting, recording and

reporting of business transactions and relevant statistical data so as to advance decision-making

among the managers of an enterprise (Apak and et.al., 2012). Management Accounting Systems

are one of the supporting structures that enable decision makers to form strategic conclusions.

This is achieved through the preparation and interpretation of relevant information as well as

their communication in the form of internal reports. These reports are usually maintained for

each management function operative in the organisation such as Finance, IT, Purchase

Department and others.

As the company needs to take into account all the relevant factors before coming to a

conclusion, it is important to integrate such reports in a comprehensible manner. This would

render a wholesome view of the critical areas that are required to be considered during the

decision-making process. The concept of management accounting can be dated back to the 19th

Century, Industrial Revolution. Since then it has undergone a lot of changes. In present scenario,

this framework plays a crucial role in connecting all functional activities of an enterprise by a

common thread.

1

Management or Managerial Accounting refers to the systematic acquisition,

classification, interpretation and presentation of financial information to the management so that

they are able to make informed decisions and formulate policies. This is mainly related to

internal processes that help in proper coordination and control of activities so as to generate

maximum profits for the business. This report essentially discusses the various types of

accounting system employed by the companies, their role in formation of income statements,

budgetary controls and resolution of financial problems. In order to depict these with clarity, a

dynamic organisation, Zylla has been chosen whose management is looking for revamping of its

accounting system so as to make it more relevant to the changes that have occurred in its

operations over the years.

TASK 1

P1. Management Accounting and essential requirements of various accounting systems

Management Accounting:

Management Accounting can be defined as the process of collecting, recording and

reporting of business transactions and relevant statistical data so as to advance decision-making

among the managers of an enterprise (Apak and et.al., 2012). Management Accounting Systems

are one of the supporting structures that enable decision makers to form strategic conclusions.

This is achieved through the preparation and interpretation of relevant information as well as

their communication in the form of internal reports. These reports are usually maintained for

each management function operative in the organisation such as Finance, IT, Purchase

Department and others.

As the company needs to take into account all the relevant factors before coming to a

conclusion, it is important to integrate such reports in a comprehensible manner. This would

render a wholesome view of the critical areas that are required to be considered during the

decision-making process. The concept of management accounting can be dated back to the 19th

Century, Industrial Revolution. Since then it has undergone a lot of changes. In present scenario,

this framework plays a crucial role in connecting all functional activities of an enterprise by a

common thread.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In general, management accounting tends to facilitate two important roles. One is to

provide meaningful information to the decision-makers and other is to influence as well as

facilitate judgements through communicating the results derived from them. It informs the

managers regarding important parameters that enable budgeting, investment appraisals,

forecasting, cost analysis for a given time period in an effective manner. However, one should

not confuse this concept with that of financial accounting. These terms may be used

interchangeably but have some features that distinct them from one another. They are:

Basis Management Accounting Financial Accounting

Aggregation Concerned with internal processes that are

employed to enable aggregation of

important accounting information.

Relates to aggregation of

accounting information through

preparation of financial statements.

Reporting

Focus

Concerned with internal reports as well as

efficiency and their communication thereof

to management.

Oriented towards preparation of

final reports and their

communication to stakeholders.

Systems Involves locating bottlenecks in operations

of a business as well as resolving them.

Concerns itself with final outcome

rather than the process involved in

generating that outcome.

Types of Management Accounting System:

An organisation may have different types of internal systems in place based on their

organisational needs and preferences. However, the management accounting systems can be

widely classified under following four heads:

Cost-Accounting Systems: This system assists in determination of costs to enable

managers in identifying various profit centre. Additionally, it provides essential control

metrics in regards to inventory valuation so as to maintain economies of scale in the

enterprise. It helps in efficient budgeting of inputs in relation to outputs by critically

examining individual products, services or jobs of different departments or operations in

a reasonably accurate manner (Chenhall and Moers, 2015).

Inventory Management Systems: Inventory Management system is one which helps in

keeping check of the stock located in company's warehouse so as to avoid overstock or

2

provide meaningful information to the decision-makers and other is to influence as well as

facilitate judgements through communicating the results derived from them. It informs the

managers regarding important parameters that enable budgeting, investment appraisals,

forecasting, cost analysis for a given time period in an effective manner. However, one should

not confuse this concept with that of financial accounting. These terms may be used

interchangeably but have some features that distinct them from one another. They are:

Basis Management Accounting Financial Accounting

Aggregation Concerned with internal processes that are

employed to enable aggregation of

important accounting information.

Relates to aggregation of

accounting information through

preparation of financial statements.

Reporting

Focus

Concerned with internal reports as well as

efficiency and their communication thereof

to management.

Oriented towards preparation of

final reports and their

communication to stakeholders.

Systems Involves locating bottlenecks in operations

of a business as well as resolving them.

Concerns itself with final outcome

rather than the process involved in

generating that outcome.

Types of Management Accounting System:

An organisation may have different types of internal systems in place based on their

organisational needs and preferences. However, the management accounting systems can be

widely classified under following four heads:

Cost-Accounting Systems: This system assists in determination of costs to enable

managers in identifying various profit centre. Additionally, it provides essential control

metrics in regards to inventory valuation so as to maintain economies of scale in the

enterprise. It helps in efficient budgeting of inputs in relation to outputs by critically

examining individual products, services or jobs of different departments or operations in

a reasonably accurate manner (Chenhall and Moers, 2015).

Inventory Management Systems: Inventory Management system is one which helps in

keeping check of the stock located in company's warehouse so as to avoid overstock or

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understock situations at any given point of time. By efficiently tracking stock quantities,

this system provides essential insights to make smarter inventory decisions by ensuring

no wastage is done on firm's part. This system helps in generating revenue and promotes

unhindered flow of production process.

Job-Costing Systems: This type of management accounting system helps in accumulation

of specific job-related manufacturing costs concerning an individual input or output. This

system is adopted by mainly those enterprises that produce customized products having

their own significant costs. For such organisations, implementation of this system is

necessary as it accurately classifies each project and helps in precise estimation of future

bids. Also, one can easily locate the problems for a specific job and resolve them much

quickly.

Price-Optimising Systems: As the name suggests, this system employs mathematical

analysis to forecast responses of customers regarding different prices of a product using

assorted channels. It focuses on three critical areas viz. Pricing strategies, profit centres

and value of product for firm as well as its customers. Employment of such systems help

in initial or promotional pricing of a new product as well as markdown or discount

pricing of an existing one. It is crucial system for any organisation looking for syncing its

business volume with profits so as to encourage customer retention (Hasniza Haron and

et.al., 2013).

As Zylla Company has undergone number of changes such as restructuring, acquisitions

as well as expansion in new markets and locations, it is important for the business to adopt such

internal systems so as to synchronize its operations with relevant changes that have occurred.

This would increase company's efficiency in regards to productivity as well as decision-making.

P2. Different Methods for Management Accounting Reporting

Management Accounting Reporting concerns itself with the communication and

presentation of useful statistical data or information to advance effective decision-making. For

this purpose, a company may use different reporting methods such as:

Budgets Report:

A Budget refers to a financial document that entails projections of future incomes and expenses.

This method also takes into account the historical accounting information to evidence such

projections regarding number of budgeted units to be sold as well as their prices. Such method of

3

this system provides essential insights to make smarter inventory decisions by ensuring

no wastage is done on firm's part. This system helps in generating revenue and promotes

unhindered flow of production process.

Job-Costing Systems: This type of management accounting system helps in accumulation

of specific job-related manufacturing costs concerning an individual input or output. This

system is adopted by mainly those enterprises that produce customized products having

their own significant costs. For such organisations, implementation of this system is

necessary as it accurately classifies each project and helps in precise estimation of future

bids. Also, one can easily locate the problems for a specific job and resolve them much

quickly.

Price-Optimising Systems: As the name suggests, this system employs mathematical

analysis to forecast responses of customers regarding different prices of a product using

assorted channels. It focuses on three critical areas viz. Pricing strategies, profit centres

and value of product for firm as well as its customers. Employment of such systems help

in initial or promotional pricing of a new product as well as markdown or discount

pricing of an existing one. It is crucial system for any organisation looking for syncing its

business volume with profits so as to encourage customer retention (Hasniza Haron and

et.al., 2013).

As Zylla Company has undergone number of changes such as restructuring, acquisitions

as well as expansion in new markets and locations, it is important for the business to adopt such

internal systems so as to synchronize its operations with relevant changes that have occurred.

This would increase company's efficiency in regards to productivity as well as decision-making.

P2. Different Methods for Management Accounting Reporting

Management Accounting Reporting concerns itself with the communication and

presentation of useful statistical data or information to advance effective decision-making. For

this purpose, a company may use different reporting methods such as:

Budgets Report:

A Budget refers to a financial document that entails projections of future incomes and expenses.

This method also takes into account the historical accounting information to evidence such

projections regarding number of budgeted units to be sold as well as their prices. Such method of

3

reporting assists a finance manager in carrying out strategic production planning decisions by

giving a comparative view of present as well as future revenues and expenditures.

Performance Reports:

These reports are produced by an organisation to review performance of the business as whole as

well as on functional level. These reports help in identifying the contributions of employees as

well as recognize under-performers. Consequently, offering a deep insight in productivity of

employees towards completion of various tasks or roles and responsibilities. Performance

Reports are important measuring criteria to ensure that implementation of strategies is executed

effectively to achieve overall goals of the business.

Ageing Reports:

These reporting methodologies provide resourceful insights regarding the defaulters and the

problems arising in the collection process of the business regarding their debtors. As these

documents give a detailed account of indebted clients based for different time periods, they

ensure that the credit policies of the business are effectively implemented and bad debts are

avoided.

By adopting such reporting methods, Zylla Company can compare its financial

performance in regards to costs incurred and profit generated as well as check how efficiently its

employees are performing their responsibilities. Also, it can keep track of its account receivables

by ensuring that its credit policies are wholesome and effectively followed across all

organisational levels.

TASK 2

P3. Implementation of suitable Cost Analysis techniques to generate Income Statements

Cost Analysis involves the process of assessing strategic activities that define the value

chain of a firm by investigating cost drivers governing them (Harris and Durden, 2012). It also

aims to examine future possibilities through minimization of costs and generation of additional

revenue to build firm's competitiveness in a sustainable manner. This is usually done by either

controlling the cost drivers or revamping the value chain activities itself.

While conducting a cost analysis, a manager may adopt one or more methodologies based

on their requirements and purpose of conducting such analysis. Here, two techniques have been

4

giving a comparative view of present as well as future revenues and expenditures.

Performance Reports:

These reports are produced by an organisation to review performance of the business as whole as

well as on functional level. These reports help in identifying the contributions of employees as

well as recognize under-performers. Consequently, offering a deep insight in productivity of

employees towards completion of various tasks or roles and responsibilities. Performance

Reports are important measuring criteria to ensure that implementation of strategies is executed

effectively to achieve overall goals of the business.

Ageing Reports:

These reporting methodologies provide resourceful insights regarding the defaulters and the

problems arising in the collection process of the business regarding their debtors. As these

documents give a detailed account of indebted clients based for different time periods, they

ensure that the credit policies of the business are effectively implemented and bad debts are

avoided.

By adopting such reporting methods, Zylla Company can compare its financial

performance in regards to costs incurred and profit generated as well as check how efficiently its

employees are performing their responsibilities. Also, it can keep track of its account receivables

by ensuring that its credit policies are wholesome and effectively followed across all

organisational levels.

TASK 2

P3. Implementation of suitable Cost Analysis techniques to generate Income Statements

Cost Analysis involves the process of assessing strategic activities that define the value

chain of a firm by investigating cost drivers governing them (Harris and Durden, 2012). It also

aims to examine future possibilities through minimization of costs and generation of additional

revenue to build firm's competitiveness in a sustainable manner. This is usually done by either

controlling the cost drivers or revamping the value chain activities itself.

While conducting a cost analysis, a manager may adopt one or more methodologies based

on their requirements and purpose of conducting such analysis. Here, two techniques have been

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

illustrated to showcase how income statements are generated on their basis. The two techniques

are Marginal and Absorption Costing. These are explained as under:

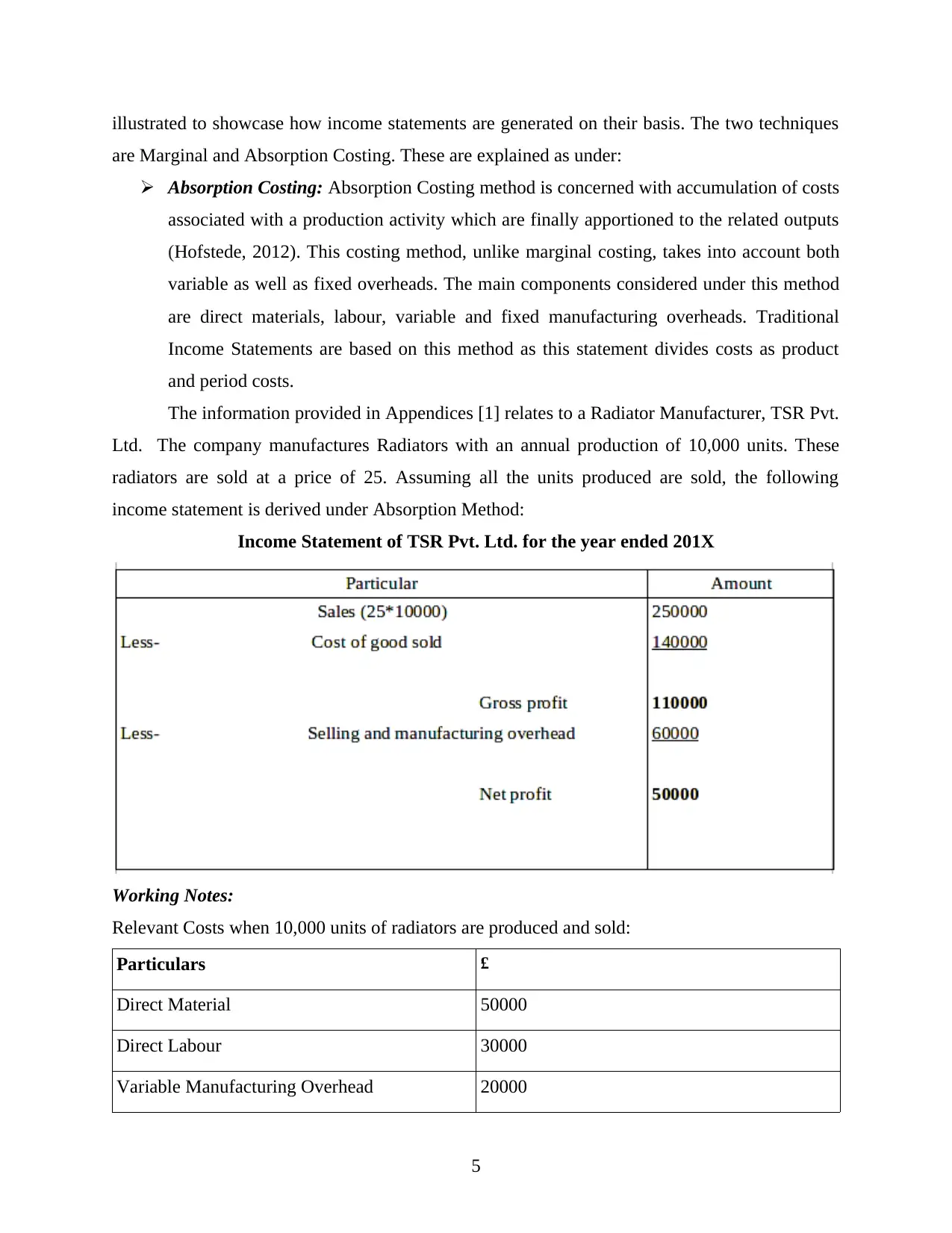

Absorption Costing: Absorption Costing method is concerned with accumulation of costs

associated with a production activity which are finally apportioned to the related outputs

(Hofstede, 2012). This costing method, unlike marginal costing, takes into account both

variable as well as fixed overheads. The main components considered under this method

are direct materials, labour, variable and fixed manufacturing overheads. Traditional

Income Statements are based on this method as this statement divides costs as product

and period costs.

The information provided in Appendices [1] relates to a Radiator Manufacturer, TSR Pvt.

Ltd. The company manufactures Radiators with an annual production of 10,000 units. These

radiators are sold at a price of 25. Assuming all the units produced are sold, the following

income statement is derived under Absorption Method:

Income Statement of TSR Pvt. Ltd. for the year ended 201X

Working Notes:

Relevant Costs when 10,000 units of radiators are produced and sold:

Particulars £

Direct Material 50000

Direct Labour 30000

Variable Manufacturing Overhead 20000

5

are Marginal and Absorption Costing. These are explained as under:

Absorption Costing: Absorption Costing method is concerned with accumulation of costs

associated with a production activity which are finally apportioned to the related outputs

(Hofstede, 2012). This costing method, unlike marginal costing, takes into account both

variable as well as fixed overheads. The main components considered under this method

are direct materials, labour, variable and fixed manufacturing overheads. Traditional

Income Statements are based on this method as this statement divides costs as product

and period costs.

The information provided in Appendices [1] relates to a Radiator Manufacturer, TSR Pvt.

Ltd. The company manufactures Radiators with an annual production of 10,000 units. These

radiators are sold at a price of 25. Assuming all the units produced are sold, the following

income statement is derived under Absorption Method:

Income Statement of TSR Pvt. Ltd. for the year ended 201X

Working Notes:

Relevant Costs when 10,000 units of radiators are produced and sold:

Particulars £

Direct Material 50000

Direct Labour 30000

Variable Manufacturing Overhead 20000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

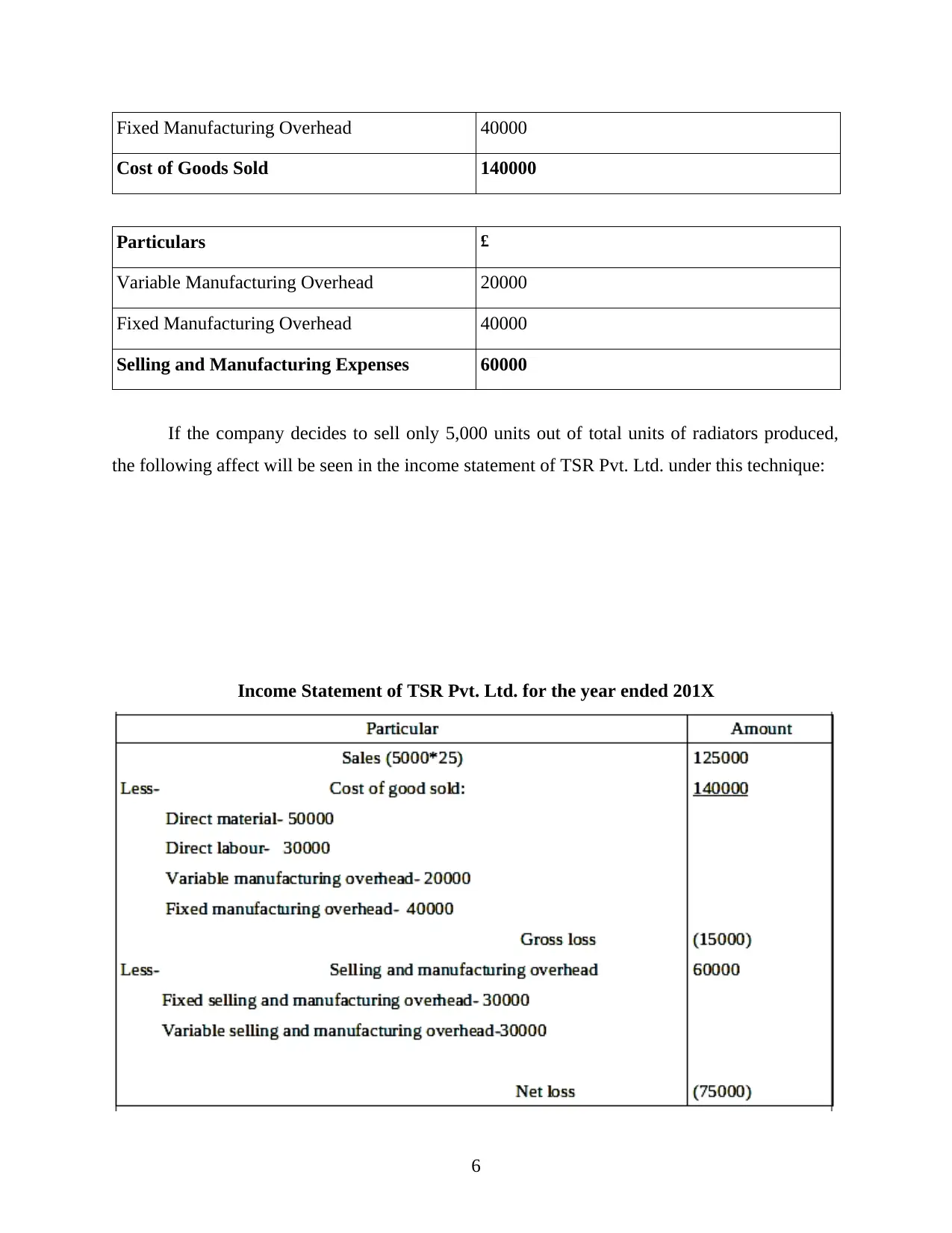

Fixed Manufacturing Overhead 40000

Cost of Goods Sold 140000

Particulars £

Variable Manufacturing Overhead 20000

Fixed Manufacturing Overhead 40000

Selling and Manufacturing Expenses 60000

If the company decides to sell only 5,000 units out of total units of radiators produced,

the following affect will be seen in the income statement of TSR Pvt. Ltd. under this technique:

Income Statement of TSR Pvt. Ltd. for the year ended 201X

6

Cost of Goods Sold 140000

Particulars £

Variable Manufacturing Overhead 20000

Fixed Manufacturing Overhead 40000

Selling and Manufacturing Expenses 60000

If the company decides to sell only 5,000 units out of total units of radiators produced,

the following affect will be seen in the income statement of TSR Pvt. Ltd. under this technique:

Income Statement of TSR Pvt. Ltd. for the year ended 201X

6

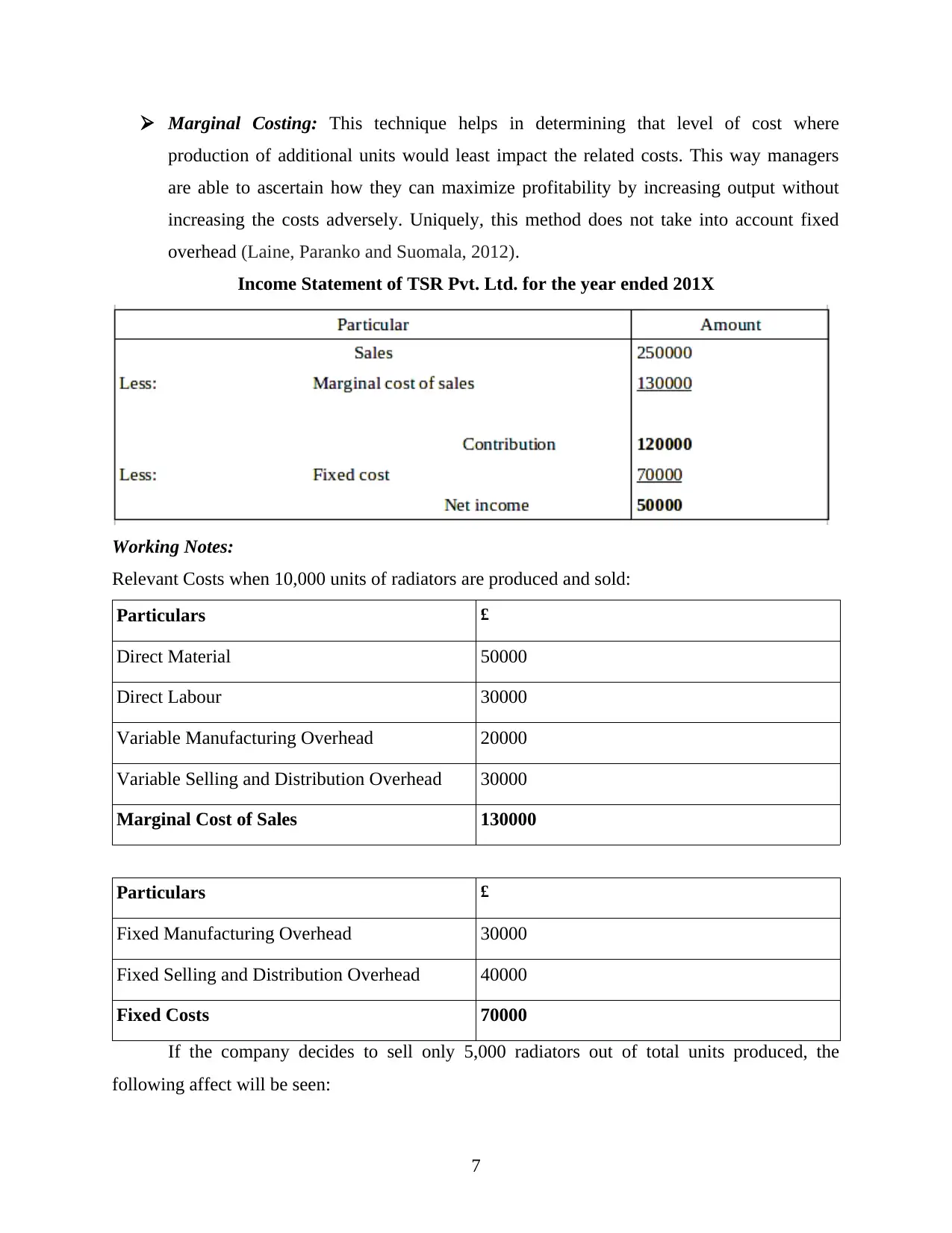

Marginal Costing: This technique helps in determining that level of cost where

production of additional units would least impact the related costs. This way managers

are able to ascertain how they can maximize profitability by increasing output without

increasing the costs adversely. Uniquely, this method does not take into account fixed

overhead (Laine, Paranko and Suomala, 2012).

Income Statement of TSR Pvt. Ltd. for the year ended 201X

Working Notes:

Relevant Costs when 10,000 units of radiators are produced and sold:

Particulars £

Direct Material 50000

Direct Labour 30000

Variable Manufacturing Overhead 20000

Variable Selling and Distribution Overhead 30000

Marginal Cost of Sales 130000

Particulars £

Fixed Manufacturing Overhead 30000

Fixed Selling and Distribution Overhead 40000

Fixed Costs 70000

If the company decides to sell only 5,000 radiators out of total units produced, the

following affect will be seen:

7

production of additional units would least impact the related costs. This way managers

are able to ascertain how they can maximize profitability by increasing output without

increasing the costs adversely. Uniquely, this method does not take into account fixed

overhead (Laine, Paranko and Suomala, 2012).

Income Statement of TSR Pvt. Ltd. for the year ended 201X

Working Notes:

Relevant Costs when 10,000 units of radiators are produced and sold:

Particulars £

Direct Material 50000

Direct Labour 30000

Variable Manufacturing Overhead 20000

Variable Selling and Distribution Overhead 30000

Marginal Cost of Sales 130000

Particulars £

Fixed Manufacturing Overhead 30000

Fixed Selling and Distribution Overhead 40000

Fixed Costs 70000

If the company decides to sell only 5,000 radiators out of total units produced, the

following affect will be seen:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income Statement of TSR Pvt. Ltd. for the year ended 201X

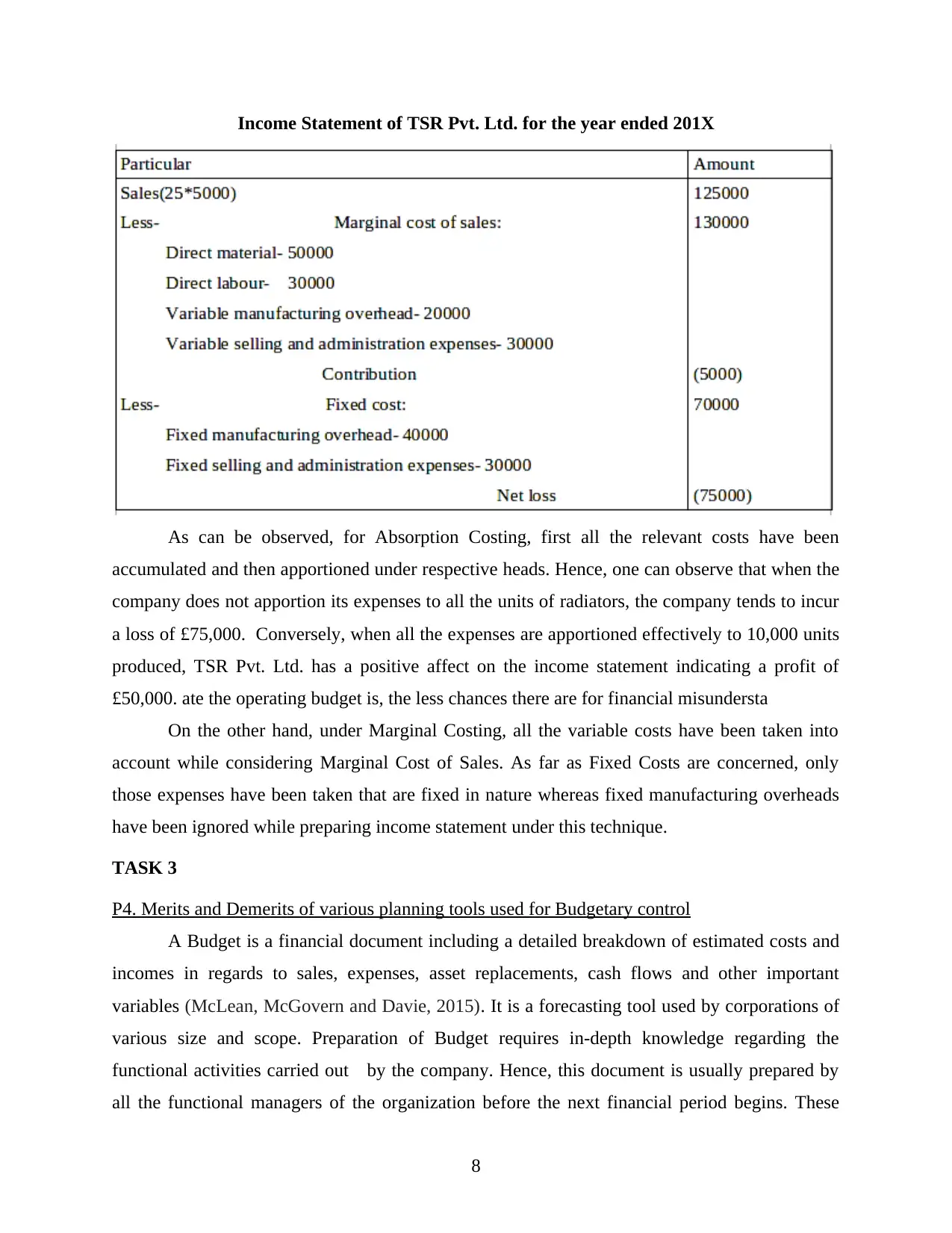

As can be observed, for Absorption Costing, first all the relevant costs have been

accumulated and then apportioned under respective heads. Hence, one can observe that when the

company does not apportion its expenses to all the units of radiators, the company tends to incur

a loss of £75,000. Conversely, when all the expenses are apportioned effectively to 10,000 units

produced, TSR Pvt. Ltd. has a positive affect on the income statement indicating a profit of

£50,000. ate the operating budget is, the less chances there are for financial misundersta

On the other hand, under Marginal Costing, all the variable costs have been taken into

account while considering Marginal Cost of Sales. As far as Fixed Costs are concerned, only

those expenses have been taken that are fixed in nature whereas fixed manufacturing overheads

have been ignored while preparing income statement under this technique.

TASK 3

P4. Merits and Demerits of various planning tools used for Budgetary control

A Budget is a financial document including a detailed breakdown of estimated costs and

incomes in regards to sales, expenses, asset replacements, cash flows and other important

variables (McLean, McGovern and Davie, 2015). It is a forecasting tool used by corporations of

various size and scope. Preparation of Budget requires in-depth knowledge regarding the

functional activities carried out by the company. Hence, this document is usually prepared by

all the functional managers of the organization before the next financial period begins. These

8

As can be observed, for Absorption Costing, first all the relevant costs have been

accumulated and then apportioned under respective heads. Hence, one can observe that when the

company does not apportion its expenses to all the units of radiators, the company tends to incur

a loss of £75,000. Conversely, when all the expenses are apportioned effectively to 10,000 units

produced, TSR Pvt. Ltd. has a positive affect on the income statement indicating a profit of

£50,000. ate the operating budget is, the less chances there are for financial misundersta

On the other hand, under Marginal Costing, all the variable costs have been taken into

account while considering Marginal Cost of Sales. As far as Fixed Costs are concerned, only

those expenses have been taken that are fixed in nature whereas fixed manufacturing overheads

have been ignored while preparing income statement under this technique.

TASK 3

P4. Merits and Demerits of various planning tools used for Budgetary control

A Budget is a financial document including a detailed breakdown of estimated costs and

incomes in regards to sales, expenses, asset replacements, cash flows and other important

variables (McLean, McGovern and Davie, 2015). It is a forecasting tool used by corporations of

various size and scope. Preparation of Budget requires in-depth knowledge regarding the

functional activities carried out by the company. Hence, this document is usually prepared by

all the functional managers of the organization before the next financial period begins. These

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

help in identification of variances or deviations by measuring the actual performance of

organisational activities for which the budget was prepared in the first place. While preparing a

budget, a manager must review its past assumptions that have been used in their last budget so as

to update them on the basis of current business environment. Also, the manager must review

bottlenecks that have been hindering the production process resulting in under-performance of

activities and bottom-line, consequently, hindering the growth of the company.

Budgetary Control refers to the process of goal-setting regarding financial performance

by managers in the form of budgets. These budgets provide a comparable view between actual

and standard performance. Through this, managers can ascertain easily which criteria was duly

met with and which failed. Such procedures help the business in proper allocation of resources so

as to meet their strategic goals that the business aims to achieve in a given financial period.

Through Budgetary Control, management will be able to minimize the problems and develop an

alternative course of plan that can avoid such occurrences in future (Otley, 2016).

As Zylla has been involved in acquisition and expansion activities, it is important for the

company to plan ahead regarding its future strategic actions. For this, the company would have

budgetary control systems in place that would set-up both overall as well as functional budgets at

the beginning of the each period. This will act as an incentive for managers and improve their

future performance, thus, leading to overall increase in productivity of organisation's operations.

Also, budgetary control would ensure that there is no deviation of performance as well as costs

in and among the departments. For this purpose, a company may choose from an assortment of

planning tools to help organisations and their members reach their goals effectively. The two

main planning tools used to exercise budgetary controls have been explained below in detail:

Capital Budgeting:

This is one of the most widely used planning tool by organisations to exert budgetary control

over their operational activities (Salterio, 2015). Capital Budgeting mainly looks after the income

and expenditures that are capital in nature and include large influx as well as efflux of cash flows

from the business. Commonly, these are proposed investment projects that a business is

considering to undertake in future. Under budgetary control, this technique helps in estimating

the amount of investments or finance the business would require to complete a certain project,

resulting in forecasting of expected cash inflows and outflows in an efficient manner and

9

organisational activities for which the budget was prepared in the first place. While preparing a

budget, a manager must review its past assumptions that have been used in their last budget so as

to update them on the basis of current business environment. Also, the manager must review

bottlenecks that have been hindering the production process resulting in under-performance of

activities and bottom-line, consequently, hindering the growth of the company.

Budgetary Control refers to the process of goal-setting regarding financial performance

by managers in the form of budgets. These budgets provide a comparable view between actual

and standard performance. Through this, managers can ascertain easily which criteria was duly

met with and which failed. Such procedures help the business in proper allocation of resources so

as to meet their strategic goals that the business aims to achieve in a given financial period.

Through Budgetary Control, management will be able to minimize the problems and develop an

alternative course of plan that can avoid such occurrences in future (Otley, 2016).

As Zylla has been involved in acquisition and expansion activities, it is important for the

company to plan ahead regarding its future strategic actions. For this, the company would have

budgetary control systems in place that would set-up both overall as well as functional budgets at

the beginning of the each period. This will act as an incentive for managers and improve their

future performance, thus, leading to overall increase in productivity of organisation's operations.

Also, budgetary control would ensure that there is no deviation of performance as well as costs

in and among the departments. For this purpose, a company may choose from an assortment of

planning tools to help organisations and their members reach their goals effectively. The two

main planning tools used to exercise budgetary controls have been explained below in detail:

Capital Budgeting:

This is one of the most widely used planning tool by organisations to exert budgetary control

over their operational activities (Salterio, 2015). Capital Budgeting mainly looks after the income

and expenditures that are capital in nature and include large influx as well as efflux of cash flows

from the business. Commonly, these are proposed investment projects that a business is

considering to undertake in future. Under budgetary control, this technique helps in estimating

the amount of investments or finance the business would require to complete a certain project,

resulting in forecasting of expected cash inflows and outflows in an efficient manner and

9

organisation of finance in advance. For Zylla, this planning tool can pose to have following

benefits and limitations: Merits: This planning tool helps in estimating as well as assessing various risks that are

attached to a given investment opportunity. As a result, managers of Zylla would be able

to make accurate strategic decisions in relation to long-term investments. Also, this

would technique would ensure adequate control over expenditure done on projects

consciously.

Demerits: As investment decisions are made taking the long-tern benefits into

consideration, it tends to irreversible in nature. Additionally, future uncertainty can

always hamper the estimations and assumptions taken into consideration while indulging

in the process of Capital Budgeting.

Operating Budgeting:

An Operating Budget consists of revenue, capital, variable and fixed costs, non-cash and non-

operating expenses that are estimated to be gained or incurred for a given period of time

(Shields, 2015). This budget helps in creation of financial plan so as to control the debt

obligations of the business and help the company grow sustainably over time. Such budgeting

tools if implemented successfully can help an organisation such as Zylla to attract valuable

investment opportunities in future. This budget is one of the most basic planning tool adopted by

the businesses worldwide in order to exercise effective budgetary control over its incomes and

expenditures. For Zylla, this planning tool can pose to have following benefits and limitations: Merits: This tool can help managers to plan ahead of future expenses and manage their

incomes for the same regarding any future contingency such as repairs, maintenance and

tax obligations. If formulated accurately, it can also prevent financial misunderstandings

providing financial investment opportunities to external users.

Demerits: Preparation of Operating Budgeting can prove to be a time-consuming process.

In addition to this, failure to meet the budgeted results by one department may affect the

performance of other departments adversely leading to demotivation to contribute fully to

their roles and responsibilities.

However, in order to overcome the limitations of these budgeting planning tools, Zylla

may undertake alternate budgeting models such as Static Budgeting, Zero-based Budgeting,

Flexible or Incremental Budgeting, a rolling budget or forecast.

10

benefits and limitations: Merits: This planning tool helps in estimating as well as assessing various risks that are

attached to a given investment opportunity. As a result, managers of Zylla would be able

to make accurate strategic decisions in relation to long-term investments. Also, this

would technique would ensure adequate control over expenditure done on projects

consciously.

Demerits: As investment decisions are made taking the long-tern benefits into

consideration, it tends to irreversible in nature. Additionally, future uncertainty can

always hamper the estimations and assumptions taken into consideration while indulging

in the process of Capital Budgeting.

Operating Budgeting:

An Operating Budget consists of revenue, capital, variable and fixed costs, non-cash and non-

operating expenses that are estimated to be gained or incurred for a given period of time

(Shields, 2015). This budget helps in creation of financial plan so as to control the debt

obligations of the business and help the company grow sustainably over time. Such budgeting

tools if implemented successfully can help an organisation such as Zylla to attract valuable

investment opportunities in future. This budget is one of the most basic planning tool adopted by

the businesses worldwide in order to exercise effective budgetary control over its incomes and

expenditures. For Zylla, this planning tool can pose to have following benefits and limitations: Merits: This tool can help managers to plan ahead of future expenses and manage their

incomes for the same regarding any future contingency such as repairs, maintenance and

tax obligations. If formulated accurately, it can also prevent financial misunderstandings

providing financial investment opportunities to external users.

Demerits: Preparation of Operating Budgeting can prove to be a time-consuming process.

In addition to this, failure to meet the budgeted results by one department may affect the

performance of other departments adversely leading to demotivation to contribute fully to

their roles and responsibilities.

However, in order to overcome the limitations of these budgeting planning tools, Zylla

may undertake alternate budgeting models such as Static Budgeting, Zero-based Budgeting,

Flexible or Incremental Budgeting, a rolling budget or forecast.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.