Management Accounting Report: IMDA Tech Case Study Analysis

VerifiedAdded on 2020/02/03

|13

|4109

|37

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the case study of IMDA Tech. It begins with an introduction to management accounting, differentiating it from financial accounting and exploring its various applications in business decision-making, planning, and control. The report then delves into different types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. A significant portion is dedicated to comparing absorption and marginal costing methods, illustrating their application through income statements and reconciliation. The report also touches upon the conceptualization of the balance scorecard. The assignment covers various aspects of management accounting, including costing, budgeting, and financial statement analysis to aid in effective decision-making within a business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...................................................................................................................................................3

TASK 1....................................................................................................................................................................3

P1. Definition of M.A and differ with financial accounting...............................................................................3

P2.Types of M.A systems with respect to several sections.................................................................................5

TASK 2....................................................................................................................................................................6

P3 Income statements of absorption and marginal costing.................................................................................6

TASK 3....................................................................................................................................................................8

P4 Types of budgets............................................................................................................................................8

TASK 4..................................................................................................................................................................10

P5 Balance score card conceptualization..........................................................................................................10

CONCLUSION.....................................................................................................................................................11

REFERENCES......................................................................................................................................................12

INTRODUCTION...................................................................................................................................................3

TASK 1....................................................................................................................................................................3

P1. Definition of M.A and differ with financial accounting...............................................................................3

P2.Types of M.A systems with respect to several sections.................................................................................5

TASK 2....................................................................................................................................................................6

P3 Income statements of absorption and marginal costing.................................................................................6

TASK 3....................................................................................................................................................................8

P4 Types of budgets............................................................................................................................................8

TASK 4..................................................................................................................................................................10

P5 Balance score card conceptualization..........................................................................................................10

CONCLUSION.....................................................................................................................................................11

REFERENCES......................................................................................................................................................12

INTRODUCTION

Management accounting is the procedure which helps an organisation to keep record of their data. It

enables them to make provision of their financial data and advice to the company to use such provision in

development of an organisation .There are wide variety of a scopes associated with this type of accounting.

Some of them are directing plan of action, execution and risk governance. It aims at applying an individual

professionalism related with the accounting terms in o preparing and presenting the accountancy and money

management determinations. This is done according to envisages several regulations and policies at the

management level related in order to plan and coordinate the overall functional financial structure. The auditors

of management are considered as the worth Making. IMDA tech was established in 15 June 2015 to determine

the actual global trade issues. The basic motive of this company is to adopt modern innovative technology and

come up with new concepts and ideas by neglecting the old methods to resolve difficulties for attaining better

results. Moreover for a new plan firm creates a budgetary plan in which all the advantages and disadvantages

are going to elaborate briefly (Yahya-Zadeh, 2011).

TASK 1

P1. Definition of M.A and differ with financial accounting

Management accounting is a type of auditing process related with governing all the rules and regulations

according to the financial, banking, budgeting and investment sources. In general it is based on a

profession of partnership in management decision making, planning and executive

management system with the help of financial reporting expertise and involving

management in developing and implementing administrative plan of action. The basic

functions of management accounting are cash flow analysis, ratio analysis, fund flow

analysis and budgetary control, it is used in increasing efficiency in the operating

company, maximizing profitability, determination of simple and financial statements,

taking complex business decisions and controlling business. Distinctions of

management and financial accounting are as follows:-

Fiscal accountancy Management accounting

Financial accountancy is based on calculating

methods of ratio assessments.

This is carried out with the future and existing

aspects of budgetary control

Management accounting is the procedure which helps an organisation to keep record of their data. It

enables them to make provision of their financial data and advice to the company to use such provision in

development of an organisation .There are wide variety of a scopes associated with this type of accounting.

Some of them are directing plan of action, execution and risk governance. It aims at applying an individual

professionalism related with the accounting terms in o preparing and presenting the accountancy and money

management determinations. This is done according to envisages several regulations and policies at the

management level related in order to plan and coordinate the overall functional financial structure. The auditors

of management are considered as the worth Making. IMDA tech was established in 15 June 2015 to determine

the actual global trade issues. The basic motive of this company is to adopt modern innovative technology and

come up with new concepts and ideas by neglecting the old methods to resolve difficulties for attaining better

results. Moreover for a new plan firm creates a budgetary plan in which all the advantages and disadvantages

are going to elaborate briefly (Yahya-Zadeh, 2011).

TASK 1

P1. Definition of M.A and differ with financial accounting

Management accounting is a type of auditing process related with governing all the rules and regulations

according to the financial, banking, budgeting and investment sources. In general it is based on a

profession of partnership in management decision making, planning and executive

management system with the help of financial reporting expertise and involving

management in developing and implementing administrative plan of action. The basic

functions of management accounting are cash flow analysis, ratio analysis, fund flow

analysis and budgetary control, it is used in increasing efficiency in the operating

company, maximizing profitability, determination of simple and financial statements,

taking complex business decisions and controlling business. Distinctions of

management and financial accounting are as follows:-

Fiscal accountancy Management accounting

Financial accountancy is based on calculating

methods of ratio assessments.

This is carried out with the future and existing

aspects of budgetary control

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The assessment is carried out through

quantitative methods of several graphs ,

diagrams, tales and calculations.

Measuring of certain variations and

assessment of decisions are carried out through

the budget estimations.

The decisions are made as per the cash flow

analysis.

Enterprise prognostication defines a fresh

concepts and methods of improvements which

needed enormous amount of a flowing capital.

Basically its an accounting related with the

financial terms therefore it posses a deficiency

at the success level of the undertaking.

For better evaluating projection there is great

need of generating an effective decision.

These are the above functions and differences with respect to the financial and administrative accounting.

Importance of M.A information at the decisions

M.A is based on planning and decision support criteria in the field of

management. It is related with any transactions or banking sources instead of related

with business decision making, planning, organizing, controlling, staffing and directing.

According to IMDA tech management accounting is a non financial data capture

method. It involves several steps of implementing and controlling operations related

with audits. Planning involves what when where and how to make plans in a systematic

and organised way. Organising is considered through complete systematic process of

maintaining a consistency level ( Quattrone, 2010). Directing is done through managers by

giving orders by following instructions or controlling is the process of dominance.

Staffing is carried out by making an organization fully professional and follow certain

rules and regulations in the organizations. Management accounting is generally based

on additive and wrapped costing, adjustive operation and cost based planning,

budgeting and prediction, processing products, channel, customer plan of action

adaptations and enterprise improvement. There are several sections at the

administration level. These are manufacturing , supply unit , procurement, human

resource , commercial enterprise and investigation and improvement . According to

these sections the decisions are made as follows.

Governing plan of action – this is a plan of action process in relation with audit

governance for making advancements in the functions or duty of accountant in order to

consider as a strategic partner in the organization (Angelkort, 2011).

Execution direction – this based on the further implementation in business

decision making practices and directing organizational performance.

quantitative methods of several graphs ,

diagrams, tales and calculations.

Measuring of certain variations and

assessment of decisions are carried out through

the budget estimations.

The decisions are made as per the cash flow

analysis.

Enterprise prognostication defines a fresh

concepts and methods of improvements which

needed enormous amount of a flowing capital.

Basically its an accounting related with the

financial terms therefore it posses a deficiency

at the success level of the undertaking.

For better evaluating projection there is great

need of generating an effective decision.

These are the above functions and differences with respect to the financial and administrative accounting.

Importance of M.A information at the decisions

M.A is based on planning and decision support criteria in the field of

management. It is related with any transactions or banking sources instead of related

with business decision making, planning, organizing, controlling, staffing and directing.

According to IMDA tech management accounting is a non financial data capture

method. It involves several steps of implementing and controlling operations related

with audits. Planning involves what when where and how to make plans in a systematic

and organised way. Organising is considered through complete systematic process of

maintaining a consistency level ( Quattrone, 2010). Directing is done through managers by

giving orders by following instructions or controlling is the process of dominance.

Staffing is carried out by making an organization fully professional and follow certain

rules and regulations in the organizations. Management accounting is generally based

on additive and wrapped costing, adjustive operation and cost based planning,

budgeting and prediction, processing products, channel, customer plan of action

adaptations and enterprise improvement. There are several sections at the

administration level. These are manufacturing , supply unit , procurement, human

resource , commercial enterprise and investigation and improvement . According to

these sections the decisions are made as follows.

Governing plan of action – this is a plan of action process in relation with audit

governance for making advancements in the functions or duty of accountant in order to

consider as a strategic partner in the organization (Angelkort, 2011).

Execution direction – this based on the further implementation in business

decision making practices and directing organizational performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk management – basically deals with contribution framework to identify

measure, manage and risk reporting for attaining targets and objectives.

This is a type of accounting process used by the managers in provisions of

accounting information to themselves before they determine matters between the

organizations which helps in the controlling and directing functions according to

management by managers. Generally it is based on a profession of partnership in

management decision making, making planning and executive management system

with the help of financial reporting expertise and involving management in developing

and implementing administrative plan of action. The basic functions of management

accounting are cash flow analysis, ratio analysis, fund flow analysis and budgetary

control, it is used in increasing efficiency in operating company, maximizing the

profitability, determination of simple and financial statements, taking complex business

decisions and con troll of business funds. These are the above points in decision

analysis in management auditing

P2.Types of M.A systems with respect to several sections.

There are several types of management auditing system . Some of them are discussed below.

Cost accounting systems

1) Standard costing- This is a costing in which the stocks presents only on the standardised price and

not considering actualized or mean price. In general it is a method of using cost and revenue standards on

reasons of deviation assessments controlling. It describes the formal methods of performance and efficiency

assessments. It is helpful in budgeting settlement process. It provides motivational criteria towards the

administrative staff. It helpful in estimations and modifications. The basic aim is to furnishing the employees by

giving certain instructions and assistance (Angelkort, 2011).

Mean activity – it is funded or expectable and considerations are the more than four years of

forthcoming time period. In a abstractive hypothesis the industrial plant production is based on negligible

disruptions and difficulties.

Practical activity – The extreme working act in which an industry attaining targets including the given

difficulties or disruptions.

Standard kinds

Current standards – it enables for a small span of time in relation with the existing situations.

Basic standards – it is apply for large time span with respect to the matured present regulation.

2) Actual cost – it is the sum amount which is paid in return in order to get goods and assets. This

includes historical, past, or existing price of the goods. It is an real expenses design to get assets.

measure, manage and risk reporting for attaining targets and objectives.

This is a type of accounting process used by the managers in provisions of

accounting information to themselves before they determine matters between the

organizations which helps in the controlling and directing functions according to

management by managers. Generally it is based on a profession of partnership in

management decision making, making planning and executive management system

with the help of financial reporting expertise and involving management in developing

and implementing administrative plan of action. The basic functions of management

accounting are cash flow analysis, ratio analysis, fund flow analysis and budgetary

control, it is used in increasing efficiency in operating company, maximizing the

profitability, determination of simple and financial statements, taking complex business

decisions and con troll of business funds. These are the above points in decision

analysis in management auditing

P2.Types of M.A systems with respect to several sections.

There are several types of management auditing system . Some of them are discussed below.

Cost accounting systems

1) Standard costing- This is a costing in which the stocks presents only on the standardised price and

not considering actualized or mean price. In general it is a method of using cost and revenue standards on

reasons of deviation assessments controlling. It describes the formal methods of performance and efficiency

assessments. It is helpful in budgeting settlement process. It provides motivational criteria towards the

administrative staff. It helpful in estimations and modifications. The basic aim is to furnishing the employees by

giving certain instructions and assistance (Angelkort, 2011).

Mean activity – it is funded or expectable and considerations are the more than four years of

forthcoming time period. In a abstractive hypothesis the industrial plant production is based on negligible

disruptions and difficulties.

Practical activity – The extreme working act in which an industry attaining targets including the given

difficulties or disruptions.

Standard kinds

Current standards – it enables for a small span of time in relation with the existing situations.

Basic standards – it is apply for large time span with respect to the matured present regulation.

2) Actual cost – it is the sum amount which is paid in return in order to get goods and assets. This

includes historical, past, or existing price of the goods. It is an real expenses design to get assets.

3) Normal cost – it includes through working class and real material prices. The estimations are based

on the overheads only.

Inventory management systems

Basically it is a scrutiny for non-capitalized assets and stocks. It investigates the products flowing

through fabricators to storage installation to the marking point. The management of inventory consists of

requesting about the materials, indulgent response , constituents, company and project components, yearly and

serial basis of records and distributions.

Job costing systems

It consists of increasing material , labour and overhead prices to a given occupation. This method is

useful in tracking particular requirements for several jobs and determining the reduction level of the costs in

coming employment. It is used in collecting of small size units.

Material allocation – the utilization of materials such as goods and services firstly get into the

provision and then passes to the merchandise.

Overhead allocation – The goods which are not oriented are concentrated into more than one

operating costs excavation. traditional cost accounting is based on allocation of

manufacturing overhead costs to the products obtained. It is the conventional method

of cost accounting which apportion the factory's indirect costs to the the factory-made

items in no of units produced like the direct labour or machine hours. Machine hours

are main reason of the factory overhead (Sirén, 2010).

Labour allocation – there are certain charges applicable to the workers at job costing systems. The

production-al labours are recorded in the costing of the job if they are traceable. By this method labour

allocation can be done.

Price optimizing systems- this is very valuable and beneficiary method used in mathematical approach

of calculating several reactions of consumers in accordance with prices of different products and services by

certain networking links. This method is providing in price determinations in order to attain goals and

accusatives.

These are the above management accounting systems.

TASK 2

P3 Income statements of absorption and marginal costing

There are several techniques used by an organisation to prepare the income statement. Such methods are

helpful in finding out the cost which affects the project. The company uses this approach in calculating profits

and net loss. It helps in creating an effectual information through which it becomes easier to take decision. One

of the two best suitable methods in framing of income statements is

on the overheads only.

Inventory management systems

Basically it is a scrutiny for non-capitalized assets and stocks. It investigates the products flowing

through fabricators to storage installation to the marking point. The management of inventory consists of

requesting about the materials, indulgent response , constituents, company and project components, yearly and

serial basis of records and distributions.

Job costing systems

It consists of increasing material , labour and overhead prices to a given occupation. This method is

useful in tracking particular requirements for several jobs and determining the reduction level of the costs in

coming employment. It is used in collecting of small size units.

Material allocation – the utilization of materials such as goods and services firstly get into the

provision and then passes to the merchandise.

Overhead allocation – The goods which are not oriented are concentrated into more than one

operating costs excavation. traditional cost accounting is based on allocation of

manufacturing overhead costs to the products obtained. It is the conventional method

of cost accounting which apportion the factory's indirect costs to the the factory-made

items in no of units produced like the direct labour or machine hours. Machine hours

are main reason of the factory overhead (Sirén, 2010).

Labour allocation – there are certain charges applicable to the workers at job costing systems. The

production-al labours are recorded in the costing of the job if they are traceable. By this method labour

allocation can be done.

Price optimizing systems- this is very valuable and beneficiary method used in mathematical approach

of calculating several reactions of consumers in accordance with prices of different products and services by

certain networking links. This method is providing in price determinations in order to attain goals and

accusatives.

These are the above management accounting systems.

TASK 2

P3 Income statements of absorption and marginal costing

There are several techniques used by an organisation to prepare the income statement. Such methods are

helpful in finding out the cost which affects the project. The company uses this approach in calculating profits

and net loss. It helps in creating an effectual information through which it becomes easier to take decision. One

of the two best suitable methods in framing of income statements is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

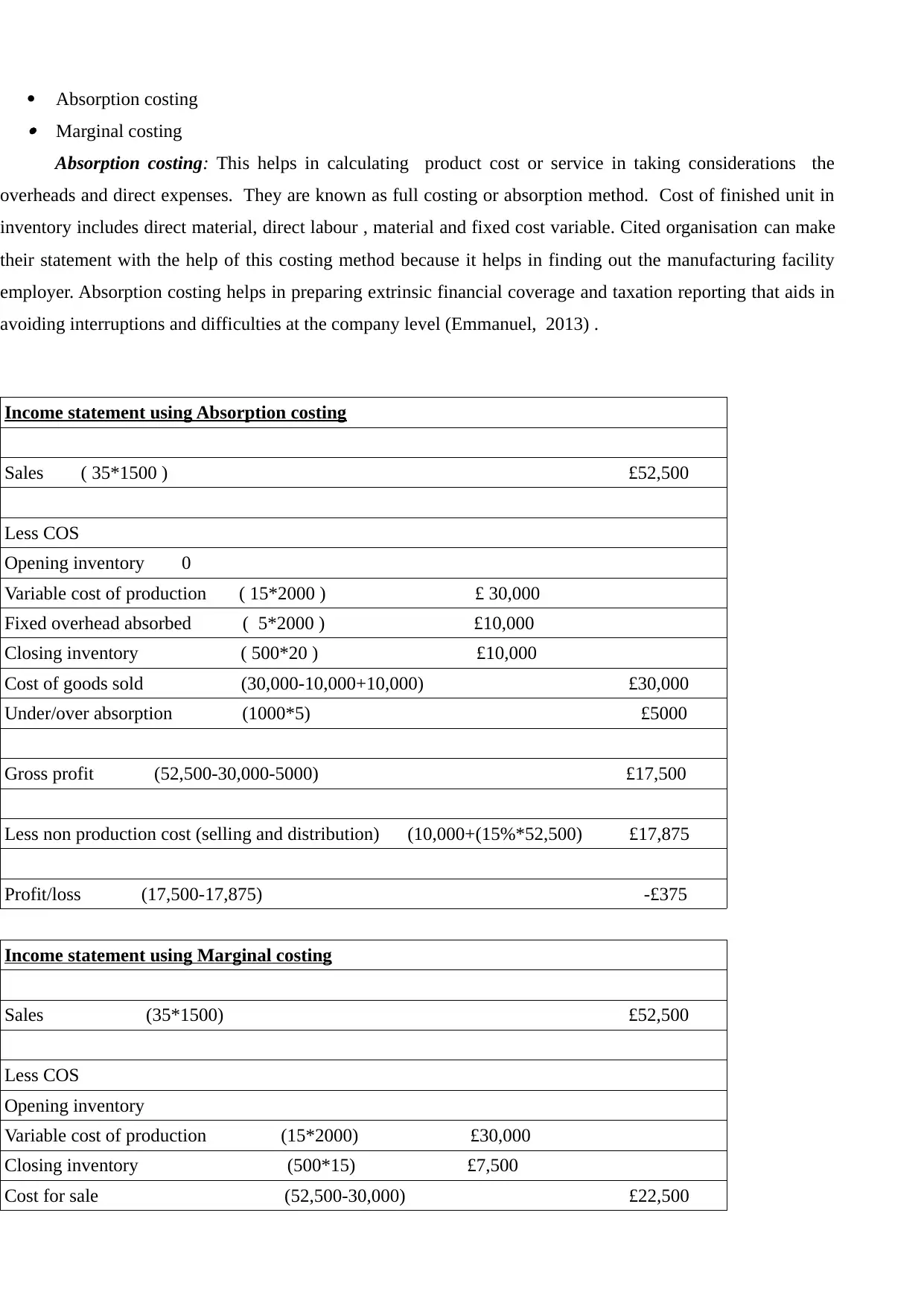

Absorption costing

Marginal costing

Absorption costing: This helps in calculating product cost or service in taking considerations the

overheads and direct expenses. They are known as full costing or absorption method. Cost of finished unit in

inventory includes direct material, direct labour , material and fixed cost variable. Cited organisation can make

their statement with the help of this costing method because it helps in finding out the manufacturing facility

employer. Absorption costing helps in preparing extrinsic financial coverage and taxation reporting that aids in

avoiding interruptions and difficulties at the company level (Emmanuel, 2013) .

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Marginal costing

Absorption costing: This helps in calculating product cost or service in taking considerations the

overheads and direct expenses. They are known as full costing or absorption method. Cost of finished unit in

inventory includes direct material, direct labour , material and fixed cost variable. Cited organisation can make

their statement with the help of this costing method because it helps in finding out the manufacturing facility

employer. Absorption costing helps in preparing extrinsic financial coverage and taxation reporting that aids in

avoiding interruptions and difficulties at the company level (Emmanuel, 2013) .

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

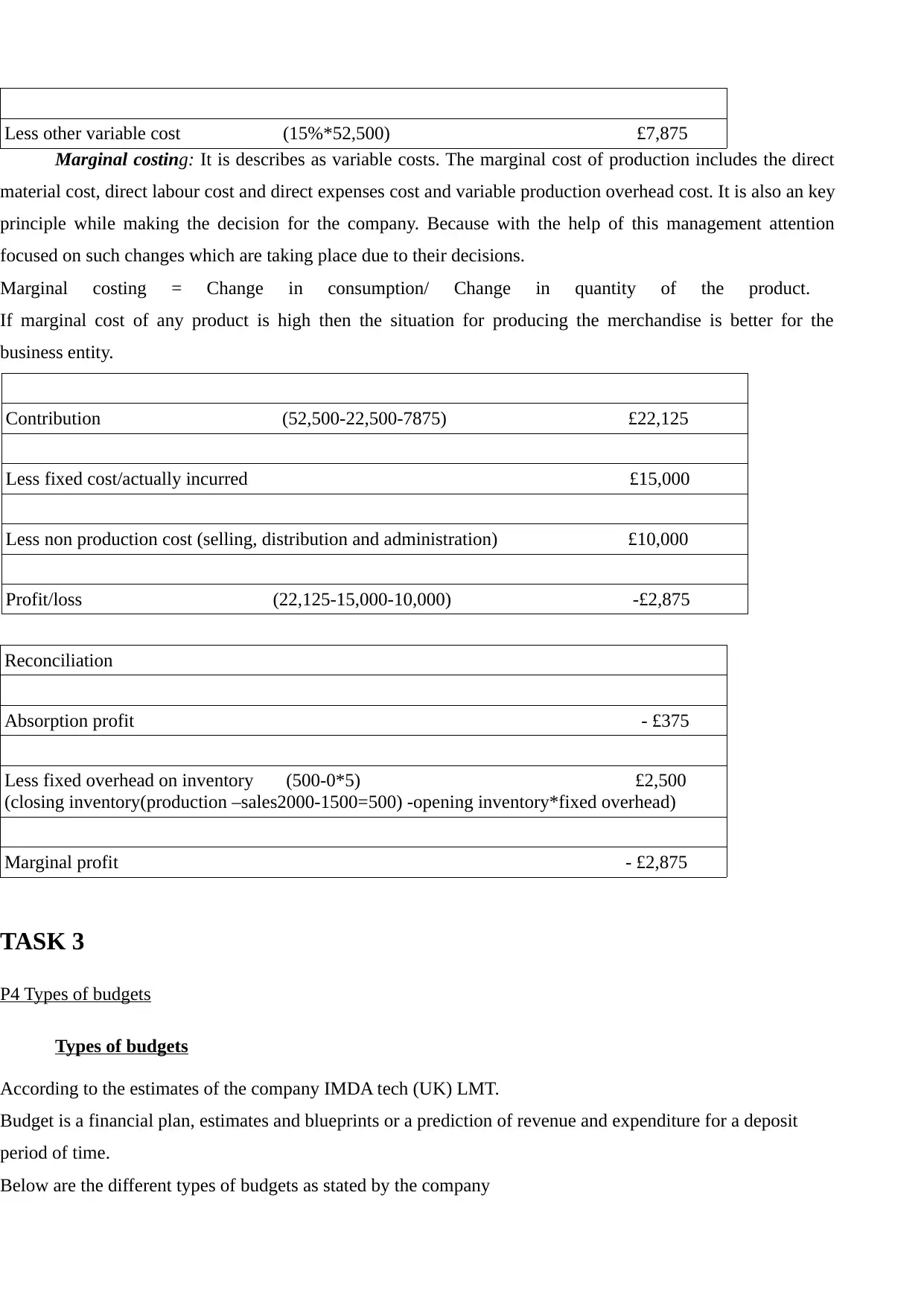

Less other variable cost (15%*52,500) £7,875

Marginal costing: It is describes as variable costs. The marginal cost of production includes the direct

material cost, direct labour cost and direct expenses cost and variable production overhead cost. It is also an key

principle while making the decision for the company. Because with the help of this management attention

focused on such changes which are taking place due to their decisions.

Marginal costing = Change in consumption/ Change in quantity of the product.

If marginal cost of any product is high then the situation for producing the merchandise is better for the

business entity.

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

TASK 3

P4 Types of budgets

Types of budgets

According to the estimates of the company IMDA tech (UK) LMT.

Budget is a financial plan, estimates and blueprints or a prediction of revenue and expenditure for a deposit

period of time.

Below are the different types of budgets as stated by the company

Marginal costing: It is describes as variable costs. The marginal cost of production includes the direct

material cost, direct labour cost and direct expenses cost and variable production overhead cost. It is also an key

principle while making the decision for the company. Because with the help of this management attention

focused on such changes which are taking place due to their decisions.

Marginal costing = Change in consumption/ Change in quantity of the product.

If marginal cost of any product is high then the situation for producing the merchandise is better for the

business entity.

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

TASK 3

P4 Types of budgets

Types of budgets

According to the estimates of the company IMDA tech (UK) LMT.

Budget is a financial plan, estimates and blueprints or a prediction of revenue and expenditure for a deposit

period of time.

Below are the different types of budgets as stated by the company

MASTER BUDGET

Master budget is grand total of organizations independent budgets depiction of complete financial undertaking

and health. It is the combination of factors like sales, operating expenses, assets and income series to permit

companies to manifest goals evaluate their overall competency as well as their independent cost centres itself in

the organization (Quattrone, 2010).

OPERATING BUDGET

forecasting and analysis of projecting income and expenditure over the course of given time period is called

operating budget. Operating budget accounts on factors like sales, production, labour cost, material cost,

overhead, manufacturing cost and administrative expenses for creating an canonical or precise picture. In

general or normally operating budgets are created weekly, monthly or yearly basis.

FINANCIAL BUDGET

Financial budget put forward a company's plans manipulate its assets, cash flows, income and expenses. it has

been used to establish a portray of company's financial health and extant a comprehensive analysis of its

spending to relative from its central view. A part from this they are they are time consuming and costly, there is

excessive spending on funds, conflicts in the organization.

Advantages ad disadvantages of several types of budgets

1) Master budgets are used in the company in order to keep all the managers aligned. It may subjected to

lack of specificity and difficult to read and update.

2) In operating budgets It is difficult to find out the estimates of revenue and expenses in a business

enterprise realistically. More paper work is required, it is not flexible toward management, it is not be

behaviourally anchored,very much complex,not cost effective aside from management (Quattrone, 2010).

3)Financial budgets are very are time consuming and costly, there is excessive spending on funds,

conflicts in the organization.

4) Budget is for the future period so it is difficult to predict the future value and it is not necessary that

the predicted data will always work. If the condition changed in the budget in future then it is difficult to predict

the data.

5) Budget is not substitute for the management, it is the only the tool to the management and can not

replace the decision making.

Although budgeting comes with many restrictions and shortcoming it may be wrong to come up with

conclusion that budgeting process is impractical.

Process of budget preparation

This method is carried out by the government making and authorization. The steps in budgeting

preparation are as follows

monetary fund preparation

Master budget is grand total of organizations independent budgets depiction of complete financial undertaking

and health. It is the combination of factors like sales, operating expenses, assets and income series to permit

companies to manifest goals evaluate their overall competency as well as their independent cost centres itself in

the organization (Quattrone, 2010).

OPERATING BUDGET

forecasting and analysis of projecting income and expenditure over the course of given time period is called

operating budget. Operating budget accounts on factors like sales, production, labour cost, material cost,

overhead, manufacturing cost and administrative expenses for creating an canonical or precise picture. In

general or normally operating budgets are created weekly, monthly or yearly basis.

FINANCIAL BUDGET

Financial budget put forward a company's plans manipulate its assets, cash flows, income and expenses. it has

been used to establish a portray of company's financial health and extant a comprehensive analysis of its

spending to relative from its central view. A part from this they are they are time consuming and costly, there is

excessive spending on funds, conflicts in the organization.

Advantages ad disadvantages of several types of budgets

1) Master budgets are used in the company in order to keep all the managers aligned. It may subjected to

lack of specificity and difficult to read and update.

2) In operating budgets It is difficult to find out the estimates of revenue and expenses in a business

enterprise realistically. More paper work is required, it is not flexible toward management, it is not be

behaviourally anchored,very much complex,not cost effective aside from management (Quattrone, 2010).

3)Financial budgets are very are time consuming and costly, there is excessive spending on funds,

conflicts in the organization.

4) Budget is for the future period so it is difficult to predict the future value and it is not necessary that

the predicted data will always work. If the condition changed in the budget in future then it is difficult to predict

the data.

5) Budget is not substitute for the management, it is the only the tool to the management and can not

replace the decision making.

Although budgeting comes with many restrictions and shortcoming it may be wrong to come up with

conclusion that budgeting process is impractical.

Process of budget preparation

This method is carried out by the government making and authorization. The steps in budgeting

preparation are as follows

monetary fund preparation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fund legislation

Execution related with budgets – This is a step in company uses its authorised budgets and in

accountability state all the associates control and assess the budget utility. In this step past analysis related with

the budgets is reviewed by the company and necessary amendments are made in the budgets (Sponem, 2012 ).

Availability of funds – this is an evaluation of present funds available at the company to prepare

budgets.

Measure costing steps - Determination of the cost that may arise during the year in the operation of the

company.

Department Budget- Company collects the requirement of fund at each department. By means funds

can be allocated.

Forecasting revenue - Company forecast the revenue and the income so that they can easily allocate

the fund to each department.

Create budget package- In this step, the instructions are followed with the recent amendments .

Issue budget package- Budget is issued and required to answer to the recipients.

Answers - When budget package is issued by the company then there are some question that may arise.

So it required for the company to answer such question and if these points are required then consider such in the

budgets.

Budget preparation - When all the data related with income and expenditure are assembled then such

information is implemented in practical sense and budget is prepared.

Issuing budget - When final budget is prepared then it is required for the company to issue it so that

funds can be allotted to each department as per the budgeted amount (Sponem, 2012).

Pricing strategies

Basically pricing strategies are used in determining the aims and objectives of the company. It is

essential for an enterprise to apply several variations in their pricing strategy for better running of company. It

depends upon increasing marketing share and widen out net income edges . There are several strategies

explained below

Cost based strategy – It determines products and services. It includes absorption pricing, break even

pricing, cost plus pricing, marginal cost pricing, time and materials pricing

Value pricing strategy – It determines the overall attitude of the customers towards product and

services. It includes ever-changing, superior, price skimming and value pricing.

Teaser pricing strategy – This includes the selling of low prices products by considering high prices

towards the customers. It includes premium prices, high low prices and loss leader prices. This is the above

pricing strategy with respect to management accounting.

Execution related with budgets – This is a step in company uses its authorised budgets and in

accountability state all the associates control and assess the budget utility. In this step past analysis related with

the budgets is reviewed by the company and necessary amendments are made in the budgets (Sponem, 2012 ).

Availability of funds – this is an evaluation of present funds available at the company to prepare

budgets.

Measure costing steps - Determination of the cost that may arise during the year in the operation of the

company.

Department Budget- Company collects the requirement of fund at each department. By means funds

can be allocated.

Forecasting revenue - Company forecast the revenue and the income so that they can easily allocate

the fund to each department.

Create budget package- In this step, the instructions are followed with the recent amendments .

Issue budget package- Budget is issued and required to answer to the recipients.

Answers - When budget package is issued by the company then there are some question that may arise.

So it required for the company to answer such question and if these points are required then consider such in the

budgets.

Budget preparation - When all the data related with income and expenditure are assembled then such

information is implemented in practical sense and budget is prepared.

Issuing budget - When final budget is prepared then it is required for the company to issue it so that

funds can be allotted to each department as per the budgeted amount (Sponem, 2012).

Pricing strategies

Basically pricing strategies are used in determining the aims and objectives of the company. It is

essential for an enterprise to apply several variations in their pricing strategy for better running of company. It

depends upon increasing marketing share and widen out net income edges . There are several strategies

explained below

Cost based strategy – It determines products and services. It includes absorption pricing, break even

pricing, cost plus pricing, marginal cost pricing, time and materials pricing

Value pricing strategy – It determines the overall attitude of the customers towards product and

services. It includes ever-changing, superior, price skimming and value pricing.

Teaser pricing strategy – This includes the selling of low prices products by considering high prices

towards the customers. It includes premium prices, high low prices and loss leader prices. This is the above

pricing strategy with respect to management accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5 Balance score card conceptualization

Balance score card is a performance measurement tool used in administration plan of action

management for identification and developing several intrinsic operations related with business which results in

extrinsic outcomes. It is helpful in measuring performance and giving responses to administration. There are

four areas concerned with the BSC perspectives. Financial, interior business process, learning and growth. It is

short and long run of the internal business process of administration. It consists of four important parts .

Companies are adopting a method of BSC for learning, growth and implementation. The vision and strategy

determines on the basis of consumer consideration, internal process of business, learning and growth

orientations and financial appearance ( Tenucci, 2010).

Financial perspectives

It is based on the fiscal aspects of currency flows, tax return on investment funds, fiscal

outcomes and capital return on employed. It provides some advance methods of eliminating financial

problems at an organizational level. It is helpful in finding strengths and weakness of the company to

attain goals and objectives.

It is used in measurement of cash flow analysis

Helps in measuring the quarterly growth of sales

Helpful in the judgements of operating income by division

Financial governance and development

it is used to improve financial governance and development of strategy

Balance score card techniques can be used by the company to eliminate financial difficulties that are faced by

the company. This technique is used to measure the performance of the company so that corrective actions can

be taken to improve such conditions. It is used to improve financial governance and to detect the issues that are

faced by the company. There are four perspective of

Balance score card is used to develop strategy so that issues can be resolved. Balance score card approach

evaluates the performance of the company. It measure the performance in various perspective as finance related,

Internal process of the company, customer related issues, growth of the company. It provides data to the

management so that they can take decisions and formulate their strategies accordingly. This technique is used to

formulate better strategies that can solve the problems that are faced by the company (Nørreklit, 2010).

CONCLUSION

According to the above discussion it can be concluded that management accounting provides various

tools and techniques that can be used in the business to establish effective mechanism in the business and

overcome the difficulty faced due to financial issues. It covers the aspect that budget should be prepared by

every organisation so that funds can be distributed among the various sector as per their needs but there are

P5 Balance score card conceptualization

Balance score card is a performance measurement tool used in administration plan of action

management for identification and developing several intrinsic operations related with business which results in

extrinsic outcomes. It is helpful in measuring performance and giving responses to administration. There are

four areas concerned with the BSC perspectives. Financial, interior business process, learning and growth. It is

short and long run of the internal business process of administration. It consists of four important parts .

Companies are adopting a method of BSC for learning, growth and implementation. The vision and strategy

determines on the basis of consumer consideration, internal process of business, learning and growth

orientations and financial appearance ( Tenucci, 2010).

Financial perspectives

It is based on the fiscal aspects of currency flows, tax return on investment funds, fiscal

outcomes and capital return on employed. It provides some advance methods of eliminating financial

problems at an organizational level. It is helpful in finding strengths and weakness of the company to

attain goals and objectives.

It is used in measurement of cash flow analysis

Helps in measuring the quarterly growth of sales

Helpful in the judgements of operating income by division

Financial governance and development

it is used to improve financial governance and development of strategy

Balance score card techniques can be used by the company to eliminate financial difficulties that are faced by

the company. This technique is used to measure the performance of the company so that corrective actions can

be taken to improve such conditions. It is used to improve financial governance and to detect the issues that are

faced by the company. There are four perspective of

Balance score card is used to develop strategy so that issues can be resolved. Balance score card approach

evaluates the performance of the company. It measure the performance in various perspective as finance related,

Internal process of the company, customer related issues, growth of the company. It provides data to the

management so that they can take decisions and formulate their strategies accordingly. This technique is used to

formulate better strategies that can solve the problems that are faced by the company (Nørreklit, 2010).

CONCLUSION

According to the above discussion it can be concluded that management accounting provides various

tools and techniques that can be used in the business to establish effective mechanism in the business and

overcome the difficulty faced due to financial issues. It covers the aspect that budget should be prepared by

every organisation so that funds can be distributed among the various sector as per their needs but there are

many advantages and disadvantages available for to establish budgetary control. Budgetary control mechanism

establish the control mechanism of budget and provide sustainable growth to the business.

REFERENCES

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory and practice

in management accounting. Management Accounting Research.21(2). pp.79-82.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a loose coupling?.

Journal of Accounting & organizational change.6(2).pp.228-259.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society.38(1). pp.50-71.

Herbert, I.P. and Seal, W.B., 2012. Shared services as a new organisational form: Some implications for

management accounting. The British Accounting Review.44(2). pp.83-97.

Lambert, C. and Sponem, S., 2012. Roles, authority and involvement of the management accounting function: a

multiple case-study perspective. European Accounting Review.21(3).pp.565-589.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research. Accounting,

Organizations and Society.35(4). pp.462-477.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An organizational and

sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional accountants: A renewed

research agenda. Journal of applied management accounting research.8(1). p.65.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Scapens, R.W. and Bromwich, M., 2010. Management accounting research: 20 years on.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive management

accounting research. Management Accounting Research.21(2). pp.130-141.

Ward, K., 2012. Strategic management accounting. Routledge.

Weißenberger, B.E. and Angelkort, H., 2011. Integration of financial and management accounting systems: The

mediating influence of a consistent financial language on controllership effectiveness. Management

establish the control mechanism of budget and provide sustainable growth to the business.

REFERENCES

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory and practice

in management accounting. Management Accounting Research.21(2). pp.79-82.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a loose coupling?.

Journal of Accounting & organizational change.6(2).pp.228-259.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society.38(1). pp.50-71.

Herbert, I.P. and Seal, W.B., 2012. Shared services as a new organisational form: Some implications for

management accounting. The British Accounting Review.44(2). pp.83-97.

Lambert, C. and Sponem, S., 2012. Roles, authority and involvement of the management accounting function: a

multiple case-study perspective. European Accounting Review.21(3).pp.565-589.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research. Accounting,

Organizations and Society.35(4). pp.462-477.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An organizational and

sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional accountants: A renewed

research agenda. Journal of applied management accounting research.8(1). p.65.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Scapens, R.W. and Bromwich, M., 2010. Management accounting research: 20 years on.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive management

accounting research. Management Accounting Research.21(2). pp.130-141.

Ward, K., 2012. Strategic management accounting. Routledge.

Weißenberger, B.E. and Angelkort, H., 2011. Integration of financial and management accounting systems: The

mediating influence of a consistent financial language on controllership effectiveness. Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.